The COVID-19 Outbreak and Risk–Return Spillovers between Main and SME Stock Markets in the MENA Region

Abstract

:1. Introduction

2. Data Definitions, Descriptive Statistics, and Preliminary Analysis

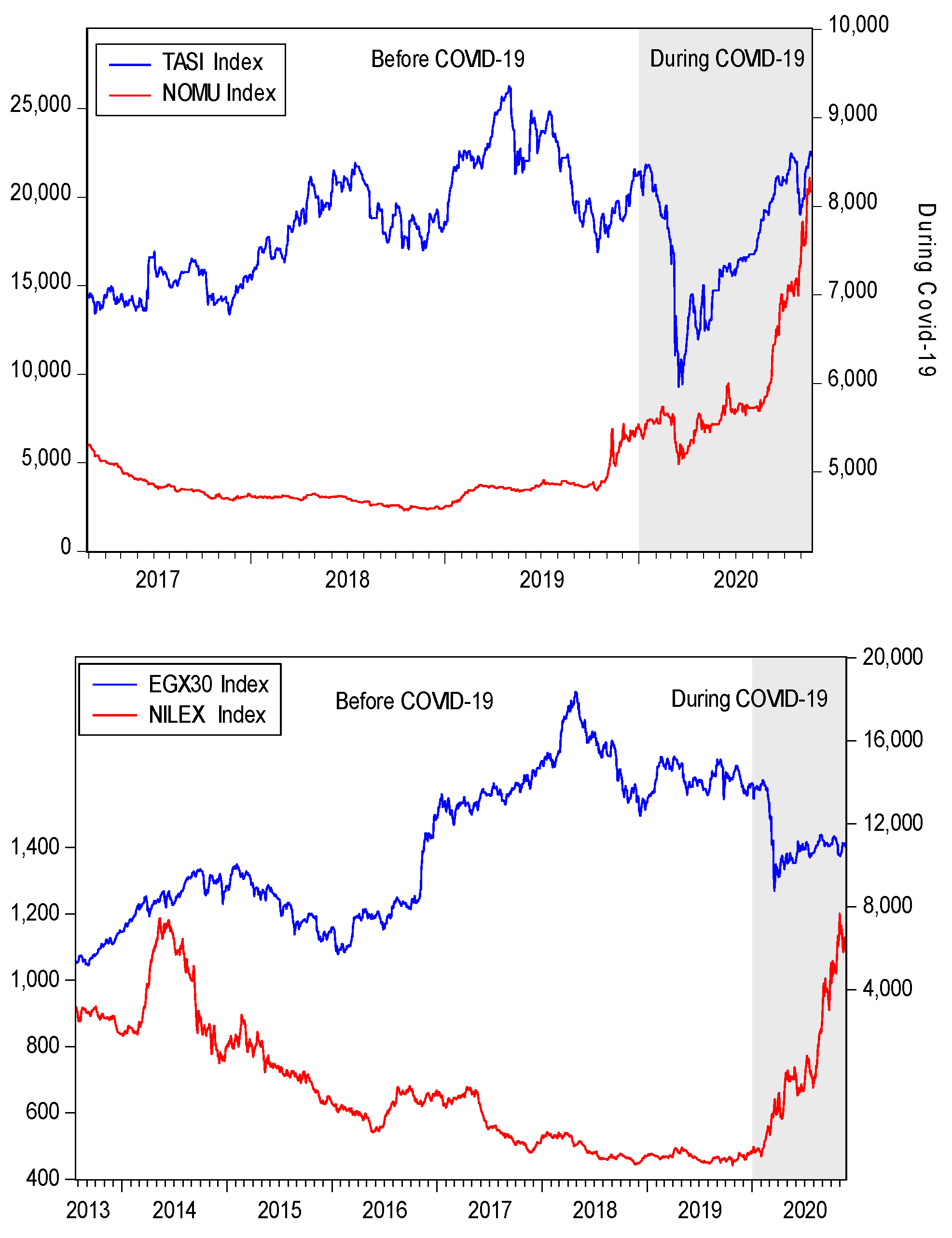

2.1. Data Definitions

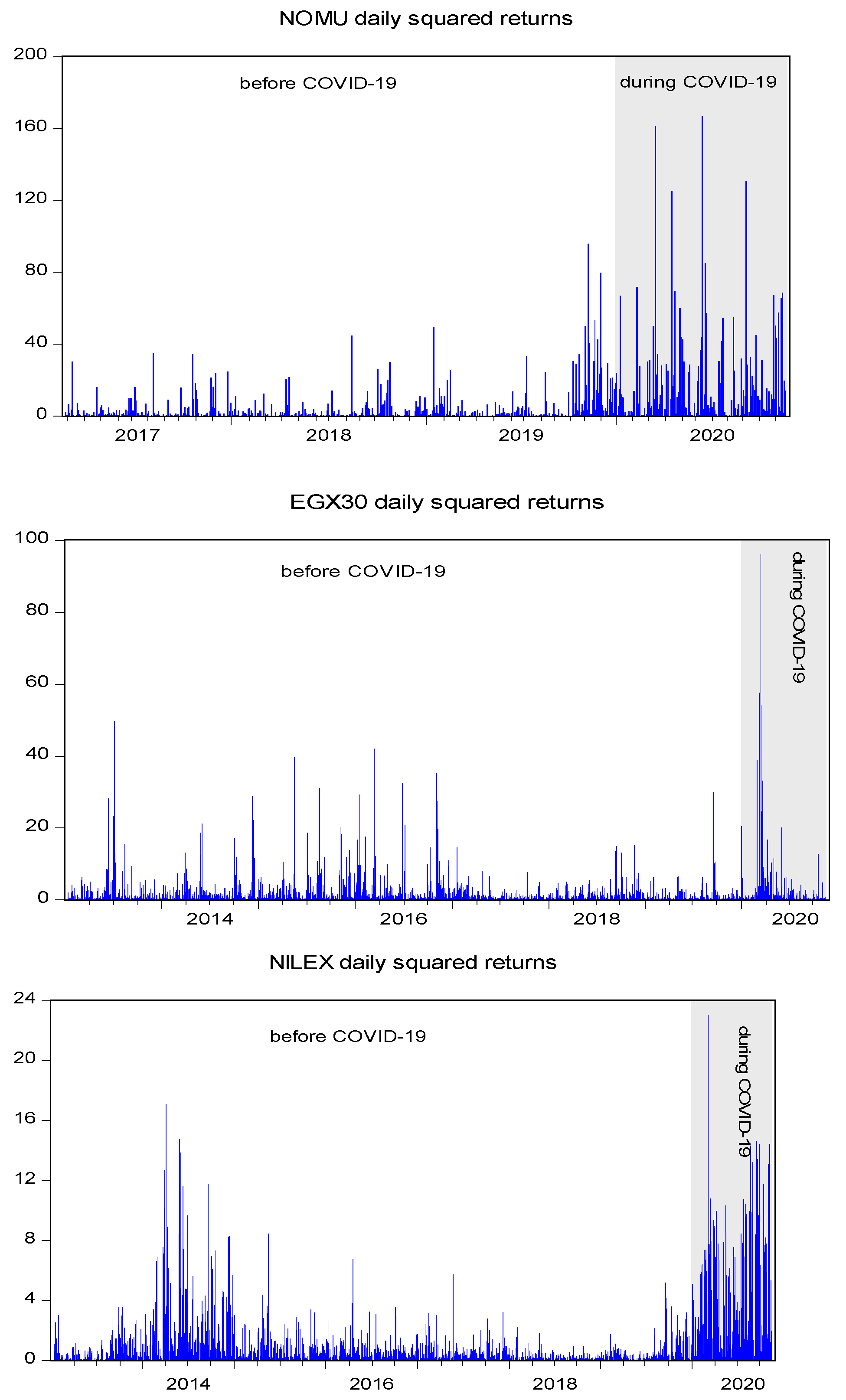

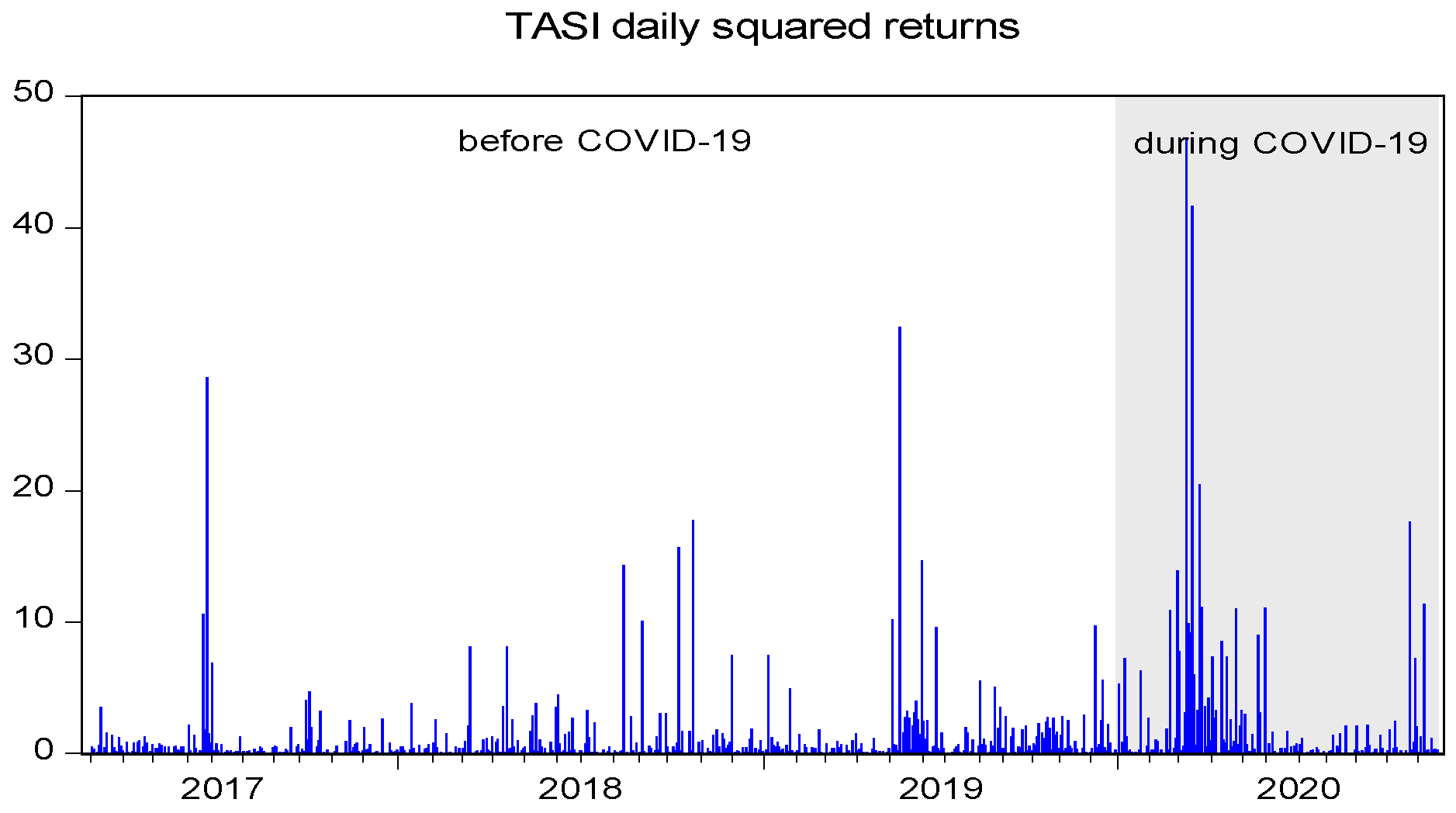

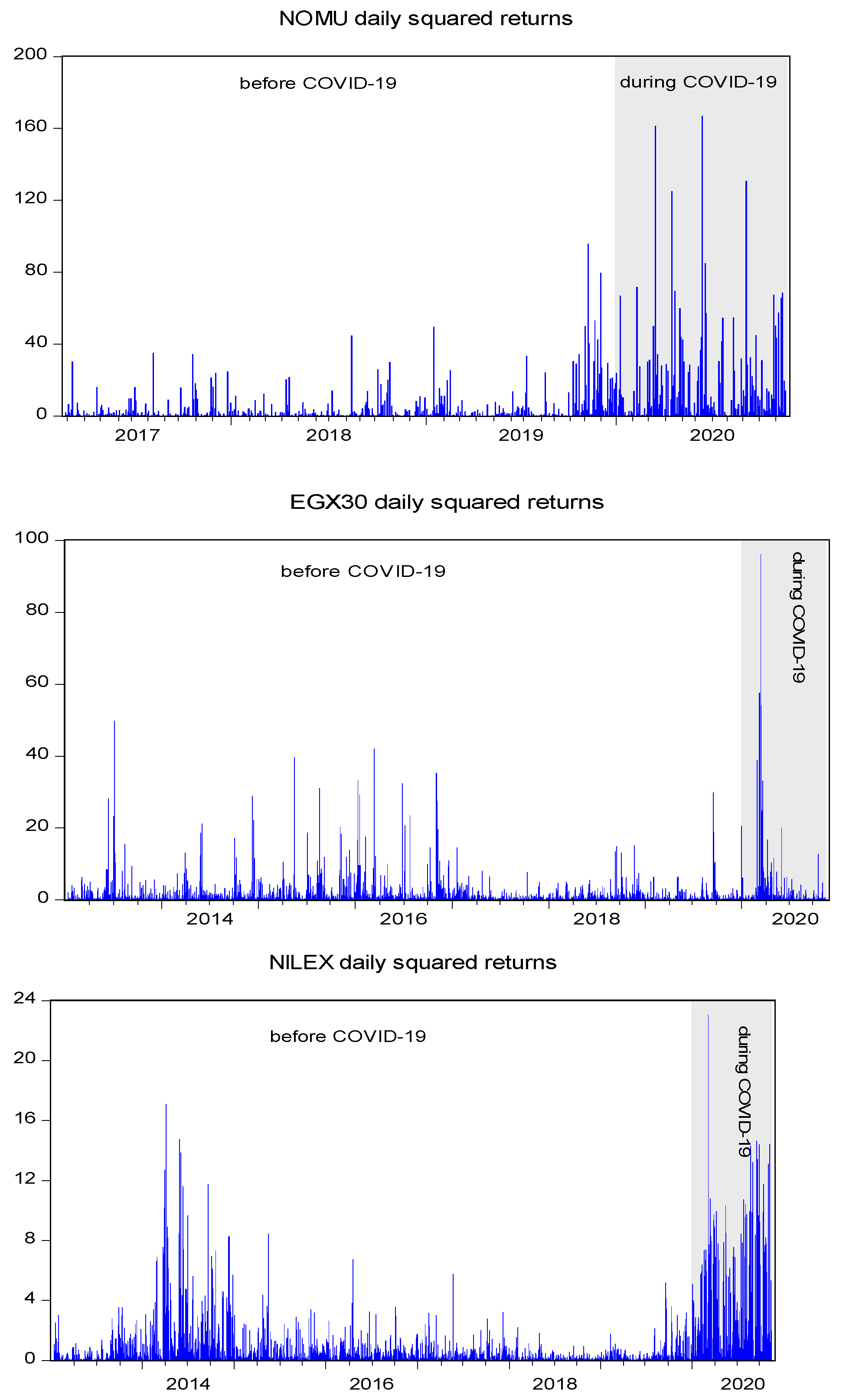

2.2. Descriptive Statistics

2.3. Preliminary Analysis

2.3.1. Asymmetric Causality Test between the Main and SME Stock Markets

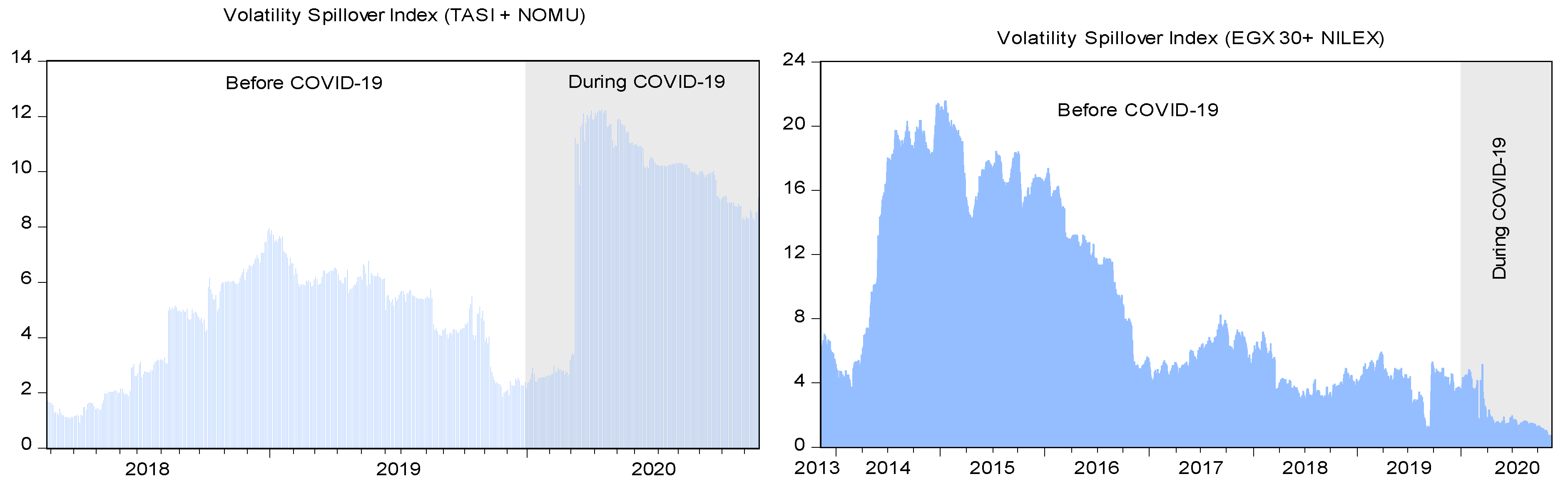

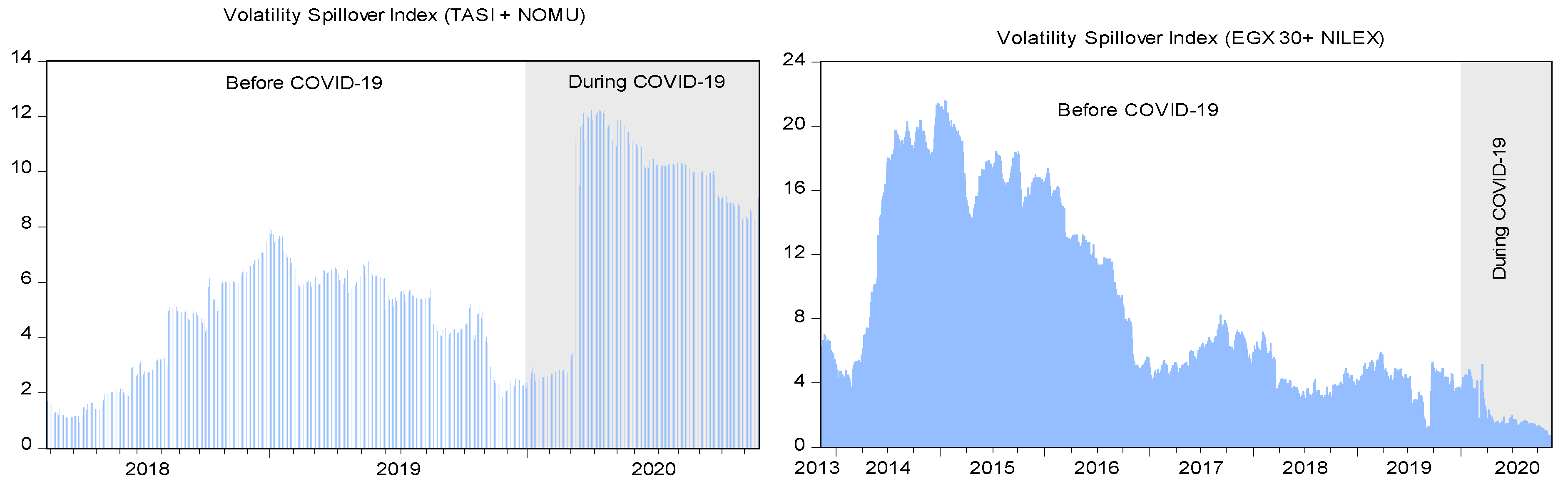

2.3.2. Directional Connectedness between the Main and SME Stock Markets

3. Materials and Methods

3.1. The Asymmetric BEKK–GARCH Model

3.2. The Asymmetric DCC–GARCH Model

3.3. Optimal Portfolio Allocation and Risk Management

3.3.1. Optimal Portfolio Weights

3.3.2. Dynamic Optimal Hedge Ratios

3.3.3. Hedging Effectiveness during the COVID-19 Pandemic

4. Empirical Results and Discussion

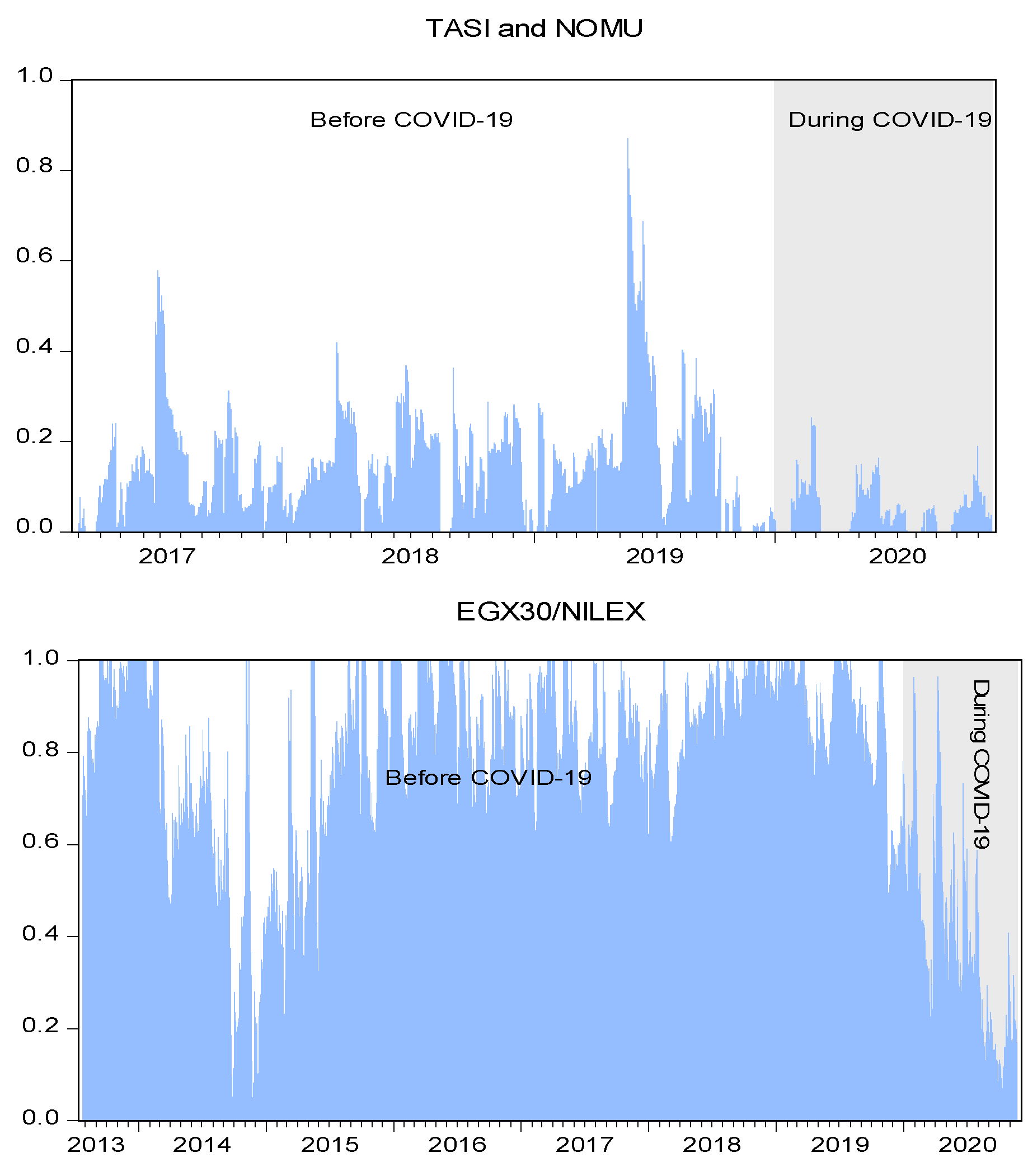

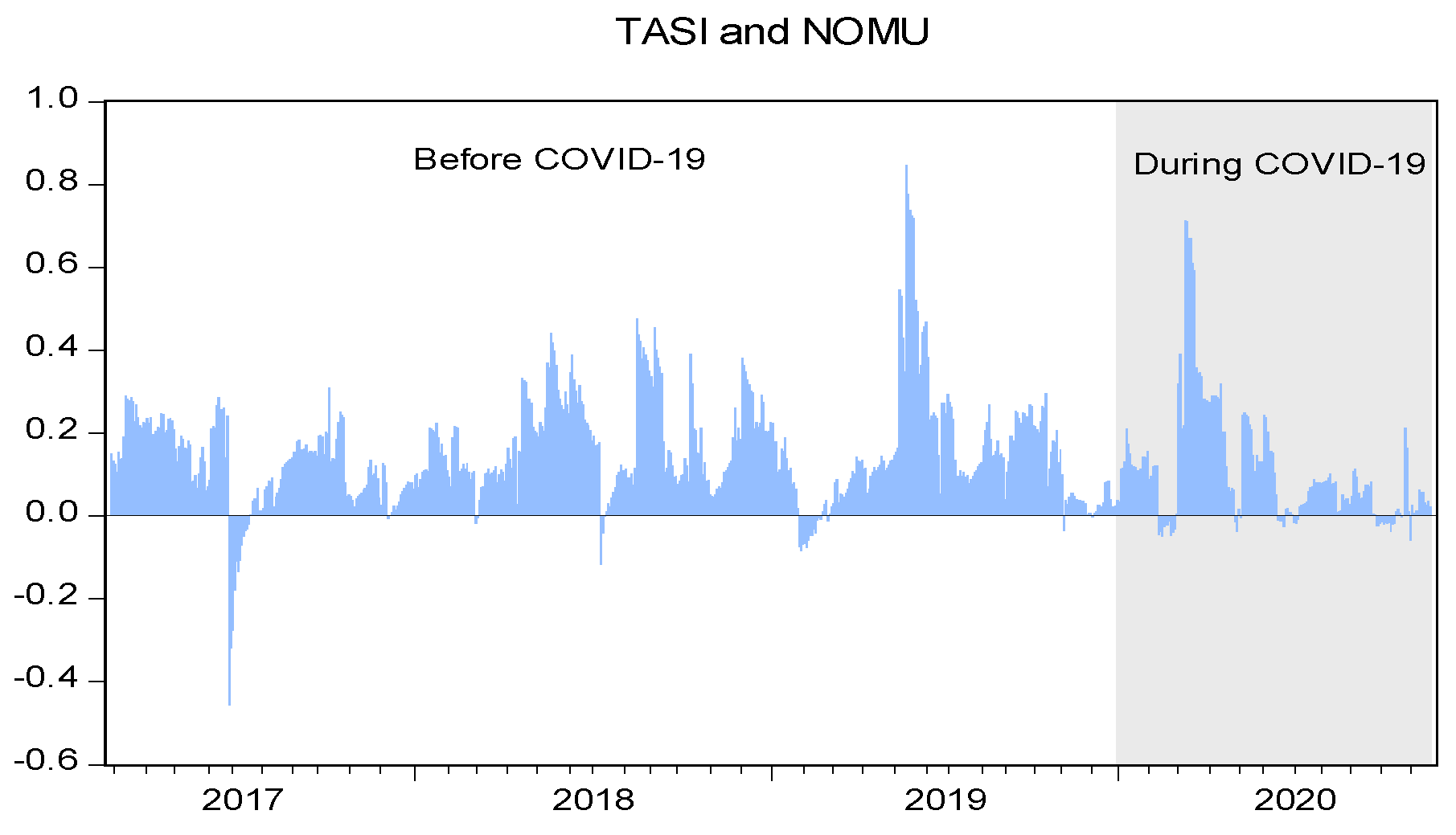

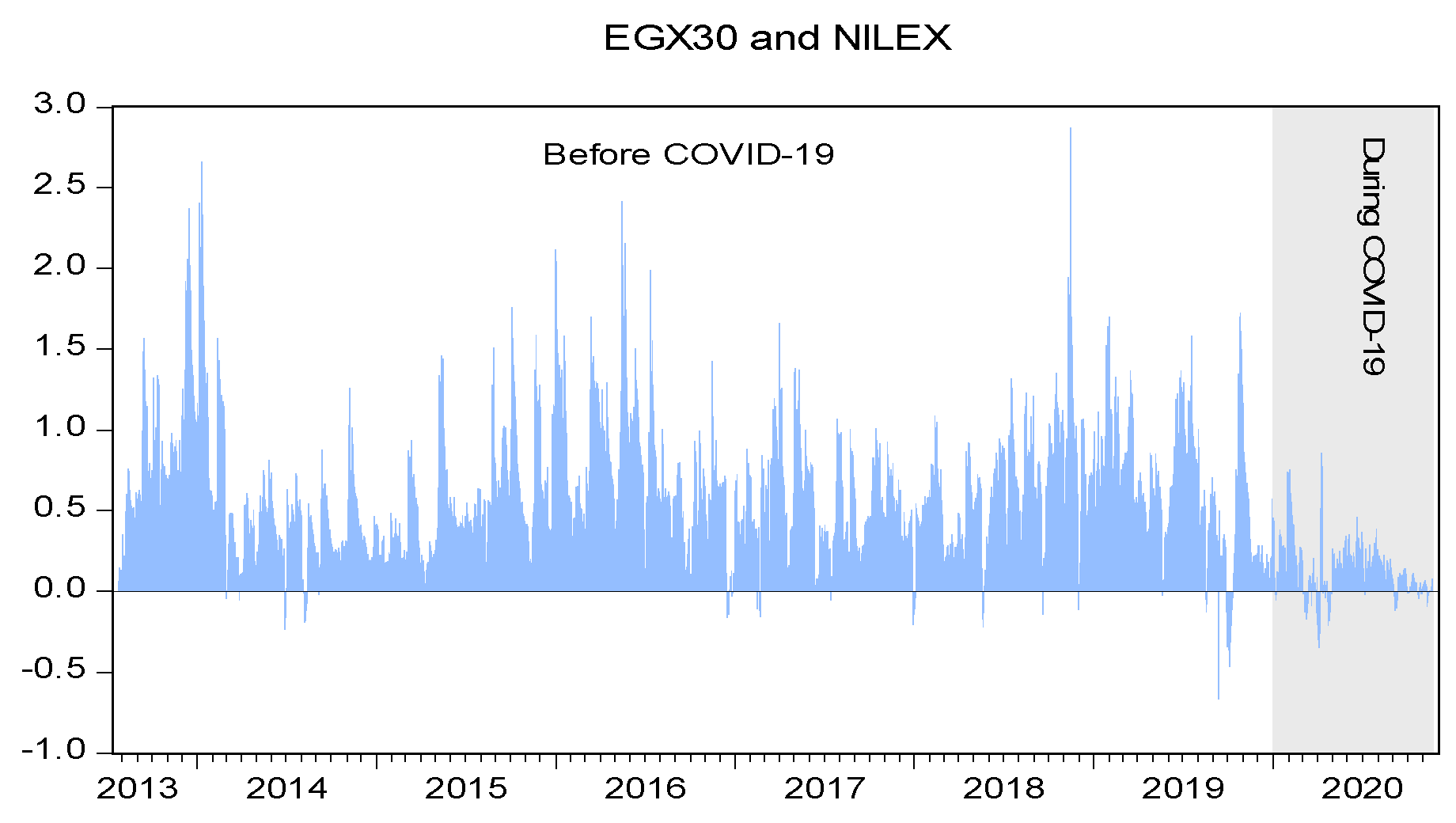

4.1. Returns and Risk Spillovers between the Main and SME Stock Markets

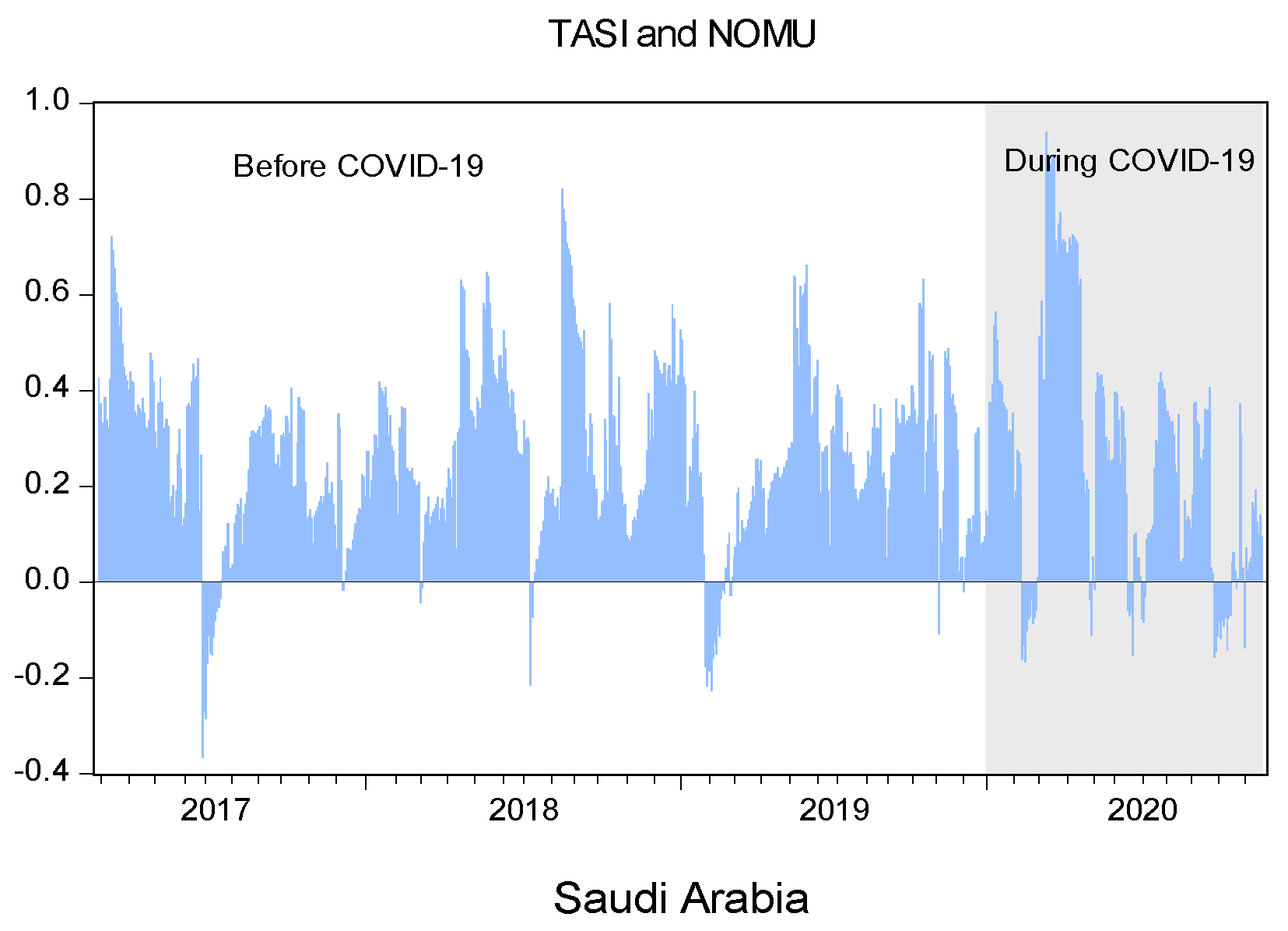

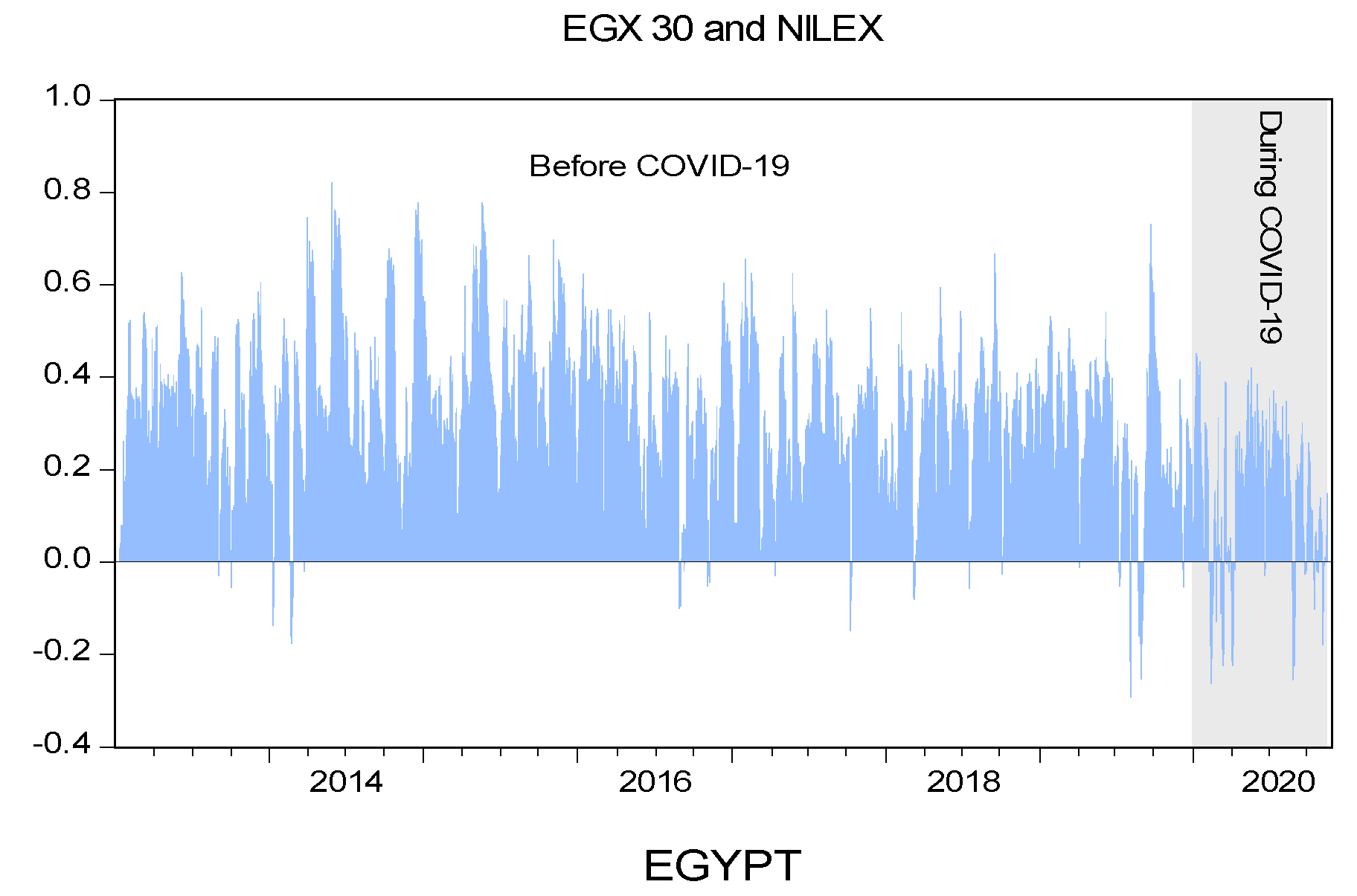

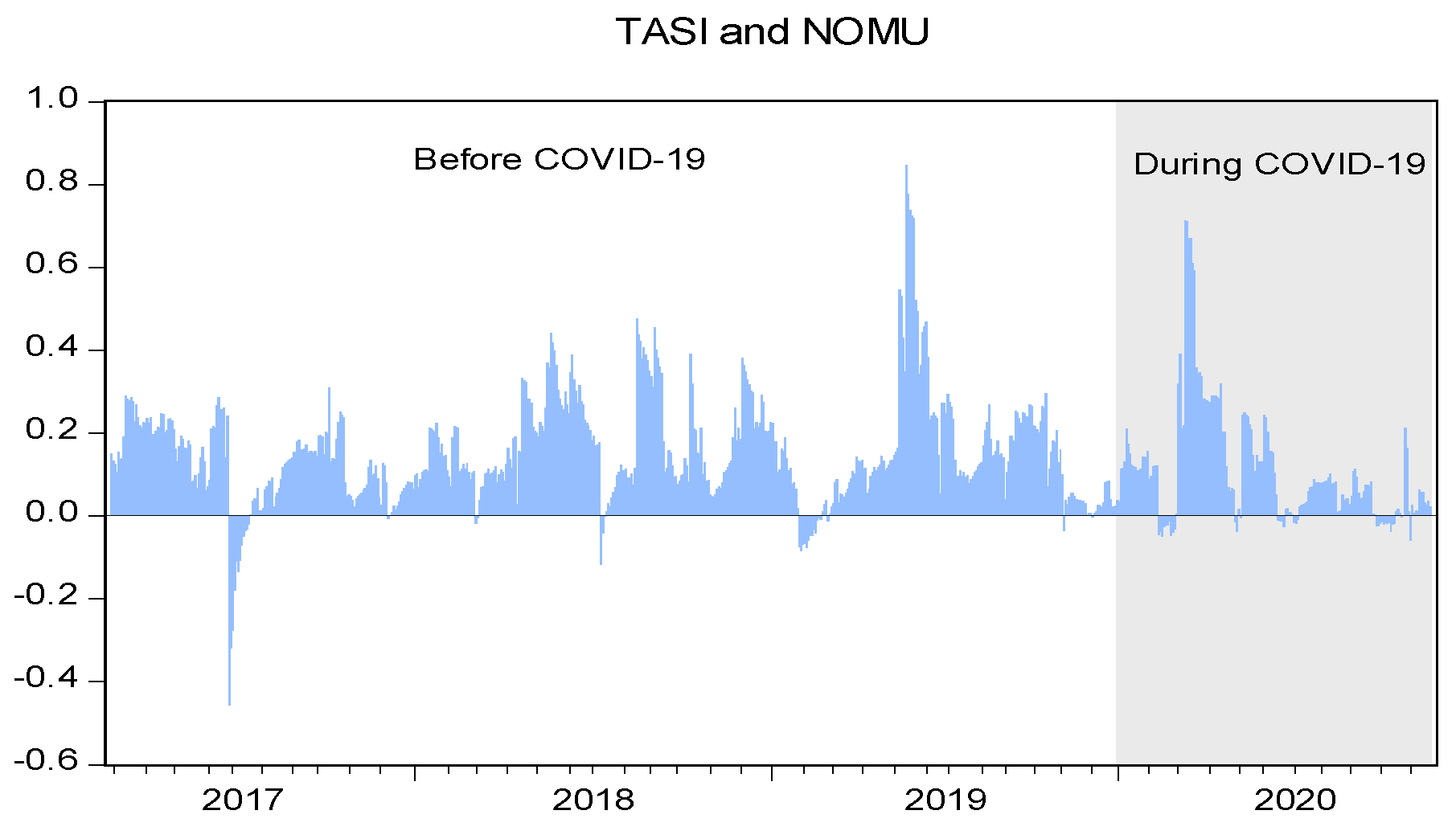

4.2. Dynamic Conditional Correlations between the Main and SME Stock Markets

4.3. Portfolio Weights, Hedge Ratios, and Hedging Effectiveness

5. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Saudi Arabia | Egypt | |||||||

|---|---|---|---|---|---|---|---|---|

| Main Market | SME Market | Main Market | SME Market | |||||

| Years | 2019 | 2020 | 2019 | 2020 | 2019 | 2020 | 2019 | 2020 |

| Inception a | 1985 | 2017 | 1998 | 2012 | ||||

| No. of listed companies | 199 | 203 | 5 d | 4 | 210 | 209 | 27 e | 27 |

| Representative index | TASI | NOMU | EGX 30 | NILEX | ||||

| Market capitalization b | 2406.73 | 2427.15 | 0.68 | 3.25 | 44.13 | 41.35 | 0.07 | 0.06 |

| Percentage of GDP | 303.51% | 347% | 0.09% | 0.46% | 14.56% | 11% | 0.02% | 0.02% |

| Percentage of main index | - | - | 0.03% | 0.13% | - | - | 0.16% | 0.15% |

| Trading value b | 234.7 | 556.75 | 0.61 | 1.90 | 11.28 | 16.14 | 0.016 | 0.083 |

| Percentage of main index | - | - | 0.26% | 0.34% | - | - | 0.14% | 0.51% |

| Trading volume c | 33.06 | 79.32 | 0.08 | 0.11 | 43.74 | 87.10 | 0.77 | 1.58 |

| Percentage of main index | - | - | 0.24% | 0.14% | - | - | 1.8% | 1.8% |

| Full Sample Period | Before the COVID-19 Crisis | During the COVID-19 Crisis | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TASI | NOMU | EGX30 | NILEX | TASI | NOMU | EGX30 | NILEX | TASI | NOMU | EGX30 | NILEX | |

| Panel A: VAR (1)-asymmetric BEKK–GARCH (1,1) model | ||||||||||||

| ARCH–LM(5) | 8.8641 (0.1146) | 4.4711 (0.4834) | 6.4930 (0.2612) | 3.6942 (0.5942) | 11.9986 (0.3485) | 7.2395 (0.1601) | 7.0067 (0.2201) | 7.4165 (0.2209) | 5.400 (0.6678) | 7.9289 (0.1602) | 3.2929 (0.8073) | 6.1898. (0.8221) |

| 9.0712 (0.6312) | 5.5485 (0.3214) | 6.2715 (0.1800) | 4.7411 (0.3151) | 5.7916 (0.2154) | 5.3610 (0.2529) | 3.5884 (0.5464) | 4.5581 (0.3367) | 3.723 (0.4343) | 4.091 (0.3993) | 5.1287 (0.2742) | 6.7398 (0.2046) | |

| 9.0953 (0.1053) | 4.4905 (0.4812) | 6.6196 (0.2516) | 3.7643 (0.584) | 12.5598 (0.3520) | 8.2212 (0.1445) | 7.0025 (0.2221) | 7.4870 (0.1879) | 5.655 (0.6819) | 8.2819 (0.1415) | 3.3292 (0.8871) | 6.3895 (0.2934) | |

| Panel B: VAR (1)-asymmetric DCC–GARCH (1,1) model | ||||||||||||

| ARCH–LM(5) | 3.7645 (0.5834) | 2.9368 (0.7079) | 3.573 (0.6123) | 6.7855 (0.2371) | 10.5801 (0.6042) | 5.2708 (0.3837) | 6.8975 (0.2284) | 7.4975 (0.18625) | 0.8181 (0.9759) | 5.8824 (0.3178) | 2.2472 (0.8140) | 9.9312 (0.7106) |

| 12.007 (0.1754) | 4.9998 (0.2872) | 5.2439 (0.2630) | 6.0145 (0.1980) | 7.6671 (0.1066) | 3.4814 (0.1482) | 4.0498 (0.3991) | 4.4744 (0.3468) | 5.0911 (0.1650) | 3.3827 (0.4963) | 5.7879 (0.435) | 6.4391 (0.1693) | |

| 3.9104 (0.5620) | 2.9740 (0.7040) | 3.5939 (0.6090) | 6.9802 (0.2225) | 10.3100 (0.6315) | 5.9150 (0.3562) | 6.8068 (0.2351) | 7.6227 (0.1783) | 0.8712 (0.9720) | 6.1399 (0.2939) | 2.2021 (0.8214) | 9.0987 (0.6859) | |

| 1 | Several financing sources exist for SMEs, including venture capital, private equity, private debt, trade credit, initial public offerings (IPOs), business angel finance, and crowdfunding, as well as grants, funding from incubators or accelerators, and support from family and friends (Cumming et al. 2019); however, bank loans remain their main source of funding (Beck et al. 2008; The World Federation of Exchanges 2015). Nonetheless, Cosh et al. (2009) find that SMEs are less likely than larger firms to receive the desired amount of funding from banks. This is primarily due to information asymmetries, a lack of brick-and-mortar collateral, a lack of positive and regular cash flows, and the need for longer maturities to finance capital expenditure (Berger and Udell 2006; Jaffee and Russell 1976; Nassr and Wehinger 2016; Stiglitz and Weiss 1981). Moreover, SMEs are found to be more vulnerable in financial crises, as several studies have shown that the global financial crisis (GFC) exacerbated credit rationing, thereby undermining SMEs’ business and investment activities (see Cowling et al. 2016; D’Amato 2019; Ferrando and Ruggieri 2018). |

| 2 | Other models of second-tier market segmentation include sectoral and demand-side models (see Vismara et al. 2012). However, the sequential segmentation (steppingstone) model is recommended by international bodies (Nassr and Wehinger 2016, p. 70). Under the sequential segmentation (steppingstone) model, second-tier markets are expected to screen small companies in the ‘seasoning’ market, and if a company is successful, it graduates to the main market. |

| 3 | For more on the specificities of emerging markets, including the MENA region and their intraction with the global economy, see Arouri et al. (2013), while Boubaker et al. (2016) focus on risk management practices in emerging markets. |

| 4 | Based on GDP, PPP (current international USD); see https://data.worldbank.org/indicator/NY.GDP.MKTP.PP.CD (accessed on 15 June 2021). |

| 5 | The Nile Exchange (NILEX) was launched under the Egyptian Exchange in 2007, whereas the NOMU—Parallel Market was initiated in 2017 under Tadawul. While both markets had a slow start at the outset, interest has noticeably grown in the past few years (see Table A1 in the Appendix A). |

| 6 | An unbalanced sample is used, where the starting date is selected based on the following two considerations: the first is data availability for the corresponding SME market index, and the second is the desire to avoid any overlap with previous crises, including the European sovereign debt crisis (2010–2012) and the 2013 Egyptian coup d’état. Accordingly, the sample starting date was 24 July 2013, for Egypt, and 27 February 2017, for Saudi Arabia, and the sample ended on 20 November 2020, for both markets. |

| 7 | The starting date of the COVID-19 subsample was 31 December 2019, according to the World Health Organization (WHO) (see WHO 2020). |

| 8 | https://www.imf.org/en/News/Articles/2021/07/14/na070621-egypt-overcoming-the-COVID-shock-and-maintaining-growth (accessed on 15 June 2021). |

| 9 | , which denotes how shocks in the main stock market are transmitted to the SME stock market and how the main stock market receives shocks from the SME stock market . |

| 10 | |

| 11 | The normality assumption produces the highest value of the log-likelihood; see, e.g., Liu et al. (2017). |

| 12 | Jin et al. (2020) also examine hedging performance. |

| 13 | Table A2 in the Appendix A displays the postestimation diagnostics for the bivariate VAR (1)-asymmetric BEKK–GARCH (1,1) and VAR (1)-asymmetric DCC–GARCH (1,1) models. The Ljung–Box and Engle ARCH–LM tests at five lags are used to test for the presence of serial correlation and heteroskedasticity in the standardized residuals, respectively. All the models pass the diagnostic tests, suggesting that they are well specified. |

| 14 | Al Rasasi et al. (2019) examine the stock market and economic growth nexus in Saudi Arabia. They find a significant long-run relationship between the real price level of the main market index and real economic activity, indicating that stock prices have a significant impact on real economic growth. |

| 15 | A major advantage of the model is its capacity to account for cross-market asymmetric shock spillovers, which capture whether a positive or a negative shock in one market translates to either a positive or negative shock in another market. |

| 16 | The Egyptian Exchange is embarking on a restructuring plan for the Nile Exchange with the European Bank for Reconstruction and Development (Enterprise 2020a). |

| 17 | Campbell et al. (2002) show that during periods of heightened volatility, stocks tend to become more correlated. This finding has important implications for portfolio and risk management because it means that the benefits of diversification are somewhat undermined just when investors have the greatest need for them. |

References

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021a. Financial Contagion during COVID-19 Crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Zaghum Umar. 2021b. COVID-19 media coverage and ESG leader indices. Finance Research Letters, 102170. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, Brian M. Lucey, and Ahmet Sensoy. 2021c. Is gold a hedge or a safe-haven asset in the COVID–19 crisis? Economic Modelling 102: 105588. [Google Scholar] [CrossRef]

- Al Rasasi, Moayad H., Soleman O. Alsabban, and Omar A. Alarfaj. 2019. Does Stock Market Performance Affect Economic Growth? Empirical Evidence from Saudi Arabia. International Journal of Economics and Finance 11: 1–21. [Google Scholar] [CrossRef] [Green Version]

- Alexakis, Christos, and Vasileios Pappas. 2018. Sectoral dynamics of financial contagion in Europe—The cases of the recent crises episodes. Economic Modelling 73: 222–39. [Google Scholar] [CrossRef]

- Al-Yahyaee, Khamis Hamed, Walid Mensi, Ahmet Sensoy, and Sang Hoon Kang. 2019. Energy, precious metals, and GCC stock markets: Is there any risk spillover? Pacific-Basin Finance Journal 56: 45–70. [Google Scholar] [CrossRef]

- Arouri, Mohammed El Hedi, Sabri Boubaker, and Duc Khuong Nguyen. 2013. Emerging Markets and the Global Economy: A Handbook. Cambridge: Academic Press. [Google Scholar]

- Asl, Mahdi Ghaemi, Giorgio Canarella, and Stephen M. Miller. 2021. Dynamic asymmetric optimal portfolio allocation between energy stocks and energy commodities: Evidence from clean energy and oil and gas companies. Resources Policy 71: 101982. [Google Scholar] [CrossRef]

- Bahloul, Slah, and Imen Khemakhem. 2021. Dynamic return and volatility connectedness between commodities and Islamic stock market indices. Resources Policy 71: 101993. [Google Scholar] [CrossRef]

- Basher, Syed Abul, and Perry Sadorsky. 2016. Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GO-GARCH. Energy Economics 54: 235–47. [Google Scholar] [CrossRef] [Green Version]

- Baumöhl, Eduard, and Štefan Lyócsa. 2014. Volatility and dynamic conditional correlations of worldwide emerging and frontier markets. Economic Modelling 38: 175–83. [Google Scholar] [CrossRef]

- Beck, Thorsten, Asli Demirguc-Kunt, and Vojislav Maksimovic. 2008. Financing Patterns around the World: Are Small Firms Different? Journal of Financial Economics 89: 467–87. [Google Scholar] [CrossRef] [Green Version]

- Berger, Allen N., and Gregory F. Udell. 2006. A more complete conceptual framework for SME finance. Journal of Banking & Finance 30: 2945–66. [Google Scholar] [CrossRef]

- Boldanov, Rustam, Stavros Degiannakis, and George Filis. 2016. Time-varying correlation between oil and stock market volatilities: Evidence from oil-importing and oil-exporting countries. International Review of Financial Analysis 48: 209–20. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, Sabri, Bonnie Buchanan, and Duc Khuong Nguyen. 2016. Risk Management in Emerging Markets: Issues, Framework, and Modeling. Bingley: Emerald Group Publishing. [Google Scholar]

- Campbell, Rachel, Kees Koedijk, and Paul Kofman. 2002. Increased Correlation in Bear Markets. Financial Analysts Journal 58: 87–94. [Google Scholar] [CrossRef]

- Cappiello, Lorenzo, Robert F. Engle, and Kevin Sheppard. 2006. Asymmetric Dynamics in the Correlations of Global Equity and Bond Returns. Journal of Financial Econometrics 4: 537–72. [Google Scholar] [CrossRef]

- Corbet, Shaen, Yang Hou, Yang Hu, Les Oxley, and Danyang Xu. 2021. Pandemic-related financial market volatility spillovers: Evidence from the Chinese COVID-19 epicentre. International Review of Economics & Finance 71: 55–81. [Google Scholar] [CrossRef]

- Cosh, Andy, Douglas Cumming, and Alan Hughes. 2009. Outside Enterpreneurial Capital. The Economic Journal 119: 1494–533. [Google Scholar] [CrossRef]

- Cowling, Marc, Weixi Liu, and Ning Zhang. 2016. Access to bank finance for UK SMEs in the wake of the recent financial crisis. International Journal of Entrepreneurial Behavior & Research 22: 903–32. [Google Scholar] [CrossRef] [Green Version]

- Cumming, Douglas, Marc Deloof, Sophie Manigart, and Mike Wright. 2019. New directions in entrepreneurial finance. Journal of Banking & Finance 100: 252–60. [Google Scholar] [CrossRef]

- D’Amato, Antonio. 2019. Capital Structure, Debt Maturity, and Financial Crisis: Empirical Evidence from SMEs. Small Business Economics 55: 919–41. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1981. Likelihood Ratio Statistics for Autoregressive Time Series with a Unit Root. Econometrica 49: 1057–72. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yılmaz. 2014. On the network topology of variance decompositions: Measuring the connectedness of financial firms. Journal of Econometrics 182: 119–34. [Google Scholar] [CrossRef] [Green Version]

- Ederington, Louis H. 1979. The Hedging Performance of the New Futures Markets. The Journal of Finance 34: 157–70. [Google Scholar] [CrossRef]

- Elsayed, Ahmed H., and Larisa Yarovaya. 2019. Financial stress dynamics in the MENA region: Evidence from the Arab Spring. Journal of International Financial Markets, Institutions and Money 62: 20–34. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 50: 987–1007. [Google Scholar] [CrossRef]

- Engle, Robert F. 2002. Dynamic Conditional Correlation. Journal of Business & Economic Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Engle, Robert F., and Kenneth F. Kroner. 1995. Multivariate Simultaneous Generalized ARCH. Econometric Theory 11: 122–50. [Google Scholar] [CrossRef]

- Enterprise. 2020a. EBRD Could Support Small-Caps Facing New Sponsor Regs. Available online: https://enterprise.press/stories/2020/09/08/ebrd-could-support-small-caps-facing-new-sponsor-regs-21459/ (accessed on 15 June 2021).

- Enterprise. 2020b. Speed Medical to be the First Jump from Nilex to the EGX. Available online: https://enterprise.press/stories/2020/12/03/speed-medical-to-be-the-first-jump-from-nilex-to-the-egx-26032/ (accessed on 15 June 2021).

- Ferrando, Annalisa, and Alessandro Ruggieri. 2018. Financial constraints and productivity: Evidence from euro area companies. International Journal of Finance & Economics 23: 257–82. [Google Scholar] [CrossRef]

- Fleming, Jeff, Chris Kirby, and Barbara Ostdiek. 1998. Information and volatility linkages in the stock, bond, and money markets. Journal of Financial Economics 49: 111–37. [Google Scholar] [CrossRef]

- Gharib, C., S. Mefteh-Wali, and S. B. Jabeur. 2021. The Bubble Contagion Effect of COVID-19 Outbreak: Evidence from Crude Oil and Gold Markets. Finance Research Letters 38: 101703. [Google Scholar] [CrossRef]

- Glosten, Lawrence R, Ravi Jagannathan, and David E Runkle. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. J. Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Hatemi-J, Abdulnasser. 2012. Asymmetric causality tests with an application. Empirical Economics 43: 447–56. [Google Scholar] [CrossRef]

- Hemche, Omar, Fredj Jawadi, Samir B. Maliki, and Abdoulkarim Idi Cheffou. 2016. On the study of contagion in the context of the subprime crisis: A dynamic conditional correlation–multivariate GARCH approach. Economic Modelling 52: 292–99. [Google Scholar] [CrossRef]

- Hou, Yang, and Steven Li. 2016. Information transmission between U.S. and China index futures markets: An asymmetric DCC GARCH approach. Economic Modelling 52: 884–97. [Google Scholar] [CrossRef]

- Hwang, Jae-Kwang. 2014. Spillover effects of the 2008 financial crisis in Latin America stock markets. International Advances in Economic Research 20: 311–24. [Google Scholar] [CrossRef]

- Iglesias-Casal, Ana, María Celia López-Penabad, Carmen López-Andión, and José Manuel Maside-Sanfiz. 2020. Diversification and Optimal Hedges for Socially Responsible Investment in Brazil. Economic Modelling 85: 106–18. [Google Scholar] [CrossRef]

- Jaffee, Dwight M., and Thomas Russell. 1976. Imperfect Information, Uncertainty, and Credit Rationing. The Quarterly Journal of Economics 90: 651–66. [Google Scholar] [CrossRef]

- Jarque, Carlos M., and Anil K. Bera. 1980. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Economics Letters 6: 255–59. [Google Scholar] [CrossRef]

- Jiang, Yonghong, Yuyuan Fu, and Weihua Ruan. 2019. Risk Spillovers and Portfolio Management between Precious Metal and BRICS Stock Markets. Physica A: Statistical Mechanics and its Applications 534: 120993. [Google Scholar] [CrossRef]

- Jin, Jiayu, Liyan Han, Lei Wu, and Hongchao Zeng. 2020. The hedging effectiveness of global sectors in emerging and developed stock markets. International Review of Economics & Finance 66: 92–117. [Google Scholar] [CrossRef]

- Junttila, Juha, Juho Pesonen, and Juhani Raatikainen. 2018. Commodity market based hedging against stock market risk in times of financial crisis: The case of crude oil and gold. Journal of International Financial Markets, Institutions and Money 56: 255–80. [Google Scholar] [CrossRef]

- Karanasos, Menelaos, Alexandros G. Paraskevopoulos, Faek Menla Ali, Michail Karoglou, and Stavroula Yfanti. 2014. Modelling stock volatilities during financial crises: A time varying coefficient approach. Journal of Empirical Finance 29: 113–28. [Google Scholar] [CrossRef] [Green Version]

- Karmakar, Madhusudan. 2010. Information transmission between small and large stocks in the National Stock Exchange in India: An empirical study. The Quarterly Review of Economics and Finance 50: 110–20. [Google Scholar] [CrossRef]

- Kinateder, Harald, Ross Campbell, and Tonmoy Choudhury. 2021. Safe haven in GFC versus COVID-19: 100 turbulent days in the financial markets. Finance Research Letters 43: 101951. [Google Scholar] [CrossRef]

- Koulakiotis, Athanasios, Vassilios Babalos, and Nicholas Papasyriopoulos. 2016. Financial crisis, liquidity and dynamic linkages between large and small stocks: Evidence from the Athens Stock Exchange. Journal of International Financial Markets, Institutions and Money 40: 46–62. [Google Scholar] [CrossRef]

- Kroner, Kenneth F., and Victor K. Ng. 1998. Modeling Asymmetric Comovements of Asset Returns. Review of Financial Studies 11: 817–44. [Google Scholar] [CrossRef]

- Kroner, Kenneth F., and Jahangir Sultan. 1993. Time-Varying Distributions and Dynamic Hedging with Foreign Currency Futures. The Journal of Financial and Quantitative Analysis 28: 535–51. [Google Scholar] [CrossRef]

- Kyrkilis, Dimitrios, Athanasios Koulakiotis, Vassilios Babalos, and Maria Kyriakou. 2018. Feedback Trading and Short-Term Return Dynamics in Athens Stock Exchange. International Journal of Managerial Finance 14: 574–90. [Google Scholar] [CrossRef]

- Li, Hong. 2007. International linkages of the Chinese stock exchanges: A multivariate GARCH analysis. Applied Financial Economics 17: 285–97. [Google Scholar] [CrossRef]

- Ling, Shiqing, and Michael McAleer. 2003. Asymptotic Theory for a Vector ARMA-GARCH Model. Econometric Theory 19: 280–310. [Google Scholar] [CrossRef] [Green Version]

- Liu, Xueyong, Haizhong An, Shupei Huang, and Shaobo Wen. 2017. The evolution of spillover effects between oil and stock markets across multi-scales using a wavelet-based GARCH–BEKK model. Physica A: Statistical Mechanics and its Applications 465: 374–83. [Google Scholar] [CrossRef] [Green Version]

- Lo, Andrew W., and A. Craig MacKinlay. 1990. When Are Contrarian Profits Due to Stock Market Overreaction? Review of Financial Studies 3: 175–205. [Google Scholar] [CrossRef]

- Majumder, Sayantan Bandhu, and Ranjanendra Narayan Nag. 2018. Shock and volatility spillovers among equity sectors of the national stock exchange in India. Global Business Review 19: 227–40. [Google Scholar] [CrossRef]

- Markwat, Thijs, Erik Kole, and Dick van Dijk. 2009. Contagion as a domino effect in global stock markets. Journal of Banking & Finance 33: 1996–2012. [Google Scholar] [CrossRef] [Green Version]

- McAleer, Michael, Suhejla Hoti, and Felix Chan. 2009. Structure and Asymptotic Theory for Multivariate Asymmetric Conditional Volatility. Econometric Reviews 28: 422–40. [Google Scholar] [CrossRef]

- McIver, Ron P., and Sang Hoon Kang. 2020. Financial crises and the dynamics of the spillovers between the U.S. and BRICS stock markets. Research in International Business and Finance 54: 101276. [Google Scholar] [CrossRef]

- Nassr, Iota Kaousar, and Gert Wehinger. 2016. Opportunities and limitations of public equity markets for SMEs. OECD Journal: Financial Market Trends 2015: 49–84. [Google Scholar]

- Nguyen, Duc Khuong, Ricardo M. Sousa, and Gazi Salah Uddin. 2015. Testing for asymmetric causality between U.S. equity returns and commodity futures returns. Finance Research Letters 12: 38–47. [Google Scholar] [CrossRef]

- Nguyen, Trang, Taha Chaiechi, Lynne Eagle, and David Low. 2020. Dynamic transmissions between main stock markets and SME stock markets: Evidence from tropical economies. The Quarterly Review of Economics and Finance 75: 308–24. [Google Scholar] [CrossRef]

- Nikkinen, Jussi, Vanja Piljak, and Timo Rothovius. 2020. Impact of the 2008–2009 financial crisis on the external and internal linkages of European frontier stock markets. Global Finance Journal 46: 100481. [Google Scholar] [CrossRef]

- Papadamou, Stephanos, Athanasios P. Fassas, Dimitris Kenourgios, and Dimitrios Dimitriou. 2021. Flight-to-quality between global stock and bond markets in the COVID era. Finance Research Letters 38: 101852. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., and Pierre Perron. 1988. Testing for a Unit Root in Time Series Regression. Biometrika 75: 335–46. [Google Scholar] [CrossRef]

- Rose, Andrew K., and Mark M. Spiegel. 2010. Cross-country causes and consequences of the 2008 crisis: International linkages and American exposure. Pacific Economic Review 15: 340–63. [Google Scholar] [CrossRef] [Green Version]

- Salisu, Afees A., and Tirimisiyu F. Oloko. 2015. Modeling oil price–US stock nexus: A VARMA–BEKK–AGARCH approach. Energy Economics 50: 1–12. [Google Scholar] [CrossRef]

- Salisu, Afees, Xuan Vinh Vo, and Adedoyin Isola Lawal. 2021. Hedging Oil Price Risk with Gold during COVID-19 Pandemic. Resources Policy 70: 101897. [Google Scholar] [CrossRef]

- Samarakoon, Lalith P. 2011. Stock market interdependence, contagion, and the U.S. financial crisis: The case of emerging and frontier markets. Journal of International Financial Markets, Institutions and Money 21: 724–42. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Dimitris Kenourgios, and Nick Konstantopoulos. 2006. The small business capital market behavior in Athens Stock Exchange. Small Business Economics 27: 409–17. [Google Scholar] [CrossRef]

- Singhal, Shelly, and Sajal Ghosh. 2016. Returns and volatility linkages between international crude oil price, metal and other stock indices in India: Evidence from VAR-DCC-GARCH models. Resources Policy 50: 276–88. [Google Scholar] [CrossRef]

- Stiglitz, Joseph E., and Andrew Weiss. 1981. Credit Rationing in Markets with Imperfect Information. The American Economic Review 71: 393–410. [Google Scholar]

- The World Federation of Exchanges. 2015. WFE Report on SME Exchanges. Available online: https://www.world-exchanges.org/storage/app/media/research/Studies_Reports/WFE%20Report%20on%20SME%20Exchanges.pdf (accessed on 27 February 2021).

- The World Federation of Exchanges. 2018. An Overview of WFE SME Markets. Available online: https://www.world-exchanges.org/news/articles/world-federation-exchanges-publishes-report-global-sme-markets (accessed on 27 February 2021).

- Tiwari, Aviral Kumar, and Claudiu Tiberiu Albulescu. 2016. Oil price and exchange rate in India: Fresh evidence from continuous wavelet approach and asymmetric, multi-horizon Granger-causality tests. Applied Energy 179: 272–83. [Google Scholar] [CrossRef]

- Tiwari, Aviral Kumar, Ibrahim Dolapo Raheem, and Sang Hoon Kang. 2019. Time-varying dynamic conditional correlation between stock and cryptocurrency markets using the copula-ADCC-EGARCH model. Physica A: Statistical Mechanics and its Applications 535: 122295. [Google Scholar] [CrossRef]

- Umar, Zaghum, Youssef Manel, Yasir Riaz, and Mariya Gubareva. 2021. Return and volatility transmission between emerging markets and US debt throughout the pandemic crisis. Pacific-Basin Finance Journal 67: 101563. [Google Scholar] [CrossRef]

- Vardar, Gülin, Yener Coşkun, and Tezer Yelkenci. 2018. Shock transmission and volatility spillover in stock and commodity markets: Evidence from advanced and emerging markets. Eurasian Economic Review 8: 231–88. [Google Scholar] [CrossRef]

- Vismara, Silvio, Stefano Paleari, and Jay R. Ritter. 2012. Europe’s Second Markets for Small Companies. European Financial Management 18: 352–88. [Google Scholar] [CrossRef]

- Vrieze, Scott I. 2012. Model Selection and Psychological Theory: A Discussion of the Differences between the Akaike Information Criterion (AIC) and the Bayesian Information Criterion (BIC). Psychol Methods 17: 228–43. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wang, Gang Jin, Chi Xie, Zhi Qiang Jiang, and H. Eugene Stanley. 2016. Extreme Risk Spillover Effects in World Gold Markets and The Global Financial Crisis. International Review of Economics & Finance 46: 55–77. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Chi Xie, Min Lin, and H. Eugene Stanley. 2017. Stock Market Contagion during the Global Financial Crisis: A Multiscale Approach. Finance Research Letters 22: 163–68. [Google Scholar] [CrossRef]

- Wen, Xiaoqian, Yanfeng Guo, Yu Wei, and Dengshi Huang. 2014. How do the stock prices of new energy and fossil fuel companies correlate? Evidence from China. Energy Economics 41: 63–75. [Google Scholar] [CrossRef]

- Wen, Danyan, Yudong Wang, Chaoqun Ma, and Yaojie Zhang. 2020. Information transmission between gold and financial assets: Mean, volatility, or risk spillovers? Resources Policy 69: 101871. [Google Scholar] [CrossRef]

- WHO. 2020. Novel Coronavirus (2019-nCOV) Situation Report-1. Available online: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200121-sitrep-1-2019-ncov.pdf?sfvrsn=20a99c10_4 (accessed on 10 March 2021).

- Wu, Fei, Dayong Zhang, and Zhiwei Zhang. 2019. Connectedness and risk spillovers in China’s stock market: A sectoral analysis. Economic Systems 43: 100718. [Google Scholar] [CrossRef]

- Xu, Haifeng, and Shigeyuki Hamori. 2012. Dynamic Linkages of Stock Prices between the BRICs and the United States: Effects of the 2008–09 Financial Crisis. Journal of Asian Economics 23: 344–52. [Google Scholar] [CrossRef]

- Xu, Weiju, Feng Ma, Wang Chen, and Bing Zhang. 2019. Asymmetric volatility spillovers between oil and stock markets: Evidence from China and the United States. Energy Economics 80: 310–20. [Google Scholar] [CrossRef]

- Yarovaya, Larisa, and Marco Chi Keung Lau. 2016. Stock market comovements around the Global Financial Crisis: Evidence from the UK, BRICS and MIST markets. Research in International Business and Finance 37: 605–19. [Google Scholar] [CrossRef]

- Yu, Lean, Rui Zha, Dimitrios Stafylas, Kaijian He, and Jia Liu. 2020. Dependences and volatility spillovers between the oil and stock markets: New evidence from the copula and VAR-BEKK-GARCH models. International Review of Financial Analysis 68: 101280. [Google Scholar] [CrossRef]

- Zhang, Wenting, and Shigeyuki Hamori. 2021. Crude oil market and stock markets during the COVID-19 pandemic: Evidence from the US, Japan, and Germany. International Review of Financial Analysis 74: 101702. [Google Scholar] [CrossRef]

| Full Sample Period | Before the COVID-19 Crisis | During the COVID-19 Crisis | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Saudi Arabia | Egypt | Saudi Arabia | Egypt | Saudi Arabia | Egypt | |||||||

| TASI | NOMU | EGX 30 | NILEX | TASI | NOMU | EGX 30 | NILEX | TASI | NOMU | EGX 30 | NILEX | |

| Mean (%) | 0.0213 | 0.1260 | 0.0332 | 0.0087 | 0.0250 | 0.0264 | 0.0527 | −0.0379 | 0.0111 | 0.462 | −0.114 | 0.383 |

| S.D. (%) | 1.898 | 2.824 | 1.362 | 1.011 | 0.857 | 2.226 | 1.299 | 0.813 | 2.123 | 4.186 | 1.786 | 1.946 |

| Skew. | −3.633 | 0.413 | −0.500 | 0.261 | −0.033 | 1.267 | −0.181 | −0.150 | −4.109 | −0.249 | −1.336 | −0.062 |

| Kurt. | 6.960 | 14.380 | 8.021 | 5.350 | 10.678 | 40.90 | 6.306 | 5.294 | 3.992 | 7.432 | 9.931 | 2.057 |

| J–B [Prob] | 12312.1 [0.0000] | 12298.3 [0.0000] | 2088.45 [0.0000] | 461.74 [0.0000] | 1820.32 [0.0000] | 44567.57 [0.0000] | 783.49 [0.0000] | 379.27 [0.0000] | 13832.7 [0.0000] | 192.34 [0.0000] | 487.52 [0.0000] | 7.989 [0.0184] |

| ADF test | −11.40 *** | −33.02 *** | −34.48 *** | −27.42 *** | −25.96 *** | −25.65 *** | −33.03 *** | −30.36 *** | −4.89 *** | −17.92 *** | −10.89 *** | −10.13 *** |

| PP test | −34.43 *** | −33.04 *** | −34.42 *** | −31.08 *** | −26.00 *** | −25.62 *** | −33.02 *** | −29.78 *** | −18.55 *** | −17.92 *** | −10.90 *** | −10.45 *** |

| ARCH–LM(5) | 59.02 *** | 79.35 *** | 273.66 *** | 472.49 *** | 11.67 *** | 177.4 *** | 135.31 *** | 235.4 *** | 15.23 *** | 18.66 *** | 66.95 *** | 15.37 ** |

| 32.21 *** | 31.43 *** | 8.280 * | 15.90 *** | 5.43 *** | 4.61 | 5.31 | 18.125 *** | 32.1 *** | 3.57 | 10.2 *** | 8.76 * | |

| 82.85 *** | 135.06 *** | 455.77 *** | 1089.7 *** | 11.92 *** | 200.34 *** | 197.52 *** | 459.5 *** | 17.79 *** | 21.77 *** | 108.11 *** | 19.52 *** | |

| 0.320 | - | 0.308 | - | 0.125 | - | 0.40 | - | 0.44 | - | 0.136 | - | |

| Null Hypothesis | Full Sample Period | Before COVID-19 | During COVID-19 | |||

|---|---|---|---|---|---|---|

| F Statistic | Prob. | F Statistic | Prob. | F Statistic | Prob. | |

| Panel A: Saudi Arabia | ||||||

| 6.150 | 0. 2531 | 2.689 | 0.2606 | 7.9111 | 0.2447 | |

| 4.697 | 0.6975 | 14.067 * | 0.0800 | 11.689 | 0.1112 | |

| 17.790 ** | 0.0129 | 10.7162 | 0.2183 | 7.2451 | 0.5104 | |

| 49.037 *** | 0.0000 | 5.676 | 0.1285 | 71.596 *** | 0.0000 | |

| 62.792 *** | 0.0000 | 10.375 *** | 0.0056 | 34.181 *** | 0.0000 | |

| 31.515 *** | 0.0001 | 8.1965 | 0.4145 | 17.133 *** | 0.0001 | |

| 21.510 *** | 0.0001 | 13.983 | 0.1000 | 21.790 *** | 0.0003 | |

| 21.226 *** | 0.0017 | 3.5871 | 0.3096 | 9.3461 | 0.1550 | |

| Panel B: Egypt | ||||||

| 23.157 ** | 0.0016 | 13.680 *** | 0.0084 | 9.341 * | 0.0531 | |

| 14.222 ** | 0.0143 | 13.123 *** | 0.0004 | 5.7398 | 0.1250 | |

| 2.011 | 0.8475 | 9.369 * | 0.0952 | 1.5012 | 0.8460 | |

| 24.279 *** | 0.0001 | 28.693 *** | 0.0000 | 3.1651 | 0.2054 | |

| 17.421 ** | 0.0149 | 10.203 *** | 0.0001 | 6.2447 | 0.1816 | |

| 36.819 *** | 0.0000 | 5.0603 | 0.1674 | 7.201 *** | 0.0007 | |

| 17.955 *** | 0.0030 | 9.0561 | 0.1069 | 0.2396 | 0.9934 | |

| 1.428 | 0.8392 | 0.4557 | 0.9777 | 0.2762 | 0.8710 | |

| Before COVID-19 Crisis | During COVID-19 Crisis | |||||

|---|---|---|---|---|---|---|

| Panel A: Saudi Arabia | ||||||

| TASI | NOMU | From others | TASI | NOMU | From others | |

| TASI | 99.8 | 0.2 | 0.2 | 94.4 | 5.6 | 5.6 |

| NOMU | 3 | 97 | 3 | 19.8 | 80.2 | 19.8 |

| To others | 3 | 0.2 | 19.8 | 5.6 | ||

| Net spillover | 2.8 | −2.8 | Total spillover index = 1.6% | 14.2 | −14.2 | Total spillover index = 12.7% |

| Panel B: Egypt | ||||||

| EGX 30 | NILEX | From others | EGX 30 | NILEX | From others | |

| EGX30 | 99.8 | 0.2 | 0.2 | 100 | 00 | 00 |

| NILEX | 15.8 | 84.2 | 15.8 | 1.7 | 98.3 | 1.7 |

| To others | 15.8 | 0.2 | 1.7 | 00 | ||

| Net spillover | 15.6 | −15.6 | Total spillover index = 8% | 1.7 | −1.7 | Total spillover index = 1% |

| Full Sample Period | Before the COVID-19 Crisis | During the COVID-19 Crisis | ||||

|---|---|---|---|---|---|---|

| TASI and NOMU | EGX30 and NILEX | TASI and NOMU | EGX30 and NILEX | TASI and NOMU | EGX30 and NILEX | |

| Panel A: Mean equation (return spillover effect) | ||||||

| 0.00441 (0.03652) | 0.02496 (0.02386) | 0.03081 (0.03035) | 0.03547 (0.02400) | 0.18085 ** (0.07248) | 0.00300 (0.07981) | |

| 0.16369 *** (0.04343) | 0.24139 *** (0.02293) | 0.08339 ** (0.04230) | 0.23174 *** (0.02495) | −0.19311 *** (0.08229) | 0.22984 *** (0.07140) | |

| 0.02293 ** (0.01410) | −0.01629 (0.02555) | 0.01402 ** (0.00563) | −0.00342 (0.03445) | 0.01955 (0.01786) | −0.04440 (0.04208) | |

| −0.10026 (0.07192) | −0.02204 (0.01343) | −0.12944 ** (0.05494) | −0.02412 ** (0.01398) | 0.676519 * (0.20550) | 0.25902 ** (0.11792) | |

| 0.20119 ** (0.04570) | 0.01249 (0.01108) | 0.15090 ** (0.06899) | 0.01192 (0.01167) | −0.156405 (0.25054) | −0.03511 (0.07178) | |

| −0.01695 ** (0.04336) | 0.25350 *** (0.02071) | −0.01509 ** (0.04411) | 0.24408 *** (0.02433) | −0.140690 *** (0.07654) | 0.27365 *** (0.05919) | |

| Panel B: Conditional variance equations (volatility spillover effect) | ||||||

| 0.25100 *** (0.03165) | 0.43191 *** (0.03992) | 0.23309 *** (0.03576) | 0.47387 *** (0.04431) | 0.17362 *** (0.07161) | 0.18913 (0.11962) | |

| 0.05366 (0.14411) | 0.06673 *** (0.01349) | 0.22025 *** (0.08526) | 0.04275 *** (0.01644) | −1.70020 *** (0.28934) | −0.18464 (0.48177) | |

| 0.76324 *** (0.09685) | −0.00374 (0.25423) | 0.37944 *** (0.06072) | 0.00000 (0.03578) | −0.00010 (2.63984) | 0.51744 ** (0.30220) | |

| 0.18592 ** (0.06413) | 0.28356 *** (0.03222) | 0.14763 ** (0.04705) | 0.30402 *** (0.03688) | −0.17436 ** (0.09028) | −0.25080 ** (0.09743) | |

| −0.3409 ** (0.01228) | 0.01858 (0.01240) | −0.33526 *** (0.07529) | 0.02033 ** (0.01237) | −0.53576 ** (0.33170) | −0.14173 (0.10435) | |

| 0.02236 ** (0.01259) | −0.00077 (0.03448) | 0.01115 ** (0.01572) | 0.04961 ** (0.04788) | −0.04630 ** (0.02040) | −0.03797 (0.05555) | |

| 0.53654 *** (0.05210) | 0.23443 *** (0.02194) | 0.35297 *** (0.03025) | 0.22483 *** (0.02131) | 0.39969 *** (0.08641) | 0.38042 *** (0.09274) | |

| 0.92867 *** (0.01425) | 0.84554 *** (0.02298) | 0.93871 *** (0.01564) | 0.81278 *** (0.03000) | 0.87824 *** (0.02634) | 0.88801 *** (0.03354) | |

| 0.20114 *** (0.07706) | −0.03054 *** (0.00823) | −0.00284 (0.03556) | −0.03157 *** (0.00605) | 0.08876 *** (0.07783) | 0.03975 (0.04175) | |

| −0.02635 *** (0.00939) | 0.01965 ** (0.01159) | −0.00734 (0.00569) | 0.05273 *** (0.02078) | 0.05948 *** (0.01653) | 0.03115 (0.04351) | |

| 0.78720 *** (0.03936) | 0.97586 *** (0.00646) | 0.90426 *** (0.01565) | 0.98379 *** (0.00455) | 0.74097 *** (0.06429) | 0.86587 *** (0.07436) | |

| Panel C: Asymmetric effects | ||||||

| 0.51250 *** (0.05722) | 0.35705 *** (0.04325) | 0.29036 *** (0.05282) | 0.36441 *** (0.05091) | 0.44093 *** (0.13762) | 0.39200 *** (0.09881) | |

| −0.08969 (0.18839) | 0.04788 *** (0.01702) | 0.04534 (0.12402) | 0.04897 *** (0.01610) | 0.74479 *** (0.42758) | −0.13556 (0.10703) | |

| 0.00078 (0.03402) | 0.14860 *** (0.05123) | 0.02321 (0.01910) | 0.09098 (0.09086) | −0.0455 (0.03653) | 0.13555 *** (0.06543) | |

| 0.04242 (0.09771) | 0.10959 *** (0.03762) | 0.00803 (0.05792) | 0.07632 ** (0.05251) | −0.00715 (0.17922) | 0.10675 (0.12857) | |

| LL | −2812.210 | −5267.420 | −2345.689 | −4430.582 | −1044.956 | −807.398 |

| AIC | 7.63521 | 5.51926 | 6.35543 | 5.22611 | 9.08582 | 7.70187 |

| Full Sample Period | Before the COVID-19 Crisis | During the COVID-19 Crisis | ||||

|---|---|---|---|---|---|---|

| TASI and NOMU | EGX30 and NILEX | TASI and NOMU | EGX30 and NILEX | TASI and NOMU | EGX 30 and NILEX | |

| Panel A: Mean equation (return spillover effect) | ||||||

| 0.05657 *** (0.01350) | 0.03333 0.02445) | 0.02118 *** (0.00008) | 0.04853 *** (0.00897) | 0.10913 ** (0.05178) | −0.02097 0.06075) | |

| 0.11829 *** (0.02159) | 0.24066 *** (0.02279) | 0.08185 *** (0.00120) | 0.22646 *** (0.02205) | −0.16544 ** (0.06967) | 0.26969 *** (0.07102) | |

| 0.01889 *** (0.00144) | −0.02062 0.02426) | 0.02120 *** (0.00167) | −0.01829 0.03015) | 0.01762 ** (0.00767) | −0.01505 0.03741) | |

| 0.01350 *** (0.00091) | −0.01152 (0.01342) | −0.11419 *** (0.00481) | −0.01534 (0.01281) | 0.77861 *** (0.10711) | 0.24797 ** (0.11092) | |

| 0.14522 *** (0.04590) | 0.00187 (0.01012) | 0.17708 *** (0.06223) | 0.00817 (0.01053) | −0.23337 (0.21170) | 0.01050 (0.06260) | |

| −0.02941 *** (0.00415) | 0.25737 *** (0.02162) | −0.07221 ** (0.04334) | 0.26244 *** (0.02063) | −0.12911 *** (0.03970) | 0.28056 *** (0.05352) | |

| Panel B: Conditional variance equations (volatility spillover effect) | ||||||

| 0.08100 *** (0.00624) | 0.22313 *** (0.04364) | 0.34316 *** (0.00883) | 0.40755 *** (0.01414) | −0.03929 *** (0.00273) | 0.05606 *** (0.01525) | |

| 0.26446 *** (0.02568) | 0.00885 *** (0.00233) | 0.22825 *** (0.01010) | 0.02833 *** (0.00174) | 1.28638 *** (0.09560) | 1.65014 *** (0.20122) | |

| 0.10580 *** (0.00399) | 0.10056 *** (0.02164) | 0.03871 *** (0.00131) | 0.15492 *** (0.00386) | 0.05583 *** (0.00941) | 0.14108 *** (0.01465) | |

| −0.00220 *** (0.00004) | 0.07170 *** (0.00918) | −0.00102 *** (0.00002) | 0.06672 *** (0.02012) | −0.00506 *** (0.00042) | 0.02227 *** (0.00384) | |

| 0.23210 *** (0.00706) | 0.15413 *** (0.03368) | 0.08244 *** (0.02517) | 0.14616 *** (0.00152) | 0.16293 *** (0.01112) | 0.03732 *** (0.01928) | |

| 0.22916 *** (0.01963) | 0.00327 ** (0.00160) | 0.02990 ** (0.01569) | 0.01109 *** (0.00008) | 1.87141 *** (0.12688) | 0.01177 (0.03802) | |

| 0.30063 *** (0.00702) | 0.08614 *** (0.01178) | 0.13128 *** (0.00701) | 0.13368 *** (0.00237) | 0.06153 *** (0.00819) | 0.06463 ** (0.03046) | |

| −0.30069 *** (0.02520) | −0.03159 ** (0.01461) | −0.14870 *** (0.02038) | −0.05124 *** (0.00263) | −0.14308 *** (0.00202) | 0.00605 *** (0.08788) | |

| 0.76549 *** (0.00072) | 0.68815 *** (0.04510) | 0.47170 *** (0.01159) | 0.53500 *** (0.00631) | 0.85497 *** (0.00549) | 0.79428 *** (0.01217) | |

| 0.00444 *** (0.00001) | 0.00024 (0.02117) | −0.00062 *** (0.00010) | −0.08176 *** (0.01889) | 0.01182 *** (0.00094) | −0.00831 ** (0.00455) | |

| 0.09770 *** (0.01957) | −0.00673 *** (0.00255) | 0.00971 (0.01440) | −0.02295 *** (0.00051) | −0.44919 *** (0.04882) | −0.00079 (0.04278) | |

| 0.75779 *** (0.00467) | 0.92731 *** (0.01024) | 0.83646 *** (0.00506) | 0.88454 *** (0.00562) | 0.85314 *** (0.00262) | 0.44311 *** (0.05991) | |

| Panel C: Correlation equation (dynamic conditional correlation) | ||||||

| 0.01123 *** (0.00005) | 0.00917 * (0.00566) | 0.06262 *** (0.01081) | 0.02821 ** (0.01793) | 0.02799 *** (0.02127) | 0.01160 (0.04888) | |

| 0.81885 *** (0.00517) | 0.98086 *** (0.00764) | 0.62398 *** (0.11106) | 0.80909 ** (0.07456) | 0.87502 *** (0.02613) | −0.05000 (1.33491) | |

| 0.05333 *** (0.00094) | 0.01071 ** (0.00740) | −0.08302 *** (0.01209) | 0.07106 *** (0.03428) | 0.12703 *** (0.04486) | −0.01784 (0.08549) | |

| LL | −2765.8992 | −5261.614 | −2329.571 | −4426.451 | −1039.771 | −803.425 |

| AIC | 7.61288 | 5.51528 | 6.31733 | 5.22360 | 9.05836 | 7.68326 |

| (%) | (%) | ||||

|---|---|---|---|---|---|

| Panel A: Full sample period | |||||

| TASI/NOMU | 0.265 | 0.133 | 0.142 | 0.323 | 9.4 |

| EGX 30/NILEX | 0.312 | 0.751 | 0.561 | 54.20 | −27.21 |

| Panel B: Before the COVID-19 crisis | |||||

| TASI/NOMU | 0.234 | 0.159 | 0.128 | 0.132 | - |

| EGX 30/NILEX | 0.331 | 0.804 | 0.614 | 62.95 | - |

| Panel C: During the COVID-19 crisis | |||||

| TASI/NOMU | 0.281 | 0.0720 | 0.127 | 0.226 | - |

| EGX 30/NILEX | 0.100 | 0.331 | 0.0586 | 35.74 | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al-Nassar, N.S.; Makram, B. The COVID-19 Outbreak and Risk–Return Spillovers between Main and SME Stock Markets in the MENA Region. Int. J. Financial Stud. 2022, 10, 6. https://doi.org/10.3390/ijfs10010006

Al-Nassar NS, Makram B. The COVID-19 Outbreak and Risk–Return Spillovers between Main and SME Stock Markets in the MENA Region. International Journal of Financial Studies. 2022; 10(1):6. https://doi.org/10.3390/ijfs10010006

Chicago/Turabian StyleAl-Nassar, Nassar S., and Beljid Makram. 2022. "The COVID-19 Outbreak and Risk–Return Spillovers between Main and SME Stock Markets in the MENA Region" International Journal of Financial Studies 10, no. 1: 6. https://doi.org/10.3390/ijfs10010006

APA StyleAl-Nassar, N. S., & Makram, B. (2022). The COVID-19 Outbreak and Risk–Return Spillovers between Main and SME Stock Markets in the MENA Region. International Journal of Financial Studies, 10(1), 6. https://doi.org/10.3390/ijfs10010006