Intraday Patterns of Liquidity on the Warsaw Stock Exchange before and after the Outbreak of the COVID-19 Pandemic

Abstract

1. Introduction

2. Literature Review

2.1. Stock Markets and Liquidity

- Allow a central bank to deploy indirect monetary instruments, resulting in a more stable monetary transmission mechanism;

- Enable financial institutions to accept larger asset-liability mismatches, both in terms of maturity and currency, leading to more efficient crisis management by individual institutions;

- Help financial assets become more appealing to investors by making it easier for them to trade.

- Investors are rational and wealth-maximizing.

- No buyer or seller can affect the price themselves.

- All information is available to all investors and there are no transaction costs.

2.2. Intraday Patterns of Liquidity on the Stock Markets

2.3. The COVID-19 Impact on the Stock Markets

2.4. Warsaw Stock Exchange

- 08:30–09:00—opening call;

- 09:00—opening;

- 09:00–16:50—trading session;

- 16:50–17:00—closing call;

- 17:00—closing;

- 17:00–17:05—trading at last.

3. Methodology

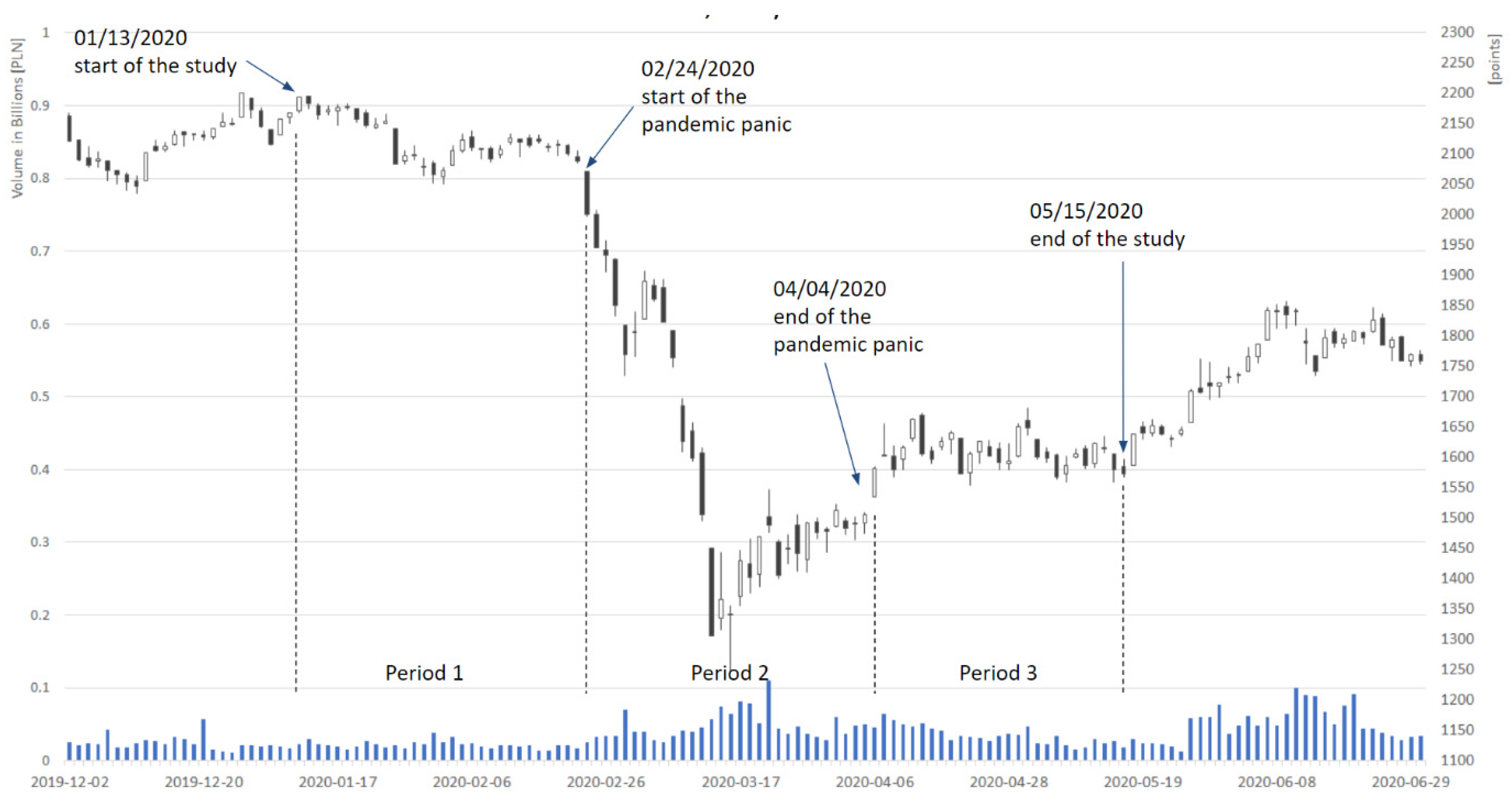

- From 13 January 2020 to 21 February 2020 (Period 1);

- From 24 February 2020 to 4 April 2020 (Period 2);

- From 6 April 2020 to 15 May 2020 (Period 3).

- The number of transactions made;

- The sum of the transaction volume;

- Total turnover;

- The sum of differences between transactions in seconds;

- The sum of the percentage changes caused by transactions.

- The average time interval between transactions in seconds;

- The average percentage change between transactions;

- The average transaction value.

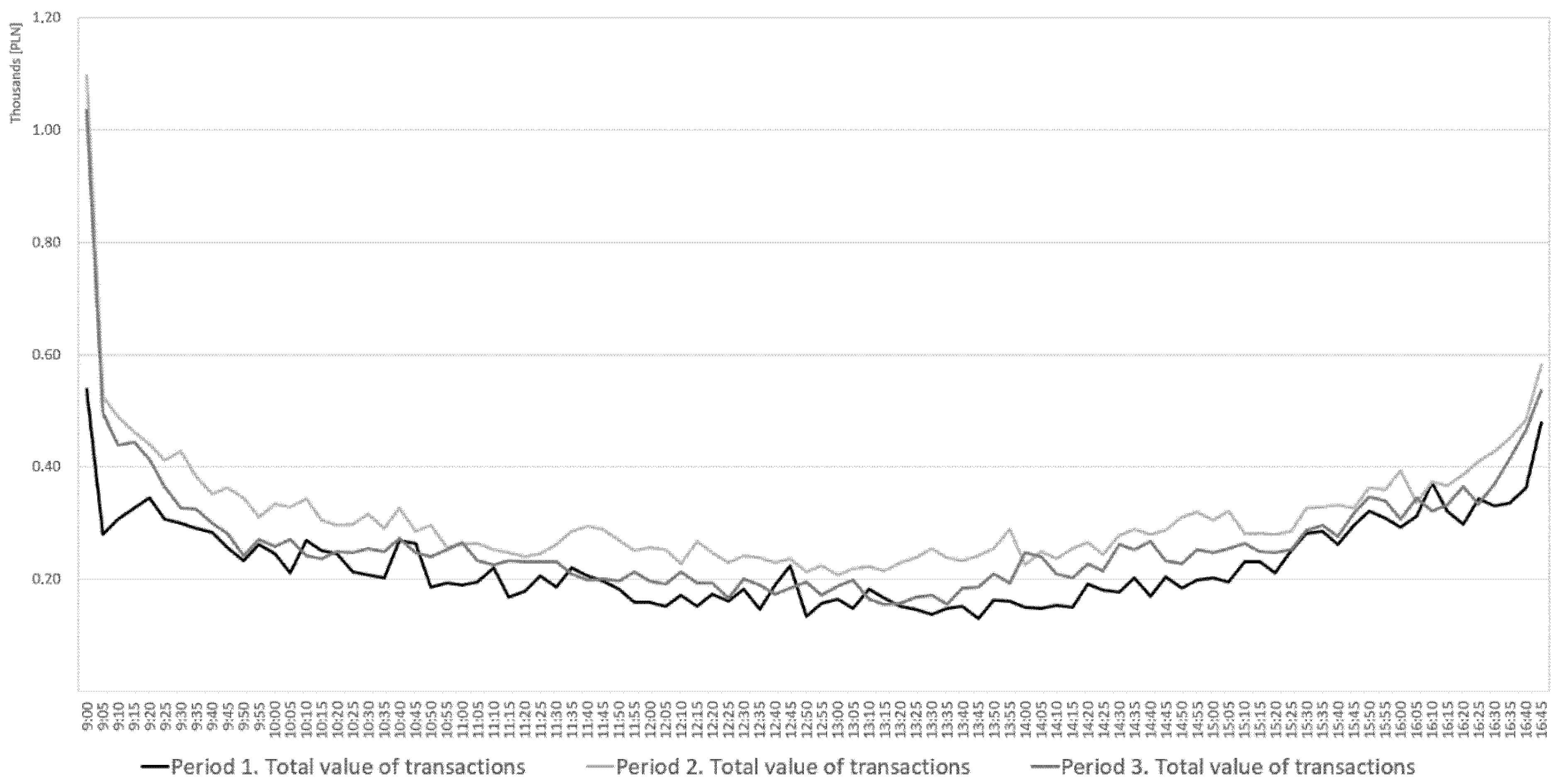

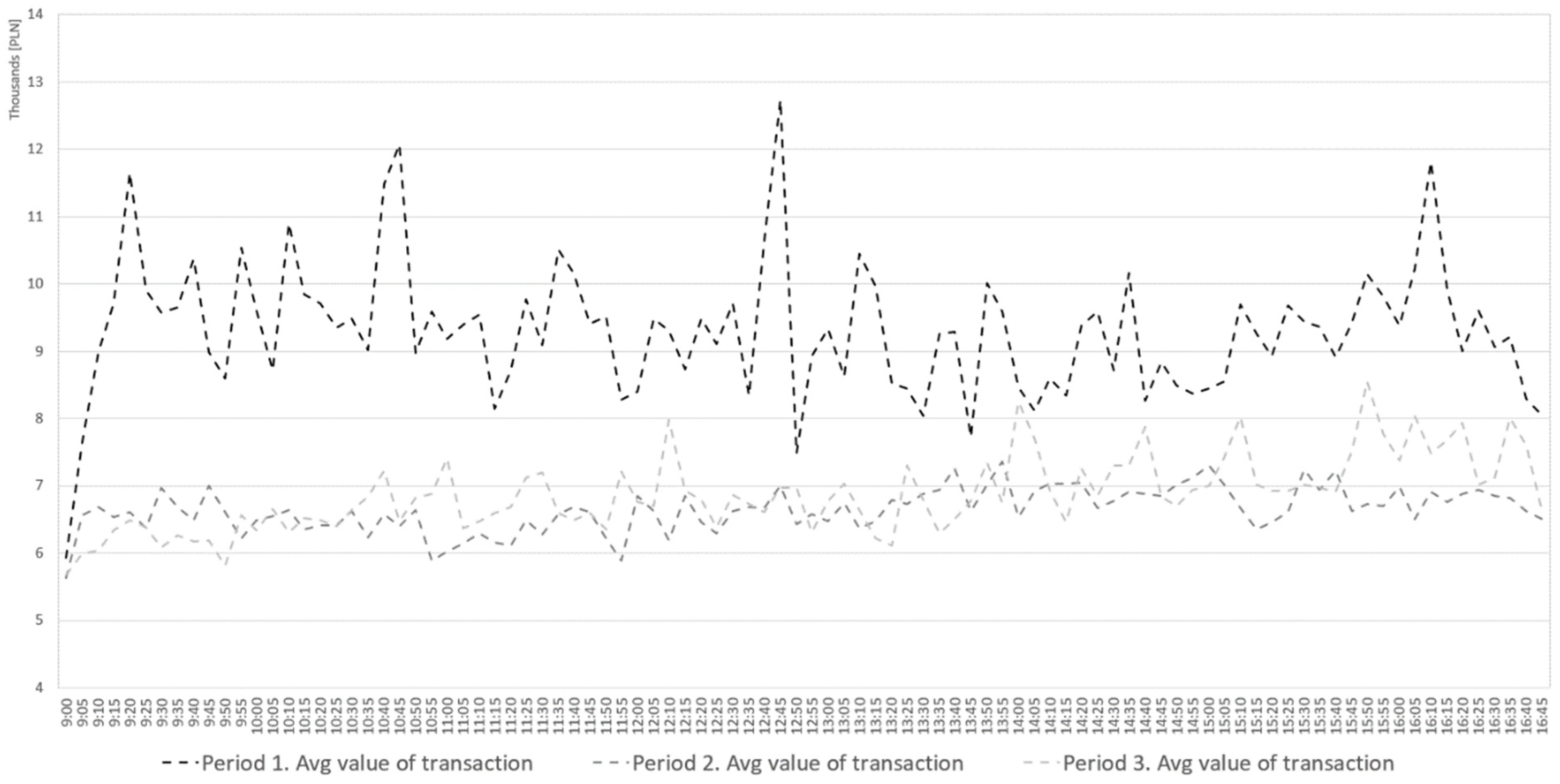

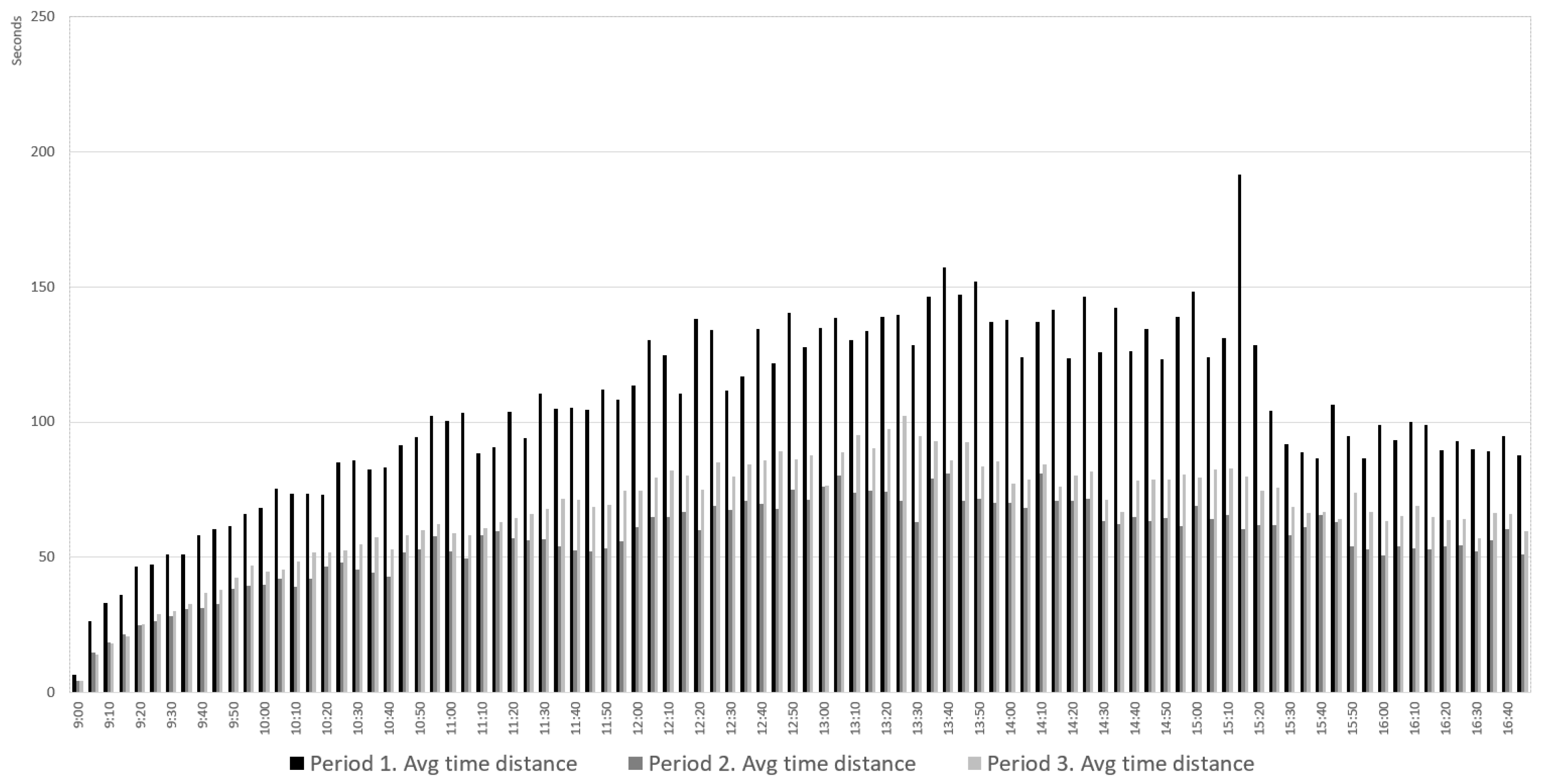

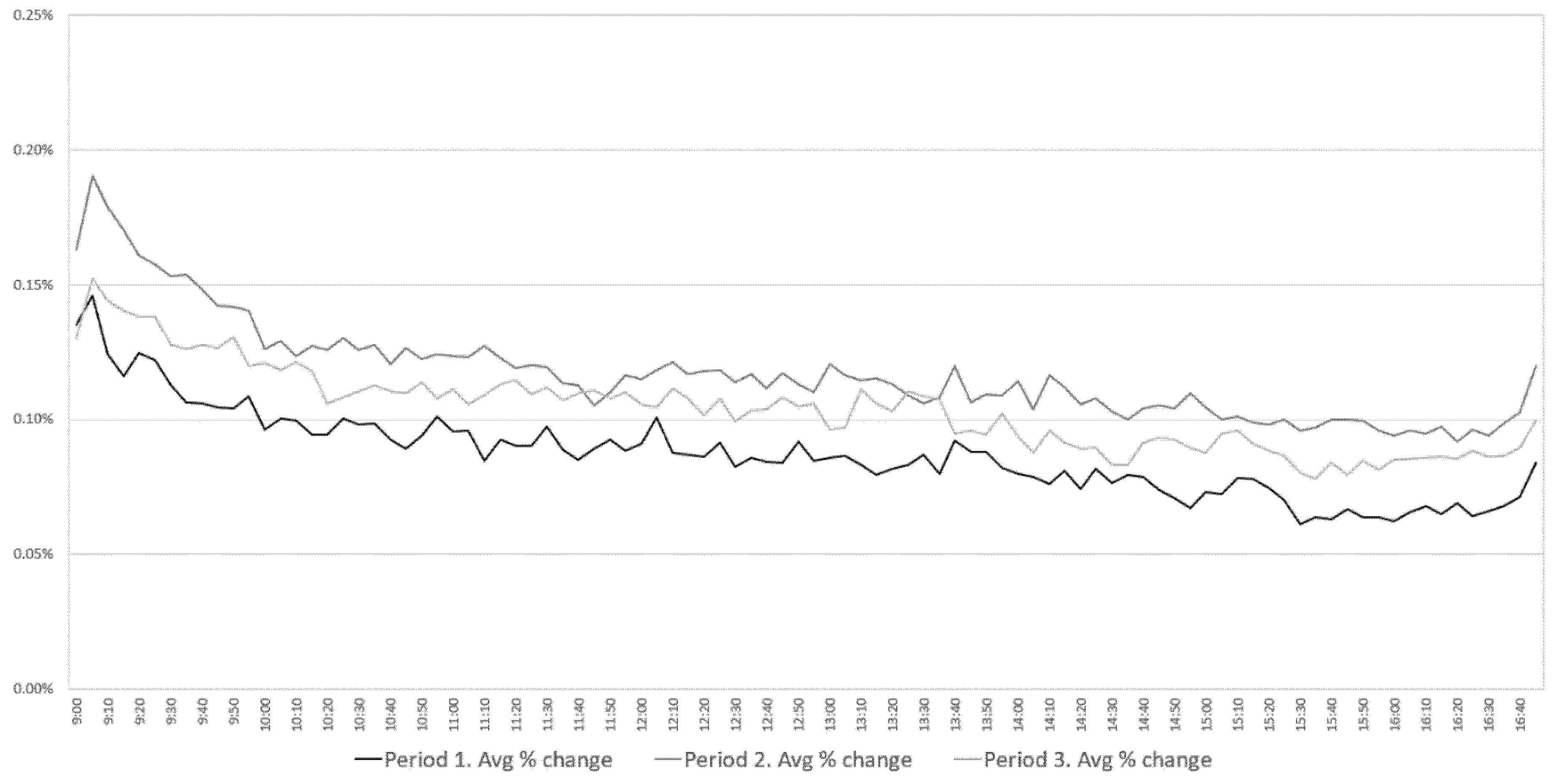

4. Results

Statistical Verification

5. Discussion

6. Conclusions

6.1. Practical Implications

6.2. Limitations

6.3. Further Study

Author Contributions

Funding

Conflicts of Interest

References

- Admati, Anat R., and Paul Pfleiderer. 1988. A theory of intraday patterns: volume and price variability. Review of Financial Studies 1: 3–40. [Google Scholar] [CrossRef]

- Ahn, Hee-Joon, and Yan-Leung Cheung. 1999. The Intraday Patterns of the Spread and Depth in a Market without Market Makers: The Stock Exchange of Hong Kong. Pacific-Basin Finance Journal 7: 539–56. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021a. Financial Contagion during COVID–19 Crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef] [PubMed]

- Akhtaruzzaman, Md, Sabri Boubaker, Brian M. Lucey, and Ahmet Sensoy. 2021b. Is Gold a Hedge or a Safe-Haven Asset in the COVID–19 Crisis? Economic Modelling 102: 105588. [Google Scholar] [CrossRef]

- Al-Awadhi, Abdullah M., Khaled Alsaifi, Ahmad Al-Awadhi, and Salah Alhammadi. 2020. Death and Contagious Infectious Diseases: Impact of the COVID-19 Virus on Stock Market Returns. Journal of Behavioral and Experimental Finance 27: 100326. [Google Scholar] [CrossRef] [PubMed]

- Amihud, Yakov, and Haim Mendelson. 1987. Trading Mechanisms and Stock Returns: An Empirical Investigation. The Journal of Finance 42: 533–53. [Google Scholar] [CrossRef]

- Amihud, Yakov, Haim Mendelson, and Robert A. Wood. 1990. Liquidity and the 1987 Stock Market Crash. The Journal of Portfolio Management 16: 65–69. [Google Scholar] [CrossRef]

- Angerer, Michael, Georg Peter, Sebastian Stoeckl, Thomas Wachter, Matthias Bank, and Marco Menichetti. 2018. Bid-Ask Spread Patterns and the Optimal Timing for Discretionary Liquidity Traders on Xetra. Schmalenbach Business Review 70: 209–30. [Google Scholar] [CrossRef]

- Anghel, Dan Gabriel, Elena Valentina Ţilică, and Victor Dragotă. 2020. Intraday Patterns in Returns on the Romanian and Bulgarian Stock Markets. Romanian Journal of Economic Forecasting 23: 92. [Google Scholar]

- Arif, Muhammad, Mudassar Hasan, Suha M. Alawi, and Muhammad Abubakr Naeem. 2021. COVID-19 and Time-Frequency Connectedness between Green and Conventional Financial Markets. Global Finance Journal 49: 100650. [Google Scholar] [CrossRef]

- Ashraf, Badar Nadeem. 2021. Stock Markets’ Reaction to COVID-19: Moderating Role of National Culture. Finance Research Letters 41: 101857. [Google Scholar] [CrossRef]

- Bai, Lan, Yu Wei, Guiwu Wei, Xiafei Li, and Songyun Zhang. 2021. Infectious Disease Pandemic and Permanent Volatility of International Stock Markets: A Long-Term Perspective. Finance Research Letters 40: 101709. [Google Scholar] [CrossRef]

- Baker, Scott, Nicholas Bloom, Steven Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020. The Unprecedented Stock Market Impact of COVID-19. Working Paper No. 26945. National Bureau of Economic Research: Available online: https://www.nber.org/papers/w26945 (accessed on 26 December 2021).

- Będowska-Sójka, Barbara. 2013. Intraday Stealth Trading and Volatility: The Evidence from the Warsaw Stock Exchange. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Będowska-Sójka, Barbara. 2018. The Coherence of Liquidity Measures. The Evidence from the Emerging Market. Finance Research Letters 27: 118–23. [Google Scholar] [CrossRef]

- Będowska-Sójka, Barbara, and Agata Kilber. 2019. The causality between liquidity and volatility in the Polish stock market. Finance Research Letters 30: 110–115. [Google Scholar] [CrossRef]

- Bernstein, Peter L. 1987. Liquidity, Stock Markets, and Market Makers. Financial Management 16: 54. [Google Scholar] [CrossRef]

- Biais, Bruno, Pierre Hillion, and Chester Spatt. 1995. An Empirical Analysis of the Limit Order Book and the Order Flow in the Paris Bourse. The Journal of Finance 50: 1655–89. [Google Scholar] [CrossRef]

- Bildik, Recep. 2001. Intra-Day Seasonalities on Stock Returns: Evidence from the Turkish Stock Market. Emerging Markets Review 2: 387–417. [Google Scholar] [CrossRef]

- Buszko, Michał, Witold Orzeszko, and Marcin Stawarz. 2021. COVID-19 pandemic and stability of stock market—A sectoral approach. PLoS ONE 16: e0250938. [Google Scholar] [CrossRef]

- Caporale, Guglielmo Maria, Peter G. Howells, and Alaa Soliman. 2004. Stock market development and economic growth: the causal linkage. Journal of Economic Development 29: 33–50. [Google Scholar]

- Chang, Kai, Rongda Chen, and Julien Chevallier. 2018. Market fragmentation, liquidity measures and improvement perspectives from China’s emissions trading scheme pilots. Energy Economics 75: 249–60. [Google Scholar] [CrossRef]

- Chelley-Steeley, Patricia, and Keebong Park. 2011. Intraday Patterns in London Listed Exchange Traded Funds. International Review of Financial Analysis 20: 244–51. [Google Scholar] [CrossRef]

- Contessi, Silvio, and Pierangelo De Pace. 2021. The International Spread of COVID-19 Stock Market Collapses. Finance Research Letters 42: 101894. [Google Scholar] [CrossRef] [PubMed]

- Czerwonka, Monika, and Bartłomiej Gorlewski. 2012. Finanse Behawioralne. Warszawa: Oficyna Wydawnicza SGH. [Google Scholar]

- Dang, Tung Lam, and Thi Minh Hue Nguyen. 2020. Liquidity Risk and Stock Performance during the Financial Crisis. Research in International Business and Finance 52: 101165. [Google Scholar] [CrossRef]

- El Wassal, Kamal A. 2013. The development of stock markets: In search of a theory. International Journal of Economics and Financial Issues 3: 606–24. [Google Scholar]

- Emery, Gary W., and Kenneth O. Cogger. 1982. The Measurement of Liquidity. Journal of Accounting Research 20: 290. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1965. The behavior of stock-market prices. Journal of Business 38: 34–105. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1970. Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance 25: 383. [Google Scholar] [CrossRef]

- Friedman, Milton. 1937. The Use of Ranks to Avoid the Assumption of Normality Implicit in the Analysis of Variance. Journal of the American Statistical Association 32: 675–701. [Google Scholar] [CrossRef]

- Garcia, Valeriano F., and Lin Liu. 1999. Macroeconomic Determinants of Stock Market Development. Journal of Applied Economics 2: 29–59. [Google Scholar] [CrossRef]

- Glavina, Sofya. 2015. Influence of globalization on the regional capital markets and consequences: Evidence from Warsaw stock exchange. European Research Studies Journal 18: 117–34. [Google Scholar] [CrossRef]

- Goyenko, Ruslan Y., Craig W. Holden, and Charles A. Trzcinka. 2009. Do liquidity measures measure liquidity? Journal of Financial Economics 92: 153–81. [Google Scholar] [CrossRef]

- Haddad, Valentin, Alan Moreira, and Tyler Muir. 2020. When Selling Becomes Viral: Disruptions in Debt Markets in the COVID-19 Crisis and the Fed’s Response. Working Paper No. 27168. National Bureau of Economic Research: Available online: https://www.nber.org/papers/w27168 (accessed on 26 December 2021).

- Hanselaar, Rogier M., René M. Stulz, and Mathijs A. van Dijk. 2019. Do Firms Issue More Equity When Markets Become More Liquid? Journal of Financial Economics 133: 64–82. [Google Scholar] [CrossRef]

- Jin, Muzhao, Fearghal Kearney, Youwei Li, and Yung Chiang Yang. 2019. Intraday Time-series Momentum: Evidence from China. Journal of Futures Markets 40: 632–50. [Google Scholar] [CrossRef]

- Kholisoh, Luluk, and Sri Hermawati. 2011. New Liquidity Measurement: Mechanical Approach (Case of Pre Opening Session on IDX). SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Klein, Olga, and Shiyun Song. 2021. Commonality in intraday liquidity and multilateral trading facilities: Evidence from Chi-X Europe. Journal of International Financial Markets, Institutions and Money 73: 101349. [Google Scholar] [CrossRef]

- Krishnan, Rajaram, and Vinod Mishra. 2013. Intraday liquidity patterns in Indian stock market. Journal of Asian Economics 28: 99–114. [Google Scholar] [CrossRef]

- Kszczotek, Mikołaj, Błażej Kiermasz, and Michał Cisek. 2021. Efektywność informacyjna polskiego rynku kapitałowego w formie słabej na przykładzie spółek z indeksu WIG20. Studia Prawno-Ekonomiczne 118: 249–64. [Google Scholar] [CrossRef]

- Kubiczek, Jakub. 2020. Corporate Bond Market in Poland—Prospects for Development. Journal of Risk and Financial Management 13: 306. [Google Scholar] [CrossRef]

- Kubiczek, Jakub, and Wojciech Derej. 2021. Financial performance of businesses in the COVID-19 pandemic conditions–comparative study. Polish Journal of Management Studies 24: 183–201. [Google Scholar] [CrossRef]

- Kubiczek, Jakub, and Bartłomiej Hadasik. 2021. Challenges in reporting COVID-19 daily cases and presenting them to society. Journal of Data and Information Quality 13: 1–7. [Google Scholar] [CrossRef]

- Kumar, Gaurav, and Arun Kumar Misra. 2015. Closer View at the Stock Market Liquidity: A Literature Review. Asian Journal of Finance & Accounting 7: 35. [Google Scholar] [CrossRef]

- Kyle, Albert S. 1985. Continuous Auctions and Insider Trading. Econometrica 53: 1315. [Google Scholar] [CrossRef]

- Levine, Ross. 1991. Stock Markets, Growth, and Tax Policy. The Journal of Finance 46: 1445–65. [Google Scholar] [CrossRef]

- Levine, R., and S. Zervos. 1996. Stock Market Development and Long-Run Growth. The World Bank Economic Review 10: 323–39. [Google Scholar] [CrossRef]

- Lyócsa, Štefan, Eduard Baumöhl, Tomáš Výrost, and Peter Molnár. 2020. Fear of the Coronavirus and the Stock Markets. Finance Research Letters 36: 101735. [Google Scholar] [CrossRef] [PubMed]

- Madhavan, Ananth. 1992. Trading mechanisms in securities markets. The Journal of Finance 47: 607–41. [Google Scholar] [CrossRef]

- Malik, Azeem, and Wing Lon Ng. 2014. Intraday liquidity patterns in limit order books. Studies in Economics and Finance 31: 46–71. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2021. COVID-19 and the March 2020 Stock Market Crash. Evi-dence from S&P1500. Finance Research Letters 38: 101690. [Google Scholar] [CrossRef]

- Miloș, Marius Cristian, Laura Raisa Miloș, Flavia Barna, and Claudiu Boțoc. 2021. Impact of MiFID II on Romanian Stock Market Liquidity—Comparative Analysis with a Developed Stock Market. International Journal of Financial Studies 9: 69. [Google Scholar] [CrossRef]

- Miwa, Kotaro. 2019. Trading Hours Extension and Intraday Price Behavior. International Review of Economics & Finance 64: 572–85. [Google Scholar] [CrossRef]

- Naes, Randi, Johannes A. Skejltorp, and Bernt Arne Ødegaard. 2011. Stock Market Liquidity and the Business Cycle. The Journal of Finance 66: 139–76. [Google Scholar] [CrossRef]

- Nofsinger, John R. 2005. Social Mood and Financial Economics. Journal of Behavioral Finance 6: 144–60. [Google Scholar] [CrossRef]

- Olbryś, Joanna, and Michał Mursztyn. 2017. Measurement of Stock Market Liquidity Supported by an Algorithm Inferring the Initiator of a Trade. Operations Research and Decisions 27: 111–27. [Google Scholar] [CrossRef]

- Ramos, Henrique Pinto, and Marcelo Brutti Righi. 2020. Liquidity, Implied Volatility and Tail Risk: A Comparison of Liquidity Measures. International Review of Financial Analysis 69: 101463. [Google Scholar] [CrossRef]

- Ranaldo, Angelo. 2001. Intraday Market Liquidity on the Swiss Stock Exchange. Financial Markets and Portfolio Management 15: 309–27. [Google Scholar] [CrossRef]

- Sadka, Ronnie, and Anna Schrebina. 2007. Analyst Disagreement, Mispricing, and Liquidity. The Journal of Finance 62: 2367–403. [Google Scholar] [CrossRef]

- Salisu, Afees A., and Ahamuefula E. Ogbonna. 2021. The Return Volatility of Cryptocurrencies during the COVID-19 Pandemic: Assessing the News Effect. Global Finance Journal, 100641, in press. [Google Scholar] [CrossRef]

- Sarr, Abdourahmane, and Tonny Lybek. 2002. Measuring Liquidity in Financial Markets. Available online: https://www.imf.org/en/Publications/WP/Issues/2016/12/30/Measuring-Liquidity-in-Financial-Markets-16211 (accessed on 26 December 2021). IMF Working Paper. WP/02/232.

- Singh, Mahipal. 2011. Security Analysis with Investment and Portfolio Management. New Delhi: Gyan Publishing House. [Google Scholar]

- Stereńczak, Szymon. 2018. Stock Liquidity on the Warsaw Stock Exchange in the 21st Century: Time-Series and Cross-Sectional Dependencies. Zeszyty Naukowe Uniwersytetu Szczecińskiego Finanse Rynki Finansowe Ubezpieczenia 91: 281–92. [Google Scholar] [CrossRef][Green Version]

- Topcu, Mert, and Omer Serkan Gulal. 2020. The Impact of COVID-19 on Emerging Stock Markets. Finance Research Letters 36: 101691. [Google Scholar] [CrossRef]

- Tuszkiewicz, Marcin. 2022. Wpływ pandemii COVID-19 na płynność akcji notowanych na Giełdzie Papierów Wartościowych w Warszawie. Journal of Finance and Financial Law, in press. [Google Scholar]

- Weigerding, Michael, and Michael Hanke. 2018. Drivers of seasonal return patterns in German stocks. Business Research 11: 173–96. [Google Scholar] [CrossRef]

- Wilcoxon, Frank. 1945. Individual Comparisons by Ranking Methods. Biometrics Bulletin 1: 80–83. [Google Scholar] [CrossRef]

- World Health Organization. 2020. Media briefing on COVID-19—11 March 2020. Geneva: World Health Organization. [Google Scholar]

- Włosik, Katarzyna. 2017. Płynność Przy Wycenie Akcji Na Giełdzie Papierów Wartościowych w Warszawie. Ruch Prawniczy, Ekonomiczny i Socjologiczny 79: 127–41. [Google Scholar] [CrossRef][Green Version]

- Xu, Yuanyuan, Jian Li, Linjie Wang, and Chongguang Li. 2022. Liquidity of China’s agricultural futures market: Measurement and cross-market dependence. China Agricultural Economic Review, ahead-of-print. [Google Scholar]

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial Markets under the Global Pandemic of COVID-19. Finance Research Letters 36: 101528. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Data | Period 1 | Period 2 | Period 3 | |

|---|---|---|---|---|

| Value | First minute (M1) | 263,746,689.17 | 540,641,475.30 | 516,385,355.91 |

| First five minutes (M5) | 537,539,837.56 | 1,095,353,523.02 | 1,034,603,648.34 | |

| Continuous trading phase (CT) | 21,265,524,794.31 | 29,397,949,841.01 | 25,029,530,275.01 | |

| Trading-at-last (TL) | 3,374,133,211.27 | 4,515,754,203.99 | 3,304,741,228.59 | |

| Ratio | M1/CT | 1.24% | 1.84% | 2.06% |

| M5/CT | 2.53% | 3.73% | 4.13% | |

| TL/(CT+TL) | 13.69% | 13.32% | 11.66% | |

| Period 1 | Period 2 | Period 3 | |

|---|---|---|---|

| First minute (M1) | 56,708 | 112,297 | 100,957 |

| First five minutes (M5) | 90,590 | 194,716 | 182,308 |

| Continuous trading phase (CT) | 2,307,175 | 4,449,096 | 3,675,064 |

| Trading-at-last (TL) | 81,189 | 108,975 | 90,434 |

| M1/CT | 2.46% | 2.52% | 2.75% |

| M5/CT | 3.93% | 4.38% | 4.96% |

| TL/(CT+TL) | 3.40% | 2.39% | 2.40% |

| Period 1 | Period 2 | Period 3 | |

|---|---|---|---|

| First minute (M1) | 4650.96 | 4814.39 | 5114.90 |

| First five minutes (M5) | 5933.77 | 5625.39 | 5675.03 |

| Continuous trading phase (CT) | 9217.13 | 6607.62 | 6810.64 |

| Trading-at-last (TL) | 41,558.99 | 41,438.82 | 36,543.13 |

| Mean | Standard Deviation | |||||||

|---|---|---|---|---|---|---|---|---|

| Period 1–Period 3 | Period 1 | Period 2 | Period 3 | Period 1–Period 3 | Period 1 | Period 2 | Period 3 | |

| F5 | 5649 | 3020 | 6703 | 7069 | 10,054 | 5146 | 11,851 | 11,404 |

| CL | 1271 | 782 | 1548 | 1467 | 1901 | 979 | 2473 | 1927 |

| L5 | 2833 | 1988 | 3086 | 3362 | 4932 | 3407 | 5575 | 5499 |

| Period 1–Period 3 | Period 1 | Period 2 | Period 3 | |

|---|---|---|---|---|

| F5 | 2.68 | 2.77 | 2.52 | 2.74 |

| Cl | 1.52 | 1.43 | 1.55 | 1.56 |

| L5 | 1.81 | 1.8 | 1.93 | 1.71 |

| Chi-square | 67.935 | 28.467 | 13.724 | 27.941 |

| Period 1–Period 3 | Period 1 | Period 2 | Period 3 | |

|---|---|---|---|---|

| F5/L5 | −7.069 | −4.576 | −3.146 | −4.616 |

| CL/L5 | −3.473 | −2.047 * | −2.216 * | −1.633 ** |

| CL/F5 | −7.265 | −4.535 | −3.579 | −4.419 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kubiczek, J.; Tuszkiewicz, M. Intraday Patterns of Liquidity on the Warsaw Stock Exchange before and after the Outbreak of the COVID-19 Pandemic. Int. J. Financial Stud. 2022, 10, 13. https://doi.org/10.3390/ijfs10010013

Kubiczek J, Tuszkiewicz M. Intraday Patterns of Liquidity on the Warsaw Stock Exchange before and after the Outbreak of the COVID-19 Pandemic. International Journal of Financial Studies. 2022; 10(1):13. https://doi.org/10.3390/ijfs10010013

Chicago/Turabian StyleKubiczek, Jakub, and Marcin Tuszkiewicz. 2022. "Intraday Patterns of Liquidity on the Warsaw Stock Exchange before and after the Outbreak of the COVID-19 Pandemic" International Journal of Financial Studies 10, no. 1: 13. https://doi.org/10.3390/ijfs10010013

APA StyleKubiczek, J., & Tuszkiewicz, M. (2022). Intraday Patterns of Liquidity on the Warsaw Stock Exchange before and after the Outbreak of the COVID-19 Pandemic. International Journal of Financial Studies, 10(1), 13. https://doi.org/10.3390/ijfs10010013