Modeling Real Exchange Rate Persistence in Chile

Abstract

1. Introduction

2. Theoretical Framework

2.1. Parity Conditions

2.2. Persistence in the Data

2.3. Theory-Consistent CVAR Scenario Results

3. The CVAR Model and the Representation

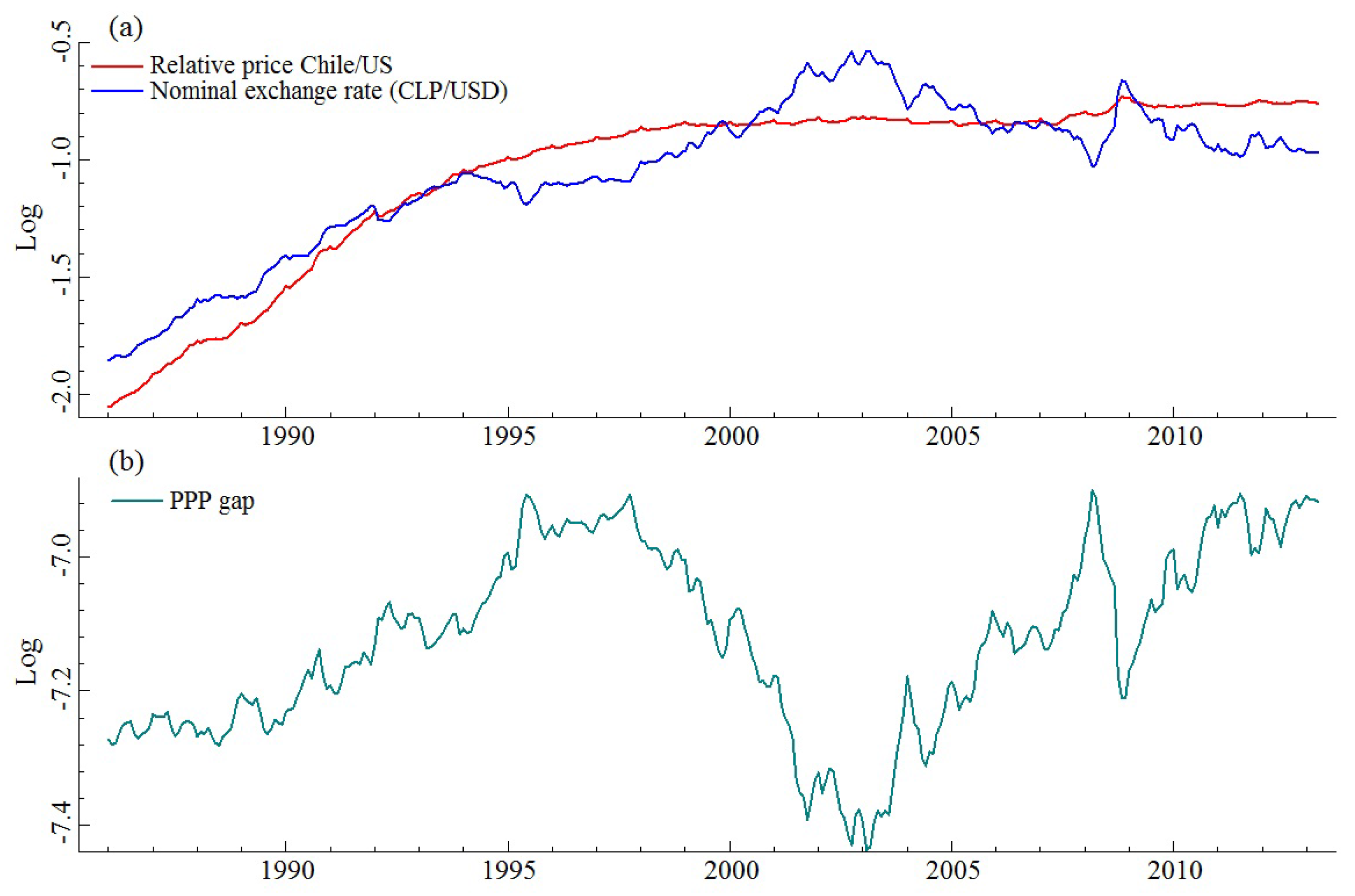

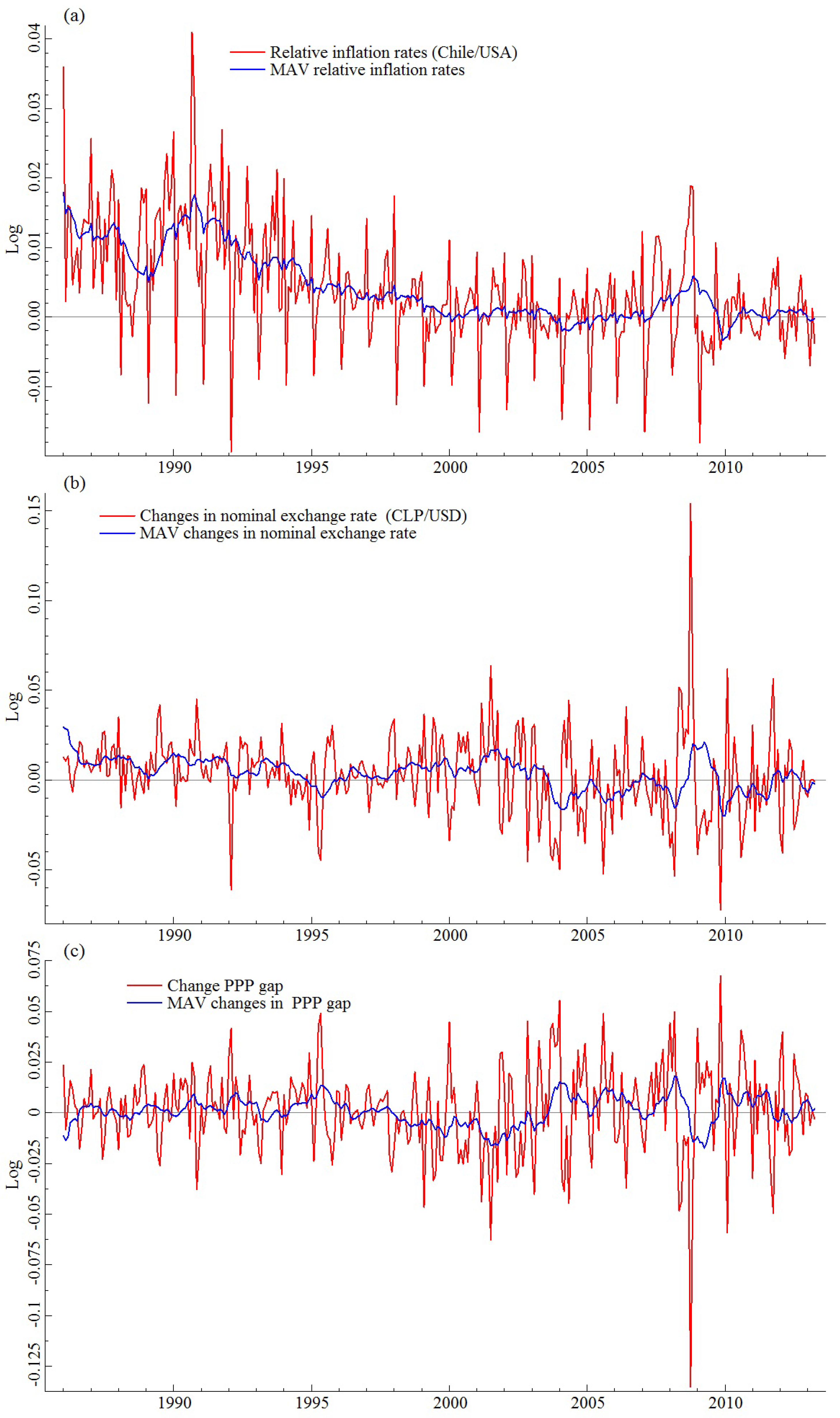

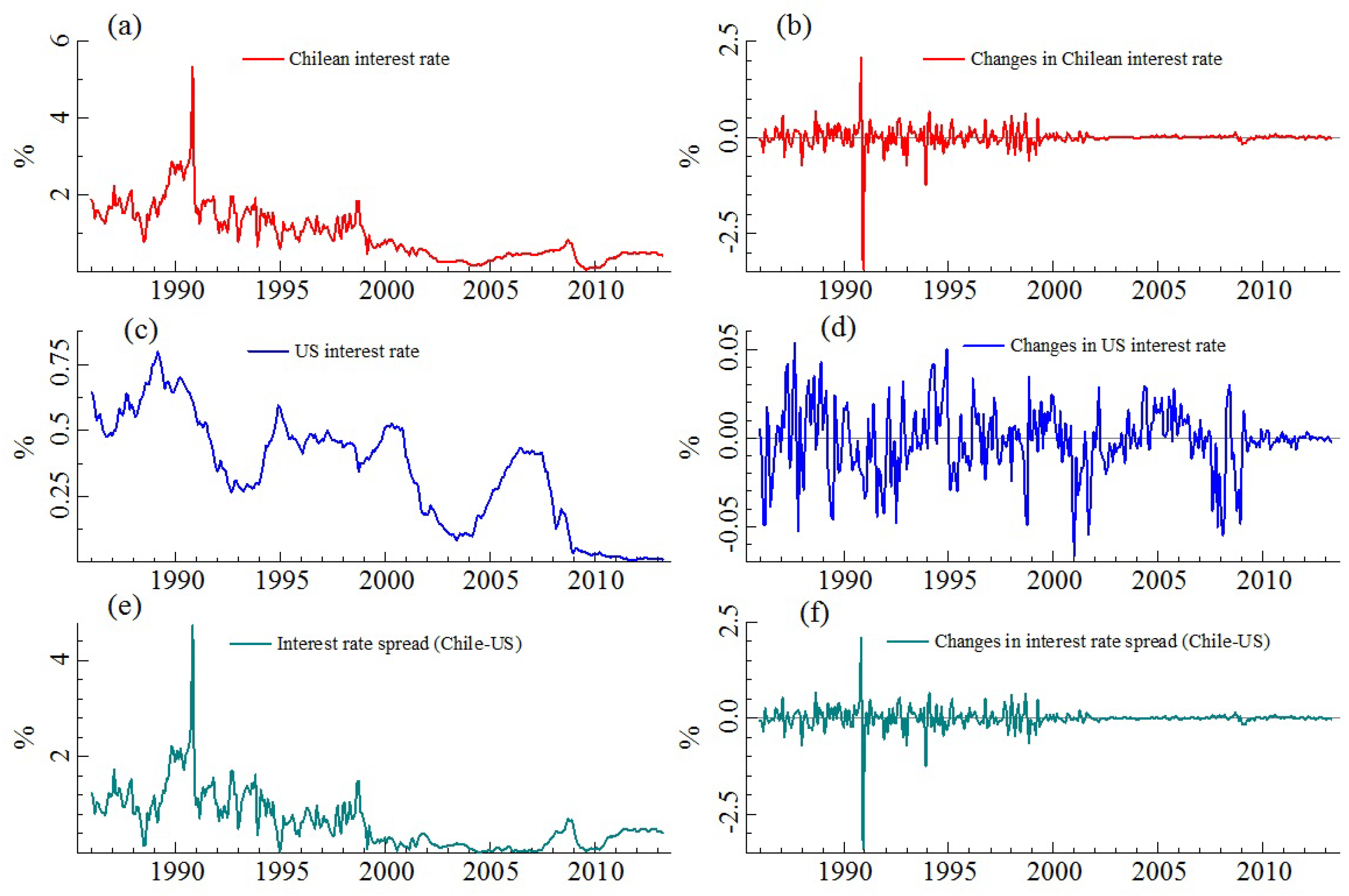

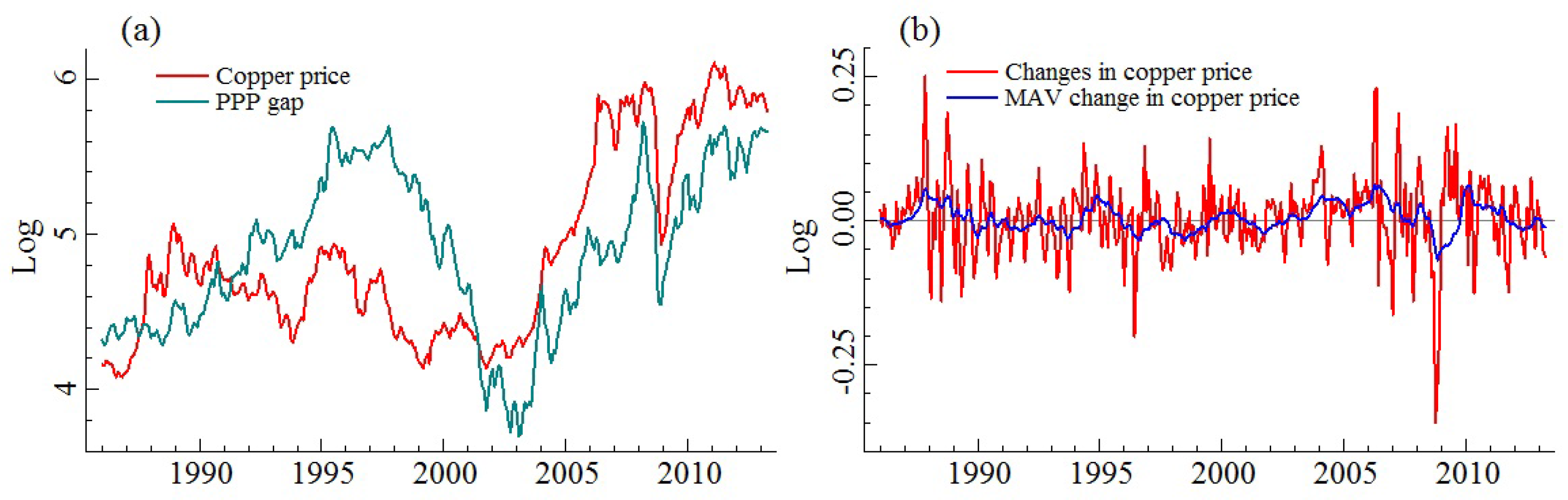

4. Stylized Facts

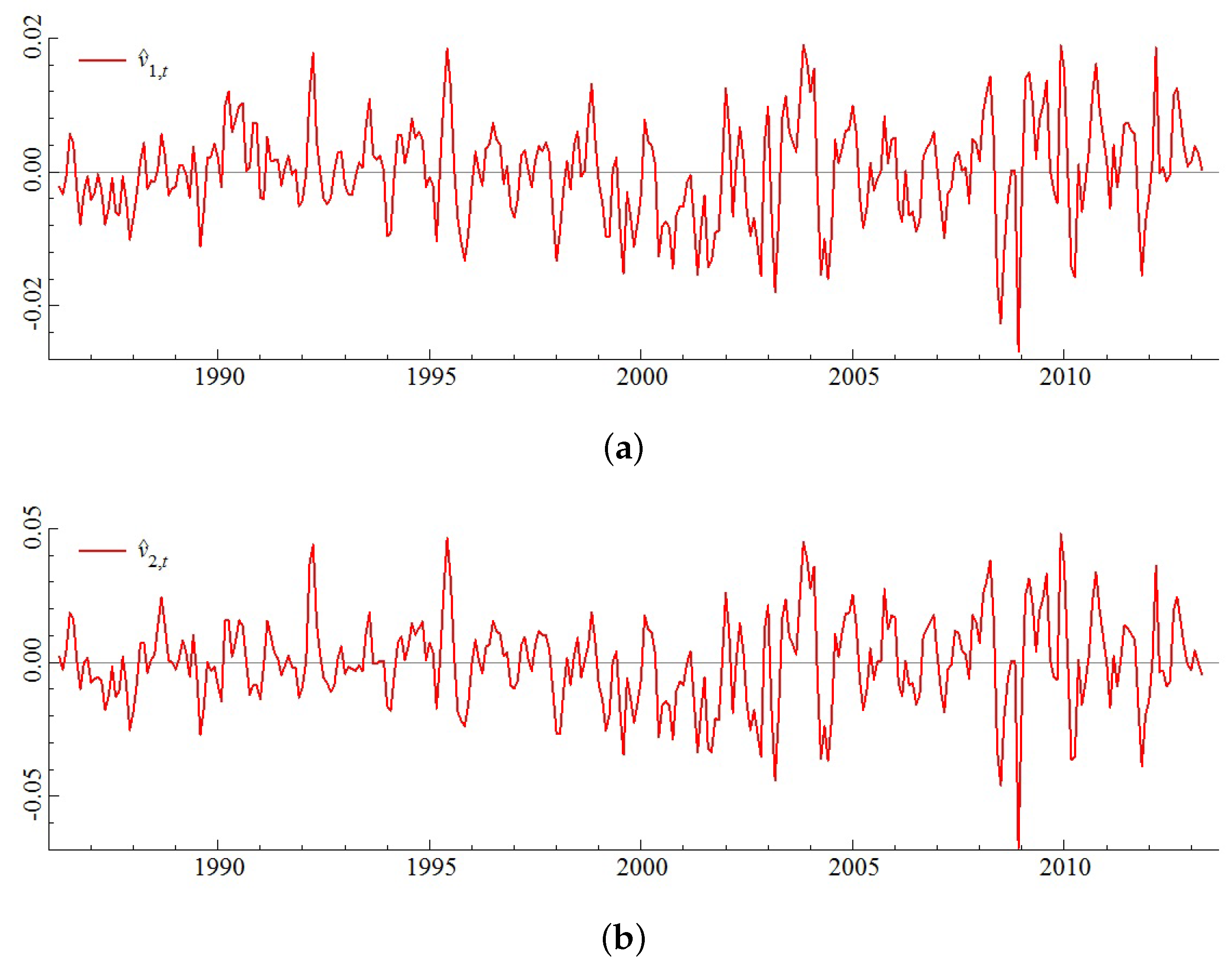

5. Empirical Model Analysis

5.1. Rank Determination

5.2. Partial System

5.2.1. Testing Non-Identifying Hypotheses in the Model

- Same restrictions on all

- A known vector in

5.2.2. Testing Identifying Restrictions on the Long-Run Structure

- If (given ), then is equilibrium error correcting to (medium run).

- If , then the acceleration rate is equilibrium error correcting to the polynomially cointegrated relation (long run).

5.2.3. The Common Stochastic Trends

6. Conclusions

Conflicts of Interest

Appendix A. Data

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Description | Source | Transformation |

|---|---|---|---|

| Chilean Consumer Price Index | Central Bank of Chile | Natural logarithm | |

| US Consumer Price Index | Bureau of Labor Statistics, United States | Natural logarithm | |

| Nominal exchange rate (Chilean pesos per US dollar) | Central Bank of Chile | Natural logarithm | |

| 1-year Chilean average weighted rates of all transactions in the month by financial commercial banks in Chilean pesos (nominal). Nominal interest rates are annualized (base 360 days) using the conversion of simple interest. | Own elaboration based on data from the Central Bank of Chile | The original variable was divided by 1200 to make it comparable with monthly data | |

| United States interest rate, Constant Maturity Yields, 1 Year, Average, USD | Own elaboration based on data from the International Monetary Fund | The original variable was divided by 1200 to make it comparable with monthly data | |

| Real copper price (USD cents./lb.) | Comisión Chilena del Cobre | Natural logarithm |

Appendix B. Lag-Length Selection

| Lag-Length Selection | ||||

| Lag: | SC | H-Q | LM(1) | LM() |

| 4 | 0.34 | 0.52 | ||

| 3 | 0.13 | 0.38 | ||

| 2 | 0.05 | 0.04 | ||

| 1 | 0.00 | 0.00 | ||

| Lag Reduction | ||||

| Reduction from - to | Test | p-Value | ||

| VAR(4) - VAR(3) | 0.24 | |||

| VAR (3) - VAR(2) | 0.00 | |||

| VAR(2)-VAR(1) | 0.00 | |||

Appendix C. Dummy Variables

| Dummy | Variable | Justification |

|---|---|---|

| P 1990:9 | The Central Bank of Chile started the partial implementation of an inflation targeting system | |

| T 1990:11 | INA | |

| P 1993:12 | INA | |

| P 1998:9 | Central Bank of Chile increased the real monetary policy interest rate from 8.5% to 14% | |

| P 2005:9 | Energy costs increased sharply. Overall, the index for energy commodities (petroleum-based energy) | |

| P 2006:04 | The copper price increased in 30% in April triggered by the lower inventories and higher demand | |

| P 2008:10 | The energy index fell 8.6% and the transportation index fell in 5.4% in October . The nominal exchange rate depreciated 12% due to the dollar strengthening in international markets | |

| P 2008:11 | The overall CPI index decreased mainly due to a decrease in energy prices, particularly gasoline. | |

| P 2010:2 | The nominal exchange rate depreciated due to changes in the forward position of the pension funds |

| Dummy | ||||||

|---|---|---|---|---|---|---|

| P 1990:9 | * | * | * | * | * | |

| T 1990:11 | * | * | * | * | * | |

| P 1993:12 | * | * | * | * | * | |

| P 1998:9 | * | * | * | * | * | |

| P 2005:9 | * | * | * | * | * | |

| P 2006:4 | * | * | * | * | * | |

| P 2008:10 | * | * | * | |||

| P 2008:11 | * | * | * | * | * | |

| P 2010:2 | * | * | * | * |

References

- Bacchiocchi, Emanuele, and Luca Fanelli. 2005. Testing the PPP through I (2) cointegration techniques. Journal of Applied Econometrics 20: 749–70. [Google Scholar] [CrossRef]

- Céspedes, Luis.F., and José De Gregorio. 1999. Tipo de cambio real, desalineamiento y devaluaciones: teoría y evidencia para Chile. Unpublished paper. Santiago, Chile: University of Chile, March. [Google Scholar]

- Cowan, Kevin, David Rappoport, and Jorge Selaive. 2007. High Frequency Dynamics of the Exchange Rate in Chile. Santiago: Central Bank of Chile. [Google Scholar]

- De Gregorio, José, and Felipe Labbé. 2011. Copper, the Real Exchange Rate and Macroeconomic Fluctuations In Chile. Santiago: Central Bank of Chile. [Google Scholar]

- Délano, Valentín, and Rodrigo Valdés. 1998. Productividad y Tipo Cambio Real en Chile. Central Bank of Chile Working Paper 38: 1–19. [Google Scholar]

- Diamandis, Panayiotis F. 2003. Market efficiency, purchasing power parity, and the official and parallel markets for foreign currency in Latin America. International Review of Economics & Finance 12: 89–110. [Google Scholar]

- Doornik, Jurgen A., and Katarina Juselius. 2017. Cointegration Analysis of Time Series Using CATS 3 for OxMetrics. London: Timerlake Consultants Ltd. [Google Scholar]

- Duncan, Roberto, and César Calderón. 2003. Purchasing Power Parity in an Emerging Market Economy: A Long-Span Study for Chile. Estudios de Economía 30: 103–132. [Google Scholar]

- Erten, Bilge, and José Antonio Ocampo. 2013. Super cycles of commodity prices since the mid-nineteenth century. World Development 44: 14–30. [Google Scholar] [CrossRef]

- Froot, Kenneth A., and Kenneth Rogoff. 1995. Perspectives on PPP and long-run real exchange rates. In Handbook of International Economics. Amsterdam: Elsevier, Volume 3, pp. 1647–88. [Google Scholar]

- Frydman, Roman, and Michael D. Goldberg. 2011. Beyond Mechanical Markets: Asset Price Swings, Risk, and The Role of the State. Princeton: Princeton University Press. [Google Scholar]

- Frydman, Roman, and Michael D. Goldberg. 2007. Imperfect Knowledge Economics: Exchange Rates and Risk. Princeton: Princeton University Press. [Google Scholar]

- Gonzalo, Jesus. 1994. Five alternative methods of estimating long-run equilibrium relationships. Journal of Econometrics 60: 203–33. [Google Scholar] [CrossRef]

- Johansen, Søren. 1992. A representation of vector autoregressive processes integrated of order 2. Econometric Theory 8: 188–202. [Google Scholar] [CrossRef]

- Johansen, Søren. 1995. A statistical analysis of cointegration for I(2) variables. Econometric Theory 11: 25–59. [Google Scholar] [CrossRef]

- Johansen, Søren. 1996. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press. [Google Scholar]

- Johansen, Søren. 1997. Likelihood analysis of the I(2) model. Scandinavian Journal of Statistics 24: 433–62. [Google Scholar] [CrossRef]

- Johansen, Søren. 2006. Statistical analysis of hypotheses on the cointegrating relations in the I(2) model. Journal of Econometrics 132: 81–115. [Google Scholar] [CrossRef]

- Johansen, Søren, Katarina Juselius, Roman Frydman, and Michael Goldberg. 2010. Testing hypotheses in an I(2) model with piecewise linear trends. An analysis of the persistent long swings in the Dmk/$ rate. Journal of Econometrics 158: 117–29. [Google Scholar] [CrossRef]

- Juselius, Katarina. 2006. The Cointegrated VAR Model: Methodology and Applications. Oxford: Oxford University Press. [Google Scholar]

- Juselius, Katarina. 2010. Imperfect Knowledge, Asset Price Swings and Structural Slumps: A Cointegrated VAR Analysis of Their Interdependence. Technical Report. Copenhagen: Department of Economics, University of Copenhagen. [Google Scholar]

- Juselius, Katarina. 2014. Testing for Near I(2) Trends When the Signal-to-Noise Ratio Is Small. Economics: The Open-Access, Open-Assessment E-Journal 8: 2014-21. [Google Scholar] [CrossRef]

- Juselius, Katarina. 2017a. Using a Theory-Consistent CVAR Scenario to Test an Exchange Rate Model Based on Imperfect Knowledge. Unpublished manuscript. Copenhagen, Denmark: Department of Economics, University of Copenhagen. [Google Scholar]

- Juselius, Katarina. 2017b. A Theory Consistent CVAR Scenario for a Standard Monetary Model Using Data-Generated Expectaions. Unpublished manuscript. Copenhagen, Denmark: Department of Economics, University of Copenhagen. [Google Scholar]

- Juselius, Katarina, and Katrin Assenmacher. 2017. Real exchange rate persistence and the excess return puzzle: The case of Switzerland versus the US. Journal of Applied Econometrics. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica 47: 263–91. [Google Scholar] [CrossRef]

- Kohlscheen, Emanuel, Fernando Avalos, and Andreas Schrimpf. 2017. When the Walk Is Not Random: Commodity Prices and Exchange Rates. International Journal of Central Banking, June. [Google Scholar] [CrossRef][Green Version]

- Kongsted, Hans Christian. 2005. Testing the nominal-to-real transformation. Journal of Econometrics 124: 205–25. [Google Scholar] [CrossRef]

- Krugman, Paul R., Maurice Obstfeld, and Marc Melitz. 2011. International Economics: Theory and Policy, 9th ed. Boston: Addison-Wesley. [Google Scholar]

- Mark, Nelson C. 2001. International Macroeconomics and Finance: Theory and Econometric Methods, 1st ed. Malden: Wiley-Blackwell. [Google Scholar]

- Medina, Juan Pablo, and Claudio Soto. 2007. Copper Price, Fiscal Policy and Business Cycle in Chile. Documentos de Trabajo. Santiago: Banco Central de Chile, p. 1. [Google Scholar]

- Phelps, Edmund S. 1994. Structural Slumps: The Modern Equilibrium Theory of Unemployment, Interest, and Assets. Harvard: Harvard University Press. [Google Scholar]

- Rahbek, Anders, Hans Christian Kongsted, and Clara Jørgensen. 1999. Trend stationarity in the I(2) cointegration model. Journal of Econometrics 90: 265–89. [Google Scholar] [CrossRef]

- Sarno, Lucio, and Mark P. Taylor. 2002. The Economics of Exchange Rates. Cambridge: Cambridge University Press. [Google Scholar]

- Tabor, Morten Nyboe. 2014. Essays on Imperfect Knowledge Economics, Structural Change, And Persistence in the Cointegrated VAR Model. Ph.D. thesis, University of Copenhagen, Copenhagen, Denmark. [Google Scholar]

- Taylor, Alan M., and Mark P. Taylor. 2004. The Purchasing Power Parity Debate. Journal of Economic Perspectives 18: 135–58. [Google Scholar] [CrossRef]

- Wu, Yi. 2013. What Explains Movements in the Peso/Dollar Exchange Rate? IMF Working papers No. 13/171. Washington, DC, USA: International Monetary Fund. [Google Scholar]

| 1 | This concept is known as absolute PPP. |

| 2 | A CVAR scenario tests the empirical consistency of the basic underlying assumptions of a model rather than imposing them on the data from the outset (Juselius 2017a). |

| 3 | Duncan and Calderón (2003), and Froot and Rogoff (1995) present a thorough review of the literature on PPP testing. |

| 4 | In empirical testing, the PPP condition is normally replaced by , where is expected. |

| 5 | The real exchange rate is defined as . It corresponds to the ratio of the foreign price level and the domestic price level, once the foreign price has been converted to the domestic currency through the nominal exchange rate. |

| 6 | If deviations from PPP are assumed to be near , the deviations from UIP also behave as nonstationary, near- processes. |

| 7 | This subsection is based mainly on Juselius (2017a), Juselius and Assenmacher (2017), and Frydman and Goldberg (2007, 2011). |

| 8 | This assumption is based on simulations that show that has to be extremely large for to have a marked effect on . Frydman and Goldberg (2007) use this assumption (“conservative revision”) in their IKE-based monetary model to illustrate the fact that forecasting behavior is led by new realizations of the causal variables, , rather than revision of forecasting strategies, . |

| 9 | This is consistent with the FG IKE-based model developed by Frydman and Goldberg (2007), which assumes that individuals recognize their imperfect knowledge about the underlying processes that drive outcomes. Thus, they use a multitude of forecasting strategies that are revised over time in a way that cannot be fully prespecified. Indeed, given the diversity of forecasting strategies, this model assumes two kinds of individuals in the foreign currency market: bulls, who speculate on the belief that the asset price will rise, and bears, who speculate on its fall. |

| 10 | When periods where is far from its benchmark value are shorter compared with the near vicinity periods, it describes a persistent but mean-reverting process. |

| 11 | Frydman and Goldberg (2007) extend the concept of loss aversion given by Kahneman and Tversky (1979) to the concept of endogenous loss aversion, which says that the greater the potential loss, the higher the degree of loss aversion. This definition establishes that the UA-UIP equilibrium exists. |

| 12 | |

| 13 | From the MA representation (23), it follows that the unrestricted constant, , cumulates once to a linear trend and twice to a quadratic trend. In addition, the unrestricted trend, , cumulates once to a quadratic trend and twice to a cubic trend. To avoid the latter, quadratic and cubic trends have been restricted to zero in the subsequent analysis. For further information, see Chapter 17 in Juselius (2006). |

| 14 | The distribution of the this is found in Johansen (1995) provided that model (22) does not restrict deterministic components; otherwise see Rahbek et al. (1999). |

| 15 | Appendix B presents the selection of the number of lags. |

| 16 | Appendix A presents the source, description, and transformation of the data. Dataset and code to replicate the results are available from the author. |

| 17 | Appendix C specifies the intervention dummies and their estimated coefficients. |

| 18 | Initially, the cointegration space considered a broken linear trend that started in September 1999, corresponding to the beginning of the floating exchange rate regime in Chile. However, this broken linear trend was revealed to be non-significant. The potential effect of the new regime on the nominal exchange rate was, possibly, offset by changes in the Chilean inflation rate and/or interest rate. |

| 19 | For a thorough description of the tests see Doornik and Juselius (2017). |

| 20 | The hypothesis was rejected in all cases, except for the Chilean interest rate based on with a p-value of 0.06 and for the interest rate spread based on with a p-value of 0.23. Thus, the hypotheses and are not presented because the distribution of the test is not necessarily . |

| 21 | The estimated long-run structure is identified. That is, restrictions were imposed, at least, on each of the vectors. See Doornik and Juselius (2017) for further information. |

| 22 |

| Multivariate Specification Tests | ||||||

|---|---|---|---|---|---|---|

| Autocorrelation | Normality | ARCH | ||||

| Order 1: | Order 2: | Order 1: | Order 2: | |||

| Univariate Specification Tests | ||||||

| Equation | ||||||

| ARCH Order 2: | ||||||

| Normality | ||||||

| Skewness | 0.23 | 0.07 | 0.03 | 0.02 | ||

| Kurtosis | 3.99 | 4.12 | 3.98 | 4.81 | 4.87 | 3.60 |

| S.E. | 4.38 | 1.96 | 16.68 | 52.17 | 1.51 | 0.15 |

| r | ||||||||

|---|---|---|---|---|---|---|---|---|

| 6 | 0 | |||||||

| 5 | 1 | |||||||

| 4 | 2 | |||||||

| 3 | 3 | |||||||

| 2 | 4 | |||||||

| 1 | 5 |

| Seven Largest Characteristic Roots | |||||||

|---|---|---|---|---|---|---|---|

| Model | Moduli | ||||||

| 0.98 | 0.98 | 0.98 | 0.95 | 0.95 | 0.82 | 0.56 | |

| 1.00 | 1.00 | 1.00 | 1.00 | 0.98 | 0.82 | 0.56 | |

| 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 0.56 | |

| Hypothesis | Matrix Restriction Design | Distribution | p-Value |

|---|---|---|---|

| PPP restriction | 0.00 | ||

| Price homogeneity | 0.00 | ||

| Excludable trend | 0.00 | ||

| Chilean price | 0.00 | ||

| US price | 0.00 | ||

| Relative price | 0.00 | ||

| Nominal exchange rate | 0.00 | ||

| PPP gap | 0.11 | ||

| US interest rate | 0.01 | ||

| Copper price | 0.00 |

| c | ||||||||

|---|---|---|---|---|---|---|---|---|

| 1.00 | - | |||||||

| - | - | - | ||||||

| - | 1.00 | - | ||||||

| - |

© 2017 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Salazar, L. Modeling Real Exchange Rate Persistence in Chile. Econometrics 2017, 5, 29. https://doi.org/10.3390/econometrics5030029

Salazar L. Modeling Real Exchange Rate Persistence in Chile. Econometrics. 2017; 5(3):29. https://doi.org/10.3390/econometrics5030029

Chicago/Turabian StyleSalazar, Leonardo. 2017. "Modeling Real Exchange Rate Persistence in Chile" Econometrics 5, no. 3: 29. https://doi.org/10.3390/econometrics5030029

APA StyleSalazar, L. (2017). Modeling Real Exchange Rate Persistence in Chile. Econometrics, 5(3), 29. https://doi.org/10.3390/econometrics5030029