Abstract

The global spread and use of the internet and mobile phones has contributed to the development of digital payments. Despite its growth potential, until now there is a lack of research providing a comprehensive synthesis and analysis of factors affecting the use, adoption, and acceptance of digital payment methods. This study aims to address this gap by providing a comprehensive review of the related literature retrieved from Scopus and Web of Science databases. Following a systematic method, a final sample of 193 research articles was identified and analysed. The results highlight that a single theory has failed to comprehensively explain the complex nature of electronic payment adoption. The key limitation of the existing theories is their inability to consider the role of social and cultural facets in the adoption of new technology. While literature reviews are a widespread practice in business studies, there are scant reviews that use the systematic review methodology that aggregates knowledge using clearly defined processes and criteria. This is the first systematic review on electronic payment adoption, which structures the existing knowledge and provides directions for future research.

1. Introduction

The omnipresent penetration of mobile devices, along with unambiguous developments in wireless telecommunication, has fueled widespread adoption of mobile technology and a significant boost to e-commerce, mainly e-commerce through mobile devices or mobile commerce. This expansion was followed by the introduction of new payment methods, such as digital payment, which refers to the use of wireless communication technology and electronic gadgets to make the purchase of products and services more convenient. Digital payment may benefit both companies and customers by offering quick, secure, and easy ways of completing financial transactions.

In the past few years, many corporations have been focusing on introducing more e-payment services, as enterprises involved in payment and communication technologies attempt to solve people’s everyday challenges and perceive it as a viable economic opportunity. Additionally, the exponential development of wireless communications and technology has revolutionised today’s world commerce activities. Customers can now carry out a wide variety of tasks, including mobile payments (m-payment), which is the purchase of goods and services using proximity payments at the point of sale. Mobile services provide customers with benefits such as flexibility, mobility, and efficiency, making it easier to live a stress-free life. However, m-payment is underutilised in several countries, like Malaysia, Singapore, India, and China, because people prefer to pay for products and services using cash [1,2,3]. The low or slow uptake of digital payment technologies can be attributed to security concerns, privacy, usage barriers, and value barriers [2,4,5]. For instance, Yang et al. [6] reported that consumers find it harder to assert their rights due to regulatory gaps in privacy protection in mobile commerce. Consequently, regulatory uncertainty around mobile payments raises customer privacy and financial concerns.

A growing number of studies has been published in recent years on digital payments because of the rapid expansion of e-banking and payment systems, as well as the complexities of the factors that influence their use and adoption. Previous studies demonstrate that a significant number of these publications have looked at factors that influence the outcome, customer acceptance and adoption of digital payment, such as stakeholders’ expectations [7], cultural orientation differences [8], customer satisfaction [9], security and privacy risk [10,11,12], design attributes [13], and innovation [14,15]. Despite the growing number of publications on digital payments, there is little peer-reviewed literature about their impact and determinants. Dahlberg et al. [16] suggested that there is still a need to conduct an extensive literature review and provide suggestions for future research on developed nations. Furthermore, Dahlberg et al. [17] mentioned that the field had experienced a rise in publications, yet it still missing a thorough review of existing work. The existing studies, such as that by Taylor [18], was limited to mobile payment in retail sectors. Similarly, Alkhowaiter [19] limited their review to the banking adoption research in Gulf countries.

The field’s recent expansion provides several opportunities to look back and reflect on how to advance the field forward. Moreover, the unprecedented Coronavirus disease (COVID-19) crisis has brought about radical changes in our daily lives—from how we interact, work, and study, to our mobility and use of space and time [20]. Many of these transformations were anchored in state-of-the-art technologies including digital payment activities, which generate a new opportunity for our research community to study technology-related behavior in the global crisis [21]. It is suggested that the crisis seems to deepen the profound impact of technology in shaping our lives.

With regard to payment behaviour of individuals, the COVID-19 and related lockdown measures of social distancing have contributed to a substantial change in the payment behaviour of customers. Kraenzlin et al. [22] reported empirical evidence of a significant drop in the retail card payments and such a crisis highlights the need to facilitate and secure the settlement of electronic payments. It can be concluded that COVID-19 shed lights on the importance of the external environment of digital payment adoption behaviour of individuals, which required more work in the future.

So far, the research appears to be fractured and lacks a roadmap or agenda. Hence, this paper aims to summarise findings from previous mobile payment studies and identify possible research topics for the future. According to Dahlberg et al. [17], the adoption elements may be explored in depth in order to develop more specific recommendations that mobile payment service providers and researchers can use. Reviewing existing literature provides a clearer understanding of the current state of research in the area and identifies patterns in the development of the field itself. Finally, a review of past papers saves researchers from repeating work and reveals important gaps in the field. In other words, it draws a line across regions where there is already a plethora of studies while revealing areas where there is a dearth of research, which may be regarded as another contribution of the current literature review.

This study, therefore, followed a systematic methodology to identify the sample literature included in the content analysis. A final sample of 193 research articles published in Scopus and Web of Science were identified. Following several review studies [23,24,25], the sample literature was investigated by concentrating on the annual trend of research, important studies, geographical distribution, theoretical basis, methodology and modelling, and theme analysis. Researchers discovered that there had been considerable interest in studying the adoption of e-payments in recent years, but these studies are still limited. Very few studies have been conducted on the antecedents of switching behaviour, actual use, continuous use, recommended intention, and satisfaction of customers (post-adoption behaviour).

Furthermore, it is widely confirmed that the technology acceptance model (TAM) alone does not explain the complex nature of customer intention. Therefore, several studies have focused mainly on the TAM, with additional constructs adapted from mobile payment research, including cost, trust, and mobility. Nevertheless, most of the theories applied in the sample (i.e., Unified Theory of Acceptance and Use of Technology model) have limitations. The most significant limitation is being unable to consider cultural factors when studying the adoption of new technology. Because of these constraints, there is a pressing need for additional theoretical advancement in this area.

This study contributes to the existing knowledge by presenting a comprehensive and in-depth look at the current studies on electronic payments. It also provides a review of the research landscape in the area of the pre- and post-adoption of e-payments that presents interesting insights and directions for future research and contribute to the theoretical development of consumer behaviour research, which would assist researchers in discovering potential research possibilities and identifying the most important research topics in the current literature. As the first comprehensive content analysis in this field, this research differentiates itself from previous reviews by offering a supplementary method to the more traditional literature review.

The rest of the article is organised as follows: Section 2 presents the methodology and research strategy applied in the current research. Section 3 introduces the SLR findings. Section 4 discusses the gaps identified in the previous literature and future research avenues. Section 5 concludes the study.

2. Methodology

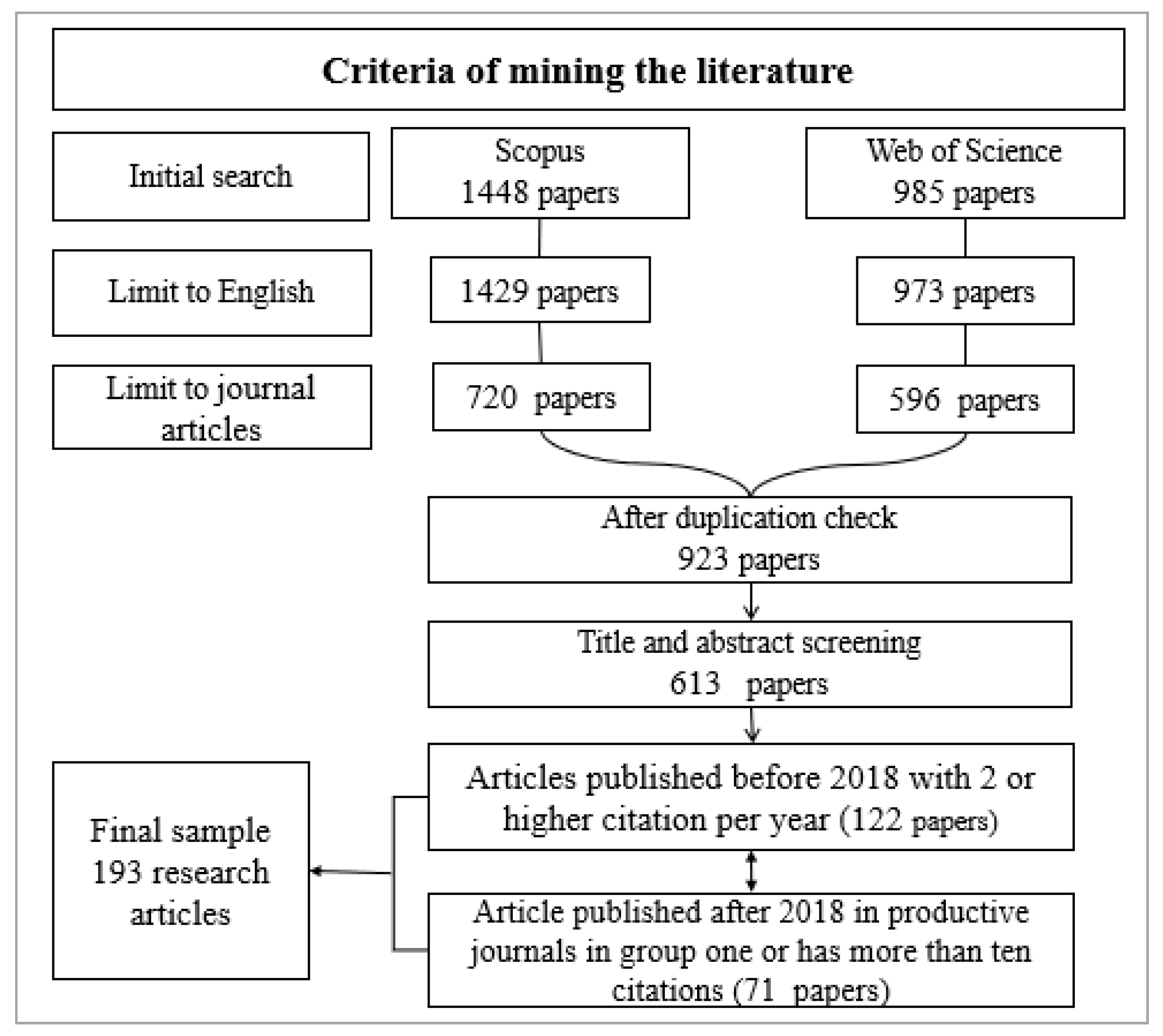

In the business research field, the literature review tool is the most popular and widespread. The literature review provides researchers with useful results to identify possible research trends and essential research insights for both junior and academic researchers interested in conducting further work and highlights the related questions that need to be answered in future investigations [23,24,25,26,27,28]. For this reason, this study followed a systematic methodology in identifying the sample literature included in the content analysis. The data were collected from the Scopus and Web of Science (WoS) databases. To determine the relevant research articles, several keywords were used to search the literature, including (“Digital Payment*” OR “Mobile Payment*” OR “Mobile wallet*” OR “MPayment*” OR “Electronic Payment*” OR “Virtual Payment*” OR “Virtual Payment*” OR “Cashless payment*” OR “ePayment*” OR “e-Payment*” AND customer* OR consumer*). This search string was developed after reviewing similar studies [18,19] and was searched in the documents’ title, abstract, and keywords. Keywords of research were operationalized through three keyword clouds, namely, digital payment and customer perspective. Target articles needed to match at least one word in each cloud. This review does not claim to cover all publications primarily dealing with the concept of digital payment and only focuses on the customer perspective.

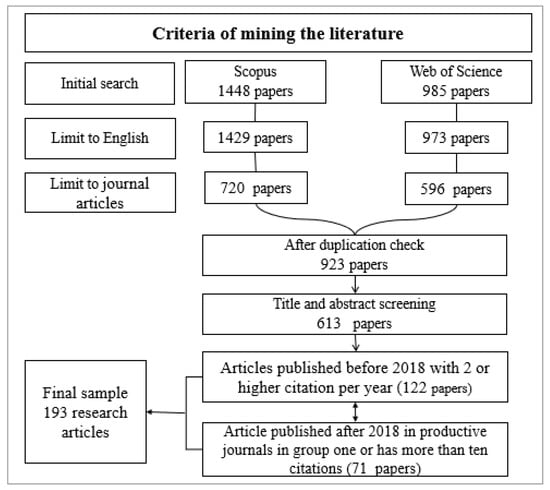

As shown in Figure 1, the initial sample using the search string hit several 2433 research articles from both databases. We then limited the search to articles published in the English language, which resulted in 2402 documents. By narrowing the scope of the study to papers that have been published in peer-reviewed journals, the total number of articles was decreased even further to 1316 (720 from Scopus and 596 from WoS). Next, 393 duplicated studies were removed, which resulted in 923 unique studies from both databases. After that, studies that did not explicitly discuss the customer aspect of digital payments have been excluded after screening the abstract and the full content of the sample literature. This process has resulted in a final sample of 613 studies that were supposed to be included in this investigation.

Figure 1.

The flow chart of the data collection.

This step carried out a standardised data extraction process to reduce author subjectivity in reducing the sample literature to focus on the most influential studies. We employed a citation search to identify the publications that have influenced the field. Given that the time of publication plays a vital role in attracting readers where old publications might have more citations compared to the recent ones, the sample literature was divided into two groups, old publications (before 2018) and recent publications (2019–2021). Articles from old publications have to achieve a minimum citation requirement of at least two citations a year on average in order to pass the quality test. The total number of studies included in this category was 122. Recently published papers were required to have a minimum of 10 citations to pass the quality test and/or have been published in one of the leading journals in the field (see Table A1), as newly published articles have not yet had enough time to collect citations. These top journals published more than 60% of the articles before 2018. The final sample in the group was 71 research articles. Following several review studies [23,24,25], we analyse the sample literature by focusing on the research yearly trend, influential studies, regional distribution, theoretical background, methodology and modelling, and thematic analysis.

3. Results

We followed the approach used by several studies and focused on the evaluation of seven areas: research questions, modelling, data geography, theories, research methods, journal outlets, and concepts under study [23,24,25,29]. These themes were chosen because they proved the ability to facilitate completely exhaustive reviews and their common exclusivity. To address these themes, we first analyse the year frequency of the publication, research methodology, questions, and data geography. Second, we provided a more comprehensive assessment by reviewing theories, models, and concepts under the study of the sample literature.

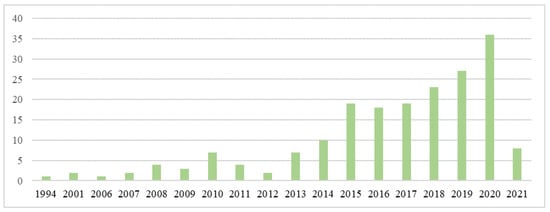

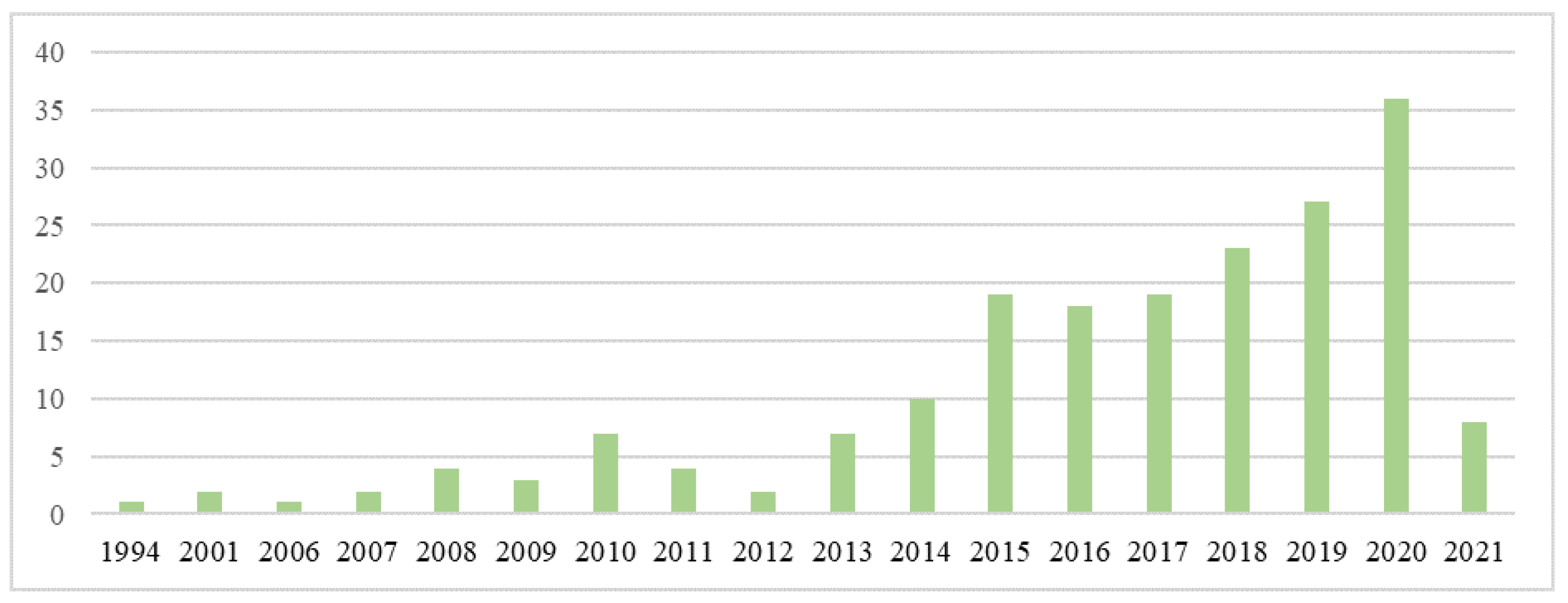

In terms of the publication trend, the earliest research papers identified in the sample literature were dated as early as 1994. After that, there was no research until the year 2001. Between 2001 and 2014, the number of publications remained less than seven studies per year. Since then, there has been a substantial increase in the number of scientific articles on customer digital payments (see Figure 2). This might be because of the exponential development of communication and the advances in mobile network technologies that have revolutionised today’s world, where an individual can now conduct many activities, such as a mobile payments, that provides convenience in terms of mobility and ease of use at any time and situation.

Figure 2.

Publications per year.

In this narrative analysis of the electronic payment literature, scholars [30,31,32,33,34] convincingly highlighted several significant gaps in the literature: (a) a scarcity of widely recognised theoretical frameworks and the growth of theory; (b) ineffective, and a wide variety of approaches were employed to operationalise the construct; (c) a lack of generalised findings in the prior studies, and (d) definitional consensus. The data were synthesised and analysed with these three fundamental issues in mind. The three issues will serve as a guide for the rest of the paper’s discussion.

3.1. Theories Applied in the Literature

As shown in Table 1, the most frequently used theoretical perspective is the technology acceptance model (TAM) (62 papers), followed by the unified theory of acceptance and use of technology (UTAUT) (44 papers), the innovation diffusion theory (IDT) (43 papers), and the unified theory of acceptance and use of technology two (UTAUT2) (44 papers) (30 papers).

Table 1.

Theoretical perspective in prior studies.

Prior research specifically utilised 65 different theories, with each article using just one of the 33 theoretical perspectives. There are eighteen theoretical views that exist in at least two publications, whereas seventeen articles make no clear reference to a theoretical foundation. Taken together, our results parallel previous findings which have emphasised the prevalence of TAM, UTAUT, and IDT [35]. However, the majority of the applied theories in the sample (i.e., the UTAUT and UTAUT2 models) have restrictions. Their primary issue is their failure to account for the cultural factors that influence the acceptance of new technologies. Due to these constraints, further theoretical development is required.

3.1.1. Technology Acceptance Model (TAM)

The TAM has been one of the most cited theoretical frameworks to study the adoption of a wide variety of technologies [36,37,38]. Davis [39] developed the TAM, which enables experts and researchers to assess user intention and understand the reasons behind the rejection or purchase of a product or service [40]. TAM also explains the interrelationship between the simplicity of use, perceived usefulness, attitude, and adoption intention of individuals, and various researchers have extensively tested it in the field of information technology (IT). Meanwhile, the TAM model has been tested in a number of settings to forecast the adoption of information technology-enabled innovations, and the model’s results have been proven to be genuinely accurate in terms of human attitudes. However, it has been widely confirmed that TAM alone does not explain the complex nature of customer intention. As a consequence, many researchers have mainly focused on the TAM with more constructs adapted from mobile payment studies, such as pricing, reliability, mobility, expressiveness, suitability, transaction speed, usage situation, social reference groups, enabling conditions, appealingness, and technological anxiety.

3.1.2. The Unified Theory of Acceptance and Use of Technology (UTAUT)

UTAUT is the second most theoretical perspective used in our sample, and it postulates four key elements as determinants of use willingness with technology adoption: Expectations about performance, effort, social influence, and facilitating conditions [41]. Among various theories/models, research indicates that the UTAUT elucidates the variations in behavioural intention to use a technology [42,43]. Many academics have experimentally verified the UTAUT model, which has several antecedents in a number of nations and cultures. However, it has been revealed that this UTAUT model and its determinants do explain approximately 70% of the variance in the behavioural intentions of users, as this model was originally created within an organisational context to justify employees’ adaption of technology. Therefore, most of the studies extend it by incorporating the self-efficacy and attitude constructs from the TAM.

3.1.3. Innovation Diffusion Theory (IDT)

Inventive Disruptive Technology (IDT) is a transdisciplinary theory developed by Rogers in 1995 [44]. It claims that novel characteristics such as conformity, complexity, observability, trialability, and other associated benefits have a major impact on the adoption rate of new technology. Rogers [44] stated that innovation is a concept that can be defined as “an idea, practice or an object which is perceived as new by an individual or any other unit of adoption”, and diffusion is described as “the process in which an innovation is communicated through certain channels, over time, among the members of social systems”. It has been observed in previous research on innovation diffusion that there is a pro-change bias [45,46]. It was believed that all innovations should be implemented, since they were always beneficial to all parties involved [46]. Moreover, empirical evidence supports the diffusion theory’s usefulness in forecasting consumer adoption behaviour [47]. It may account for a variation in the adoption of between 49% and 87%. A study by Lee et al. [5] found that the complexity of the service is not a significant hindrance in e-payment adoption. Furthermore, Yang et al. [48] reported that there is a degree of resemblance between TAM, TAM2, and IDT, such that these models and theories are complementary to one another in their approach.

3.1.4. Unified Theory of Acceptance and Use of Technology Two (UTAUT2)

To improve the predicting power of the UTAUT, UTAUT2 was developed by incorporating three additional constructs: price value, hedonic motivation, and habit. Individual differences in age, gender, and experience were hypothesised to moderate the effects of constructs on behavioural intention and technological use [49]. UTAUT2 is a recent model, and it has been significantly applied in the literature in the last five years [2,50,51]. According to Morosan and DeFranco [35], the application of UTAUT2 is vigorous in the context of measuring new technology acceptance in consumer-centric products and services. Up to now, UTAUT2 has been examined in several contexts; however, it has focused on the direct association between antecedents and intention to use, despite the fact that many researchers have indicated that the main determinants of technology adoption may not be independent.

3.1.5. Other Theoretical Perspectives

Other theories have been applied in a few studies. For instance, Fishbein and Ajzen [52] introduced the theory of reasoned action, one of the most widely tested social psychology settings that examines human behaviour. As claimed by this theory, behavioural intentions are the direct antecedents of actual behaviour and are impacted by beliefs about the likelihood that performing a specific behaviour would result in a particular outcome. Several studies have applied this theory in explaining the determinant of customer adoption intention of e-payment [53,54]. The expansion of TAM3 depended on the theoretical ground of the use of TAM in many contexts and applications. According to Venkatesh and Bala [55], TAM3 is a comprehensive, integrated model used to measure the determinants of acceptance and use at the individual level with explanations of the predictive power of 34–53% of the variance.

According to prior research, innovation resistance theory appears to be the preferred choice among academics to study innovation resistance; for example, eight past empirical studies utilised this theory as the sole theoretical framework. Moreover, five empirical studies used other theoretical frameworks to complement it with UTAUT2, the innovation diffusion theory, and the valence framework. The innovation resistance theory has been used to investigate the barriers and resistance toward different user innovations, such as online shopping [56], m-banking [57], m-commerce [58,59], and e-banking [60]. Based on self-determination theory, when customers’ needs are fulfilled, their payment satisfaction could be obtained [61]. This theory was used to test the effect of the QR code approach (autonomous vs. dependent payment) on payment pleasure and the mediating and moderating processes that affect payment pleasure and satisfaction [62]. Status quo bias indicates customers’ bias toward keeping the inertial use of incumbent systems, even if there are new and potentially superior systems to switch [63]. Based on the status quo bias theory, three classes of elements are accountable for inertia: rational decision making, psychological commitment, and cognitive misperception [31]. It has already been shown that the possibility of benefit loss costs has a favourable impact on people’s willingness to maintain their current status quo. This decision is made because individuals consider possible losses to be greater than potential advantages anytime they change from their present state to an alternative [64].

3.2. Research Settings and Geographic Distribution of the Literature

In this section, the geographical distribution and research settings of the sample literature were evaluated. The 193 articles included in our review consist of eight empirical studies [65,66,67] and were based on cross country data, while the rest of the empirical articles are single-country studies. Despite the fact that the maturity and use of mobile payment apps vary by nation, cross-regional research is very scarce. The investigation showed that the studies were distributed among 37 countries only. Table 2 shows that India is the most investigated country in our sample, with 33 articles. This can be attributed to the demonetisation decision taken by the Indian Government in the year 2016. Consumer transactions using cash accounted for 98 percent of all transactions prior to demonetisation. However, after demonetisation, digital transactions transpired remarkably. Recently, there has been a dramatic rise in the usage of mobile wallets for different payment services, with 530 million phone users reported in 2018, up from 240 million the year before [50]. Additionally, mobile payments enable merchants to reach out to retail consumers in distant areas of large nations such as India.

Table 2.

The research settings of the prior studies.

China is the second most investigated market with 29 studies, followed by the USA, Spain, and Malaysia (15, 12, and 11 articles respectively). The rest of the countries were subject to fewer than ten studies each, and among them, 27 countries were subject to fewer than two studies. Interestingly, it has been commonly highlighted in the literature that cultural or psychological elements are essential in understanding the behavioural differences in consumers from different cultural backgrounds [31,68,69], yet limited work has been found evaluating social and cultural factors from various countries. Moreover, the literature has reported that customer adoption of e-payments depends on cultural differences and market conditions of different countries, yet there is an absence of studies from countries in Latin America, Africa, and Asia despite their large socio-economic impact [67,70].

The study design used in the empirical publications varied considerably, and quantitative, qualitative, and mixed approaches for analysis were used. The sample literature in our review consisted of 154 quantitative, 11 mixed methods, 11 non-empirical, 10 Reviews, 5 qualitative studies, and 2 case studies (as detailed in Table 2). The purely qualitative studies were based on interviews [7,18,70,71,72], and the mixed-method research used both a verbal protocol analysis and a field study for its qualitative component, and regression for the quantitative component [67,73,74,75,76,77,78]. By blending qualitative and quantitative methods in a case study design, Iman [66] analyses whether mobile payment is still relevant in the fintech era, while Pousttchi et al. [79] applied multi-case study analysis to develop an m-payment business model framework. Among the review studies in prior work, two meta-analyses were identified, and both focused on mobile payment behaviour determinants [80,81]. Following the review of the literature, it was determined that several methodological gaps identified by scholars should be addressed in the context of future work, such as sample size [31,38,82,83], sample unit [2,84], lack longitudinal studies [85,86,87], lack of qualitative work [88,89], limitations of a single-country context [70,90,91], and analysis technique [92].

3.3. Thematic Analysis

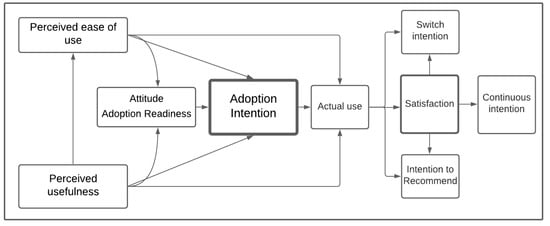

Over the past two decades, the range of subjects addressed by e-payment research in international business has multiplied in tandem with the rapid rise in the number of publications. Unlike previous reviews [3] that focus on important determinants that affect e-payment behaviour, we organise our comprehensive review of research findings according to the customers’ outcome behaviour related to electronic payment adoption, namely adoption factors (acceptance and use), actual use factors, satisfaction factors, continue to use factors, and switch or recommend intention factors (see Figure 3). These constructs formulate the general model of customers electronic payment behaviour, which depends on the TAM that evaluates the interrelationship between perceived ease of use, attitude, usefulness, and adoption intention. This model is frequently observed in our sample literature; about 55% of research concentrated on the characteristics of adoption behaviour, whereas the remaining components that got little attention in previous research were generated using the literature reviewed. All the general model variables were discussed separately to make it easier and simpler for researchers to comprehend.

Figure 3.

The general electronic payment behaviour model.

3.3.1. Adoption Attention Factors (Acceptance/Use Behavior/Usage)

The advent of modern retail channels like the Internet and mobile commerce necessitates the development of new payment instruments in order to facilitate viable and accessible transactions in these channels. Although current card payments are accepted for most purchases, their transaction fees are incredibly high, making them unprofitable in micropayment transactions [70]. Furthermore, in recent decades, the fast societal adoption of mobile gadgets and the role they have played in the development of personal and professional activities has been one of the most significant technological events, owing to the widespread belief that mobile phones have the potential to serve as a platform for e-payments that can eventually replace cash-based payments. However, there is still a lack of payment through mobile devices, especially in the developing world, and many challenges still need to be overcome. According to Schierz et al. [93], despite the existence of technologically sophisticated options, mobile payment remains shockingly underutilised. Consumers seem to continue to be resistant to mobile payment systems.

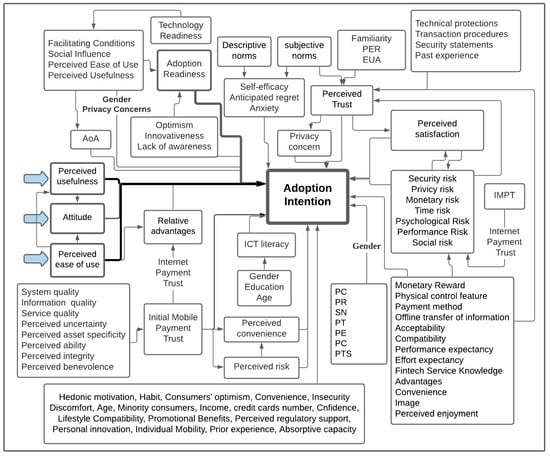

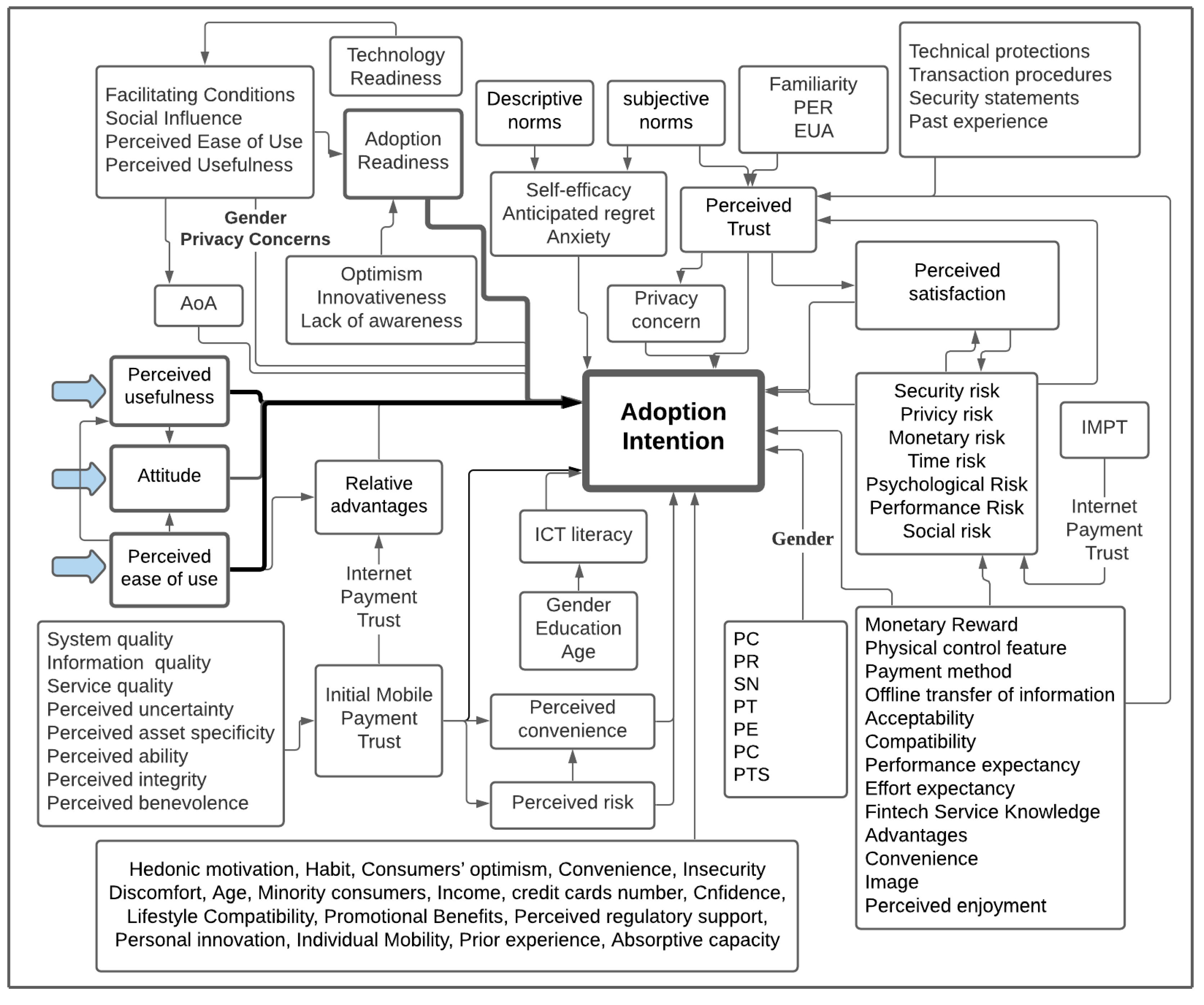

The literature has mainly discussed the factors of customer electronic payment behaviour related to the TAM and TAM2 [94,95,96,97], and other studies extended the work by adding risk, quality, and trust as antecedents of ease of use and customer attitude [98], or the moderating effect of gender by F. J. Liébana-Cabanillas et al. [99] where customers’ gender was found to have a major role in the suggested relationship between ease of use and usefulness of the new system, between usefulness and attitude and intentions toward using the system, and between customers’ trust and a positive attitude toward using the system. Other studies have concentrated on the characteristics of UTAUT and UTAUT2 [35,42,81,100,101], and this work was expanded by incorporating the moderating effect of [5], and religiosity [43]. Both moderators were found to have a major effect on the antecedents of adoption behaviour. Some scholars (16 studies) have taken the analysis a step forward by investigating the moderating impact of gender, education, income, experience, age, privacy, trust, and smartphone addiction [12,102,103] with a focus on the gender impact (10 studies). In addition to the factors in those models, there are several factors that were reported to strongly influence the adoption of e-payments, such as cost [86,104], innovativeness [2,105,106,107], convenience, and relative advantages [108,109], and trust [92,110]. Handarkho and Harjoseputro [111] suggested that consumer innovativeness has the most influential direct effect on the adoption behaviour of e-payments, while other studies found it to be the reliability [112], perceived benefit and perceived trust [53], attitude and risk [42], and ease of use [113]. Figure 4 provides a summary model of all investigated variables in the sample literature that directly or indirectly influence e-payment adoption. As shown in the Figure, scholars have highlighted several types of risk that might have influenced the adoption intention of customers, including economic risk, functional risk, security risk, privacy risk, time risk, service risk, psychological risk, and social risk. However, the literature has only focused on privacy and security risk.

Figure 4.

The behavioural intention model of electronic payment. PER: Perceived Environmental Risk, EUA: Espoused Uncertainty Avoidance, PC: Perceived cost, PR: Perceived risk, SN, Subjective norms, PT: Perceived trust, PE: Perceived Enjoyment, PC: perceived convenience, PTS: Perceived transaction speed, AoA: Attractiveness of Alternatives, IMPT: Initial Mobile Payment Trust, ICT: Information and communications technology.

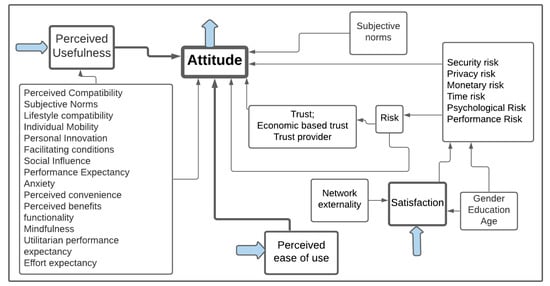

With regard to customer attitude, studies have applied it in models as a path of the perceived usefulness and ease of use influence on adoption behaviour (as introduced by TAM) [114]. However, until recently, few other scholars in this field have looked at the antecedent of customer attitude. These antecedents include the function of risk characteristics, trust, enabling conditions, lifestyle, social impact, performance expectation, anxiety, perceived advantage and convenience, subjective norms, individual mobility, personal innovation, compatibility, mindfulness, and effort expectation (see Figure A1). Most of these variables have been shown to have a substantial effect on consumer attitudes regarding e-payments [101,113,115,116,117,118,119]. However, the results of prior studies are inconsistent. For example, the majority of studies have supported the positive impact of ease of use on customer attitude [99,115,119], while some scholars [89,116] have failed to support this association.

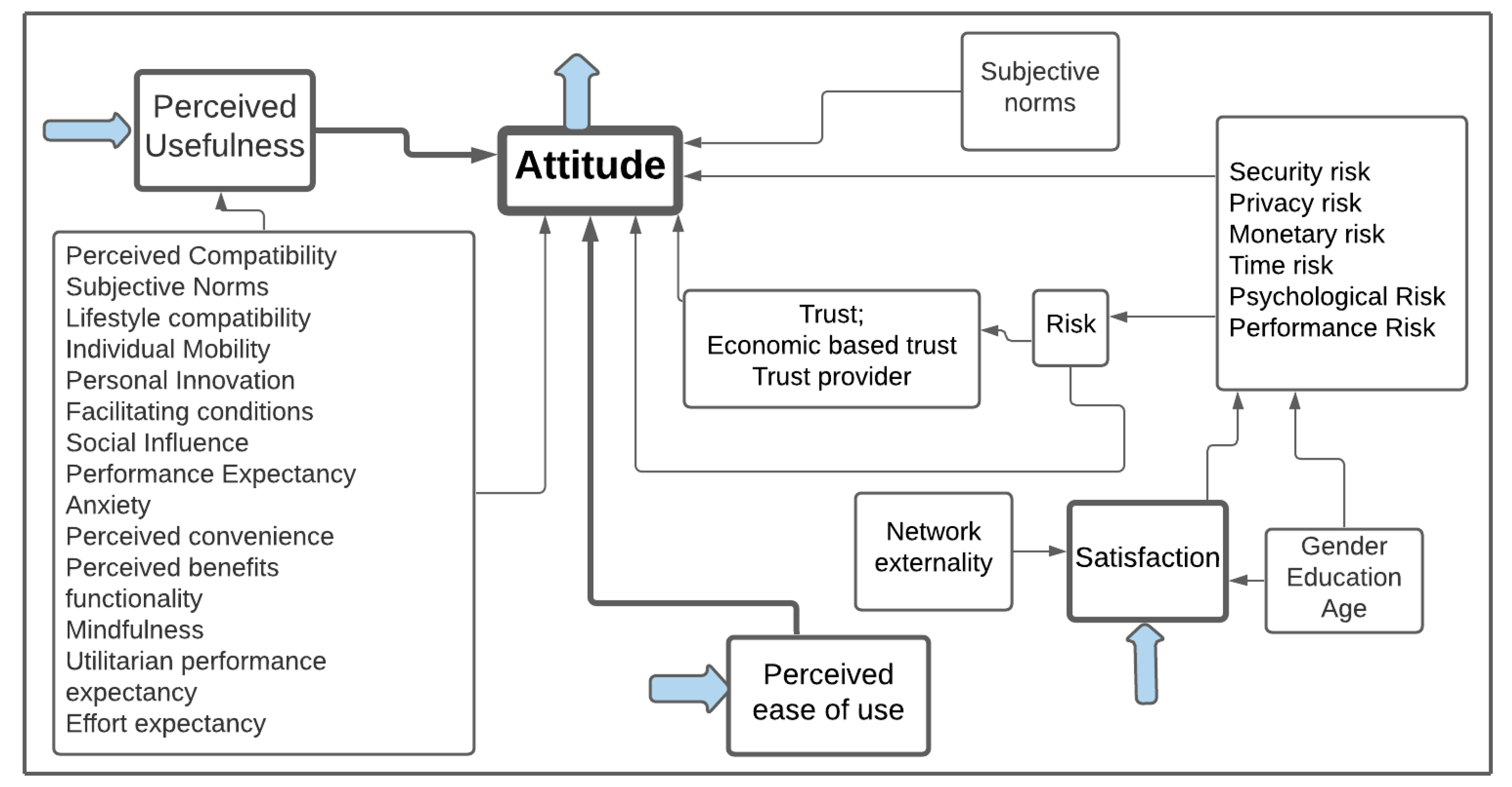

The perceived usefulness of the service is a critical element in understanding the desire to utilise electronic payments, and it was addressed in 41 pieces of research. The subjective possibility that technology would enhance the manner a customer completes their objective is referred to as perceived usefulness. In the context of our study, perceived usefulness will enhance the user’s attitude and intention to use mobile payment systems. As stated by TAM, perceived usefulness is defined as the level to which a person thinks that adopting a specific system would improve their effectiveness and performance after implementation. In mobile payment, perceived usefulness refers to the extent to which prospective users expect mobile payments to increase their performance in transactions. Previous studies have investigated the impact of various factors (see Figure A2) on usefulness and found it to be significantly affected by subjective norms [97,98], perceived security [98], ease of use [82,89,97,112,120], attitude [120], compatibility [51,120,121], reliability [112], internet experience [90], mobile and technology self-efficiency [122], mobility [89], and awareness [51]. Whereas the impact of other factors was failed to be supported, such as prior experience, innovativeness, trust, perceived risk, and financial incentives [82,89,112]. This indicates that the results of previous studies on these relationships are inconsistent.

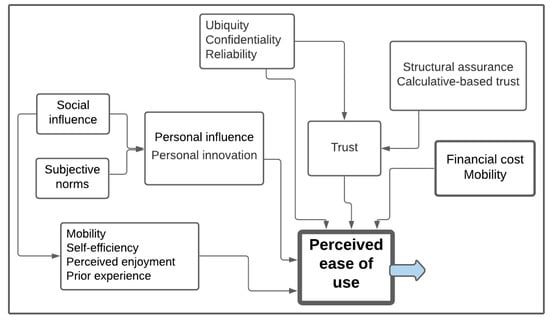

The term ‘perceived ease of use’ (also known as ‘effort expectation’ in UTAUT2) refers to the level of ease related to the customer’s utilisation of technology. It indicates a favourable susceptibility or intention toward the use, which influences self-reported actual use [39]. It has been argued that the most crucial element explaining consumers’ proclivity to utilise mobile payment systems is the ease of use [115]. Davis [39] defined ease of use as the degree to which an individual believes that using a certain technology would be easy. Numerous studies on mobile commerce and mobile banking adoption have found the ease of use to be a critical predictor of adoption intention. Several factors (see Figure A3) were introduced in the e-payment literature to exert the impact of ease of use, including reliability, prior experience, self-efficacy, perceived enjoyment, trust, innovativeness, risk, personal influences, and mobility [54,82,87,105,112,115,122,123,124,125], while the influence of other factors failed to be supported ubiquity, subjective norms, and financial cost [87,112,125]. According to Liu et al. [126], characteristics such as mobility liberate users from temporal and geographical restrictions and allow them to make payments at any time and any place, expanding consumers’ chances to utilise mobile payments and increasing their transaction volume. Additionally, some scholars have looked beyond the direct relationships and included several demographic and behavioural factors such as gender, experience, age, and smartphone addiction [95,102,125] and found them to moderate the impact of ease of use on the adoption behaviour of customers.

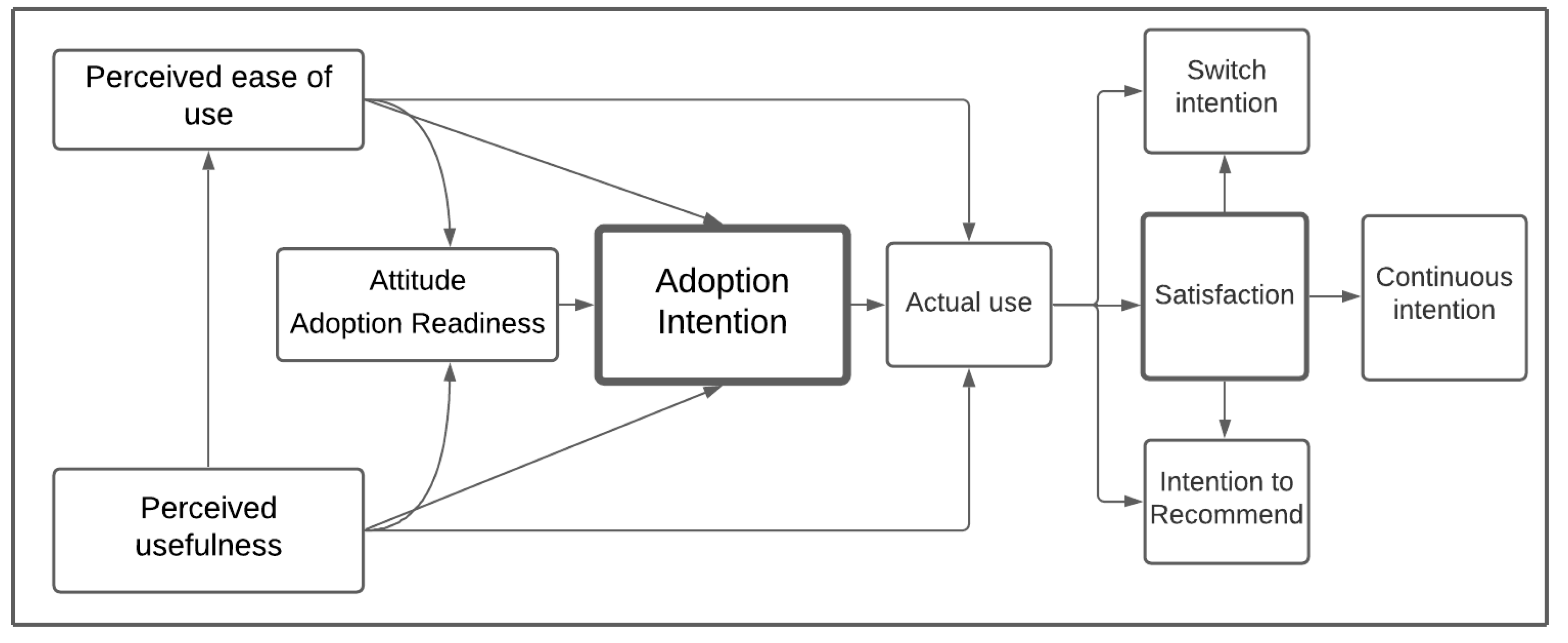

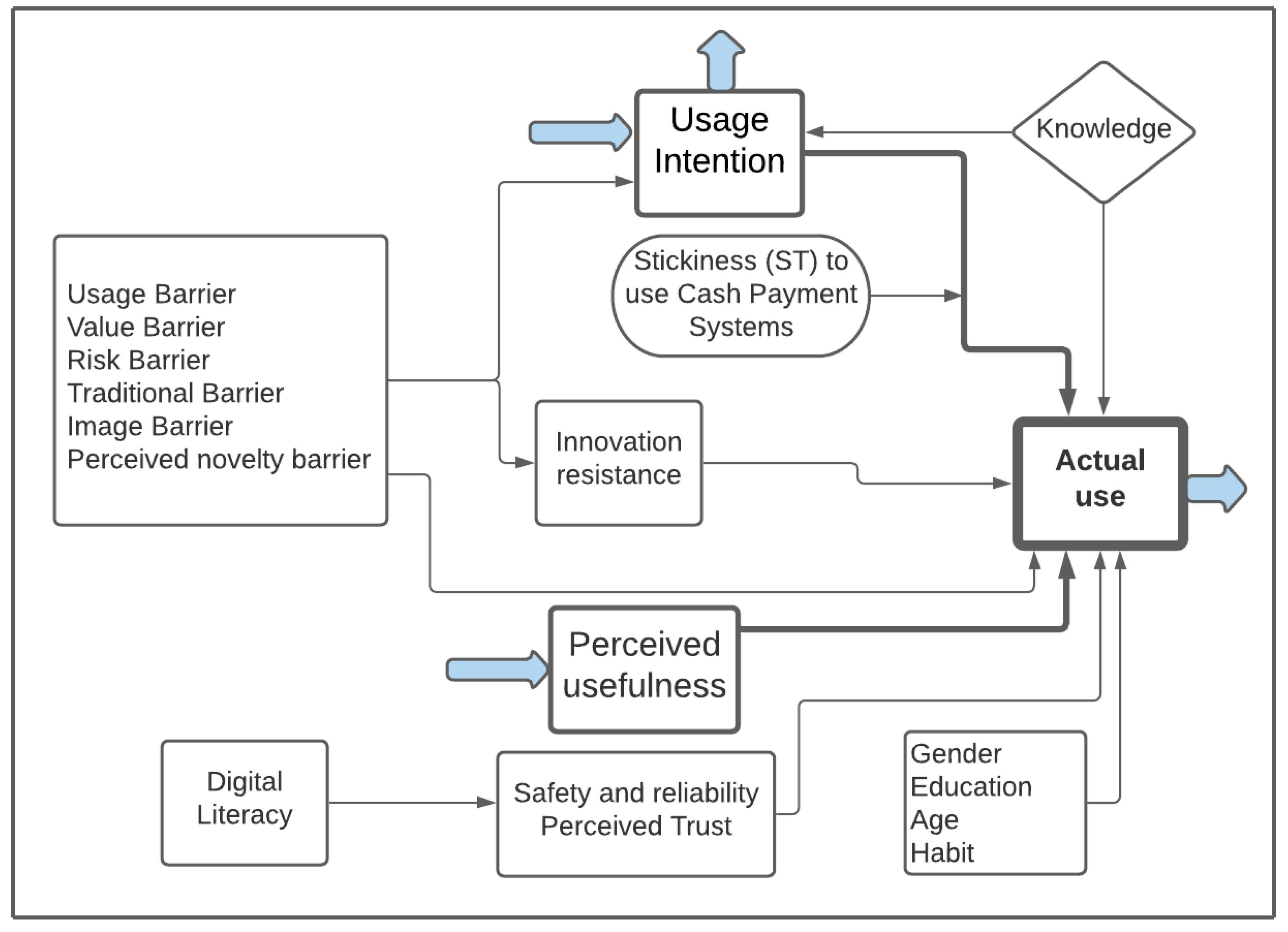

3.3.2. Actual Usage Factors

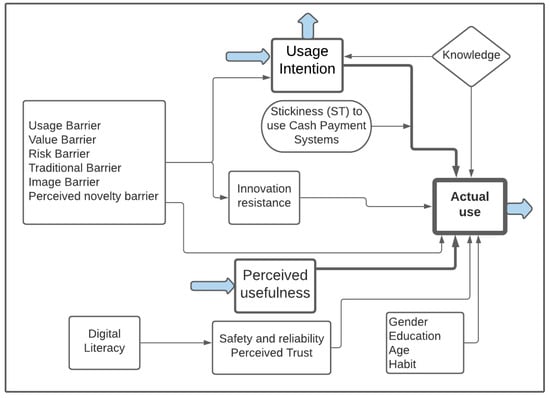

There is a significant gap in the e-payment literature in terms of actual use since the usage models mainly depend on adoption intention and ignore the actual use of consumers (7 studies). In some cases, prior studies measure intention as a proxy for actual usage; however, this is insufficient for predicting real behaviour, while it may be solved by capturing actual use in terms of frequency or intensity of system use. This could be explained by the insufficient data about time series in these settings, making it difficult to understand the actual behavioural alterations in different periods. Scholars have found the actual use of e-payment influenced by habits of customers, innovation resistance to utilise digital payment, and intention to use it [127,128]. Likewise, Sivathanu [129] found that the effect of adoption intention on the actual use of e-payment depends on the condition of cash payment (see Figure 5).

Figure 5.

The actual use model of electronic payments.

3.3.3. Satisfaction Factors

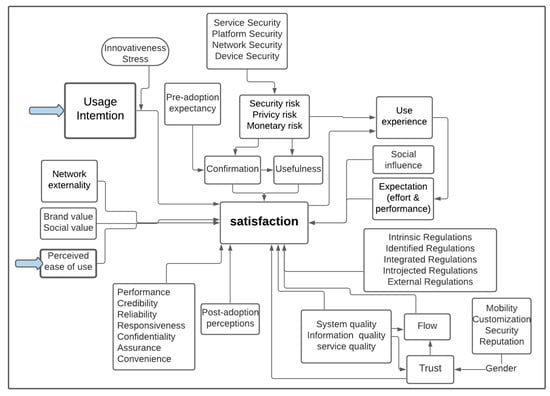

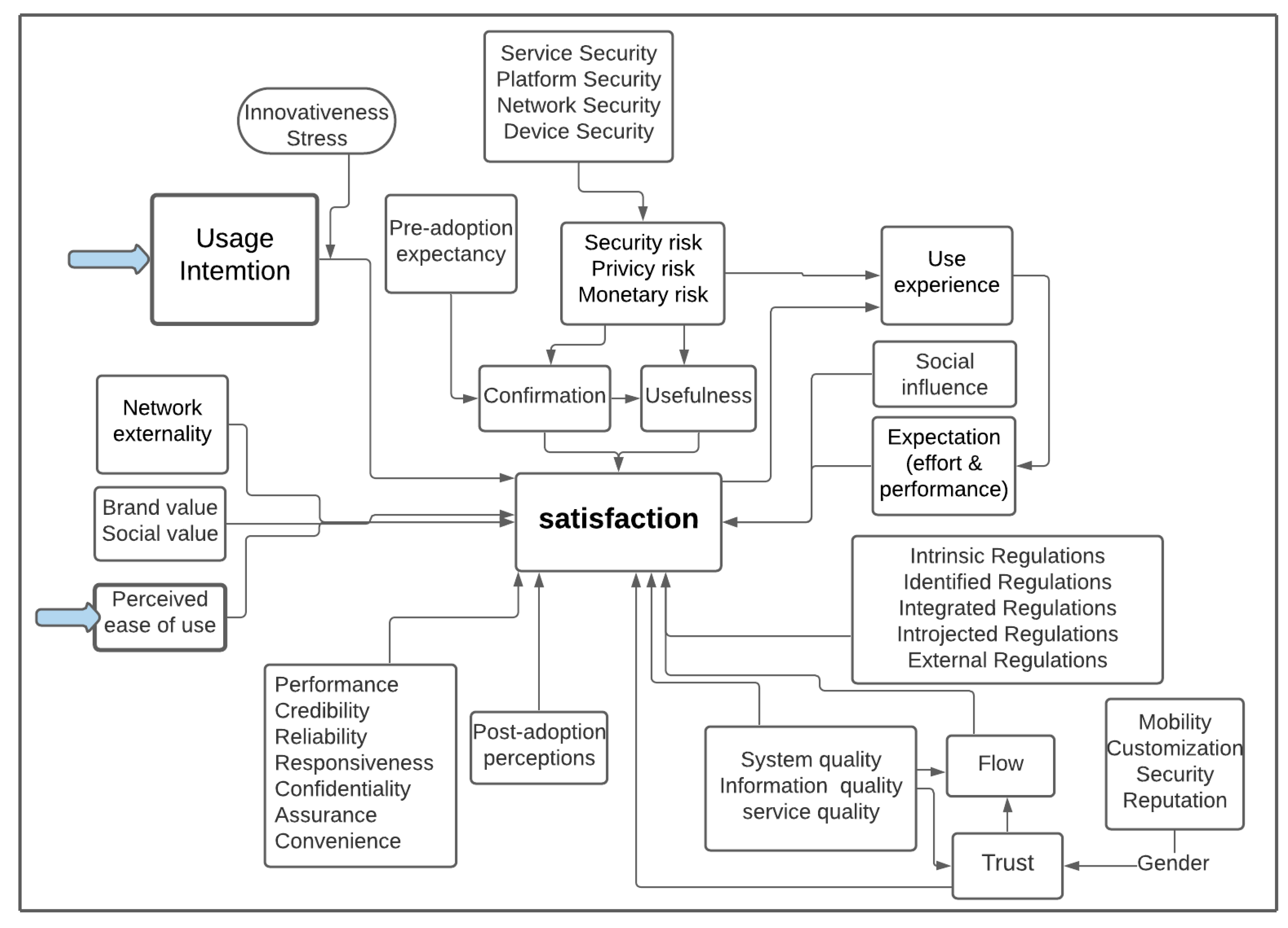

In m-commerce, customers satisfaction indicates their overall experience and general assessment of the products and services. The success of any new technology highly depends on the users’ impressions and satisfaction regarding the service encounter. Thus, the adaptation of e-payment is only possible when users are satisfied and have a positive expectation. To understand the antecedent of e-payment satisfaction, we summarised all factors discussed in the literature in Figure 6. User satisfaction is a summary of the subjective emotions that consumers have acquired as a result of their interactions with a service provider. Prior studies established that cost, usefulness, trust, social influence, credibility, information privacy, and responsiveness factors are essential to increase the user satisfaction of mobile payment services [74]. Furthermore, Yu et al. [85] observed that elevated levels of gratification will decrease the perceived benefits of switching behaviour, resulting in a high continuance intention. When considering user satisfaction, it is essential to recognise that it is distinct from user satisfaction in that it is linked to a specific context in a specific instance in which a service experience is investigated. While the total (or average) of overall experiences of service interactions over a period of time is mostly used to determine user happiness.

Figure 6.

The satisfaction factors model of electronic payment.

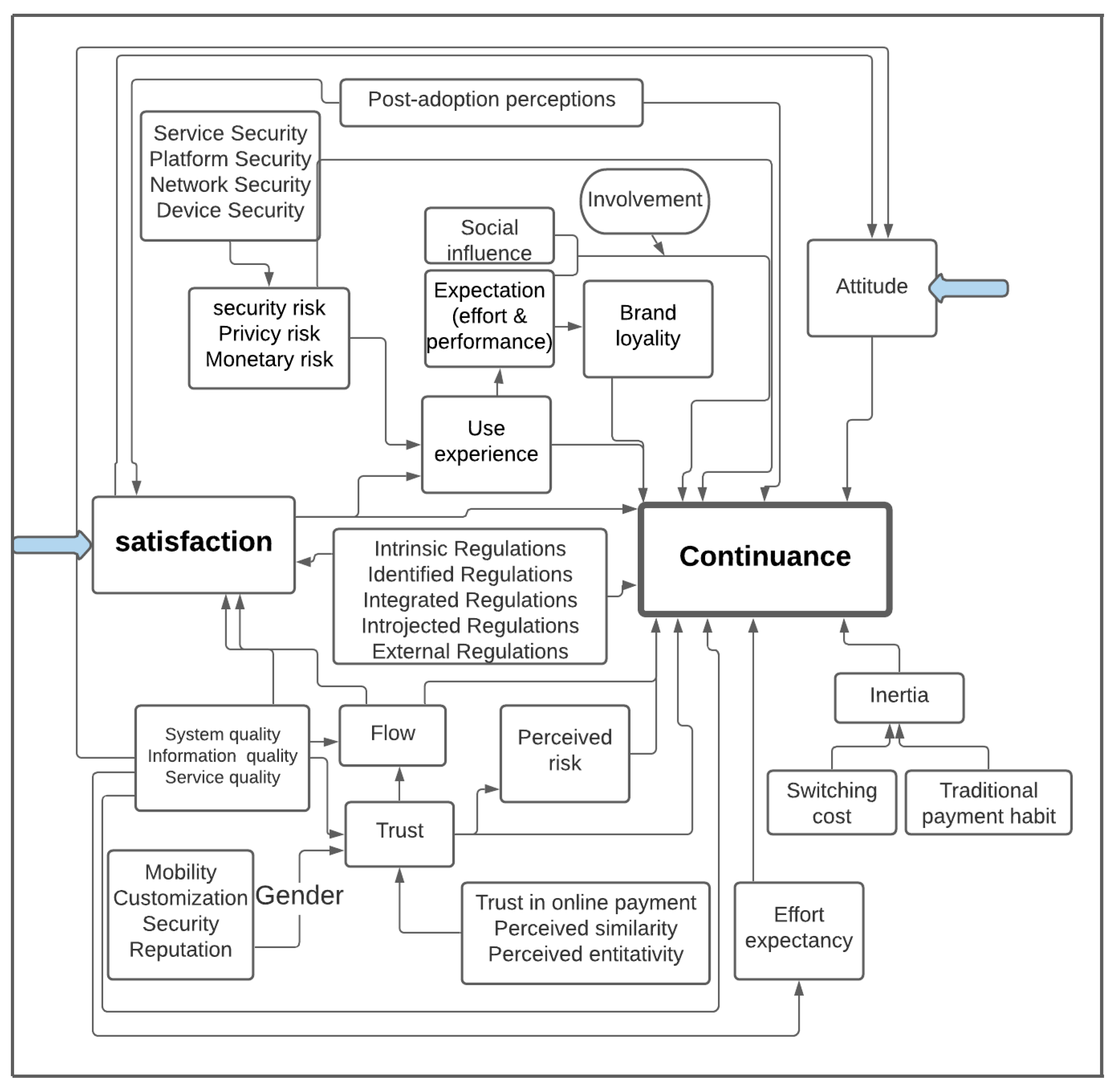

3.3.4. Continuance Factors

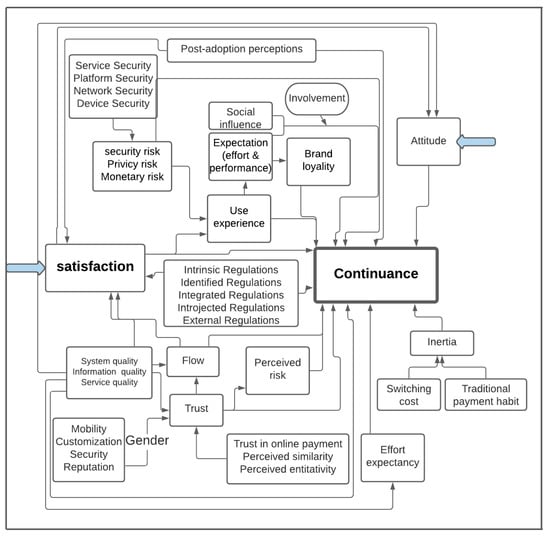

The fierce competition between e-payment providers and the affordable switching cost for users have made maintaining customers and ease their continued usage, which is critical for vendors. Clients could simply change from one service to another, which also clarifies the need to maintain customers. It is, therefore, essential to understand the antecedents of mobile payment continuous use. The post-adoption behavior, including constant use of the mobile payments, has seldom been examined, and few studies have focused on the continuous use of mobile payment services (16 studies). The continued use of mobile payment technology mostly depends on the development of long-term connections with customers, the provision of organisations with a competitive advantage, and the assurance of their survival. Providing that their expectations are fulfilled in the best possible manner, it is probable that consumers will continue to utilise mobile payment technologies. Given the importance of consumers continuing to use this new technology, the majority of researchers have focused on satisfaction as the driver of continuance behaviour and have found it to be a significant determinant [34,91,130,131,132,133,134,135], while few studies have considered other variables such as trust, risk, and loyalty (see Figure 7). However, the results of these studies are inconclusive. For instance, mixed findings were reported regarding the impact of perceived usefulness [131,136], perceived risk [84,137], and satisfaction [135,138]. Moreover, Gao et al. [84] found that customer involvement significantly moderates the impact of effort expectancy, performance expectancy, and social influence on e-payment continuous use. Despite their significance, the role of perceived security, personal influence, demographic factors in continuous intention to use e-payment, these factors have not yet been investigated in depth [130,139].

Figure 7.

The continuance model of electronic payment.

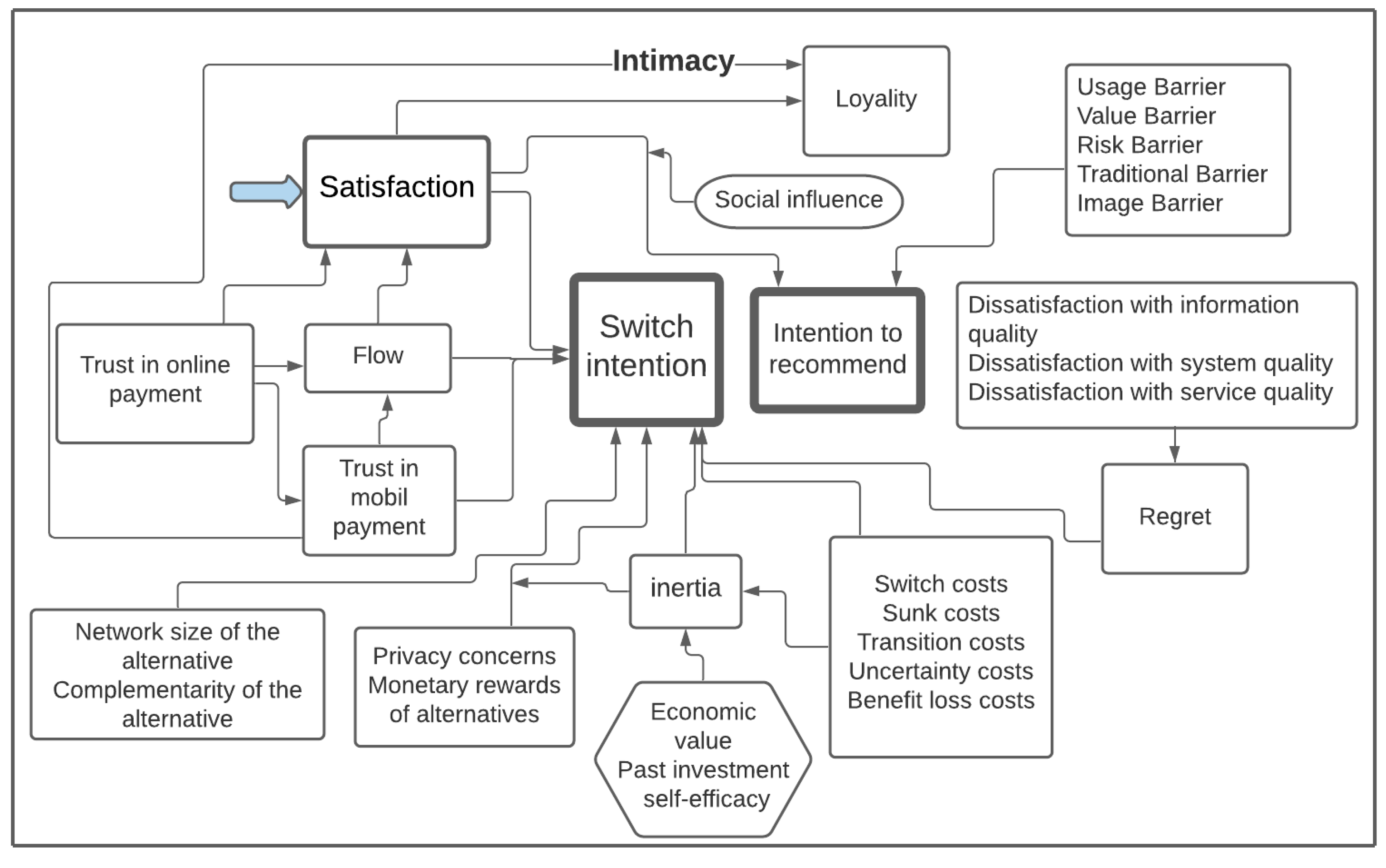

3.3.5. Switch or Recommend Factors

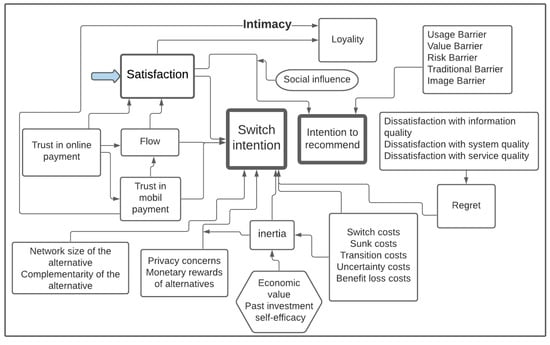

Consumers still prefer to pay with cash when purchasing products and services in many nations, which explains why e-payments are rarely utilised. The intense competition between mobile payment platforms is a classic example of winner-takes-all, a phenomenon that occurs in markets with strong network effects in which merchants and potential users tend to adopt the mobile payment platform with the most significant number of existing users, resulting in the smaller platform becoming smaller and the larger platform becoming larger. Hence, providers of mobile payment apps must focus on retaining current customers and facilitating their continuing usage in order to achieve financial viability rather than allowing consumers to switch to other alternative applications. In spite of being a key challenge for business continuity and management for MPS platform firms, there is still a lack of knowledge of the switching behaviour of users of this platform [64,140,141]. As shown in Figure 8, scholars have confirmed that switch behaviour to be highly influenced by alternative attractiveness, trust, satisfaction, switching costs, risk, and regret [1,64,140,141]. Customers tend to change the service if the price seems to be excessively high or unjustifiable [1]. Wang et al. [140] found that Inertia positively predicts switching behaviour and negatively moderates the positive relationship between alternative monetary rewards and switching behaviour. Due to the limited research, there is significant room for further research into switching behaviour considering cross-cultural surveys and other relevant factors (e.g., length of use, mobile payment methods, platform providers, etc.).

Figure 8.

The switch model of electronic payment.

4. Discussion and Future Research Suggestions

This section provides a discussion on future research directions. In earlier sections, we summarised all theoretical perspectives that have been applied in customer e-payment adoption behaviour. Most applied theories in the sample (i.e., UTAUT and UTAUT2 models) had some limitations. One of them is the incapacity of explaining the role of culture in the adoption of novel technology. Park et al. [136] reported that consumer perceptions and their effects on intention might differ from culture to culture. Mobile payment penetration differs among countries because of their different economic, cultural, social, technological, and demographic features. Interestingly, it has been commonly highlighted in the literature that cultural or psychological elements are essential in understanding the behavioural differences of consumers in different cultural backgrounds [31,68,69], yet limited work has been found evaluating social and cultural factors from various countries. These limitations necessitate the need for further theoretical development.

Additionally, the sample studies have asserted that variables related to demography and behaviour significantly affected the customers’ behaviour toward e-payment. However, a variety of other individual factors, such as socio-economic status, cognitive, cultural, and emotional attitudes toward digital products, as well as personality, may contribute to total user satisfaction and continuance intention. In the literature, these constructs have received less attention; thus, future studies should be conducted to investigate the direct and indirect effects of these factors [90,135,142]. Another major limitation that is commonly highlighted in the literature is the use of cross-sectional data. It is worth noting that user behaviour is dynamic. Thus, the longitudinal study may provide some insights into the evolution of user behaviour. For example, future research could investigate customers adoption and post-adoption of e-payment and compare initial and continuance usage determinants [127,132,143,144].

Furthermore, the results of prior studies on the antecedents of customer behaviour are inconsistent. For instance, mixed findings were reported regarding the impact of perceived usefulness [131,136], perceived risk [84,137], and satisfaction [135,138]. Furthermore, the majority of studies have supported the positive impact of ease of use on customer attitude [99,115,119], while some scholars [89,116] have failed to support this association. This necessitates in-depth study and comprehensive measurement techniques. A multi-method approach to future research on new technologies and their adoption would be beneficial since it would allow for the full description and new insights to be collected first using qualitative/mixed techniques. Following that, the novel theoretical implications are examined using other methods.

Although switching behaviour, actual use, continuous use, recommend intention, and satisfaction of customers are important issues for business continuity and management, there is still only a poor understanding of these constructs as investigated in a few prior studies compared to use intention [64,104,145]. In order to reflect the current status and predict the future market, future studies should consider these constructs. In addition, there is still scant empirical research observing significant factors, which can affect how consumers approach them including service attributes, flow experience, different risk types, personal influence, grievance redressal, and system characteristics [5,34,141,145]. Future research studies may also take into account these crucial aspects.

5. Conclusions

The rise of mobile and internet technology has significantly impacted people’s daily lives and behaviour. Digital payment continues to spread rapidly, gaining more importance. Although there has been a remarkable increase in the number of empirical studies in recent years, very few reviews have been conducted in this area. This paper, therefore, aims to offer the most up-to-date research on digital payments from a customer perspective. Our SLR analysed 193 studies retrieved from Scopus and Web of Science databases. We explored the sample literature by focusing on the research yearly trend, influential studies, regional distribution, theoretical background, methodology and modelling, and thematic analysis. It was found that a few empirical articles have focused on the switching behaviour actual use, continuous use, recommended intention, and satisfaction of digital payment users, while the majority of prior work concentrated on understanding the antecedents of intention to use. It should also be noted that a vast majority of empirical work is from evidence from an across-sectional sample, pointing to the need for longitudinal or cross-country work. Some avenues for further work were suggested after conducting the comprehensive review.

In addition to providing an overview of current academic study topics, findings, and trends, this review adds to the existing literature as research in digital payment has been fragmented and lacks a plan or an agenda. Each topic in this article contains a brief overview of research done in the field of e-payment and the key areas within each theme. Additionally, a synthesis of prior results enables researchers to avoid duplicating previous work and to identify critical gaps. This research is novel in that it offers new incentives and recommendations for future studies in order to meet the gaps of reviewed studies.

Despite the numerous implications derived from the study, it has some limitations. This study relies on the research documents indexed in Scopes and WoS only. This means that there might be some studies from other databases that were not included in this study. Hence, more databases may be added to the future review to cover a broader range of relevant materials. Furthermore, this study has developed a searching string that utilised several terms to search the literature titles, keywords, and abstracts. These terms might not cover all related literature. Therefore, future researchers are encouraged to further develop our search string that would cover all relevant literature. The literature review only included articles related to the customer perspective of digital payment adoption, excluding the supply side. The findings of this study should be interpreted with caution. Hence, future researchers are encouraged to consider the provider side of digital payment technology. Finally, the lack of language skills and restrictions on item availability excluded some publications in non-English languages. Despite the mentioned limitations, our comprehensive literature review compiled various scholarly articles for review, building a solid foundation of literature that accurately represents quality and influential contributions to the field’s governance research. Hence, we anticipate that excluding certain publications will have a minimum impact on the overall result of our study. We believe that our study serves as a starting point for a profound understanding of the current state of customer perspective of digital payment.

Author Contributions

Conceptualization, A.M.S. and S.F.A.K.; methodology, S.F.A.K.; software A.F.A.; validation, A.M.S., A.F.A. and S.F.A.K.; formal analysis, A.M.S.; investigation, S.F.A.K.; resources, A.M.S.; data curation, A.F.A.; writing—original draft preparation, A.M.S. and S.F.A.K.; writing—review and editing, S.F.A.K.; visualization, A.M.S.; supervision, H.K.; project administration, H.K.; funding acquisition, A.M.S. and A.F.A. All authors have read and agreed to the published version of the manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Details of the majority of the 193 studies selected are included in this investigation. The rest of the articles are available from the first and corresponding authors or other authors upon request.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

The most productive journals.

Table A1.

The most productive journals.

| Journal Name | Number of Articles |

|---|---|

| International Journal of Bank Marketing | 19 |

| Electronic Commerce Research and Applications | 15 |

| Journal of Retailing and Consumer Services | 13 |

| International Journal of Information Management | 8 |

| Information Systems Frontiers | 8 |

| Technology in Society | 7 |

| Computers in Human Behavior | 7 |

| International Journal of e-Business Research | 6 |

| International Journal of Mobile Communications | 5 |

| Internet Research | 5 |

| Industrial Management and Data Systems | 5 |

| Information Systems and e-Business Management | 5 |

| Information and Management | 4 |

| International Journal of Electronic Finance | 3 |

| Journal of Computer Information Systems | 3 |

| Service Industries Journal | 3 |

| International Journal of Retail and Distribution Management | 3 |

| International Journal of Contemporary Hospitality Management | 2 |

| Journal of Indian Business Research | 2 |

| Economic Research-Ekonomska Istrazivanja | 2 |

| Total | 125 |

Figure A1.

The attitude model of electronic payment.

Figure A1.

The attitude model of electronic payment.

Figure A2.

The Perceived usefulness model of electronic payment.

Figure A2.

The Perceived usefulness model of electronic payment.

Figure A3.

The perceived ease of use factors model of electronic payment.

Figure A3.

The perceived ease of use factors model of electronic payment.

References

- Loh, X.M.; Lee, V.H.; Tan, G.W.H.; Ooi, K.B.; Dwivedi, Y.K. Switching from cash to mobile payment: What’s the hold-up? Internet Res. 2021, 31, 376–399. [Google Scholar] [CrossRef]

- Balakrishnan, V.; Shuib, N.L.M. Drivers and inhibitors for digital payment adoption using the Cashless Society Readiness-Adoption model in Malaysia. Technol. Soc. 2021, 65, 101554. [Google Scholar] [CrossRef]

- Teng, S.; Khong, K.W. Examining actual consumer usage of E-wallet: A case study of big data analytics. Comput. Hum. Behav. 2021, 121, 106778. [Google Scholar] [CrossRef]

- Kim, C.; Tao, W.; Shin, N.; Kim, K.S. An empirical study of customers’ perceptions of security and trust in e-payment systems. Electron. Commer. Res. Appl. 2010, 9, 84–95. [Google Scholar] [CrossRef]

- Lee, J.M.; Lee, B.; Rha, J.Y. Determinants of mobile payment usage and the moderating effect of gender: Extending the UTAUT model with privacy risk. Int. J. Electron. Commer. Stud. 2019, 10, 43–64. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, Y.; Li, H.; Yu, B. Understanding perceived risks in mobile payment acceptance. Ind. Manag. Data Syst. 2015, 115, 253–269. [Google Scholar] [CrossRef]

- Apanasevic, T.; Markendahl, J.; Arvidsson, N. Stakeholders’ expectations of mobile payment in retail: Lessons from Sweden. Int. J. Bank Mark. 2016, 34, 37–61. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Lutfi, A.; Alsaad, A.; Taamneh, A.; Alsyouf, A. The Determinants of Digital Payment Systems’ Acceptance under Cultural Orientation Differences: The Case of Uncertainty Avoidance. Technol. Soc. 2020, 63, 101367. [Google Scholar] [CrossRef]

- Bagla, R.K.; Sancheti, V. Gaps in customer satisfaction with digital wallets: Challenge for sustainability. J. Manag. Dev. 2018, 37, 442–451. [Google Scholar] [CrossRef]

- Gupta, S.; Xu, H. Examining the relative influence of risk and control on intention to adopt risky technologies. J. Technol. Manag. Innov. 2010, 5, 22–37. [Google Scholar] [CrossRef] [Green Version]

- Johnson, V.L.; Kiser, A.; Washington, R.; Torres, R. Limitations to the rapid adoption of M-payment services: Understanding the impact of privacy risk on M-Payment services. Comput. Hum. Behav. 2018, 79, 111–122. [Google Scholar] [CrossRef]

- Sinha, M.; Majra, H.; Hutchins, J.; Saxena, R. Mobile payments in India: The privacy factor. Int. J. Bank Mark. 2019, 37, 192–209. [Google Scholar] [CrossRef]

- See-To, E.W.K.; Ho, K.K.W. A study on the impact of design attributes on E-payment service utility. Inf. Manag. 2016, 53, 668–681. [Google Scholar] [CrossRef]

- Makki, A.M.; Ozturk, A.B.; Singh, D. Role of risk, self-efficacy, and innovativeness on behavioral intentions for mobile payment systems in the restaurant industry. J. Foodserv. Bus. Res. 2016, 19, 454–473. [Google Scholar] [CrossRef]

- Kapoor, K.K.; Dwivedi, Y.K.; Williams, M.D. Examining the role of three sets of innovation attributes for determining adoption of the interbank mobile payment service. Inf. Syst. Front. 2015, 17, 1039–1056. [Google Scholar] [CrossRef] [Green Version]

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Taylor, E. Mobile payment technologies in retail: A review of potential benefits and risks. Int. J. Retail Distrib. Manag. 2016, 44, 159–177. [Google Scholar] [CrossRef]

- Alkhowaiter, W.A. Digital payment and banking adoption research in Gulf countries: A systematic literature review. Int. J. Inf. Manag. 2020, 53, 102102. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Nour, A.-N.I. The Impact of Corporate Governance on Firm Performance during the COVID-19 Pandemic: Evidence from Malaysia. J. Asian Financ. Econ. Bus. 2021, 8, 0943–0952. [Google Scholar] [CrossRef]

- Vargo, D.; Zhu, L.; Benwell, B.; Yan, Z. Digital technology use during COVID-19 pandemic: A rapid review. Hum. Behav. Emerg. Technol. 2021, 3, 13–24. [Google Scholar] [CrossRef]

- Kraenzlin, S.; Meyer, C.; Nellen, T. COVID-19 and regional shifts in Swiss retail payments. Swiss J. Econ. Stat. 2020, 156, 14. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.A.; Abueid, R. Nudging toward diversity in the boardroom: A systematic literature review of board diversity of financial institutions. Bus. Strateg. Environ. 2021, 30, 985–1002. [Google Scholar] [CrossRef]

- Hazaea, S.A.; Zhu, J.; Al-Matari, E.M.; Senan, N.A.M.; Khatib, S.F.A.; Ullah, S. Mapping of internal audit research in China: A systematic literature review and future research agenda. Cogent Bus. Manag. 2021, 8, 1938351. [Google Scholar] [CrossRef]

- Zamil, I.A.; Ramakrishnan, S.; Jamal, N.M.; Hatif, M.A.; Khatib, S.F.A. Drivers of corporate voluntary disclosure: A systematic review. J. Financ. Report. Account. 2021, in press. [Google Scholar] [CrossRef]

- Zhao, J.; Xue, F.; Khan, S.; Khatib, S.F.A. Consumer behaviour analysis for business development. Aggress. Violent Behav. 2021, 101591, in press. [Google Scholar] [CrossRef]

- Hazaea, S.A.; Zhu, J.; Khatib, S.F.A.; Bazhair, A.H.; Elamer, A.A. Sustainability assurance practices: A systematic review and future research agenda. Environ. Sci. Pollut. Res. 2021, 1–22. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.; Yahaya, I.; Owusu, A. Global trends in board diversity research: A bibliometric view. Meditari Account. Res. 2021. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Hendrawaty, E.; Elamer, A.A. A bibliometric analysis of cash holdings literature: Current status, development, and agenda for future research. Manag. Rev. Q. 2021, 1–38. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Singh, N.; Sahu, G.; Almotairi, M. An innovation resistance theory perspective on mobile payment solutions. J. Retail. Consum. Serv. 2020, 55, 102059. [Google Scholar] [CrossRef]

- Gong, X.; Zhang, K.Z.K.; Chen, C.; Cheung, C.M.K.; Lee, M.K.O. Transition from web to mobile payment services: The triple effects of status quo inertia. Int. J. Inf. Manag. 2020, 50, 310–324. [Google Scholar] [CrossRef]

- Teo, A.C.; Tan, G.W.H.; Ooi, K.B.; Lin, B. Why consumers adopt mobile payment? A partial least squares structural equation modelling (PLS-SEM) approach. Int. J. Mob. Commun. 2015, 13, 478–497. [Google Scholar] [CrossRef]

- Verkijika, S.F. An affective response model for understanding the acceptance of mobile payment systems. Electron. Commer. Res. Appl. 2020, 39, 100905. [Google Scholar] [CrossRef]

- Mouakket, S. Investigating the role of mobile payment quality characteristics in the United Arab Emirates: Implications for emerging economies. Int. J. Bank Mark. 2020, 38, 1465–1490. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, A. It’s about time: Revisiting UTAUT2 to examine consumers’ intentions to use NFC mobile payments in hotels. Int. J. Hosp. Manag. 2016, 53, 17–29. [Google Scholar] [CrossRef]

- De Luna, I.R.; Liébana-cabanillas, F.; Sánchez-fernández, J.; Muñoz-leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Barkhordari, M.; Nourollah, Z.; Mashayekhi, H.; Mashayekhi, Y.; Ahangar, M.S. Factors influencing adoption of e-payment systems: An empirical study on Iranian customers. Inf. Syst. E-Bus. Manag. 2017, 15, 89–116. [Google Scholar] [CrossRef]

- Madan, K.; Yadav, R. Behavioural intention to adopt mobile wallet: A developing country perspective. J. Indian Bus. Res. 2016, 8, 227–244. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319. [Google Scholar] [CrossRef] [Green Version]

- Brohi, I.A. Factors Affecting the Acceptance of Near Field Communication Enabled Mobile Payments: An Empirical Study of Pakistan; International Islamic University Malaysia: Kuala Lumpur, Malaysia, 2019. [Google Scholar]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425. [Google Scholar] [CrossRef] [Green Version]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Soomro, Y.A. Understanding the adoption of sadad e-payments: UTAUT combined with religiosity as moderator. Int. J. E-bus. Res. 2019, 15, 55–74. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations: Modifications of a Model for Telecommunications. In Die Diffusion von Innovationen in der Telekommunikation; Springer: Berlin/Heidelberg, Germany, 1995; pp. 25–38. [Google Scholar]

- Ram, S. A model of innovation resistance. ACR N. Am. Adv. 1987, 4, 208–212. [Google Scholar]

- Rogers, E.M. Diffusion of Innovations, 5th ed.; The Free Press: New York, NY, USA, 2003. [Google Scholar]

- Matemba, E.D.; Li, G. Consumers’ willingness to adopt and use WeChat wallet: An empirical study in South Africa. Technol. Soc. 2018, 53, 55–68. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. 2012, 36, 157. [Google Scholar] [CrossRef] [Green Version]

- Singh, N.; Sinha, N.; Liébana-Cabanillas, F.J. Determining factors in the adoption and recommendation of mobile wallet services in India: Analysis of the effect of innovativeness, stress to use and social influence. Int. J. Inf. Manag. 2020, 50, 191–205. [Google Scholar] [CrossRef]

- Singh, N.; Sinha, N. How perceived trust mediates merchant’s intention to use a mobile wallet technology. J. Retail. Consum. Serv. 2020, 52, 101894. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research; Addison-Wesley Publishing Company: Reading, MA, USA, 1975. [Google Scholar]

- Chin, A.G.; Harris, M.A.; Brookshire, R. An Empirical Investigation of Intent to Adopt Mobile Payment Systems Using a Trust-based Extended Valence Framework. Inf. Syst. Front. 2020, 1–19. [Google Scholar] [CrossRef]

- Koenig-Lewis, N.; Marquet, M.; Palmer, A.; Zhao, A.L. Enjoyment and social influence: Predicting mobile payment adoption. Serv. Ind. J. 2015, 35, 537–554. [Google Scholar] [CrossRef]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Thakur, R.; Srivastava, M. Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Res. 2014, 24, 369–392. [Google Scholar] [CrossRef]

- Sripalawat, J.; Thongmak, M.; Ngramyarn, A. M-banking in metropolitan bangkok and a comparison with other countries. J. Comput. Inf. Syst. 2011, 51, 67–76. [Google Scholar] [CrossRef]

- Leong, L.Y.; Hew, T.S.; Ooi, K.B.; Wei, J. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. Int. J. Inf. Manag. 2020, 51, 102047. [Google Scholar] [CrossRef]

- Goyal, A.; Maity, M.; Thakur, R.; Srivastava, M. Customer usage intention of mobile commerce in India: An empirical study. J. Indian Bus. Res. 2013, 5, 52–72. [Google Scholar] [CrossRef]

- Nel, J.; Boshoff, C. Traditional-bank customers’ digital-only bank resistance: Evidence from South Africa. Int. J. Bank Mark. 2020, 39, 429–454. [Google Scholar] [CrossRef]

- Ryan, R.M.; Deci, E.L. Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. Am. Psychol. 2000, 55, 68–78. [Google Scholar] [CrossRef]

- Liu, R.; Wu, J.; Yu-Buck, G.F. The influence of mobile QR code payment on payment pleasure: Evidence from China. Int. J. Bank Mark. 2021, 39, 337–356. [Google Scholar] [CrossRef]

- Kim, H.-W.; Kankanhalli, A. Investigating User Resistance to Information Systems Implementation: A Status Quo Bias Perspective. MIS Q. 2009, 33, 567. [Google Scholar] [CrossRef] [Green Version]

- Kuo, R.-Z. Why do people switch mobile payment service platforms? An empirical study in Taiwan. Technol. Soc. 2020, 62, 101312. [Google Scholar] [CrossRef]

- Boden, J.; Maier, E.; Wilken, R. The effect of credit card versus mobile payment on convenience and consumers’ willingness to pay. J. Retail. Consum. Serv. 2020, 52, 101910. [Google Scholar] [CrossRef]

- Iman, N. Is mobile payment still relevant in the fintech era? Electron. Commer. Res. Appl. 2018, 30, 72–82. [Google Scholar] [CrossRef]

- Ramadan, R.; Aita, J. A model of mobile payment usage among Arab consumers. Int. J. Bank Mark. 2018, 36, 1213–1234. [Google Scholar] [CrossRef]

- Sun, S.; Law, R.; Schuckert, M. Mediating effects of attitude, subjective norms and perceived behavioural control for mobile payment-based hotel reservations. Int. J. Hosp. Manag. 2020, 84, 102331. [Google Scholar] [CrossRef]

- Khan, A.N.; Cao, X.; Pitafi, A.H. Personality traits as predictor of M-payment systems: A sEM-neural networks approach. J. Organ. End User Comput. 2019, 31, 89–110. [Google Scholar] [CrossRef] [Green Version]

- Mallat, N. Exploring consumer adoption of mobile payments—A qualitative study. J. Strateg. Inf. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Kazancoglu, I.; Aydin, H. An investigation of consumers’ purchase intentions towards omni-channel shopping: A qualitative exploratory study. Int. J. Retail Distrib. Manag. 2018, 46, 959–976. [Google Scholar] [CrossRef]

- O’Neill, J.; Dhareshwar, A.; Muralidhar, S.H. Working Digital Money into a Cash Economy: The Collaborative Work of Loan Payment. Comput. Support. Coop. Work CSCW Int. J. 2017, 26, 733–768. [Google Scholar] [CrossRef]

- Kim, M.; Kim, S.; Kim, J. Can mobile and biometric payments replace cards in the Korean offline payments market? Consumer preference analysis for payment systems using a discrete choice model. Telemat. Inform. 2019, 38, 46–58. [Google Scholar] [CrossRef]

- Kar, A.K. What Affects Usage Satisfaction in Mobile Payments? Modelling User Generated Content to Develop the “Digital Service Usage Satisfaction Model”. Inf. Syst. Front. 2020, 1–21. [Google Scholar] [CrossRef]

- Chang, W.L.; Chen, L.M.; Hashimoto, T. Cashless Japan: Unlocking Influential Risk on Mobile Payment Service. Inf. Syst. Front. 2021, 1–14. [Google Scholar] [CrossRef] [PubMed]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M.W.L. An investigation of mobile payment (m-payment) services in Thailand. Asia-Pac. J. Bus. Adm. 2016, 8, 37–54. [Google Scholar] [CrossRef]

- Hampshire, C. A mixed methods empirical exploration of UK consumer perceptions of trust, risk and usefulness of mobile payments. Int. J. Bank Mark. 2017, 35, 354–369. [Google Scholar] [CrossRef] [Green Version]

- Rouibah, K.; Lowry, P.B.; Hwang, Y. The effects of perceived enjoyment and perceived risks on trust formation and intentions to use online payment systems: New perspectives from an Arab country. Electron. Commer. Res. Appl. 2016, 19, 33–43. [Google Scholar] [CrossRef]

- Pousttchi, K.; Schiessler, M.; Wiedemann, D.G. Proposing a comprehensive framework for analysis and engineering of mobile payment business models. Inf. Syst. E-Bus. Manag. 2009, 7, 363–393. [Google Scholar] [CrossRef]

- Liu, Z.; Ben, S.; Zhang, R. Factors affecting consumers’ mobile payment behavior: A meta-analysis. Electron. Commer. Res. 2019, 19, 575–601. [Google Scholar] [CrossRef]

- Al-Saedi, K.; Al-Emran, M.; Ramayah, T.; Abusham, E. Developing a general extended UTAUT model for M-payment adoption. Technol. Soc. 2020, 62, 101293. [Google Scholar] [CrossRef]

- Zhao, H.; Anong, S.T.; Zhang, L. Understanding the impact of financial incentives on NFC mobile payment adoption: An experimental analysis. Int. J. Bank Mark. 2019, 37, 1296–1312. [Google Scholar] [CrossRef]

- Singh, N.; Srivastava, S.; Sinha, N. Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. Int. J. Bank Mark. 2017, 35, 944–965. [Google Scholar] [CrossRef]

- Gao, S.; Yang, X.; Guo, H.; Jing, J. An Empirical Study on Users’ Continuous Usage Intention of QR Code Mobile Payment Services in China. Int. J. E-Adopt. 2018, 10, 18–33. [Google Scholar] [CrossRef]

- Yu, L.; Cao, X.; Liu, Z.; Gong, M.; Adee, L. Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Res. 2016, 28, 456–476. [Google Scholar] [CrossRef]

- Zhou, T. The effect of initial trust on user adoption of mobile payment. Inf. Dev. 2011, 27, 290–300. [Google Scholar] [CrossRef]

- Leong, L.Y.; Hew, T.S.; Tan, G.W.W.H.; Ooi, K.B. Predicting the determinants of the NFC-enabled mobile credit card acceptance: A neural networks approach. Expert Syst. Appl. 2013, 40, 5604–5620. [Google Scholar] [CrossRef]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M. User intentions to adopt mobile payment services: A study of early adopters in Thailand. J. Internet Bank. Commer. 2015, 20. Available online: https://www.icommercecentral.com/open-access/user-intentions-to-adopt-mobile-payment-services-a-study-of-early-adopters-in-thailand-.php?aid=50545&view=mobile (accessed on 24 November 2021).

- Ramos-de-Luna, I.; Montoro-Ríos, F.; Liébana-Cabanillas, F. Determinants of the intention to use NFC technology as a payment system: An acceptance model approach. Inf. Syst. E-Bus. Manag. 2016, 14, 293–314. [Google Scholar] [CrossRef]

- Su, P.; Wang, L.; Yan, J. How users’ Internet experience affects the adoption of mobile payment: A mediation model. Technol. Anal. Strateg. Manag. 2018, 30, 186–197. [Google Scholar] [CrossRef] [Green Version]

- Kumar, A.; Adlakaha, A.; Mukherjee, K. The effect of perceived security and grievance redressal on continuance intention to use M-wallets in a developing country. Int. J. Bank Mark. 2018, 36, 1170–1189. [Google Scholar] [CrossRef]

- Oney, E.; Guven, G.O.; Rizvi, W.H. The determinants of electronic payment systems usage from consumers’ perspective. Econ. Res. Istraz. 2017, 30, 394–415. [Google Scholar] [CrossRef] [Green Version]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Antecedents of the adoption of the new mobile payment systems: The moderating effect of age. Comput. Hum. Behav. 2014, 35, 464–478. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). Int. J. Inf. Manag. 2014, 34, 151–166. [Google Scholar] [CrossRef]

- Lwoga, E.T.; Lwoga, N.B. User Acceptance of Mobile Payment: The Effects of User-Centric Security, System Characteristics and Gender. Electron. J. Inf. Syst. Dev. Ctries. 2017, 81, 1–24. [Google Scholar] [CrossRef] [Green Version]

- Liébana-Cabanillas, F.; de Luna, I.R.; Montoro-Ríosa, F. Intention to use new mobile payment systems: A comparative analysis of SMS and NFC payments. Econ. Res. Istraz. 2017, 30, 892–910. [Google Scholar] [CrossRef]

- Francisco, L.C.; Francisco, M.L.; Juan, S.F. Payment systems in new electronic environments: Consumer behavior in payment systems via SMS. Int. J. Inf. Technol. Decis. Mak. 2015, 14, 421–449. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.J.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Role of gender on acceptance of mobile payment. Ind. Manag. Data Syst. 2014, 114, 220–240. [Google Scholar] [CrossRef]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Patil, P.; Tamilmani, K.; Rana, N.P.; Raghavan, V. Understanding consumer adoption of mobile payment in India: Extending Meta-UTAUT model with personal innovativeness, anxiety, trust, and grievance redressal. Int. J. Inf. Manag. 2020, 54, 102144. [Google Scholar] [CrossRef]

- Shaw, B.; Kesharwani, A. Moderating Effect of Smartphone Addiction on Mobile Wallet Payment Adoption. J. Internet Commer. 2019, 18, 291–309. [Google Scholar] [CrossRef]

- Gupta, K.; Arora, N. Investigating consumer intention to accept mobile payment systems through unified theory of acceptance model: An Indian perspective. South Asian J. Bus. Stud. 2020, 9, 88–114. [Google Scholar] [CrossRef]

- Jun, J.; Cho, I.; Park, H. Factors influencing continued use of mobile easy payment service: An empirical investigation. Total Qual. Manag. Bus. Excell. 2018, 29, 1043–1057. [Google Scholar] [CrossRef]

- Shankar, A.; Datta, B. Factors Affecting Mobile Payment Adoption Intention: An Indian Perspective. Glob. Bus. Rev. 2018, 19, S72–S89. [Google Scholar] [CrossRef]

- Humbani, M.; Wiese, M. A Cashless Society for All: Determining Consumers’ Readiness to Adopt Mobile Payment Services. J. Afr. Bus. 2018, 19, 409–429. [Google Scholar] [CrossRef] [Green Version]

- Pham, T.T.T.; Ho, J.C. The effects of product-related, personal-related factors and attractiveness of alternatives on consumer adoption of NFC-based mobile payments. Technol. Soc. 2015, 43, 159–172. [Google Scholar] [CrossRef]

- Mombeuil, C. An exploratory investigation of factors affecting and best predicting the renewed adoption of mobile wallets. J. Retail. Consum. Serv. 2020, 55, 102127. [Google Scholar] [CrossRef]

- Plouffe, C.R.; Vandenbosch, M.; Hulland, J. Intermediating technologies and multi-group adoption: A comparison of consumer and merchant adoption intentions toward a new electronic payment system. J. Prod. Innov. Manag. 2001, 18, 65–81. [Google Scholar] [CrossRef]

- Abdul-Hamid, I.K.; Shaikh, A.A.; Boateng, H.; Hinson, R.E. Customers’ perceived risk and trust in using mobile money services-an empirical study of Ghana. Int. J. E-Bus. Res. 2019, 15, 1–19. [Google Scholar] [CrossRef]

- Handarkho, Y.D.; Harjoseputro, Y. Intention to adopt mobile payment in physical stores: Individual switching behavior perspective based on Push–Pull–Mooring (PPM) theory. J. Enterp. Inf. Manag. 2020, 33, 285–308. [Google Scholar] [CrossRef]

- Chan, F.T.S.T.S.; Niu, B.; Pu, X.; Chan, F.T.S.T.S.; Chong, A.Y.L.; Niu, B. The adoption of NFC-based mobile payment services: An empirical analysis of Apple Pay in China. Int. J. Mob. Commun. 2020, 18, 343. [Google Scholar] [CrossRef]

- Arvidsson, N. Consumer attitudes on mobile payment services—Results from a proof of concept test. Int. J. Bank Mark. 2014, 32, 150–170. [Google Scholar] [CrossRef]

- Shin, D.H. Towards an understanding of the consumer acceptance of mobile wallet. Comput. Hum. Behav. 2009, 25, 1343–1354. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Muñoz-Leiva, F.; Sánchez-Fernández, J. A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment. Serv. Bus. 2018, 12, 25–64. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Consumer attitude and intention to adopt mobile wallet in India—An empirical study. Int. J. Bank Mark. 2019, 37, 1590–1618. [Google Scholar] [CrossRef]

- Chen, K.Y.; Chang, M.L. User acceptance of “near field communication” mobile phone service: An investigation based on the “unified theory of acceptance and use of technology” model. Serv. Ind. J. 2013, 33, 609–623. [Google Scholar] [CrossRef]

- Shin, D.H. Modeling the interaction of users and mobile payment system: Conceptual framework. Int. J. Hum. Comput. Interact. 2010, 26, 917–940. [Google Scholar] [CrossRef]

- Flavian, C.; Guinaliu, M.; Lu, Y. Mobile payments adoption—Introducing mindfulness to better understand consumer behavior. Int. J. Bank Mark. 2020, 38, 1575–1599. [Google Scholar] [CrossRef]

- Di Pietro, L.; Guglielmetti Mugion, R.; Mattia, G.; Renzi, M.F.; Toni, M. The Integrated Model on Mobile Payment Acceptance (IMMPA): An empirical application to public transport. Transp. Res. Part C Emerg. Technol. 2015, 56, 463–479. [Google Scholar] [CrossRef]

- Ooi, K.B.; Tan, G.W.H. Mobile technology acceptance model: An investigation using mobile users to explore smartphone credit card. Expert Syst. Appl. 2016, 59, 33–46. [Google Scholar] [CrossRef]

- Lew, S.; Tan, G.W.H.; Loh, X.M.; Hew, J.J.; Ooi, K.B. The disruptive mobile wallet in the hospitality industry: An extended mobile technology acceptance model. Technol. Soc. 2020, 63, 101430. [Google Scholar] [CrossRef]

- Oztruk, A.B. Customer acceptance of cashless payment systems in the hospitality industry. Int. J. Contemp. Hosp. Manag. 2016, 28, 1–23. [Google Scholar] [CrossRef]

- Sharma, S.K.; Sharma, H.; Dwivedi, Y.K. A Hybrid SEM-Neural Network Model for Predicting Determinants of Mobile Payment Services. Inf. Syst. Manag. 2019, 36, 243–261. [Google Scholar] [CrossRef]

- Kalinić, Z.; Liébana-Cabanillas, F.J.; Muñoz-Leiva, F.; Marinković, V. The moderating impact of gender on the acceptance of peer-to-peer mobile payment systems. Int. J. Bank Mark. 2020, 38, 138–158. [Google Scholar] [CrossRef]

- Liu, Y.; Wang, M.; Huang, D.; Huang, Q.; Yang, H.; Li, Z. The impact of mobility, risk, and cost on the users’ intention to adopt mobile payments. Inf. Syst. E-Bus. Manag. 2019, 17, 319–342. [Google Scholar] [CrossRef]

- Pal, A.; Herath, T.; De, R.; Rao, H.R. Is the Convenience Worth the Risk? An Investigation of Mobile Payment Usage. Inf. Syst. Front. 2020. [Google Scholar] [CrossRef]

- Thakur, R. Customer Adoption of Mobile Payment Services by Professionals across two Cities in India: An Empirical Study Using Modified Technology Acceptance Model. Bus. Perspect. Res. 2013, 1, 17–30. [Google Scholar] [CrossRef] [Green Version]