Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation

Abstract

1. Introduction

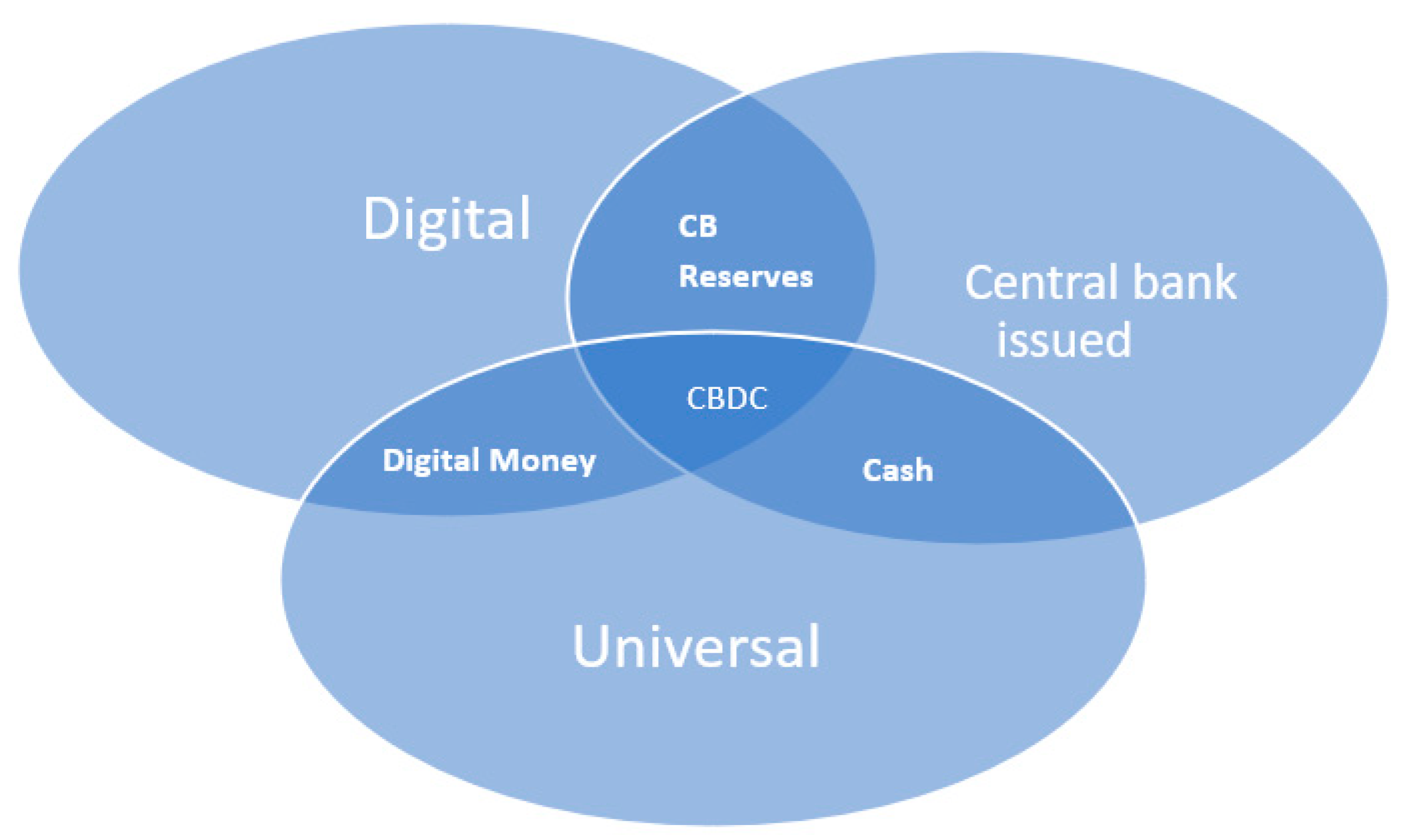

2. Literature Review: Definition of CBDCs, Differences with Cash and Cryptocurrencies

- -

- Emulate the characteristics of cash (if held by the public).

- -

- Serve as a central bank reserve (if held only by banks and other financial intermediaries that have access to the payment system).

- -

- A database in which the CBDC is registered.

- -

- An application through which payments with the CBDC are executed.

3. Materials and Methods

3.1. Materials

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reason for Establishing a CBDC | Associated Variable |

|---|---|

| Geographic dispersion | Inhab/km2 |

| Access to financial services | Commercial bank branches (per 100,000 adults) |

| Increase the banking penetration rate | Financial sector credit to the private sector (% of GDP) |

| Financial sector does not become obsolete | Digital Readiness Index |

| Security reasons: avoid money laundering and terrorism financing | Shadow economy, percent of GDP |

| Consumer protection | UNCTAD B2C E-commerce Index |

| Maintain control over monetary and macroeconomic policy Fall in use of cash (alternative) | Corresponding CB speech Broad money (% of GDP) |

| Lower costs and increased efficiency of the banking system Central Bank Speech Public interest/CBDC 1 Public interest/CBDC 2 | CB speech on CBDC CB speech on CBDC Search interest Keyword “CBDC” (2013–2020) annual average of the period. Search Interest topic “CBDC” (2013–2020) annual average of the period |

3.2. Methodology

3.2.1. Pearson’s Correlation

3.2.2. Correlation by Spearman’s Rho

3.2.3. Kendall Tau-b Correlation

4. Results

5. Discussion of Results: Central Bank Digital Currency, and Payment Industry Open Innovation

5.1. Discussion: The Way of Central Bank Digital Currency

5.2. Discussion: CBDC and Its Implication for Payment Industry Open Innovation

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Country/Reason for Establishing CBDC | Geographic Dispersion | Access to Financial Services | Increase the Banking Penetration Rate | Financial Sector Not to Become Obsolete | Security Reasons: Avoid Money Laundering and Terrorist Financing | Consumer Protection | Maintain Control over Monetary and Macroeconomic Policy | Fall in Use of Cash (Alternative) | Lower Costs and Greater Efficiency of the Banking System | Central Bank Speech | Public Interest/CBDC 1 | Public Interest/CBDC 2 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable | Inhab/km2 | Commercial bank branches (per 100,000 adults) | Financial sector credit to the private sector (% of GDP) | Digital Readiness Index | Shadow economy, percent of GDP | UNCTAD B2C E-commerce Index | Corresponding CB speech | Broad money (% of GDP) | CB speech on CBDC | CB speech on CBDC | Search interest Keyword “CBDC” (2013–2020) Annual average of the period | Search Interest topic “CBDC” (2013–2020) Annual average of the period |

| Australia | 3.2 | 28.2 | 135.8 | 17.89 | 8.1 | 92 | 1 | 122.6 | 0 | 0 | 59.8 | 48.3 |

| Bahamas | 38.5 | 24.4 | 45.2 | 12.74 | 38.55 | 65 | 0 | 55.7 | 1 | 4 | ||

| Brazil | 25.1 | 18.7 | 67.3 | 12.31 | 35.22 | 62 | 0 | 98.2 | 1 | 0 | 141.5 | 154.4 |

| Canada | 4.1 | 19.6 | 17.33 | 9.42 | 92 | 1 | 122.9 | 0 | 0 | 573.9 | 461.4 | |

| China | 148.3 | 8.9 | 164.7 | 13.22 | 12.11 | 60 | 1 | 197 | 0 | 2 | 39.4 | 94 |

| South Korea | 529.4 | 15.1 | 151.7 | 18.22 | 19.83 | 84.3 | 0 | 151.8 | 0 | 4 | 108.6 | 126.1 |

| Ecuador | 68.8 | 10.1 | 40.2 | 11.29 | 30.18 | 41 | 0 | 29.8 | 0 | 0 | ||

| Spain | 93.7 | 49.7 | 94.7 | 15.74 | 22.01 | 80 | 1 | 65.8 | 1 | 0 | 109.1 | 106.1 |

| United States of America | 35.7 | 30.5 | 51.9 | 19.03 | 7 | 87 | 1 | 92.8 | 0 | −1 | 163.6 | 152.8 |

| Estonia | 30.4 | 8.9 | 59 | 17.14 | 18.49 | 90 | 1 | 65.8 | 1 | 0 | ||

| Eurozone | 111.8 | 22 | 86.3 | 16.3 | 17.02 | 1 | 65.8 | 1 | 0 | |||

| Philippines | 357.7 | 9.2 | 48 | 11.03 | 28.04 | 40 | 0 | 76.6 | 1 | 4 | 55.6 | 79 |

| Finland | 18.1 | 3.1 | 95.1 | 17.95 | 13.3 | 93 | 1 | 65.8 | 1 | −4 | ||

| France | 122.3 | 34.3 | 107.6 | 16.25 | 11.65 | 90 | 1 | 65.8 | 1 | 2 | 141.5 | 134.8 |

| Ghana | 130.8 | 8.5 | 12.4 | 9.55 | 39.37 | 35 | 0 | 26.9 | 0 | 0 | ||

| India | 454.9 | 14.6 | 50.2 | 9.46 | 17.89 | 44 | 1 | 76.1 | 0 | 0 | 329.8 | 160.4 |

| Indonesia | 147.8 | 15.6 | 32.5 | 11.68 | 21.76 | 36 | 1 | 38.8 | 1 | 0 | 189 | 166.6 |

| Iceland | 3.5 | 30.5 | 90.6 | 18.16 | 12.45 | 93 | 1 | 66.4 | 0 | 0 | 365.1 | 160.4 |

| Israel | 410.5 | 16.8 | 65.4 | 16.67 | 19.18 | 81 | 1 | 86.8 | 1 | 0 | 43.5 | 27.3 |

| Jamaica | 271 | 7.3 | 41.3 | 11.55 | 24.97 | 65 | 1 | 50.1 | 1 | 0 | ||

| Japan | 347.1 | 33.9 | 111.2 | 17.69 | 8.19 | 93.6 | 1 | 255 | 0 | −2 | 63.3 | 109.8 |

| Kuwait | 232.2 | 23.2 | 89.3 | 13.36 | 21.72 | 63 | 1 | 101.5 | 0 | 4 | ||

| Lithuania | 44.7 | 10.4 | 38.9 | 14.78 | 18.65 | 79 | 1 | 65.8 | 1 | 1 | ||

| Madagascar | 45.1 | 2.4 | 14.2 | 6.48 | 45.29 | 29 | 0 | 24.6 | 0 | 0 | ||

| Malaysia | 96 | 10.1 | 120.9 | 14.31 | 26.07 | 77 | 1 | 123.1 | 0 | 1 | 62.4 | 79.5 |

| Norway | 14.5 | 128.4 | 17.98 | 15.07 | 96.39 | 1 | 66.2 | 0 | 0 | |||

| New Zealand | 18.4 | 25.4 | 146 | 17.75 | 8.97 | 93 | 1 | 103.8 | 1 | −2 | ||

| Netherlands | 511.5 | 9.2 | 100 | 18.66 | 7.83 | 95.9 | 1 | 65.8 | 1 | 0 | 142.8 | 123.4 |

| United Kingdom | 274.7 | 133.6 | 17.86 | 8.32 | 95.1 | 1 | 141.8 | 0 | 0 | 174 | 98.4 | |

| Russia | 8.8 | 25.6 | 52.4 | 13.63 | 33.72 | 71 | 1 | 58.6 | 1 | 0 | 76 | 95 |

| Senegal | 82.3 | 5.8 | 29.3 | 8.11 | 33.68 | 30 | 0 | 41.2 | 0 | 0 | ||

| Swaziland | 66.1 | 7 | 20.9 | 40.94 | 29 | 0 | 28.4 | 0 | 0 | |||

| South Africa | 47.6 | 9.6 | 66.7 | 11.39 | 21.99 | 54 | 0 | 74.1 | 0 | 0 | ||

| Sweden | 25 | 16.4 | 132.7 | 18.42 | 11.74 | 94.6 | 0 | 74.5 | 1 | 3 | 40.9 | 51.4 |

| Switzerland | 215.5 | 38.4 | 18.86 | 6.94 | 96.43 | 0 | 189.3 | 1 | 4 | |||

| Trinidad and Tobago | 270.9 | 11.5 | 40.1 | 12.59 | 31.4 | 47.5 | 0 | 67.4 | 0 | 0 | ||

| Tunisia | 74.4 | 22.1 | 64 | 10.87 | 30.9 | 47 | 0 | 74.2 | 0 | 0 | ||

| Ukraine | 77 | 0.4 | 22.8 | 11.47 | 42.9 | 60 | 0 | 36.2 | 1 | 0 | ||

| Uruguay | 19.7 | 10 | 28.1 | 13.88 | 20.38 | 59 | 0 | 54.2 | 0 | 0 |

| N | Minimum | Maximum | Mean | Mean Deviation Variance | |

|---|---|---|---|---|---|

| Australia | 12 | 0.00 | 135.80 | 43.0742 | 49.33454 |

| Bahamas | 10 | 0.00 | 65.00 | 28.5090 | 23.53701 |

| Brazil | 12 | 0.00 | 154.40 | 51.3108 | 54.48703 |

| Canada | 10 | 0 | 574 | 130.16 | 210.077 |

| China | 11 | 1 | 197 | 67.33 | 72.428 |

| South Korea | 12 | 0.00 | 529.40 | 100.7542 | 147.79425 |

| Ecuador | 10 | 0.00 | 68.80 | 23.1370 | 22.86584 |

| Spain | 12 | 0.00 | 109.10 | 53.2375 | 43.51692 |

| United States of America | 12 | −1.00 | 163.60 | 53.3608 | 58.33803 |

| Estonia | 10 | 0.00 | 90.00 | 29.1730 | 31.69478 |

| Eurozone | 9 | 0.00 | 111.80 | 35.6911 | 41.61316 |

| Philippines | 12 | 0.00 | 357.70 | 59.1808 | 98.18086 |

| Finland | 10 | −4.00 | 95.10 | 30.4350 | 38.89312 |

| France | 12 | 1.00 | 141.50 | 60.6833 | 56.04434 |

| Ghana | 10 | 0.00 | 130.80 | 26.2520 | 39.48668 |

| India | 12 | 0.00 | 454.90 | 96.5292 | 147.85946 |

| Indonesia | 12 | 0.00 | 189.00 | 55.1450 | 69.76761 |

| Iceland | 12 | 0.00 | 365.10 | 70.0925 | 105.64317 |

| Israel | 12 | 0.00 | 410.50 | 64.0958 | 113.27797 |

| Jamaica | 10 | 0.00 | 271.00 | 47.3220 | 81.85365 |

| Japan | 12 | −2.00 | 347.10 | 86.5650 | 110.49680 |

| Kuwait | 10 | 0.00 | 232.20 | 54.9280 | 72.41640 |

| Lithuania | 9 | 1 | 79 | 30.48 | 28.286 |

| Madagascar | 10 | 0.00 | 45.29 | 16.7070 | 18.22546 |

| Malaysia | 12 | 0.00 | 123.10 | 50.9483 | 47.64363 |

| Norway | 8 | 0 | 128 | 42.45 | 48.564 |

| New Zealand | 10 | −2.00 | 146.00 | 41.3320 | 52.74819 |

| Netherlands | 12 | 0.00 | 511.50 | 89.7575 | 142.89136 |

| United Kingdom | 11 | 0.00 | 274.70 | 85.8891 | 90.36690 |

| Russia | 12 | 0.00 | 95.00 | 36.3958 | 33.28043 |

| Senegal | 8 | 0 | 82 | 28.80 | 26.264 |

| Swaziland | 9 | 0.00 | 66.10 | 21.3711 | 22.55034 |

| South Africa | 10 | 0.00 | 74.10 | 28.5380 | 29.21708 |

| Sweden | 11 | 1 | 133 | 42.69 | 42.137 |

| Switzerland | 8 | 1 | 216 | 71.30 | 86.845 |

| Trinidad and Tobago | 10 | 0.00 | 270.90 | 48.1390 | 81.57949 |

| Tunisia | 8 | 0 | 74 | 40.44 | 28.851 |

| Ukraine | 10 | 0.00 | 77.00 | 25.1770 | 27.87591 |

| Uruguay | 8 | 0.00 | 59.00 | 25.6625 | 20.82992 |

| Frequency | Percentage | Valid Percentage | Cumulative Percentage | |

|---|---|---|---|---|

| Broad money (% of GDP) | 1 | 8.3 | 8.3 | 8.3 |

| Financial sector credit to the private sector (% of GDP) | 1 | 8.3 | 8.3 | 16.7 |

| Digital Readiness Index 2019 | 1 | 8.3 | 8.3 | 25.0 |

| CB’s discourse on CBDC | 1 | 8.3 | 8.3 | 33.3 |

| Inhab/km2 (2018) | 1 | 8.3 | 8.3 | 41.7 |

| Shadow economy, percent of GDP, 2015 | 1 | 8.3 | 8.3 | 50.0 |

| CB speech on CBDC | 2 | 16.7 | 16.7 | 66.7 |

| Search interest Keyword “CBDC” (2013–2020) annual average of the period | 1 | 8.3 | 8.3 | 75.0 |

| Search Interest topic “CBDC” (2013–2020) Annual average of the period | 1 | 8.3 | 8.3 | 83.3 |

| Commercial bank branches (per 100,000 adults) | 1 | 8.3 | 8.3 | 91.7 |

| UNCTAD B2C E-commerce Index, Index | 1 | 8.3 | 8.3 | 100.0 |

| Total | 12 | 100.0 | 100.0 |

References

- Chohan, U.W. A History of Bitcoin. SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Vigna, P.; Casey, M.J. The Age of Cryptocurrency: How Bitcoin and Digital Money Are Challenging the Global Economic Order; St. Martin’s Press: London, UK, 2015. [Google Scholar]

- Fung, E.W.; Siu-Cheong, B. Central Bank Digital Currency: Motivations and Implications; Bank of Canada, Ed.; Bank of Canada: Ottawa, ON, Canada, 2017; Available online: https://www.econstor.eu/bitstream/10419/200452/1/1008638439.pdf (accessed on 21 December 2020).

- Aste, T. Cryptocurrency market structure: Connecting emotions and economics. Digit. Financ. 2019, 1, 5–21. [Google Scholar] [CrossRef]

- Gkillas, K.; Bekiros, S.; Siriopoulos, C. Extreme Correlation in Cryptocurrency Markets. SSRN Electron. J. 2018. [Google Scholar] [CrossRef]

- De Lis, S.F.; Sebastián, J. Central Bank Digital Currencies and Distributed Ledger Technology; BBVA Research: Madrid, Spain, 2019; p. 5. Available online: http://www.bbvaresearch.com/publicaciones/las-monedas-virtuales-de-bancos-centrales-y-la-tecnologia-de-contabilidad-distribuida/ (accessed on 8 December 2020).

- Fung, E.W.; Siu-Cheong, B.; Hendry, S. Is a Cashless Society Problematic? Bank of Canada, Ed.; Bank of Canada: Ottawa, ON, Canada, 2018; Available online: https://www.bankofcanada.ca/wp-content/uploads/2018/10/sdp2018-12.pdf (accessed on 11 December 2020).

- Tercero-Lucas, D. A Global Digital Currency to Rule Them All? A Monetary-Financial View of the Facebook’s LIBRA for the Euro Area; GEAR-Graduate in Applied Economic Research-Departamento de Economí a Aplicada UAB, Ed.; Universitat Autónoma de Barcelona: Barcelona, Spain; Available online: https://ddd.uab.cat/pub/worpap/2020/232413/Gear_wp_2020_06_b.pdf (accessed on 3 December 2020).

- Alonso, S.L.N.; Fernández, M.; Ángel, E.; Bas, D.S.; Kaczmarek, J. Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review. Economies 2020, 8, 41. [Google Scholar] [CrossRef]

- Rogoff, K.S. The Curse of Cash: How Large-Denomination Bills Aid Crime and Tax Evasion and Constrain Monetary Policy; Princeton University Press: Princeton, NJ, USA, 2017. [Google Scholar]

- Alonso, S.L.N. Activities and Operations with Cryptocurrencies and Their Taxation Implications: The Spanish Case. Laws 2019, 8, 16. [Google Scholar] [CrossRef]

- Kumhof, M.; Noone, C. Central Bank Digital Currencies—Design Principles and Balance Sheet Implications Bank of England Working Paper No. 725; Bank of England: London, UK, 2018; Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3180713 (accessed on 21 December 2020).

- Bank of England. Central Bank Digital CurrencyOpportunities, Challenges and Design; Bank of England: London, UK, 2020; Available online: https://www.bankofengland.co.uk/-/media/boe/files/paper/2020/central-bank-digital-currency-opportunities-challenges-and-design.pdf (accessed on 21 December 2020).

- Panetta, F. 21st Century Cash: Central Banking, Technological innovation, and Digital Currencies. In Do We Need Central Bank Digital Currency? Economics, Technology, and Institutions; Gnan, E., Masciandaro, D., Eds.; Bocconi University and BAFFI CAREFIN: Vienna, Austria, 2018; pp. 28–31. Available online: https://iris.unibocconi.it/retrieve/handle/11565/4014058/92065/Masciandaro%20SUERF%20book%20%2b%20SUERF%20book%20chapter.pdf (accessed on 4 December 2020).

- Meaning, J.; Dyson, B.; Barker, J.; Clayton, E. Broadening Narrow Money: Monetary Policy with a Central Bank Digital Currency. SSRN Electron. J. 2018. [Google Scholar] [CrossRef]

- Bindseil, U. Central Bank Digital Currency: Financial System Implications and Control. Int. J. Political Econ. 2019, 48, 303–335. [Google Scholar] [CrossRef]

- Auer, R.; Böhme, R. The Technology of Retail Central Bank Digital Currency; BIS Quarterly Review; BIS: Basel, Switzerland, March 2020; Available online: https://ssrn.com/abstract=3561198 (accessed on 25 November 2020).

- Ward, O.; Rochemont, S. Understanding Central Bank Digital Currencies (CBDC). Inst. Fac. Actuar. 2019. Available online: https://cointhinktank.com/upload/CBDC%20-%20Understanding%20CBDCs.pdf (accessed on 23 February 2021).

- Carney, M. The Future of Money; Bank of England, Ed.; Bloomberg HQ: London, UK; Available online: https://www.bankofengland.co.uk/-/media/boe/files/speech/2018/the-future-of-money-slides.pdf (accessed on 23 December 2020).

- Frost, J.; Shin, H.S.; Wierts, P. An Early Stablecoin? The Bank of Amsterdam and the Governance of Money. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Moin, A.; Sekniqi, K.; Sirer, E.G. SoK: A Classification Framework for Stablecoin Designs. arXiv 2020, arXiv:1910.10098. [Google Scholar]

- de Lis, S.F.; Gouveia, O. Monedas Digitales Emitidas Por Bancos Centrales: Características, Opciones, Ventajas Y Desventajas. Documento De Trabajo. Madrid: BBVA Research. 2019. Available online: https://www.bbvaresearch.com/wp-content/uploads/2019/03/WP_Monedas-digitales-emitidas-por-bancos-centrales-ICO.pdf (accessed on 23 December 2020).

- Raskin, M.; Yermack, D. Digital Currencies, Decentralized Ledgers, And The Future Of Central Banking; NBER Working Paper Series; National Bureau of Economic Research: Cambridge, MA, USA, 2016; Available online: http://www.nber.org/papers/w22238 (accessed on 15 December 2020).

- Niepelt, D. Reserves For All? Central Bank Digital Currency, Deposits, And Their (Non)-Equivalence. Cesifo Working Papers; Munich Society for the Promotion of Economic Research—CESifo GmbH: Munich, Germany, 2018; Available online: http://www.CESifo-group.org/wp (accessed on 24 November 2020).

- Bordo, M.; Levin, A. Central Bank Digital Currency And The Future of Monetary Policy; NBER Working Papers; National Bureau of Economic Research: Cambridge, MA, USA, 2017; Available online: http://www.nber.org/papers/w23711 (accessed on 15 November 2020).

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Detection of Financial Inclusion Vulnerable Rural Areas through an Access to Cash Index: Solutions Based on the Pharmacy Network and a CBDC. Evidence Based on Ávila (Spain). Sustainability 2020, 12, 7480. [Google Scholar] [CrossRef]

- Auer, R.; Cornelli, G.; Frost, J. Rise of the Central Bank Digital Currencies: Drivers, Approaches and Technologies; Bank for International Settlements, Ed.; Bank for International Settlements: Basel, Switzerland, 2020; pp. 20–21. Available online: https://www.bis.org/publ/work880.pdf (accessed on 26 December 2020).

- The World Bank. Population Density (People Per sq. km of Land Area). 2020. Available online: https://data.worldbank.org/indicator/EN.POP.DNST (accessed on 22 January 2021).

- The World Bank. Commercial Bank Branches (Per 100,000 Adults). 2020. Retrieved 22 January 2021, from The World Bank. Available online: https://data.worldbank.org/indicator/FB.CBK.BRCH.P5 (accessed on 22 January 2021).

- The World Bank. Monetary Sector Credit to Private Sector (% GDP). 2020. Available online: https://data.worldbank.org/indicator/FM.AST.PRVT.GD.ZS?end=2019&start=2018 (accessed on 22 January 2021).

- Cisco. Cisco Digital Readiness 2019. 2020. Available online: https://www.cisco.com/c/m/en_us/about/corporate-social-responsibility/research-resources/digital-readiness-index.html#/ (accessed on 22 January 2021).

- United Nations. Technical Notes on ICT for Development N° 15; United Nations Conference on Trade and Development: Geneva, Switzerland, 2019; Available online: https://unctad.org/system/files/official-document/tn_unctad_ict4d15_en.pdf (accessed on 8 December 2020).

- Arvidsson, N.; Hedman, J.; Segendorf, B. Cashless Society: When Will Merchants Stop Accepting Cash in Sweden—A Research Model. In Enterprise Applications, Markets and Services in the Finance Industry; Lecture Notes in Business Information Processing; Feuerriegel, S., Neumann, D., Eds.; Springer: Cham, Switzerland, 2017; Volume 276, Available online: https://doi.org/10.1007/978-3-319-52764-2_8 (accessed on 11 November 2020).

- Fabris, N. Cashless Society—The Future of Money or a Utopia? J. Central Bank. Theory Pr. 2019, 8, 53–66. [Google Scholar] [CrossRef]

- The World Bank. Broad Money (% of GDP). 2020. Available online: https://data.worldbank.org/indicator/FM.LBL.BMNY.GD.ZS (accessed on 22 January 2021).

- Santabárbara, J. Cálculo del tamaño de muestra necesario para estimar el coeficiente de correlación de Pearson mediante sintaxis en SPSS. REIRE Rev. d’Innovació Recer. Educ. 2021, 14. [Google Scholar] [CrossRef]

- Suárez, I.; Mario, O. Coeficiente de Correlación de Karl Pearson. Available online: http://repositorio.utn.edu.ec/handle/123456789/766 (accessed on 24 January 2021).

- Gross, J. CBDC Pioneers: Which Countries are Currently Testing a Retail Central Bank Digital Currency? Available online: https://jonasgross.medium.com/cbdc-pioneers-which-countries-are-currently-testing-a-retail-central-bank-digital-currency-49333be477f4 (accessed on 20 June 2020).

- Kim, G. Why is China going to issue CBDC (Central Bank Digital Currency)? J. Internet Electron. Commer. Res. 2020, 20, 161–177. [Google Scholar] [CrossRef]

- Chorzempa, M. China, the United States, and central bank digital currencies: How important is it to be first? China Econ. J. 2021, 1–14. [Google Scholar] [CrossRef]

- Berkmen, P.; Beaton, K.; Gershenson, D.; Del Granado, J.A.; Ishi, K.; Kim, M.; Kopp, E.; Rousset, M. Fintech in Latin America and the Caribbean: Stocktaking. IMF Work. Pap. 2019, 19, 1. [Google Scholar] [CrossRef]

- Wilson, M.P. El Billete Electrónico Emitido Por El BCU: Avance En Su Aplicación; Lecture, VII Jornadas de Derecho Bancocentralista; Montevideo, Uruguay; Available online: https://www.bcu.gub.uy/Comunicaciones/DraMariaPazWilson.ppt (accessed on 7 December 2020).

- Anderson, D.R.; Sweeney, D.J.; Williams, T.A.; Camm, J.D.; Cochran, J.J. Statistics for Business & Economics. Cengage Learning. 2016. Available online: https://www.cengage.com/c/statistics-for-business-economics-14e-anderson/9781337901062/ (accessed on 23 February 2021).

- Suárez, I.; Mario, O. Probabilidades y Estadística Empleando las TIC. Available online: http://repositorio.utn.edu.ec/handle/123456789/8698 (accessed on 24 January 2021).

- Keller, G. Statistics for Management and Economics, 10th ed.; Cengage Learning: Boston, MA, USA, 2014. [Google Scholar]

- Barrera, M.A.M. Uso de la correlación de spearman en un estudio de intervención en fisioterapia. Movimiento Científico 2014, 8, 98–104. [Google Scholar] [CrossRef]

- Zhang, L.; Lu, D.; Wang, X. Measuring and testing interdependence among random vectors based on Spearman’s ρ and Kendall’s τ. Comput. Stat. 2020, 35, 1685–1713. [Google Scholar] [CrossRef]

- Brossart, D.F.; Laird, V.C.; Armstrong, T.W.; Walla, P. Interpreting Kendall’s Tau and Tau-U for single-case experimental designs. Cogent Psychol. 2018, 5, 1518687. [Google Scholar] [CrossRef]

- European Central Bank. European Central Bank: Survey Digital Euro. Available online: https://epsilon.escb.eu/limesurvey3/434111?lang=en (accessed on 26 January 2021).

- European Central Bank. ECB Consultation on Digital Euro Ends with Record Number of Responses to Public Consultation. European Central Bank, Directorate General Communications Division Global Media Relations Division. Available online: https://www.bde.es/f/webbde/GAP/Secciones/SalaPrensa/ComunicadosBCE/NotasInformativasBCE/21/presbce2021_11.pdf (accessed on 12 December 2020).

- Fernández, M.Á.E.; Bas, D.S.; Alonso, S.L.N. Ventajas e inconvenientes de las divisas virtuales centralizadas (CBDC): Un análisis de la propuesta del Euro Digital. In XIII Congreso de Economía Austriaca; de Mariana, I.J., Marroquín, U.F., Carlos, U.R.J., Eds.; Instituto Juan de Mariana: Madrid, Spain; pp. 50–66. Available online: https://www.juandemariana.org/investigacion/archivo-de-publicaciones/revista-del-xiii-congreso-de-economia-austriaca (accessed on 24 December 2020).

- Blockchain, O. China Aspira a Que Los Yuanes Digitales se usen Como Moneda de Reserva. Available online: https://observatorioblockchain.com/cbdc/banco-de-china-volvera-a-repartir-yuanes-digitales-en-ciudades-para-probar-su-cbdc/ (accessed on 26 January 2021).

- Banque Centrale des Etats de l’Afrique de l’Ouest (BCEAO). Etablissements de Monnaie Electronique. Available online: https://www.bceao.int/fr/content/etablissements-de-monnaie-electronique (accessed on 4 January 2021).

- Vázquez, J.J.; Cebolla, M.P.C.; Ramos, F.S. La transformación digital en el sector cooperativo agroalimentario español: Situación y perspectivas. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2019, 95, 39–70. [Google Scholar] [CrossRef]

- Alonso, S.L.N. The Tax Incentives in the IVTM and “Eco-Friendly Cars”: The Spanish Case. Sustainability 2020, 12, 3398. [Google Scholar] [CrossRef]

- Alonso, S.L.N.; Forradellas, R.R. Tax Incentives in Rural Environment as Economic Policy and Population Fixation. Case study of Castilla-León Region. In Business, Economics and Science Common Challenges; Bernat, T., Duda, J., Eds.; Filodiritto Editore: Bologna, Italy, 2020; pp. 205–210. [Google Scholar]

- Lee, M.; Garratt, R. Monetizing Privacy. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- The Central Bank of the Bahamas. Key Players Sand Dollar—Bahamas. Available online: https://www.sanddollar.bs/keyplayers (accessed on 18 February 2021).

- Chan, S.; Chu, J.; Zhang, Y.; Nadarajah, S. Blockchain and Cryptocurrencies. J. Risk Financial Manag. 2020, 13, 227. [Google Scholar] [CrossRef]

- Polyviou, A.; Velanas, P.; Soldatos, J. Blockchain Technology: Financial Sector Applications Beyond Cryptocurrencies. Proceedings 2019, 28, 7. [Google Scholar] [CrossRef]

| Bahamas Pearson’s Correlation | China Pearson’s Correlation | Uruguay Pearson’s Correlation | |||

|---|---|---|---|---|---|

| Lithuania | 0.930 | Switzerland | 0.954 | Lithuania | 0.956 |

| Uruguay | 0.924 | Malaysia | 0.950 | Estonia | 0.951 |

| Estonia | 0.921 | Tunisia | 0.929 | United States | 0.937 |

| Russia | 0.918 | South Africa | 0.922 | Canada | 0.924 |

| South Africa | 0.901 | Eurozone | 0.891 | Bahamas | 0.924 |

| Brazil | 0.894 | Japan | 0.850 | Russia | 0.905 |

| United States | 0.886 | Kuwait | 0.772 | Brazil | 0.882 |

| Spain | 0.838 | New Zealand | 0.743 | Finland | 0.827 |

| Malaysia | 0.832 | United Kingdom | 0.730 | South Africa | 0.819 |

| Finland | 0.829 | Lithuania | 0.706 | Iceland | 0.793 |

| Iceland | 0.807 | Ecuador | 0.701 | Australia | 0.751 |

| Tunisia | 0.792 | Australia | 0.699 | New Zealand | 0.715 |

| Canada | 0.780 | Senegal | 0.675 | Malaysia | 0.709 |

| Eurozone | 0.777 | South Korea | 0.673 | Sweden | 0.699 |

| Ecuador | 0.774 | Bahamas | 0.669 | Norway | 0.676 |

| Ukraine | 0.770 | Sweden | 0.664 | Tunisia | 0.656 |

| France | 0.769 | Finland | 0.663 | Spain | 0.585 |

| New Zealand | 0.764 | Estonia | 0.662 | China | 0.569 |

| Sweden | 0.754 | Spain | 0.637 | Ukraine | 0.555 |

| Australia | 0.753 | Norway | 0.615 | Switzerland | 0.549 |

| Norway | 0.743 | France | 0.603 | Eurozone | 0.531 |

| Madagascar | 0.714 | Trinidad and Tobago | 0.575 | France | 0.525 |

| China | 0.669 | Uruguay | 0.569 | Ecuador | 0.455 |

| Switzerland | 0.661 | Philippines | 0.558 | Japan | 0.422 |

| Swaziland | 0.659 | Israel | 0.552 | Madagascar | 0.410 |

| United Kingdom | 0.620 | Jamaica | 0.542 | Senegal | 0.364 |

| Japan | 0.596 | Ukraine | 0.537 | United Kingdom | 0.327 |

| Kuwait | 0.564 | Netherlands | 0.528 | Kuwait | 0.281 |

| Senegal | 0.549 | Swaziland | 0.527 | Swaziland | 0.272 |

| Indonesia | 0.465 | Ghana | 0.454 | Indonesia | 0.150 |

| Ghana | 0.446 | Brazil | 0.438 | South Korea | 0.144 |

| South Korea | 0.428 | Madagascar | 0.428 | Jamaica | 0.132 |

| Jamaica | 0.410 | India | 0.400 | Ghana | 0.120 |

| Trinidad and Tobago | 0.406 | Russia | 0.384 | Israel | 0.118 |

| Israel | 0.392 | United States | 0.369 | Trinidad and Tobago | 0.117 |

| Netherlands | 0.355 | Indonesia | 0.316 | Netherlands | 0.075 |

| Philippines | 0.343 | Canada | 0.169 | Philippines | 0.057 |

| India | 0.306 | Iceland | 0.097 | India | 0.028 |

| Bahamas Rho Spearman Correlation Coefficient | China Rho Spearman Correlation Coefficient | Uruguay Rho Spearman Correlation Coefficient | |||

|---|---|---|---|---|---|

| Uruguay | 0.976 | Malaysia | 0.989 | Bahamas | 0.976 |

| Brazil | 0.942 | South Africa | 0.962 | Estonia | 0.976 |

| Estonia | 0.936 | South Korea | 0.955 | Lithuania | 0.929 |

| Lithuania | 0.929 | Japan | 0.936 | Brazil | 0.905 |

| South Africa | 0.926 | Finland | 0.900 | Russia | 0.905 |

| Russia | 0.924 | Trinidad and Tobago | 0.895 | South Africa | 0.905 |

| Malaysia | 0.869 | Kuwait | 0.883 | Finland | 0.857 |

| United States of America | 0.867 | Israel | 0.882 | United States | 0.810 |

| Finland | 0.863 | Philippines | 0.873 | Malaysia | 0.810 |

| Iceland | 0.851 | Estonia | 0.867 | Norway | 0.786 |

| Trinidad and Tobago | 0.841 | Lithuania | 0.862 | Sweden | 0.786 |

| Norway | 0.833 | Switzerland | 0.857 | China | 0.762 |

| Sweden | 0.833 | Tunisia | 0.857 | Iceland | 0.762 |

| Philippines | 0.830 | Sweden | 0.842 | Jamaica | 0.762 |

| South Korea | 0.827 | Jamaica | 0.833 | Trinidad and Tobago | 0.738 |

| Indonesia | 0.827 | New Zealand | 0.833 | Indonesia | 0.714 |

| Israel | 0.827 | United Kingdom | 0.806 | Israel | 0.714 |

| Jamaica | 0.827 | Bahamas | 0.800 | Australia | 0.690 |

| New Zealand | 0.827 | Eurozone | 0.786 | South Korea | 0.690 |

| Ecuador | 0.816 | India | 0.782 | Ecuador | 0.690 |

| Australia | 0.815 | Uruguay | 0.762 | Philippines | 0.690 |

| Kuwait | 0.806 | Netherlands | 0.755 | New Zealand | 0.690 |

| Spain | 0.802 | Ecuador | 0.745 | Ukraine | 0.690 |

| India | 0.802 | Norway | 0.738 | India | 0.667 |

| China | 0.800 | Australia | 0.736 | Tunisia | 0.667 |

| Eurozone | 0.795 | Brazil | 0.733 | Canada | 0.643 |

| Madagascar | 0.791 | United States | 0.727 | Spain | 0.643 |

| Ghana | 0.779 | Indonesia | 0.718 | Madagascar | 0.643 |

| France | 0.778 | Senegal | 0.714 | Senegal | 0.643 |

| Ukraine | 0.772 | France | 0.709 | Ghana | 0.619 |

| Canada | 0.762 | Spain | 0.700 | Eurozone | 0.607 |

| Japan | 0.733 | Ukraine | 0.695 | Kuwait | 0.595 |

| Switzerland | 0.729 | Ghana | 0.661 | Netherlands | 0.571 |

| Switzerland | 0.714 | Madagascar | 0.611 | France | 0.548 |

| Swaziland | 0.712 | Swaziland | 0.611 | Japan | 0.548 |

| Tunisia | 0.695 | Canada | 0.588 | Switzerland | 0.536 |

| Tunisia | 0.690 | Russia | 0.573 | Switzerland | 0.464 |

| Senegal | 0.619 | Iceland | 0.545 | Swaziland | 0.429 |

| Bahamas Kendall’s Correlation | China Kendall’s Correlation | Uruguay Kendall’s Correlation | |||

|---|---|---|---|---|---|

| Uruguay | 0.929 | Malaysia | 0.954 | Bahamas | 0.976 |

| Brazil | 0.854 | South Africa | 0.873 | Estonia | 0.976 |

| Lithuania | 0.817 | South Korea | 0.855 | Lithuania | 0.929 |

| Estonia | 0.809 | Japan | 0.818 | Brazil | 0.905 |

| Russia | 0.809 | Finland | 0.778 | Russia | 0.905 |

| South Africa | 0.782 | Trinidad and Tobago | 0.761 | South Africa | 0.905 |

| Malaysia | 0.719 | Philippines | 0.745 | Finland | 0.857 |

| Trinidad and Tobago | 0.690 | Estonia | 0.722 | United States | 0.810 |

| United States of America | 0.689 | Kuwait | 0.722 | Malaysia | 0.810 |

| Philippines | 0.689 | Switzerland | 0.714 | Norway | 0.786 |

| South Korea | 0.674 | Tunisia | 0.714 | Sweden | 0.786 |

| Finland | 0.674 | Israel | 0.709 | China | 0.762 |

| Indonesia | 0.674 | Lithuania | 0.704 | Iceland | 0.762 |

| Iceland | 0.674 | United Kingdom | 0.689 | Jamaica | 0.762 |

| Israel | 0.674 | Sweden | 0.689 | Trinidad and Tobago | 0.738 |

| Jamaica | 0.674 | Bahamas | 0.667 | Indonesia | 0.714 |

| China | 0.667 | Jamaica | 0.667 | Israel | 0.714 |

| Sweden | 0.667 | New Zealand | 0.667 | Australia | 0.690 |

| Kuwait | 0.644 | Uruguay | 0.643 | South Korea | 0.690 |

| Ecuador | 0.644 | India | 0.600 | Ecuador | 0.690 |

| Madagascar | 0.644 | Ecuador | 0.592 | Philippines | 0.690 |

| Norway | 0.643 | Ukraine | 0.592 | New Zealand | 0.690 |

| Spain | 0.629 | Brazil | 0.587 | Ukraine | 0.690 |

| France | 0.629 | Norway | 0.571 | India | 0.667 |

| India | 0.629 | Senegal | 0.571 | Tunisia | 0.667 |

| Ghana | 0.598 | Australia | 0.564 | Canada | 0.643 |

| Eurozone | 0.592 | Netherlands | 0.564 | Spain | 0.643 |

| Australia | 0.584 | Ghana | 0.535 | Madagascar | 0.643 |

| New Zealand | 0.584 | United States | 0.527 | Senegal | 0.643 |

| Ukraine | 0.584 | Eurozone | 0.500 | Ghana | 0.619 |

| Canada | 0.571 | France | 0.491 | Eurozone | 0.607 |

| Switzerland | 0.571 | Indonesia | 0.491 | Kuwait | 0.595 |

| Tunisia | 0.571 | Madagascar | 0.479 | Netherlands | 0.571 |

| Swaziland | 0.551 | Swaziland | 0.473 | France | 0.548 |

| Japan | 0.511 | Spain | 0.455 | Japan | 0.548 |

| Netherlands | 0.494 | Canada | 0.422 | Switzerland | 0.536 |

| United Kingdom | 0.479 | Russia | 0.418 | ||

| Senegal | 0.429 | Iceland | 0.345 | Swaziland | 0.429 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Náñez Alonso, S.L.; Jorge-Vazquez, J.; Reier Forradellas, R.F. Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 72. https://doi.org/10.3390/joitmc7010072

Náñez Alonso SL, Jorge-Vazquez J, Reier Forradellas RF. Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(1):72. https://doi.org/10.3390/joitmc7010072

Chicago/Turabian StyleNáñez Alonso, Sergio Luis, Javier Jorge-Vazquez, and Ricardo Francisco Reier Forradellas. 2021. "Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 1: 72. https://doi.org/10.3390/joitmc7010072

APA StyleNáñez Alonso, S. L., Jorge-Vazquez, J., & Reier Forradellas, R. F. (2021). Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1), 72. https://doi.org/10.3390/joitmc7010072