2. Complexity of Economics or of the Economy?

A first reason why economics has become complex in the past four decades or so is due to its increasing intermediary consumption of mathematics. Some economists do contend that their scientific discipline is the most maths-consuming after theoretical physics and astrophysics. Although there is probably some exaggeration in such an assessment, a glance at the Journal of Economic Theory, the Journal of Mathematical Economics, Economic Theory, the Journal of Mathematical Economics and Finance, the International Journal of Economic Theory, Mathematics and Financial Economics or the Journal of Mathematical Finance confirms a high degree of mathematics intensity in current articles published on the knowledge frontier of theoretical economics; the same applies to Econometrica, the Econometrics Journal, the Journal of Econometrics or Econometrics as regards the most recently elaborated technical tools used in applied and empirical economics.

A second reason for complexity in economics is, in a sense, the opposite of the former one. One can start from an outsider view criticising the reductionist approach adopted by mathematical mainstream economics: for instance, Edgar Morin [

1] contends that the latter overlooks all interdependencies and interconnections among elements of the economy that usually create nonlinearities, feedback loops, and systemic self-organisation [

2] not taken on board in most mathematical economic modelling. Or, put otherwise, mainstream economics describes rational “smart people in unbelievably simple situations” while the real world involves “simple people coping with incredibly complex situations” [

3] (p. 52) relying on their bounded rationality. Then follows a search for a complexity theory in economics relaxing basic mainstream assumptions (equilibrium, representative agents, rational choices) and seeking to move beyond while emphasising the power of networks, feedback mechanisms and the heterogeneity of individuals [

4]. The idea is to investigate economic phenomena—not as derived from deterministic, predictable and mechanic dynamics—but as history-dependent, path-dependent, organic and continuously evolving processes.

Therefore, an economic theory of complexity implies more interactions with other scientific disciplines—namely psychology, anthropology, sociology, political science, history, physics, biology, and mathematics—in a highly interdisciplinary research program involving not only economists. Such a new approach has not yet delineated its final research programme since the notion of complexity is itself extremely equivocal and open to debate: the MIT physicist Seth Lloyd provided over 45 definitions of complexity [

5] exhibiting how much disagreement there is on what this very concept means. In economics at least, a complexity approach paves the way to studying:

- (a)

The economy as a global system rather than a mechanics converging to a general and stable equilibrium.

- (b)

Emergence which relates to the dynamic nature of interactions between components in a system [

6].

- (c)

Path dependence meaning just that: where we are today is a result of what has happened in the past [

7,

8,

9].

Thus complex systems, such as the nowadays globalised economy, are dynamic, nonlinear systems with multiple equilibriums and disequilibria, evolving and self-organising in time and space, characterised by historical dependencies, complex dynamics, and thresholds [

10]. One step forward toward complexity economics consists in focusing on constant disequilibrium or continuously shifting micro-equilibrium points rather than a pre-defined general equilibrium point. In the area encompassing the next parts of this paper, that is sports economics, such a step forward has been taken with the recent publication of a ‘disequilibrium sports economics’ book [

11]. In a wider sense, not limited to disequilibrium, complexity economics has occurred in different research areas [

12]. The economic policy implication is that a right policy is the one that reacts to the evolution of a system rather than pushing it in a (presumably) desired optimal equilibrium direction—a so-called Pareto-improving policy in mainstream economics. The last part of this paper exemplifies a reactive, though not Pareto-optimal, taxation policy.

Finally the new train of thought that stresses economic complexity has materialised in a new journal

Complexity Economics: Complexity, Choices & Crises launched in 2012. Among the first representative articles, one can find the following topics: global systems dynamics and policy, world market governance, economics as a global system science, ten prerequisites for a better understanding of the contemporary financial crisis, credit risk spillovers, systemic importance and vulnerability in financial networks, and a number of papers on agent-based models. The underlying radical message is that organisation and not efficiency should be the key concern of economics, and drives to investigating the interactions of individuals rather than the individuals, as already stressed by Alan Kirman [

13].

A third dimension is the increasing complexity of a globalised economy in the real world. That globalisation has made the economy very complex can be witnessed in everyone’s daily life. Buy a basic shirt and you will be able to check that it has been shaped by an Italian designer with American software, and then produced with Western African cotton and polyester buttons manufactured in China out of Indonesian petroleum. The complexity of a globalised economy has gone so far that multinational companies have elaborated on so-called global strategies to trade-off between different potential host countries before investing in them [

14,

15,

16]. To manage global complexity these firms have developed sophisticated managerial tools such as non-market transfer pricing, hedging, leads and lags, tax optimisation, and sometimes fraudulent or borderline strategies like tax evasion and money laundering through tax havens. However, foreign direct investment and production relocation in tune with these strategies require some time before being implemented by a company.

In some industries where

instant trade can be done on-line, globalisation is much swifter, so fast that trade flows are sometimes unobservable or undetectable, sometimes veiled or hidden on purpose. A first example is the finance and banking sector insofar as with the Internet and globalisation (in particular through offshore centres) money can be

instantly transferred from place to place, from country to country, and from a bank account to another one. Such is the complex way that transformed the US subprime crisis into global financial disorder. The latter was due to both the speed of international financial transactions and the complexity of new financial products—securitisation of bad loans, collateralised debt obligations, credit default swaps, mortgage-backed securities—and fuelled with fraudulent or borderline practices such as fake accounting, short selling, shadow banking, and financial pyramids [

17]. Even swifter than international financial transfers throughout a global economy, the most

instantaneous international moves of funds have been registered in the past recent years with on-line betting since bets can be placed and changed in less than one second through the worldwide web. The rest of this paper focuses on the complexity of punters’ networks which bet on the outcome of sporting events when complexity is exacerbated by connecting their bets with match fixing on a global scale.

3. Betting-Related Match-Fixing and Global On-Line Fraudulent Sport Betting Networks

Globalisation has brought about increased economic competition in the sport betting market due to both the Internet and market deregulation. Now, punters have a direct access to foreign bookmakers while the gambling business has been liberalised under the pressure of international organisations such as the World Trade Organization or the European Union. The volume of sporting bets has skyrocketed, the opportunity for frauds as well [

18]. Alongside globalisation sprung up product differentiation and the complexity of newly offered bets such as live betting (60% of all placed bets nowadays), are in-play betting, handicap betting, spread betting, proposition betting, and betting exchanges, all of which bring in new rigging opportunities and risks. Now, as a result, fraudulent fixes often materialise in spot-fixing instead of match-outcome fixes.

3.1. Non Exhaustive Empirical Evidence

With globalisation, most on-line betting operators offer bets everywhere in the world often without a required legal authorisation or a license. Such bets are usually considered as “illegal” and they are assessed to represent about 80% of overall bets in the global sport betting market. In relation with this evidence, 80% of on-line betting operators are based in tax havens. Since 1995, and even more so after 2002, the number of new on-line betting operators has skyrocketed; they were about 10,000 in the world of which 80% to 90% had no license in 2006 [

19]. Many of them had been created in small countries/areas eager to attract significant financial flows such as Alderney, Gibraltar, the Isle of Man, Malta, the Cagayan province in the Philippines, the Kahnawake territory in the Quebec region, Antigua and Barbuda, Nevada and Delaware states in the US, Costa Rica, and Curacao.

Gross win (or gross gaming revenue) on the global market for sporting bets was assessed in the range of €16,000 million in 2011, of which about €10,500 million was in the legal market and about €5500 million in the illegal market. Placed bets were assessed overall at €322,700 million of which €47,700 (15%) was in the legal and €275,000 (85%) in the illegal market [

20]. From 2000 to 2010, gross gaming revenue of sporting bets evolved in the EU 28 countries from €2.2 billion to €11.2 billion, growing at an average 15% annual rate. Such swift growth was triggered by much higher odds and returns on newly offered varieties of on-line sporting bets compared to former betting on final game outcomes known as 1 × 2 (for win-draw-loss) (Average return rates on on-line sporting bets are usually over 95% and often close to 98% [

20]). The top ten gross wins realised on the illegal on-line market have been achieved in fourteen countries: China, the US, South Korea, Germany, India, the Czech Republic, Greece, Vietnam, Argentina, Brazil, Canada, Hong Kong, Pakistan, and Turkey.

In this global context new types of gamblers and punters have emerged. They are more geared toward new trading-off opportunities, in particular high-return ‘sure bets’; they increasingly behave as ‘players’ looking for enrichment as in any financial market. Thus, the global on-line betting market has also attracted financial traders, money launderers, and criminals. Criminals resort to runners for placing their bets without unveiling their identity; this is a way to escape being detected by either betting operators or regulation authorities supervising the legal on-line betting market, such as the ARJEL (Autorité de régulation des jeux en ligne) in France. Escape is especially easy in some countries like the UK where betting market regulation allows those on-line betting operators based in the European Economic Area or listed on a White list to offer their services to UK punters, suffice it to say that the latter open accounts with betting operators located in tax havens. In the worst case, rigged betting is used for money laundering [

21].

Consequently, match and spot fixing have become the most widespread form of corrupt sport in recent years. Fraudulent networks of punters and criminals rig matches through bribing players or referees whereas bets are placed on the fix through the Internet. Despite the surveillance of 30,000 games per season in 43 European football leagues, this corrupt business is skyrocketing; in 2011, about 10% of matches were felt suspicious, in 2012 about 700 games were found to be fixed, primarily in lower professional divisions. Many of these fraudulent networks are based in Asia, namely China, Malaysia, Singapore, the Philippines where betting outlays are not limited, and in some Central Eastern European countries. Interpol dismantled 272 such irregular bookmakers in 2007, arrested 1300 people suspected of organising bets on fixed matches from Asia and seized $16 million in cash in 2008. Before cracking down on these networks, Interpol assessed the volume of their irregular bets at $1.5 billion. Talking about corrupt sport in 2016 cannot avoid focusing on match fixing connected to irregular betting.

Exemplary of the complexity and globalisation of betting-related match fixing is the Bochum case which encompassed 50 corrupts and corruptors, and 320 fixed football matches in 13 countries of which nine were European countries, including Turkey, Germany, Switzerland, and Belgium. Rigged bets in dozens of millions of Euros were placed on fixes of which €32.4 million was with a single Asian operator Samvo, licensed in the UK. The major instigator of this betting scandal eventually was sentenced to five years jail in 2011 by a German court. A large number of other football cases came to light in just a few years [

21]. More than €12 million was injected in these rigged bets by mafia-type networks located in Asia and Eastern Europe to corrupt players, referees and managers of football federations; the gains of this gang were assessed to be €7.5 million. Since 2012, the media has been flooded with revelations about large numbers of football players and administrators being arrested in countries such as China, Greece, Hungary, Italy, Turkey, and Zimbabwe. Problems of betting-related fixes have extended beyond football to handball, volleyball, snooker, sumo wrestling, cricket, and tennis. Apparently, those proven cases are only the tip of an iceberg. The most recent and comprehensive coverage of rigged sports betting is going to be published in [

22].

Some football leagues are more affected by match fixing than any other kind of leagues. Declan Hill’s [

23] Fixed-Match Database (FMD) has gathered evidence of about 301 fixed matches in 60 different countries and 55 different soccer leagues and cup games. A second data base (FMD2) only selected 137 games with the highest degree of certainty that a fix actually occurred. Next, these games were matched with a randomly selected control group of 130 honestly played games. From this comparison, the factors that lead to wide-scale match fixing are: (a) leagues marked by high relative exploitation of players (low wages, wage arrears, non-payment of wages); (b) an expectation of official corruption; and (c) the presence of large and complex illegal gambling networks.

Country ranking on the World Bank’s CPI (Corruption Perception Index) does not affect the presence of high levels of match fixing in a country. Singapore, ranked fifth in the CPI index, has a soccer league that suffers from high levels of corruption as does a country like Vietnam, which is ranked 106 places below on the CPI listing. Some leagues defend their product quality by actively sanctioning players or coaches; but this suggests that match corruption is still going on. However, some national football associations or leagues themselves may be corrupt (e.g., Colombia, Brazil). In 2010–2011 in China, several betting scandals led to the arrest of referees and players, and even some managers of the Chinese football federation, including its president; thus, in April 2012, the championship started up again without its major sponsor, Pirelli, which breached its contract with the football league while the domestic China Central Television refused to broadcast any game. Until a scandal bursts out, most football associations do not publicise corruption cases, on the contrary they attempt to blur or hide them. Absent transparency always facilitates and triggers blooming corruption [

23].

In the past dozen years, match fixing that interacts with rigged betting has become a global complex issue which is now chased by international police and sentenced at national justice courts. Except the Internet, two preconditions have facilitated its emergence. For one, fraudulent punters need to network internationally in order to be able to gather a large amount of money to place on a fix. In most cases in court, several (connected) people from different countries have been judged and sentenced together. The second precondition is that fraudulent punters, or their agents, handle a complex match-fixing technology. To get a deep insight into the latter, Declan Hill spent over ten years living close to and observing from within some match-fixing networks operating in soccer [

24]. He inferred from this long-lasting experience a check list of all that a punters’ network (corruptors) has to do to successfully fix a match and pocket a huge amount of money from betting on the fix [

25]. In a nutshell, it is a rather complex five-stage technology:

- (a)

Corruptors have to employ agents, known as runners, to approach players or referees.

- (b)

A counterfeit intimacy must be implemented with a targeted referee or player, then finding his weakness (he likes drugs or expensive watches or blond prostitutes) to exploit it to compromise him. Once he has accepted gifts or money, he is ripe to be corrupt.

- (c)

Since the ultimate goal of match fixing is profit-maximisation two distortions must go together: fixing the match and rigging the bet. On the betting market, corruptors have to find out the spread and place the bet that will ensure the greatest profit with a fixed match. Corruptors usually will not place a bet in their own names, and preferably will use third parties, known as “beards”, “mules” or runners. With live betting, it is crucial that corruptors signal to the corrupt player or referee what is to be done on the pitch without attracting attention and let him give a signal that he has understood the request (a win or a loss, a definite scoring, shooting the ball offside or in the corner, etc.).

- (d)

For the most part, players do not perform fixes by deliberately losing a match. They simply underperform at the appropriate time in the game to achieve the desired result. Or referees take a wrong decision as if it were a slight mistake in judgment.

- (e)

Over 70% of the payments to corrupt players and referees involved in a fix are in cash, often in two steps. A first symbolic payment settles the deal that the player or referee will take part in the fix. The main payment is postponed until after the match once the fix is delivered.

Thus, the technology of betting-related match fixing is rather complex. In practice, a corruptor cannot operate alone through the five aforementioned stages. Consequently, corruptors act within hidden networks that are not easy to detect. Nowadays, sport corruption is far away from initial petty corruption and has reached a high degree of networking and organisation. This is facilitated with on-line betting and globalisation that together may be used to create major distortions in significant sporting contests and whose economic consequences are often in the millions of dollars.

Since it is not possible to put a policeman on the back of any potential fraudulent gambler, even less behind any potential match fixer, combating this type of sport corruption therefore requires a complex technology as well (electronic surveillance to instantly check unbelievable odds) and strong coordination between different international organisations. In recent years, an increasing cooperation has been witnessed in the fight against betting-related match fixing between the UNESCO, the Council of Europe, the European Union, Interpol, and Sport Accord. Would it be enough to detect complex match fixing? Surely not because one has to notice that a sport insider (player, referee) must always be involved in match fixing; practically the fix cannot materialise without an active participation from inside sport. Thus, combating match fixing first and foremost must come from within the sport movement, that is, the sport governing bodies.

From previous evidence, some economists would infer that a radical option to definitely cut the roots of rigged betting-related match fixing would seem to be a final halt of money inflow into sports. The question is whether it is feasible or even realistic when rich sports are so financially addicted, flooded with money, and economically globalised.

A recent transaction costs approach of sport betting scandals [

26] has stated that, in the 21st century, with football globalisation and the invention of the Internet, a new type of betting emerged with betting platforms: anyone can offer a bet on any game in the world and punters can take up the bet and bet against it choosing among the different above-mentioned products in the sport betting market; national betting regulations can be easily circumvented by global on-line betting possibilities. The fixtures and sporting outcomes are used by so many different providers that the property rights of football game organisers are completely attenuated, fixtures and outcomes becoming a kind of public goods. Then there is an over-use of these public goods and, as for any public good, the variable cost of offering a single new bet is negligible, close to nil. Coupled with the new sport betting products, this has led to explosive market growth, the situation getting definitely out of control for football governing bodies and sport event organisers. This extensive usage of a public good by the betting industry and the possibility to bet high sums increase the likelihood of match fixing. The direct cost of prevention and investigation against match fixing grows and, by the same token, the indirect cost of more frequent betting scandals is up. The issue of betting-related match fixing grows in complexity.

3.2. The standard Economics of Sport Corruption: Complexity Excluded

Until the emergence of globalised on-line betting, standard economic analysis of sport corruption relied on the economics of crime [

27,

28,

29]. As in any industry, a criminal activity in sports is supposed to be triggered by an individual cost-benefit analysis when the outcome of such economic calculation turns out to be a net benefit. If so, an individual invests in the targeted crime. However, Becker added that the net economic gain of a crime must be bigger than a moral (non-monetary) cost associated to the individual’s breaching its own ethical values. For instance, investing in match fixing to derive significant monetary gains through fix-related bets is worth it, if and only if this appears to be profitable, i.e., if those gains obtained in the sport betting market are much bigger than monetary and non-monetary costs of bribing players, referees, and of being sanctioned if detected. In a Beckerian train of thought, all individuals have the same perfectly rational behaviour so that overall demand of fixes in the whole economy grows with an increase in the expected value of the net benefit derived from sport corruption, i.e., when “crime does pay back”. Finally if, as assumed by Becker, anyone has some personal ethical values, including potential corruptors, the latter transgress to some point their own values when undertaking a corrupting action; some non-monetary disutility of corruption ensues which must be taken into account. This adds one more precondition on the demand for corruption that is a higher positive expected benefit than corruptor’s disutility. As a consequence, the more widespread and deeply-rooted sport ethics in the population, the lower the level of sport corruption in a society. Logically, if sport ethics erodes, for a given expected benefit from corruption, the number of corrupt practices increases in society. Eventually when the magnitude of money inflows into sports grows and ethical culture and education weaken in society, this triggers the expansion of sport corruption.

Maennig [

30] elaborated further on this approach in encompassing more non-monetary effects of sport corruption such as a negative reputation falling on corrupt players, a non-monetary opportunity cost of corruption, and a utility associated to being involved in an informal corruption network. However, one limitation of this kind of approach is that supply of corruption by sports insiders basically does not show up anywhere.

Forrest et al. [

18] following Ehrlich [

28], as revisited by Forrest and Simmons [

31], presented a model in which a risk-neutral athlete accepts being corrupted and then offers to fix a match outcome if:

with

Gf: the value of monetary gains derived from betting on a fix

f;

q: the probability that the fix would be both successful and undetected;

p: the probability that the fix would be detected and sanctioned;

Ff: the financial cost (such as a fine) of sanction if the fix is detected;

V (

Df): the monetary value of athlete’s disutility linked to its underperformance in view of achieving the fix, its future bad reputation as corrupt, and the complaints or blames from his team mates;

V (

Cf): the monetary value of undertaking (preparing, organising) a fix.

Potential fraudulent match fixers assess both sides of inequality Equation (1) and, if gains are higher than costs, they invest in a fix. The sport betting market is all the more threatened by match fixing that it is very liquid. Overall market liquidity grows with the cumulative number and amount of bets because, as in any financial market, the expected value of gains increases with liquidity. Thus, increasing liquidity in the sport betting market attracts a bigger supply of fixes while it lowers the probability p that a fix would be detected. Moreover, the current magnitude of sanctions falling on detected and caught match fixers is relatively low compared to inflating revenues of professional athletes and the expected value of bet gains realised on a fix with on-line betting and market globalisation. The latter accompanied with market deregulation has increased the betting market liquidity and decreased transaction costs of fixes linked to sport betting. For instance, in the UK, a fee on sport bets was abolished in 2001 and replaced by a rather modest levy on bookmakers’ profits. In France, the public monopoly (Française des Jeux) over the supply of sport bets has been phased out in 2010 with opening of the domestic market to new and foreign competitors.

On the supply side of the betting market new products have emerged that offer more opportunities for fixes: live betting, in-play betting, proposition betting and betting exchanges. In Forrest et al. [

18], a supply side approach to match fixing is evidence-based on detected fixes undertaken by corrupt athletes for bribes (namely the Bochum case) and, in a sense, is complementary to the demand-oriented analysis of corruption in typical Beckerian models. Although Forrest [

32] contains interesting details about the modus operandi of match fixers, innovation and new techniques for supplying punters with rigged sporting bets, a more complex model integrating demand and supply on both betting and match-fixing markets is still missing in the literature. The idea of a supply-demand model in a market for fixes, though illegal, is sketched in Forrest [

33] where fixes appear to be sold and purchased. On the supply side, the corrupt ones are sport insiders such as players, referees, umpires, coaches, and managers. On the demand side, corruptors are criminals in a Beckerian sense, those who request some matches to be fixed in order to inflate their gains in the sport betting market. Such is the launch pad to our own model below.

4. A More Complex Economic Model of Interacting Match Fixing and Sport Betting

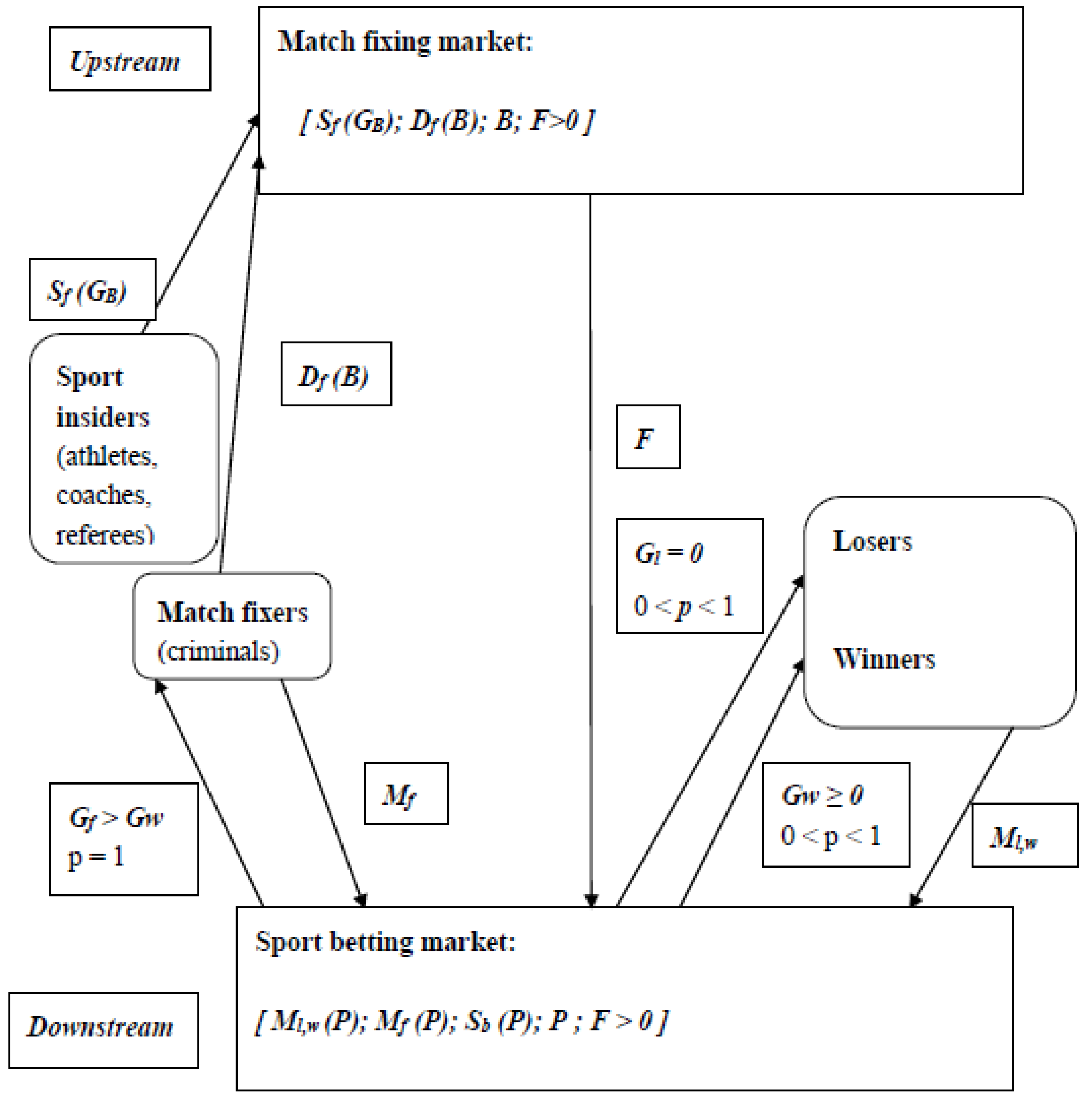

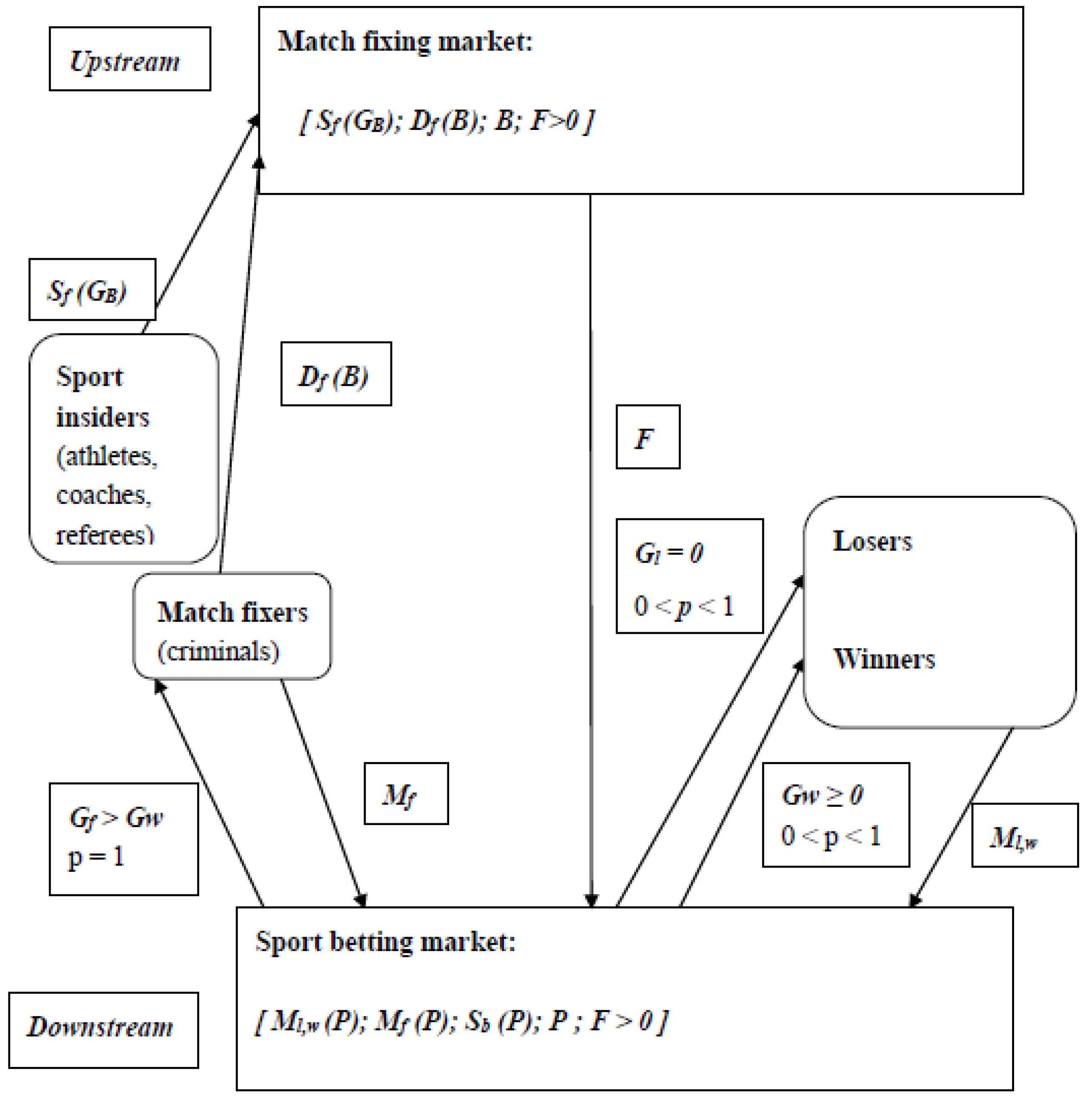

Part of the complexity in the reality of globalised betting-related match fixing comes from interconnections and interactions between operators on two different markets, a sport betting market and a market for fixes. This is the issue tackled here while it is unheeded in the aforementioned standard model of sport corruption. To go beyond the latter’s shortcomings in this respect and clearly represent the most widespread kind of corruption in today’s sports, a model is based on some crucial interrelationships between the two markets, match-fixing and sport betting (

Figure 1 and

Frame 1).

The match-fixing market is upstream (or supplier) to the betting market. If it does not supply any fix (

F = 0), then the sport betting market functions ‘normally’ and is to be analysed like any financial market on the one hand. However with globalisation, shadow banking, securitisation, hedge funds, stock price manipulation, short selling and the subprime crisis, financial markets have derailed from their ‘normal’ functioning [

17]. On the other hand, if the upstream market supplies some quantity of fixes (

F > 0), this heavily affects how the downstream sport betting market functions. When criminal match fixers demand more fixes, such demand increase is an incentive for sport insiders to augment their supply of fixes. The more fixes, the more the gain distribution in the market for sporting bets is distorted between those gains

Gw of regular punters—those not involved in fixes—and the gains

Gf of corruptors, the more the latter invest again and again in fixes, then they collect more distorted and huge gains on rigged bets (those connected to fixes) and so on. The two markets are interacting. This boils down to considering sport insiders as factors of production and suppliers of fixes; consequently fixes are to be treated as inputs delivered in relation with some sporting bets placed by match fixers acting as punters in the downstream market for sport betting. Forrest [

34] and Dietl and Weingärtner [

26] have pointed out that the outcome of a sporting event is an input used by sport bets’ suppliers in a regular bet—without upstream match fixing. A fixed sporting outcome obviously is also an input though it is not the one expected (wished) by regular punters, bookmakers and betting operators.

Frame 1. Variables encompassed in the model of interacting match fixing and sport betting markets in

Figure 1.

Match fixing market

Sf (GB): supply of fixes by sport insiders in function of their gains GB depending on price B,

Df (B): demand for fixes by criminal match fixers in function of their price B,

B: the price of a fix = the bribe that must be offered to sport insiders in order to convince them fixing a match,

F: the quantity (volume) of fixes.

Sport betting market

The supply of sport bets by bookmakers and betting operators does not show up in

Figure 1 since it is assumed both that their supply is not influenced by fixes and bookmakers-operators are not involved into match fixing,

Mf: demand for fix-connected sport bets, the volume of bets placed by match fixers is used as a proxy,

Ml,w: demand for sport bets by honest punters unconnected to match fixers, the volume of honest punters’ bets—going to lose l or to win w—is used as a proxy,

Ml,w + Mf: overall demand for sport bets (with Mf = 0 if there is no fix) which, interacting with supply, determines market liquidity (the total volume of bets),

Gf: gains realised by match fixers on their rigged sport bets,

Gf is assumed to be bigger than the gains Gw realised by winning punters on bets which are not linked to match fixing; the probability of winning Gf is p = 1 due to match fixing; thus in expected value terms: E (Gf) > E (Gw),

Gw: gains of punters without connection to an upstream fix; its ex ante probability p (0 < p < 1) diminishes with match fixing since a predominant share of gains is diverted to match fixers, thus lowering the winning probability of regular bets without upstream fix,

Gl = 0: gains are nil for losing punters.

When such input happens to fuel sporting bets, this obviously changes the volume of bets and is likely to trigger price and odds variations, and to asymmetrically affect the probability of gains across different punters. This probability moves up to 1 for punters involved into upstream match fixing whereas it falls down closer to zero though still 0 ≤ p ≤ 1 for non-involved punters. A fix results in a falling probability to a gain towards zero for honest punters which are not in collusion with match fixers. Such a strongly distorting effect on the gain distribution favours those punters who simultaneously are match fixers, which is exactly the effect they are looking for. When sporting bets are placed on a fix, the percentage of losers increases—all those which have not foreseen the unexpected fixed outcome—while the share of honest punters in overall gains decreases and happens to fall down to zero. By the same token, match fixers nearly take-it-all, so that Gf > Gw (≥Gl = 0, for losers).

Most or all bets laid out (Ml,w + Mf) come back to the hands of match fixers in the form of betting gains, therefore a predominant share of or all lay outs (Ml,w) by honest regular punters are diverted toward match fixers’ gains. By definition, any sport betting system redistributes the losers’ lay outs to the winners’ gains. However, when a match is fixed the redistribution is heavily distorted in favour of match fixers; in extreme cases they take-it-all, being the only ones who have bet on the fixed sporting outcome.

In the sport betting market, the supply of bookmakers and betting operators meets the honest regular punters’ demand and, if the match is fixed, an additional match fixers’ demand. Usually suppliers of bets cannot distinguish and disentangle which betting lay outs are placed on a fix in the current state of on-line surveillance technology and radars supposed to supervise such a global market.

As regards the determinants of supply and demand on both markets, their interactions have to be taken into account, that is the volume of fixes that flows down in the sport betting market, the volume of betting lay outs placed by match fixers, and the demand reaction in the match fixing market to enormous gains of match fixers in the sport betting market.

In the match-fixing market, the supply of fixes is a function of net gain that will accrue to a sport insider participating into the fix. The revenue drawn from a fix by a sport insider is a bribe

B—bribing is used here to mean the generic form of different monetary and non-monetary benefits obtained by a corrupt sport insider from criminal match fixers such as those covered in detail in Declan Hill’s works. However, a sport insider who fixes a match incurs a series of effective and potential costs which are likely to restrict its supply of fixes. The higher and more certain the net gain from bribes

GB for a sport insider, the higher its supply of fixes which is thus an increasing function of

GB. Eventually the supply of fixes is determined by:

the amount of bribes B,

the expected cost of a sporting and/or monetary sanction in case of detection E(s),

the athlete’s disutility associated to his/her counter-performance (and impact on his/her personal record of achievements) in view of achieving the fixed outcome: U(T); a negative effect on the athlete’s reputation, the blames of team mates, etc., are included in this disutility,

the expected financial loss if the fix is detected E(Cf) that is current and future revenues (wages, bonuses) that the athlete would have earned had not it been detected,

those lost sponsorship and advertising contracts as well as a depreciated athlete’s value on the transfer market after the fix has been detected that is a depreciation of its expected market value E(DV),

a moral or ethical disutility U (ETH).

Matches are fixed (

F > 0) when the net gain of a sport insider participating to a fix has a positive value and is bigger than the moral disutility fuelled by its ethics. The supply function of fixes

Sf (

GB) thus is written:

Given a probability

q (0 <

q < 1) to be caught, the Equation (3) also writes as follows:

If Equations (3) and (4) are fulfilled, a supply of fixes Sf (GB) > 0 effectively emerges and, if it meets a non-nil demand for fixes in the market, at a B price (bribe), then a non-nil production of fixes F > 0 will result.

The demand for fixes emanating from match fixers is a function of the net gains they draw with certainty (

p = 1) from laying out

Mf in bets connected to fixes; it is even the motivation for such a demand to emerge. However, a match fixer (or a criminal network) incurs some costs generated by arranging a fix which are likely to limit the demand for fixes. Defining the following variables:

Gf: net gains obtained with certainty by match fixers on their fix-related bets,

B: cost of bribing, the price to pay with certainty by match fixers to corrupt sport insiders,

Cf: other production costs of (arranging, organising) a fix to be paid with certainty including networking costs (when criminal networks) and the cost of money laundering (when fixes are used for this purpose),

Mf: betting lay-outs invested by match fixers right before or during the course (with on-line in-play betting) of a fixed match,

E (Cs): expected cost of sanctions if the fix is detected directly (by the police, a betting surveillance system, a penitent’s confession) or indirectly by an ex post discovery that some sporting bets were connected to a fix,

Then the demand function for fixes turns out to be

Df (

B) such as:

The Equation (7) simply says that a fix is arranged only if its return in terms of gains in the betting market is higher than what an honest regular winner expects to win. If the probability that a fix would be detected is 0 <

q < 1, then the Equation (6) is written:

If demand and supply match in the match-fixing market is:

then an effective volume of fixes (

F > 0) is delivered by corrupt sport insiders as an input for some bets associated to fixes placed by corruptors in the sport betting market.

Now analysing the sport betting market, one has to distinguish two situations depending on whether the bets are placed on fixes (

F > 0) or not (

F = 0). If a match is not fixed, the demand and supply functions of sporting bets are ‘normal’, without any distortion due to upstream fixes. The determinants of the demand for sporting bets

Ml,w (

P)—with

Mlw the total amount of placed bets by future losers and winners—are:

Rb: the share of its revenues that a punter allocates to placing sport bets,

E (Gw): the expected value of a winner’s gain Gw; of course losers’ gains are Gl = 0,

τ = Gw/Mlw: the rate of return on a sporting bet which is the ratio between all gains paid to the winners Gw and overall betting lay-outs Mlw; τ actually gears the punters across existing suppliers (bookmakers, betting operators) but its quantitative influence on demand is taken on board with the next variable P,

P: the price of sporting bets which is the money that is not paid back to winners out of overall lay-outs, thus P = Mlw (1 − τ). Today in the global unregulated on-line sport betting market the rate of return attains up to 95%–98% so that the bet price has fallen down to about 2% to 5% of betting outlays.

The determinants of the supply of sporting bets

Sb (

P), when there is no upstream fix (however in the current state of market surveillance, bookmakers and betting operators do not know either ex ante or ex post if a match is fixed in the upstream market, except if they participate themselves into the fix, an assumption which is not retained here) in the match-fixing market (

F = 0) are:

Ro: revenues of sport betting operators and bookmakers derived from betting lay-outs and the return they pay to winners,

P: the price of a sporting bet,

Cb: a variable cost of supplying sporting bets, which becomes low once a betting operator has invested in a platform of on-line betting—such investment cost has enormously decreased in recent years [

26],

Ci: an institutional cost to be borne when there is some market regulation or a limitation on maximum acceptable betting outlays,

r: a risk premium (or risk assessment).

In the sport betting market a supply of bets

Sb (

P) matches a demand for bets

Mlw (

P). Assuming that there is no fix, demand and supply functions of sporting bets are:

the sport betting market functions as it is expected to—it is a ‘normal’ financial market.

Now assume that a number F > 0 of matches are fixed in the upstream market, several new variables have to be taken on board in the model such as the volume of fixes F, match fixers’ betting outlays Mf and their fraudulent gains Gf. Primarily those punters participating in match fixing will bet on the future fixed outcome while all other punters cannot guess it and will be betting otherwise; then honest regular punters are losers and thus E(Gw) (now zero) disappears from the demand function. All bets unconnected to the fix are losing (Gl = 0) (Indeed, some non-involved punters can, just by chance but not very often, bet on the fixed outcome but they are very few and this would not change the whole model).

The demand function for sporting bets connected to fixes, confined to match fixers, is:

with:

Rf: revenues that match fixers are able to mobilise or network (namely from street punters) in order to lay them out on sporting bets when they fix a match;

Gf/B: the ratio between high gains on bets derived with certainty from an upstream fix and the bribe paid to corrupt sport insiders (a sort of profitability ratio for fix-connected bets); this ratio improves when the number of sporting bets grows, and this attracts a greater volume of fixes in the upstream market.

The supply function of bets remains unchanged—as with Equations (11) and (12)—as long as betting operators, though aware of possible match fixing, are unable to know whether each match offered for betting is plagued with a fix or not.

Now the model is more complex and comprehensive than the standard economics of corruption and more specific to fix-related sport betting since it encapsulates the two markets involved in the most massive global sport corruption today, including their interaction. It may be of some help for policy recommendation.

5. A Global ‘Sportbet-Tobin’ Tax to Combat Betting-Related Match Fixing

Since it is not possible for a regulator, a bookmaker, a betting operator or a government to obtain the required transparency for scrutinising the very existence of transactions in the market for match fixing, they cannot straightforwardly intervene, regulate, sanction, fine or tax these kinds of underground transactions. If one wishes to phase out or at least diminish the current volume of bet-related match fixing the only way to proceed, for governments, sport governing bodies or bookmakers’ professional unions, is to act on the market for sport betting.

All economic analyses conclude that the bigger money inflow into sport the higher sport corruption. Since a drastic money withdrawal from sport, however nice a solution, is unrealistic with the current sport economic globalisation, other options must be looked for. One is

prohibition of activities that most likely channel corruption through sport betting. Some countries have opted for definitely prohibiting sporting bets: the US, Brazil, Cuba, Indonesia, India, Malaysia and several CIS countries [

20]. More precisely, the US has banned sports betting in all states but Oregon, Montana, Delaware, and Nevada, of which only Nevada offers full sports books. Another group still maintains a state monopoly over sport betting such as Canada, Chile, China, Colombia, Japan, South Korea, Singapore, and a few European countries (Finland, Greece, Hungary, The Netherlands, Norway, and Portugal). The great bulk of irregular fix-related sport bets emanate from these first two groups of countries namely China, Malaysia, and Colombia. National prohibition or a state-owned betting system, facing a global demand for sport betting, generates a worldwide black market primarily based in those countries where punters have to—and are used to—circumventing a legal impossibility to bet or a legal possibility to bet only under state control. A safety valve was created in countries like the US, with local exemptions to more general gambling prohibitions. For example, prior to the wave of gambling legalizations starting in the 1980s, casino gambling and sports betting were illegal nationwide with the exception of Nevada and Atlantic City, NJ, USA (which still prohibited sports betting). At that time illegal bets on all games were nearly 99 times bigger than legal ones and since then, casino gambling has spread to most states, but sports wagering remains illegal outside of Nevada except for minor allowances in Montana, Oregon, and Delaware [

35]. Moreover, a recent research report [

36] states that Americans want to bet on sports and prohibition has largely failed as restrictions are ignored; left unchecked, black market gambling in the US has thrived.

Standard counteracting policies against corruption are legal sanctions that raise the cost of corruption to corrupts and corruptors, and regulation though its enforcement must increase corruption prevention, surveillance, and detection costs for governments.

In terms of

sanctions, criminalisation of corrupts, corruptors and corrupt activities is conceived of as the major tool for combating match fixing and illegal or irregular betting [

37]. Maennig [

38] advocates severe sanctions that would maximally worsen the bad reputation of corrupt sport insiders and by the same token would increase ex post non-monetary costs of corruption; corruptors and corrupt insiders would have to be more cautious to avoid detection and sanction if the expected value of direct monetary costs of corruption were to increase. Sanctions may be taken not only on a (common) legal base but also from within sport by enforcing sport federations’ rules. However, it is precisely because sanctions against corrupt sport participants coming from sport governing bodies were much too few in the past that sport is facing a skyrocketing trend of corruption; therefore there is a need for governmental sanctions as well, despite the sport’s claim for absolute autonomy.

When it comes to regulation, the target may be either the price or the volume of sport corruption. Appropriate regulation maintains some ex ante control over potential corrupt activities as, about sport betting, delivering licenses to gambling operators (Panama, the UK and most European countries). For Maennig, controls over sport bets must be strengthened in view of making punters more aware of their responsibilities. In some countries, gambling operators are required to pay property rights to offer sport bets (1% to 2.5% of bets); the rights are paid to organising sport associations. In other countries, some sorts of bets are forbidden like spread betting that favours match fixing. Another option for public regulation would be to fix a very high minimum price of sport bets that would put a ceiling on and deteriorate the rate of return to punters which, at the end of the day, would deflate the volume of bets and thus the probability of match fixing. Fine tuning a regulation can diminish the number of betting scandals though not definitely come up with phasing all of them out. Moreover, domestic regulation against sport corruption and match fixing enforced on a national base would crowd corruptors and match fixers out to those countries without regulation or where regulation is usually circumvented. Illegal bets would then migrate to China, Colombia, or Malaysia: in fact, they already have! Last not least, the more significant the regulation the more crucial the issues of enforcing it and avoiding regulators themselves to be attracted into corrupt sport business.

Dietl and Weingärtner [

26] follow up Coase [

39] in assuming that transaction costs are nil or negligible; then the identity of who holds the property rights on an asset does not matter (In this famous article, Ronald Coase contends that the initial allocation of legal entitlements does not matter from the perspective of economic efficiency as long as they are clearly defined and can be freely traded on a perfect competition market—implying nil transaction costs; thus, once the property rights are strictly delineated—i.e., not attenuated or alleviated—selling the rights is coined a Coasian solution). They suggest an original solution to resolve the issue of external costs borne by football organisers due to completely attenuated property rights on public goods (fixtures, outcomes). It is to find a reallocation of property rights over sport betting that would nullify external costs for football, once admitted that the objective is a “social optimum, but also with regard to the optimum outcome for the game of football and its institutions” ([

26], p. 10). Additionally, since “the government will always aim for the social optimum rather than the football optimum” ([

26], p. 12), they do not trust regulation or taxation as the best solution. Therefore they advocate allocating property rights over sport bets back to the producing football institutions rather than the exploiting bet providers. A total elimination of betting scandals simply would require that football institutions stop selling any property rights to the gambling industry.

Is such radical solution realistic? For the one, would the football (sport) institutions decide to deprive themselves from attracting money into their industry through sport betting? Would they cut themselves from the betting godsend simply to clean up betting scandals? Here comes the issue of good or bad governance of sport clubs and governing bodies, pointed at in particular in football [

40]. If transaction costs are not nil, the allocation of property rights over public goods (fixtures, outcomes) to football private institutions—a solution that must be coined a

privatisation of public goods—often leads in different contexts to embezzlements, cheating, asset grabbing … and corruption [

41]. Combating corruption in creating new opportunities for corruption is paradoxical, to say the least. Eventually, such a privatisation drive would not phase the illegal sport betting market out since those bookmakers or betting operators which would have not paid the rights to use sport outcomes for offering bets, would become “now unofficial betting providers” as to Dietl and Weingärtner (p. 15). Betting scandals will go on. Finally, if one actually considers betting scandals as a social issue, it is debatable to look for a football social optimum instead of an overall social optimum (for all industries and the whole society). The latter has no chance to coincide with specific aspirations of football (or even all sports) institutions and industry.

Another option suggested by Dietl and Weingärtner is that sporting entities could request betting rights—in the same vein as broadcasting rights—to be paid to them directly by betting operators and by the same token privatise both property rights on public goods (fixtures, outcomes) and their negative external effects (fraudulent bets). The idea is that betting rights should compensate each sporting entity for the cost of combating frauds generated by rigged sporting bets. Betting rights would avoid the political difficulty of individualising different rules and taxes aimed at different sports. However, a precondition for this Coasian solution to work well is that transaction costs must be nil, which means that sporting entities would be able, without any cost, to deprive those betting operators which are not willing to pay the rights from the practical possibility of organising sporting bets. This seems to be out of reach to sporting institutions since information about sport fixtures and outcomes is accessible to anyone, be they fans, TV viewers or illegal betting operators. Thus betting rights might not be a solution since some governments (in the UK and the US) do not recognise an intellectual property over sporting events and consequently do not allow sporting entities to request the payment of betting rights. Moreover, in countries where betting rights are recognised (France, Germany), paying them increases the costs of legal betting operators and improves the relative competitiveness of illegal operators which would take over an increased market share.

Dietl and Weingärtner contend that taxation of bookmakers and betting operators whose receipts would compensate football for the burden of its fraudulent betting external costs is likely to significantly reduce the quantity of betting scandals but they object that the tax must be too high and perhaps so high that it would dissuade all football betting. Such taxation would not necessarily affect bookmakers’ behaviour in such a way that they avoid those types of bets which facilitate match fixing. More basically, domestic taxation in a national betting market would not be efficient in the face of a complex global fix-related sport betting market.

Consequently we suggest here a new tool to combat fix-related sporting bets, a so-called

global ‘Sportbet-Tobin’ tax with a variable tax rate (“

Appendix A”). It is inspired from the famous Tobin tax [

42], and closer to the sports industry, the so-called “Coubertobin” tax [

43,

44,

45]. The former targets a slowdown in global financial transactions and international capital flows while the latter is proposed with the aim of hindering and scaling down the flourishing international trade (transfers) of athletes below the age of 18 from developing to developed countries. The interesting aspect of the latter is its variable rate which increases when the age of transferred athletes is going down whereas the Tobin tax was designed with a 1% flat rate, and its first ongoing implementations retain even a lower rate.

In order to adapt the concept to sport betting, one has first to sketch the threshold over which the ‘Sportbet-Tobin’ tax should be levied, i.e., the amount of betting gains that triggers taxation, say at the lowest 1% rate. A low tax rate may have a sort of moralising impact on punters and must target a low threshold of gains above which levying the tax. However, one cannot expect to actually slowdown sport betting on fixes only with such moralising effect. The debate is open about how high this threshold should be: €50,000, 100,000 or 500,000? Corrupt betting money generally works by making large amounts of money on a small number of bets. However, in particular in Asia (China), small bets are collected (even in the street) and networked (aggregated into a large amount of money) from small punters eager to make money even through illegal means, who usually place much less than $10,000 each. When fraudulent punters are cracked down and sued in the court, it often appears that the judge has to face a significant network (dozens, sometimes hundreds) of participants. It would be more efficient to put a brake on fix-related sport betting with a variable tax rate rising significantly above the moralising 1% level. A tax rate growing with the amount of betting gains above the threshold is likely to dissuade a number of bets placed by match fixers and crowd out criminals using those bets to enrich themselves; they would move out of sport corruption for some other criminal activity. If the highest rate of taxation is fixed high enough, the worst of fix-related sport betting would vanish since the tax would confiscate the great bulk of gains and lower match fixing profitability down enough to dry it up. With such a tax, hyper-gains on rigged bets would shrink due to hyper-taxation of gains.

What would the revenues from the ‘Sportbet-Tobin’ tax be used for? Overall tax receipts would first finance more efficient and widespread surveillance systems of on-line sport betting. It may also help some countries, among the Asian and less developed ones, where betting on fixes is the most concentrated, to implement rigorous systems of surveillance. Which body would be accountable for levying the ‘Sportbet-Tobin’ tax? Various options may be envisaged such as a specific worldwide organisation like a World Fund for the Tax on Sport Betting or a branch of an existing intergovernmental body placed under the aegis of the UN as the UNDP, or the World Bank. In any case, it should not be an international sport governing body (an international sport federation or the IOC) because sport governing bodies are full of sport insiders and the most greedy ones can be bribed [

46], and also because the accountability of public taxation must never fall into private bodies’ hands. Levying a global tax must remain within the responsibility of a public governing body. The global ‘Sportbet-Tobin’ tax must and can only result from an international agreement between as many governments as possible.

{kind=link}