A Systemic Approach to Evaluating Fintech-Driven Competitiveness in Commercial Banks: Integrating Delphi and ANP Methods

Abstract

1. Introduction

2. Theoretical Background and Literature Review

2.1. Theoretical Background

2.2. Literature Review

3. Research Objective, Methodology and Data

3.1. Research Objective

- Which indicators ought to be selected, and how should they be measured to appropriately assess the fintech competitiveness of commercial banks?

- What are the interrelationships among the various evaluation indicators of fintech competitiveness within commercial banks?

- How can scientific methodologies be employed to ascertain the weights of each fintech competitiveness evaluation indicator for commercial banks?

3.2. Research Methodology

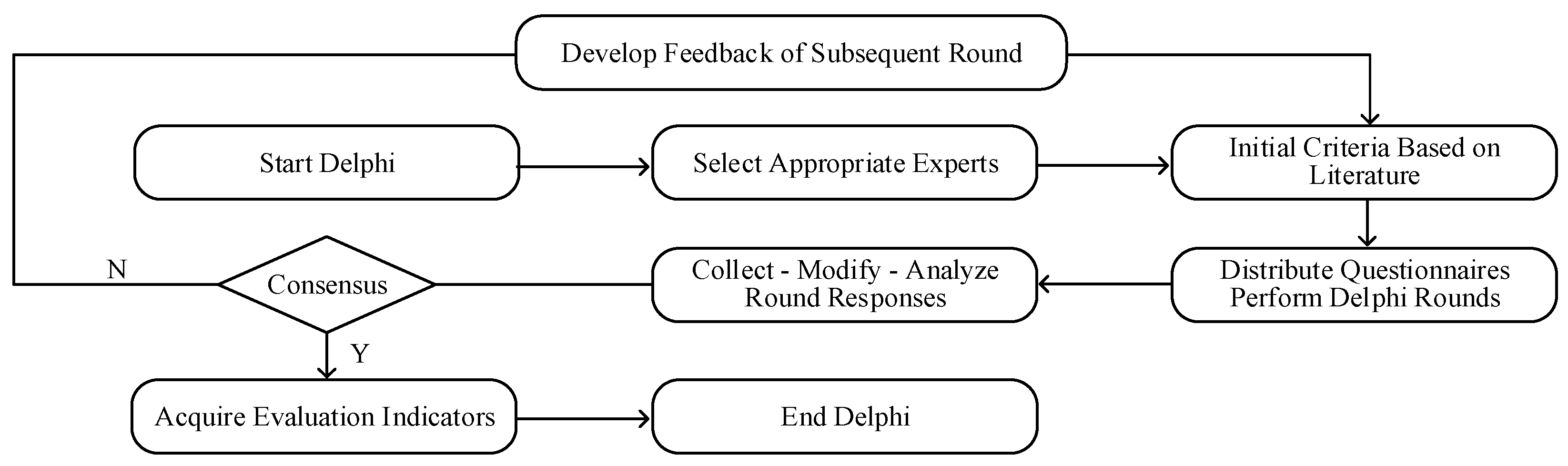

3.2.1. Delphi Method

- Relevance. The fintech competitiveness evaluation system established in this study diverges from the competitiveness evaluation systems developed by previous scholars, as it highlights the application capabilities of these banks within the realm of fintech. Thus, the indicator system should be systematically designed to align with the theme of commercial banks’ application capabilities in the fintech domain;

- Accessibility. A multitude of indicators exist to measure the fintech competitiveness of commercial banks; however, in practice, many of these indicators present challenges in data collection, and some may even be impossible to obtain. Thus, to ensure that the final evaluation system can be broadly disseminated within the banking sector, indicators should be designed to be easily searchable and collectible, thereby enhancing the operability of the research process;

- Coordination. The strength of a commercial bank’s fintech competitiveness results from the collective impact of various technology applications. Therefore, the constructed evaluation system should aim to encompass all relevant factors to form a complete system while ensuring good coordination among the subsystems within this system, thus maintaining the balance of indicators at all levels of the evaluation system.

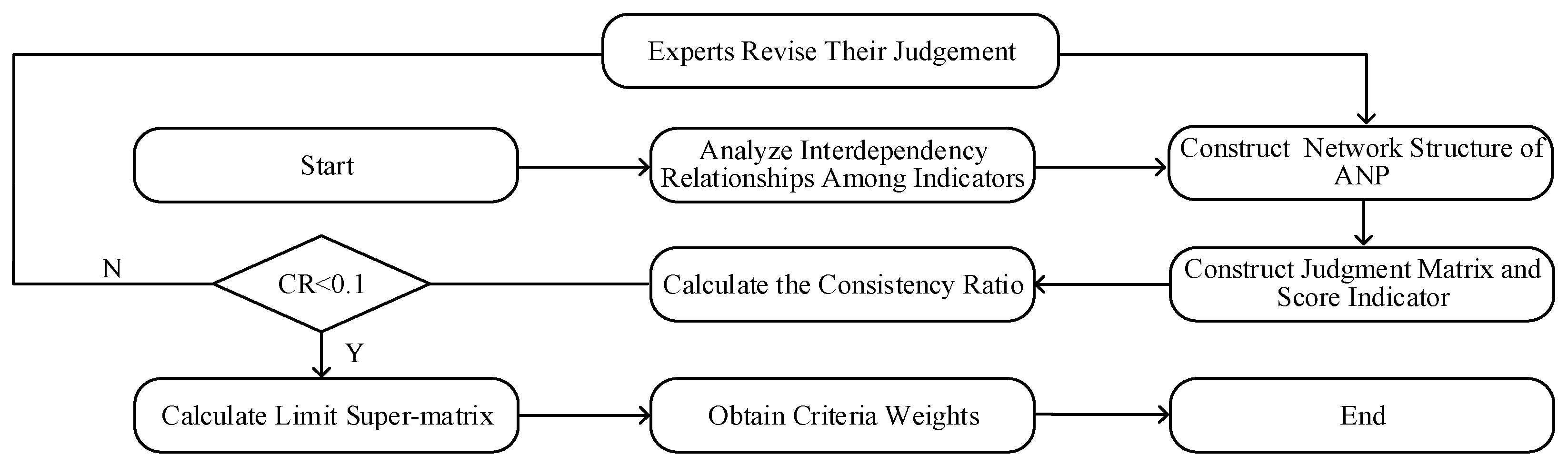

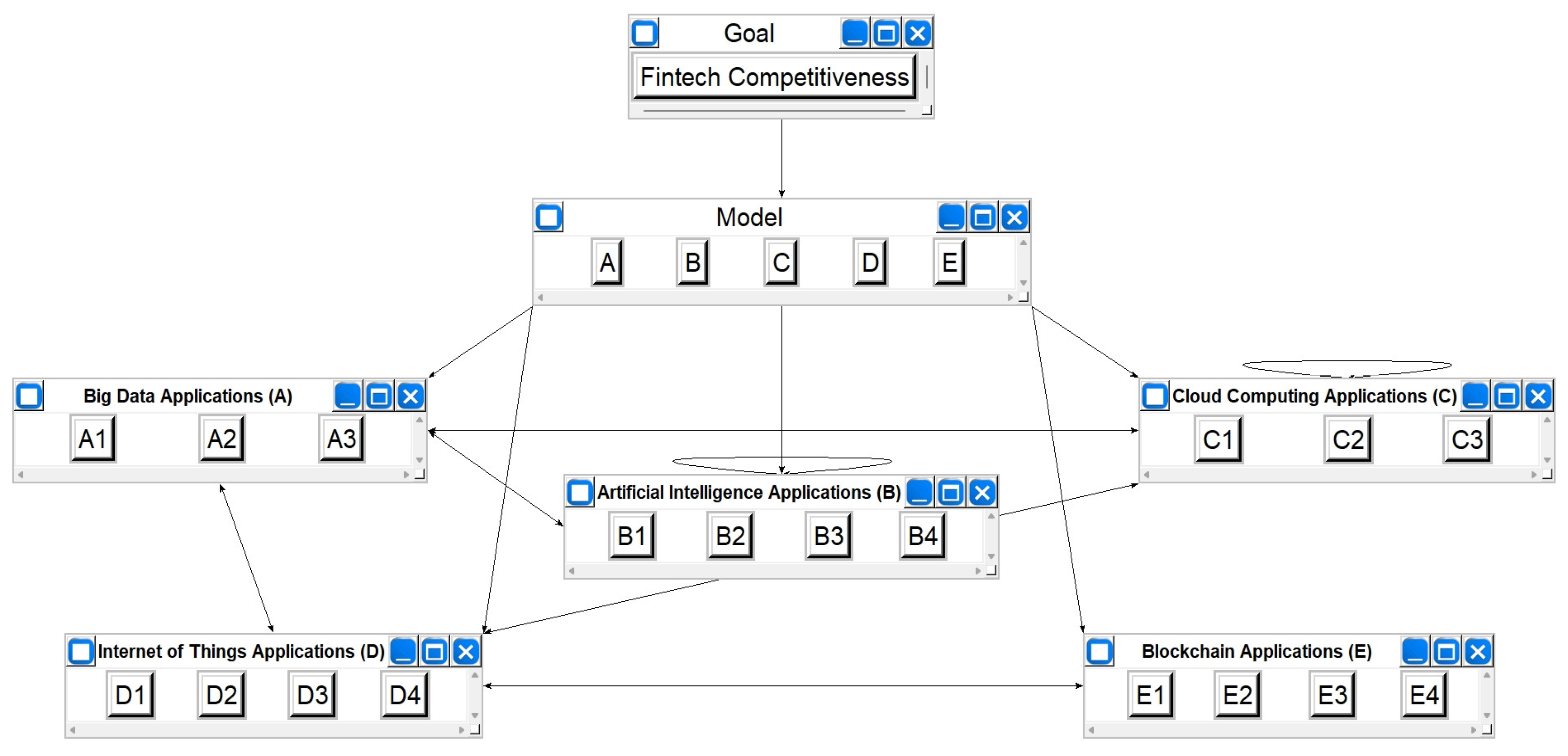

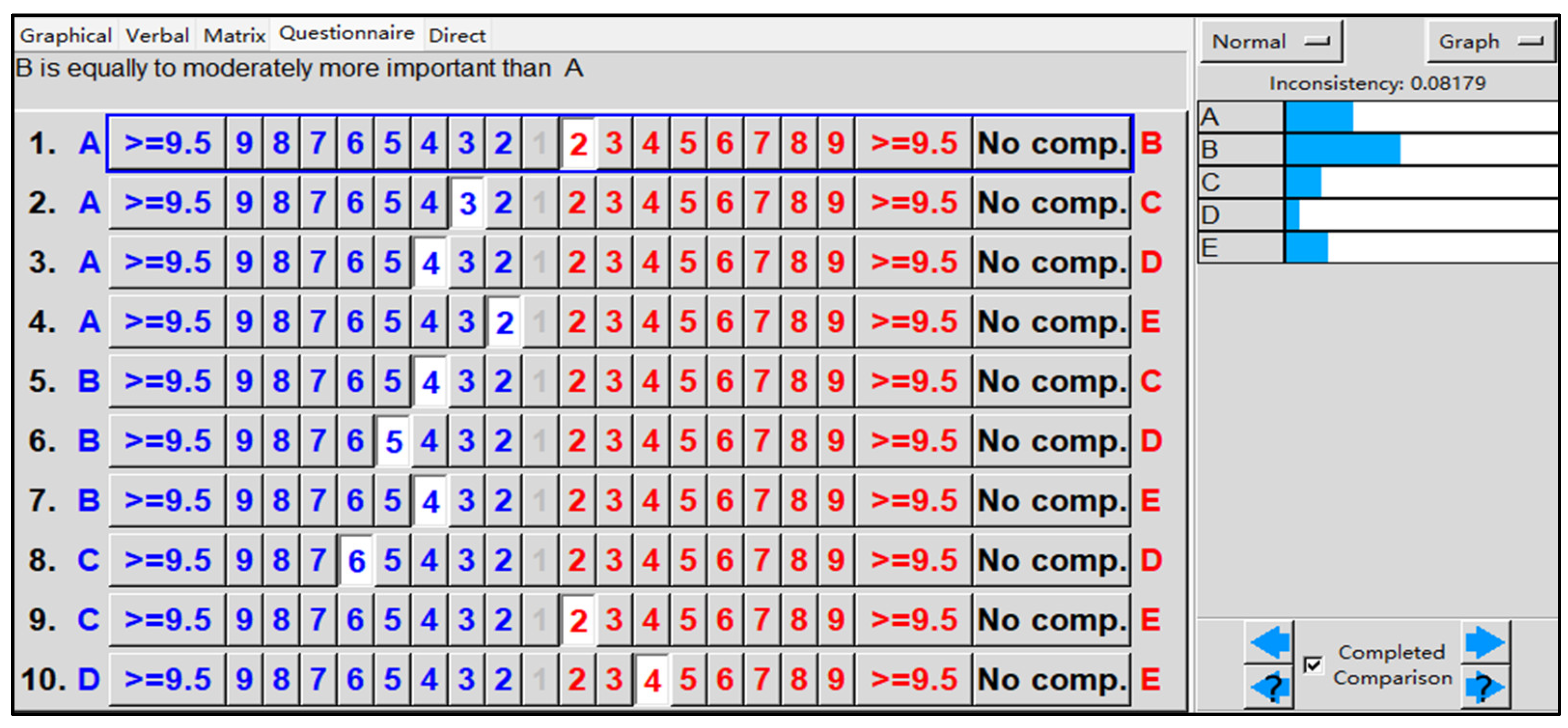

3.2.2. ANP Method

3.3. Research Data

4. Results and Discussion

4.1. Delphi Analysis Results

4.2. ANP Analysis Results

4.3. Discussion

5. Conclusions, Contributions, and Future Work

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

- Questionnaire Survey

- Dear Expert,

- Evaluation Section

- Please evaluate the relevance, accessibility, and coordination of each of the following indicators by scoring them on a scale of 1 to 5 (1 = very poorly aligned; 5 = very well aligned).

- Evaluation Dimensions 1: Big Data Application

- Observation Indicator 1.1: Risk Management Capability

- Relevance_________ Accessibility_________ Coordination_________

- Observation Indicator 1.2: Precision Marketing Capability

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 1.3: Operational Efficiency Optimization Capability

- Relevance_________ Accessibility _________ Coordination_________

- Evaluation Dimensions 2: Artificial Intelligence Application

- Observation Indicator 2.1: Robo-advisors Services

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 2.2: Chatbots Efficiency

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 2.3: Intelligent Identification Efficiency

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 2.4: Intelligent Claims Processing Services

- Relevance_________ Accessibility _________ Coordination_________

- Evaluation Dimensions 3: Cloud Computing Application

- Observation Indicator 3.1: Information Data Integration Capability

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 3.2: Business Process Optimization Capability

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 3.3: Data Security Protection Capability

- Relevance_________ Accessibility _________ Coordination_________

- Evaluation Dimensions 4: Internet of Things Application

- Observation Indicator 4.1: Movable Property Pledge Financing Capability

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 4.2: Payment Function Optimization Capability

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 4.3: Machine Fault Detection Capability

- Relevance_________ Accessibility _________ Coordination_________

- Evaluation Dimensions 5: Blockchain Application

- Observation Indicator 5.1: Digital Credit Financing Services

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 5.2: Digital Payment Settlement Services

- Relevance_________ Accessibility _________ Coordination_________

- Observation Indicator 5.3: Digital Bill Discounting Services

- Relevance_________ Accessibility _________ Coordination_________

- Open-ended Suggestions Section

- Please provide suggestions for modifications or additions to the evaluation dimensions or observation indicators in the indicator system. __________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

References

- Gonenc, H.; Jansen, F.; Tinoco, M.H.; Vulanovic, M. The impact of credit reforms on bank loans and firm leverage around the world. Eur. Financ. Manag. 2024, 30, 2449–2502. [Google Scholar] [CrossRef]

- Lee, C.C.; Ni, W.; Zhang, X. FinTech development and commercial bank efficiency in China. Glob. Financ. J. 2023, 57, 100850. [Google Scholar] [CrossRef]

- Lóska, G.; Uotila, J. Digital transformation in corporate banking: Toward a blended service model. Calif. Manag. Rev. 2024, 66, 93–115. [Google Scholar] [CrossRef]

- Magdy, M.; Raouf, E.; Al-wakeel, N. The Integration of Fintech and Banks: A Balancing Act Between Risk and Opportunity. Int. J. 2023, 10, 2467–2479. [Google Scholar] [CrossRef]

- Song, X.; Yu, H.; He, Z. Heterogeneous impact of fintech on the profitability of commercial banks: Competition and spillover effects. J. Risk Financ. Manag. 2023, 16, 471. [Google Scholar] [CrossRef]

- Nurwulandari, A.; Hasanudin, H.; Subiyanto, B.; Pratiwi, Y.C. Risk Based bank rating and financial performance of Indonesian commercial banks with GCG as intervening variable. Cogent Econ. Financ. 2022, 10, 2127486. [Google Scholar] [CrossRef]

- Rehman, Z.U.; Muhammad, N.; Sarwar, B.; Raz, M.A. Impact of risk management strategies on the credit risk faced by commercial banks of Balochistan. Financ. Innov. 2019, 5, 44. [Google Scholar] [CrossRef]

- Jungo, J.; Madaleno, M.; Botelho, A. The effect of financial inclusion and competitiveness on financial stability: Why financial regulation matters in developing countries? J. Risk Financ. Manag. 2022, 15, 122. [Google Scholar] [CrossRef]

- Arbolino, R.; Boffardi, R.; Kounetas, K.; Marani, U.; Napolitano, O. Are There Conditions That Can Predict When an M&A Works? Case Ital. List. Banks Econ. 2024, 12, 58. [Google Scholar]

- Dinu, V.; Bunea, M. The impact of competition and risk exposure on profitability of the Romanian banking system during the COVID-19 pandemic. J. Compet. 2022, 14, 5–22. [Google Scholar] [CrossRef]

- Mateev, M.; Moudud-Ul-Huq, S.; Sahyouni, A.; Tariq, M.U. Capital regulation, competition and risk-taking: Policy implications for banking sector stability in the MENA region. Res. Int. Bus. Financ. 2022, 60, 101579. [Google Scholar] [CrossRef]

- Barr, R.S.; Killgo, K.A.; Siems, T.F.; Zimmel, S. Evaluating the productive efficiency and performance of US commercial banks. Manag. Financ. 2002, 28, 3–25. [Google Scholar] [CrossRef]

- Chhaidar, A.; Abdelhedi, M.; Abdelkafi, I. The effect of financial technology investment level on European banks’ profitability. J. Knowl. Econ. 2023, 14, 2959–2981. [Google Scholar] [CrossRef]

- Haldar, A.; Sethi, N. Environmental effects of Information and Communication Technology-Exploring the roles of renewable energy, innovation, trade and financial development. Renew. Sustain. Energy Rev. 2022, 153, 111754. [Google Scholar] [CrossRef]

- Najaf, K.; Chin, A.; Fook, A.L.W.; Dhiaf, M.M.; Asiaei, K. Fintech and corporate governance: At times of financial crisis. Electron. Commer. Res. 2024, 24, 605–628. [Google Scholar] [CrossRef]

- Menicucci, E.; Paolucci, G. ESG dimensions and bank performance: An empirical investigation in Italy. Corp. Gov. Int. J. Bus. Soc. 2023, 23, 563–586. [Google Scholar] [CrossRef]

- Holland, J.H. Hidden Order: How Adaptation Builds Complexity; Basic Books: New York, NY, USA, 2011. [Google Scholar]

- Buckley, W. Society as a complex adaptive system. In Systems Research for Behavioral Science; Routledge: Abingdon, UK, 2017; pp. 490–513. [Google Scholar]

- Rabbani, M.R. The competitive structure and strategic positioning of commercial banks in Saudi Arabia. Int. J. Emerg. Technol. 2020, 11, 43–46. [Google Scholar]

- Alqahtani, M.M.M.; Singh, H.; Haddadi, E.A.A.; Al-Shibli, F.S.R.; Al-balushi, H.A.A. Impact of Internet of Things, Cloud Computing, Artificial Intelligence, Digital Capabilities, Digital Innovation, IT Flexibility on Firm Performance in Saudi Arabia Islamic Bank. Adv. Soc. Sci. Res. J. 2024, 11, 71–91. [Google Scholar] [CrossRef]

- Moran, N. Bank versus FinTech: Can Traditional Banks Protect Market Share from FinTech Start-Ups in the Area of Corporate Payment Services? Ph.D. thesis, National College of Ireland, Dublin, Ireland, 2020. [Google Scholar]

- Kumar, S.; Sharma, D.; Rao, S.; Lim, W.M.; Mangla, S.K. Past, present, and future of sustainable finance: Insights from big data analytics through machine learning of scholarly research. Ann. Oper. Res. 2022, 345, 1061–1104. [Google Scholar] [CrossRef]

- Hasan, M.M.; Popp, J.; Oláh, J. Current landscape and influence of big data on finance. J. Big Data 2020, 7, 21. [Google Scholar] [CrossRef]

- Du, G.; Liu, Z.; Lu, H. Application of innovative risk early warning mode under big data technology in Internet credit financial risk assessment. J. Comput. Appl. Math. 2021, 386, 113260. [Google Scholar] [CrossRef]

- Moradi, S.; Mokhatab Rafiei, F. A dynamic credit risk assessment model with data mining techniques: Evidence from Iranian banks. Financ. Innov. 2019, 5, 15. [Google Scholar] [CrossRef]

- Hernández-Nieves, E.; Hernández, G.; Gil-González, A.B.; Rodríguez-González, S.; Corchado, J.M. Fog computing architecture for personalized recommendation of banking products. Expert. Syst. Appl. 2020, 140, 112900. [Google Scholar] [CrossRef]

- Lehrer, C.; Wieneke, A.; Vom Brocke, J.A.N.; Jung, R.; Seidel, S. How big data analytics enables service innovation: Materiality, affordance, and the individualization of service. J. Manag. Inf. Syst. 2018, 35, 424–460. [Google Scholar] [CrossRef]

- Kshetri, N. Big data’s role in expanding access to financial services in China. Int. J. Inf. Manag. 2016, 36, 297–308. [Google Scholar] [CrossRef]

- Mikalef, P.; Krogstie, J.; Pappas, I.O.; Pavlou, P. Exploring the relationship between big data analytics capability and competitive performance: The mediating roles of dynamic and operational capabilities. Inf. Manag. 2020, 57, 103169. [Google Scholar] [CrossRef]

- Battisti, E.; Shams, S.R.; Sakka, G.; Miglietta, N. Big data and risk management in business processes: Implications for corporate real estate. Bus. Process Manag. J. 2020, 26, 1141–1155. [Google Scholar] [CrossRef]

- Broby, D. Financial technology and the future of banking. Financ. Innov. 2021, 7, 47. [Google Scholar] [CrossRef]

- Hentzen, J.K.; Hoffmann, A.; Dolan, R.; Pala, E. Artificial intelligence in customer-facing financial services: A systematic literature review and agenda for future research. Int. J. Bank Mark. 2022, 40, 1299–1336. [Google Scholar] [CrossRef]

- Shihembetsa, E. Use of Artificial Intelligence Algorithms to Enhance Fraud Detection in the Banking Industry. Ph.D. thesis, University of Nairobi, Nairobi, Kenya, 2021. [Google Scholar]

- Königstorfer, F.; Thalmann, S. Applications of Artificial Intelligence in commercial banks—A research agenda for behavioral finance. J. Behav. Exp. Financ. 2020, 27, 100352. [Google Scholar] [CrossRef]

- Sheth, J.N.; Jain, V.; Roy, G.; Chakraborty, A. AI-driven banking services: The next frontier for a personalised experience in the emerging market. Int. J. Bank Mark. 2022, 40, 1248–1271. [Google Scholar] [CrossRef]

- Ris, K.; Stankovic, Z.; Avramovic, Z. Implications of implementation of artificial intelligence in the banking business with correlation to the human factor. J. Comput. Commun. 2020, 8, 130. [Google Scholar] [CrossRef]

- Rahman, M.; Ming, T.H.; Baigh, T.A.; Sarker, M. Adoption of artificial intelligence in banking services: An empirical analysis. Int. J. Emerg. Mark. 2023, 18, 4270–4300. [Google Scholar] [CrossRef]

- Riikkinen, M.; Saarijärvi, H.; Sarlin, P.; Lähteenmäki, I. Using artificial intelligence to create value in insurance. Int. J. Bank Mark. 2018, 36, 1145–1168. [Google Scholar] [CrossRef]

- Boustani, N.M. Artificial intelligence impact on banks clients and employees in an Asian developing country. J. Asia Bus. Stud. 2022, 16, 267–278. [Google Scholar] [CrossRef]

- Hon, W.K.; Millard, C. Banking in the cloud: Part 1—Banks’ use of cloud services. Comput. Law Secur. Rev. 2018, 34, 4–24. [Google Scholar] [CrossRef]

- Habib, G.; Sharma, S.; Ibrahim, S.; Ahmad, I.; Qureshi, S.; Ishfaq, M. Blockchain technology: Benefits, challenges, applications, and integration of blockchain technology with cloud computing. Future Internet 2022, 14, 341. [Google Scholar] [CrossRef]

- Chen, X.; You, X.; Chang, V. FinTech and commercial banks’ performance in China: A leap forward or survival of the fittest? Technol. Forecast. Soc. Change 2021, 166, 120645. [Google Scholar] [CrossRef]

- Calderon-Monge, E.; Ribeiro-Soriano, D. The role of digitalization in business and management: A systematic literature review. Rev. Manag. Sci. 2024, 18, 449–491. [Google Scholar] [CrossRef]

- Golightly, L.; Chang, V.; Xu, Q.A.; Gao, X.; Liu, B.S. Adoption of cloud computing as innovation in the organization. Int. J. Eng. Bus. Manag. 2022, 14, 18479790221093992. [Google Scholar] [CrossRef]

- Subramanian, N.; Jeyaraj, A. Recent security challenges in cloud computing. Comput. Electr. Eng. 2018, 71, 28–42. [Google Scholar] [CrossRef]

- Bhat, J.R.; AlQahtani, S.A.; Nekovee, M. FinTech enablers, use cases, and role of future internet of things. J. King Saud. Univ. Comput. Inf. Sci. 2023, 35, 87–101. [Google Scholar] [CrossRef]

- Olugbade, S.; Ojo, S.; Imoize, A.L.; Isabona, J.; Alaba, M.O. A review of artificial intelligence and machine learning for incident detectors in road transport systems. Math. Comput. Appl. 2022, 27, 77. [Google Scholar] [CrossRef]

- Guo, L.; Chen, J.; Li, S.; Li, Y.; Lu, J. A blockchain and IoT-based lightweight framework for enabling information transparency in supply chain finance. Digit. Commun. Netw. 2022, 8, 576–587. [Google Scholar] [CrossRef]

- Singh, P.R.; Singh, V.K.; Yadav, R.; Chaurasia, S.N. 6G networks for artificial intelligence-enabled smart cities applications: A scoping review. Telemat. Inform. Rep. 2023, 9, 100044. [Google Scholar] [CrossRef]

- Shamshad, S.; Riaz, F.; Riaz, R.; Rizvi, S.S.; Abdulla, S. An enhanced architecture to resolve public-key cryptographic issues in the internet of things (IoT), employing quantum computing supremacy. Sensors 2022, 22, 8151. [Google Scholar] [CrossRef]

- Biju, A.K.V.N.; Thomas, A.S.; Thasneem, J. Examining the research taxonomy of artificial intelligence, deep learning & machine learning in the financial sphere—A bibliometric analysis. Qual. Quant. 2024, 58, 849–878. [Google Scholar]

- Omolara, A.E.; Alabdulatif, A.; Abiodun, O.I.; Alawida, M.; Alabdulatif, A.; Arshad, H. The internet of things security: A survey encompassing unexplored areas and new insights. Comput. Secur. 2022, 112, 102494. [Google Scholar] [CrossRef]

- Tseng, F.M.; Liang, C.W.; Nguyen, N.B. Blockchain technology adoption and business performance in large enterprises: A comparison of the United States and China. Technol. Soc. 2023, 73, 102230. [Google Scholar] [CrossRef]

- Peng, H.; Luxin, W. Digital economy and business investment efficiency: Inhibiting or facilitating? Res. Int. Bus. Financ. 2022, 63, 101797. [Google Scholar]

- Hald, K.S.; Kinra, A. How the blockchain enables and constrains supply chain performance. Int. J. Phys. Distrib. Logist. Manag. 2019, 49, 376–397. [Google Scholar] [CrossRef]

- Alhassan, U. E-government and the impact of remittances on new business creation in developing countries. Econ. Change Restruct. 2023, 56, 181–214. [Google Scholar] [CrossRef]

- Guermond, V. Remittance-scapes: The contested geographies of remittance management. Prog. Hum. Geogr. 2022, 46, 372–397. [Google Scholar] [CrossRef]

- Song, H.; Han, S.; Yu, K. Blockchain-enabled supply chain operations and financing: The perspective of expectancy theory. Int. J. Oper. Prod. Manag. 2023, 43, 1943–1975. [Google Scholar] [CrossRef]

- Dashottar, S.; Srivastava, V. Corporate banking—Risk management, regulatory and reporting framework in India: A Blockchain application-based approach. J. Bank. Regul. 2021, 22, 39–51. [Google Scholar] [CrossRef]

- Beiderbeck, D.; Frevel, N.; von der Gracht, H.A.; Schmidt, S.L.; Schweitzer, V.M. Preparing, conducting, and analyzing Delphi surveys: Cross-disciplinary practices, new directions, and advancements. MethodsX 2021, 8, 101401. [Google Scholar] [CrossRef]

- Barrios, M.; Guilera, G.; Nuño, L.; Gómez-Benito, J. Consensus in the delphi method: What makes a decision change? Technol. Forecast. Soc. Change 2021, 163, 120484. [Google Scholar] [CrossRef]

- da Silveira Junior, L.A.B.; Vasconcellos, E.; Guedes, L.V.; Guedes, L.F.A.; Costa, R.M. Technology roadmapping: A methodological proposition to refine Delphi results. Technol. Forecast. Soc. Change 2018, 126, 194–206. [Google Scholar] [CrossRef]

- Humphrey-Murto, S.; De Wit, M. The Delphi method—More research please. J. Clin. Epidemiol. 2019, 106, 136–139. [Google Scholar] [CrossRef]

- Quirke, F.A.; Battin, M.R.; Bernard, C.; Biesty, L.; Bloomfield, F.H.; Daly, M.; Devane, D. Multi-Round versus Real-Time Delphi survey approach for achieving consensus in the COHESION core outcome set: A randomised trial. Trials 2023, 24, 461. [Google Scholar] [CrossRef]

- Sánchez-Garrido, A.J.; Navarro, I.J.; García, J.; Yepes, V. An adaptive ANP & ELECTRE IS-based MCDM model using quantitative variables. Mathematics 2022, 10, 2009. [Google Scholar] [CrossRef]

- Taherdoost, H.; Madanchian, M. Analytic Network Process (ANP) method: A comprehensive review of applications, advantages, and limitations. J. Data Sci. Intell. Syst. 2023, 1, 12–18. [Google Scholar] [CrossRef]

- Saaty, T.L. The analytic hierarchy and analytic network processes for the measurement of intangible criteria and for decision-making. In Multiple Criteria Decision Analysis: State of the Art Surveys; Springer: Berlin/Heidelberg, Germany, 2016; pp. 363–419. [Google Scholar]

- Sohst, R.R.; Acostamadiedo, E.; Tjaden, J. Reducing uncertainty in Delphi surveys. Demogr. Res. 2023, 49, 983–1020. [Google Scholar] [CrossRef]

- Kadoić, N. Characteristics of the analytic network process, a multi-criteria decision-making method. Croat. Oper. Res. Rev. 2018, 9, 235–244. [Google Scholar] [CrossRef]

- Balaji, K. IoT in Financial Services Innovations in Banking and Insurance. In Managing Customer-Centric Strategies in the Digital Landscape; IGI Global: Hershey, PA, USA, 2025; pp. 75–104. [Google Scholar]

- Belanche, D.; Casaló, L.V.; Flavián, C. Artificial Intelligence in FinTech: Understanding robo-advisors adoption among customers. Ind. Manag. Data Syst. 2019, 119, 1411–1430. [Google Scholar] [CrossRef]

- Zhu, Y.; Jin, S. How does the digital transformation of banks improve efficiency and environmental, social, and governance performance? Systems 2023, 11, 328. [Google Scholar] [CrossRef]

- Musara, M.; Fatoki, O. Has technological innovations resulted in increased efficiency and cost savings for banks’ customers? Afr. J. Bus. Manag. 2010, 4, 1813. [Google Scholar]

- Love, I.; Martinez Pería, M.S.; Singh, S. Collateral registries for movable assets: Does their introduction spur firms’ access to bank financing? J. Financ. Serv. Res. 2016, 49, 1–37. [Google Scholar] [CrossRef]

- Krishnakumar, A. Quantum Computing and Blockchain in Business: Exploring the Applications, Challenges, and Collision of Quantum Computing and Blockchain; Packt Publishing Ltd.: Birmingham, UK, 2020. [Google Scholar]

- Hall, B.D. The Problem with ‘Dimensionless Quantities’. In Proceedings of the 10th International Conference on Model-Driven Engineering and Software Development (MODELSWARD 2022), Online, 6–8 February 2022; pp. 116–125. [Google Scholar]

- Rahmani, F.M.; Zohuri, B. The transformative impact of AI on financial institutions, with a focus on banking. J. Eng. Appl. Sci. Technol. 2023, 5, 1–6, SRC/JEAST-279. [Google Scholar]

- Jomon Jose, M.; Aithal, P.S. An analytical study of applications of artificial intelligence on banking practices. Int. J. Manag. Technol. Soc. Sci. (IJMTS) 2023, 8, 133–144. [Google Scholar]

- Berisha, B.; Mëziu, E.; Shabani, I. Big data analytics in Cloud computing: An overview. J. Cloud Comput. 2022, 11, 24. [Google Scholar] [CrossRef] [PubMed]

- Panarello, A.; Tapas, N.; Merlino, G.; Longo, F.; Puliafito, A. Blockchain and iot integration: A systematic survey. Sensors 2018, 18, 2575. [Google Scholar] [CrossRef] [PubMed]

- Berger, A.N.; Hasan, I.; Zhou, M. Bank ownership and efficiency in China: What will happen in the world’s largest nation? J. Bank. Financ. 2009, 33, 113–130. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Expert | Organization | Experience | Education | Research Specialization |

|---|---|---|---|---|

| 1 | State-owned commercial bank | 15 years | Ph.D. | Commercial bank operations |

| 2 | National joint-stock bank | 10 years | Ph.D. | Fintech innovation and application |

| 3 | Local commercial bank | 12 years | Master | Electronic banking and payment |

| 4 | Economic research institution | 15 years | Ph.D. | Fintech market analysis |

| 5 | Fintech company | 8 years | Master | Fintech products and services |

| 6 | University finance department | 18 years | Ph.D. | Fintech theory and practice |

| 7 | Government financial regulator | 20 years | Ph.D. | Fintech policies and regulations |

| 8 | Private financial institution | 20 years | Master | Fintech risk assessment |

| 9 | International bank | 10 years | Ph.D. | Global fintech trends |

| 10 | Innovative financial enterprise | 7 years | Master | Fintech innovation |

| No. | Observation Indicators Formed by Experts | S | CV | |

|---|---|---|---|---|

| 1 | Risk Management Capability | 4.67 | 0.50 | 0.11 |

| 2 | Precision Marketing Capability | 5.00 | 0.00 | 0.00 |

| 3 | Operational Efficiency Optimization Capability | 4.67 | 0.50 | 0.11 |

| 4 | Robo-advisors Services | 5.00 | 0.48 | 0.10 |

| 5 | Chatbots Efficiency | 4.33 | 0.50 | 0.12 |

| 6 | Intelligent Identification Efficiency | 4.00 | 0.58 | 0.15 |

| 7 | Regulatory and Compliance Assistance Capability | 4.67 | 0.60 | 0.13 |

| 8 | Information Data Integration Capability | 4.67 | 0.58 | 0.12 |

| 9 | Business Cost Reduction Capability | 4.33 | 0.50 | 0.12 |

| 10 | Data Security Protection Capability | 5.00 | 0.48 | 0.10 |

| 11 | Movable Property Pledge Financing Capability | 5.00 | 0.00 | 0.00 |

| 12 | Insurance Business Innovation Capability | 4.67 | 0.58 | 0.12 |

| 13 | Payment Function Optimization Capability | 4.00 | 0.48 | 0.12 |

| 14 | Machine Fault Detection Capability | 4.33 | 0.48 | 0.11 |

| 15 | Digital Credit Financing Services | 4.67 | 0.58 | 0.12 |

| 16 | Digital Payment Settlement Services | 5.00 | 0.48 | 0.10 |

| 17 | Digital Bill Discounting Services | 4.67 | 0.48 | 0.10 |

| 18 | Asset Custody and Clearing Services | 5.00 | 0.58 | 0.12 |

| Dimension | Observation Indicator | Measurement |

|---|---|---|

| Big Data Applications (A) | Risk Management Capability (A1) | Measured by the cumulative success rate of commercial banks using big data technology to prevent loan default risks in the current year. |

| Precision Marketing Capability (A2) | Measured by the increase in the success rate of marketing using big data technology by commercial banks compared to the previous year. | |

| Operational Efficiency Optimization Capability (A3) | Measured by the total time reduction in business processing by commercial banks using big data technology in the current year. | |

| Artificial Intelligence Applications (B) | Robo-advisors Services (B1) | Measured by the cumulative number of clients served by intelligent investment advisory services of commercial banks in the current year. |

| Chatbots Efficiency (B2) | Measured by the number of human replacements achieved through intelligent customer service machines by commercial banks in the current year. | |

| Intelligent Identification Efficiency (B3) | Measured by the average monthly business volume processed through intelligent identification ports by commercial banks in the current year. | |

| Regulatory and Compliance Assistance Capability (B4) | Measured by the cumulative number of regulatory risks identified using artificial intelligence technology by commercial banks in the current year. | |

| Cloud Computing Applications (C) | Information Data Integration Capability (C1) | Measured by the cumulative number of times customer data has been integrated using cloud computing technology by commercial banks in the current year. |

| Business Cost Reduction Capability (C2) | Measured by the difference in IT expenditures based on cloud computing technology between the previous year and the current year for commercial banks. | |

| Data Security Protection Capability (C3) | Measured by the cumulative number of data security risks encountered during data transmission in the cloud by commercial banks in the current year. The higher this number, the weaker the bank’s data security protection capability. | |

| Internet of Things Applications (D) | Movable Property Pledge Financing Capability (D1) | Measured by the cumulative number of clients served with movable property pledge financing by commercial banks in the current year. |

| Insurance Business Innovation Capability (D2) | Measured by the cumulative number of transactions completed through the UBI port by commercial banks in the current year. | |

| Payment Function Optimization Capability (D3) | Measured by the cumulative working days since the activation of photon payment methods by commercial banks, recorded as 0 if not activated. | |

| Machine Fault Detection Capability (D4) | Measured by the cumulative number of ATM malfunctions detected using IoT sensing technology by commercial banks in the current year. | |

| Blockchain Applications (E) | Digital Credit Financing Services (E1) | Measured by the cumulative number of small and micro enterprises served with digital credit financing by commercial banks in the current year. |

| Digital Payment Settlement Services (E2) | Measured by the cumulative transaction volume of cross-border currency settlements conducted using blockchain technology by commercial banks in the current year. | |

| Digital Bill Discounting Services (E3) | Measured by the volume of bill discounting transactions based on blockchain technology by commercial banks in the current year. | |

| Asset Custody and Clearing Services (E4) | Measured by the cumulative business volume at the asset custody settlement port based on blockchain technology by commercial banks in the current year. |

| Matrix Order (n) | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| R·I | 0 | 0 | 0.58 | 0.90 | 1.12 | 1.24 | 1.32 | 1.41 | 1.45 | 1.49 |

| Judgment Matrices | G | A | B | C | D | E |

|---|---|---|---|---|---|---|

| C·R | 0.08179 | 0.01759 | 0.02463 | 0.00855 | 0.02660 | 0.01160 |

| Evaluation Dimension | Standardized Weights | Observation Indicator | Standardized Weights | Limit Value |

|---|---|---|---|---|

| Big Data Applications (A) | 0.24881 | Risk Management Capability (A1) | 0.10108 | 0.02027 |

| Precision Marketing Capability (A2) | 0.63857 | 0.12721 | ||

| Operational Efficiency Optimization Capability (A3) | 0.26035 | 0.03215 | ||

| Artificial Intelligence Applications (B) | 0.32428 | Robo-advisors Services (B1) | 0.47974 | 0.14808 |

| Chatbots Efficiency (B2) | 0.19143 | 0.02136 | ||

| Intelligent Identification Efficiency (B3) | 0.10239 | 0.01305 | ||

| Regulatory and Compliance Assistance Capability (B4) | 0.22644 | 0.03421 | ||

| Cloud Computing Applications (C) | 0.17587 | Information Data Integration Capability (C1) | 0.39034 | 0.08833 |

| Business Cost Reduction Capability (C2) | 0.16475 | 0.03728 | ||

| Data Security Protection Capability (C3) | 0.44491 | 0.10068 | ||

| Internet of Things Applications (D) | 0.10728 | Movable Property Pledge Financing Capability (D1) | 0.41221 | 0.08757 |

| Insurance Business Innovation Capability (D2) | 0.15437 | 0.03674 | ||

| Payment Function Optimization Capability (D3) | 0.32506 | 0.05305 | ||

| Machine Fault Detection Capability (D4) | 0.10836 | 0.02103 | ||

| Blockchain Applications (E) | 0.14376 | Digital Credit Financing Services (E1) | 0.45599 | 0.07882 |

| Digital Payment Settlement Services (E2) | 0.35485 | 0.06534 | ||

| Digital Bill Discounting Services (E3) | 0.07065 | 0.01301 | ||

| Asset Custody and Clearing Services (E4) | 0.11851 | 0.02182 |

| Name of Bank | Big Data Applications | Artificial Intelligence Applications | Cloud Computing Applications | Internet of Things Applications | Blockchain Applications | Composite Score | Ranking |

|---|---|---|---|---|---|---|---|

| ICBC | 9.18360 | 9.19847 | 8.78893 | 9.05813 | 8.68046 | 9.03322 | 1 |

| CCB | 9.02673 | 8.10726 | 8.86928 | 8.94386 | 8.87206 | 8.66975 | 3 |

| ABC | 8.16045 | 8.06225 | 8.14873 | 8.10546 | 8.15287 | 8.11956 | 5 |

| BOC | 8.31093 | 9.25247 | 8.20380 | 7.66713 | 8.59426 | 8.56908 | 4 |

| PSBC | 7.17706 | 7.03306 | 6.77173 | 6.54531 | 7.11686 | 6.98265 | 12 |

| BOCOM | 7.89385 | 8.08285 | 7.27266 | 8.45746 | 8.20043 | 7.95043 | 7 |

| CMB | 9.09883 | 9.12393 | 8.40880 | 8.49925 | 8.98585 | 8.90505 | 2 |

| CIB | 6.05621 | 6.64551 | 7.28562 | 7.02046 | 6.04068 | 6.56474 | 15 |

| PAB | 8.21686 | 7.79213 | 8.10113 | 8.02033 | 8.05047 | 8.01377 | 6 |

| SPDB | 7.84856 | 6.93186 | 7.35453 | 7.20687 | 7.98845 | 7.41568 | 10 |

| CMBC | 6.67380 | 6.58153 | 6.36920 | 7.25860 | 7.54846 | 6.77879 | 14 |

| CITIC | 7.63541 | 8.30835 | 6.86403 | 7.35106 | 8.25646 | 7.77675 | 8 |

| CEB | 7.56603 | 7.50427 | 6.74426 | 8.46918 | 8.21732 | 7.59200 | 9 |

| BON | 6.19156 | 6.07661 | 6.42887 | 7.02014 | 7.43893 | 6.46423 | 16 |

| BOJ | 6.84628 | 6.64599 | 7.08566 | 7.16693 | 6.58893 | 6.82083 | 13 |

| BOB | 7.50073 | 7.04167 | 6.99060 | 7.26307 | 6.83633 | 7.14114 | 11 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, X.; Hu, W.; Guan, N. A Systemic Approach to Evaluating Fintech-Driven Competitiveness in Commercial Banks: Integrating Delphi and ANP Methods. Systems 2025, 13, 342. https://doi.org/10.3390/systems13050342

Wang X, Hu W, Guan N. A Systemic Approach to Evaluating Fintech-Driven Competitiveness in Commercial Banks: Integrating Delphi and ANP Methods. Systems. 2025; 13(5):342. https://doi.org/10.3390/systems13050342

Chicago/Turabian StyleWang, Xin, Wenxiu Hu, and Na Guan. 2025. "A Systemic Approach to Evaluating Fintech-Driven Competitiveness in Commercial Banks: Integrating Delphi and ANP Methods" Systems 13, no. 5: 342. https://doi.org/10.3390/systems13050342

APA StyleWang, X., Hu, W., & Guan, N. (2025). A Systemic Approach to Evaluating Fintech-Driven Competitiveness in Commercial Banks: Integrating Delphi and ANP Methods. Systems, 13(5), 342. https://doi.org/10.3390/systems13050342