Can Green Credit Improve the Innovation of Enterprise Green Technology: Evidence from 271 Cities in China

Abstract

1. Introduction

2. Research Methods and Data Sources

2.1. Spatial Correlation Analysis

2.2. Spatial Measurement Modeling

2.2.1. Model Setup

2.2.2. Description of Variables

2.3. Data Sources

3. Characterization Facts

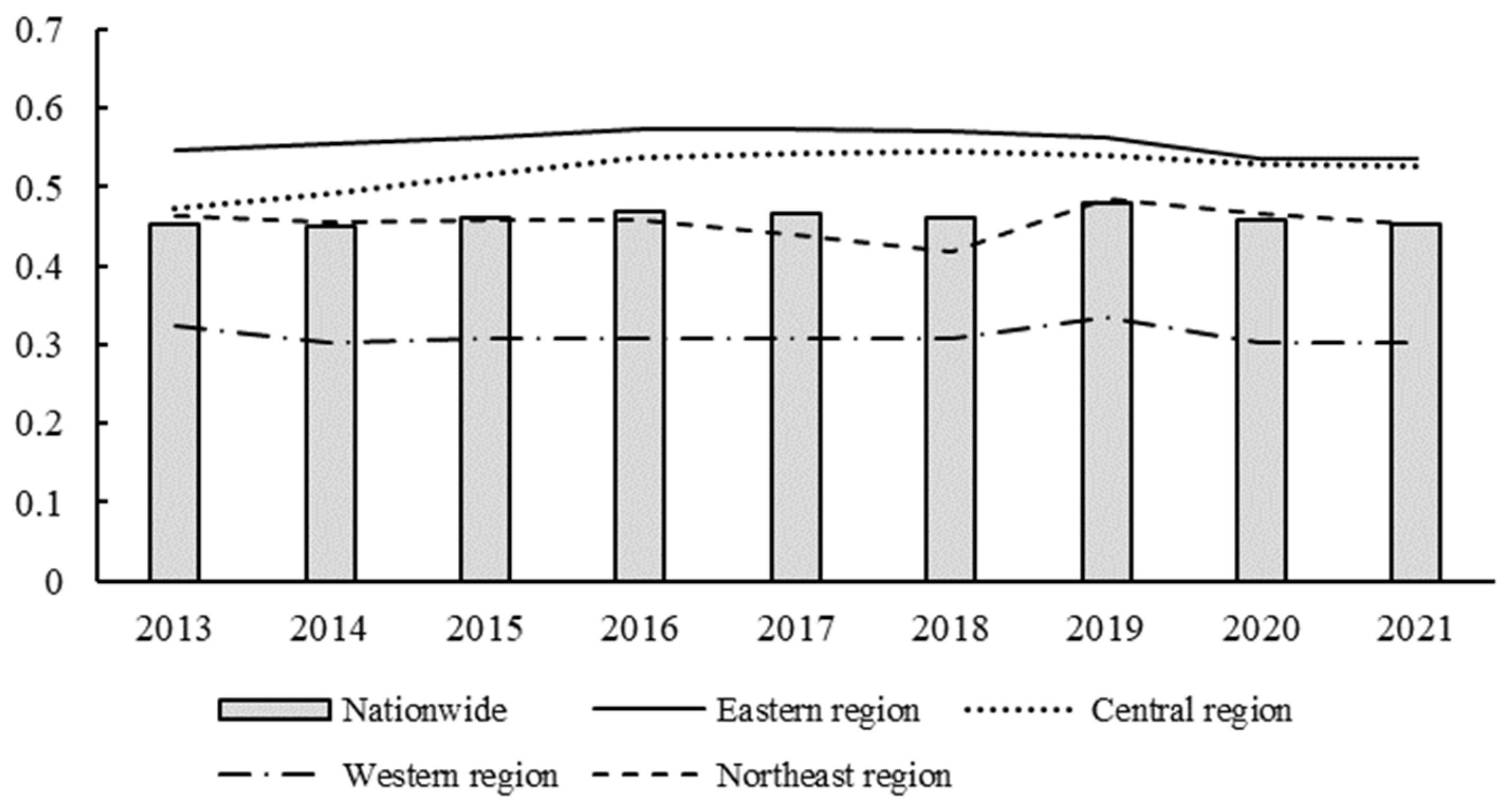

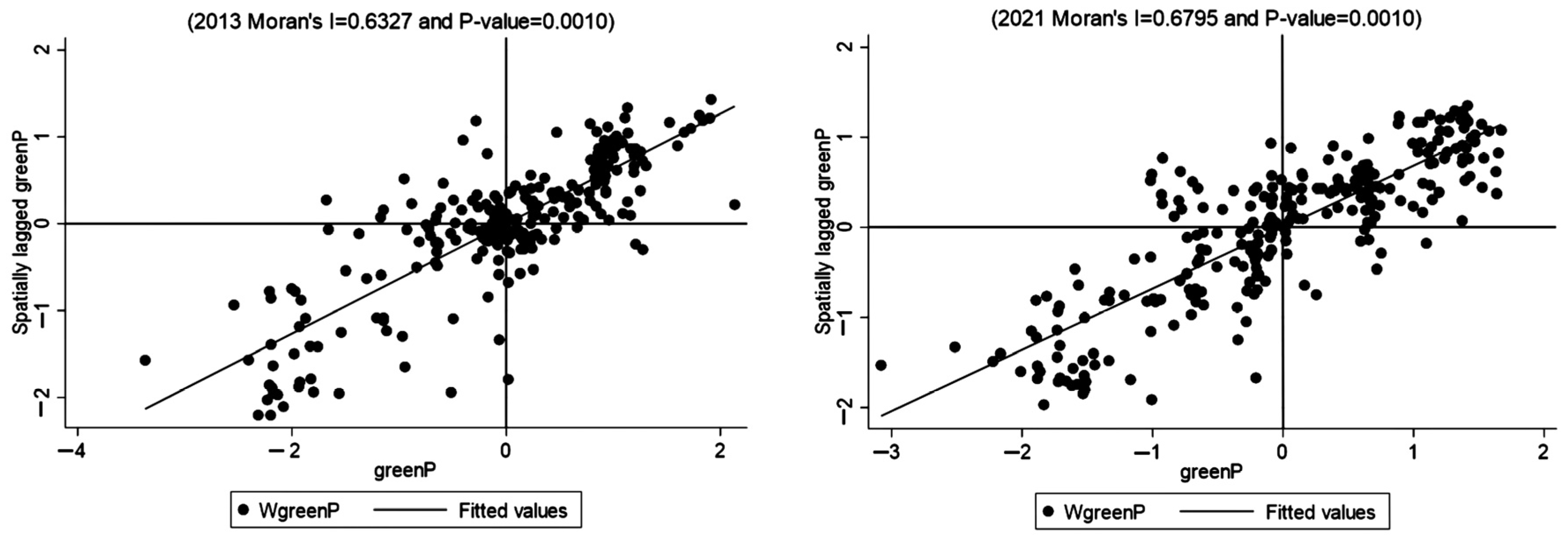

3.1. Spatial and Temporal Characteristics of Green Credit

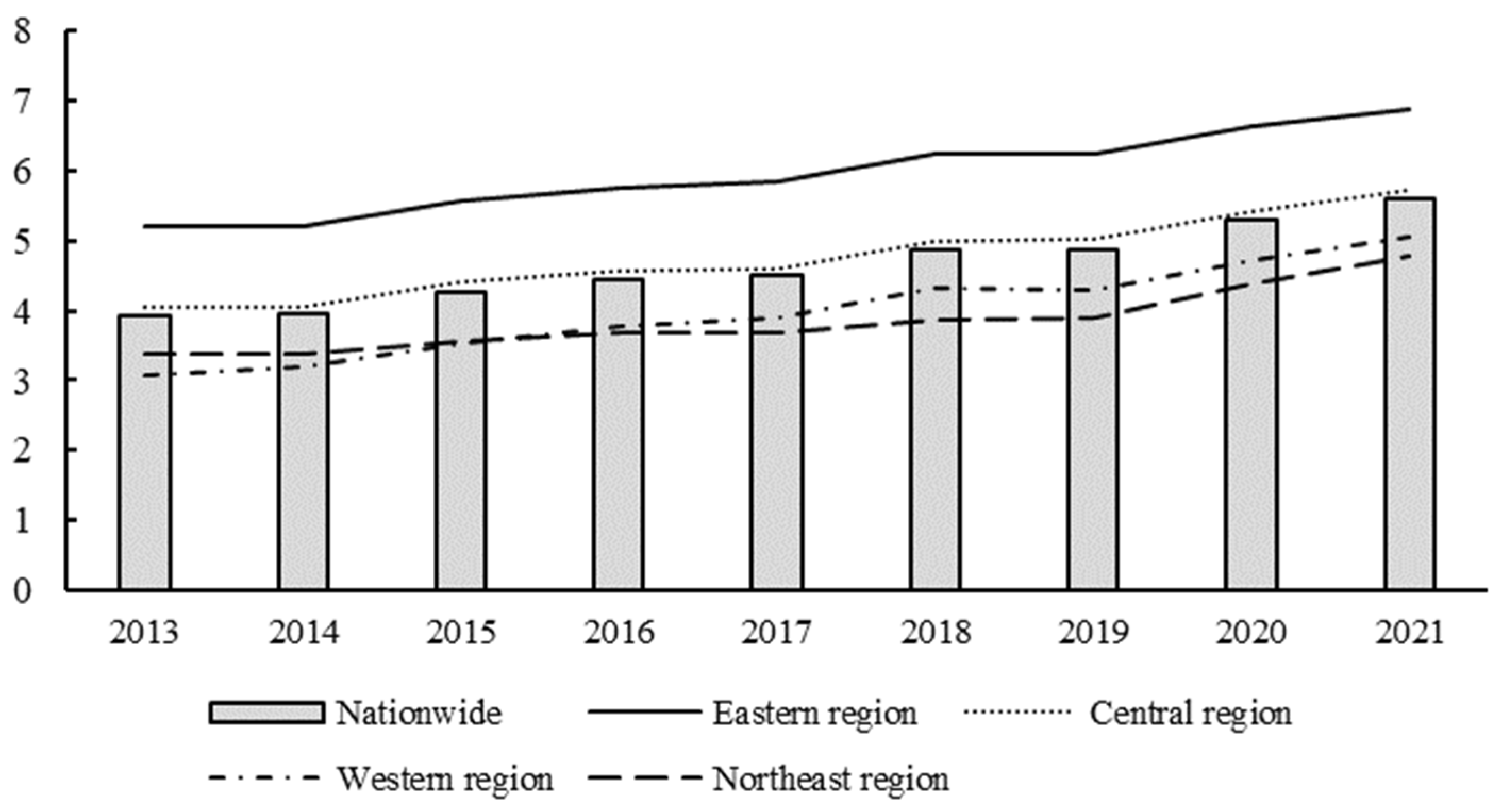

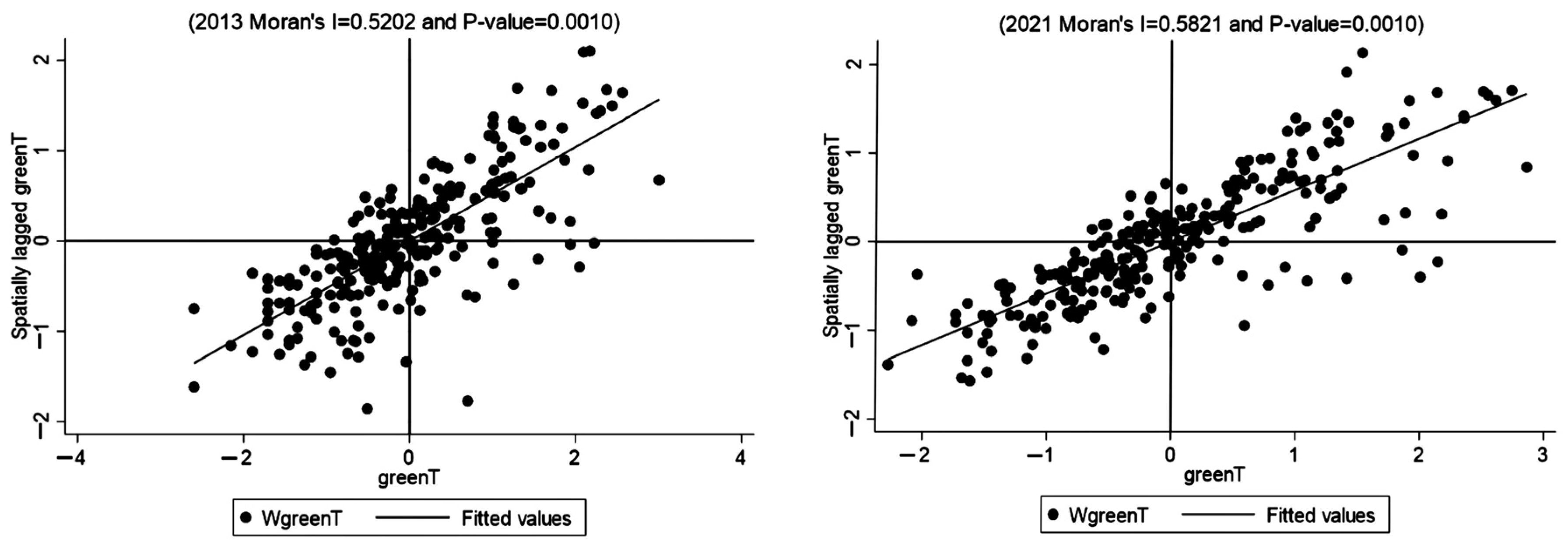

3.2. Spatial and Temporal Characteristics of Enterprises Green Technological Innovation

4. Mechanism Analysis and Empirical Testing

4.1. Mechanism Analysis

4.2. Model Testing and Selection

4.3. Benchmark Regression Results

4.4. Analysis of Regional Heterogeneity

4.5. Robustness Tests

4.6. Endogeneity Test

4.6.1. DIF-GMM Estimation

4.6.2. Instrumental Variables

4.6.3. Adding Control Variables

4.6.4. Conduction Mechanism Test

5. Conclusions and Policy Implications

5.1. Conclusions

5.2. Policy Implications

6. Discussion

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Boubaker, S.; Liu, P.Z.; Ren, Y.S.; Ma, C.Q. Do anti-corruption campaigns affect corporate environmental responsibility? Evidence from China. Int. Rev. Financ. Anal. 2024, 91, 102961. [Google Scholar] [CrossRef]

- Fan, M.; Yang, P.; Li, Q. Impact of environmental regulation on green total factor productivity: A new perspective of green technological innovation. Environ. Sci. Pollut. Res. 2022, 29, 53785–53800. [Google Scholar] [CrossRef]

- Cui, X.; Wang, P.; Sensoy, A.; Nguyen, D.K.; Pan, Y.Y. Green Credit Policy and Corporate Productivity: Evidence from a quasi-natural experiment in China. Technol. Forecast. Soc. Change 2022, 177, 121516. [Google Scholar] [CrossRef]

- Hua, Y.B. Assessing financial inclusion co-movement with low-carbon development index: Implications for regional development. Environ. Sci. Pollut. Res. 2023, 30, 104791–104804. [Google Scholar] [CrossRef]

- Matiiuk, Y.; Liobikiene, G. The role of financial, informational, and social tools on resource-saving behaviour in Lithuania: Assumptions and reflections of real situation. J. Clean. Prod. 2021, 326, 129378. [Google Scholar] [CrossRef]

- Madaleno, M.; Nogueira, M.C. How Renewable Energy and CO2 Emissions Contribute to Economic Growth, and Sustainability—An Extensive Analysis. Sustainability 2023, 15, 4089. [Google Scholar] [CrossRef]

- Li, X.; Wu, M.; Shi, C.M.; Chen, Y. Impacts of green credit policies and information asymmetry: From market perspective. Resour. Policy 2023, 81, 103395. [Google Scholar] [CrossRef]

- Umar, M.; Ji, X.F.; Mirza, N.; Naqvi, B. Carbon neutrality, bank lending, and credit risk: Evidence from the Eurozone. J. Environ. Manag. 2021, 296, 113156. [Google Scholar] [CrossRef] [PubMed]

- He, W.H.; Liu, P.; Lin, B.R.; Zhou, H.; Chen, X.S. Green finance support for development of green buildings in China: Effect, mechanism, and policy implications. Energy Policy 2022, 165, 112973. [Google Scholar] [CrossRef]

- Cui, H.R.; Wang, R.Y.; Wang, H.R. An evolutionary analysis of green finance sustainability based on multi-agent game. J. Clean. Prod. 2020, 269, 121799. [Google Scholar] [CrossRef]

- Chang, Y.; Fang, Z.; Li, Y.F. Renewable energy policies in promoting financing and investment among the East Asia Summit countries: Quantitative assessment and policy implications. Energy Policy 2016, 95, 427–436. [Google Scholar] [CrossRef]

- Yu, B.; Liu, L.; Chen, H. Can green finance improve the financial performance of green enterprises in China? Int. Rev. Econ. Financ. 2023, 88, 1287–1300. [Google Scholar] [CrossRef]

- Lv, C.C.; Fan, J.F.; Lee, C.C. Can green credit policies improve corporate green production efficiency? J. Clean. Prod. 2023, 39, 136573. [Google Scholar] [CrossRef]

- Tang, Y.M.; Wang, L.; Peng, S.G. Green credit policy, government subsidy, and enterprises “shifting from virtual to real”. Environ. Sci. Pollut. Res. 2024, 31, 3976–3994. [Google Scholar] [CrossRef] [PubMed]

- Lin, B.Q.; Pan, T. The impact of green credit on green transformation of heavily polluting enterprises: Reverse forcing or forward pushing? Energy Policy 2023, 184, 113901. [Google Scholar] [CrossRef]

- Luo, S.M.; Yu, S.H.; Zhou, G.Y. Does green credit improve the core competence of commercial banks. Based on quasi-natural experiments in China. Energy Econ. 2021, 100, 105335. [Google Scholar] [CrossRef]

- Lian, Y.H.; Gao, J.Y.; Ye, T. How does green credit affect the financial performance of commercial banks?—Evidence from China. J. Clean. Prod. 2022, 344, 131069. [Google Scholar] [CrossRef]

- Lai, X.; Yue, S.; Chen, H. Can green credit increase firm value? Evidence from Chinese listed new energy companies. Environ. Sci. Pollut. Res. 2022, 29, 18702–18720. [Google Scholar] [CrossRef]

- An, X.; Ding, Y.; Wang, Y. Green credit and bank risk: Does corporate social responsibility matter? Financ. Res. Lett. 2023, 58, 104349. [Google Scholar] [CrossRef]

- Wang, Y.Y.; Zhang, Y.Y. Remanufacturer’s production strategy with capital constraint and differentiated demand. J. Intell. Manuf. 2017, 28, 869–882. [Google Scholar] [CrossRef]

- Chinzara, Z.; Lahiri, R.; Chen, E.T. Financial liberalization and sectoral reallocation of capital in South Africa. Empir. Econ. 2017, 52, 309–356. [Google Scholar] [CrossRef]

- Nguyen, T.T. An Analysis of Non-Performing Loans, Non-Performing Loans to Loan Loss Reserves, and Diversification Effects on Lending: Three Essays; University of Southampton: Southampton, UK, 2021. [Google Scholar]

- Akhter, N. Determinants of commercial bank’s non-performing loans in Bangladesh: An empirical evidence. Cogent Econ. Financ. 2023, 11, 2194128. [Google Scholar] [CrossRef]

- Tian, J.F.; Sun, S.Y.; Cao, W.; Bu, D.; Xue, R. Make every dollar count: The impact of green credit regulation on corporate green investment efficiency. Energy Econ. 2024, 130, 107307. [Google Scholar] [CrossRef]

- Zhou, J.; Yin, Z.C.; Yue, P.P. The impact of access to credit on energy efficiency. Financ. Res. Lett. 2023, 51, 103472. [Google Scholar] [CrossRef]

- Wang, H.R.; Cui, H.R.; Zhao, Q.Z. Effect of Green Technology Innovation on Green Total Factor Productivity in China: Evidence from Spatial Durbin Model Analysis. J. Clean. Prod. 2020, 288, 125624. [Google Scholar] [CrossRef]

- Montmartin, B.; Herrera, M. Internal and external effects of R&D subsidies and fiscal incentives: Empirical evidence using spatial dynamic panel models. Res. Policy 2015, 44, 1065–1079. [Google Scholar]

- Zhou, F.X.; Wang, X.Y. The carbon emissions trading scheme and green technology innovation in China: A new structural economics perspective. Econ. Anal. Policy 2022, 74, 365–381. [Google Scholar] [CrossRef]

- Fernando, Y.; Wah, W.X.; Shaharudin, M.S. Does a firm’s innovation category matter in practising eco-innovation? Evidence from the lens of Malaysia companies practicing green technology. J. Manuf. Technol. Manag. 2016, 27, 208–233. [Google Scholar] [CrossRef]

- Duan, Y.L.; Mu, C.; Yang, M.; Deng, Z.Q.; Chin, T.C.; Zhou, L.; Fang, Q.F. Study on early warnings of strategic risk during the process of firms’ sustainable innovation based on an optimized genetic BP neural networks model: Evidence from Chinese manufacturing firms. Int. J. Prod. Econ. 2021, 242, 108293. [Google Scholar] [CrossRef]

- Zhang, J.X.; Ding, X.H.; Bao, L.Y.; Zhang, Y.D. Can the Greening of Financial Markets Be Transmitted to the Real Economy as Desired in China? Systems 2023, 11, 11030161. [Google Scholar] [CrossRef]

- Zhang, J.J.; Luo, Y.C.; Ding, X.H. Can green credit policy improve the overseas investment efficiency of enterprises in China? J. Clean. Prod. 2022, 340, 130785. [Google Scholar] [CrossRef]

- Meng, Z.S.; Sun, H.K.; Liu, X.T. Impact of green fiscal policy on the investment efficiency of renewable energy enterprises in China. Environ. Sci. Pollut. Res. 2022, 29, 76216–76234. [Google Scholar] [CrossRef] [PubMed]

- Guo, S.; Zhang, Z.X. Green credit policy and total factor productivity: Evidence from Chinese listed companies. Energy Econ. 2023, 128, 107115. [Google Scholar] [CrossRef]

- Hussain, J.; Lee, C.C.; Chen, Y. Optimal green technology investment and emission reduction in emissions generating companies under the support of green bond and subsidy. Technol. Forecast. Soc. Change 2022, 183, 121952. [Google Scholar] [CrossRef]

- Zhang, H.; Zhang, F.R.; Gong, B.; Zhang, X.; Zhu, Y.F. The Optimization of Supply Chain Financing for Bank Green Credit Using Stackelberg Game Theory in Digital Economy Under Internet of Things. J. Organ. End User Comput. 2023, 35, 318474. [Google Scholar] [CrossRef]

- Geng, L.M.; Yin, W.X.; Wu, X.X.; Zhang, C. How green credit affects corporate environmental information disclosure: Evidence from new energy listed companies in China. Front. Ecol. Evol. 2023, 11, 1301589. [Google Scholar] [CrossRef]

- Wu, S.; Zhou, X.Y. A theoretical framework for modeling dual-track granting orientation in green credit policy. Econ. Anal. Policy 2024, 81, 249–268. [Google Scholar] [CrossRef]

- Wang, H.T.; Qi, S.Z.; Zhou, C.B.; Huang, X.Y. Green credit policy, government behavior and green innovation quality of enterprises. J. Clean. Prod. 2021, 331, 129834. [Google Scholar] [CrossRef]

- Trujillo-Gallego, M.; Sarache, W.; Jabbour, A.B.L.D. Digital technologies and green human resource management: Capabilities for GSCM adoption and enhanced performance. Int. J. Prod. Econ. 2022, 249, 108531. [Google Scholar] [CrossRef]

- Zhou, D.Q.; Yu, Y.; Wang, Q.W.; Zha, D.L. Effects of a generalized dual-credit system on green technology investments and pricing decisions in a supply chain. J. Environ. Manag. 2019, 247, 269–280. [Google Scholar] [CrossRef] [PubMed]

- Tian, X.L.; Kou, G.; Zhang, W.K. Geographic distance, venture capital and technological performance: Evidence from Chinese enterprises. Technol. Forecast. Soc. Change 2020, 158, 120155. [Google Scholar] [CrossRef]

- Zhen, L.; Huang, L.F.; Wang, W.C. Green and Sustainable Closed-Loop Supply Chain Network Design under Uncertainty. J. Clean. Prod. 2019, 227, 1195–1209. [Google Scholar] [CrossRef]

- Wang, H.M.; Wang, S.Y.; Zheng, Y. China green credit policy and corporate green technology innovation: From the perspective of performance gap. Environ. Sci. Pollut. Res. 2023, 30, 24179–24191. [Google Scholar] [CrossRef]

- Amores-Salvadó, J.; Martin-De Castro, G.; Navas-López, J.E. The importance of the complementarity between environmental management systems and environmental innovation capabilities: A firm level approach to environmental and business performance benefits. Technol. Forecast. Soc. Change 2015, 96, 288–297. [Google Scholar] [CrossRef]

- He, L.Y.; Liu, R.Y.; Zhong, Z.Q.; Wang, D.Q.; Xia, Y.F. Can green financial development promote renewable energy investment efficiency? A consideration of bank credit. Renew. Energy 2019, 143, 974–984. [Google Scholar] [CrossRef]

- Ma, H.D.; Li, L.X. Could environmental regulation promote the technological innovation of China’s emerging marine enterprises? Based on the moderating effect of government grants. Environ. Res. 2021, 202, 111682. [Google Scholar] [CrossRef]

- Hall, B.H.; Moncada-Paternò-Castello, P.; Montresor, S.; Vezzani, A. Financing constraints, R&D investments and innovative performances: New empirical evidence at the firm level for Europe. Econ. Innov. New Technol. 2015, 25, 183–196. [Google Scholar]

- Song, M.L.; Wang, S.H.; Zhang, H.Y. Could Environmental Regulation and R&D Tax Incentives Affect Green Product Innovation? J. Clean. Prod. 2020, 258, 120849. [Google Scholar]

- Qiu, L.; Hu, D.; Wang, Y. How do firms achieve sustainability through green innovation under external pressures of environmental regulation and market turbulence? Bus. Strategy Environ. 2020, 29, 2695–2714. [Google Scholar] [CrossRef]

- Fang, Z.M.; Kong, X.R.; Sensoy, A.; Cui, X.; Cheng, F.Y. Government’s awareness of Environmental protection and corporate green innovation: A natural experiment from the new environmental protection law in China. Econ. Anal. Policy 2021, 70, 294–312. [Google Scholar] [CrossRef]

- Luo, Y.S.; Salman, M.; Lu, Z.N. Heterogeneous impacts of environmental regulations and foreign direct investment on green innovation across different regions in China. Sci. Total Environ. 2021, 759, 143744. [Google Scholar] [CrossRef] [PubMed]

- Yin, X.M.; Chen, D.D.; Ji, J.Y. How does environmental regulation influence green technological innovation? Moderating effect of green finance. J. Environ. Manag. 2023, 342, 118112. [Google Scholar] [CrossRef] [PubMed]

- Hamid, S.; Wang, Q.; Wang, K. Intertemporal evolution and influencing determinants of environmental productivity in South Asia’s electric power sectors: Technological heterogeneity perspective. Int. J. Environ. Sci. Technol. 2023, 23, 13762. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Type | Variable Name | Notation | Variable Definition |

|---|---|---|---|

| Explained Variable | Enterprise green technology innovation | Green T | ln(number of green patents acquired by firms in that prefectural city in the year +1) |

| Explanatory Variable | Green credit | Green P | Value added of the six major energy-intensive industries multiplied by (1—percentage of interest expenses of the six major energy-intensive enterprises in each province) |

| Control Variable | Enterprise size | size | Total assets |

| Leverage ratio | lev | Enterprise size/total liabilities | |

| Current ratio | flowr | Current assets/current liabilities | |

| Capital structure ratio | caps | Total liabilities/total owners’ equity | |

| Years of business establishment | age | ln(age of enterprise + 1) | |

| Cash flow ratio | cfo | Net cash flows from operating activities/current liabilities | |

| Instrumental Variable | Average value of green credits | avg | Average value of green credits for the year in all other regions |

| Intermediary Variable | Enterprise R&D investment | R&D | Total scientific research investments of all enterprises in each prefecture-level city |

| City | Level of Green Credit | City | Level of Green Credit | City | Level of Green Credit |

|---|---|---|---|---|---|

| Shanghai | 0.6724 | Tianjin | 0.5438 | Shijiazhuang | 0.3711 |

| Urumqi | 0.1826 | Taiyuan | 0.5897 | Fuzhou | 0.4592 |

| Lanzhou | 0.1869 | Guangzhou | 0.6242 | Xi’an | 0.4212 |

| Beijing | 0.6633 | Chengdu | 0.3761 | Guiyang | 0.2119 |

| Nanjing | 0.6069 | Kunming | 0.1222 | Zhengzhou | 0.4627 |

| Nanchang | 0.4475 | Hangzhou | 0.6518 | Chongqing | 0.5530 |

| Hefei | 0.6024 | Wuhan city | 0.4961 | Yinchuan | 0.2351 |

| Hohhot | 0.2907 | Shenyang | 0.4079 | Changchun | 0.4480 |

| Harbin | 0.5182 | Jinan | 0.5202 | Changsha | 0.4902 |

| Overall average | 0.4247 | ||||

| City | Green Technology Innovation Level of Enterprises | City | Green Technology Innovation Level of Enterprises | City | Green Technology Innovation Level of Enterprises |

|---|---|---|---|---|---|

| Shanghai | 8.6182 | Tianjin | 8.1758 | Shijiazhuang | 6.6113 |

| Urumqi | 5.8203 | Taiyuan | 6.3391 | Fuzhou | 6.7877 |

| Lanzhou | 5.9012 | Guangzhou | 8.2417 | Xian | 7.6909 |

| Beijing, | 9.2639 | Chengdu | 8.0239 | Guiyang | 6.2989 |

| Nanjing | 8.2085 | Kunming | 6.8204 | Zhengzhou | 7.3708 |

| Nanchang | 6.4066 | Hangzhou | 8.1936 | Chongqing | 7.6844 |

| Hefei | 6.3391 | Wuhan | 7.8133 | Yinchuan | 5.3235 |

| Hohhot | 5.3197 | Shenyang | 6.7403 | Changchun | 6.3944 |

| Harbin | 6.7483 | Jinan | 7.5067 | Changsha | 7.3353 |

| Overall average | 7.1103 | ||||

| Test Methods | Inspection Volume | Statistics | p-Value |

|---|---|---|---|

| LM test | LM-spatial lag | 1069.928 | 0.000 |

| Robust LM-spatial lag | 630.578 | 0.000 | |

| LM-spatial error | 442.270 | 0.000 | |

| Robust LM-spatial error | 2.919 | 0.000 | |

| Likelihood-ratio test | Ind | 442.15 | 0.000 |

| Time | 4759.24 | 0.000 | |

| LR-spatial lag | 253.63 | 0.000 | |

| LR-spatial error | 573.27 | 0.000 | |

| Wald test | Wald-spatial lag | 248.75 | 0.000 |

| Wald-spatial error | 464.40 | 0.000 |

| Variant | Direct Effect | Indirect Effect | Aggregate Effect |

|---|---|---|---|

| Green p | 0.091 (0.137) | 0.612 ** (0.258) | 0.702 *** (0.256) |

| size | 0.037 *** (0.014) | −0.088 *** (0.031) | −0.050 (0.036) |

| lev | −0.133 * (0.073) | −0.506 *** (0.179) | −0.640 *** (0.203) |

| flowr | 0.009 (0.008) | −0.036 ** (0.018) | −0.027 (0.021) |

| caps | −0.002 (0.011) | −0.013 (0.037) | −0.015 (0.040) |

| age | −0.110 (0.042) | −0.095 (0.096) | −0.206 * (0.110) |

| cfo | 0.025 (0.051) | −0.000 (0.128) | 0.245 (0.147) |

| R2 | 0.5400 | ||

| n | 2439 | ||

| Dependent Variables | Eastern Region | Central Region | Western Region | Northeastern Region | ||||

|---|---|---|---|---|---|---|---|---|

| Coefficient | Robust Std. Err. | Coefficient | Robust Std. Err. | Coefficient | Robust Std. Err. | Coefficient | Robust Std. Err. | |

| Green p | −0.419 | 0.270 | 2.229 *** | 0.322 | 1.235 *** | 0.301 | −4.392 *** | 0.808 |

| size | 0.177 *** | 0.034 | 0.126 *** | 0.023 | 0.126 *** | 0.033 | −0.010 | 0.037 |

| lev | −0.720 *** | 0.280 | −0.464 ** | 0.206 | −0.590 ** | 0.260 | 0.729 ** | 0.336 |

| flower | 0.047 | 0.056 | 0.171 *** | 0.045 | 0.116 *** | 0.035 | 0.077 | 0.077 |

| caps | 0.024 | 0.050 | −0.091 ** | 0.039 | −0.209 *** | 0.055 | 0.186 ** | 0.091 |

| age | 0.644 *** | 0.048 | 0.503 *** | 0.050 | 0.604 *** | 0.057 | 0.811 *** | 0.066 |

| cfo | −0.451 * | 0.249 | −0.136 | 0.191 | 0.565 ** | 0.259 | 0.025 * | 0.276 |

| R2 | 0.7323 | 0.5256 | 0.6425 | 0.6116 | ||||

| n | 2439 | |||||||

| Dependent Variable | Inverse Distance Weight Matrix | Nearest Neighbor Special Weight Matrix | Adjacency Weight Matrix | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Direct Effect | Indirect Effect | Total Effect | Direct Effect | Indirect Effect | Total Effect | Direct Effect | Indirect Effect | Total Effect | |

| Green p | 0.061 (0.138) | 15.347 * (8.055) | 15.407 * (8.056) | 0.032 (0.137) | 0.540 ** (0.213) | 0.573 ** (0.222) | 0.141 (0.134) | 0.375 (0.238) | 0.516 ** (0.246) |

| size | 0.030 * (0.016) | −1.900 (1.505) | −1.871 (1.512) | 0.031 ** (0.144) | −0.092 *** (0.032) | −0.061 (0.038) | 0.039 *** (0.015) | −0.014 (0.032) | 0.026 (0.035) |

| lev | −0.235 *** (0.084) | −20.705 * (11.329) | −20.941 * (11.372) | −0.144 (0.072) | −0.400 ** (0.162) | −0.544 *** (0.187) | −0.15 ** (0.073) | 0.076 (0.151) | −0.074 (0.167) |

| flowr | 0.015 (0.009) | 0.729 (0.873) | 0.744 (0.877) | 0.011 (0.008) | −0.005 (0.019) | 0.006 (0.023) | 0.009 (0.008) | −0.008 (0.017) | 0.001 (0.022) |

| caps | −0.016 (0.013) | −2.137 (1.507) | −2.153 (1.513) | −0.006 (0.011) | −0.015 (0.028) | −0.021 (0.032) | −0.003 * (0.011) | 0.051 (0.032) | 0.048 (0.035) |

| age | −0.097 ** (0.044) | −2.596 (2.504) | −2.694 (2.513) | −0.096 ** (0.042) | −0.152 * (0.078) | −0.247 *** (0.094) | −0.111 *** (0.043) | −0.105 (0.089) | −0.216 ** 0.099 |

| cfo | 0.047 (0.055) | 5.301 (4.659) | 5.348 (4.683) | 0.017 (0.051) | −0.048 (0.114) | −0.031 (0.137) | 0.027 (0.051) | −0.034 (0.122) | −0.007 (0.138) |

| R2 | 0.1822 | 0.3586 | 0.3904 | ||||||

| n | 2439 | ||||||||

| Variables | DIF-GMM | Phase I | Phase II | |||

|---|---|---|---|---|---|---|

| Coefficient | Corrected Std. Err. | Coefficient | Robust Std. Err. | Coefficient | Robust Std. Err. | |

| Instrumental variables (avg) | −216.368 *** | 6.992 | ||||

| Green T (L1) | 0.850 *** | 0.036 | ||||

| Green P | −0.115 | 0.237 | 1.001 *** | 0.225 | ||

| size | 0.012 | 0.020 | −0.004 *** | 0.001 | 0.102 *** | 0.016 |

| lev | −0.245 | 0.188 | −0.021 ** | 0.009 | −0.275 ** | 0.133 |

| flowr | 0.057 *** | 0.014 | −0.000 | 0.001 | 0.047 ** | 0.021 |

| caps | −0.070 *** | 0.018 | 0.002 | 0.001 | −0.078 *** | 0.029 |

| age | 0.103 ** | 0.042 | 0.007 *** | 0.003 | 0.569 *** | 0.029 |

| cfo | 0.338 *** | 0.129 | 0.005 | 0.008 | 0.092 | 0.138 |

| F-statistic | 959.612 | 959.612 | ||||

| AR(1) | 0.000 | |||||

| AR(2) | 0.064 | |||||

| Sargan | 0.418 | |||||

| Variables | Direct Effect | Indirect Effect | Aggregate Effect |

|---|---|---|---|

| Green p | 0.124 (0.137) | 0.703 *** (0.261) | 0.827 *** (0.268) |

| size | 0.046 *** (0.015) | −0.118 *** (0.033) | −0.072 * (0.038) |

| lev | −0.144 * (0.074) | −0.518 *** (0.183) | −0.662 *** (0.219) |

| flowr | 0.009 (0.008) | −0.035 * (0.020) | −0.026 (0.023) |

| caps | 0.000 (0.011) | −0.011 (0.035) | −0.011 (0.039) |

| age | −0.126 *** (0.043) | −0.227 ** (0.103) | −0.352 *** (0.113) |

| cfo | 0.009 (0.051) | −0.024 (0.122) | −0.015 (0.142) |

| R&D | −0.012 (0.011) | 0.121 *** (0.029) | 0.109 *** (0.031) |

| R2 | 0.5067 | ||

| n | 2439 | ||

| Dependent Variables | Independent Variables | ||

|---|---|---|---|

| Model 1 | Model 2 | Model 3 | |

| Green T | Green T | R&D | |

| R&D | 0.088 *** (0.015) | ||

| Green P | 1.518 *** (0.139) | 1.449 *** (0.139) | 0.788 *** (0.185) |

| size | 0.148 *** (0.015) | 0.082 *** (0.019) | 0.755 *** (0.020) |

| lev | −0.637 *** (0.130) | −0.486 *** (0.132) | −1.707 *** (0.172) |

| flowr | 0.084 *** (0.019) | 0.076 *** (0.019) | 0.085 *** (0.026) |

| caps | −0.114 *** (0.025) | −0.099 *** (0.025) | −0.165 *** (0.033) |

| age | 0.619 *** (0.025) | 0.584 *** (0.026) | 0.400 *** (0.033) |

| cfo | 0.188 * (0.113) | 0.161 (0.112) | 0.309 ** (0.150) |

| R2 | 0.6926 | 0.6968 | 0.8093 |

| n | 2439 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mi, K.; Cui, Z.; Zhu, X.; Zhuang, R. Can Green Credit Improve the Innovation of Enterprise Green Technology: Evidence from 271 Cities in China. Systems 2024, 12, 63. https://doi.org/10.3390/systems12020063

Mi K, Cui Z, Zhu X, Zhuang R. Can Green Credit Improve the Innovation of Enterprise Green Technology: Evidence from 271 Cities in China. Systems. 2024; 12(2):63. https://doi.org/10.3390/systems12020063

Chicago/Turabian StyleMi, Kena, Zetao Cui, Xinyi Zhu, and Rulong Zhuang. 2024. "Can Green Credit Improve the Innovation of Enterprise Green Technology: Evidence from 271 Cities in China" Systems 12, no. 2: 63. https://doi.org/10.3390/systems12020063

APA StyleMi, K., Cui, Z., Zhu, X., & Zhuang, R. (2024). Can Green Credit Improve the Innovation of Enterprise Green Technology: Evidence from 271 Cities in China. Systems, 12(2), 63. https://doi.org/10.3390/systems12020063