Digital Transformation, Firm Boundaries, and Market Power: Evidence from China’s Listed Companies

Abstract

1. Introduction

2. Theoretical Analysis and Hypothesis

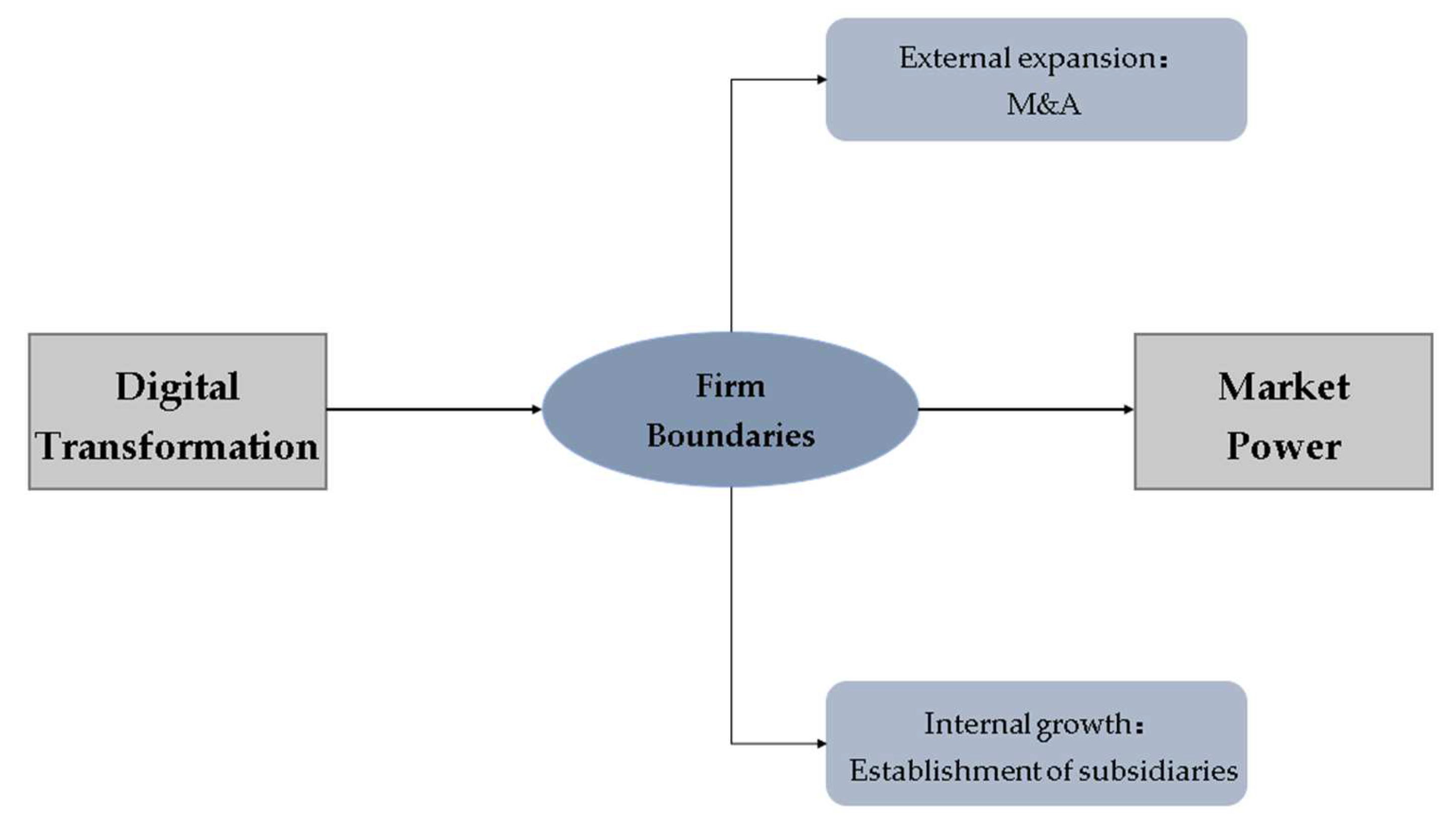

2.1. Digital Transformation Enables External Expansion and Increases Market Power by Promoting Corporate M&A

2.2. Digital Transformation Enables Internal Growth and Increases Market Power by Facilitating the Establishment of Subsidiaries

3. Research Methodology

3.1. Variables

3.1.1. Explanatory Variable

3.1.2. Explained Variable

3.1.3. Control Variables

3.2. Model

3.3. Data Sources

4. Results

4.1. Descriptive Statistics

4.2. Regression Results and Analysis

4.3. Intrinsic Mechanisms of Digital Transformation Affecting Market Power: Firm Boundaries

4.3.1. Digital Transformation Promotes M&A for External Expansion

4.3.2. Digital Transformation Promotes the Establishment of Subsidiaries for Internal Growth

5. Discussion and Conclusions

5.1. Discussion

5.2. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Sembenelli, A.; Siotis, G. Foreign Direct Investment and Mark-up Dynamics: Evidence from Spanish Firms. J. Int. Econ. 2008, 76, 107–115. [Google Scholar] [CrossRef]

- Toolsema-Veldman, L. Monetary Policy and Market Power in Banking. Economics 2004, 83, 71–83. [Google Scholar] [CrossRef][Green Version]

- Cole, M.T.; Eckel, C. Tariffs and Markups in Retailing. J. Int. Econ. 2018, 113, 139–153. [Google Scholar] [CrossRef]

- Mukherjee, S.; Chanda, R. Tariff Liberalization and Firm-Level Markups in Indian Manufacturing. Econ. Model. 2021, 103, 105594. [Google Scholar] [CrossRef]

- Stiebale, J.; Vencappa, D. Acquisitions, Markups, Efficiency, and Product Quality: Evidence from India. J. Int. Econ. 2018, 112, 70–87. [Google Scholar] [CrossRef]

- Li, C.; Xu, Y.; Zheng, H.; Wang, Z.; Han, H.; Zeng, L. Artificial Intelligence, Resource Reallocation, and Corporate Innovation Efficiency: Evidence from China’s Listed Companies. Resour. Policy 2023, 81, 103324. [Google Scholar] [CrossRef]

- Vial, G. Understanding Digital Transformation: A Review and a Research Agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Jiang, K.; Du, X.; Chen, Z. Firms’ Digitalization and Stock Price Crash Risk. Int. Rev. Financ. Anal. 2022, 82, 102196. [Google Scholar] [CrossRef]

- Nagle, F.; Seamans, R.; Tadelis, S. Transaction Cost Economics in the Digital Economy: A Research Agenda. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Hao, X.; Wen, S.; Xue, Y.; Wu, H.; Hao, Y. How to Improve Environment, Resources and Economic Efficiency in the Digital Era? Resour. Policy 2023, 80, 103198. [Google Scholar] [CrossRef]

- Rammer, C.; Fernández, G.P.; Czarnitzki, D. Artificial Intelligence and Industrial Innovation: Evidence from German Firm-Level Data. Res. Policy 2022, 51, 104555. [Google Scholar] [CrossRef]

- Liu, Y.; Dong, J.; Mei, L.; Shen, R. Digital Innovation and Performance of Manufacturing Firms: An Affordance Perspective. Technovation 2022, 119, 102458. [Google Scholar] [CrossRef]

- Harford, J. What Drives Merger Waves? J. Financ. Econ. 2005, 77, 529–560. [Google Scholar] [CrossRef]

- Maksimovic, V.; Phillips, G.; Yang, L. Private and Public Merger Waves. J. Financ. 2013, 68, 2177–2217. [Google Scholar] [CrossRef]

- Ardolino, M.; Rapaccini, M.; Saccani, N.; Gaiardelli, P.; Crespi, G.; Ruggeri, C. The Role of Digital Technologies for the Service Transformation of Industrial Companies. Int. J. Prod. Res. 2017, 56, 2116–2132. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R.W. Stock Market Driven Acquisitions. SSRN Electron. J. Financ. Econ. 2001, 70, 295–311. [Google Scholar] [CrossRef]

- Vahlne, J.-E.; Schweizer, R.; Johanson, J. Overcoming the Liability of Outsidership—The Challenge of HQ of the Global Firm. J. Int. Manag. 2012, 18, 224–232. [Google Scholar] [CrossRef]

- Bloom, N.; Garicano, L.; Sadun, R.; Van Reenen, J. The Distinct Effects of Information Technology and Communication Technology on Firm Organization. Manag. Sci. 2014, 60, 2859–2885. [Google Scholar] [CrossRef]

- Makridakis, S. The Forthcoming Artificial Intelligence (AI) Revolution: Its Impact on Society and Firms. Futures 2017, 90, 46–60. [Google Scholar] [CrossRef]

- Matarazzo, M.; Penco, L.; Profumo, G.; Quaglia, R. Digital Transformation and Customer Value Creation in Made in Italy SMEs: A Dynamic Capabilities Perspective. J. Bus. Res. 2021, 123, 642–656. [Google Scholar] [CrossRef]

- Foster, L.; Haltiwanger, J.C.; Syverson, C. The Slow Growth of New Plants: Learning about Demand? SSRN Electron. J. 2012, 83, 91–129. [Google Scholar] [CrossRef][Green Version]

- Hottman, C.J.; Redding, S.J.; Weinstein, D.E. Quantifying the Sources of Firm Heterogeneity. Q. J. Econ. 2016, 131, 1291–1364. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Gao, G.Y.; Zhao, H. State Ownership and Firm Innovation in China: An Integrated View of Institutional and Efficiency Logics. Adm. Sci. Q. 2016, 62, 375–404. [Google Scholar] [CrossRef]

- Ran, Q.; Yang, X.; Yan, H.; Xu, Y.; Cao, J. Natural Resource Consumption and Industrial Green Transformation: Does the Digital Economy Matter? Resour. Policy 2023, 81, 103396. [Google Scholar] [CrossRef]

- Wu, D.; Xie, Y.; Lyu, S. Disentangling the Complex Impacts of Urban Digital Transformation and Environmental Pollution: Evidence from Smart City Pilots in China. Sustain. Cities Soc. 2022, 88, 104266. [Google Scholar] [CrossRef]

- Cheng, Y.; Zhou, X.; Li, Y. The Effect of Digital Transformation on Real Economy Enterprises’ Total Factor Productivity. Int. Rev. Econ. Financ. 2023, 85, 488–501. [Google Scholar] [CrossRef]

- Chen, P.; Kim, S. The Impact of Digital Transformation on Innovation Performance—the Mediating Role of Innovation Factors. Heliyon 2023, 9, e13916. [Google Scholar] [CrossRef]

- Li, C.; He, S.; Tian, Y.; Sun, S.; Ning, L. Does the Bank’s FinTech Innovation Reduce Its Risk-Taking? Evidence from China’s Banking Industry. J. Innov. Knowl. 2022, 7, 100219. [Google Scholar] [CrossRef]

- Nunn, N.; Qian, N. US Food Aid and Civil Conflict. Am. Econ. Rev. 2014, 104, 1630–1666. [Google Scholar] [CrossRef]

- Nocke, V.; Yeaple, S. An Assignment Theory of Foreign Direct Investment. Rev. Econ. Stud. 2008, 75, 529–557. [Google Scholar] [CrossRef]

- Blonigen, B.A.; Pierce, J.R. Evidence for the Effects of Mergers on Market Power and Efficiency. SSRN Electron. J. 2016. [Google Scholar] [CrossRef]

- Neary, J.P. Cross-Border Mergers as Instruments of Comparative Advantage. Rev. Econ. Stud. 2007, 74, 1229–1257. [Google Scholar] [CrossRef]

- Berry, H. When Do Firms Divest Foreign Operations? Organ. Sci. 2013, 24, 246–261. [Google Scholar] [CrossRef]

- Lu, J.W.; Xu, D. Growth and Survival of International Joint Ventures: An External-Internal Legitimacy Perspective. J. Manag. 2006, 32, 426–448. [Google Scholar] [CrossRef]

{kind=link}

| Types | Abbreviation | Definition |

|---|---|---|

| Explanatory Variable | Digital | Standardized digital transformation thesaurus word frequency |

| Explained Variable | Power | Price mark-up |

| Control Variables | Size | ln(1 + total assets) |

| Roa | Net profit/total assets | |

| Top | Shareholding ratio of the largest shareholder | |

| Lev | Total liabilities/total assets | |

| Fix | Fixed assets/total assets |

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| Power | 24,361 | 1.270 | 0.207 | 0.211 | 2.981 |

| Digital | 24,361 | 3.224 | 1.246 | 0 | 7.368 |

| Size | 24,361 | 22.17 | 1.328 | 15.38 | 28.64 |

| Roa | 24,361 | 0.0370 | 0.124 | −3.164 | 10.40 |

| Top | 24,361 | 34.92 | 14.95 | 2.197 | 89.99 |

| Lev | 24,361 | 0.447 | 0.210 | 0.00700 | 1 |

| Fix | 24,361 | 0.227 | 0.157 | 0 | 0.929 |

| (3) | (4) | |

|---|---|---|

| IV1 | IV2 | |

| Digital | 0.006 ** | 0.074 ** |

| (0.003) | (0.030) | |

| Size | −0.019 *** | −0.032 *** |

| (0.002) | (0.006) | |

| Roa | −0.056 *** | −0.070 *** |

| (0.010) | (0.013) | |

| Top | 0.000 *** | 0.000 |

| (0.000) | (0.000) | |

| Lev | −0.079 *** | −0.081 *** |

| (0.007) | (0.013) | |

| Fix | 0.368 *** | 0.346 *** |

| (0.010) | (0.014) | |

| _cons | ||

| N | 21,147 | 19,931 |

| R2 | 0.305 | 0.133 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| MA | Power | Subsidiary | Power | |

| Digital | 0.047 *** | 0.050 *** | 0.041 *** | 0.028 *** |

| (0.016) | (0.001) | (0.006) | (0.001) | |

| MA | 0.004 *** | |||

| (0.001) | ||||

| Subsidiary | 0.019 *** | |||

| (0.001) | ||||

| Size | 0.298 *** | −0.025 *** | 0.374 *** | 0.017 *** |

| (0.027) | (0.001) | (0.010) | (0.002) | |

| Roa | 0.476 ** | −0.284 *** | −0.277 *** | −0.267 *** |

| (0.238) | (0.022) | (0.094) | (0.016) | |

| Top | −0.017 *** | −0.000 *** | 0.004 *** | −0.001 *** |

| (0.002) | (0.000) | (0.001) | (0.000) | |

| Lev | 0.150 | −0.267 *** | 0.268 *** | −0.145 *** |

| (0.110) | (0.007) | (0.043) | (0.007) | |

| Fix | 0.032 | 0.334 *** | 0.116 ** | 0.337 *** |

| (0.141) | (0.009) | (0.057) | (0.010) | |

| _cons | −5.226 *** | 1.726 *** | −6.582 *** | 0.792 *** |

| (0.576) | (0.022) | (0.224) | (0.036) | |

| N | 23,550 | 23,719 | 24,195 | 24,195 |

| R2 | 0.325 | 0.295 | 0.818 | 0.781 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, Y.; Li, C. Digital Transformation, Firm Boundaries, and Market Power: Evidence from China’s Listed Companies. Systems 2023, 11, 479. https://doi.org/10.3390/systems11090479

Xu Y, Li C. Digital Transformation, Firm Boundaries, and Market Power: Evidence from China’s Listed Companies. Systems. 2023; 11(9):479. https://doi.org/10.3390/systems11090479

Chicago/Turabian StyleXu, Yang, and Chengming Li. 2023. "Digital Transformation, Firm Boundaries, and Market Power: Evidence from China’s Listed Companies" Systems 11, no. 9: 479. https://doi.org/10.3390/systems11090479

APA StyleXu, Y., & Li, C. (2023). Digital Transformation, Firm Boundaries, and Market Power: Evidence from China’s Listed Companies. Systems, 11(9), 479. https://doi.org/10.3390/systems11090479