The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises

1

School of Business, Ningbo University, Ningbo 315211, China

2

School of Mathematics, Thapar Institute of Engineering & Technology (Deemed University), Patiala 147004, Punjab, India

3

Department of Mathematics, Graphic Era Deemed to be University, Dehradun 248002, Uttarakhand, India

4

Applied Science Research Center, Applied Science Private University, Amman 11931, Jordan

*

Author to whom correspondence should be addressed.

Systems 2023, 11(2), 67; https://doi.org/10.3390/systems11020067

Submission received: 13 December 2022

/

Revised: 19 January 2023

/

Accepted: 25 January 2023

/

Published: 28 January 2023

Abstract

:Private construction businesses have grown quickly, greatly boosting China’s economic growth; nonetheless, these businesses suffer tremendous developmental uncertainty, particularly when compared to larger state-owned businesses. The traits of the top management team (TMT) may have a direct impact on how risk-taking and decision-making behaviors are exhibited by businesses, according to earlier studies. The majority of private construction companies in China are family businesses with family members making up the majority of their top executives. As a result, these companies are vulnerable to family centralization, which will definitely boost their risk-taking level. This study used a sample of private listed companies in China’s construction industry from 2009 to 2019 to explore the impact of CEO traits on the risk-taking degree of enterprises. The findings show that a higher percentage of top female managers and a higher average rate of TMT member both lower the level of risk taking in private construction businesses. The level of risk taking, however, is positively impacted by the top management’s higher average education level. The average tenure and overseas experience of TMTs and the degree of risk taking in private construction enterprises are not significantly correlated. Additionally, the degree of risk taking in private construction firms can vary depending on the qualities of the senior management team.

1. Introduction

With a gross domestic product (GDP) of CNY 26,394.7 billion in 2020—a rise of 6.2% over the previous year—and accounting for 25.98% of China’s overall GDP in the wake of COVID-19 pandemic and the accompanying economic recession, construction has emerged as a significant sector in China. The private economy is a crucial component of the socialist market economy in China; it promotes vitality in business operations and has grown to be a driving force for the country’s economic development. Private construction companies now make up a substantial portion of the Chinese construction sector due to the market economy system’s ongoing improvements. However, while experiencing enormous development, these companies now struggle to maintain that growth.

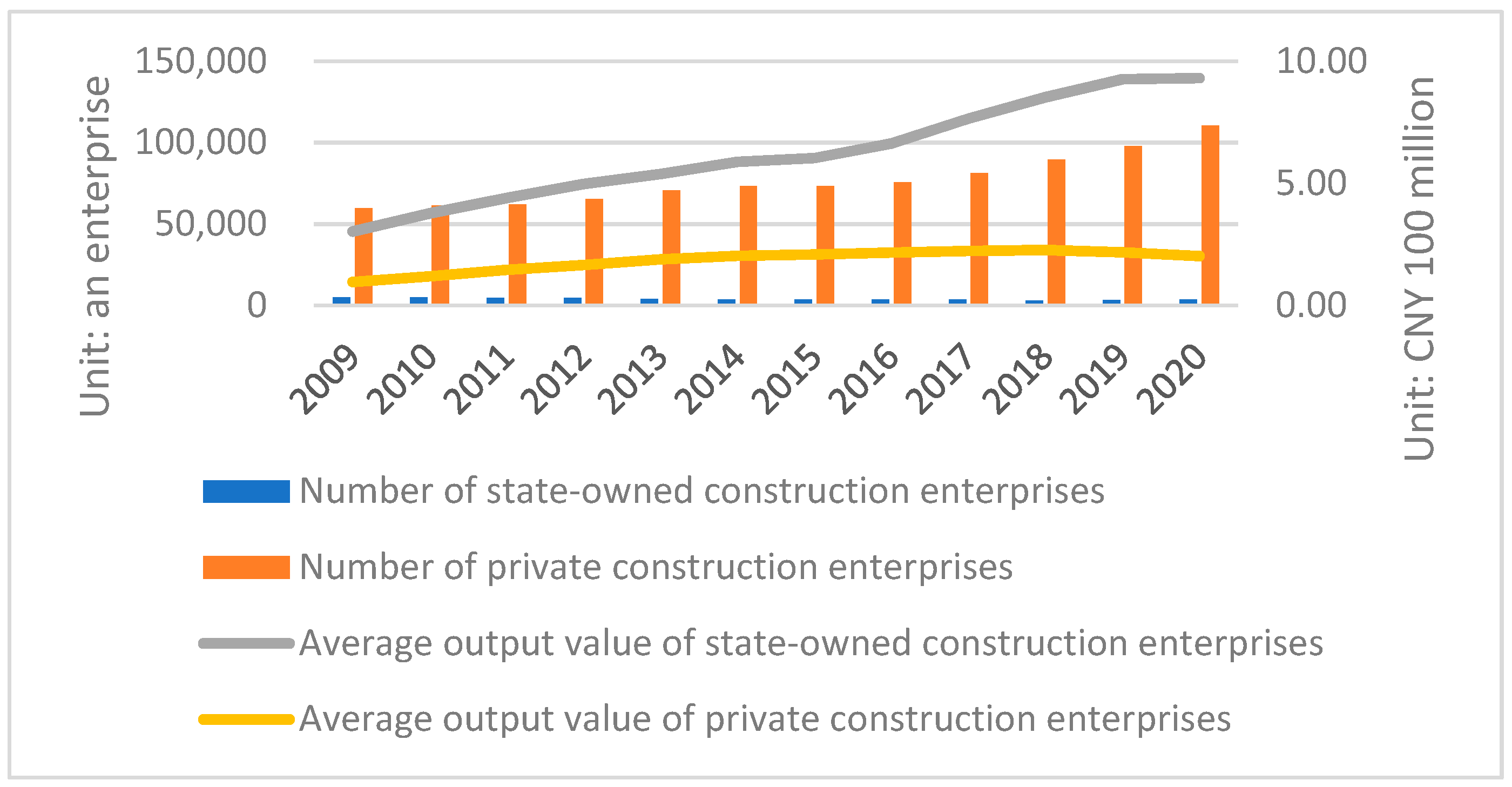

Compared with large construction enterprises that are state-owned, the scenario of private construction enterprises is very different. According to the National Bureau of Statistics, the number of private construction enterprises in China has far exceeded that of state-owned construction enterprises. In contrast to the 3700 state-owned construction enterprises, there were more than 110,000 private construction companies as of 2020 (see Figure 1 for details). Private construction enterprises are becoming more prevalent, although there are issues with them being “small and not strong.” According to Figure 1, there is still a huge gap between the average output value of enterprises. Wang et al.’s research [1] shows that private construction firms produce a lot less than state-owned firms; research also reveals that the Chinese state-owned construction companies are 2.74 times more competitive than private construction enterprises. State-owned construction companies, on the other hand, developed earlier and constantly enhanced their management levels, drew a large number of professionals through excellent pay and benefits, and continuously strengthened the development of construction technology. They can, therefore, adopt a development strategy that is rather stable. In contrast, Zhang [2] points out that Chinese private construction enterprises have a lesser level of technology and expertise, less capital, and a smaller scale. Due to their acute lack of market competitiveness, they must take bigger risks in order to achieve higher profits because they use a lot of untrained rural laborers in order to keep costs down. Additionally, these businesses have some inherent problems. For instance, the majority of private construction enterprises are family-owned and prone to centralization and management by families, which may be brought on by construction organizations and contracting teams.

The Communist Party of China’s Central Economic Work Conference urged that infrastructure spending be carried out considerably in advance in December 2021. The development of new infrastructure, such as communications and the internet, has recently emerged as one of China’s economic growth new highlights. While this undoubtedly creates new development opportunities for the construction industry, the majority of the private construction enterprises are not among them. According to the data, only a small number of private construction enterprises such as Longyuan Construction are eligible to participate in building the nation’s infrastructure, and even then, their infrastructure construction revenues make up just 0.2% of their overall revenue. More than 80% of the revenue generated by private construction companies still comes from the traditional housing construction industry. In the past 30 years, China’s real estate industry has been regarded as the craziest, with many businesses entering the sector as well as private construction enterprises. However, since 2020, as a result of the government’s adherence to the “no speculation in real estate” policy, the real estate market has entered a depression, with many real estate businesses experiencing liquidity crises and even going out of business. Therefore, private construction enterprises with real estate as the main business face great risks. Undoubtedly, it is crucial to modernize private construction companies so they are less dependent on real estate development and may join the national new infrastructure team. To do this, the senior management team must be wise and capable of making sound decisions.

The decision making of the top management team (TMT) is closely related to companies’ risk-taking level and future development; the TMT is the most executive decision maker and operator of the private construction enterprise and it is the most important factor that also reflects its human capacity, which has a decisive role in the risk-taking ability and the development prospect of the private construction enterprise. In addition, some scholars believe that differences in perception among executives are the main source of contradictions, as extreme heterogeneity leads to a reduction in common language among executives and a decline in teamwork ability. At the same time, a sense of identity within the team can improve the scientific validity of decision making.

Therefore, it is necessary to study the influence of executive team characteristics on the risk taking of Chinese private construction firms. In light of this, this study investigates how the TMT characteristics affect private construction enterprises. In order to investigate the effects of TMT characteristics on risk taking in Chinese private construction firms, the study compiles and sorts pertinent data on Chinese listed private construction enterprises from 2009–2019 and builds an empirical model. The reason we chose the period from 2000 to 2019 is that conventional private enterprises were very prominent during this time, and China’s private construction industry experienced fast growth during this time. The results shows that a higher TMT average age and a higher proportion of top female managers lower the level of the risk taking of private construction enterprises. In contrast, the greater average education level in TMT positively impacts the degree of risk taking. The average tenure and overseas experience of TMTs and the degree of risk taking in private construction enterprises are not significantly correlated.

The importance of the construction industry is unique, regardless of the level of development of the country. Human factors are important factors that influence the management of risk perception and analysis in the construction industry [3,4]. Work experience, physical health, educational background, professional competence, and emotional intelligence all have an impact on construction enterprise risk management [5]. However, most of the existing studies on the risk taking or risk appetite of real estate firms focus on the influence of policy factors [6,7,8].

The contributions of this study are as follows: (1) Most of the existing research on the TMTs focuses on the average level characteristics of the TMTs of listed companies, and the research on one industry is relatively rare, while the research on the private construction industry in China is even rarer; This paper aims to analyze the impact of the characteristics of the TMT of private construction enterprises and the level of heterogeneity within the team on their risk taking, which will help expand the research perspective of the TMT characteristics. (2) Considering the close relationship between private construction enterprises and the real estate industry, this paper adds China’s house price index as a control variable in the empirical model to more accurately analyze the influencing factors of private construction enterprises’ risk taking; It enriches the research perspective on the risk taking of Chinese construction enterprises. (3) In terms of the heterogeneity level of the TMT, we will further explore and analyze the impact of the difference between the characteristics of TMT and the characteristics of the lower management on the level of risk taking of the private construction enterprises from the vertical perspective, thus enriching the research on the characteristics of improving the cooperation ability of the TMT. (4) The background characteristic data of the TMT in the empirical model are collected and collated manually from the annual reports of China’s private listed construction companies, which are relatively complete and reliable [9].

The rest of this study is structured as follows: The second section includes the literature review, the research hypothesis, and the theoretical basis for this study, sorting out the relevant literature about the impact of five executive characteristics (age, gender, education, tenure, and overseas background) on enterprises’ level of risk taking. Then, combined with the features of the private construction enterprises examined in this study, we put forward some hypotheses to be analyzed. The third part presents the research design, including the data sources, variable definitions, and model construction. The fourth part details the empirical analysis and the corresponding robustness test of the relationship between TMT characteristics and the level of risk taking. The fifth section further studies the impact of the heterogeneity in the TMT on the risk-taking level of private construction enterprises. Finally, we present the summary of the analysis results, the research conclusions, and corresponding suggestions for risk control in Chinese private construction enterprises from the perspective of adjusting the TMT.

2. Definition of Core Concepts, Literature Review, and Research Hypothesis

2.1. Definition of Core Concepts

2.1.1. TMT and TMT Characteristics

In addition to managing and supervising the work of lower-level employees, top managers determine the development direction of the entire enterprise. In a narrow sense, the TMT only refers to the core senior managers of the enterprise, including the chairman of the board, chief executive officer (CEO), general manager, and chief financial officer (CFO) [10,11,12]. At the same time, in a broad sense, TMT refers to all personnel who hold positions in the company’s management, are responsible for the company’s operation and management, and have access to important company information [10,11,12]. This includes the chairman, board secretary, director, general manager, deputy manager, CFO, related financial officers, chairman of the board of supervisors (who are to supervise the behavior of directors and managers), and all supervisors.

Sperber and Linder [13] point out that demographic characteristics are important explanatory variables of a company’s innovation performance. Compared with measuring certain subjective variables (ability, influence, etc.) or psychological characteristics, measuring demographic characteristics is more straightforward and intuitive. For example, the educational background may simultaneously affect personal values, risk appetite, and other psychological characteristics. Reviewing the literature, we determined that the most commonly used demographic variables to examine TMT are age, gender, education, educational major, tenure, career experiences, overseas experience, political–economic background, and financial position.

2.1.2. Risk-Taking Level

Risk-taking level is the level of risk that an enterprise can accept to obtain a higher rate of return. A higher risk-taking ability is beneficial to the company for obtaining greater profits, accumulating wealth, and promoting innovation and development, but it also brings greater uncertainty. Therefore, a moderate risk-taking level is of great significance to a company. Risk taking indicates an enterprise’s tolerance and control over risks, and is ultimately reflected in the enterprise’s willingness to invest [14]. Higher risk preferences of enterprises can also accelerate technological progress and economic growth in society [15].

There are different ways to measure risk taking based on its different conceptualizations. Angie [16] uses the logarithmic value of the daily stock price return change in the financial year as an evaluation index. Based on the relationship between stock return volatility, R&D investment, and financial leverage, Jeffrey et al. [17] use R&D and the financial leverage ratio as indicators to measure corporate risk taking. Owing to the high volatility of China’s stock market, Yu and Li [9] use earnings volatility to measure a firm’s risk-taking level. Risk taking is a key indicator examined in the present study. The author concludes that the existing methods for measuring the level of enterprise risk taking can be mainly divided into five types: (i) earnings volatility; (ii) standard deviation of stock returns; (iii) capital R&D expenditure; (iv) profit standard deviation; and (v) debt ratio.

2.2. Literature Review

Since the private construction enterprises in this study are mostly family enterprises, the characteristics of their executive teams are somewhat different from those of other industries. Specifically, this can be explained as follows: (1) since some of the executives are family members rather than individuals from outside the family fold, the age of their TMTs is older than those of other industries, their education level is lower, and their tenure is longer and more stable; (2) since the predecessors of private construction enterprises are mostly private “construction teams,” the construction technology level talent is relatively abundant and dominated by men, the proportion of women in their executive team is low, and the number of executives with an overseas background is low as well. Therefore, this study mainly selects five variables: age, gender, education, tenure, and overseas background, as the core explanatory variables to measure the characteristics of the TMT of private construction enterprises [18,19,20].

2.2.1. Risk Taking by Family Firms

A family firm is a type of firm that is controlled by the family. Family firms have much less financial risk than non-family firms, and the more family members in the TMT, the lower the financial risk when other risks are under control [21]. Research on CEOs of family firms shows that if the CEO of a family firm is not a family member, it increases the level of risk taking in the family firm during the initial years of their tenure, but the risk taking decreases as their tenure continues [22]. Moreover, if the CEOs are family members who are about to retire, they will change their risk aversion mentality, which will increase the risk-taking level of family businesses [23]. Family firms with lower levels of TMT heterogeneity typically take more risks than firms with higher levels of TMT heterogeneity [24].

2.2.2. TMT Age and Risk-Taking Level

Age represents an entrepreneur’s experience and risk preference, affecting their strategic views and choices [25]. Generally speaking, young executives with high levels of energy, physical strength, and an active mind easily absorb new knowledge and ideas. Compared to older executives, younger TMT members are more ideologically advanced; they accept new developments more quickly. The younger the executive, the more innovative they are [26]. In contrast, the higher the TMT members’ average age, the more experience they bring to operations and management [27]. Tanikawa and Jung [10] draw a similar conclusion regarding age, which correlates with the TMT’s decision making and reaction speed. In addition, compared to state-owned construction enterprises, private construction enterprises tend to take higher risks to expand their financing scale, overcome their size scale and capital constraints, and promote further development. The following hypothesis is put out considering the analyses above mentioned:

H1:

The age of TMT members is negatively correlated with the risk taking of private construction companies.

2.2.3. TMT Gender and Risk-Taking Level

With social progress and economic development, more women have joined the TMTs of enterprises based on their merits and efforts [28]. Some scholars have found that 57.2% of Shanghai and Shenzhen A-share listed companies have female members in their TMT, and the average proportion of female members in these companies is about 13.2%. Female executives tend to be more conservative and cautious in their decision making compared to male executives [29]. First, differences in physiological indicators lead to different attitudes toward risk between women and men. Women are more risk-averse, as they have higher levels of monoamine oxidase (MAO)—physiologically and psychologically, MAO may affect people’s risk attitudes—and tend to play a nurturing role within the firm. Moreover, pregnancy and breastfeeding experience makes women more risk-averse [30]. Some studies have found that women have a higher level of morals than men in finance-related matters [31]. Therefore, the risk-aversion tendency of female executives reduces the investment risk of enterprises to a large extent. Due to their characteristics, the TMT of private construction enterprises is often dominated by men, and the proportion of women is relatively low.

Based on the above analysis, the following hypothesis is proposed:

H2:

The proportion of women among TMT members is negatively correlated with the risk taking of private construction companies.

2.2.4. TMT Education and Risk-Taking Level

Details of a person’s educational experience can yield sufficient and complex information, which, to a certain extent, can reflect their knowledge and skill set [32]. Executives with high educational levels have a strong ability to deal with uncertain scenarios and are more capable of handling such situations to gain benefits than their lower-educated peers [32]. Through an empirical analysis of Chinese listed companies in Shanghai and Shenzhen A-share markets from 2001 to 2010, Yu and Li [9] draw the following conclusions: a TMT with a higher educational level is more capable of accepting uncertainty, can make more comprehensive decisions considering the environment of the enterprise, and has stronger environmental adaptability. King et al. [33] find that CEOs who graduated from the top 20 universities in the United States are able to achieve superior corporate management. Therefore, highly educated executives are more willing to accept strategic change and innovation [19], possess a stronger ability to deal with complex issues, and prefer to execute high-risk investment decisions. Accordingly, the following hypothesis is proposed:

H3:

The educational level of TMT members is positively correlated with the risk-taking behavior of private construction companies.

2.2.5. TMT Tenure and Risk-Taking Level

Generally, the tenure of executives affects their cognitive level, management experience, and concentration of management power, which in turn affects management decision making and performance. Longer-term executives are often reluctant to take risks to initiate strategic change [34] and will make every effort to avoid implementing risky decisions toward the end of their tenure [35]. Heyden et al. [36] highlight that longer-tenured TMTs are under less pressure to prove their competence to stakeholders; further, they tend to mitigate risk and use inherent paradigms or strategies that have proven effective in running the business. Accordingly, we propose the following hypothesis:

H4:

The tenure of TMT members is negatively correlated with the risk taking of private construction companies.

2.2.6. TMT Overseas Background and Risk-Taking Level

An overseas background refers to the experience of TMT members in studying or working abroad. Extensive international experience can enhance the executive risk management and information-gathering skills of the TMT [37]. Executives with overseas backgrounds tend to have highly specialized skills, advanced management experience, and diverse perspectives, which make them more adept at dealing with various risks and contingencies [11,38]. However, the rapid economic development and continuous improvement of market liberalization in emerging economies can lead to issues such as the underdevelopment of the institutional infrastructure [39]. Therefore, the role of overseas talent in emerging economies is limited to a certain extent. Lin et al. [40] research small- and medium-sized enterprises in Zhongguancun (a famous district in China) and conclude that the innovation performance of companies with returnee CEOs is lower than that of companies with local CEOs.

From a review of the relevant literature, it can be concluded that scholars have gradually incorporated the TMT structure, executive compensation, executive government background, innovation investment, and agency costs into their research. They have explored how TMT characteristics influence companies’ risk taking through different impact mechanisms under different research backgrounds. On the one hand, there is disagreement among academics as to whether there is a favorable or unfavorable correlation between these traits and taking risks. In contrast, some of the variables chosen based on demographic traits have substantial connections, while others have weak correlations, possibly as a result of variations in research backgrounds and sectors. However, these conclusions still have a positive reference value.

As mentioned, most scholars’ research describes the relationship between the characteristics of executives and the level of risk taking of enterprises in a general way and does not focus on specific industries. In the current scenario of uncertainty in China’s real estate industry and from the perspective of risk control, this study focuses on the challenges faced by Chinese private construction companies. Further, it analyzes the relationship between their risk taking and executive characteristics. The study aims to help companies nurture a suitable TMT environment and put forward relevant suggestions to strengthen the TMT composition to help private construction enterprises enhance their risk awareness, optimize their risk-taking level, and develop more healthily. The following hypothesis is put out considering the analyses above mentioned:

H5:

TMT members’ overseas backgrounds negatively correlate with the risk taking of private construction companies.

3. Research Design

3.1. Study Subjects and Data Sources

This study selected Chinese A share listed private construction enterprises from 2009 to 2019 as the research object. The following exclusion criteria were applied: (1) companies with incomplete information disclosures on their executives, and (2) companies with incomplete disclosures of relevant financial information. Finally, data from 81 companies were collected, with 648 observations that met the requirements. The age, gender, education, tenure, and overseas background data of the executives in this study were obtained from www.cninfo.com.cn as well as manually from the companies’ annual reports. The rest of the financial data came from the CSMAR database of Cathay Pacific. All the collected data have been standardized.

3.2. Variable Setting

The empirical analysis draws on previous studies on TMT characteristics and enterprise risk taking to determine the explained, explanatory, and control variables.

3.2.1. Explained Variable

The explained variable in this study is the risk-taking level of private construction enterprises. Since it cannot be measured directly, drawing on the practice of John K.L. [15], Faccio et al. [41], He and Liu [12], we use earnings volatility (Ris) to measure the risk-taking level of enterprises. As a risk-consideration standard, a company’s earnings volatility reflects the riskiness of investment decisions, and it is used to measure the propensity for risk. The lower the earnings volatility, the lower the risk-taking level. The formula is as follows:

where ;

is the level of risk taking for the enterprise;

is the return on assets for the enterprise;

is the adjusted return on assets for the enterprise, which is obtained by subtracting the industry’s average return on assets for the year from the company’s return on assets for the year; and is the number of rolling years in which earnings volatility is calculated. In this study, the observation period is every two years, and the standard deviation of in every two years of the enterprise is calculated on a rolling basis (i.e., ).

3.2.2. Core Explanatory Variables

As mentioned previously, the core explanatory variables of this study are the age, gender, education, tenure, and overseas background of the TMT.

- Age (Age): Average age of the company’s TMT.

- Gender (Gen): Proportion of women to the total number of TMT members.

- Education (Edu): After collecting details of the educational qualifications of various executives, a score is manually assigned, with technical secondary school and below being 1, junior college 2, undergraduate 3, master’s degree 4, and doctor’s degree 5. Finally, the average is taken to represent the average educational level of each company’s TMT each year.

- Tenure (Ten): Average tenure of TMT members.

- Overseas background (Ovs): The proportion of those with overseas backgrounds to the total TMT members.

3.2.3. Control Variables

Referring to John K.L. [15], Faccio et al. [41] and the three most popular studies on the risk taking by Chinese scholars [40,42,43], this study selects the following five control variables.

- Main business profit margin (Mainpro). The main business profit margin is the percentage of the main business profit and the main business income. The higher the index, the higher the added value of the enterprise’s products, the stronger competitiveness of the main business market, the greater development potential and the higher profit level.

- Enterprise size (Siz). The natural logarithm of the company’s total assets at the end of the year measures its size.

- House price index (Hpr). This is the ratio of the national average house price in the current year to the national average house price in the previous year. As mentioned the private construction industry is closely related to the real estate industry, and fluctuations in one industry can directly impact the level of risk in another.

- Proportion of independent directors (Idr). Refers to the ratio of independent directors on the board. It is generally believed that independent directors can act as external supervisors of the company, playing a supervisory role in the company’s daily operations and limiting excessive risk behavior.

- Shareholding ratio of the largest shareholder (Tp1). Most Chinese private construction companies are family-owned enterprises and the largest shareholder is often the company’s founder. Further, the shareholding ratio is generally very high. However, if the shareholding ratio is too high, it may lead to the phenomenon where the decision making serves the interests of the family rather than the company [3].

The detailed variable definition is listed in Table 1.

3.3. Model Settings

Based on the hypotheses and variable design, in order to verify the relationship between the characteristics of the TMT and the risk bearing of private construction enterprises, and learn from the existing research experience [4,9], the classic linear regression model is constructed as follows:

In order to improve the significance and distinguish from existing literature [4,6,7,9], this paper makes the following steps in least squares regression: step 1. use a single explanatory variable (plus control variable) to regress one by one with the explained variable; step 2. conduct the overall regression including all variables; step 3. remove insignificant variables and control variables.

4. Empirical Test

4.1. Descriptive Statistics

First, we conduct descriptive statistics on all variables in Table 1 to observe the overall characteristics of variables. Table 2 shows that: (1) The average level of risk-taking of the sample enterprises is 0.0346, the maximum value is 0.4496, and the minimum value is close to 0. A large difference indicates a large gap in the risk-taking level of different private construction enterprises; (2) Regarding the background characteristics of the TMTs, first, the average age in years of the TMTs is 47.3, the maximum is 57.4, the minimum is 37.1, and the maximum gap is about 20 years. In general, Chinese private construction companies have middle-aged TMTs. Second, the average educational level of the TMT is 3.2895, indicating that most executives had received undergraduate education. Third, the average proportion of female executives is 0.1919, indicating that there are very few female executives (less than 20%). Male executives dominate the current executive teams of private construction companies in China. Fourth, the average proportion of members with an overseas backgrounds in the TMT is about 7%, indicating that executives with overseas backgrounds are rare in private construction enterprises.

4.2. Regression Analysis

Before regression analysis, the Pearson coefficient correlation analysis method is used to detect the correlations between the variables and the result shows that there is no severe multicollinearity between the variables. Then, substitute the above variable data into the model for regression analysis to verify research hypothesis 1 to 5. As the data of all listed private construction enterprises are collected in this study, it can be considered a full sample; therefore, we use a fixed-effects model. Additionally, to improve the significance, based on the overall regression, the single explanatory variable (plus all control variables) and the explained variable are regressed one by one. Table 3 presents the results.

Table 3 shows that, first, there is a significant negative relationship between the age of the TMT of private construction firms and corporate risk taking, which is consistent with hypothesis H1. Second, the percentage of female executives in the overall regression model is negatively correlated with corporate risk taking at the 5% significance level, which can be considered consistent with hypothesis H2. Third, the average education of the TMTs is positively related to corporate risk taking at level 5%, which is consistent with hypothesis H3. Finally, the correlations between TMT tenure and overseas background and corporate risk taking failed the significance test, indicating that the tenure and overseas background of the TMTs has no significant impact on the risk taking of private construction companies. Thus, H4 and H5 do not hold. In addition, Mainpro, Siz, and Tp1 in the control variables have a significant negative correlation with corporate risk taking.

4.3. Robustness Test

To further verify the reliability and robustness of the above regression analysis conclusions, in the following, we will use the commonly used methods of replacing and resetting variables for robustness test.

(1) Replacing the explained variable

The debt ratio of an enterprise is the percentage of total liabilities divided by total assets at the end of the period, and it is an important indicator for measuring the financial risk of the enterprise. Private construction enterprises typically have high leverage and liabilities. Therefore, this study uses the debt ratio (Debt) to replace the original explained variable—the calculation formula is —to conduct the robustness test and further explore its impact on the risk taking of private construction enterprises. Table 4 presents the regression results.

The results in Table 4 show that the age of the TMT and the proportion of women in the TMT are both significantly negatively correlated with the risk taking of private construction companies at the 1% level. At the 1% level, TMT education is significantly and positively related to risk taking. The impact of TMT tenure and overseas background on risk taking is not significant. This result is consistent with the previous conclusions.

(2) Resetting the education variable

There are many ways to measure educational levels in mainstream academic circles. Therefore, after setting the dummy variables, we replace the education variable with years of education. The results in Table 5 show a significant positive correlation between TMT educational level and corporate risk taking, consistent with previous conclusions.

4.4. Heterogeneity Analysis

In studies on the characteristics of the executive team, the mainstream view in academia can be divided into two parts: the average level, and the level of heterogeneity. The heterogeneity of the executive team refers to the differences between the TMT members’ demographic factors, such as age, gender, education, tenure, professional background, and cognitive outlook and values [44]. In terms of variable measurement, gender heterogeneity (Hgen) and education heterogeneity (Hedu) are discrete variables. Collins and Blau [45] used the Herfindahl–Hirschman coefficient to measure these two heterogeneities within the executive team for the first time, and it has been widely used since then; the formula is , ranging from 0 to 1; the higher the value, the more heterogeneous the team. Here, refers to the percentage of members belonging to the i category in the executive team, and n is the total number of different types. The age heterogeneity (Hage) and tenure heterogeneity (Hten) are continuous variables. Allison [46] explored the practice of centrally measuring heterogeneity and found that the standard deviation coefficient method is more accurate. The formula is . The higher the ratio, the more heterogeneous the team.

Considering that the proportion of executives with overseas backgrounds is relatively small, and to maintain consistency with the preceding analysis, this part uses four variables—age heterogeneity (Hage), gender heterogeneity (Hgen), educational heterogeneity (Hedu), and tenure heterogeneity (Hten)—to measure the impact of TMT heterogeneity on private construction enterprises’ risk-taking levels. The control variables were the same as in previous analyses, and Table 6 lists the results.

Table 6 shows that, first, age heterogeneity is positively significant at the 5% level in the separate regression and positively correlated with enterprise risk taking at the 1% level in the overall model. Second, gender heterogeneity is negatively associated with risk taking at the 5% significance level in the separate regression model and negatively significant at the 1% significance level in the overall regression model. Third, educational heterogeneity is negatively correlated with firm risk taking at the 1% significance level in both the individual and overall models. Finally, the heterogeneity of executive team tenure is positively significant at the 1% level in the separate regression and positively correlated with corporate risk taking at the 10% level in the overall model.

5. Conclusions

5.1. Research Conclusions

This study focuses on the impact of Chinese private construction enterprises’ TMT characteristics on their risk taking and builds a suitable TMT for China’s private construction enterprises. With a combination of qualitative and quantitative research methods, the conclusions drawn by the present study can be divided into two parts: the conclusions that are similar to the existing research and the conclusions that are completely different.

(1) Both the age of executives and the proportion of female executives have a negative impact on the risk taking of private construction companies, which id consistent with existing research conclusions on other industries [10,25,26,27,28,29,30,31]. The reasons are as follows: First, as mentioned previously, most private construction companies in China are family-owned enterprises whose TMT members are often appointed by family members; compared with state-owned construction companies, their average age (47 years old) is much higher, which leads to a more prominent negative relationship between age and corporate risk taking. Second, women are inherently more risk-averse than men and choose investments with lower risks, in addition, the relatively low proportion of women in the TMT in private construction companies in China, which leads to a greater marginal effect.

(2) The higher the educational level of the TMT, the higher the risk-taking level of private construction companies, which is inconsistent with existing research conclusions [9,19,32,33,34]. Compared with state-owned construction companies, the Chinese private construction companies’ “first-generation” executives’ educational qualifications were generally low, with less than 40% having a master’s degree or above. Thus, the positive impact of executive education on the risk-taking level of private construction enterprises is more significant, which was verified in robustness tests as well.

(3) The impact of the TMT’s tenure and the overseas background on the risk taking of private construction enterprises is not significant, which is quite different from existing research conclusions [11,35,36,37,38,39,40]. This may be because most private construction companies are family-owned enterprises, and some of their executive positions are held by important family members whose actual tenure is generally long. Indeed, the annual reports suggested that many executives were repeatedly appointed for three to four times and maintained their re-election for more than ten years. In addition, the proportion of executives in private construction companies with overseas experience is relatively low, being only 7%, resulting in an insignificant impact on risk taking.

(4) The impact of heterogeneity of the TMT: First, the age heterogeneity and tenure heterogeneity of the TMT have a significant positive impact on the risk taking of private construction enterprises, which means that a TMT with a greater age and tenure dispersion will improve the risk-taking level. Because there is a certain correlation between tenure and age, tenure can be understood to a certain extent as the “age” of in the enterprise, and senior executives at different ages have different ways of understanding and thinking logic. From the perspective of information decision-making theory [7], diversified information and ideas can help the team have broader perspectives and concepts. Due to the rigid demand of China’s construction market and the continuous expansion of the size of the TMT, private construction enterprises are at a critical stage that needs rapid development. The TMT with more heterogeneity in age and tenure can be more confident and motivated to take higher risks and gain greater profits after comprehensively considering multiple factors and summarizing multiple information.

Second, the gender and educational heterogeneity of the TMT has a significant negative impact on the risk taking of private construction enterprises, indicating that the gender and educational differences within the TMT will reduce the risk taking level. In combination with the characteristics of private construction enterprises with a relatively small proportion of women, the higher gender difference in the TMT means a relatively higher proportion of women. The empirical evidence shows that the average proportion of women in the TMT is significantly negatively correlated with the risk taking of private construction enterprises. The research on gender heterogeneity further proves the reliability of the results. Academic qualifications represent different levels of knowledge and learning ability, which is a characteristic that is relatively easy to cause conflicts [11]. Thus contradictions and conflicts within the TMT with high education heterogeneity are more serious, which may reduce the decision-making efficiency and decrease the enterprise’s level of risk taking.

5.2. Recommendations for Practice

(1) First, Chinese private construction companies are encouraged to spontaneously change the status quo of family businesses and introduce external members to the TMT. Family-led enterprises are often conservative in their decision making, which causes the company to lose out on many opportunities for innovation and profit. In particular, the current wave of digital reform requires companies to adjust their development strategy of transformation in a timely manner [7]. Young executives introduced from the outside are often active in their engagement, have strong learning ability, are more confident, have greater willingness to take certain risks in exchange for more benefits, and strive to challenge themselves.

(2) Bring an appropriate increase in the proportion and position of women in the TMT. Private construction companies are high-risk, and an excessive proportion of male executives is likely to result in strategic decisions that are too radical or unscientific due to overconfidence. Appropriately increasing the proportion and position of women in the TMT can provide more scientific supervision and rigorous management of high-risk enterprises.

(3) Hire well-educated and international talent for the TMT. Well-educated talent has a strong grasp of the changing market environment and international talent can bring advanced experience. With private construction enterprises in urgent need of development, hiring well-educated and international professionals for the TMTs can appropriately improve the risk-taking level of private construction enterprises and promote better and faster development.

(4) Fourth, maintain a moderate level of heterogeneity in the TMT. Too high TMT heterogeneity will lead to the increase of contradictions and conflicts; too low heterogeneity of the TMT can easily lead to the team’s single perspective of thinking, unable to analyze problems in multiple dimensions, and resulting in errors in decision making. As mentioned, most of the Chinese private construction enterprises are family enterprises, and important senior management positions are often held by family members, which leads to the consistency of the background and objectives of the TMT. Therefore, private construction enterprises can control risks within a reasonable range by properly maintaining the heterogeneity level of the TMT.

Since the reform and opening up, private enterprises have been an indispensable and important force in the process of China’s sustainable economic development. Private construction enterprises have been the backbone of China’s urban construction and infrastructure development for decades; therefore, the healthy development of private construction enterprises is of great significance to China’s urban development and economic growth. Currently, the development of private construction enterprises requires significant effort from multiple channels, ranging from theoretical research to practice.

The research limitations of this paper are as follows: First, it only studies the linear relationship between the characteristics of the TMT of private construction enterprises and the heterogeneity on the enterprises’ risk taking, and whether the impact of the characteristics of TMT on the risk taking of private construction enterprises is non-linear (such as U-shaped or inverted U-shaped) needs further discussion; The second is that this paper does not deeply explore how the TMT of private construction enterprises affects their enterprise risk through a certain transmission mechanism, and does not carry out the research on the intermediary effect of the influence mechanism of the characteristics of the TMT on the risk of private construction enterprises. Future research can be carried out from these two aspects.

Author Contributions

Conceptualization, Y.Z.; methodology, all authors; formal analysis, Y.Z. and C.C.; investigation, J.G.; resources, all authors; data curation, C.C.; writing—original draft preparation, Y.Z. and C.C.; writing—review and editing, H.G.; supervision, Y.Z. and H.G.; project administration, Y.Z.; funding acquisition, Y.Z. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by [Project of Longyuan Construction Finance Research Institute, NingBo University] grant number [LYZDB2009] And The APC was funded by [Project of Longyuan Construction Finance Research Institute, NingBo University].

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Wang, Y.; Li, Y.; Yan, H. Comparative study on the competitiveness of listed state-owned and private enterprises in the construction industry. J. Eng. Manag. 2020, 34, 16–20. [Google Scholar]

- Zhang, L. Research on Internationalization Strategy Optimization of C Group as a Private Construction Enterprise; University of Finance and Economics: Shandong, China, 2018; pp. 1–58. [Google Scholar]

- Wang, C.M.; Xu, B.B.; Zhang, S.J.; Chen, Y.Q. Influence of personality and risk propensity on risk perception of Chinese construction project managers. Int. J. Proj. Manag. 2016, 34, 1294–1304. [Google Scholar] [CrossRef]

- Zeng, S.Z.; Hu, Y.; Llopis-Albert, C. Stakeholder-inclusive multi-criteria development of smart cities. J. Bus. Res. 2023, 154, 113281. [Google Scholar] [CrossRef]

- Moshood, T.D.; Adeleke, A.Q.; Nawanir, G.; Mahmud, F. Ranking of human factors affecting contractors’ risk attitudes in the Malaysian construction industry. Soc. Sci. Humanit. Open 2020, 2, 100064. [Google Scholar] [CrossRef]

- Taofeeq, D.M.; Adeleke, A.Q.; Lee, C.K. Individual factors influencing contractors’ risk attitudes among Malaysian construction industries: The moderating role of government policy. Int. J. Constr. Manag. 2019, 22, 612–631. [Google Scholar] [CrossRef]

- Taofeeq, D.M.; Adeleke, A.Q.; Ajibike, W.A. Human factors influencing contractors’ risk attitudes: A case study of the Malaysian construction industry. Constr. Econ. Build. 2020, 20, 96–116. [Google Scholar]

- Taofeeq, D.M.; Adeleke, A.Q.; Lee, C.K. The synergy between human factors and risk attitudes of Malaysian contractors’: Moderating effect of government policy. Saf. Sci. 2020, 121, 331–347. [Google Scholar] [CrossRef]

- Zeng, S.Z.; Zhou, J.M.; Zhang, C.H.; Merigó, J.M. Intuitionistic fuzzy social network hybrid MCDM model for an assessment of digital reforms of manufacturing industry in China. Technol. Forecast. Soc. Chang. 2022, 176, 121435. [Google Scholar] [CrossRef]

- Battilana, J.; Casciaro, T. Change Agents, Networks, and Institutions: A Contingency Theory of Organizational Change. Acad. Manag. J. 2012, 55, 381–398. [Google Scholar] [CrossRef] [Green Version]

- Sambharya, R.B. Foreign Experience of Top Management Teams and International Diversification Strategies of U.S. Multinational Corporations. Strateg. Manag. J. 2015, 17, 739–746. [Google Scholar] [CrossRef]

- Lin, D.; Lu, J.; Liu, X.; Choi, S.-J. Returnee CEO and Innovation in Chinese High-Tech Smes. Int. J. Technol. Manag. 2014, 65, 151–171. [Google Scholar] [CrossRef]

- Sperber, S.; Linder, C. The Impact of Top Management Teams on Firm Innovativeness: A Configurational Analysis of Demographic Characteristics, Leadership Style and Team Power Distribution. Rev. Manag. Sci. 2018, 12, 285–316. [Google Scholar] [CrossRef]

- Dess, G.G.; Lumpkin, G.T. Research Edge: The Role of Entrepreneurial Orientation in Stimulating Effective Corporate Entrepreneurship. Acad. Manag. Perspect. 2005, 19, 147–156. [Google Scholar] [CrossRef]

- John, K.; Litov, L.; Yeung, B. Corporate Governance and Risk-Taking. J. Financ. 2008, 63, 1679–1728. [Google Scholar] [CrossRef]

- Low, A. Managerial Risk-Taking Behavior and Equity-Based Compensation. J. Financ. Econ. 2008, 92, 470–490. [Google Scholar] [CrossRef]

- Coles, J.L.; Daniel, N.D.; Naveen, L. Managerial Incentives and Risk-taking. J. Financ. Econ. 2006, 79, 431–468. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper Echelons: The Organization as a Reflection of Its Top Managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Wiersema, M.F.; Bantel, K.A. Top Management Team Demography and Corporate Strategic Change. Acad. Manag. J. 1992, 35, 91–121. [Google Scholar] [CrossRef]

- Bodie, Z.; Kane, A.; Marcus, A.J. Investment, 10th ed.; Machinery Industry Press: Beijing, China, 2017; pp. 130–140. [Google Scholar]

- Gottardo, P.; Moisello, A.M. Family Firms, Risk-Taking and Financial Distress. Probl. Perspect. Manag. 2017, 15, 168–177. [Google Scholar] [CrossRef] [Green Version]

- Huybrechts, J.; Voordeckers, W.; Lybaert, N. Entrepreneurial Risk Taking of Private Family Firms: The Influence of a Non-Family CEO and the Moderating Effect of CEO Tenure. Fam. Bus. Rev. 2013, 26, 161–179. [Google Scholar] [CrossRef]

- Yeoh, S.B.; Hooy, C.W. CEO Age and Risk-Taking of Family Business in Malaysia: The Inverse S-curve Relationship. Asia Pac. J. Manag. 2020, 39, 273–293. [Google Scholar] [CrossRef]

- Zhang, C.; Luo, L. Board Diversity and Risk-Taking of Family Firms: Evidence from China. Int. Entrep. Manag. J. 2021, 17, 1569–1590. [Google Scholar] [CrossRef]

- Chen, C.; Sun, J. Entrepreneurs’ Demographic Background Characteristics and Diversification Strategy Choices: An Empirical Study Based on Panel Data of Chinese Listed Companies. Manag. World 2008, 5, 124–133. (In Chinese) [Google Scholar]

- Chowdhury, J.; Fink, J. How Does CEO Age Affect Firm Risk? Asia-Pac. J. Financ. Stud. 2017, 46, 381–412. [Google Scholar] [CrossRef]

- Tanikawa, T.; Jung, Y. Top Management Team (TMT) Tenure Diversity and Firm Performance: Examining the Moderating Effect of TMT Average Age. Int. J. Organ. Anal. 2016, 24, 454–470. [Google Scholar] [CrossRef]

- Rowley, R.; Kang, H.-R.; Lim, H.-J. Female Manager Career Success: The Importance of Individual and Organizational Factors in South Korea. Asia Pac. J. Hum. Resour. 2016, 54, 98–122. [Google Scholar] [CrossRef]

- Byron, K.; Post, C. Women on Boards and Firm Financial Performance: A Meta-Analysis. Acad. Manag. J. 2015, 58, 1546–1571. [Google Scholar]

- Felton, J.; Gibson, B.; Sanbonmatsu, D.M. Preference for Risk in Investing as a Function of Trait Optimism and Gender. Soc. Sci. Electron. Publ. 2003, 4, 33–40. [Google Scholar] [CrossRef]

- Francis, B.; Hasan, I.; Park, J.C.; Wu, Q. Gender Differences in Financial Reporting Decision Making: Evidence from Accounting Conservatism. Contemp. Account. Res. 2015, 32, 1285–1318. [Google Scholar] [CrossRef]

- King, T.; Srivastav, A.; Williams, J. What’s in an Education? Implications of CEO Education for Bank Performance. J. Corp. Financ. 2016, 37, 287–308. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Chirico, F.; Zyung, J.D.; Gambeta, E. Managerial Risk Taking: A Multitheoretical Review and Future Research Agenda. J. Manag. 2016, 43, 137–169. [Google Scholar] [CrossRef] [Green Version]

- Oh, W.Y.; Chang, Y.K.; Cheng, Z. When CEO Career Horizon Problems Matter for Corporate Social Responsibility: The Moderating Roles of Industry-Level Discretion and Blockholder Ownership. J. Bus. Ethics 2016, 133, 279–291. [Google Scholar] [CrossRef]

- Heyden, M.L.M.; Reimer, M.; van Doorn, S. Innovating Beyond the Horizon: CEO Career Horizon, Top Management Composition, and R&D Intensity. Hum. Resour. Manag. 2017, 56, 205–224. [Google Scholar]

- Mohr, A.; Batsakis, G. The Contingent Effect of TMT International Experience on Firms’ Internationalization Speed. Br. J. Manag. 2019, 30, 869–887. [Google Scholar] [CrossRef]

- Yuan, R.; Wen, R. Managerial Foreign Experience and Corporate Innovation. J. Corp. Financ. 2018, 48, 752–770. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Eden, L.; Lau, C.M.; Wright, M. Strategy in Emerging Economies. Acad. Manag. J. 2000, 43, 249–267. [Google Scholar] [CrossRef]

- He, W.; Liu, W. Management Team Characteristics and Dynamic Adjustment of Capital Structure. Financ. Res. 2015, 3, 50–62. (In Chinese) [Google Scholar]

- Li, X.; Zhang, R. Equity Incentives Affect Risk-Taking: Agency Costs or Risk Aversion? Account. Res. 2014, 1, 57–63. [Google Scholar]

- Faccio, M.; Marchica, M.-T.; Mura, R. Large Shareholder Diversification and Corporate Risk-Taking. Rev. Financ. Stud. 2011, 24, 3601–3641. [Google Scholar] [CrossRef] [Green Version]

- Li, W.; Yu, M. Nature of Ownership, Marketization Process and Enterprise Risk Taking. China Ind. Econ. 2012, 12, 115–127. [Google Scholar]

- Zhang, M.; Tong, L.; Xu, H. Social Networks and Corporate Risk Taking—Empirical Evidence Based on Listed Companies in China. Manag. World 2015, 11, 161–175. [Google Scholar]

- Carpenter, M.A.; Geletkanycz, M.A.; Sanders, W.G. Upper Echilons research Revisited: Antecedents, Element, and Consequences of Top Management Team Composition. J. Manag. 2004, 30, 749–778. [Google Scholar]

- Collins, R.; Blau, P.M. Inequality and Heterogeneity: A Primitive Theory of Social Structure. Soc. Forces 1977, 58, 677. [Google Scholar] [CrossRef]

- Allison, P. Measures of Inequality. Am. Sociol. Rev. 1978, 43, 865–880. [Google Scholar] [CrossRef]

Figure 1.

The number of state-owned construction enterprises and private construction enterprises and the average output value.

Figure 1.

The number of state-owned construction enterprises and private construction enterprises and the average output value.

{kind=link}

Table 1.

Variable definition.

| Type | Variable | Formula and Explanation |

|---|---|---|

| Explained variable | risk-taking level (Ris) | (Measure a company’s earnings volatility reflects the riskiness of investment decisions) |

| Core explanatory variables | Age (Age) | Average age of the company’s TMT |

| Gender (Gen) | (Proportion of women to the total number of TMT members) | |

| Education (Edu) | With technical secondary school and below being 1, junior college 2, undergraduate 3, master’s degree 4, and doctor’s degree 5. Finally, the average is taken to represent the average educational level of each company’s TMT each year | |

| Tenure (Ten) | Average tenure of TMT members | |

| Overseas background (Ovs) | The proportion of those with overseas backgrounds to the total TMT members | |

| Control variables | main business profit margin (Mainpro) | (the percentage of the main business profit and the main business income) |

| Size (Siz) | (The natural logarithm of the company’s total assets at the end of the year) | |

| houseprice index (Hpr) | (the ratio of the national average house price in the current year to the national average house price in the previous year) | |

| proportion of independent directors (Idr) | (The ratio of independent directors on the board) | |

| shareholding ratio of the largest shareholder (Tp1) | (The shareholding ratio of the largest shareholder) |

Table 2.

Descriptive statistics (2009–2019).

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Ris | 648 | 0.0346 | 0.0594 | 0.0001 | 0.4496 |

| Age | 648 | 47.3051 | 3.1497 | 37.0000 | 57.3571 |

| Gen | 648 | 0.1919 | 0.1069 | 0.0000 | 0.5625 |

| Edu | 648 | 3.2895 | 0.3581 | 2.2777 | 4.2631 |

| Ten | 648 | 3.7375 | 1.3774 | 1.0000 | 8.5789 |

| Ovs | 648 | 0.0696 | 0.0804 | 0.0000 | 0.5333 |

| Mainpro | 648 | 0.0268 | 0.0438 | -0.4755 | 0.4807 |

| Siz | 648 | 21.9990 | 1.4156 | 16.1847 | 26.4284 |

| Hpr | 648 | 1.0815 | 0.0414 | 1.0139 | 1.2318 |

| Idr | 648 | 0.3758 | 0.0512 | 0.2500 | 0.6000 |

| Tp1 | 648 | 0.3188 | 0.1305 | 0.0449 | 0.8186 |

Table 3.

Regression results of TMT characteristics and risk taking.

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Age | −0.002 ** | −0.001 ** | ||||

| (−2.29) | (−2.23) | |||||

| Gen | −0.033 * | −0.052 ** | ||||

| (−1.66) | (−2.56) | |||||

| Edu | 0.016 ** | 0.015 ** | ||||

| (2.57) | (2.19) | |||||

| Ten | 0.002 | 0.002 | ||||

| (1.15) | (1.08) | |||||

| Ovs | 0.038 | 0.016 | ||||

| (1.46) | (0.58) | |||||

| Mainpro | −0.001 ** | −0.001 ** | −0.001 ** | −0.001 ** | −0.001 ** | −0.001 ** |

| (−2.34) | (−2.21) | (−2.16) | (−2.29) | (−2.22) | (−2.29) | |

| Siz | −0.010 *** | −0.011 *** | −0.012 *** | −0.010 *** | −0.010 *** | −0.012 *** |

| (−5.97) | (−6.62) | (−6.93) | (−6.50) | (−6.54) | (−6.83) | |

| Hpr | 0.058 | 0.056 | 0.056 | 0.060 | 0.058 | 0.049 |

| (1.16) | (1.11) | (1.11) | (1.19) | (1.14) | (0.97) | |

| Idr | 0.061 | 0.069 * | 0.046 | 0.058 | 0.061 | 0.054 |

| (1.51) | (1.67) | (1.12) | (1.41) | (1.49) | (1.32) | |

| Tp1 | −0.064 *** | −0.064 *** | −0.071 *** | −0.063 *** | −0.068 *** | −0.072 *** |

| (−3.93) | (−3.90) | (−4.32) | (−3.87) | (−4.11) | (−4.37) | |

| Constant | 0.252 *** | 0.210 *** | 0.182 ** | 0.190 *** | 0.198 *** | 0.269 *** |

| (3.35) | (2.94) | (2.57) | (2.69) | (2.80) | (3.51) | |

| Observations | 640 | 640 | 640 | 640 | 640 | 640 |

| R−squared | 0.13 | 0.12 | 0.13 | 0.13 | 0.13 | 0.15 |

Note: *, **, *** means the parameters are significant at 10%, 5%, and 1% levels, respectively, and the t statistic is in parentheses, the same below.

Table 4.

Regression results after replacing the explained variable.

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Age | −0.022 *** | −0.025 *** | ||||

| (−3.07) | (−3.51) | |||||

| Gen | −0.778 *** | −1.013 *** | ||||

| (−3.70) | (−4.75) | |||||

| Edu | 0.146 ** | 0.214 *** | ||||

| (2.17) | (2.97) | |||||

| Ten | 0.011 | 0.008 | ||||

| (0.69) | (0.52) | |||||

| Ovs | −0.250 | −0.551 * | ||||

| (−0.89) | (−1.87) | |||||

| Concrols | Yes | |||||

| Constant | 1.028 | 0.593 | 0.083 | 0.167 | 0.139 | 1.446 * |

| (1.28) | (0.78) | (0.11) | (0.22) | (0.18) | (1.79) | |

| Observations | 642 | 642 | 642 | 642 | 642 | 642 |

| R−squared | 0.03 | 0.03 | 0.02 | 0.01 | 0.01 | 0.07 |

Table 5.

Regression results after resetting the education variable.

| Variables | (1) | (2) |

|---|---|---|

| Age | −0.002 ** | |

| (−2.33) | ||

| Gen | −0.052 ** | |

| (−2.57) | ||

| Eduy | 0.006 ** | 0.006 ** |

| (2.32) | (2.09) | |

| Ten | 0.002 | |

| (1.15) | ||

| Ovs | 0.019 | |

| (0.68) | ||

| Mainpro | −0.001 ** | −0.001 ** |

| (−2.16) | (−2.29) | |

| Controls | √ | √ |

| Constant | 0.129 * | 0.221 *** |

| (1.70) | (2.67) | |

| Observations | 640 | 640 |

| R−squared | 0.13 | 0.15 |

Table 6.

Regression results of impact of TMT heterogeneity on risk taking.

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Hage | 0.118 ** | 0.146 *** | |||

| (2.58) | (3.21) | ||||

| Hgen | −0.043 ** | −0.052 *** | |||

| (−2.54) | (−3.09) | ||||

| Hedu | −0.098 *** | −0.105 *** | |||

| (−3.62) | (−3.71) | ||||

| Hten | 0.027 *** | 0.019 ** | |||

| (3.16) | (2.19) | ||||

| Controls | √ | √ | √ | √ | √ |

| Constant | 0.189 *** | 0.222 *** | 0.235 *** | 0.202 *** | 0.277 *** |

| (2.68) | (3.11) | (3.31) | (2.87) | (3.89) | |

| Observations | 640 | 640 | 640 | 640 | 640 |

| R−squared | 0.13 | 0.13 | 0.14 | 0.14 | 0.18 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhang, Y.; Cao, C.; Gu, J.; Garg, H. The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises. Systems 2023, 11, 67. https://doi.org/10.3390/systems11020067

AMA Style

Zhang Y, Cao C, Gu J, Garg H. The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises. Systems. 2023; 11(2):67. https://doi.org/10.3390/systems11020067

Chicago/Turabian StyleZhang, Yunhua, Chen Cao, Jiaxing Gu, and Harish Garg. 2023. "The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises" Systems 11, no. 2: 67. https://doi.org/10.3390/systems11020067

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.