The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises

Abstract

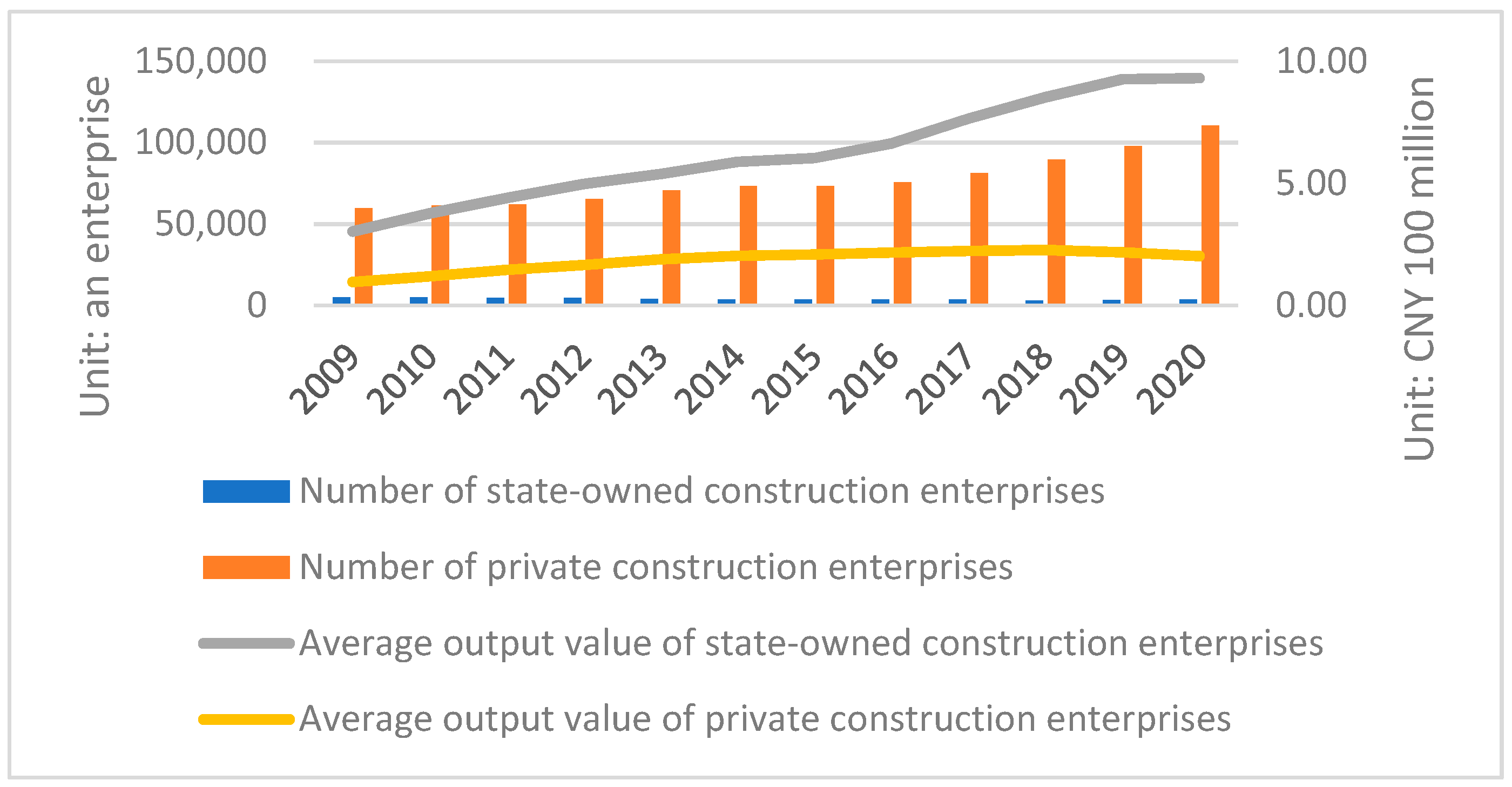

1. Introduction

2. Definition of Core Concepts, Literature Review, and Research Hypothesis

2.1. Definition of Core Concepts

2.1.1. TMT and TMT Characteristics

2.1.2. Risk-Taking Level

2.2. Literature Review

2.2.1. Risk Taking by Family Firms

2.2.2. TMT Age and Risk-Taking Level

2.2.3. TMT Gender and Risk-Taking Level

2.2.4. TMT Education and Risk-Taking Level

2.2.5. TMT Tenure and Risk-Taking Level

2.2.6. TMT Overseas Background and Risk-Taking Level

3. Research Design

3.1. Study Subjects and Data Sources

3.2. Variable Setting

3.2.1. Explained Variable

3.2.2. Core Explanatory Variables

- Age (Age): Average age of the company’s TMT.

- Gender (Gen): Proportion of women to the total number of TMT members.

- Education (Edu): After collecting details of the educational qualifications of various executives, a score is manually assigned, with technical secondary school and below being 1, junior college 2, undergraduate 3, master’s degree 4, and doctor’s degree 5. Finally, the average is taken to represent the average educational level of each company’s TMT each year.

- Tenure (Ten): Average tenure of TMT members.

- Overseas background (Ovs): The proportion of those with overseas backgrounds to the total TMT members.

3.2.3. Control Variables

- Main business profit margin (Mainpro). The main business profit margin is the percentage of the main business profit and the main business income. The higher the index, the higher the added value of the enterprise’s products, the stronger competitiveness of the main business market, the greater development potential and the higher profit level.

- Enterprise size (Siz). The natural logarithm of the company’s total assets at the end of the year measures its size.

- House price index (Hpr). This is the ratio of the national average house price in the current year to the national average house price in the previous year. As mentioned the private construction industry is closely related to the real estate industry, and fluctuations in one industry can directly impact the level of risk in another.

- Proportion of independent directors (Idr). Refers to the ratio of independent directors on the board. It is generally believed that independent directors can act as external supervisors of the company, playing a supervisory role in the company’s daily operations and limiting excessive risk behavior.

- Shareholding ratio of the largest shareholder (Tp1). Most Chinese private construction companies are family-owned enterprises and the largest shareholder is often the company’s founder. Further, the shareholding ratio is generally very high. However, if the shareholding ratio is too high, it may lead to the phenomenon where the decision making serves the interests of the family rather than the company [3].

3.3. Model Settings

4. Empirical Test

4.1. Descriptive Statistics

4.2. Regression Analysis

4.3. Robustness Test

4.4. Heterogeneity Analysis

5. Conclusions

5.1. Research Conclusions

5.2. Recommendations for Practice

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wang, Y.; Li, Y.; Yan, H. Comparative study on the competitiveness of listed state-owned and private enterprises in the construction industry. J. Eng. Manag. 2020, 34, 16–20. [Google Scholar]

- Zhang, L. Research on Internationalization Strategy Optimization of C Group as a Private Construction Enterprise; University of Finance and Economics: Shandong, China, 2018; pp. 1–58. [Google Scholar]

- Wang, C.M.; Xu, B.B.; Zhang, S.J.; Chen, Y.Q. Influence of personality and risk propensity on risk perception of Chinese construction project managers. Int. J. Proj. Manag. 2016, 34, 1294–1304. [Google Scholar] [CrossRef]

- Zeng, S.Z.; Hu, Y.; Llopis-Albert, C. Stakeholder-inclusive multi-criteria development of smart cities. J. Bus. Res. 2023, 154, 113281. [Google Scholar] [CrossRef]

- Moshood, T.D.; Adeleke, A.Q.; Nawanir, G.; Mahmud, F. Ranking of human factors affecting contractors’ risk attitudes in the Malaysian construction industry. Soc. Sci. Humanit. Open 2020, 2, 100064. [Google Scholar] [CrossRef]

- Taofeeq, D.M.; Adeleke, A.Q.; Lee, C.K. Individual factors influencing contractors’ risk attitudes among Malaysian construction industries: The moderating role of government policy. Int. J. Constr. Manag. 2019, 22, 612–631. [Google Scholar] [CrossRef]

- Taofeeq, D.M.; Adeleke, A.Q.; Ajibike, W.A. Human factors influencing contractors’ risk attitudes: A case study of the Malaysian construction industry. Constr. Econ. Build. 2020, 20, 96–116. [Google Scholar]

- Taofeeq, D.M.; Adeleke, A.Q.; Lee, C.K. The synergy between human factors and risk attitudes of Malaysian contractors’: Moderating effect of government policy. Saf. Sci. 2020, 121, 331–347. [Google Scholar] [CrossRef]

- Zeng, S.Z.; Zhou, J.M.; Zhang, C.H.; Merigó, J.M. Intuitionistic fuzzy social network hybrid MCDM model for an assessment of digital reforms of manufacturing industry in China. Technol. Forecast. Soc. Chang. 2022, 176, 121435. [Google Scholar] [CrossRef]

- Battilana, J.; Casciaro, T. Change Agents, Networks, and Institutions: A Contingency Theory of Organizational Change. Acad. Manag. J. 2012, 55, 381–398. [Google Scholar] [CrossRef]

- Sambharya, R.B. Foreign Experience of Top Management Teams and International Diversification Strategies of U.S. Multinational Corporations. Strateg. Manag. J. 2015, 17, 739–746. [Google Scholar] [CrossRef]

- Lin, D.; Lu, J.; Liu, X.; Choi, S.-J. Returnee CEO and Innovation in Chinese High-Tech Smes. Int. J. Technol. Manag. 2014, 65, 151–171. [Google Scholar] [CrossRef]

- Sperber, S.; Linder, C. The Impact of Top Management Teams on Firm Innovativeness: A Configurational Analysis of Demographic Characteristics, Leadership Style and Team Power Distribution. Rev. Manag. Sci. 2018, 12, 285–316. [Google Scholar] [CrossRef]

- Dess, G.G.; Lumpkin, G.T. Research Edge: The Role of Entrepreneurial Orientation in Stimulating Effective Corporate Entrepreneurship. Acad. Manag. Perspect. 2005, 19, 147–156. [Google Scholar] [CrossRef]

- John, K.; Litov, L.; Yeung, B. Corporate Governance and Risk-Taking. J. Financ. 2008, 63, 1679–1728. [Google Scholar] [CrossRef]

- Low, A. Managerial Risk-Taking Behavior and Equity-Based Compensation. J. Financ. Econ. 2008, 92, 470–490. [Google Scholar] [CrossRef]

- Coles, J.L.; Daniel, N.D.; Naveen, L. Managerial Incentives and Risk-taking. J. Financ. Econ. 2006, 79, 431–468. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper Echelons: The Organization as a Reflection of Its Top Managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Wiersema, M.F.; Bantel, K.A. Top Management Team Demography and Corporate Strategic Change. Acad. Manag. J. 1992, 35, 91–121. [Google Scholar] [CrossRef]

- Bodie, Z.; Kane, A.; Marcus, A.J. Investment, 10th ed.; Machinery Industry Press: Beijing, China, 2017; pp. 130–140. [Google Scholar]

- Gottardo, P.; Moisello, A.M. Family Firms, Risk-Taking and Financial Distress. Probl. Perspect. Manag. 2017, 15, 168–177. [Google Scholar] [CrossRef]

- Huybrechts, J.; Voordeckers, W.; Lybaert, N. Entrepreneurial Risk Taking of Private Family Firms: The Influence of a Non-Family CEO and the Moderating Effect of CEO Tenure. Fam. Bus. Rev. 2013, 26, 161–179. [Google Scholar] [CrossRef]

- Yeoh, S.B.; Hooy, C.W. CEO Age and Risk-Taking of Family Business in Malaysia: The Inverse S-curve Relationship. Asia Pac. J. Manag. 2020, 39, 273–293. [Google Scholar] [CrossRef]

- Zhang, C.; Luo, L. Board Diversity and Risk-Taking of Family Firms: Evidence from China. Int. Entrep. Manag. J. 2021, 17, 1569–1590. [Google Scholar] [CrossRef]

- Chen, C.; Sun, J. Entrepreneurs’ Demographic Background Characteristics and Diversification Strategy Choices: An Empirical Study Based on Panel Data of Chinese Listed Companies. Manag. World 2008, 5, 124–133. (In Chinese) [Google Scholar]

- Chowdhury, J.; Fink, J. How Does CEO Age Affect Firm Risk? Asia-Pac. J. Financ. Stud. 2017, 46, 381–412. [Google Scholar] [CrossRef]

- Tanikawa, T.; Jung, Y. Top Management Team (TMT) Tenure Diversity and Firm Performance: Examining the Moderating Effect of TMT Average Age. Int. J. Organ. Anal. 2016, 24, 454–470. [Google Scholar] [CrossRef]

- Rowley, R.; Kang, H.-R.; Lim, H.-J. Female Manager Career Success: The Importance of Individual and Organizational Factors in South Korea. Asia Pac. J. Hum. Resour. 2016, 54, 98–122. [Google Scholar] [CrossRef]

- Byron, K.; Post, C. Women on Boards and Firm Financial Performance: A Meta-Analysis. Acad. Manag. J. 2015, 58, 1546–1571. [Google Scholar]

- Felton, J.; Gibson, B.; Sanbonmatsu, D.M. Preference for Risk in Investing as a Function of Trait Optimism and Gender. Soc. Sci. Electron. Publ. 2003, 4, 33–40. [Google Scholar] [CrossRef]

- Francis, B.; Hasan, I.; Park, J.C.; Wu, Q. Gender Differences in Financial Reporting Decision Making: Evidence from Accounting Conservatism. Contemp. Account. Res. 2015, 32, 1285–1318. [Google Scholar] [CrossRef]

- King, T.; Srivastav, A.; Williams, J. What’s in an Education? Implications of CEO Education for Bank Performance. J. Corp. Financ. 2016, 37, 287–308. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Chirico, F.; Zyung, J.D.; Gambeta, E. Managerial Risk Taking: A Multitheoretical Review and Future Research Agenda. J. Manag. 2016, 43, 137–169. [Google Scholar] [CrossRef]

- Oh, W.Y.; Chang, Y.K.; Cheng, Z. When CEO Career Horizon Problems Matter for Corporate Social Responsibility: The Moderating Roles of Industry-Level Discretion and Blockholder Ownership. J. Bus. Ethics 2016, 133, 279–291. [Google Scholar] [CrossRef]

- Heyden, M.L.M.; Reimer, M.; van Doorn, S. Innovating Beyond the Horizon: CEO Career Horizon, Top Management Composition, and R&D Intensity. Hum. Resour. Manag. 2017, 56, 205–224. [Google Scholar]

- Mohr, A.; Batsakis, G. The Contingent Effect of TMT International Experience on Firms’ Internationalization Speed. Br. J. Manag. 2019, 30, 869–887. [Google Scholar] [CrossRef]

- Yuan, R.; Wen, R. Managerial Foreign Experience and Corporate Innovation. J. Corp. Financ. 2018, 48, 752–770. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Eden, L.; Lau, C.M.; Wright, M. Strategy in Emerging Economies. Acad. Manag. J. 2000, 43, 249–267. [Google Scholar] [CrossRef]

- He, W.; Liu, W. Management Team Characteristics and Dynamic Adjustment of Capital Structure. Financ. Res. 2015, 3, 50–62. (In Chinese) [Google Scholar]

- Li, X.; Zhang, R. Equity Incentives Affect Risk-Taking: Agency Costs or Risk Aversion? Account. Res. 2014, 1, 57–63. [Google Scholar]

- Faccio, M.; Marchica, M.-T.; Mura, R. Large Shareholder Diversification and Corporate Risk-Taking. Rev. Financ. Stud. 2011, 24, 3601–3641. [Google Scholar] [CrossRef]

- Li, W.; Yu, M. Nature of Ownership, Marketization Process and Enterprise Risk Taking. China Ind. Econ. 2012, 12, 115–127. [Google Scholar]

- Zhang, M.; Tong, L.; Xu, H. Social Networks and Corporate Risk Taking—Empirical Evidence Based on Listed Companies in China. Manag. World 2015, 11, 161–175. [Google Scholar]

- Carpenter, M.A.; Geletkanycz, M.A.; Sanders, W.G. Upper Echilons research Revisited: Antecedents, Element, and Consequences of Top Management Team Composition. J. Manag. 2004, 30, 749–778. [Google Scholar]

- Collins, R.; Blau, P.M. Inequality and Heterogeneity: A Primitive Theory of Social Structure. Soc. Forces 1977, 58, 677. [Google Scholar] [CrossRef]

- Allison, P. Measures of Inequality. Am. Sociol. Rev. 1978, 43, 865–880. [Google Scholar] [CrossRef]

{kind=link}

| Type | Variable | Formula and Explanation |

|---|---|---|

| Explained variable | risk-taking level (Ris) | (Measure a company’s earnings volatility reflects the riskiness of investment decisions) |

| Core explanatory variables | Age (Age) | Average age of the company’s TMT |

| Gender (Gen) | (Proportion of women to the total number of TMT members) | |

| Education (Edu) | With technical secondary school and below being 1, junior college 2, undergraduate 3, master’s degree 4, and doctor’s degree 5. Finally, the average is taken to represent the average educational level of each company’s TMT each year | |

| Tenure (Ten) | Average tenure of TMT members | |

| Overseas background (Ovs) | The proportion of those with overseas backgrounds to the total TMT members | |

| Control variables | main business profit margin (Mainpro) | (the percentage of the main business profit and the main business income) |

| Size (Siz) | (The natural logarithm of the company’s total assets at the end of the year) | |

| houseprice index (Hpr) | (the ratio of the national average house price in the current year to the national average house price in the previous year) | |

| proportion of independent directors (Idr) | (The ratio of independent directors on the board) | |

| shareholding ratio of the largest shareholder (Tp1) | (The shareholding ratio of the largest shareholder) |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Ris | 648 | 0.0346 | 0.0594 | 0.0001 | 0.4496 |

| Age | 648 | 47.3051 | 3.1497 | 37.0000 | 57.3571 |

| Gen | 648 | 0.1919 | 0.1069 | 0.0000 | 0.5625 |

| Edu | 648 | 3.2895 | 0.3581 | 2.2777 | 4.2631 |

| Ten | 648 | 3.7375 | 1.3774 | 1.0000 | 8.5789 |

| Ovs | 648 | 0.0696 | 0.0804 | 0.0000 | 0.5333 |

| Mainpro | 648 | 0.0268 | 0.0438 | -0.4755 | 0.4807 |

| Siz | 648 | 21.9990 | 1.4156 | 16.1847 | 26.4284 |

| Hpr | 648 | 1.0815 | 0.0414 | 1.0139 | 1.2318 |

| Idr | 648 | 0.3758 | 0.0512 | 0.2500 | 0.6000 |

| Tp1 | 648 | 0.3188 | 0.1305 | 0.0449 | 0.8186 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Age | −0.002 ** | −0.001 ** | ||||

| (−2.29) | (−2.23) | |||||

| Gen | −0.033 * | −0.052 ** | ||||

| (−1.66) | (−2.56) | |||||

| Edu | 0.016 ** | 0.015 ** | ||||

| (2.57) | (2.19) | |||||

| Ten | 0.002 | 0.002 | ||||

| (1.15) | (1.08) | |||||

| Ovs | 0.038 | 0.016 | ||||

| (1.46) | (0.58) | |||||

| Mainpro | −0.001 ** | −0.001 ** | −0.001 ** | −0.001 ** | −0.001 ** | −0.001 ** |

| (−2.34) | (−2.21) | (−2.16) | (−2.29) | (−2.22) | (−2.29) | |

| Siz | −0.010 *** | −0.011 *** | −0.012 *** | −0.010 *** | −0.010 *** | −0.012 *** |

| (−5.97) | (−6.62) | (−6.93) | (−6.50) | (−6.54) | (−6.83) | |

| Hpr | 0.058 | 0.056 | 0.056 | 0.060 | 0.058 | 0.049 |

| (1.16) | (1.11) | (1.11) | (1.19) | (1.14) | (0.97) | |

| Idr | 0.061 | 0.069 * | 0.046 | 0.058 | 0.061 | 0.054 |

| (1.51) | (1.67) | (1.12) | (1.41) | (1.49) | (1.32) | |

| Tp1 | −0.064 *** | −0.064 *** | −0.071 *** | −0.063 *** | −0.068 *** | −0.072 *** |

| (−3.93) | (−3.90) | (−4.32) | (−3.87) | (−4.11) | (−4.37) | |

| Constant | 0.252 *** | 0.210 *** | 0.182 ** | 0.190 *** | 0.198 *** | 0.269 *** |

| (3.35) | (2.94) | (2.57) | (2.69) | (2.80) | (3.51) | |

| Observations | 640 | 640 | 640 | 640 | 640 | 640 |

| R−squared | 0.13 | 0.12 | 0.13 | 0.13 | 0.13 | 0.15 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Age | −0.022 *** | −0.025 *** | ||||

| (−3.07) | (−3.51) | |||||

| Gen | −0.778 *** | −1.013 *** | ||||

| (−3.70) | (−4.75) | |||||

| Edu | 0.146 ** | 0.214 *** | ||||

| (2.17) | (2.97) | |||||

| Ten | 0.011 | 0.008 | ||||

| (0.69) | (0.52) | |||||

| Ovs | −0.250 | −0.551 * | ||||

| (−0.89) | (−1.87) | |||||

| Concrols | Yes | |||||

| Constant | 1.028 | 0.593 | 0.083 | 0.167 | 0.139 | 1.446 * |

| (1.28) | (0.78) | (0.11) | (0.22) | (0.18) | (1.79) | |

| Observations | 642 | 642 | 642 | 642 | 642 | 642 |

| R−squared | 0.03 | 0.03 | 0.02 | 0.01 | 0.01 | 0.07 |

| Variables | (1) | (2) |

|---|---|---|

| Age | −0.002 ** | |

| (−2.33) | ||

| Gen | −0.052 ** | |

| (−2.57) | ||

| Eduy | 0.006 ** | 0.006 ** |

| (2.32) | (2.09) | |

| Ten | 0.002 | |

| (1.15) | ||

| Ovs | 0.019 | |

| (0.68) | ||

| Mainpro | −0.001 ** | −0.001 ** |

| (−2.16) | (−2.29) | |

| Controls | √ | √ |

| Constant | 0.129 * | 0.221 *** |

| (1.70) | (2.67) | |

| Observations | 640 | 640 |

| R−squared | 0.13 | 0.15 |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Hage | 0.118 ** | 0.146 *** | |||

| (2.58) | (3.21) | ||||

| Hgen | −0.043 ** | −0.052 *** | |||

| (−2.54) | (−3.09) | ||||

| Hedu | −0.098 *** | −0.105 *** | |||

| (−3.62) | (−3.71) | ||||

| Hten | 0.027 *** | 0.019 ** | |||

| (3.16) | (2.19) | ||||

| Controls | √ | √ | √ | √ | √ |

| Constant | 0.189 *** | 0.222 *** | 0.235 *** | 0.202 *** | 0.277 *** |

| (2.68) | (3.11) | (3.31) | (2.87) | (3.89) | |

| Observations | 640 | 640 | 640 | 640 | 640 |

| R−squared | 0.13 | 0.13 | 0.14 | 0.14 | 0.18 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Y.; Cao, C.; Gu, J.; Garg, H. The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises. Systems 2023, 11, 67. https://doi.org/10.3390/systems11020067

Zhang Y, Cao C, Gu J, Garg H. The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises. Systems. 2023; 11(2):67. https://doi.org/10.3390/systems11020067

Chicago/Turabian StyleZhang, Yunhua, Chen Cao, Jiaxing Gu, and Harish Garg. 2023. "The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises" Systems 11, no. 2: 67. https://doi.org/10.3390/systems11020067

APA StyleZhang, Y., Cao, C., Gu, J., & Garg, H. (2023). The Impact of Top Management Team Characteristics on the Risk Taking of Chinese Private Construction Enterprises. Systems, 11(2), 67. https://doi.org/10.3390/systems11020067