A Systemic Analysis of Vestigial Racism in Housing Finance †

Abstract

:1. Introduction

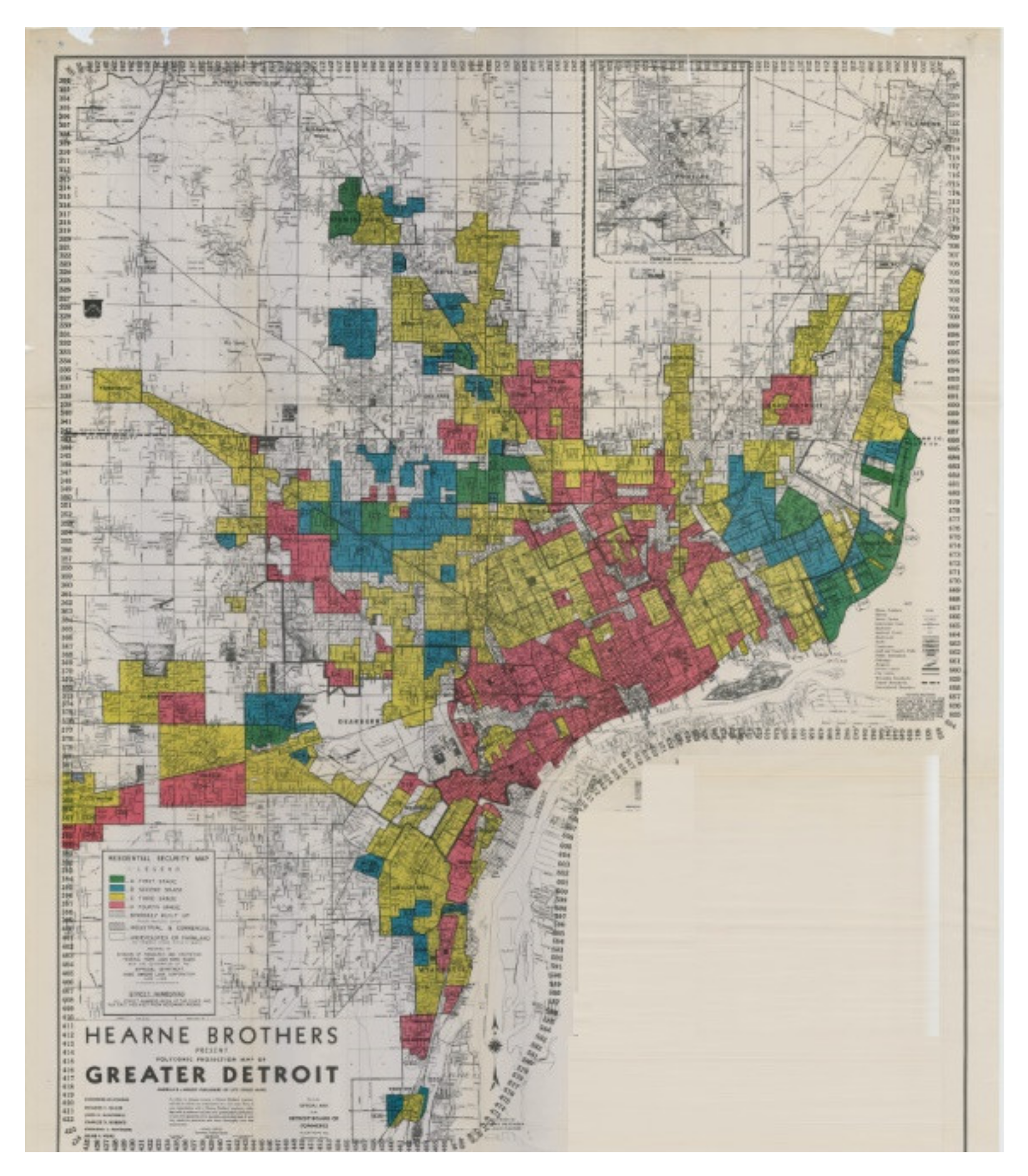

- Best (green).

- Desirable (blue).

- Declining (yellow).

- Hazardous (red).

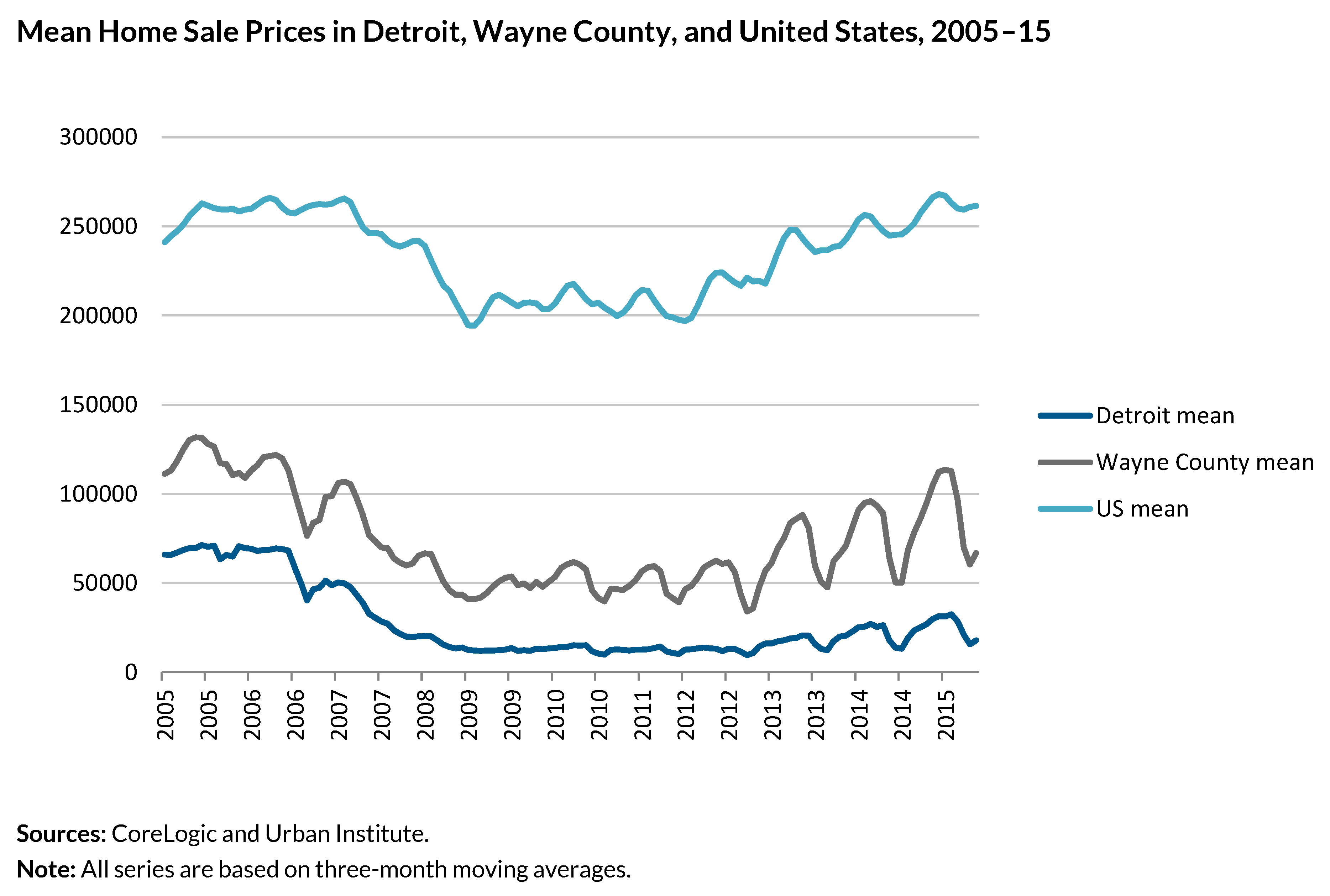

“…Making mortgages in Detroit is a convoluted task. The dearth of credit is largely a consequence of battered property values plus a commercial reality that depresses them further: Lenders can’t earn money on tiny mortgages, so they don’t make them.”.[11]

2. Materials and Methods

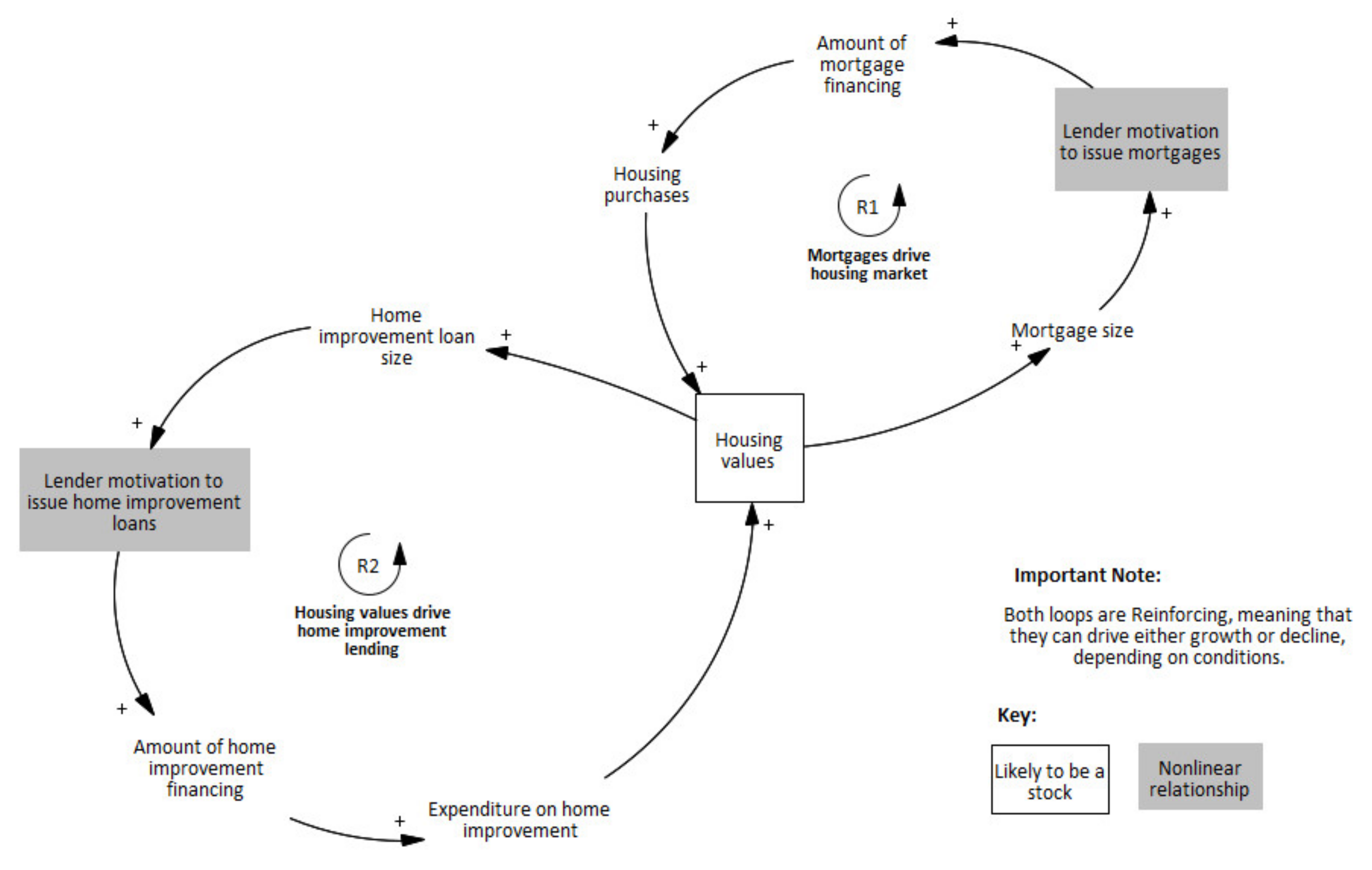

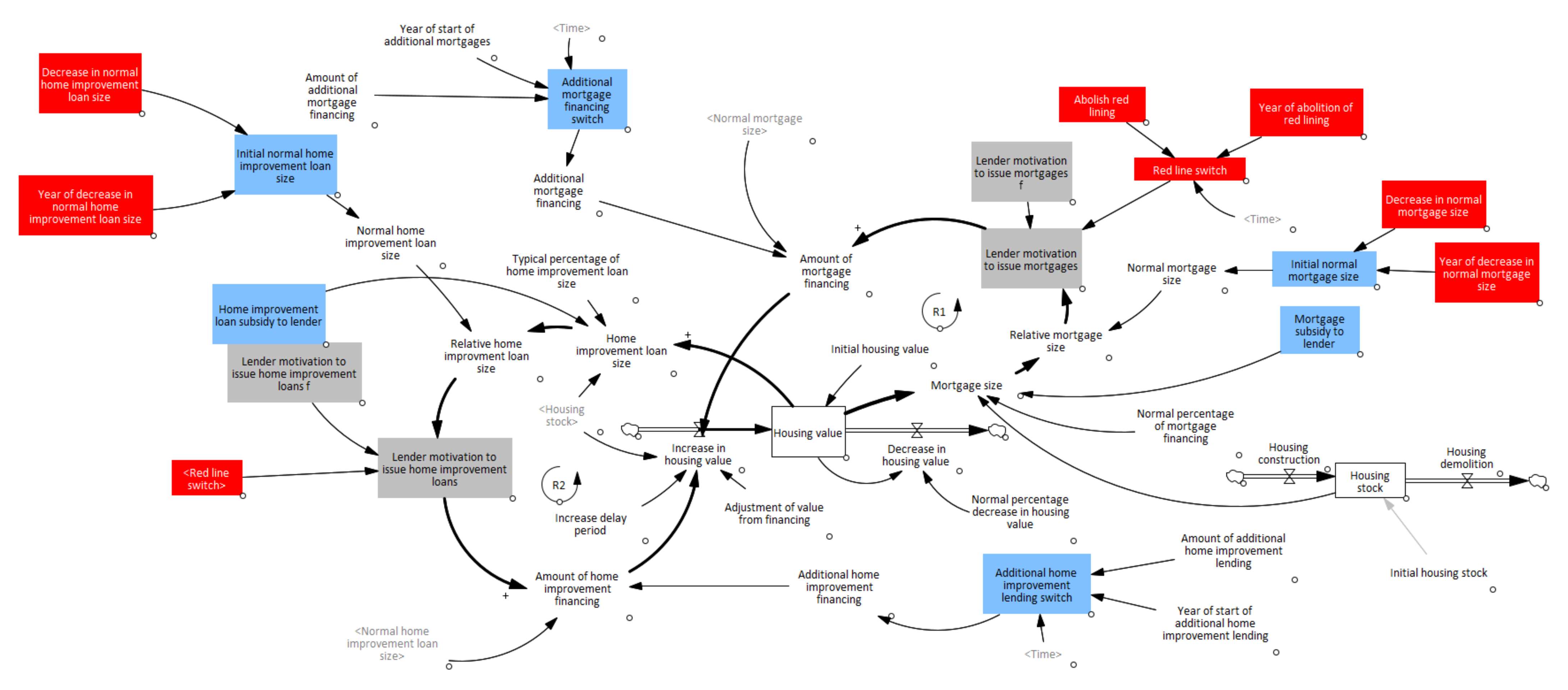

2.1. Dynamic Hypothesis

2.2. Stock and Flow Model

3. Results

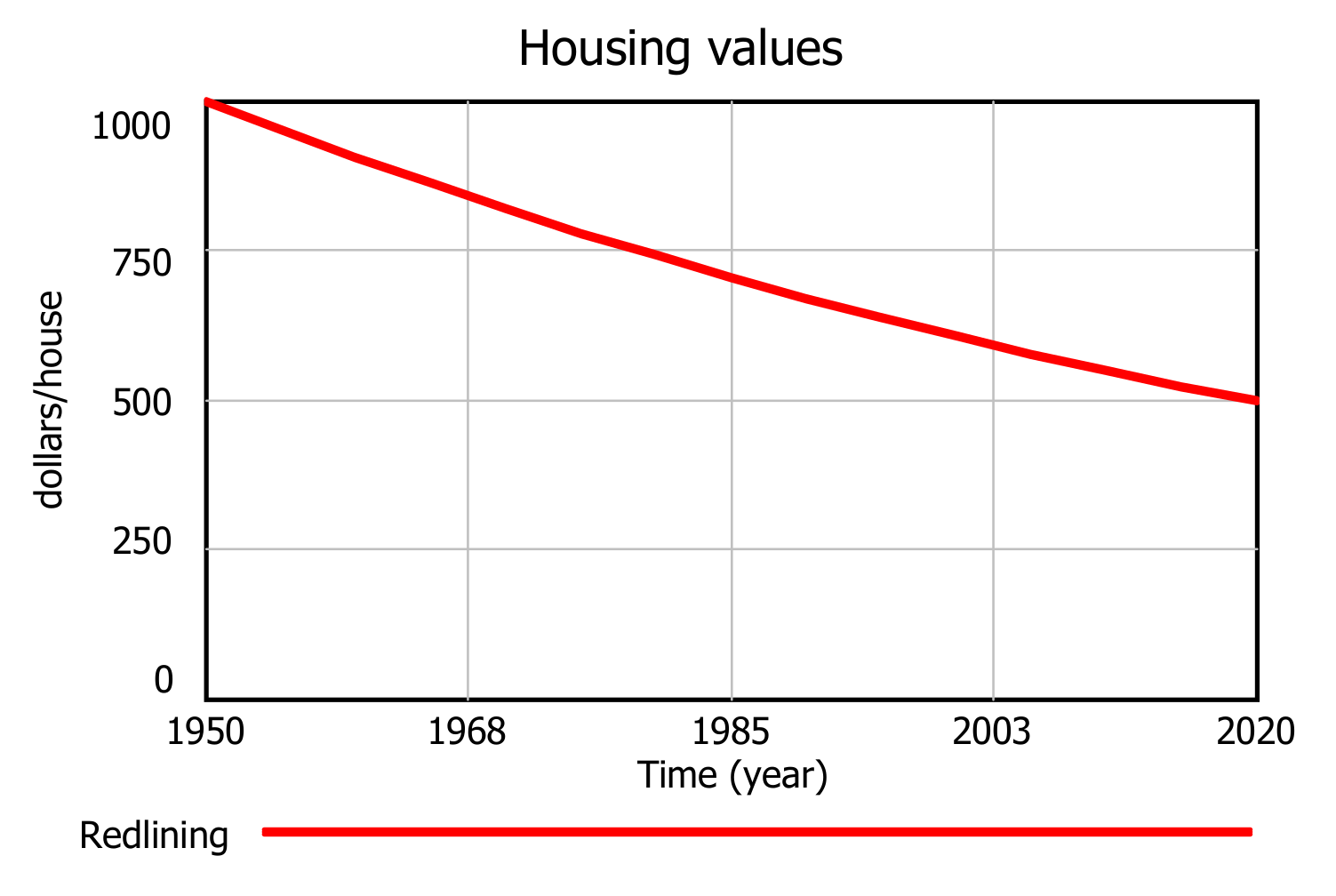

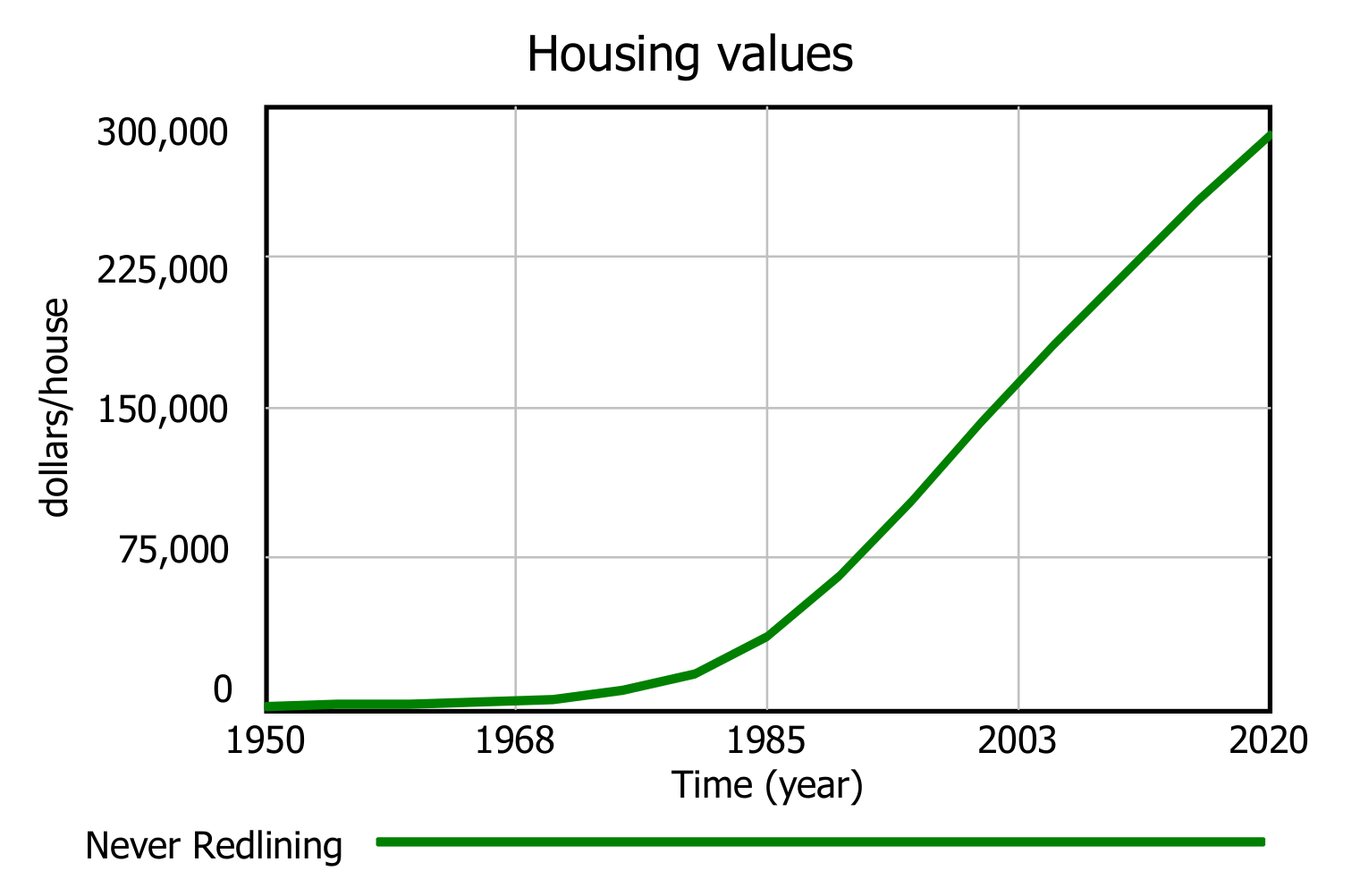

3.1. Model Test: Redlining for Entire Period (or No Redlining Ever)

Model Validation

3.2. Policy Experiments

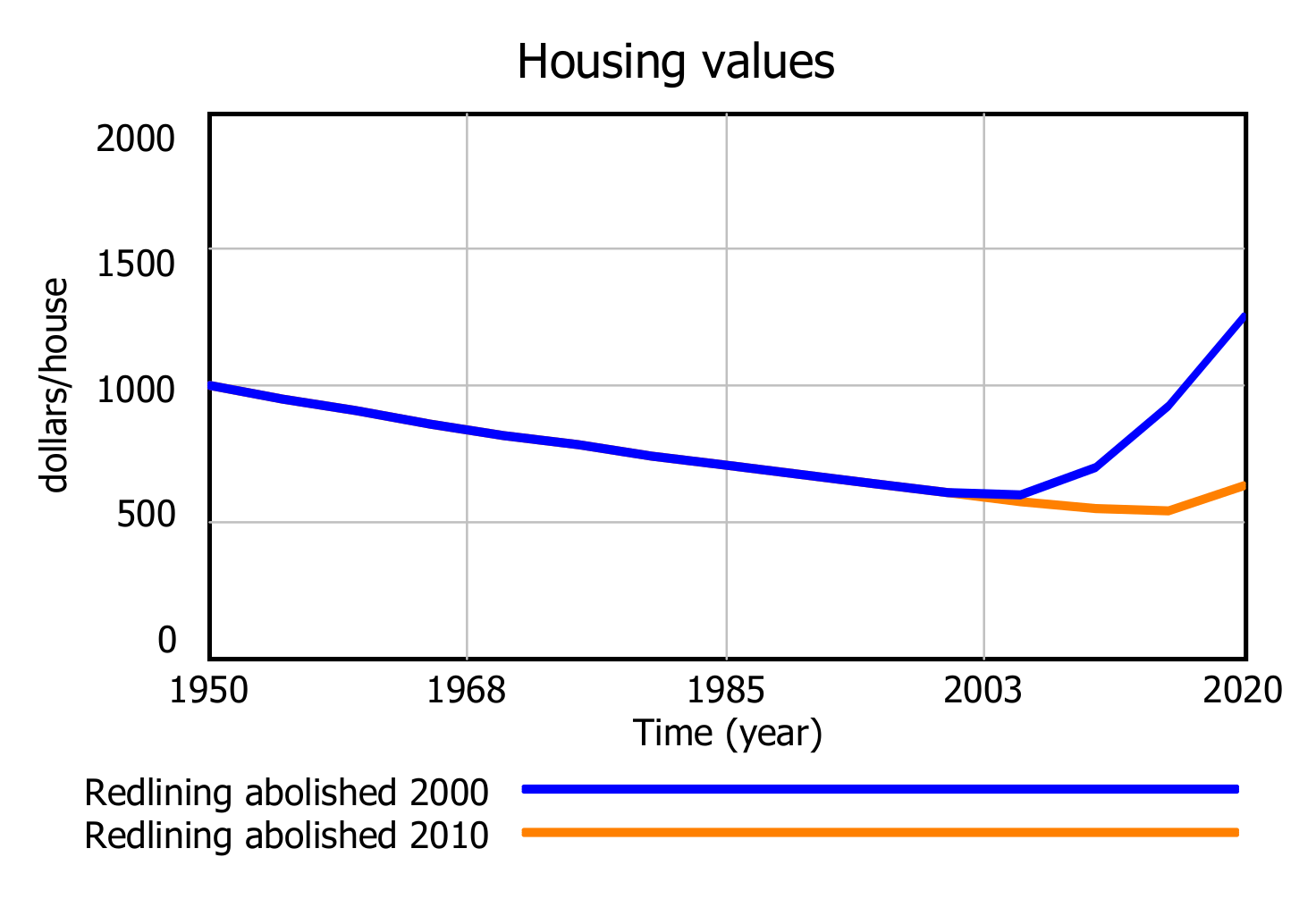

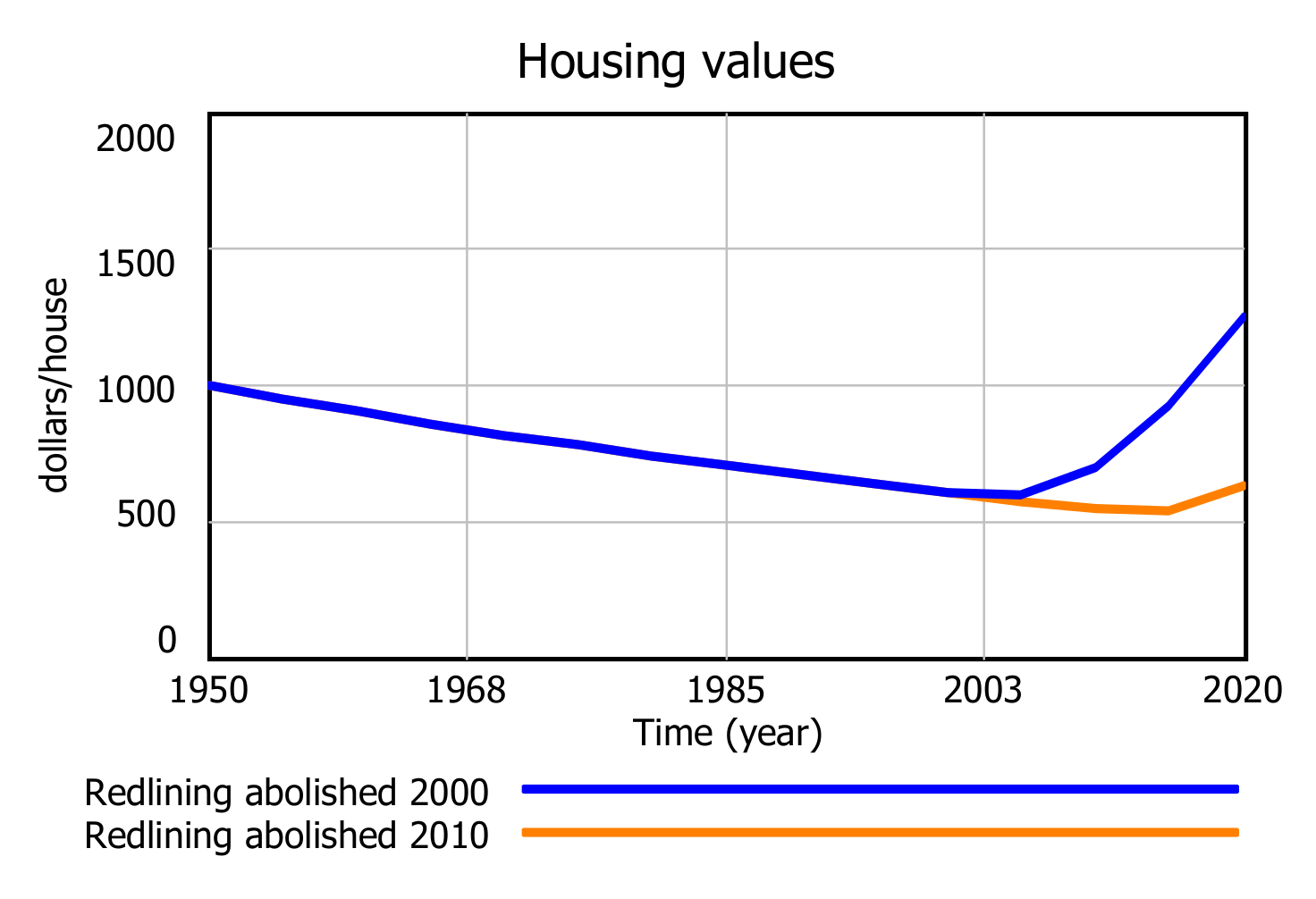

3.2.1. Scenario 1: Redlining Abolished Late in Period

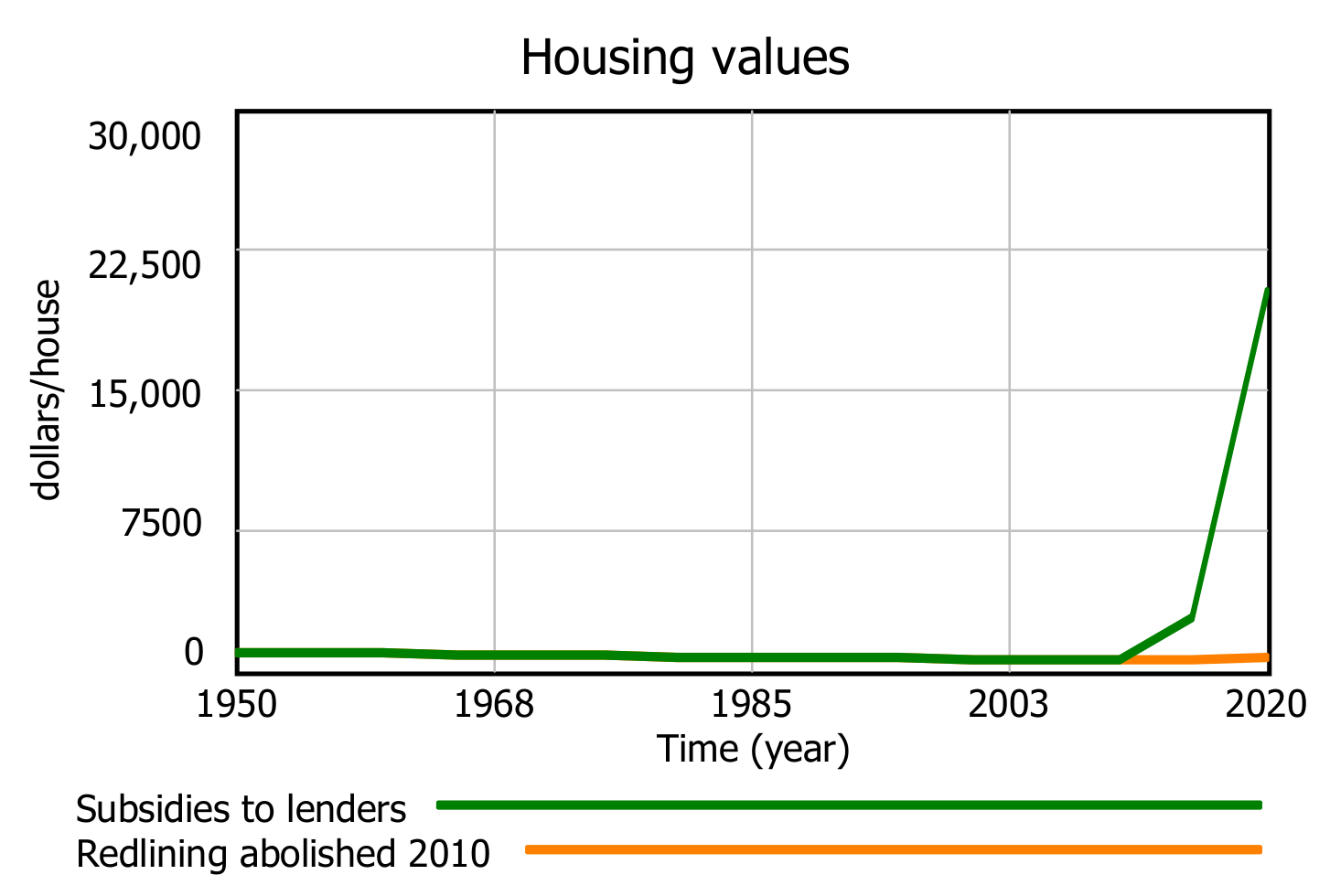

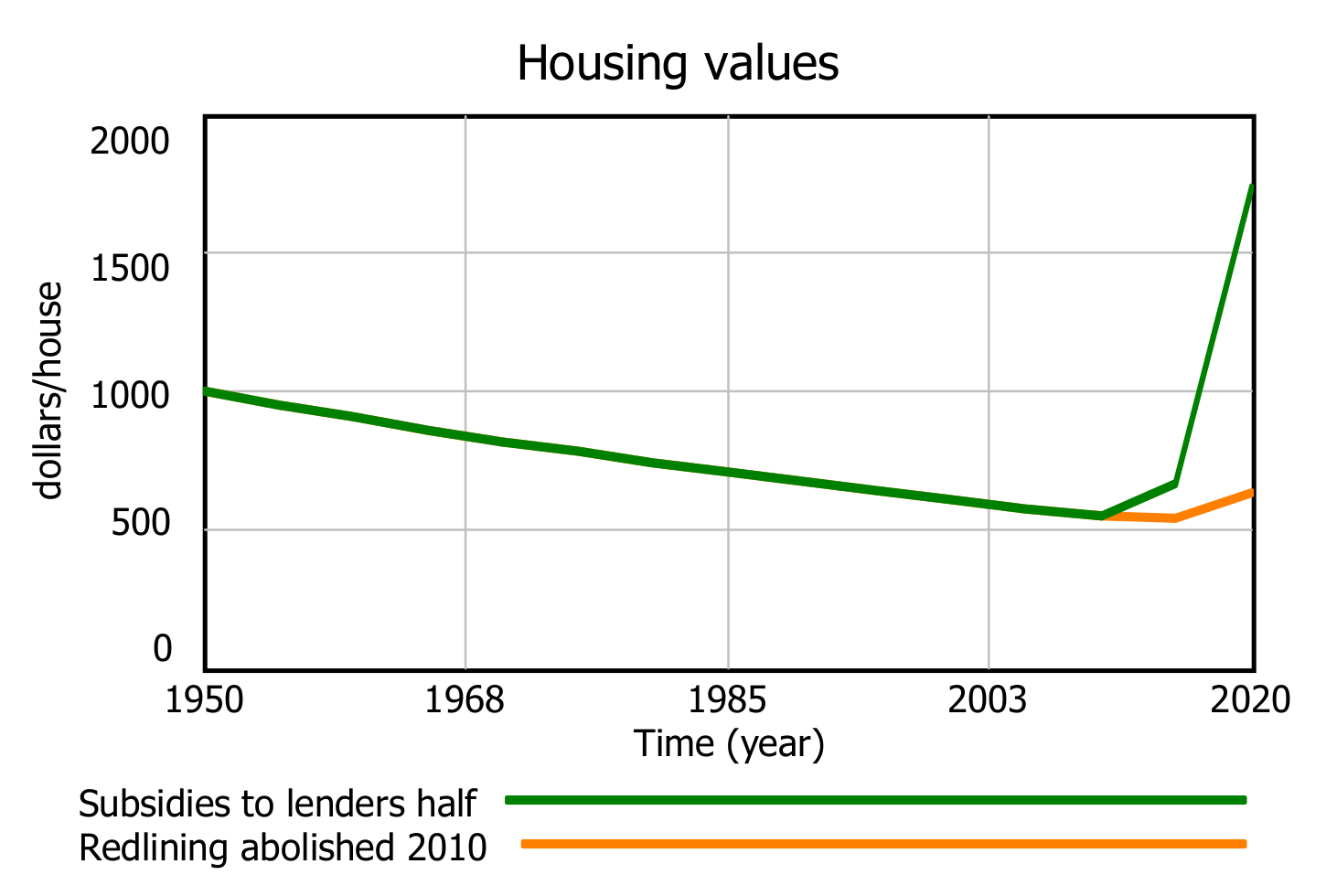

3.2.2. Scenario 2: Subsidizing Lenders

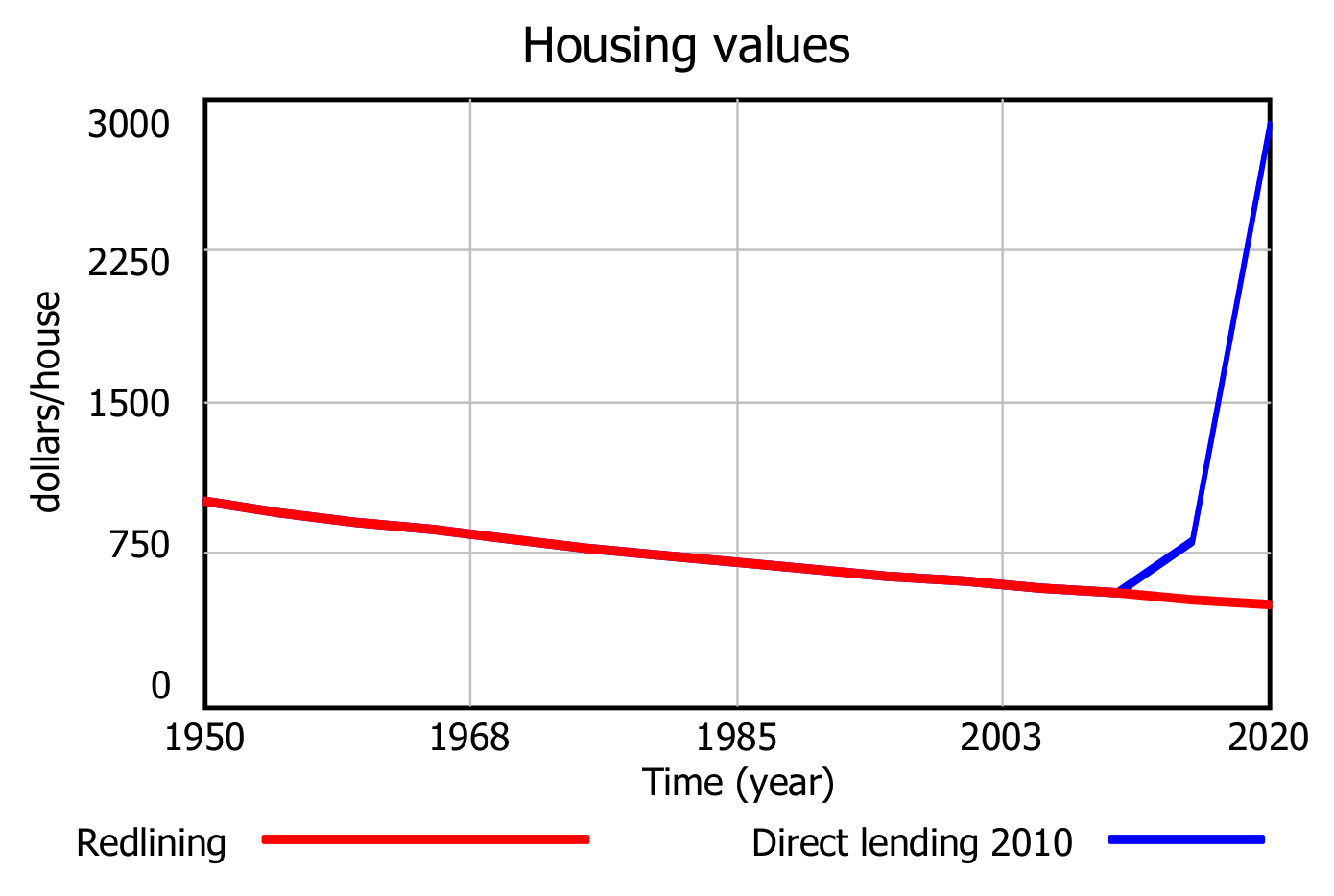

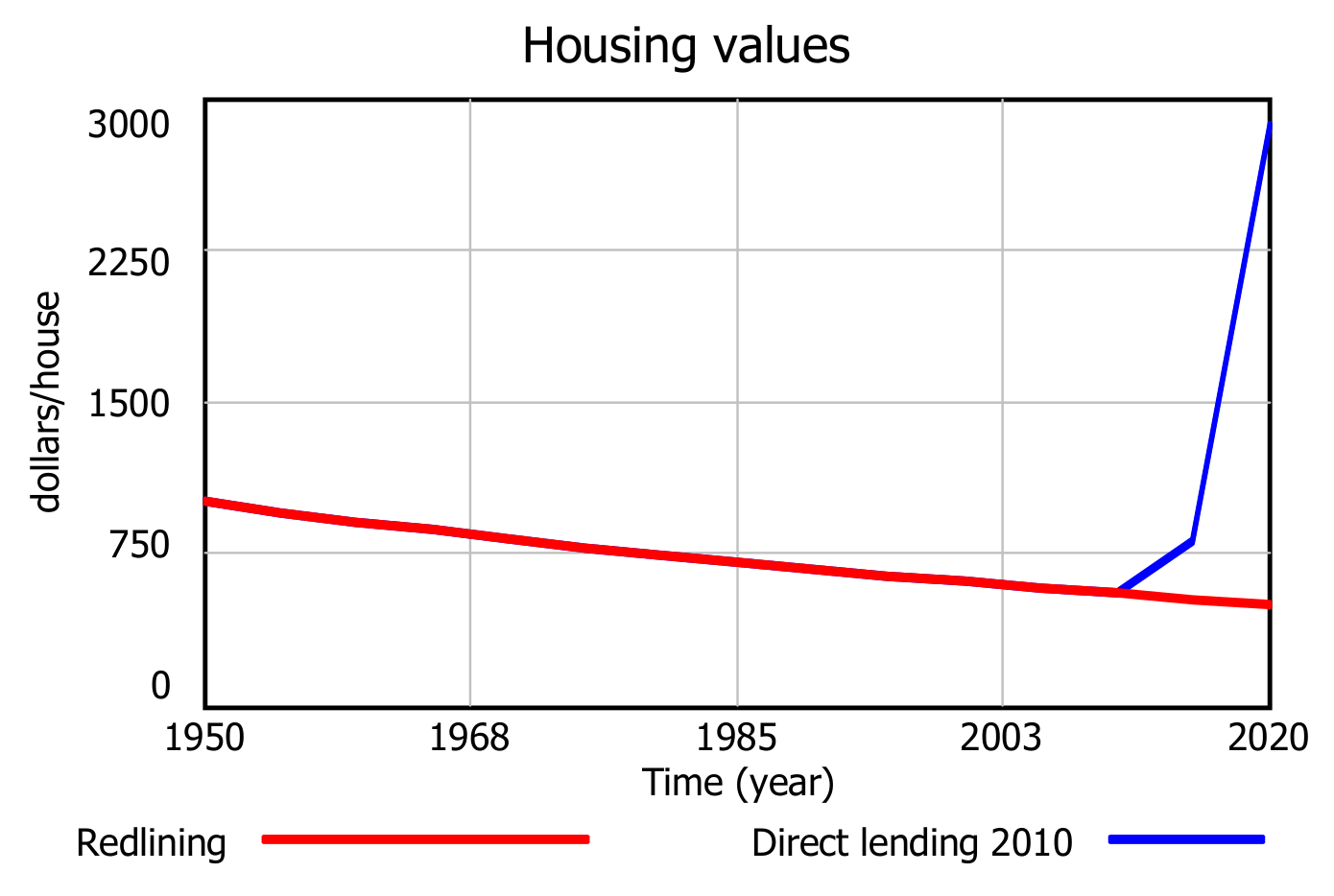

3.2.3. Scenario 3: Direct Lending from Government or Nonprofits

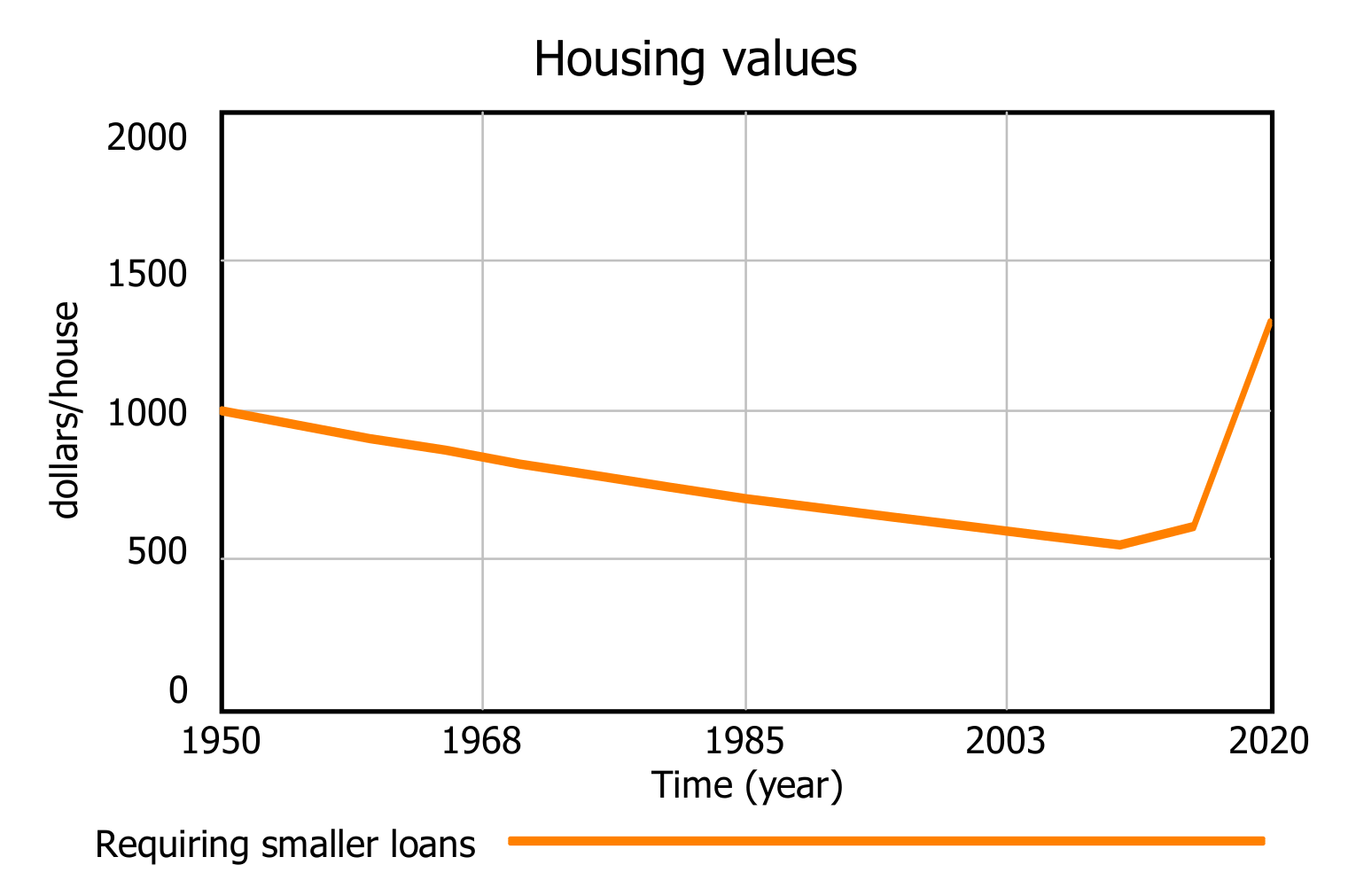

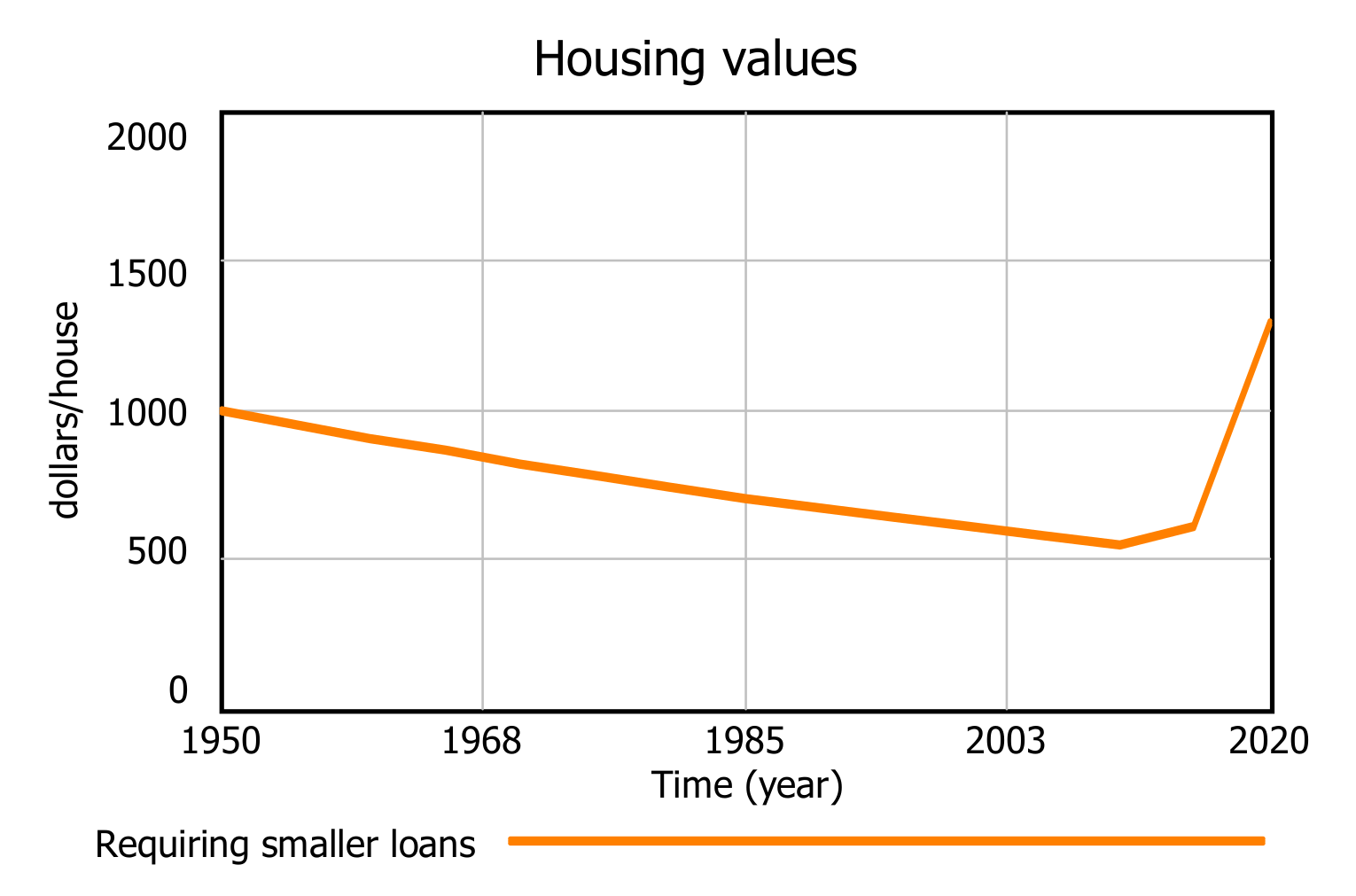

3.2.4. Scenario 4: Requiring Lenders to Make Smaller Loans

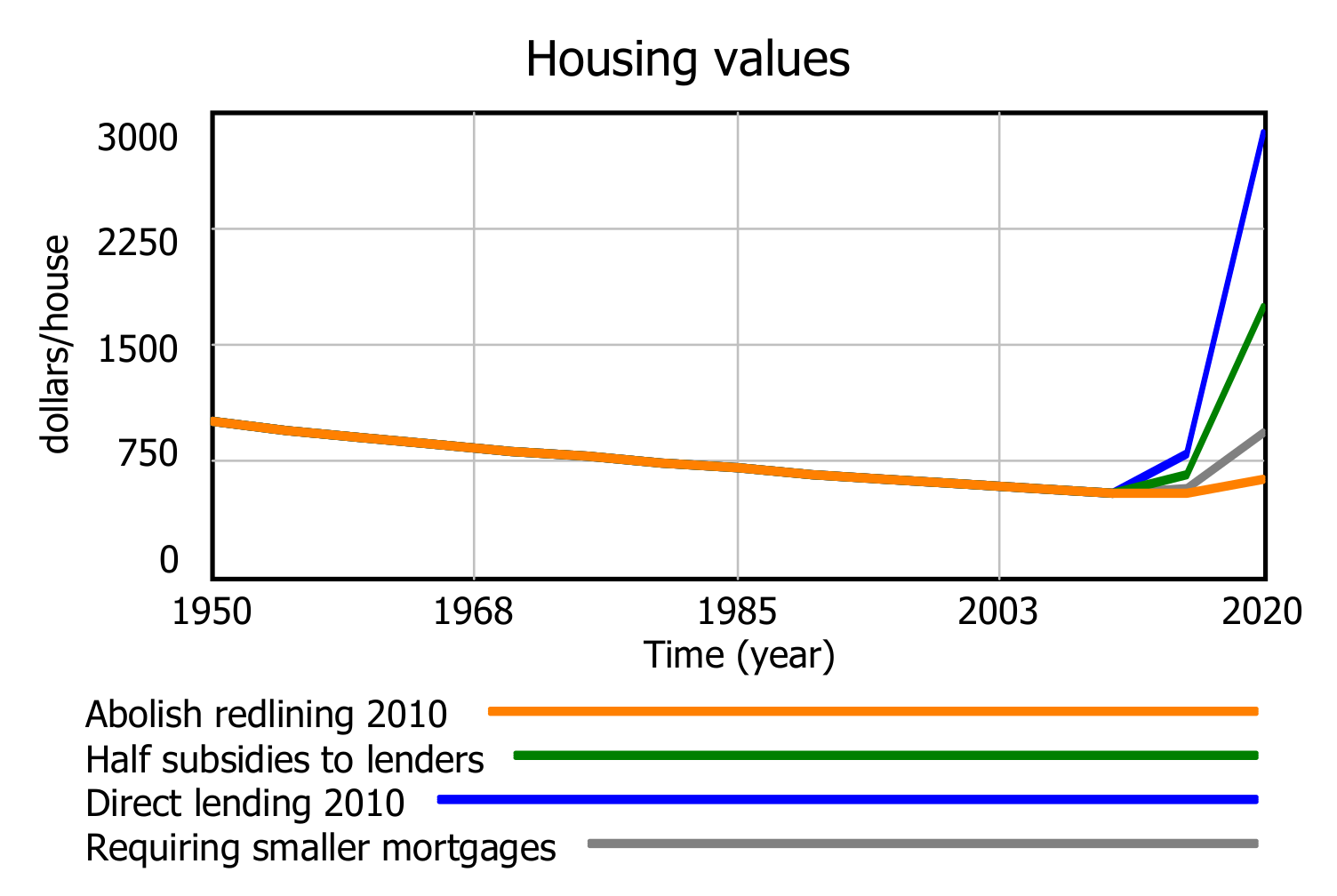

3.2.5. Comparison of Policies

4. Discussion

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. The Model in Text Form

| Normal home improvement loan size = initial normal home improvement loan size |

| Units: dollars/house |

| Decrease in normal home improvement loan size = 2250 |

| Units: dollars/house |

| Initial normal home improvement loan size = 2500-STEP (decrease in normal home improvement loan size; year of decrease in normal home improvement loan size) |

| Units: dollars/house |

| Year of decrease in normal home improvement loan size = 2021 |

| Units: year |

| Initial normal mortgage size = 10,000-STEP (decrease in normal mortgage size; year of decrease in normal mortgage size) |

| Units: dollars/house |

| Year of decrease in normal mortgage size = 2021 |

| Units: year |

| Decrease in normal mortgage size = 9500 |

| Units: dollars/house |

| Normal mortgage size = initial normal mortgage size |

| Units: dollars/house |

| Mortgage size = (housing value * normal percentage of mortgage financing) + mortgage subsidy to lender |

| Units: dollars/house |

| Home improvement loan size = (typical percentage of home improvement loan size * housing value) + home improvement loan subsidy to lender |

| Units: dollars/house |

| Home improvement loan subsidy to lender = 0 |

| Units: dollars/house |

| Relative home improvement loan size = home improvement loan size/normal home improvement loan size |

| Units: dimensionless |

| Mortgage subsidy to lender = 0 |

| Units: dollars/house |

| Year of start of additional mortgages = 2021 |

| Units: year |

| Additional home improvement financing = 0 + additional home improvement lending switch |

| Units: dollars/house |

| Additional home improvement lending switch = IF THEN ELSE (time < year of start of additional home improvement lending, 0—amount of additional home improvement lending) |

| Units: dollars/house |

| Additional mortgage financing = additional mortgage financing switch |

| Units: dollars/house |

| Additional mortgage financing switch = IF THEN ELSE (time < year of start of additional mortgages, 0—amount of additional mortgage financing) |

| Units: dollars/house |

| Amount of mortgage financing = (normal mortgage size * lender motivation to issue mortgages) + additional mortgage financing |

| Units: dollars/house |

| Amount of additional home improvement lending = 0 |

| Units: dollars/house |

| Amount of additional mortgage financing = 0 |

| Units: dollars/house |

| Amount of home improvement financing = (normal home improvement loan size * lender motivation to issue home-improvement loans) + additional home improvement financing |

| Units: dollars/house |

| Increase in housing value = DELAY3 ((amount of home improvement financing + amount of mortgage financing) * adjustment of value from financing, increased delay period) |

| Units: dollars/house/year |

| Increase delay period = 10 |

| Units: year |

| Year of start of additional home improvement lending = 2021 |

| Units: year |

| Abolish redlining = 1 |

| Units: dimensionless |

| Comment: Setting this to 1 makes redlining illegal. |

| Lender motivation to issue home-improvement loans = lender motivation to issue home-improvement loans f(relative home improvement loan size) * redline switch |

| Units: dimensionless |

| Lender motivation to issue mortgages = lender motivation to issue mortgages f(relative mortgage size) * redline switch |

| Units: dimensionless |

| Normal percentage of mortgage financing = 0.8 |

| Units: dimensionless |

| Red line switch = IF THEN ELSE (time < year of abolition of redlining, 0—abolish redlining) |

| Units: dimensionless |

| Comment: set to zero to implement “red line” lending policy. This zeroes out the motivation to lend. |

| Year of abolition of redlining = 2021 |

| Units: year |

| Adjustment of value from financing = 0.75 |

| Units: dimensionless/year |

| Units: financing does not increase value one-for-one. This makes an arbitrary adjustment. |

| Normal percentage decrease in housing value = 0.01 |

| Units: dimensionless/year |

| Decrease in housing value = housing value * normal percentage decrease in housing value |

| Units: dollars/(year * house) |

| Typical percentage of home improvement loan size = 0.8 |

| Units: dimensionless |

| Housing value = INTEG (increase in housing value—decrease in housing value; initial housing value) |

| Units: dollars/house |

| Lender motivation to issue home-improvement loans f([(0, 0)–(1, 1)], (0, 0), (0.5, 0.05), (0.8, 0.1), (1, 1)) |

| Units: dimensionless |

| Comment: ascending non-linear function; as loan size increases, motivation to lend increases. |

| Lender motivation to issue mortgages f([(0, 0)–(1, 1)], (0, 0), (0.5, 0.05), (0.8, 0.1), (1, 1)) |

| Units: dimensionless |

| Comment: ascending non-linear function; as loan size increases, motivation to lend increases. |

| Relative mortgage size = mortgage size/normal mortgage size |

| Units: dimensionless |

| Initial housing value = 1000 |

| Units: dollars/house |

| ******************************************************** |

| Control |

| ******************************************************** |

| Units: simulation control parameters |

| FINAL TIME = 2020 |

| Units: year |

| Units: the final time for the simulation. |

| INITIAL TIME = 1950 |

| Units: year |

| Units: the initial time for the simulation. |

| SAVEPER = 5 |

| Units: year |

| Units: the frequency with which output is stored. |

| TIME STEP = 0.25 |

| Units: year |

| Units: the time step for the simulation. |

References

- Voyer, J. Housing finance: A vestige of systemic racism? In Proceedings of the 39th International Conference of the System Dynamics Society, Chicago, IL, USA, 25–29 July 2021. [Google Scholar]

- National Archives of the United States. Records of the Home Owners’ Loan Corporation (HOLC), 1933–1951. Available online: https://www.archives.gov/research/guide-fed-records/groups/195.html#195.3 (accessed on 13 March 2021).

- Department of Housing and Urban Development. History of Fair Housing. 2021. Available online: https://www.hud.gov/program_offices/fair_housing_equal_opp/aboutfheo/history (accessed on 13 March 2021).

- Jan, T. Redlining was banned 50 years ago. It’s still hurting minorities today. The Washington Post. 28 March 2018. Available online: https://www.washingtonpost.com/news/wonk/wp/2018/03/28/redlining-was-banned-50-years-ago-its-still-hurting-minorities-today/ (accessed on 13 March 2021).

- McClure, L. Map: Redlining and Health in Detroit. DETROITography, 2008. Available online: https://detroitography.com/2020/02/17/map-redlining-and-health-in-detroit-2008/ (accessed on 13 March 2021).

- Mehdipanah, R.; Bess, K.; Tomkowiak, S.; Richardson, A.; Stokes, C.; White Perkins, D.; Cleage, S.; Israel, B.A.; Schulz, A.J. Residential Racial and Socioeconomic Segregation as Predictors of Housing Discrimination in Detroit Metropolitan Area. Sustainability 2020, 12, 10429. [Google Scholar] [CrossRef]

- McClure, E.; Feinstein, L.; Cordoba, E.; Douglas, C.; Emch, M.; Robinson, W.; Galea, S.; Aiello, A.E. The legacy of redlining in the effect of foreclosures on Detroit residents’ self-rated health. Health Place 2019, 55, 9–19. [Google Scholar] [CrossRef] [PubMed]

- Mitchell, B.; Franco, J. HOLC “Redlining” Maps: The Persistent Structure of Segregation and Economic Inequality. Report of National Community Reinvestment Coalition. 2018. Available online: https://ncrc.org/holc/ (accessed on 13 March 2021).

- Nardone, A.; Chiang, J.; Corburn, J. Historic Redlining and Urban Health Today in U.S. Cities. Environ. Justice 2020, 13, 109–119. [Google Scholar] [CrossRef]

- Silverman, R.M. Redlining in a Majority Black City? Mortgage Lending and the Racial Composition of Detroit Neighborhoods. West. J. Black Stud. 2005, 29, 531–541. [Google Scholar]

- Hill, A.B. Detroit Redlining Map, 1939. DETROITography, 2014. Available online: https://detroitography.com/2014/12/10/detroit-redlining-map-1939/ (accessed on 13 March 2021).

- Eisen, B. Dearth of Credit Starves Detroit’s Housing Market. Wall Street Journal. 29 October 2020. Available online: https://library.umaine.edu/auth/EZproxy/test/authej.asp?url=https://search.proquest.com/newspapers/dearth-credit-starves-detroit-s-housing-market/docview/2455565459/se-2?accountid=8120 (accessed on 13 March 2021).

- Swanstrom, T. Market-savvy housing and community development policy: Grappling with the equity-efficiency trade-off. In Facing Segregation: Housing Policy Solutions for a Stronger Society; Metzger, M.W., Webber, H.S., Eds.; Oxford University Press: New York, NY, USA, 2019; pp. 173–196. [Google Scholar]

- Midgley, G.; Johnson, M.P.; Chichirau, G. What is community operational research? Eur. J. Oper. Res. 2018, 268, 771–783. [Google Scholar] [CrossRef]

- Johnson, M.P.; Midgley, G.; Chichirau, G. Emerging trends and new frontiers in community operational research. Eur. J. Oper. Res. 2018, 268, 1178–1191. [Google Scholar] [CrossRef]

- Poethig, E.C.; Schilling, J.; Goodman, L.; Bai, B.; Gastner, J.; Pendall, R.; Fazili, S. The Detroit Housing Market: Challenges and Innovations for a Path Forward. Urban Institute Research Report. 2017. Available online: https://www.urban.org/sites/default/files/publication/88656/detroit_path_forward_0.pdf (accessed on 9 February 2022).

- Coffin, S.L. Financing affordability: Tax increment financing and the potential for concentrated reinvestment. In Facing Segregation: Housing Policy Solutions for a Stronger Society; Metzger, M.W., Webber, H.S., Eds.; Oxford University Press: New York, NY, USA, 2019; pp. 197–214. [Google Scholar]

- Kang, H.H. Looking Toward Restorative Justice for Redlined Communities Displaced by Eco-Gentrification. Mich. J. Race Law 2021, 23, 26. [Google Scholar] [CrossRef]

- Reece, J. Confronting the Legacy of “Separate but Equal”: Can the History of Race, Real Estate, and Discrimination Engage and Inform Contemporary Policy? RSF Russell Sage Found. J. Soc. Sci. 2021, 7, 110–133. [Google Scholar] [CrossRef]

- McGrew, T. The History of Residential Segregation in the United States, Title VIII, and the Homeownership Remedy. Am. J. Econ. Sociol. 2018, 77, 1013–1048. [Google Scholar] [CrossRef]

- Bhutta, N.; Chang, A.C.; Lisa, J.; Dettling, L.J.; Hsu, J.W.; Hewitt, J. Disparities in Wealth by Race and Ethnicity in the 2019 Survey of Consumer Finances. FEDS Notes; 2020. Available online: https://www.federalreserve.gov/econres/notes/feds-notes/disparities-in-wealth-by-race-and-ethnicity-in-the-2019-survey-of-consumer-finances-20200928.htm (accessed on 17 March 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Scenario | 1: Redlining Abolished Late | 2: Half Subsidy to Lenders | 3: Direct Lending from Government or Nonprofits | 4: Requiring Smaller Loans |

|---|---|---|---|---|

| Year of abolition of redlining | 2000 and 2010 | 2010 | 2010 | 2010 |

| Half subsidy to lenders | 2010 | USD 2500 mortgage USD 1250 HI loan | 0 | 0 |

| Additional lending from government or nonprofit | 0 | 0 | USD 5000 mortgage USD 1250 HI loan | 0 |

| Decrease in normal loan size | 0 | 0 | 0 | USD 9500 mortgage USD 1250 HI loan |

| Scenario | 1: Redlining Abolished Late | 2: Half Subsidy to Lenders Starting in 2010 | 3: Direct Lending from Government or Nonprofits Starting in 2010 | 4: Requiring Smaller Loans Starting in 2010 |

|---|---|---|---|---|

| Financial costs | None | USD 2500 mortgage subsidy; USD 1250 home improvement loan subsidy; cost of administering subsidy program | USD 5000 mortgage; USD 1250 HI loan; cost of administering lending program; cost of creating nonprofit organizations | Bank losses on loans—about USD 9000 on mortgages, about USD 3500 on home-improvement loans |

| Financial benefits | Modest increase in housing values | Increase in housing value up to USD 1750 in ten years; banks remain profitable | Government and nonprofits gain from loan repayments; housing value increased sixfold in ten years to almost USD 3000 | Increase in housing value almost triples—from roughly USD 500 up to USD 1250 in ten years |

| Social costs | Late abolition delays full participation in housing market | Higher taxes to fund subsidies | Intrusion of governments or nonprofits into fabric of neighborhoods | Bank management resentment of government mandates |

| Social benefits | Residents of formerly redlined areas participate fully in housing market; neighborhoods improve physically and civically | Residents of formerly redlined areas participate fully in housing market; neighborhoods improve physically and civically | Residents of formerly redlined areas participate fully in housing market; neighborhoods improve physically and civically | Residents of formerly redlined areas participate fully in housing market; neighborhoods improve physically and civically |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Voyer, J.J. A Systemic Analysis of Vestigial Racism in Housing Finance. Systems 2022, 10, 48. https://doi.org/10.3390/systems10020048

Voyer JJ. A Systemic Analysis of Vestigial Racism in Housing Finance. Systems. 2022; 10(2):48. https://doi.org/10.3390/systems10020048

Chicago/Turabian StyleVoyer, John J. 2022. "A Systemic Analysis of Vestigial Racism in Housing Finance" Systems 10, no. 2: 48. https://doi.org/10.3390/systems10020048

APA StyleVoyer, J. J. (2022). A Systemic Analysis of Vestigial Racism in Housing Finance. Systems, 10(2), 48. https://doi.org/10.3390/systems10020048