Measuring Bank Systemic Risk in China: A Network Model Analysis

Abstract

:1. Introduction

2. The Measurement Model of Bank Systemic Risk

2.1. The Construction of an Inter-Bank Asset Liability Network

2.2. Inter-Bank Risk Contagion Mechanism

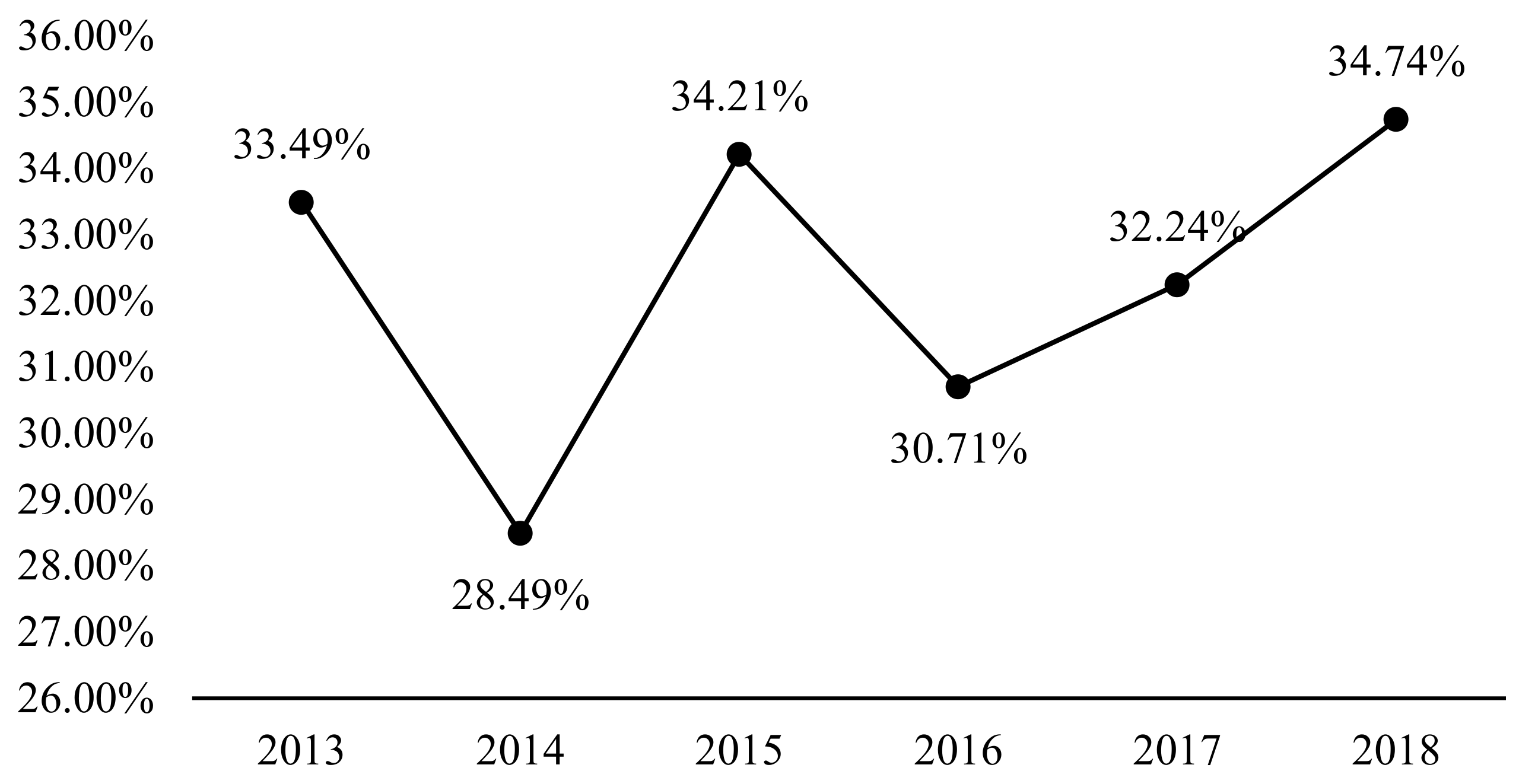

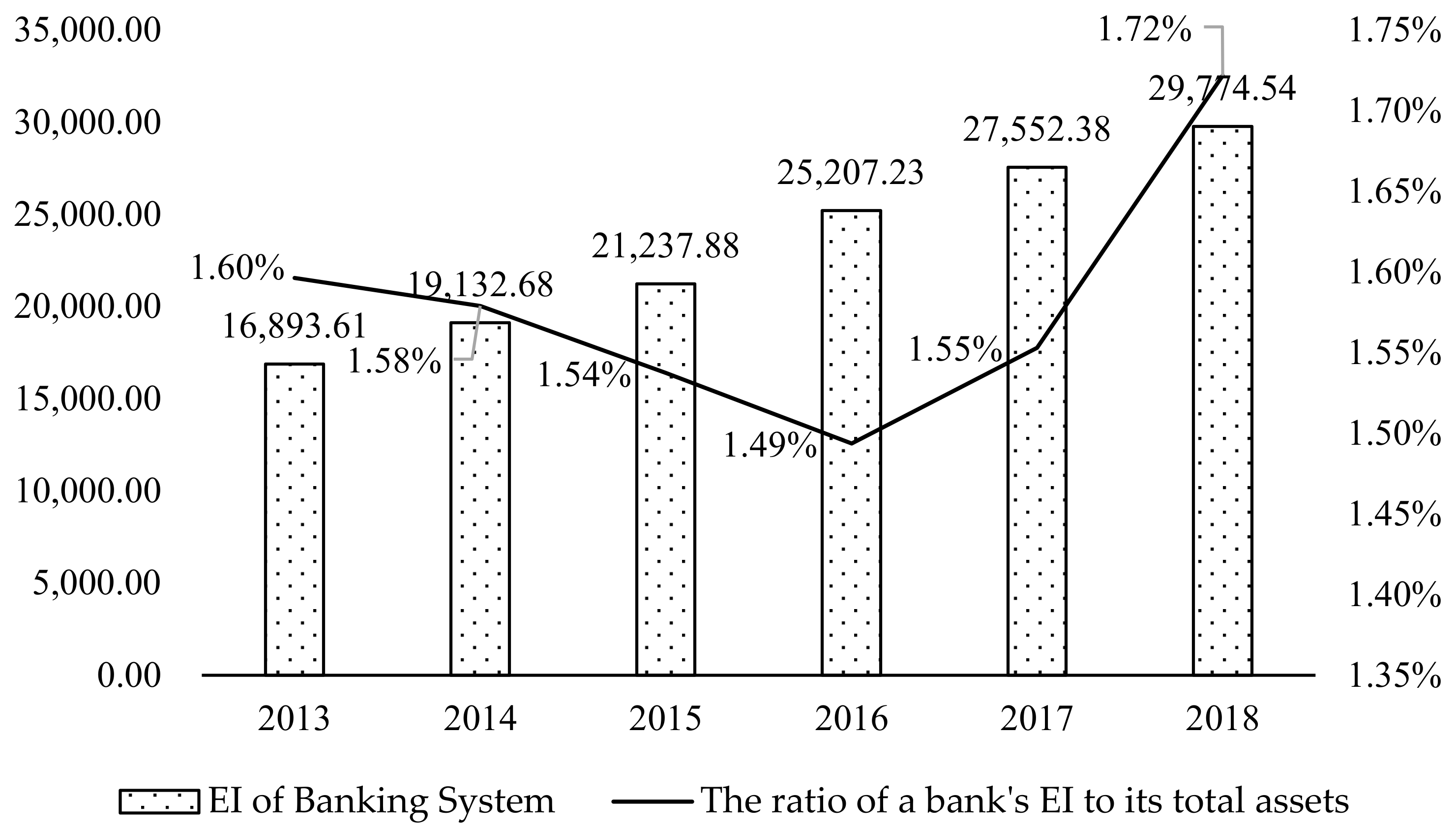

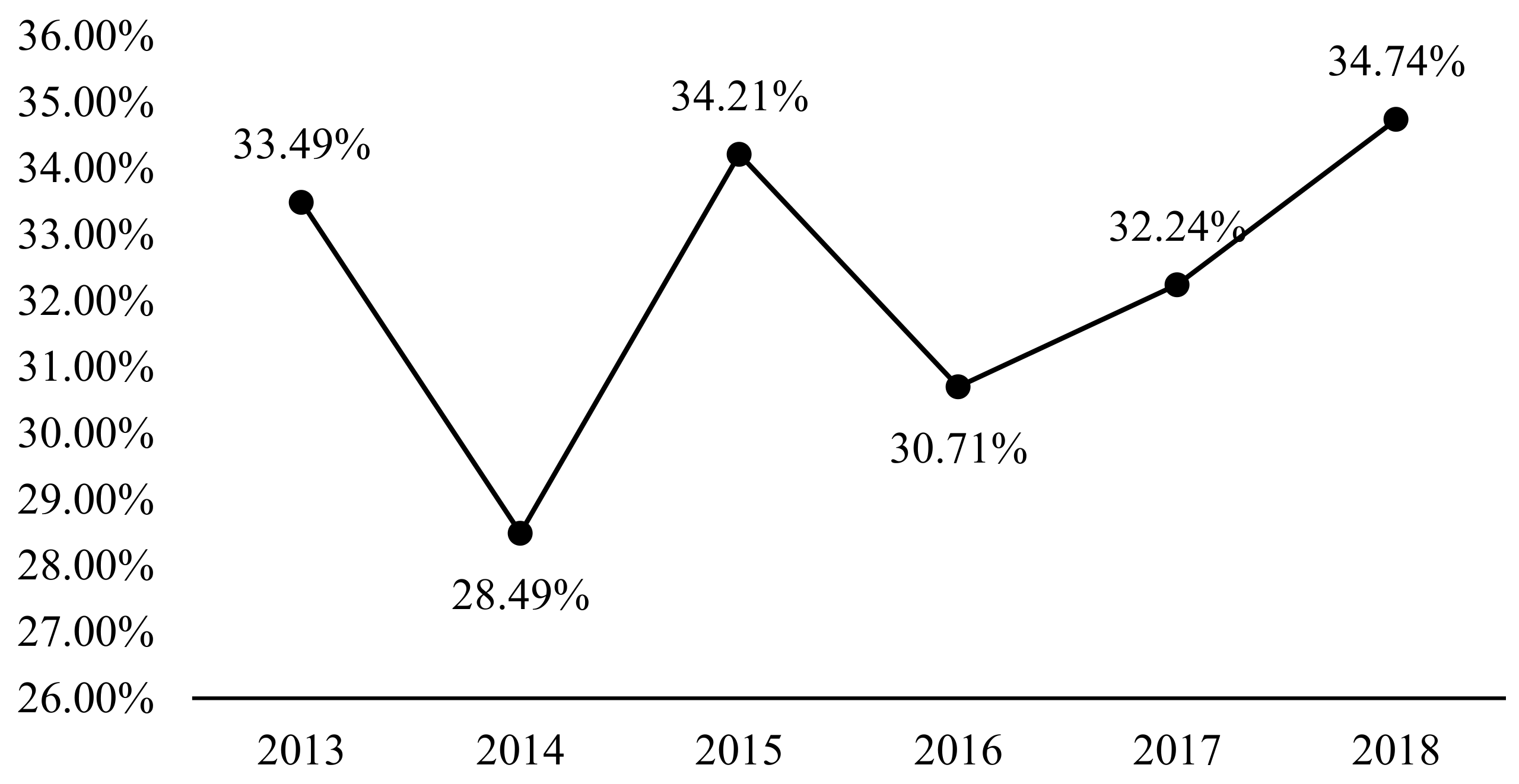

3. Bank Systemic Risk Simulation

4. Further Discussion

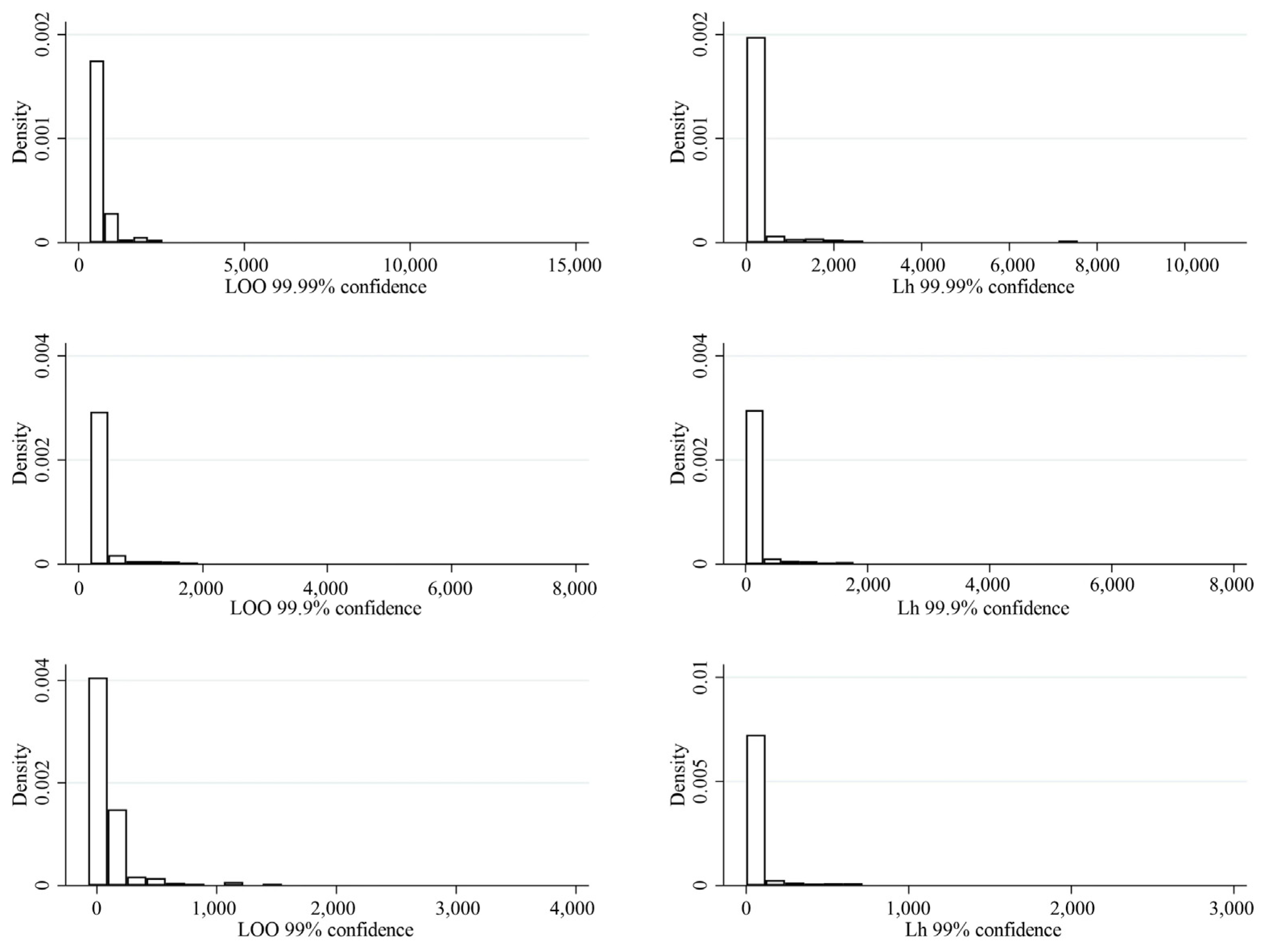

4.1. Robustness Check

4.2. Banking Systemic Risk Influencing Factors: The Supervision of Shadow Banking

5. Conclusions

- (1)

- In China’s banking system, contagion risk has become a key component of potential financial risk. In addition to managing individual bank risks from a micro-prudential perspective, we must also consider the impact of contagion across the banking system from a macro-prudential perspective. Furthermore, a bank’s asset–liability ratio shows a strong correlation with its contagious risk. It consequently suggests that China should track the inter-bank market capital transactions in real time in order to detect hidden risks and prevent the spread of contagious risks, thereby reducing the systemic financial risks of the banking industry and enhancing economic stability.

- (2)

- The results show that the contribution of different types of banks to systemic financial risk varies. Thus, it is a good idea to focus on classified banking supervision. Additionally, China should adopt flexible regulations for different types of banks to address different types of potential systematic risks, in particular paying more attention to small- and medium-sized banks, such as city commercial banks. In spite of the fact that these banking mechanisms are relatively flexible and provide a potential for financial innovation, they fail to address financial risks effectively, resulting in systemic risks. It is important for supervisors to ensure proper internal controls and to standardize business operations, to keep them from over-relying upon inter-bank market positions, and to provide liquidity during times of crisis.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Bank Name | Bank Type | No. | Bank Name | Bank Type |

|---|---|---|---|---|---|

| 1 | Bank of Shanghai | City commercial bank | 80 | Dazhou Bank | City commercial bank |

| 2 | Bank of Dongguan | City commercial bank | 81 | Bank of Zhengzhou | City commercial bank |

| 3 | Dongying Bank | City commercial bank | 82 | Chongqing Three Gorges Bank | City commercial bank |

| 4 | Zhongyuan Bank | City commercial bank | 83 | Bank of Chongqing | City commercial bank |

| 5 | Linshang Bank | City commercial bank | 84 | Jinhua Bank | City commercial bank |

| 6 | Leshan City Commercial Bank | City commercial bank | 85 | Bank of Jinzhou | City commercial bank |

| 7 | Jiujiang Bank | City commercial bank | 86 | Great Wall West China Bank | City commercial bank |

| 8 | Bank of Lanzhou | City commercial bank | 87 | Chang’an Bank | City commercial bank |

| 9 | Bank of Inner Mongolia | City commercial bank | 88 | Bank of Changsha | City commercial bank |

| 10 | Bao Shang Bank | City commercial bank | 89 | Fuxin Bank | City commercial bank |

| 11 | Bank of Beijing | City commercial bank | 90 | Bank of Qingdao | City commercial bank |

| 12 | Huarong Xiangjiang Bank | City commercial bank | 91 | Anshan Bank | City commercial bank |

| 13 | Bank of Nanjing | City commercial bank | 92 | Qi Shang Bank | City commercial bank |

| 14 | Xiamen International Bank | City commercial bank | 93 | Qilu Bank | City commercial bank |

| 15 | Bank of Xiamen | City commercial bank | 94 | Longjiang Bank | City commercial bank |

| 16 | Bank of Taizhou | City commercial bank | 95 | Citic Bank | Joint-stock commercial bank |

| 17 | Bank of Jilin | City commercial bank | 96 | China Minsheng Bank | Joint-stock commercial bank |

| 18 | Bank of Harbin | City commercial bank | 97 | Jiaozuo China Tourism Bank | Joint-stock commercial bank |

| 19 | Tangshan Bank | City commercial bank | 98 | Everbright Bank | Joint-stock commercial bank |

| 20 | Bank of Jiaxing | City commercial bank | 99 | Industrial Bank | Joint-stock commercial bank |

| 21 | Sichuan Tianfu Bank | City commercial bank | 100 | Huaxia Bank | Joint-stock commercial bank |

| 22 | Datong Bank | City commercial bank | 101 | Ping An Bank | Joint-stock commercial bank |

| 23 | Bank of Dalian | City commercial bank | 102 | Guangfa Bank | Joint-stock commercial bank |

| 24 | Bank of Tianjin | City commercial bank | 103 | Hengfeng Bank | Joint-stock commercial bank |

| 25 | Weihai City Commercial Bank | City commercial bank | 104 | China Merchants Bank | Joint-stock commercial bank |

| 26 | Bank of Ningxia | City commercial bank | 105 | Zheshang Bank | Joint-stock commercial bank |

| 27 | Ningbo Tongshang Bank | City commercial bank | 106 | Bohai Bank | Joint-stock commercial bank |

| 28 | Bank of Ningbo | City commercial bank | 107 | Agricultural Bank of China | Large state-owned controlled commercial bank |

| 29 | Yibin City Commercial Bank | City commercial bank | 108 | Industrial and Commercial Bank of China | Large state-owned controlled commercial bank |

| 30 | Fudian Bank | City commercial bank | 109 | China Construction Bank | Large state-owned controlled commercial bank |

| 31 | Pingdingshan Bank | City commercial bank | 110 | Bank of China | Large state-owned controlled commercial bank |

| 32 | Guangdong Huaxing Bank | City commercial bank | 111 | Bank of Communications | Large state-owned controlled commercial bank |

| 33 | Bank of Guangzhou | City commercial bank | 112 | The Postal Savings Bank of China | Large state-owned controlled commercial bank |

| 34 | Guangxi Beibu Gulf Bank | City commercial bank | 113 | Cixi Rural Commercial Bank | Rural cooperative bank |

| 35 | Langfang Bank | City commercial bank | 114 | Wenling Rural Commercial Bank | Rural cooperative bank |

| 36 | Huishang Bank | City commercial bank | 115 | Shanghai Rural Commercial Bank | Rural commercial bank |

| 37 | Bank of Chengdu | City commercial bank | 116 | Dongguan Rural Commercial Bank | Rural commercial bank |

| 38 | Chengde Bank | City commercial bank | 117 | Zhongshan Rural Commercial Bank | Rural commercial bank |

| 39 | Fushun Bank | City commercial bank | 118 | Yiwu Rural Commercial Bank | Rural commercial bank |

| 40 | Panzhihua City Commercial Bank | City commercial bank | 119 | Yuhang Rural Commercial Bank | Rural commercial bank |

| 41 | Rizhao Bank | City commercial bank | 120 | Foshan Rural Commercial Bank | Rural commercial bank |

| 42 | Kunlun Bank | City commercial bank | 121 | Beijing Rural Commercial Bank | Rural commercial bank |

| 43 | Jinzhong Bank | City commercial bank | 122 | Nanxun Rural Commercial Bank | Rural commercial bank |

| 44 | Jin merchants bank | City commercial bank | 123 | Nanhai Rural Commercial Bank | Rural commercial bank |

| 45 | Jincheng Bank | City commercial bank | 124 | Hefei Science and Technology Rural Commercial Bank | Rural commercial bank |

| 46 | Qujing City Commercial Bank | City commercial bank | 125 | Dalian Rural Commercial Bank | Rural commercial bank |

| 47 | Bank of Hangzhou | City commercial bank | 126 | Tianjin Rural Commercial Bank | Rural commercial bank |

| 48 | Bank of Liuzhou | City commercial bank | 127 | Guangzhou Rural Commercial Bank | Rural commercial bank |

| 49 | Bank of Guilin | City commercial bank | 128 | Zhangjiagang Rural Commercial Bank | Rural commercial bank |

| 50 | Hankou Bank | City commercial bank | 129 | Chengdu Rural Commercial Bank | Rural commercial bank |

| 51 | Bank of Jiangsu | City commercial bank | 130 | Kunshan Rural Commercial Bank | Rural commercial bank |

| 52 | Bank of Jiangxi | City commercial bank | 131 | Hangzhou United Bank | Rural commercial bank |

| 53 | Cangzhou Bank | City commercial bank | 132 | Wuhan Rural Commercial Bank | Rural commercial bank |

| 54 | Bank of Hebei | City commercial bank | 133 | Jiangyin Bank | Rural commercial bank |

| 55 | Bank of Quanzhou | City commercial bank | 134 | Hai’an Rural Commercial Bank | Rural commercial bank |

| 56 | Tai’an Bank | City commercial bank | 135 | Zhuhai Rural Commercial Bank | Rural commercial bank |

| 57 | Bank of Luoyang | City commercial bank | 136 | Zijin Rural Commercial Bank | Rural commercial bank |

| 58 | Jining Bank | City commercial bank | 137 | Chongqing Rural Commercial Bank | Rural commercial bank |

| 59 | Zhejiang Mintai Commercial Bank | City commercial bank | 138 | Qingdao Rural Commercial Bank | Rural commercial bank |

| 60 | Zhejiang Tailong Commercial Bank | City commercial bank | 139 | Shunde Rural Commercial Bank | Rural commercial bank |

| 61 | Zhejiang Chouzhou Commercial Bank | City commercial bank | 140 | Gaoming Rural Commercial Bank | Rural commercial bank |

| 62 | Bank of Wenzhou | City commercial bank | 141 | Lucheng Rural Commercial Bank | Rural commercial bank |

| 63 | Bank of Hubei | City commercial bank | 142 | Zhaoqing Danzhou Rural Commercial Bank | Rural commercial bank |

| 64 | Bank of Huzhou | City commercial bank | 143 | Sumitomo Mitsui (China) | Foreign bank |

| 65 | Weifang Bank | City commercial bank | 144 | East Asia China | Foreign bank |

| 66 | Bank of Yantai | City commercial bank | 145 | Huashang Bank | Foreign bank |

| 67 | Zhuhai China Resources Bank | City commercial bank | 146 | Nanyang Commercial Bank (China) | Foreign bank |

| 68 | Bank of Gansu | City commercial bank | 147 | Youli (China) | Foreign bank |

| 69 | Shengjing Bank | City commercial bank | 148 | National (China) | Foreign bank |

| 70 | Fujian Strait Bank | City commercial bank | 149 | Fubonhua a bank | Foreign bank |

| 71 | Shaoxing Bank | City commercial bank | 150 | Morgan Stanley International Bank (China), Ltd. | Foreign bank |

| 72 | Bank of Suzhou | City commercial bank | 151 | JPMorgan Chase Bank (China) | Foreign bank |

| 73 | Commercial Bank | City commercial bank | 152 | New Korea China | Foreign bank |

| 74 | Yingkou Bank | City commercial bank | 153 | Star Show China | Foreign bank |

| 75 | Huludao Bank | City commercial bank | 154 | HSBC China | Foreign bank |

| 76 | Hengshui Bank | City commercial bank | 155 | Standard Chartered China | Foreign bank |

| 77 | Bank of Xi’an | City commercial bank | 156 | Australia New (China) | Foreign bank |

| 78 | Bank of Guizhou | City commercial bank | 157 | Ruizang Bank | Foreign bank |

| 79 | Guiyang Bank | City commercial bank | 158 | Bank of Korea | Foreign bank |

References

- Adrian, T.; Brunnermeier, M. CoVaR; NBER Working Paper, No.17454; National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar]

- Xu, Q.; Chen, L.; Jiang, C.; Yuan, J. Measuring systemic risk of the banking industry in China: A DCC-MIDAS-t approach. Pac.-Basin Financ. J. 2018, 51, 13–31. [Google Scholar] [CrossRef]

- Acharya, V.V.; Steffen, S. Analyzing systemic risk of the European banking sector. In Handbook on Systemic Risk; Fouque, J.P., Langsam, J.A., Eds.; Cambridge University Press: Cambridge, UK, 2013; pp. 247–282. [Google Scholar]

- Brownlees, C.T.; Engle, R. Volatility, Correlation and Tails for Systemic Risk Measurement. Available online: https://www.semanticscholar.org/paper/Volatility%2C-Correlation-and-Tails-for-Systemic-Risk-Brownlees-Engle/c3c8133b4b946aa72e939da4fa001dc8b4a16ce2 (accessed on 12 December 2021).

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 1, 57–66. [Google Scholar] [CrossRef] [Green Version]

- Diebold, F.X.; Yilmaz, K. Measuring financial asset return and volatility spillovers, with application to global equity markets. Econ. J. 2009, 534, 158–171. [Google Scholar] [CrossRef] [Green Version]

- Diebold, F.X.; Yilmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econ. 2014, 182, 119–134. [Google Scholar] [CrossRef] [Green Version]

- Härdle, W.K.; Wang, W.; Yu, L. TENET: Tail-Event driven NETwork risk. J. Econ. 2016, 192, 499–513. [Google Scholar] [CrossRef]

- Lelyveld, I.; Liedorp, F. Interbank Contagion in the Dutch Banking Sector: A Sensitivity Analysis. Int. J. Cent. Bank. 2006, 5, 99–133. [Google Scholar]

- Upper, C.; Worms, A. Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? Eur. Econ. Rev. 2004, 48, 827–849. [Google Scholar] [CrossRef] [Green Version]

- Verma, R.; Ahmad, W.; Uddin, G.S.; Bekiros, S. Analysing the systemic risk of Indian banks. Econ. Lett. 2019, 176, 103–108. [Google Scholar] [CrossRef]

- Wang, G.J.; Jiang, Z.Q.; Lin, M.; Xie, C.; Stanley, H.E. Interconnectedness and systemic risk of China’s financial institutions. Emerg. Mark. Rev. 2018, 35, 1–18. [Google Scholar] [CrossRef]

- Wang, G.-J.; Chen, Y.-Y.; Si, H.-B.; Xie, C.; Chevallier, J. Multilayer information spillover networks analysis of China’s financial institutions based on variance decompositions. Int. Rev. Econ. Finance 2021, 73, 325–347. [Google Scholar] [CrossRef]

- Benoit, S.; Colliard, J.E.; Hurlin, C.; Pérignon, C. Where the Risks Lie: A Survey on Systemic Risk. Narnia 2017, 21, 109–152. [Google Scholar] [CrossRef]

- Billio, M.; Getmansky, M.; Lo, A.W.; Pelizzon, L. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. J. Financ. Econ. 2012, 104, 535–559. [Google Scholar] [CrossRef]

- Beltratti, A.; Bortolotti, B.; Caccavaio, M. Stock market efficiency in China: Evidence from the split-share reform. Q. Rev. Econ. Financ. 2016, 60, 125–137. [Google Scholar] [CrossRef] [Green Version]

- Anand, K.; Craig, B.R.; Von Peter, G. Filling in the Blanks: Network Structure and Interbank Contagion. Quant. Financ. 2014, 15, 625–636. [Google Scholar] [CrossRef] [Green Version]

- Gandy, A.; Veraart, L.A.M. A Bayesian methodology for systemic risk assessment in financial networks. LSE Res. Online Doc. Econ. 2017, 63, 215–229. [Google Scholar] [CrossRef]

- Zedda, S.; Cannas, G. Analysis of banks’ systemic risk contribution and contagion determinants through the leave-one-out approach. J. Bank. Financ. 2017, 112, 105160. [Google Scholar] [CrossRef]

- Lisa, R.D.; Zedda, S.; Vallascas, F.; Campolongo, F.; Marchesi, M. Modelling Deposit Insurance Scheme Losses in a Basel 2 Framework. J. Financ. Serv. Res. 2011, 40, 123–141. [Google Scholar] [CrossRef]

- Frankel, J.A.; Rose, A.K. Currency crashes in emerging markets: An empirical treatment. J. Int. Econ. 1996, 41, 351–366. [Google Scholar] [CrossRef] [Green Version]

- Corsi, F.; Lillo, F.; Pirino, D.; Trapin, L. Measuring the propagation of financial distress with granger-causality tail risk networks. J. Financ. Stab. 2018, 38, 18–36. [Google Scholar] [CrossRef]

- Furfine, C. Interbank Exposures: Quantifying the Risk of Contagion. J. Money Crédit. Bank. 2003, 35, 111–128. [Google Scholar] [CrossRef]

- Chen, B.; Li, L.; Peng, F.; Anwar, S. Risk contagion in the banking network: New evidence from China. North Am. J. Econ. Financ. 2020, 54, 101276. [Google Scholar] [CrossRef]

- Elsinger, H.; Lehar, A.; Summer, M. Network Models and Systemic Risk Assessment. Handb. Syst. Risk 2013, 1, 287–305. [Google Scholar]

- Upper, C. Simulation methods to assess the danger of contagion in interbank markets. J. Financ. Stab. 2011, 7, 111–125. [Google Scholar] [CrossRef]

- Mistrulli, P.E. Assessing financial contagion in the interbank market: Maximum entropy versus observed interbank lending patterns. J. Bank. Financ. 2011, 35, 1114–1127. [Google Scholar] [CrossRef]

- Blien, U.; Graef, F. Entropy Optimizing Methods for the Estimation of Tables. In Classification, Data Analysis, and Data Highways; Springer: Berlin/Heidelberg, Germany, 1998; pp. 3–15. [Google Scholar]

- Huang, X.; Zhou, H.; Zhu, H. Systemic Risk Contributions. J. Financ. Serv. Res. 2012, 42, 55–83. [Google Scholar] [CrossRef]

- Paltalidis, N.; Gounopoulos, D.; Kizys, R.; Koutelidakis, Y. Transmission channels of systemic risk and contagion in the European financial network. J. Bank. Financ. 2015, 61, S36–S52. [Google Scholar] [CrossRef] [Green Version]

| Year | Proportion of Sample Bank Assets in Total Banking Assets |

|---|---|

| 2013 | 69.93% |

| 2014 | 70.31% |

| 2015 | 69.30% |

| 2016 | 72.66% |

| 2017 | 70.28% |

| 2018 | 66.15% |

| Year | Total Assets of Sample Banks | ||

|---|---|---|---|

| UCBs | JSCBs | SOCBs | |

| 2013 | 14.38% | 21.45% | 64.18% |

| 2014 | 12.27% | 23.65% | 64.08% |

| 2015 | 13.74% | 24.58% | 61.68% |

| 2016 | 14.62% | 28.98% | 56.40% |

| 2017 | 15.03% | 27.41% | 57.56% |

| 2018 | 13.70% | 23.62% | 62.68% |

| Variable | Obs. | Mean | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|

| Systematic risk | 513 | 246.321 | 459.123 | −3.276 | 2919.786 |

| Infectious risk | 513 | 66.737 | 66.237 | −482.553 | 387.879 |

| Individual risk | 513 | 179.584 | 449.146 | 1.518 | 2982.52 |

| Cash and the logarithm of deposited central bank payments | 513 | 24.125 | 2.857 | 0 | 28.916 |

| Logarithm of inter-bank money on deposit | 513 | 22.463 | 3.096 | 0 | 27.313 |

| Logarithm of traded financial assets | 513 | 18.16 | 8.675 | 0 | 27.415 |

| Logarithm of derived financial assets | 513 | 6.492 | 9.934 | 0 | 25.595 |

| Log of fixed assets | 506 | 21.295 | 1.698 | 17.394 | 26.259 |

| Log of total assets | 508 | 26.468 | 1.621 | 23.495 | 30.952 |

| Logarithm of total liabilities | 508 | 26.385 | 1.646 | 20.177 | 30.864 |

| Logarithm of provisions for risk | 501 | 21.886 | 1.722 | 16.644 | 26.357 |

| Variable | Systematic Risk | Infectious Risk | Individual Risk | |||

|---|---|---|---|---|---|---|

| Total Sample | Total Sample | State-Owned Banks | Joint-Stock Banks | City Commercial Banks | Total Sample | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Logarithm of cash and deposited central bank payments | −0.255 ** | −0.165 | 6.822 * | 1.225 | −0.231 * | 0.041 |

| (0.099) | (0.163) | (3.339) | (2.305) | (0.133) | (0.029) | |

| Logarithm of inter-bank money on deposit | −0.003 | −0.003 | −0.216 | −0.004 | −0.011 | −0.007 |

| (0.015) | (0.025) | (0.460) | (0.080) | (0.037) | (0.004) | |

| Logarithm of traded financial assets | 0.011 ** | 0.005 | −0.571 | −0.328 | 0.006 | 0.001 |

| (0.005) | (0.008) | (0.801) | (0.289) | (0.006) | (0.001) | |

| Logarithm of derivative assets | 0.003 | 0.004 | −0.223 | −0.393 | 0.004 | 0.001 |

| (0.007) | (0.012) | (0.636) | (0.465) | (0.009) | (0.002) | |

| Log of fixed assets | 0.052 | 0.034 | 0.706 | −0.439 | 0.103 | 0.059 *** |

| (0.074) | (0.122) | (1.580) | (1.653) | (0.099) | (0.021) | |

| Log of total assets | 0.497 *** | 0.256 | 53.699 | 15.439 | 0.142 | 0.611 *** |

| (0.173) | (0.284) | (50.843) | (41.733) | (0.229) | (0.063) | |

| Logarithm of total liabilities | 0.407 *** | 0.531 *** | −53.087 | −9.365 | 0.540 *** | 0.056 ** |

| (0.093) | (0.150) | (53.274) | (41.329) | (0.118) | (0.026) | |

| Logarithm of the general risk preparation | 0.037 | 0.024 | −1.431 | −2.225 | 0.079 | 0.070 *** |

| (0.077) | (0.125) | (4.360) | (1.947) | (0.100) | (0.020) | |

| Constant terms | −14.958 *** | −13.824 *** | −165.476 | −122.411 * | −11.664 *** | −17.861 *** |

| (2.547) | (4.132) | (94.125) | (64.712) | (3.376) | (1.213) | |

| Individual fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 499 | 473 | 22 | 52 | 399 | 501 |

| R-squared | 0.400 | 0.177 | 0.651 | 0.142 | 0.278 | 0.907 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zou, J.; Fu, X.; Yang, J.; Gong, C. Measuring Bank Systemic Risk in China: A Network Model Analysis. Systems 2022, 10, 14. https://doi.org/10.3390/systems10010014

Zou J, Fu X, Yang J, Gong C. Measuring Bank Systemic Risk in China: A Network Model Analysis. Systems. 2022; 10(1):14. https://doi.org/10.3390/systems10010014

Chicago/Turabian StyleZou, Jin, Xu Fu, Jun Yang, and Chi Gong. 2022. "Measuring Bank Systemic Risk in China: A Network Model Analysis" Systems 10, no. 1: 14. https://doi.org/10.3390/systems10010014

APA StyleZou, J., Fu, X., Yang, J., & Gong, C. (2022). Measuring Bank Systemic Risk in China: A Network Model Analysis. Systems, 10(1), 14. https://doi.org/10.3390/systems10010014