On the Generalized Inverse Gaussian Volatility in the Continuous Ho–Lee Model

Abstract

1. Introduction

2. Materials and Methods

2.1. Continuous-Time Ho–Lee Model

2.2. Generalized Inverse Gaussian Distributions

3. Results

3.1. GIG Continuous-Time Ho–Lee Model

3.2. Bond Price and Its Moments

3.3. Bond Options

4. Numerical Analysis

4.1. Parameters

4.2. Time Interval

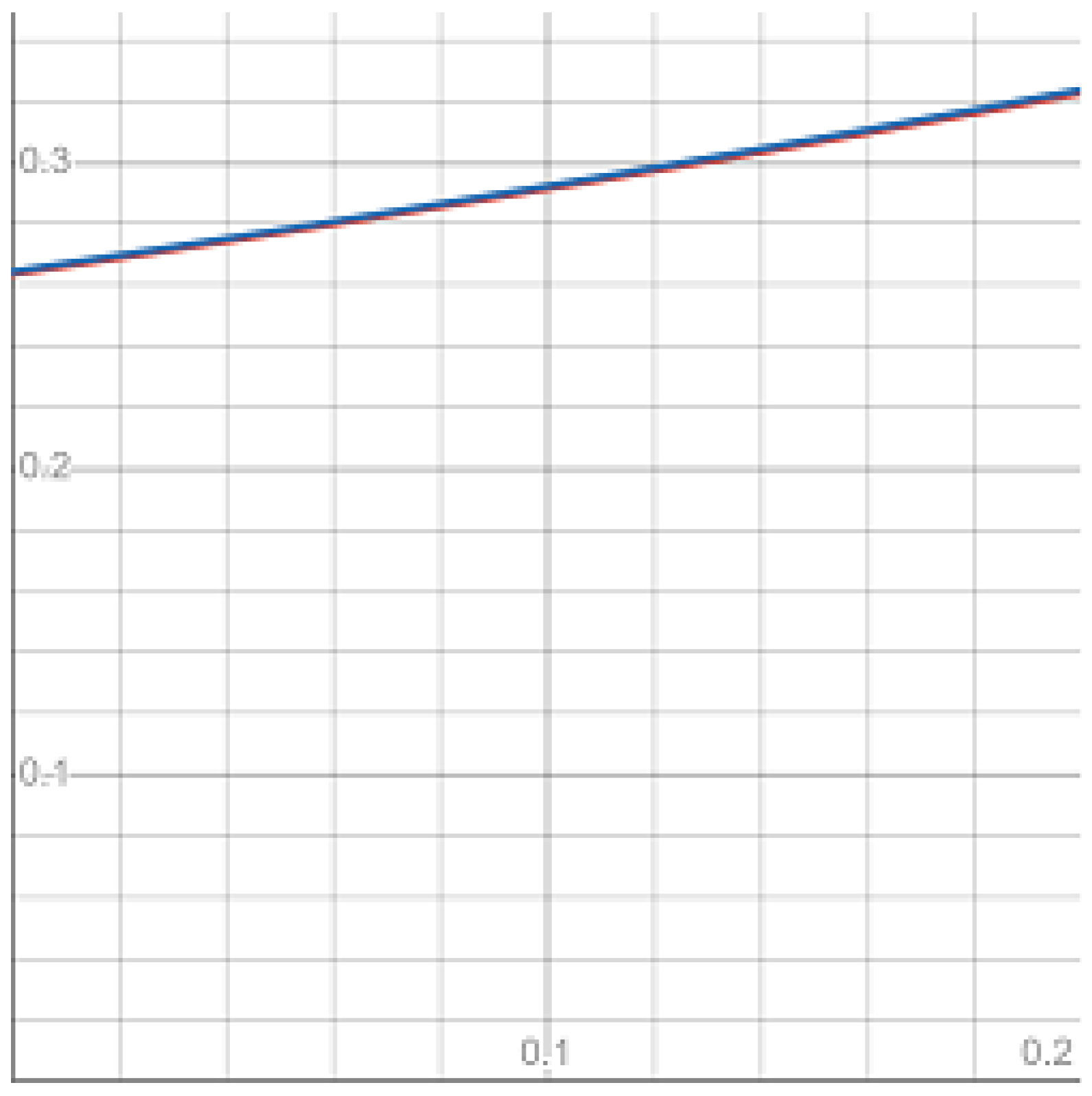

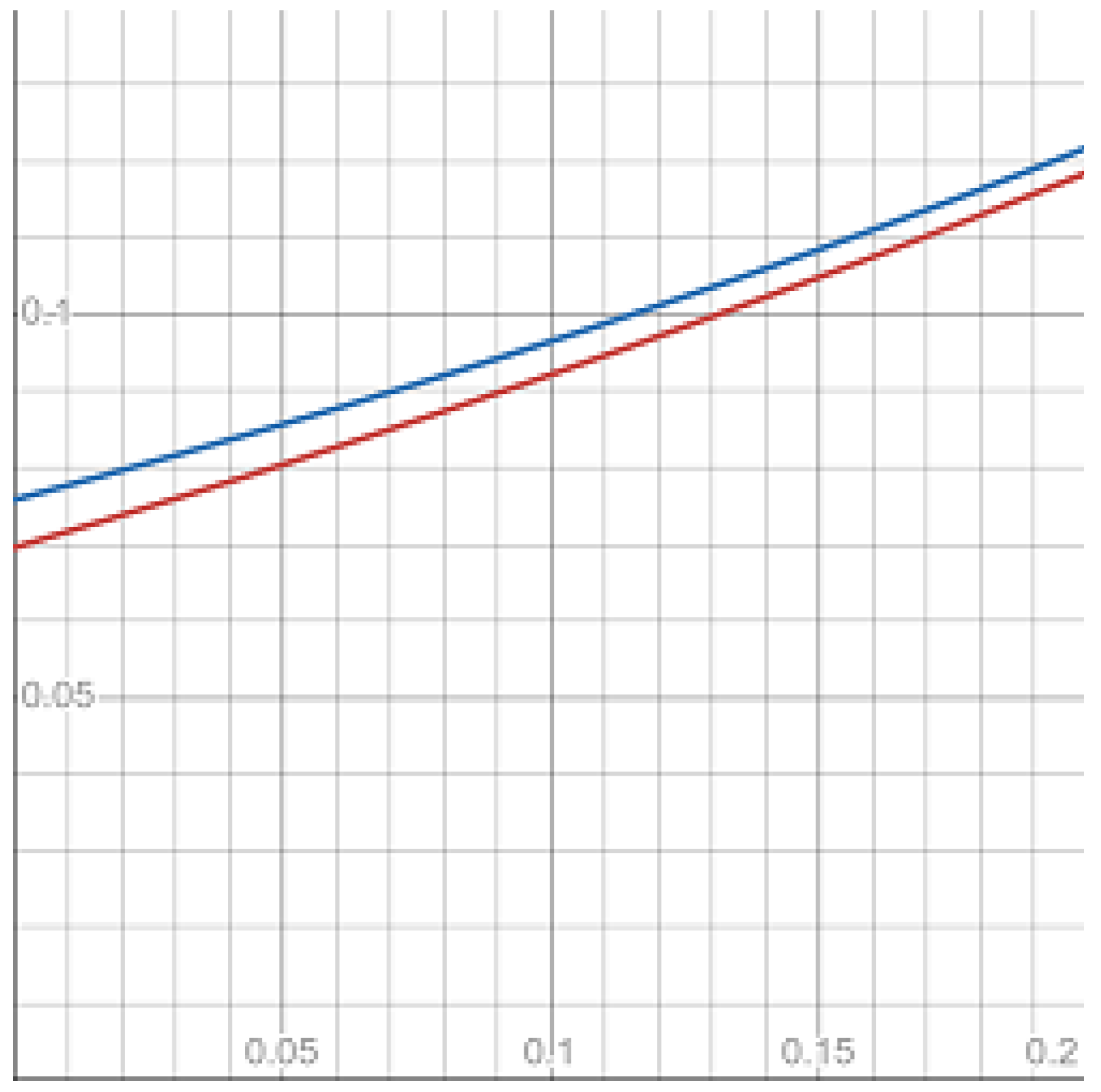

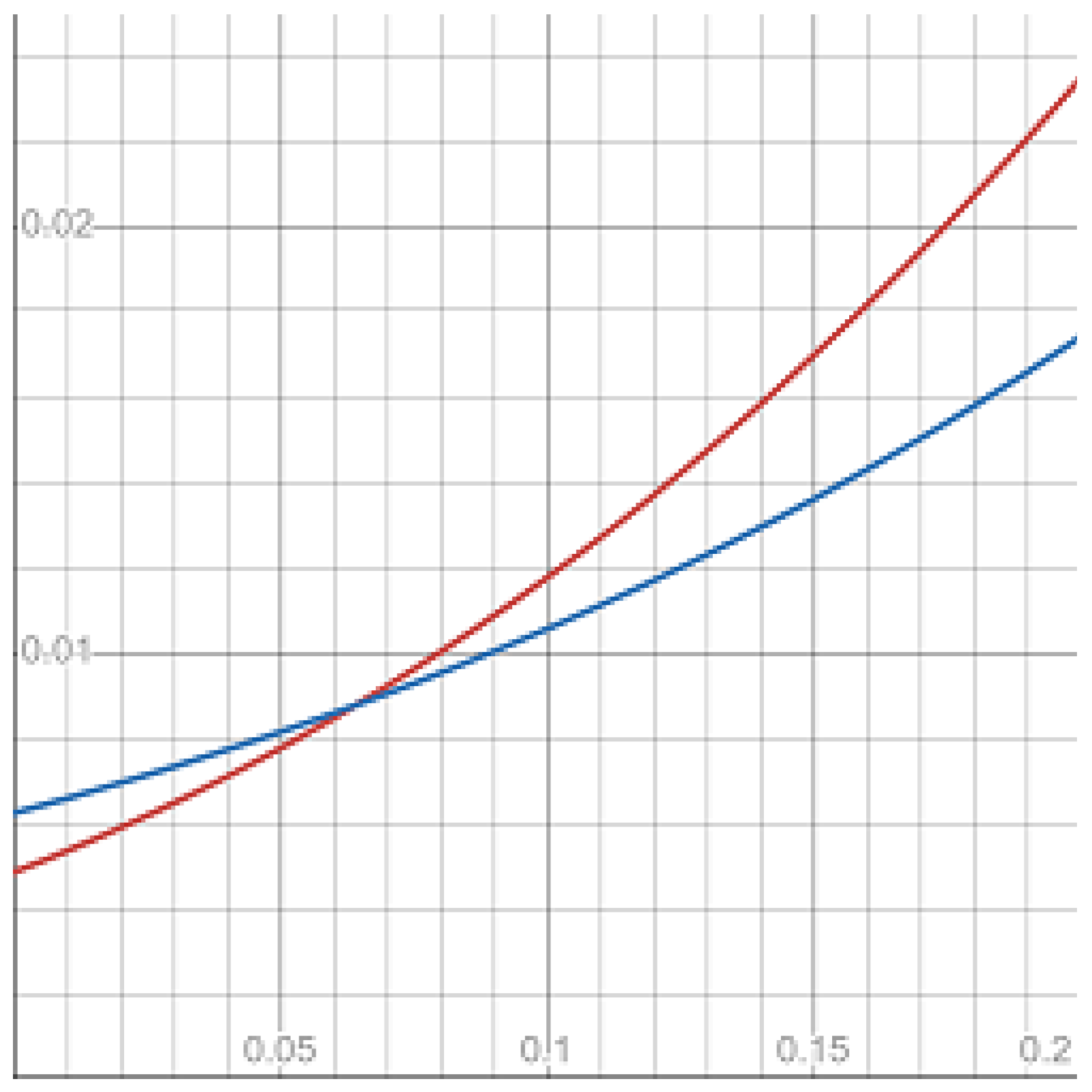

4.3. Moments of the Bond Prices

4.4. Complex Example

5. Discussion

6. Conclusions

- The proposed model is analytically tractable. We have found the closed-form expressions for the bond price, its moments, and the prices of European call and put bond options. However, the results related to the option prices are obtained under the special restrictions on the parameters of model;

- The numerical experiments have shown that the third and fourth moments of the continuous Ho–Lee and GIG continuous Ho–Lee bond prices with the same mean may differentiate at up to 15.6% and 25.8%, respectively. And the higher moments of the GIG bond price can take infinite values. Therefore, the compound model could better reflect the properties of market yield curves;

- In the next examinations, the call and put bond option prices could be found with fewer constraints on the parameters. The problem of swap and exotic derivative pricing in the new model should be discussed. The possibility of the extension of the introduced model to the GIG Vasicek model should be considered as well.

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| GIG | Generalized inverse Gaussian |

| GH | Generalized hyperbolic |

| HIG | Hyperbolic-inverse Gaussian |

| IG | Inverse Gaussian |

| NIG | Normal-inverse Gaussian |

| HJM | Heath–Jarrow–Morton |

| determ. | Deterministic |

| cont. | Continuous |

| stoch. | Stochastic |

Appendix A

Appendix B

References

- Ho, T.S.Y.; Lee, S.B. Term structure movements and pricing interest rate contingent claims. J. Financ. 1986, 41, 1011–1029. [Google Scholar] [CrossRef]

- Hull, J.; White, A. Pricing interest-rate-derivative securities. Rev. Finan. Stud. 1990, 3, 573–592. [Google Scholar] [CrossRef]

- Heath, D.; Jarrow, R.; Morton, A. Bond pricing and the term structure of interest rate: A new methodology for contingent claims valuation. Econometrica 1992, 60, 77–105. [Google Scholar] [CrossRef]

- Subrahmanyam, M.G. The term structure of interest rates: Alternative approaches and their implications for the valuation of contingent claims. Geneva Pap. Risk Insur. Theory 1996, 21, 7–28. [Google Scholar] [CrossRef]

- Musiela, M.; Rutkowski, M. Martingale Methods in Financial Modelling, 2nd ed.; Springer: Berlin, Germany, 2005; pp. 331–337, 348–349, 381–412, 431–526. [Google Scholar]

- Halphen, É. Sur un nouveau type de courbe de fréquence. C. R. Hebdom. Séances Académ. Sc. 1941, 213, 634–635. [Google Scholar]

- Barndorff-Nielsen, O.E. Exponentially decreasing distributions for the logarithm of particle size. Proc. R. Soc. Lond. A 1977, 353, 401–419. [Google Scholar]

- Eberlein, E.; Keller, U. Hyperbolic distributions in finance. Bernoulli 1995, 1, 281–299. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E. Processes of normal inverse Gaussian type. Financ. Stoch. 1998, 2, 41–68. [Google Scholar] [CrossRef]

- Küchler, U.; Neumann, K.; Sørensen, M.; Streller, A. Stock returns and hyperbolic distributions. Math. Comput. Model. 1999, 29, 1–15. [Google Scholar] [CrossRef]

- Bauer, C. Value at risk using hyperbolic distributions. J. Econ. Bus. 2000, 52, 455–467. [Google Scholar] [CrossRef]

- Eriksson, A.; Ghysels, E.; Wang, F. The normal inverse Gaussian distribution and the pricing of derivatives. J. Deriv. 2009, 16, 23–37. [Google Scholar] [CrossRef]

- Luciano, E.; Marena, M.; Semeraro, P. Dependence calibration and portfolio fit with factor-based subordinators. Quant. Finan. 2016, 16, 1037–1052. [Google Scholar] [CrossRef]

- Fajardo, J.; Farias, A. Multivariate affine generalized hyperbolic distributions: An empirical investigation. Internat. Rev. Finan. Anal. 2009, 18, 174–184. [Google Scholar] [CrossRef]

- Daskalaki, S.; Katris, C. Marginal distribution modeling and value at risk estimation for stock index returns. J. Appl. Oper. Res. 2014, 6, 207–221. [Google Scholar]

- Rathgeber, A.W.; Stadler, J.; Stöckl, S. Fitting generalized hyperbolic processes—New insights for generating initial values. Commun. Stat. Simul. Comput. 2017, 46, 5752–5762. [Google Scholar] [CrossRef]

- Rathgeber, A.W.; Stadler, J.; Stöckl, S. Financial modelling applying multivariate Lévy processes: New insights into estimation and simulation. Phys. A Stat. Mech. Appl. 2019, 532, 121386. [Google Scholar] [CrossRef]

- Nakakita, M.; Nakatsuma, T. Bayesian analysis of intraday stochastic volatility models of high frequency stock returns with skew heavy tailed errors. J. Risk Finan. Manag. 2021, 14, 145. [Google Scholar] [CrossRef]

- Nakajima, J. Skew selection for factor stochastic volatility models. J. Appl. Stat. 2020, 47, 582–601. [Google Scholar] [CrossRef]

- Chan, S.; Chu, J.; Nadarajah, S.; Osterrieder, J. A statistical analysis of cryptocurrencies. J. Risk Finan. Manag. 2017, 10, 12. [Google Scholar] [CrossRef]

- Sheraz, M.H.M.; Dedu, S.A. Bitcoin cash: Stochastic models of fat-tail returns and risk modeling. Econ. Comput. Econ. Cyber. Stud. Res. 2020, 54, 43–58. [Google Scholar]

- Abraham, B.; Balakrishna, N.; Sivakumar, R. Gamma stochastic volatility models. J. Forecast. 2006, 25, 153–171. [Google Scholar] [CrossRef]

- Frühwirth-Schnatter, S.; Sögner, L. Bayesian estimation of stochastic volatility models based on OU processes with marginal Gamma law. Ann. Inst. Stat. Math. 2009, 61, 159–179. [Google Scholar] [CrossRef]

- James, L.F.; Müller, G.; Zhang, Z. Stochastic volatility models based on OU-gamma time change: Theory and estimation. J. Busin. Econ. Stat. 2018, 36, 75–87. [Google Scholar] [CrossRef]

- Nzokem, A.H. Pricing European options under stochastic volatility models: Case of five-parameter variance-gamma process. J. Risk Finan. Manag. 2023, 16, 55. [Google Scholar] [CrossRef]

- Fung, T.; Seneta, E. Modelling and estimation for bivariate financial returns. Int. Stat. Rev. 2010, 78, 117–133. [Google Scholar] [CrossRef]

- Liu, J. A Bayesian semiparametric realized stochastic volatility model. J. Risk Finan. Manag. 2021, 14, 617. [Google Scholar] [CrossRef]

- Nakajima, J.; Omori, Y. Stochastic volatility model with leverage and asymmetrically heavy-tailed error using GH skew Student’s t-distribution. Comput. Stat. Data Anal. 2012, 56, 3690–3704. [Google Scholar] [CrossRef]

- Men, Z.; Wirjanto, T.S.; Kolkiewicz, A.W. Multiscale stochastic volatility model with heavy tails and leverage effects. J. Risk Finan. Manag. 2021, 14, 225. [Google Scholar] [CrossRef]

- Takahashi, M.; Watanabe, T.; Omori, Y. Forecasting daily volatility of stock price index using daily returns and realized volatility. Econom. Stat. 2024, 32, 34–56. [Google Scholar] [CrossRef]

- Eberlein, E.; von Hammerstein, E.A. Generalized hyperbolic and inverse Gaussian distributions: Limiting cases and approximation of processes. In Seminar on Stochastic Analysis, Random Fields and Applications IV, Progress in Probability; Dalang, R.C., Dozzi, M., Russo, F., Eds.; Birkhäuser Verlag: Berlin, Germany, 2004; Volume 58, pp. 221–264. [Google Scholar]

- Ivanov, R.V. The semi-hyperbolic distribution and its applications. Stats 2023, 6, 1126–1146. [Google Scholar] [CrossRef]

- Maltsev, V.; Pokojovy, M. Applying Heath-Jarrow-Morton model to forecasting the US treasury daily yield curve rates. Mathematics 2021, 9, 114. [Google Scholar] [CrossRef]

- Tóth-Lakits, D.; Arató, M. On the calibration of the Kennedy model. Mathematics 2024, 12, 3059. [Google Scholar] [CrossRef]

- Fontana, C.; Lanaro, G.; Murgoci, A. The geometry of multi-curve interest rate models. Quantit. Finance 2024, 1–20, in print. [Google Scholar] [CrossRef]

- Gardini, M.; Santilli, E. A Heath-Jarrow-Morton framework for energy markets: Review and applications for practitioners. Decisions Econom. Finan. 2024, 1–40, in print. [Google Scholar] [CrossRef]

- Hull, J.; White, A. One-factor interest-rate models and the valuation of interest-rate derivative securities. J. Financ. Quant. Anal. 1993, 28, 235–254. [Google Scholar] [CrossRef]

- Serafin, T.; Michalak, A.; Bielak, L.; Wylomańska, A. Averaged-calibration-length prediction for currency exchange rates by a time-dependent Vasicek model. Theor. Econ. Lett. 2020, 10, 579–599. [Google Scholar] [CrossRef]

- Orlando, G.; Bufalo, M. Interest rates forecasting: Between Hull and White and the CIR#—How to make a single-factor model work. J. Forecast. 2021, 40, 1566–1580. [Google Scholar]

- van der Zwaard, T.; Grzelak, L.A.; Oosterlee, C.W. On the Hull-White model with volatility smile for valuation adjustments. arXiv 2024, arXiv:2403.14841. [Google Scholar] [CrossRef]

- Ivanov, R.V. On the stochastic volatility in the generalized Black-Scholes-Merton model. Risks 2023, 11, 111. [Google Scholar] [CrossRef]

- Madan, D.B.; Carr, P.; Chang, E.C. The variance gamma process and option pricing. Rev. Finan. 1998, 2, 79–105. [Google Scholar] [CrossRef]

- Ano, K.; Ivanov, R.V. On exact pricing of FX options in multivariate time-changed Lévy models. Rev. Deriv. Res. 2016, 19, 201–216. [Google Scholar]

- Ivanov, R.V. On properties of the hyperbolic distribution. Mathematics 2024, 12, 2888. [Google Scholar] [CrossRef]

- Eberlein, E.; Gerhart, C.; Grbac, Z. Multiple curve Lévy forward price model allowing for negative interest rates. Math. Finan. 2020, 30, 167–195. [Google Scholar] [CrossRef]

- Orlando, G.; Taglialatela, G. A review on implied volatility calculation. J. Comput. Appl. Math. 2017, 320, 202–220. [Google Scholar] [CrossRef]

- Merton, R.C. Theory of rational option pricing. Bell J. Econom. Manag.Sci. 1973, 4, 141–183. [Google Scholar] [CrossRef]

- Shiryaev, A.N. Essentials of Stochastic Finance; World Scientific: Singapore, 1999; pp. 792–799. [Google Scholar]

- Barndorff-Nielsen, O.E.; Halgreen, C. Infinite divisibility of the hyperbolic and generalized inverse Gaussian distributions. Z. Wahrscheinlichkeitstheorie Verw. Geb. 1977, 38, 309–312. [Google Scholar] [CrossRef]

- Gradshteyn, I.S.; Ryzhik, I.M. Table of Integrals, Series and Products, 7th ed.; Elsevier Academic Press: New York, NY, USA, 2007; pp. 368, 925. [Google Scholar]

- Jørgensen, B. Statistical Properties of the Generalized Inverse Gaussian Distribution; Springer: New York, NY, USA, 1982; pp. 5–19, 39–65. [Google Scholar]

- Barndorff-Nielsen, O.E. Hyperbolic distributions and distributions on hyperbolae. Scand. J. Statist. 1978, 5, 151–157. [Google Scholar]

- Blaesild, P. Conditioning with conic sections in the two-dimensional normal distribution. Ann. Stat. 1979, 7, 659–670. [Google Scholar] [CrossRef]

- Shreve, S.E. Stochastic Calculus for Finance II Continuous-Time Models; Springer: New York, NY, USA, 2004; pp. 124–128. [Google Scholar]

- Eberlein, E. Application of generalized hyperbolic Lévy motions to finance. In Lévy Processes; Barndorff-Nielsen, O.E., Resnick, S.I., Mikosch, T., Eds.; Birkhäuser: Boston, MA, USA, 2001; pp. 319–336. [Google Scholar]

- Brigo, D.; Mercurio, F. Interest Rate Models—Theory and Practice, 2nd ed.; Berlin: Springer, Germany, 2006; pp. 39–40. [Google Scholar]

- Srivastava, H.M.; Karlsson, W. Multiple Gaussian Hypergeometric Series; Ellis Horwood Limited: New York, NY, USA, 1985; p. 25. [Google Scholar]

- Humbert, P. The confluent hypergeometric functions of two variables. Proc. R. Soc. Edinb. 1922, 41, 73–96. [Google Scholar] [CrossRef]

- Bateman, H.; Erdélyi, A. Higher Transcendental Functions; McGraw-Hill: New York, NY, USA, 1953; Volume I, pp. 222–247. [Google Scholar]

- Fontana, C.; Gnoatto, A.; Szulda, G. Multiple yield curve modelling with CBI processes. Math. Finan. Econom. 2021, 15, 579–610. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Merton | Cont. Ho–Lee | Vasicek | Hull–White | Heath–Jarrow–Morton | |

|---|---|---|---|---|---|

| determ. | stoch. | ||||

| determ. | determ. | stoch. |

| GIG | inverse Gaussian | harmonic | hyperbolic-inverse Gaussian |

| GH | normal-inverse Gaussian | semi-hyperbolic | hyperbolic |

| 0 | 0.025 | 0.05 | 0.075 | 0.1 | 0.125 | 0.15 | 0.175 | 0.2 | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | |||||||||

| 2 | |||||||||

| 3 | |||||||||

| 4 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ivanov, R.V. On the Generalized Inverse Gaussian Volatility in the Continuous Ho–Lee Model. Computation 2025, 13, 100. https://doi.org/10.3390/computation13040100

Ivanov RV. On the Generalized Inverse Gaussian Volatility in the Continuous Ho–Lee Model. Computation. 2025; 13(4):100. https://doi.org/10.3390/computation13040100

Chicago/Turabian StyleIvanov, Roman V. 2025. "On the Generalized Inverse Gaussian Volatility in the Continuous Ho–Lee Model" Computation 13, no. 4: 100. https://doi.org/10.3390/computation13040100

APA StyleIvanov, R. V. (2025). On the Generalized Inverse Gaussian Volatility in the Continuous Ho–Lee Model. Computation, 13(4), 100. https://doi.org/10.3390/computation13040100