1. Introduction

Innovation, defined as the process whereby an invention or a concept is translated into a tangible commercial asset, typically proceeds from several stages, including idea generation, hypothesis testing, translation into a prototype product or service, and commercialization. Applied to high technology, typical actors involved in this value chain include scientists at academic laboratories to discover and design the fundamental bases, entrepreneurs at start-up companies and their financial backers to de-risk the new technology, and larger organizations to deploy technology polishing and financial strength, as well as global reach, for commercializing the new product on a large scale. What is more, a greater share of radical innovation, that is, innovation that initiates a new technology cycle and that frequently has the intrinsic potential to fundamentally challenge existing products or services [

1], is developed at the academia-“high technology venture” interface; whereas incremental innovation, that is, innovation that generates marginal but nevertheless important improvements over existing products or services, is developed to a greater extent at the “high technology venture”—large organization interface [

2].

In industrial and healthcare biotechnology, this value chain is operational in conditions of access to sufficient capital, as demonstrated by the numerous licensing agreements that are signed each year between academia and biotechnology companies, as well as between biotechnology companies and large pharmaceutical or large chemical firms [

3,

4,

5]. In the chemical arena, Big Chemical mostly compete on price for a share of commodity markets [

6], with few possibilities to compete based on technology protected by composition of matter patents, except in the polymer industry with an emerging focus on biopolymers [

7]. In the healthcare arena, to compete Big Pharma have increased their reliance on large R&D budgets to develop proprietary products and and on in-licensing late stage assets to support their franchises [

4,

5,

8]. However, given a fierce competition in the pursuit of blockbuster products, these firms have been forced in their arms race not only to move more and more upstream of the innovation chain when partnering [

9], but also to increase their R&D and Sales&Marketing outlays [

8,

10]. In contrast to Big Chemical, which typically spends 1–3% of sales in R&D, Big Pharma spends 15–20% of the total of which reached $69.5b in 2008 for the US pharmaceutical industry alone [

6,

11]. What is more, despite the value of Big Pharma late stage pipelines being historically directly proportional to their R&D spends [

12], these companies are experiencing diminishing returns on investment and a broken business model, still to this date too conventionally focused on reaching increasingly elusive blockbuster products using conventional technologies [

8,

12,

13,

14,

15,

16,

17]. In response, beyond merger and acquisition strategies, Big Pharma are currently attempting to become more cost-effective and more efficient at R&D; this includes restructuring internal pharmaceutical workforces [

10], targeting emerging or niche markets such as rare diseases [

18], implementing personalized medicines [

19], and rethinking innovation processes and models [

8,

14,

15,

16,

20,

21,

22].

A puzzling observation is that while individually small biotechnology companies are a much less reliable source of new medical entities (NMEs) than Big Pharma, collectively biotechs produce more NMEs for only a fraction of the cost [

8]. As a result, there are currently numerous experiments being conducted at Big Pharma to replicate the innovative spirit and success of biotechs, including open-source R&D, consortia, small and focused centres of excellence, as well as internal entrepreneurship [

8,

20,

23,

24]. Accessing academic innovation directly by way of partnering or licensing agreements to boost innovation productivity, and in so doing emulate the success of biotechs, has long been an attractive approach for Big Pharma. This has typically been experimented with via multiyear and multimillion dollar alliances in exchange for some control given to the corporate partner regarding the intellectual property (IP) that is generated, for example in the form of a first right to negotiate. However, case studies suggest that value capture in this partnering model has all but failed [

25,

26]. Notably, these failures have been ascribed to unrealistic expectations regarding the long term commitments that are necessary for success to emerge, the difficulty to balance on the one hand an arm’s length approach (to encourage academic creativity) and on the other hand targeted guidance towards commercial outcomes, and the fact that returns that are hard to measure are extremely hard to justify in times of constrained resources [

25]. An important exception here can be made regarding the field of bioenergy and sustainable chemicals, since recent investments in this field by Big Chemical and Big Oil via similar multiyear and multimillion dollar alliances can be viewed as primarily aiming at building in the marketplace the productivity factors that are necessary for the new industry to flourish, considering a newly perceived market urgency and the relatively extremely low level of public funding in this domain for the past few decades [

7,

27,

28].

Efficient access to innovation is a key competitiveness factor for large firms, and particularly in high technology arenas. Since the market teaches us that simply increasing internal R&D outlays with the hope to boost innovation engines for changing the economic return gear of big pharmaceutical companies is insufficient, what is then the new philosophy of innovation that is necessary? A noteworthy experiment is that of Procter & Gamble (P&G), a consumer goods company, which has solved its innovation success rate shortcoming by implementing its

Connect + Develop network leveraging initiative, the aim of which was to access 50% of its innovation from external sources. The outcome was clear-cut, with P&G doubling its percentage of new products that met financial objectives and significantly decreasing its R&D budget as a percentage of sales [

16,

29]. In this context, can research developed by academia, and biotechnology start-ups alike, be more efficiently harnessed by Big Pharma, and what could be a new model of interactions?

2. Business Fundamentals

From the viewpoint of the corporate partner, value-adding academic partnerships stem from three fundamental pillars: (1) excellence in science, (2) prospects for value play, and (3) efficient risk management. From the university viewpoint, advancing fundamental research, promoting teaching, attracting grants, and commercializing university IP are worthy goals. Obstacles to university IP commercialisation have long been known, including the facts that only a minor fraction of licenses (mostly those regarding disruptive technologies) generate significant licensing and royalty income, that many of the “golden nuggets” are not aggregated, and that it is rarely easy for academic spinoffs to find appropriate venture funding [

30]. Other systemic imperfections that diminish the financial value leveraged from university IP include insufficient biotechnology expertise in technology transfer offices, insufficient commercialisation policies of public research organisations, inappropriate models to manage IP between researchers and research organisations, and the lack of specific skills necessary to translate inventions into commercial products [

31].

Corporate venturing has been explored by large firms as a means to remedy these shortcomings, in a process whereby the corporation and its staff: fund the start-ups (at least in part), house them in incubators as relatively autonomous structures to maintain intact their entrepreneurial cultures, and manage them. This model has been exploited particularly to assess the market viability of radical innovation with the hope to benefit not only from financial returns, but also from strategic ones [

32,

33]. Empirical evidence suggests that successful corporate ventures are developed through five well identified stages: (1) idea generation, (2) concept development, (3) business plan development, (4) incubation and commercialization, (5) value capture [

33]. A drawback of this model is that typically the business concepts that are being pursued are internally generated; this is a fundamental constraint that restricts the pool of ideas being explored to knowledge essentially circumscribed within the corporation boundaries and its beliefs. What is more, corporate venturing requires specific skills that may not exist within the realm of the corporation, or seeding new companies may not fall within the mandate of its corporate venture fund as many such funds are still measured by financial returns alone, although this obsolete design that carries inherent conflicts of interest and lacks strategic relevance and vision is gradually being phased out [

34]. A variation of corporate venturing that addresses some of its inefficiencies, as well as limits initial financial risks and reduces accounting complexities, is currently being deployed by large pharmaceutical companies, which are more willing nowadays to incubate promising high technology start-ups in fully owned dedicated “accelerator” sites. The new ventures can thus benefit from belonging to a large scientific community base; and may even use some of the capital-intensive capabilities that these large companies can offer, such as large compound libraries or high throughput screening suites [

35]. In return, when successful, these companies already have natural links with their respective hosts. Examples of large firms operating similar incubators include Pfizer and Biogen Idec [

35]. This design not only enhances the virtual space of technology solutions that are explored by these corporations, but also it enables them to benefit from information asymmetry while leaving, as they should, a greater part of the early financial risks in the hands of the financial backers of the new ventures that are more apt at managing such risks. However, this design still requires owning and operating expensive brick-and-mortar facilities, and does not make full use of the knowledge of the corporation such as its identified strategic technological needs and product concepts.

In parallel, models of industry-academia collaborations have emerged that are characterized by the implementation of proactive alliance management techniques [

36], where both parties are aligned behind both common interests (intellectual and financial) and a common product or technology development vision. In one embodiment, the interests and values of each party are detailed in advance such as to increase trust and resolve upfront possible conflict-of-interest issues [

37], and communication or decision sharing are optimized [

26,

38]. For example, Genentech and the University of California at San Francisco (UCSF) have entered in 2010 into a drug discovery partnership, whereby UCSF and Genentech scientists jointly pursue selected target pathways, with UCSF receiving royalties on commercialized products in addition to development and commercial milestone payments [

39]. Pfizer also established with UCSF an $85m/5-year partnership for Pfizer scientists and UCSF researchers to work alongside on campus on a range of discovery projects with the goal for each funded project to deliver a drug through phase I within that period [

40]. Likewise, Roche established a translational research hub in Singapore to develop strategies for drug development and personalized healthcare; notably, the hub is managed by a joint steering committee that sets the strategy and oversees the research projects [

41].

Empirical evidence suggests that these latter models of interaction have a clear potential to generate value for both academia and large corporations. Nevertheless, both of these models exhibit limitations in scope: on the one hand corporate venturing is restricted not only to knowledge existing or developed within the boundaries of the corporation, but also it requires competences that may, by cultural design, not be available at these large firms; whereas on the other hand actively managed industry-academia collaborations tend to focus on incremental innovation. In contrast, there is an increasingly acute need, particularly in the pharmaceutical field, to access cutting-edge innovation such as platform-to-product technologies [

42,

43]. This challenge is a critical one since, as an asset class, the pharmaceutical industry is believed to be exposed to a risk of downward valuation unless “new science quickly brings innovative therapies to the market” [

44]. What is needed is a complementary tool to access radical innovation, as this class of innovation is essential for corporations to build sustainable competitive advantages and future economic success [

1,

2], in a process where operational risks and financial exposures are limited, while access to world class scientific capabilities and commercial potential are maximised. Notably, traditional venture capital companies are ill-designed to bring a radical innovation to its highest value inflexion point, since these companies typically have a medium-term time horizon, which may differ by several decades from the timelines it takes to develop a new pharmaceutical or a new chemical polymer [

43,

45]. In turn, those misaligned timelines and incentives more often than not make life science company managers aggressively pursue a first positive discovery rather than build the scientific fundamentals that are necessary to exploit to its fullest a game-changing innovation [

43,

46].

3. Syndicated Innovation Venturing

Building on the corporate venturing experiment of the 1990s [

47], innovation venturing, a process whereby a corporation invests in many innovation-driven projects to de-risk new concepts, is worth revisiting. This form of corporate venturing has translated into some success, but was found mostly appropriate for corporations that: in some areas do not perform according to their potentials given insufficient resources to exploit them, have latent entrepreneurial skills, and have upper management teams willing to encourage and reward internal entrepreneurship and behaviour; with the key to success being to focus on addressing specific opportunities in specific functions while complementing existing operations [

47]. Likewise, global innovation networks have recently emerged to disaggregate the R&D function as a means to reduce costs, better address the increasing complexity of innovation, and better sense customer needs [

48]. However, such innovation networking creates risks of IP theft and loss of control over R&D projects and strategies [

48].

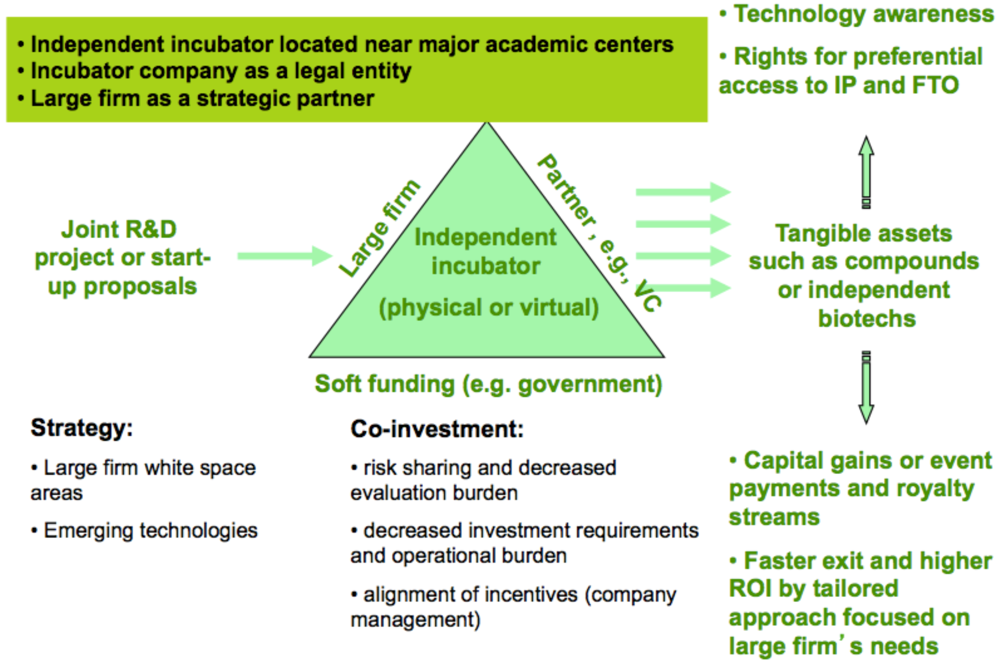

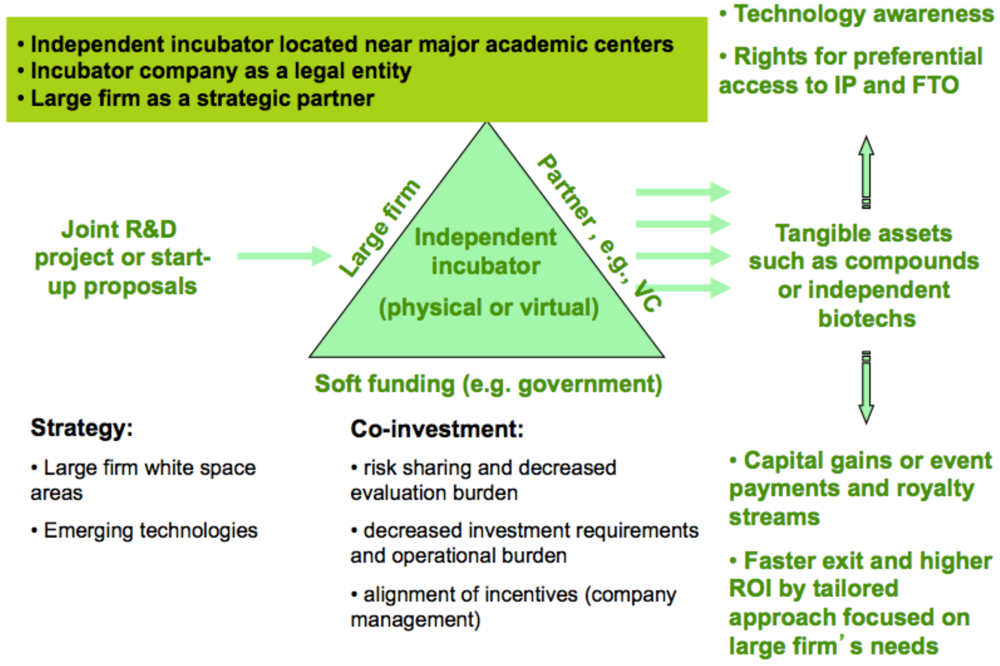

With the hope to increase probabilities of success and bypass some of their intrinsic risks, these two models can be combined. In so doing, innovation venturing is externalised by forming syndicates with outside parties as a means to reduce risks, virtually secure critical skills, and access visibility and influence in new geographical or technical areas. Notably, and dissimilar to consortia-based innovation, the parties forming the syndicate can represent totally non overlapping businesses, such that access to the generated IP is under no circumstance the reward of a zero-sum game but rather of a Nash equilibrium [

49]; an example would be a non exclusive syndicate comprising (

Figure 1 and

Box 1): (1) a large multinational firm; (2) a local or national public entity; (3) a venture capital partnership; and (4) an incubator company, which ideally is controlled and at least partly owned by the venture capital partnership. In this more virtual model of innovation venturing, each party manages the risks that, of the parties’ syndicate, it is the best at managing, and performs the tasks that it is the best at performing. Notably, assuming high visibility and attractiveness of the syndicate, scouting academic IP is performed here also by external would-be-entrepreneurs who develop business plans and product concepts, sieve academic IP since highly valuable IP is hard to locate [

50], and bundle IP assets as a basis for a new venture. Using an open network for this process is efficient since it not only alleviates the need for the large firm to employ a large number of IP analysts, but also it eliminates the cost of developing start-ups business plans, a task that is frequently outsourced in corporate venturing [

32,

33,

47]. What is more, as emphasised by Houghton

et al. [

50], patents are only a part of the intellectual capital necessary, which comprises ideas, know-how, and field awareness.

Figure 1.

Syndicated innovation venturing. IP: intellectual property. FTO: freedom to operate. ROI: return on investment. VC: venture capital partnership.

Figure 1.

Syndicated innovation venturing. IP: intellectual property. FTO: freedom to operate. ROI: return on investment. VC: venture capital partnership.

Box 1. Accelerating disruptive innovation deployment and new therapeutic product development.

Syndicated innovation venturing combines the business approaches to R&D of corporate venturing and innovation networks. Ideally, the syndicate comprises a large firm, a venture partnership (VC), an incubator company controlled at least in part by the VC (to avoid stalemates), and a public entity such as a local or national government body. The large firm provides strategic direction encompassing its knowledge of the market and of the underlying science and technology of product development. The VC provides not only financial and managerial expertise (including identifying, recruiting, and retaining key staff), but also a deep knowledge of its particular area of influence (geographic and market domains). The public entity provides support, such as financial or structural. The incubator company provides the seeding environment. Alignment of incentives is ensured by each party contributing a share of the seed capital. Key success factors include defined strategies complementing the large firm’s internal R&D, quality of the science and teamwork, defined market and product concept. Project quality is promoted by the four different entities having to use their own independent expert panels and independent perspectives to reach a positive funding decision. Deal flow is alimented by the quality and breadth of the networks of each of the parties of the syndicate. High visibility is an advantage as it allows posting calls for proposal to would-be-entrepreneurs, who in turn would develop business plans, including paths to bundle the necessary relevant but dispersed existing (academic) IP. The outcome is a unique investment strategy that meets all the typical filters of an investment committee: strategic fit, scientific excellence, and business potential [

17]. The endgame is characterized by each party being rewarded primarily in its preferred “currency”: the large firm with new products as tangible assets, the VC with financial returns, the public entity with economic development, and the incubator company with financial returns. The other actors, the academia, are rewarded through technology licensing. Importantly, the design reduces information asymmetry between the large firm and the independent new ventures, as well as increases cultural fit. In turn, this may result in faster exit and higher ROI. Moreover, transaction costs can thus be significantly reduced, and the target scientific and technological landscape can be scouted more efficiently. Sharing upfront risk can be particularly attractive for assessing the value potential of radical innovations. In the pharmaceutical field, this translates into incremental innovation projects (small molecules, biologics), radical innovation projects (emerging technologies such as therapeutic stem cells, gene therapy, siRNA, miRNA, or therapeutic vaccines, as well as heretofore undruggable targets), and convergence innovation (e.g., personalized medicines). In the chemical field, this design could be useful for example to pursue the development of novel polymers, or of novel processes to manufacture renewable chemicals, fuels, and materials. In the energy field, it could be useful to promote the development of, for example, more efficient batteries, or solar energy capture technologies. Notably, the design implemented in syndicate innovation venturing allows to some extent resolution of the dilemma that typically exists between the time it takes to develop an emerging technology to a suitable point of value inflexion and the expectations of financial investors. Indeed, the risk sharing structure here enables interested venture capital firms to enter into superior Series A, financed appropriately to reach an attractive exit point rather than a “bridge to nowhere”, since the additional information gained during this initial stage of early projects reduces both technology risks and moral hazards, given that both technologies and management teams can be tested in conditions where risks are shared without a symmetrical impact on the payout. Furthermore, exit can be facilitated for example via acquisition by the big Pharma member of the syndicate. What is more, a portfolio approach remains possible to build long- and short-term value; in healthcare for example this can be achieved by carrying out both pre-clinical and clinical projects.

The key challenge here is to balance influence and independence, reach early on clarity on strategy, align divergent incentives, and define upfront the endgame for each of the parties. This is implemented by the parties being motivated by a common interest and being rewarded with different “currencies” at the endgame. Perhaps even more so than in any other alliance, a key enabler is excellence in alliance management and in communication skills in addition to expert-level business and scientific competences. The general approach here is for the large firm to reactively work with incubator companies to capture commercial outcomes of strategic interest. To this end, and given the involvement of various levels of networks, the model builds on four important drivers of innovation: (1) R&D intensity (increasing funding and networking), (2) de-risking (leveraging efficiently collective wisdom), (3) serendipity (multiplexing), and (4) creativity (brainstorming).

4. Initial Testing

Implementation hurdles of the model of syndicated innovation venturing comprise visibility as it relates to deal flow, quality of the incubator company and of its start-ups that will act also as beacons of visibility to attract high value potential business plans, local total factor productivity, project selection, entrepreneur and human resources recruitment, financing, ability to softly influence deal flow towards what is relevant to the large firm, operational management, as well as the appetite of local actors to attract external funds. Optimally, to make the most efficient use of the monies invested and thus to maximise returns, the syndicate should utilize existing infrastructures, including management, laboratory space, local venture finance environment, and underused intellectual capital. As a result, the geographic choice is a critical one. Notably, barriers to entry and market distortions can be leveraged to efficiently attract best-in-class start-ups in a given environment (

Box 2).

Box 2. Optimal locations of incubators for syndicated innovation venturing.

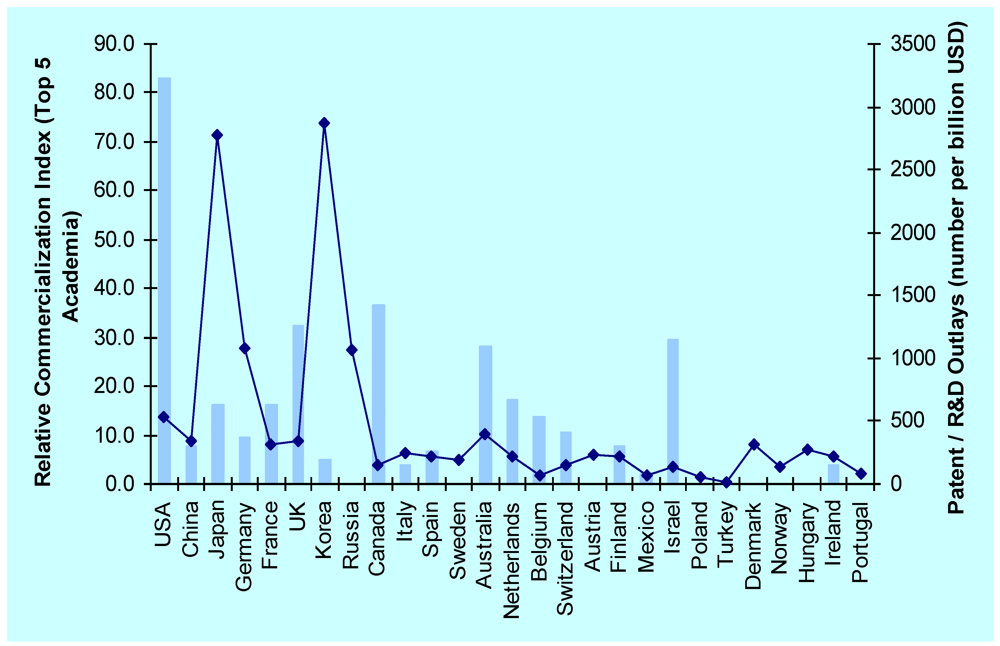

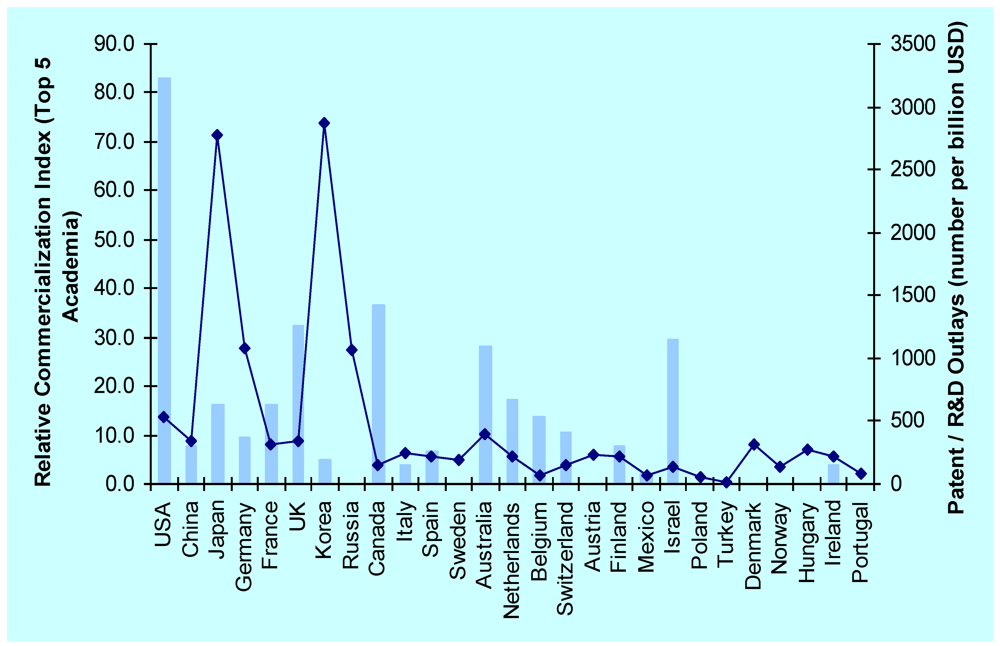

The geographic location for implementing syndicated innovation venturing should be made based on market distortions that the syndicate can successfully address to its advantage for maximising returns. These can be identified using a series of macroeconomic indicators, as follows: global trends in R&D intensity [

51] (well funded regions have high total factor productivity and harbor scientific excellence in the form of blue chip or niche academic institutions; in these regions, arbitrage opportunities and higher appetite for funding may exist in conditions of restricted access to capital, likewise in hubs of immature markets with strong growth potential), scientific publication indices per R&D outlays, patent productivity (number of triadic patent families per R&D outlays), nascent and established entrepreneurship trends, venture capital investment

vs. patent productivity, access to foreign directed investments

vs. patent productivity, country competitiveness, revenues and number of employees per sector, patent commercialization indices

vs. patents per R&D outlays. A detailed review of these indicators is beyond the scope of this paper. The indicators presented in

Figure 2 suggest for example that Japan and Korea constitute countries with possible arbitrage opportunities for accessing valuable IP considering the relative scarcity of venture capital available in these countries despite their scientific excellence. Using instead as key indicator that of R&D intensity that impacts total factor productivity, Israel with its 4.5% of GDP invested in R&D in 2007 [

51] represents a different case of market distortion where the syndicate innovation venturing design could also be maximised as compared to other locations.

Figure 2.

Biotechnology patent commercialisation. Composite index 2000–2004. Source: GDP from International Energy Agency; Patent number estimates from R&D Magazine; Biotechnology patent commercialization rankings from the Milken Institute. Bars: country relative publication index of its top five academia; line: patents / national R&D outlays.

Figure 2.

Biotechnology patent commercialisation. Composite index 2000–2004. Source: GDP from International Energy Agency; Patent number estimates from R&D Magazine; Biotechnology patent commercialization rankings from the Milken Institute. Bars: country relative publication index of its top five academia; line: patents / national R&D outlays.

Roche implemented such experiments in 2009 by partnering with Pontifax, an Israel-based venture capital fund with links to Teva investing in Israel’s life science sector, to focus on seed-stage companies and later-stage companies, and with b3Bio, a North Carolina-based biotech housed by the Hamner Institute for Health Sciences, a not-for-profit research organisation. Israel is an attractive location for testing this model, given the outstanding R&D investment made by this country that reached 4.5% of GDP in 2007 [

51], its R&D incentives, relatively low level of foreign directed investment and investment from Western funds, the high publication index of its top academia, and relatively high patent commercialisation index (

Figure 2). Likewise, in the USA, North Carolina [

52] and New York among others harbour top research institutions, and implement efforts to develop the necessary clustering framework for biotechnology start-ups to flourish, including tax incentives, loans, grants, and state-of-the-art biotechnology incubators such as New York’s East River Science Park.

Under the agreement with Roche, Pontifax, using its leverage brought by a deep knowledge of the local culture and networks, mines Israeli innovation based on a confidential list of key areas of interest to Roche. The selected start-ups are incubated in an incubator affiliated with Pontifax, and Roche and Pontifax co-invest. A key success factor here is Pontifax’s hands-on management oversight. These joint investments are complemented with funding derived from Israel’s incubator program [

53]. In addition, Pontifax leads a process of identifying established biotechnology companies that are of potential strategic interest to Roche. Notably, within a year of the implementation of the agreement, four new ventures have been created stemming from investments by the incubator company Biomedix, Pontifax, and Roche that invested $0.25m in each (Biovent Ltd., $1.2m on aggregate to develop aptamers against the flu virus; siRNA Gagomers, $1m to develop siRNA delivery technologies; Anti SRB1, $0.5m to develop anti-SRB1 monoclonal antibodies for the treatment of inflammatory bowel diseases; and cCAM, $1.1m to develop monoclonal antibodies against a tumor cell protein) [

54]. Similarly, b3Bio builds on its network of university contacts and business experience to bring a variety of projects to a concept demonstration point in an effort to “bridge the chasm between academic’s scientific breakthroughs and the point at which the technology’s commercial potential is proven” [

55]. As part of the agreement, Roche has made an equity investment in b3Bio, and pays to buy and develop the technologies in exchange for rights to test and commercialise them. Here again, the partnership establishes for Roche a direct pipeline to an outside incubator. These initial experiments seem successful as the company is considering forming similar partnerships in other US states, as well as in Europe and China [

56]. Japan, with its tradition of innovation excellence but relatively dormant venture capital industry and start-up ecosystem represents another region where this concept could be implemented with good return potentials. From a technology point of view, in addition to the technology of siRNA that initially generated a surge of interest and investment from big Pharma, only to fall back shortly thereafter [

57] thus illustrating the difficulty of large corporations to deploy radical innovation [

58], the development and deployment of the therapeutic stem cells technology could perhaps be dramatically accelerated also through syndicated innovation venturing, as suggested by the low level of venture capital transactions in the latter technology during the 2-year period 2009–2010 [

59] (nine stem cell deals, of which five therapeutic, representing $161.7m, as compared to 65 deals implemented during the same period in oncology representing $1,316.2m).

5. Conclusions

Initial tests of syndicate innovation venturing suggests the model functions since mini-innovation value chains can thus efficiently and swiftly be created that involve in joint projects parties which neither compete with one another nor would otherwise necessarily collaborate. Importantly, incentives are aligned while each party is rewarded in a manner that does not involve zero-sum games at project completion since each party is unlikely to increase its profit by unilaterally changing its syndicate strategy. As demonstrated by the Roche-Pontifax strategic partnership, this venturing model represents an instrument that enables a large firm to benefit from large open networks to access scientific excellence and valuable academia-generated technology while facilitating investment decisions in areas of high perceived technology risk. This is enabled not only by risk sharing or by relaxing resource constraints such as financial ones, but also by relaxing psychological constraints such as the internal exposure to credibility risk of the project champions who venture into scientific terra incognita, and doing so without compromising control or decision quality. Markedly, while the ultimate success of the start-ups cannot yet be quantitated as depending to a great extent on biological reality in addition to business, scientific, and implementation excellence (parameters that are only answered over time), the first measure of four new ventures created within a year is a very positive one.

The value of open networks to access innovative products has previously been demonstrated in the market by various corporate initiatives, such as the

Connect + Develop program of P&G [

16,

29]. Notably, operational risks can be reduced to a great extent, thus enabling a large firm to assess early a large technology portfolio, comprising radical innovation. Practically, what is gained by the large firm, beyond technology awareness and enriched networks, is a privileged access to start-ups that develop and control strategic assets prior to their value inflexion points. Furthermore, this can be formalised by a variety of rights and options, such as the first right to negotiate, to ensure early communication when the resulting start-ups reach the partnering stage. It is important to emphasise here that these rights should be designed so that the drive and incentives to innovate of the entrepreneurs and scientists of the portfolio start-ups are not diminished. Remarkably, projects followed are in full congruence with the large firm’s strategy, since the VC and incubator partners are softly incentivised to pursue strategic assets (cf.

Figure 1 and

Box 1). Critical factors for the syndicate to remain effective in its filtering of business plan proposals are on the one hand the ability to attract superior business proposals and on the other hand a high decision quality. These are reinforced by the careful choice of geographic implantation and robust venture project selection processes involving more than one scientific or business hurdle. The indirect access to an open pool of entrepreneurs is important to build networks for information access, since brute force alone would not be sufficient. The contribution and fair reward of academia that have developed the underlying IP also is essential; this is typically achieved in the first instance by licensing agreements directly with the start-up companies.

Translating the selected strategy into simple actionable plans, implementing projects, and realising value at the medium-term (3–5 years) to de-risk high potential technologies, such as disruptive innovation, are only a first step. Indeed, gaining technology options or overcoming barriers to entry in a particular geographic or technological domain represent just the visible part of the upside. The second aim, perhaps even more significant, is that the large firm, the VC/incubator, and the public institute can thereby efficiently monitor technological frontiers and trajectories of technological development, such as to better prepare for their respective future challenges.

{kind=link}

{kind=link}