Helping Agribusinesses—Small Millets Value Chain—To Grow in India

Abstract

:1. Introduction

2. Theoretical Framework and Methodology

3. Results and Discussion

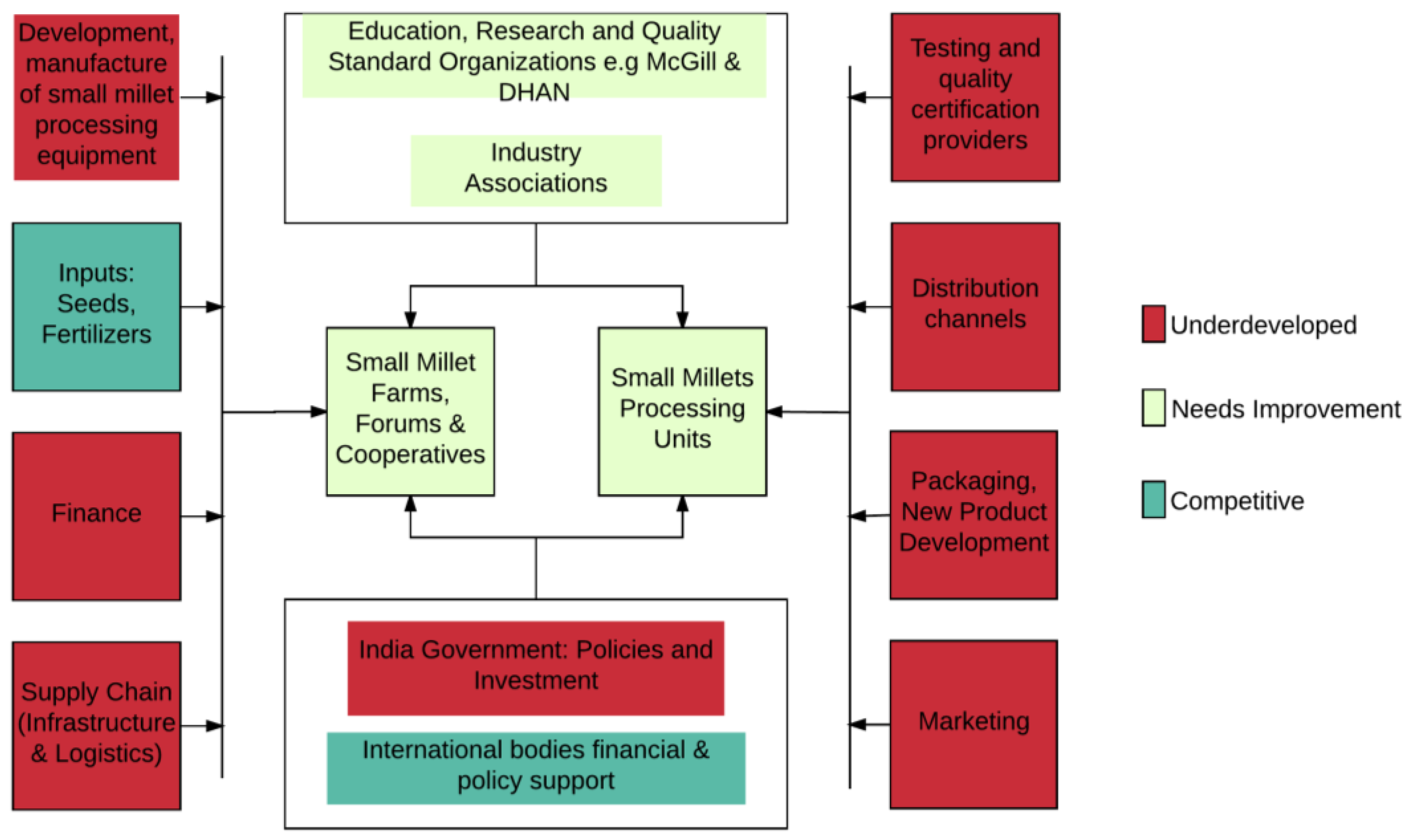

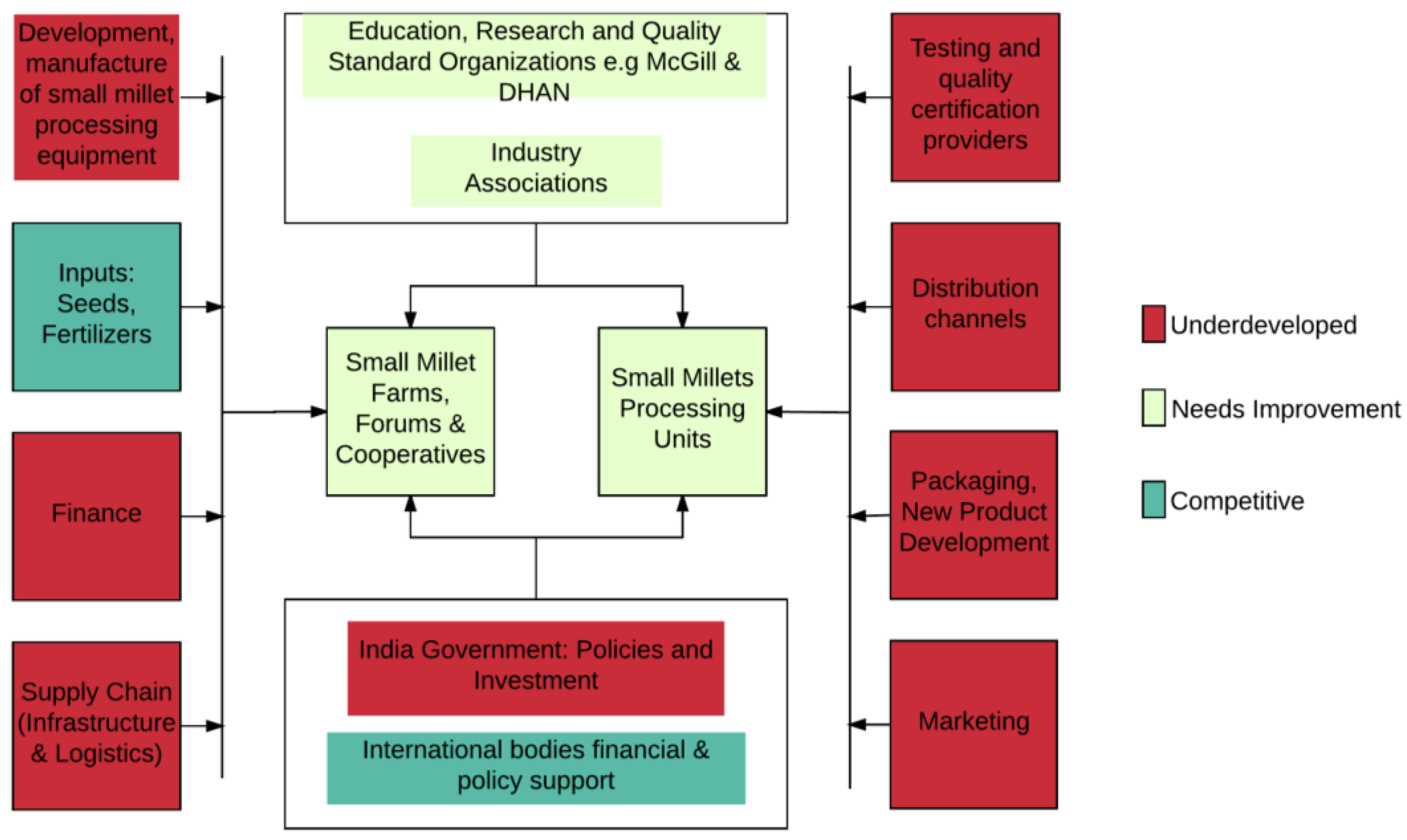

3.1. Value Chain Analysis

- (a)

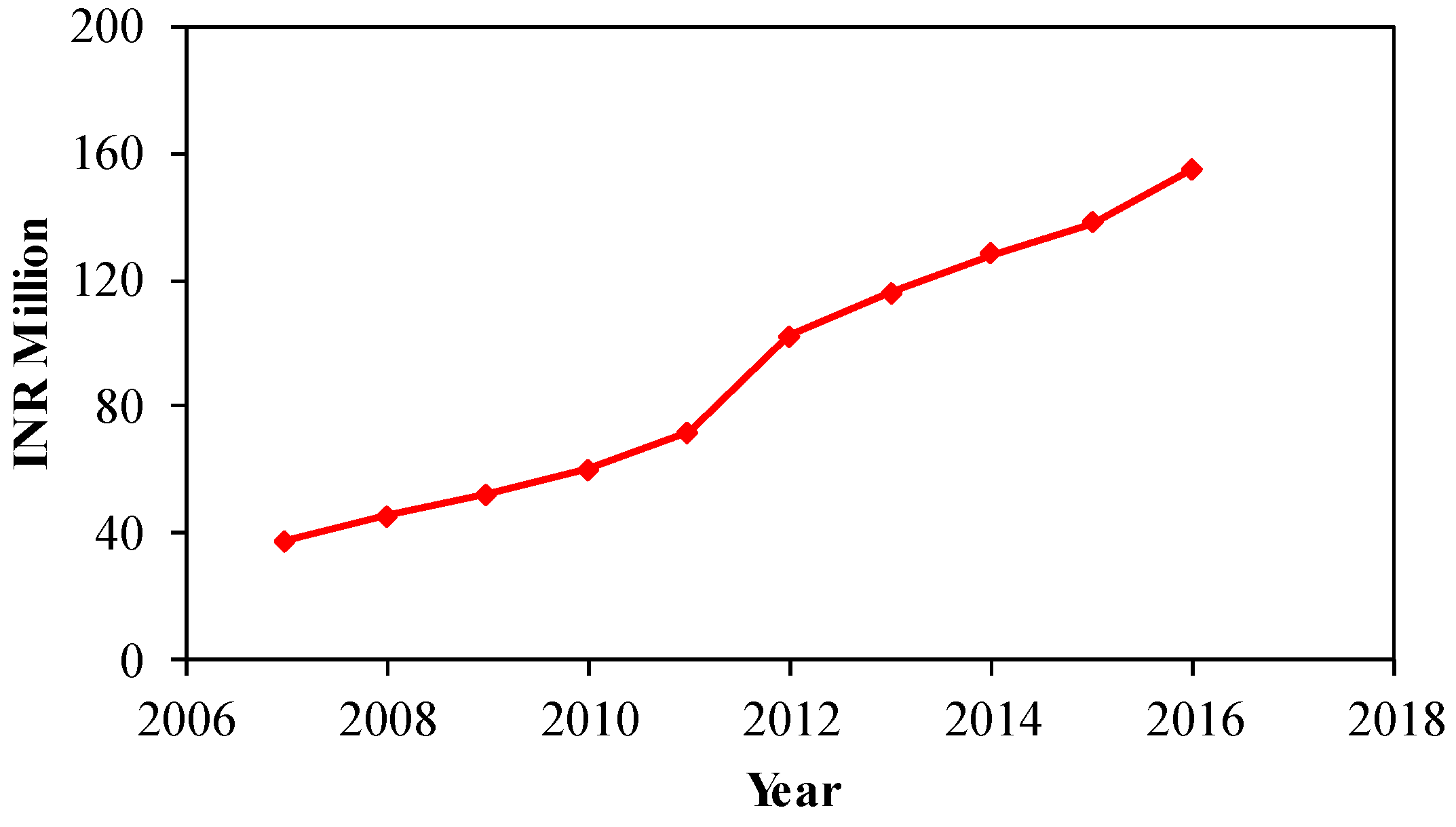

- Weak Supply Chain: Unlike rice and wheat, there has been dwindling development of the supply chain, especially as it relates to support for growers, traders, marketers, subsidiaries, and processors to ensure speed and smoothness. Several cases of intermediaries’ exploitations are documented online. Therefore, cost components continue to increase. For example, according to the manufacturers, middlemen can increase the cost component by up to 40%.

- (b)

- Customer Awareness: In addition, customer awareness of the better nutritional value of millets, as well as the ability to evaluate quality, is inadequate or practically nonexistent. Customers do not buy what they do not know about. Most of the current customer awareness about millets consists of word of mouth information, or informal discussions on its potential nutritional benefits. However, based on nutritional discussions during the customer preference survey, at least 50% of non-consumers of millets indicated an interest in purchasing them.

- (c)

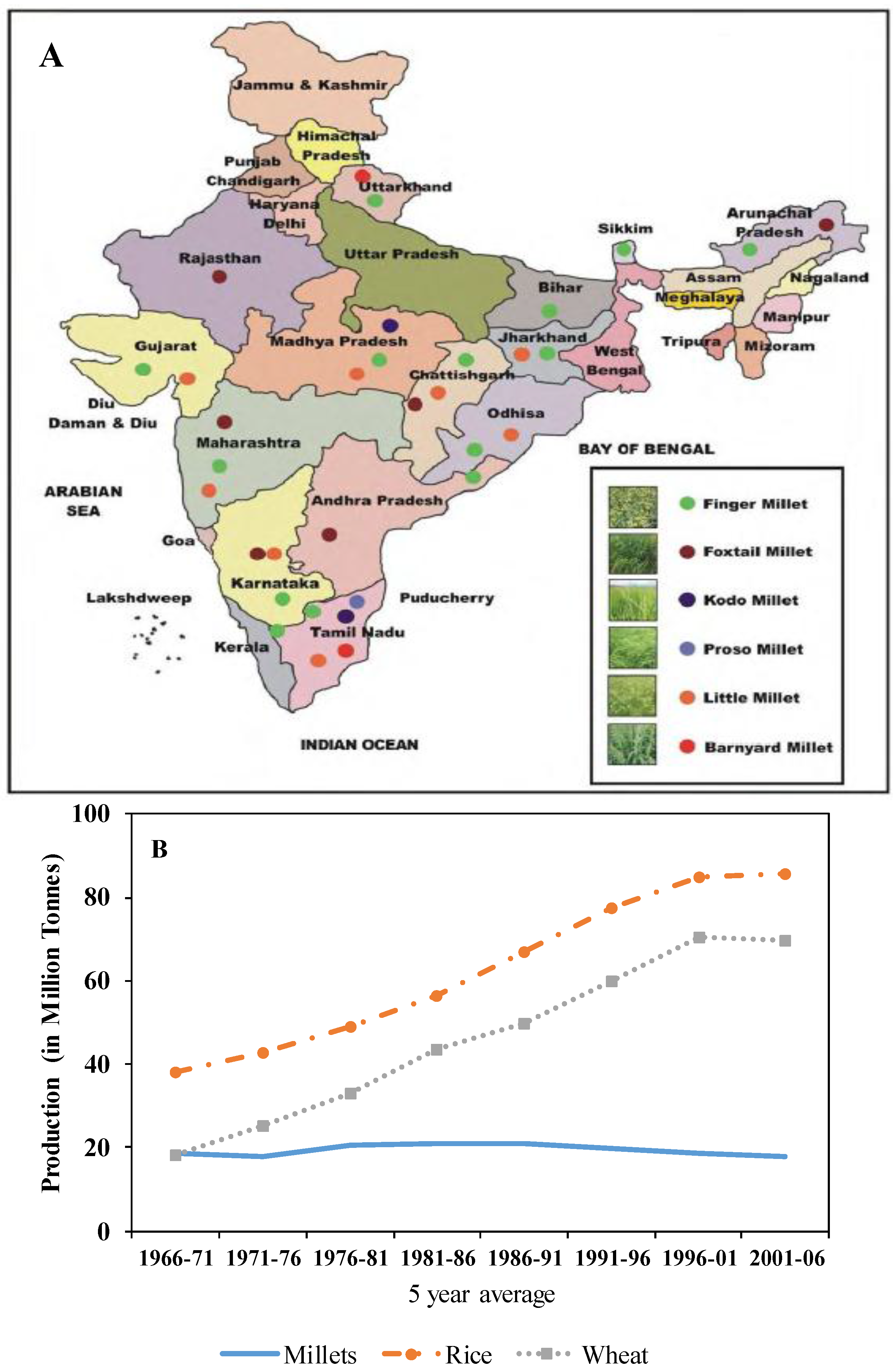

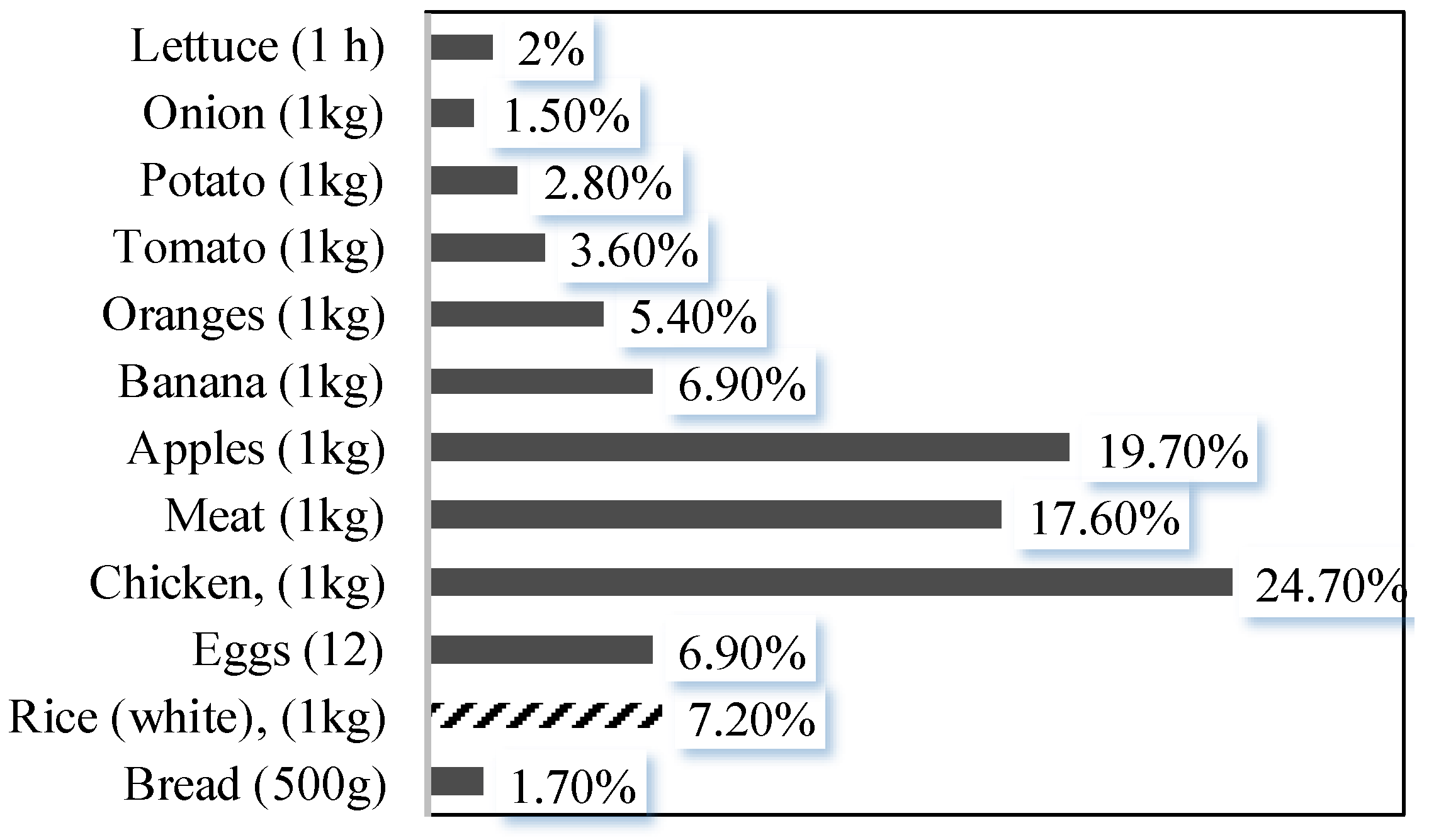

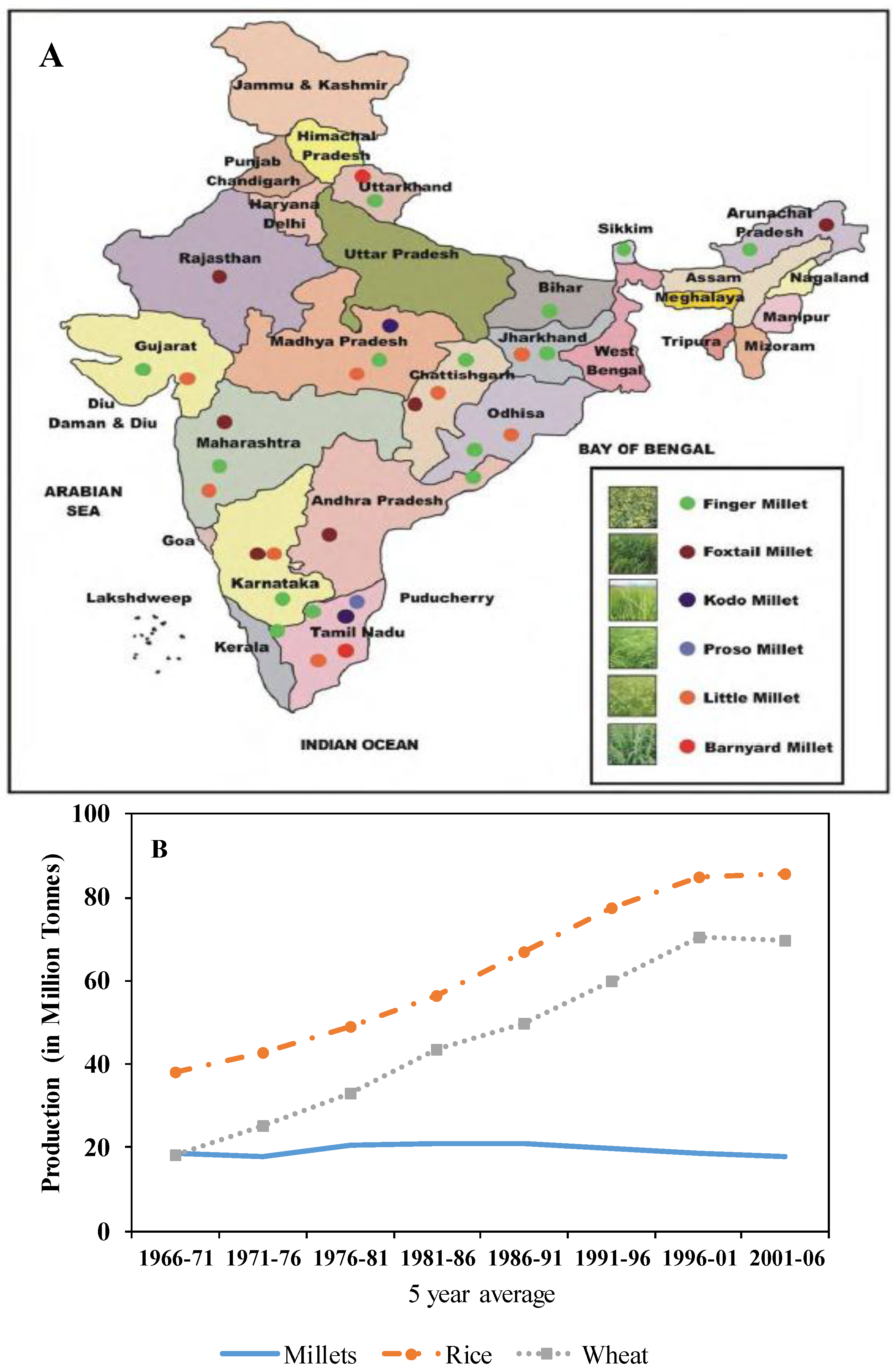

- Poor Yields: Average yields are still quite low [2]. Annual yields of 4–5 quintals as opposed to 20–25 quintals of rice, 18–20 quintals of wheat, and 25–30 quintals of maize are also drivers of the disparity in price and acceptability. Although, when juxtaposed with other factors, small millets have a better yield potential, since they require less area than rice, for example, and can grow in less fertile soils.

- (d)

- Inadequate or Inefficient Processing Facilities: Based on technical meetings and reports reviewed, innovation is a major stumbling block. The feedback loop needed to improve on innovation, development, and use, while reducing drudgery is absent. With a general 60–65% recovery rate during processing, the “un-exploration” of by-products also contributes to the higher final selling price.

- (e)

- Floundering Policy: After the Green Revolution, the policymakers in India have supported the production of intensive crops in more choice resource areas [19], contributing to the decline of millets (although millets require less cultivation area). Another example is that the Indian Public Distribution System (PDS) in 2017 did not include small millets.

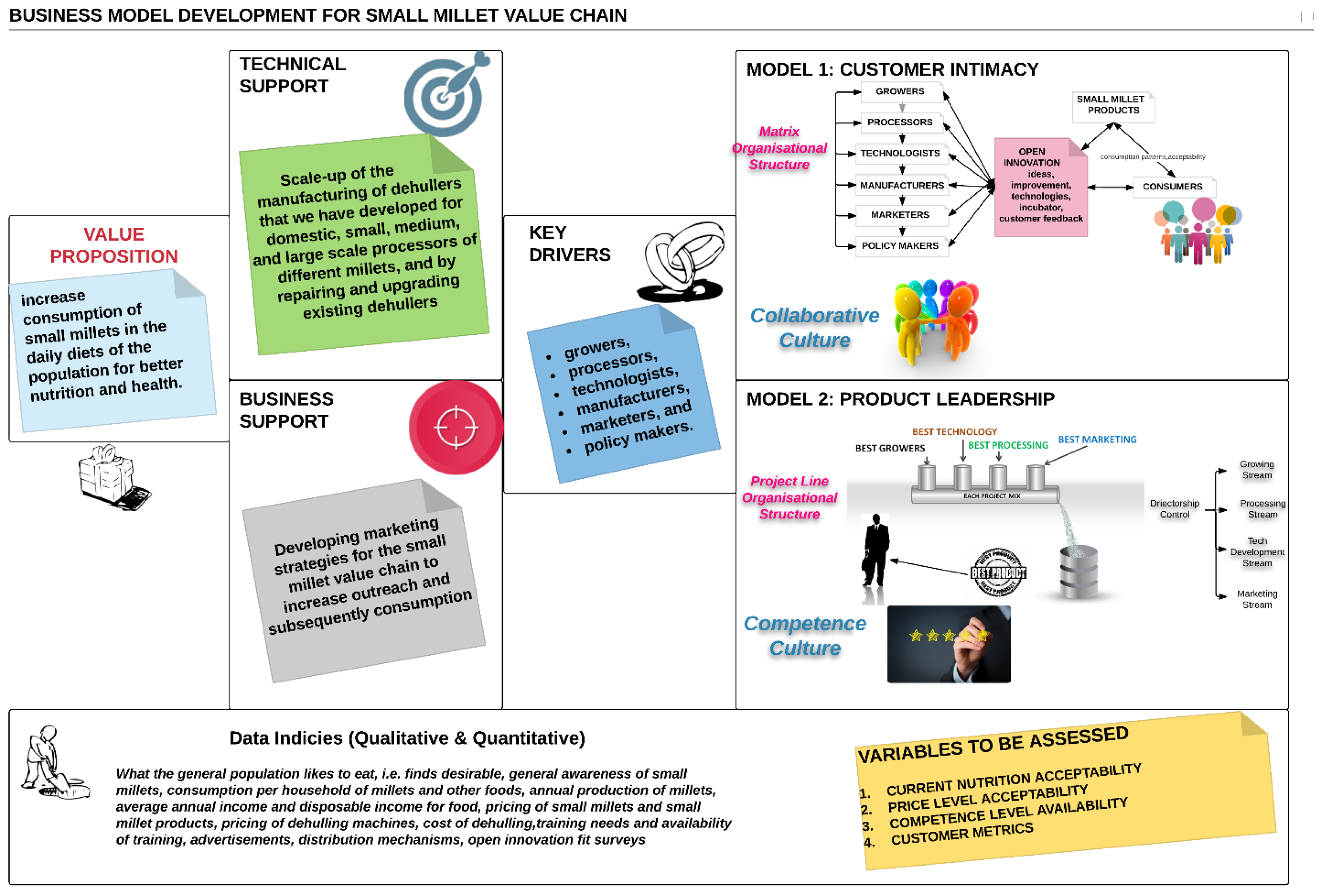

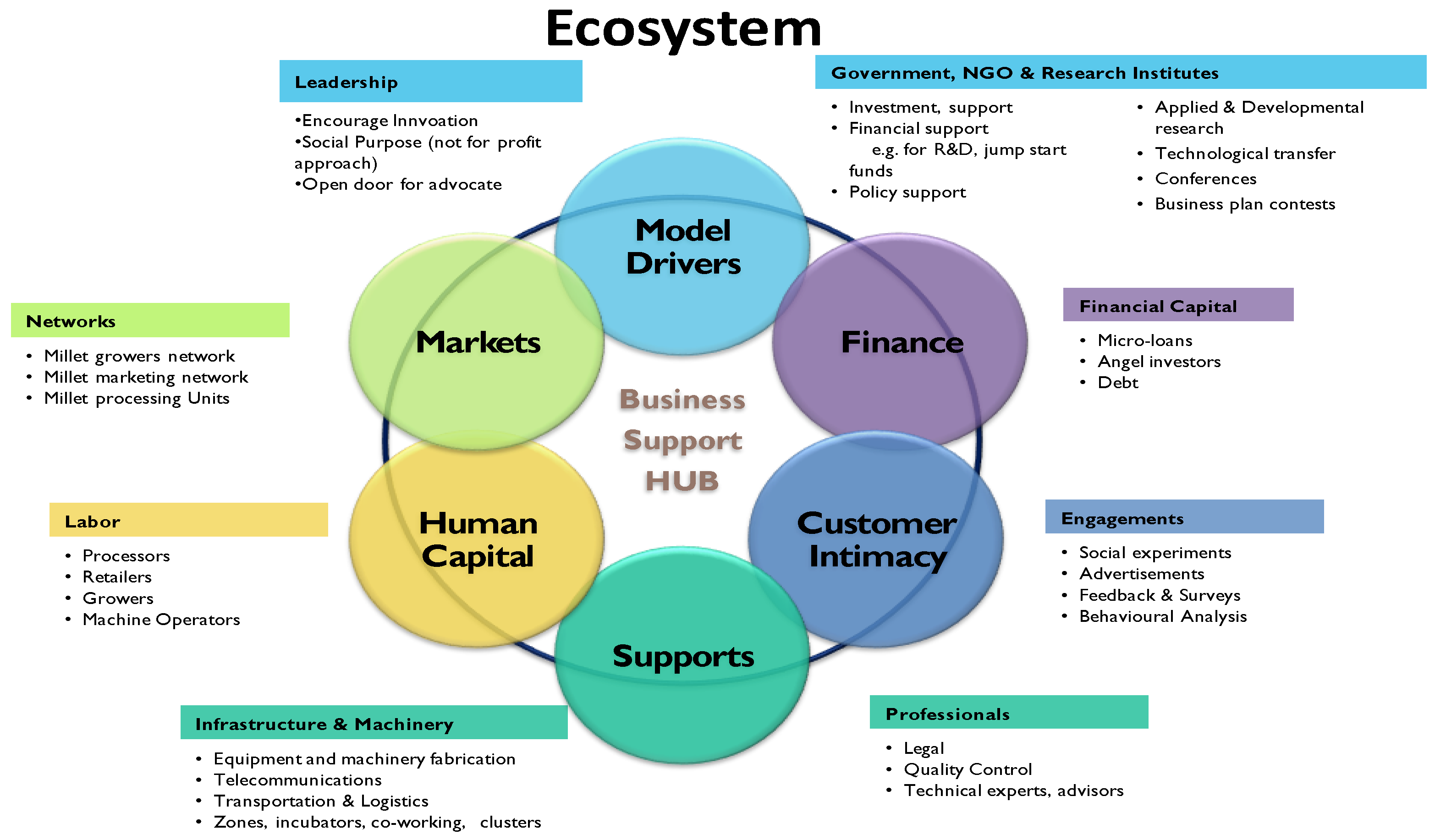

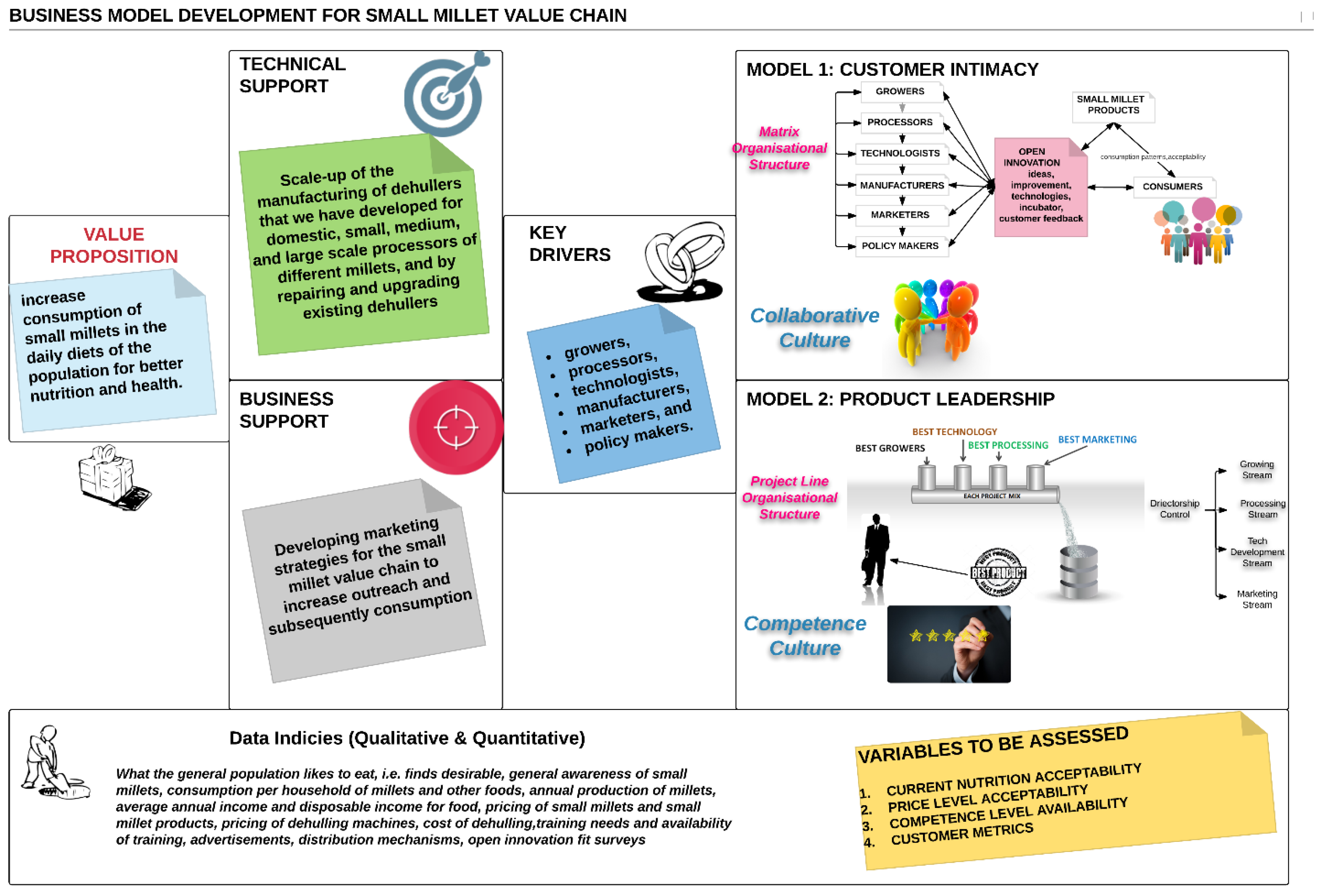

3.2. Business Model Development

Implementation of the Open Innovation-Driven Customer Intimacy Model for the Small Millets Value Chain

- Acquisition and sharing of internal knowledge from the major players in the small millets industry.

- Acquisition of external knowledge about the customer and the small millets industry.

- Improvement of the working relationships between the different components of the small millets cluster group.

3.3. Supporting Cases

3.4. Marketing Plan

4. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Nagarajan, L.; Smale, M. Village seed systems and the biological diversity of millet crops in marginal environments of India. Euphytica 2007, 155, 167–182. [Google Scholar] [CrossRef]

- ICAR. Small Millets in India: Current Status and Future Thrusts. Available online: http://www.webcitation.org/6wqP2vp1I (accessed on 7 October 2017).

- Factbook, C. The World Factbook. Available online: https://www.cia.gov/library/publications/the-world-factbook (accessed on 2 December 2018).

- Shahidi, F.; Chandrasekara, A. Millet grain phenolics and their role in disease risk reduction and health promotion: A review. J. Funct. Foods 2013, 5, 570–581. [Google Scholar] [CrossRef]

- Annor, G.A.; Tyl, C.; Marcone, M.; Ragaee, S.; Marti, A. Why do millets have slower starch and protein digestibility than other cereals? Trends Food Sci. Technol. 2017, 66, 73–83. [Google Scholar] [CrossRef]

- McSweeney, M.B.; Ferenc, A.; Smolkova, K.; Lazier, A.; Tucker, A.; Seetharaman, K.; Ramdath, D.D. Glycaemic response of proso millet-based (Panicum miliaceum) products. Int. J. Food Sci. Nutr. 2017, 68, 873–880. [Google Scholar] [CrossRef] [PubMed]

- Ugare, R.; Chimmad, B.; Naik, R.; Bharati, P.; Itagi, S. Glycemic index and significance of barnyard millet (Echinochloa frumentacae) in type II diabetics. J. Food Sci. Technol. 2014, 51, 392–395. [Google Scholar] [CrossRef] [PubMed]

- Jain, N.; Arora, P.; Tomer, R.; Mishra, S.V.; Bhatia, A.; Pathak, H.; Chakraborty, D.; Kumar, V.; Dubey, D.S.; Harit, R.C.; et al. Greenhouse gases emission from soils under major crops in Northwest India. Sci. Total Environ. 2016, 542, 551–561. [Google Scholar] [CrossRef] [PubMed]

- Mohan, V.; Radhika, G.; Sathya, R.M.; Tamil, S.R.; Ganesan, A.; Sudha, V. Dietary carbohydrates, glycaemic load, food groups and newly detected type 2 diabetes among urban Asian Indian population in Chennai, India (Chennai Urban Rural Epidemiology Study 59). Br. J. Nutr. 2009, 102, 1498–1506. [Google Scholar] [CrossRef] [PubMed]

- Kalra, S.; Unnikrishnan, A. Obesity in India: The weight of the nation. J. Med. Nutr. Nutraceut. 2012, 1, 37–41. [Google Scholar] [CrossRef]

- Vetter, S.H.; Sapkota, T.B.; Hillier, J.; Stirling, C.M.; Macdiarmid, J.I.; Aleksandrowicz, L.; Smith, P. Greenhouse gas emissions from agricultural food production to supply Indian diets: Implications for climate change mitigation. Agric. Ecosyst. Environ. 2017, 237, 234–241. [Google Scholar] [CrossRef] [PubMed]

- Osterwalder, A.; Pigneur, Y.; Tucci, C.L. Clarifying business models: Origins, present, and future of the concept. Commun. Assoc. Inf. Syst. 2005, 16, 1. [Google Scholar]

- Osterwalder, A. The Business Model Ontology: A Proposition in a Design Science Approach. Available online: http://www.hec.unil.ch/aosterwa/PhD/1.pdf (accessed on 10 June 2017).

- Economics, I. India Disposable Income. 2017. Available online: https://ieconomics.com/edit/india-disposable-personal-income (accessed on 10 June 2017).

- Times, H. Average Indian’s Monthly Expense: 40% on Food, 4% on Education. 2016. Available online: https://www.hindustantimes.com/union-budget/average-indian-s-monthly-expense-40-on-food-4-on-education/story-4ivqPm7vTX6uR65J90tdoL.html (accessed on 2 October 2017).

- Chen, S.E.; Liu, J.; Binkley, J.K. An exploration of the relationship between income and eating behavior. Agric. Resour. Econ. Rev. 2012, 41, 82–91. [Google Scholar] [CrossRef]

- Raghavan, V. Millets–Shrouded Gold. 2017. Available online: http://www.dhan.org/smallmillets2/file/Dr.Vijaya-Raghavan.pdf. (accessed on 2 October 2017).

- Numbeo. Food Prices in India. 2017. Available online: http://www.webcitation.org/6wqPvwnVZ (accessed on 6 May 2017).

- Deccan Development Society; Food First Information and Action Network (FIAN). Millets: Future of Food & Farming. Available online: http://www.webcitation.org/6wqQcXsLC (accessed on 15 February 2018).

- Adekunle, A.; Osazuwa, P.; Raghavan, V. Socio-economic determinants of agricultural mechanisation in Africa: A research note based on cassava cultivation mechanisation. Technol. Forecast. Soc. Chang. 2016, 112, 313–319. [Google Scholar] [CrossRef]

- Christensen, J.F.; Olesen, M.H.; Kjær, J.S. The industrial dynamics of Open Innovation—Evidence from the transformation of consumer electronics. Res. Policy 2005, 34, 1533–1549. [Google Scholar] [CrossRef]

- King, A.; Lakhani, K.R. Using open innovation to identify the best ideas. MIT Sloan Manag. Rev. 2013, 55, 41. [Google Scholar]

- Dries, L.; Pascucci, S.; Török, Á.; Tóth, J. Open innovation: A case—Study of the Hungarian wine sector. EuroChoices 2013, 12, 53–59. [Google Scholar] [CrossRef]

- Connecticut General Assembly (CGA). The CGA Story. Available online: http://www.webcitation.org/6xCmpy6rM (accessed on 10 February 2018).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Tasks | Timeline |

|---|---|

| Stage 1 (Initiation): Determination of the direction and responsibility of each of the components in the small millets cluster. Redefinition of achievable goals on a 5-year scale. Discussion/resolution of concerns and potential problems. | 1 year |

| Stage 2 (Engagement): Stakeholders engagement for determining the need & feasibility of innovations in their sector as well for other drivers in the ecosystem within the cluster. | 1 year (concurrent with stage 1) |

| Stage 3 (Monitoring): Development of a feedback loop for sharing information within the small millets value chain cluster. Performance assessment Information review | Continuous |

| Stage 4 (Continuous Improvement): Incubator organization support adjustments Review and modify information sharing loops, policies, and procedures. Analyze feedback, more surveys to access success within the small millets value chain (mostly with reach and sales). Market & Customer Surveys | Continuous |

| Item | Actions |

|---|---|

| Nutritional awareness drive of the small millets value chain and methods of sales amongst the Indian populace | Capitalize on the healthy drive around the world Health Rallies Free giveaways at clinics as alternatives to prevent diagnosis or prognosis |

| Intense Advertising | Social media: Food challenges, hashtags, promotions on Twitter®, Facebook®, Instagram®, and Snapchat® Cooking Competitions Sales Kiosks Tricycle Branding Posters Special Millet Carts for value-added products Occasional TV adverts |

| Educational and Policy Drives (Campaign policy makers and the customer) | Capitalize on the wave of concerns about climate change Emphasize the effects of intensive farming |

| New Product Development | Develop easy-to-use derivatives |

| Product Packaging Rebranding | Surveys to determine the best size, style, acceptable price range (needed) |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Adekunle, A.; Lyew, D.; Orsat, V.; Raghavan, V. Helping Agribusinesses—Small Millets Value Chain—To Grow in India. Agriculture 2018, 8, 44. https://doi.org/10.3390/agriculture8030044

Adekunle A, Lyew D, Orsat V, Raghavan V. Helping Agribusinesses—Small Millets Value Chain—To Grow in India. Agriculture. 2018; 8(3):44. https://doi.org/10.3390/agriculture8030044

Chicago/Turabian StyleAdekunle, Ademola, Darwin Lyew, Valérie Orsat, and Vijaya Raghavan. 2018. "Helping Agribusinesses—Small Millets Value Chain—To Grow in India" Agriculture 8, no. 3: 44. https://doi.org/10.3390/agriculture8030044

APA StyleAdekunle, A., Lyew, D., Orsat, V., & Raghavan, V. (2018). Helping Agribusinesses—Small Millets Value Chain—To Grow in India. Agriculture, 8(3), 44. https://doi.org/10.3390/agriculture8030044