Problems and Opportunities within the Wine Industry in Terms of the COVID-19 Pandemic

Abstract

1. Introduction

2. Materials and Methods

- -

- Five collections of wine: vinum bozen, prediction, prestige, oak wood, and gold prestige;

- -

- Liqueur wines;

- -

- Noble wine distillates, such as brandy;

- -

- Juices of 100% natural origin and must;

- -

- Frozen 100% grape juice;

- -

- New half-fermented wine;

- -

- Other seasonal products.

3. Results

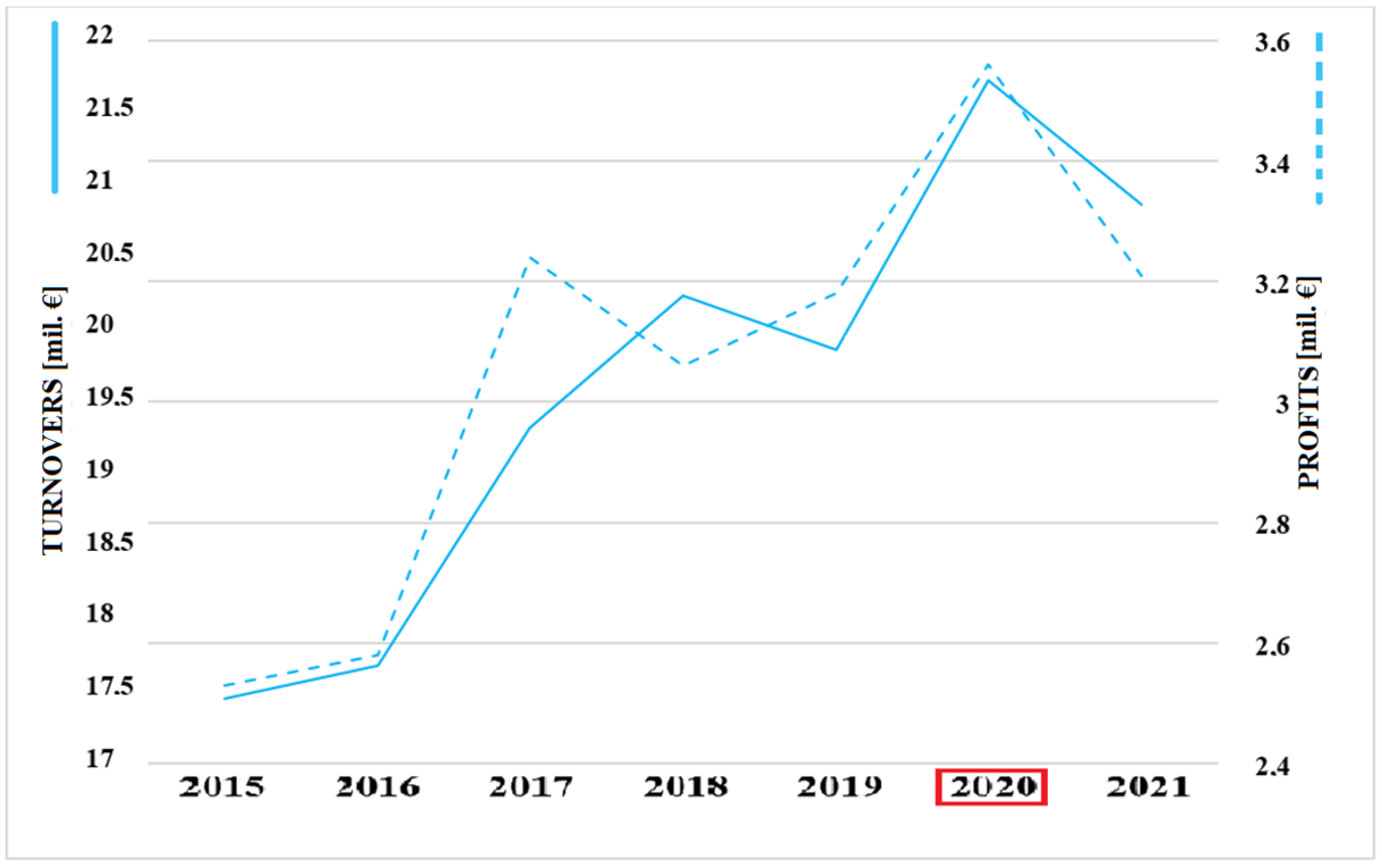

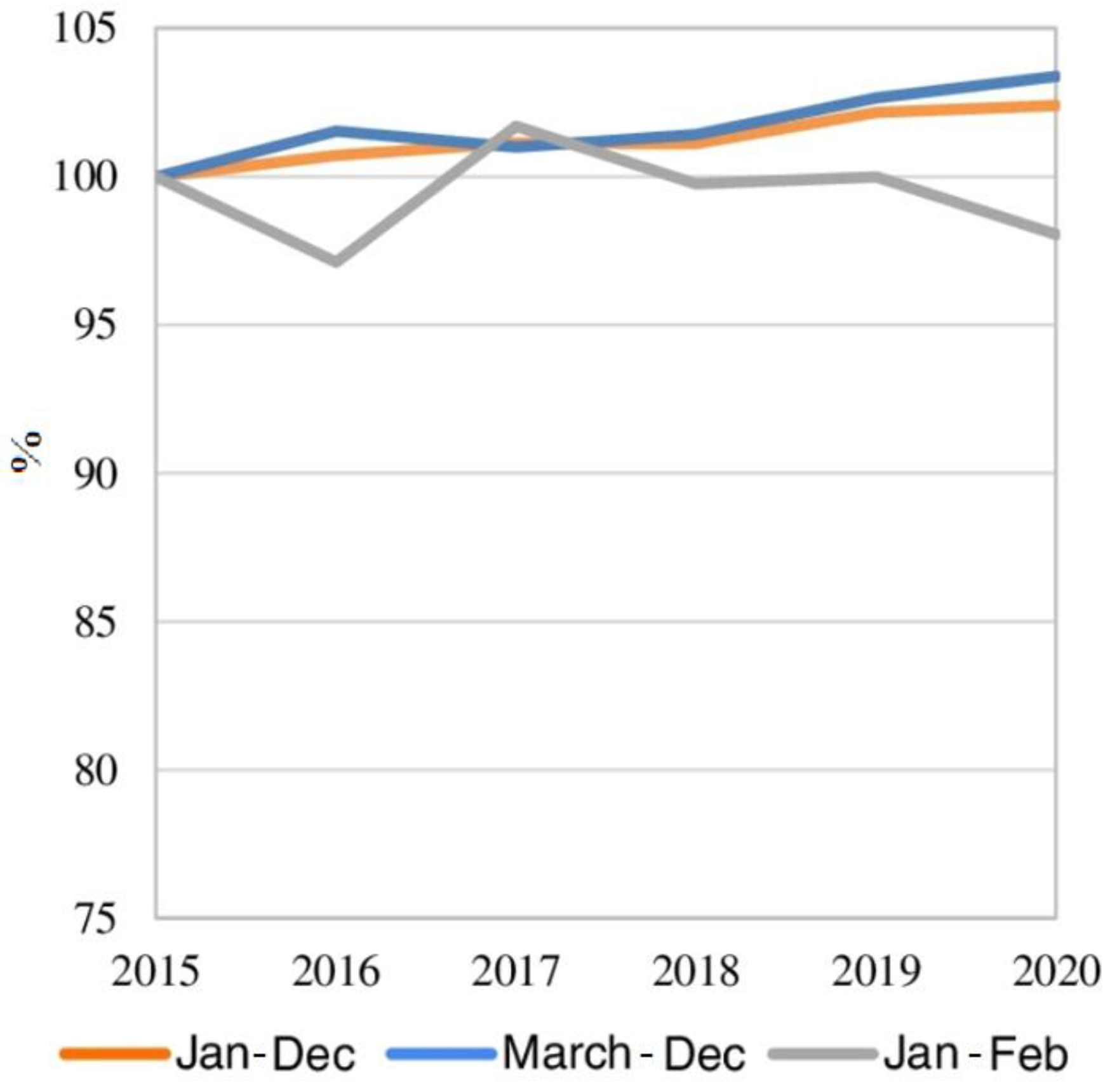

3.1. Changes in Company V Due to the COVID-19 Pandemic

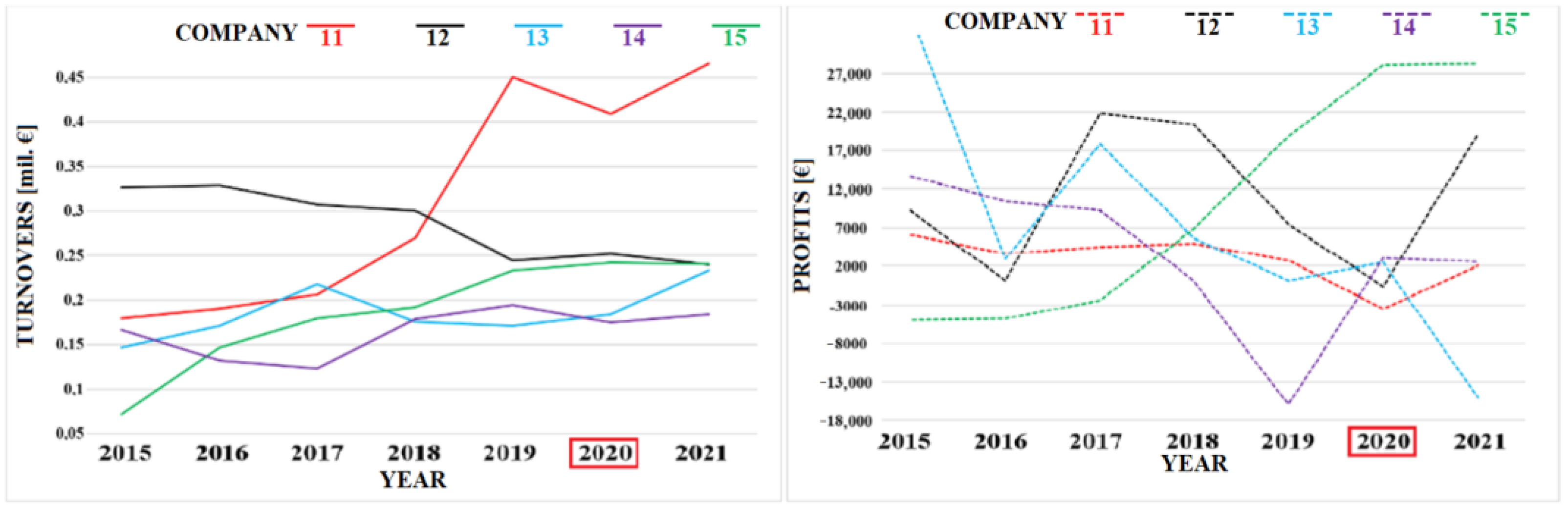

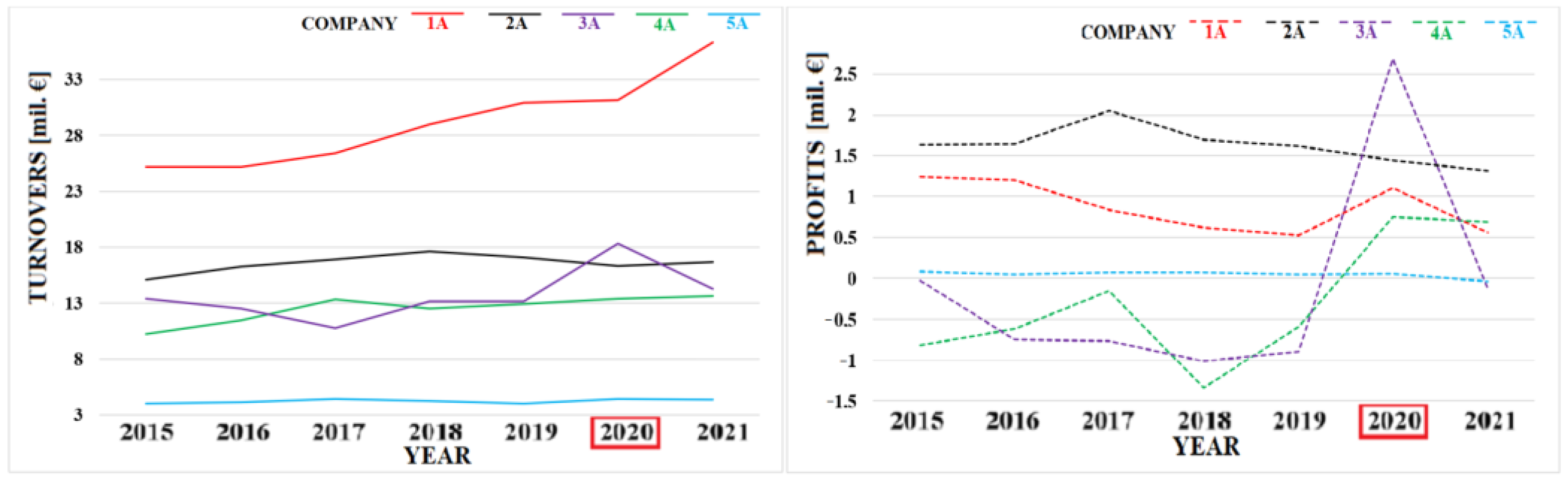

3.2. Comparison of the Changes in Company V with Selected Wine Companies

3.3. Information on Company V and the COVID-19 Pandemic Based on the Interview

3.3.1. Covering the Market in Terms of Geography and Suppliers and the Change Due to COVID-19

3.3.2. Delivery Logistics and the Change Due to COVID-19

3.3.3. Demand and the Change Due to COVID-19

3.3.4. Emergence of New Branches and Their Operation during the Pandemic

- -

- Entering the store being permitted only for customers with face masks (surgical or respirators according to the rules);

- -

- Keeping the minimum distance of 2 m between persons;

- -

- Limited number of customers depending on the size of the store;

- -

- Disinfectants located at the entry;

- -

- Disinfection of objects and spaces.

3.4. The Company’s e-Shop

4. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Seville, E.; Van Opstal, D.; Vargo, J. A Primer in Resiliency: Seven Principles for Managing the Unexpected. Glob. Bus. Organ. Excell. 2015, 34, 6–18. [Google Scholar] [CrossRef]

- Slocum, S.L.; Kline, C. Regional resilience: Opportunities, challenges and policy messages from Western North Carolina. Anatolia 2014, 25, 403–416. [Google Scholar] [CrossRef]

- Carvalho, H.; Duarte, S.; Machado, V. Lean, agile, resilient and green: Divergences and synergies. Int. J. Six Sigma 2011, 2, 151–179. [Google Scholar] [CrossRef]

- Fiksel, J. Sustainability and resilience: Toward a systems approach. Sustainability: Science. Pract. Policy 2006, 2, 14–21. [Google Scholar] [CrossRef]

- Mzid, I.; Kahachlouf, N.; Soparnot, R. How does family capital influence the resilience of family firms? J. Int. Entrep. 2019, 17, 249–277. [Google Scholar] [CrossRef]

- Khan, O.; Christopher, M.; Creazza, A. Aligning product design with the supply chain: A case study. Supply Chain Manag. 2012, 17, 323–336. [Google Scholar] [CrossRef]

- Sabatino, M. Economic crisis and resilience: Resilient capacity and competitiveness of the enterprises. J. Bus. Res. 2016, 69, 1924–1927. [Google Scholar] [CrossRef]

- Miller, D.; Wright, M.; LeBreton-Miller, I.; Scholes, L. Resources and Innovation in Family Businesses: The Janus-Face of Socioemotional Preferences. Calif. Manag. Rev. 2015, 58, 20–40. [Google Scholar] [CrossRef]

- Benedek, Z.; Fertő, I.; Marreiros, C.G.; de Aguiar, P.M.; Pocol, C.B.; Čechura, L.; Põder, A.; Pääso, P.; Bakucs, Z. Farm diversification as a potential success factor for small-scale farmers constrained by COVID-related lockdown. Contributions from a survey conducted in four European countries during the first wave of COVID-19. PLoS Sustain. Transform. 2021, 16, e0251715. [Google Scholar] [CrossRef]

- Lin, X.; Hagsten, E.; Falk, M. Stock Market Performance of the US Hospitality and Tourism During the COVID-19 Pandemic. Tour. Anal. 2022, 27, 567–574. [Google Scholar] [CrossRef]

- BEYOND 2021: Key Trends Shaping the Global Wine Market. Available online: https://wineintubes.com/blogs/beyond-2021-key-trends-shaping-the-global-wine-market/ (accessed on 5 December 2022).

- Profi Press. The Pandemic has Significantly Disrupted the Wine Market. Available online: https://zemedelec.cz/pandemie-vyrazne-narusila-trh-s-vinem/ (accessed on 5 December 2022).

- Wittwer, G.; Anderson, K. COVID-19′s impact on Australian wine markets and regions. Aust. J. Agric. Resour. Econ. 2021, 65, 822–847. [Google Scholar] [CrossRef]

- Wittwer, G.; Anderson, K. COVID-19 and global beverage e-markets: Implications for wine. J. Wine Econ. 2021, 16, 117–130. [Google Scholar] [CrossRef]

- Tracy, D.; Nick, V.; Kandas, C. COVID-19 and the South African wine industry. Agrekon 2021, 61, 42–51. [Google Scholar] [CrossRef]

- Compés, R.; Faria, S.; Gonçalves, T.; Rebelo, J.; Pinilla, V.; Elorz, K.S. The shock of lockdown on the spending on wine in the Iberian market: The effects of procurement and consumption patterns. Br. Food J. 2022, 124, 1622–1640. [Google Scholar] [CrossRef]

- Rebelo, J.; Compés, R.; Faria, S.; Gonçalves, T.; Pinilla, V.; Simón-Elorz, K. COVID-19 lockdown and wine consumption frequency in Portugal and Spain. Span. J. Agric. Res. 2021, 19, e0105. [Google Scholar] [CrossRef]

- Andrieu, N.; Hossard, L.; Graveline, N.; Dugué, P.; Guerra, P.; Chirinda, N. COVID-19 management by farmers and policymakers in Burkina Faso, Colombia and France: Lessons for climate action. Agric. Syst. 2021, 190, 103092. [Google Scholar] [CrossRef]

- Lulia, R. Evolution of the wine market in Europe: Trends and barriers in the context of the COVID-19 pandemic. In Proceedings of the 17th International Conference on Business Excellence, Bucharest, Romania, 22–23 March 2023; Volume 16, pp. 918–932. [Google Scholar] [CrossRef]

- Feature: Italy Wine Industry Adapting to Pandemic, Focusing on Direct Sales, Exports, Xinhuanet. Available online: http://www.xinhuanet.com/english/europe/2021-02/18/c_139748774.htm (accessed on 6 December 2022).

- Ellyatt, H. Italy’s Winemakers Are Reeling from the Coronavirus Impact, but Hope Demand Can Bounce Back. Europe Economy. Available online: https://www.cnbc.com/2020/07/24/italian-wine-industry-reels-from-coronavirus-but-hopes-demand-returns.html (accessed on 6 December 2022).

- Carter, F. The Impact of the Pandemic on German Wine Producers. Available online: https://www.wine-business-international.com/wine/analysis/impact-pandemic-german-wine-producers (accessed on 6 December 2022).

- Wines of Germany, German Wine Market Grows in 2020. Available online: https://www.germanwines.de/aktuelles/news/details/news/detail/News/german-wine-market-grows-in-2020/ (accessed on 6 December 2022).

- Jovanovska, S.; Dimovska, A. Marketing activities and sales of Macedonian wineries in a condition of pandemic COVID-19. BH Ekon. Forum 2021, 13, 43–59. [Google Scholar] [CrossRef]

- Fuentes-Fernández, R.; Martínez-Falcó, J.; Sánchez-García, E.; Marco-Lajara, B. Does Ecological Agriculture Moderate the Relationship between Wine Tourism and Economic Performance? A Structural Equation Analys is Applied to the Ribera del Duero Wine Context. Agriculture 2022, 12, 2143. [Google Scholar] [CrossRef]

- Aleffi, C.; Tomasi, S.; Ferrara, C.; Santini, C.; Paviotti, G.; Baldoni, F.; Cavicchi, A. Universities and wineries: Supporting sustainable development in disadvantaged rural areas. Agriculture 2020, 10, 378. [Google Scholar] [CrossRef]

- Getz, D.; Carlsen, J.; Anderson, D. Critical Success Factors for Wine Tourism. Int. J. Wine Mark. 1999, 11, 20–43. [Google Scholar] [CrossRef]

- Brodge, A. Trends in wine tourism: The Fladgate group perspective. Worldw. Hosp. Tour. Themes 2017, 9, 679–684. [Google Scholar] [CrossRef]

- Kotur, A.S. A bibliometric review of research in wine tourism experiences: Insights and future research directions. Int. J. Wine Bus. Res. 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Bibiciou, S.; Cretu, R.C. Enotourism: A niche tendency within the tourism market. Sci. Pap.–Ser. Manag. Econ. Eng. Agric. Rural. Dev. 2013, 13, 31–40. [Google Scholar]

- Oltean, F.D.; Gabor, M.R. Wine Tourism—A Sustainable Management Tool for Rural Development and Vineyards: Cross-Cultural Analysis of the Consumer Profile from Romania and Moldova. Agriculture 2022, 12, 1614. [Google Scholar] [CrossRef]

- Jimenez, J.A.C.; de la Torre, M.G.M.V.; Millán, M.G.D. Enotourism in Southern Spain: The Montilla-Moriles PDO. Int. J. Environ. Res. Public Health 2022, 19, 3393. [Google Scholar] [CrossRef]

- Santos, V.; Ramos, P.; Sousa, B.; Valeri, M. Towards a framework for the global wine tourism system. J. Organ. Chang. Manag. 2021, 35, 348–360. [Google Scholar] [CrossRef]

- Everingham, P.; Chassagne, N. Post COVID-19 ecological and social reset: Moving away from capitalist growth models towards tourism as Buen Vivir. Int. J. Tour. Place Environ. 2020, 22, 555–566. [Google Scholar] [CrossRef]

- Masot, A.N.; Rodríguez, N.R. Rural Tourism as a Development Strategy in Low-Density Areas: Case Study in Northern Extremadura (Spain). Sustainability 2021, 13, 239. [Google Scholar] [CrossRef]

- López-Sanz, J.M.; Penelas-Leguía, A.; Gutierrez, P.; Cuesta, P. Sustainable development and rural tourism in depopulated areas. Land 2021, 10, 985. [Google Scholar] [CrossRef]

- Eusébio, C.; Carneiro, M.J.; Figueiredo, E.; Duarte, P.; Pato, M.L.; Kastenholz, E. How diverse are residents’ perceptions of wine tourism impacts in three Portuguese wine routes? The role of involvement with tourism, wine production and destination life-cycle stage. Int. J. Wine Bus. Res. 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Kastenholzs, E.; Paco, A.; Nave, A. Wine tourism in rural areas—Hopes and fears amongst local residents. Worldw. Hosp. Tour. Themes 2022, 15, 29–40. [Google Scholar] [CrossRef]

- Zajac, P.; Čurlej, J.; Benešová, L.; Čapla, J. Hygiene Measures in Supermarkets, Retail Food Stores, and Grocery Shops During The COVID-19 Pandemic in Slovakia. Slovak J. Food Sci. 2021, 15, 396–422. [Google Scholar] [CrossRef]

- Caplanova, A.; Sivak, R.; Szakadatova, E. Institutional Trust and Compliance with Measures to Fight COVID-19. Int. Adv. Econ. Res. 2021, 27, 47–60. [Google Scholar] [CrossRef]

- Operation Joint Responsibility MDSR, Ministry of Defence of the Slovak Republic. Available online: https://www.somzodopvedny.sk (accessed on 5 January 2023). (In Slovak).

- Development of the Epidemic Situation in Slovakia 6.3. 2020; MIRDI SR, 2021a. 18.4.2021. Available online: https://korona.gov.sk/ (accessed on 5 January 2023). (In Slovak)

- Mirdi, S.R. Actual Regional COVID Automat. Slovakia 19.4.2021 25.4.2021.; 2021. Available online: https://korona.gov.sk/ (accessed on 6 January 2023).

- The Measure of the Public Health Authority of the Slovak Republic. PHA SR, 2020c. OLP 3461/2020. 2020. Available online: https://www.uvzsr.sk/docs/info/covid19/22_04_2020_otvorenie_prevadzok_rezimove_opatrenia_HH_SR.pdf (accessed on 6 January 2023). (In Slovak).

- Pha, S.R. The Measure of the Public Health Authority of the Slovak Republic, 2020d. OLP 3795/2020. 2020. Available online: https://www.ruvztv.sk/wp-content/pdf_downloads/covid_19/opatrenie_uvzsr_prevadzky_2_faza_05_05_2020.pdf (accessed on 6 January 2023). (In Slovak).

- The Measure of the Public Health Authority of the Slovak Republic. PHA SR, 2020e. OLP 4083/2020. 2020. Available online: https://www.uvzsr.sk/docs/info/covid19/19_05_2020_navrh_opatrenie_UVZ_SR_prevadzky_3_faza_01.pdf (accessed on 6 January 2023). (In Slovak).

- The Measure of the Public Health Authority of the Slovak Republic. PHA SR, 2020f. OLP 4362/2020. 2020. Available online: https://www.uvzsr.sk/docs/info/covid19/26_05_zmena_opatrenia_prevadzky_vynimky.pdf (accessed on 6 January 2023). (In Slovak).

- The Measure of the Public Health Authority of the Slovak Republic. PHA SR, 2020j. OLP 8326/2020. Available online: https://www.uvzsr.sk/docs/info/covid19/final_opatrenie_prevadzky_a_HP_15_10.pdf (accessed on 6 January 2023). (In Slovak).

- Pha, S.R. Decree of PHA SR no. 45: Decree of the Public Health Authority of the Slovak Republic, Which Prescribes Measures in the Event of a Threat to Public Health to Restrict Operations and Mass Events. J. Gov. Slovak Repub. 2020, 30, 17. Available online: https://www.uvzsr.sk/docs/info/ut/ciastka_26_2020.pdf (accessed on 7 January 2023). (In Slovak).

- Šebová, M.; Réveszová, Z.; Tóthová, B. The response of cultural policies to the COVID-19 pandemic: The Case of Slovakia. SciPap 2021, 29, 1245. [Google Scholar] [CrossRef]

- Pavlíková, M.; Sirotkin, A.; Králik, R.; Petrikovičová, L.; Martin, J.G. How to keep university active during COVID-19 pandemic: Experience from Slovakia. Sustainability 2021, 13, 10350. [Google Scholar] [CrossRef]

- Barath, M. Inflexibility in Flexible Business Request, Case of Organisations in Slovakia. Stud. Syst. Decis. Control 2022, 421, 327–342. [Google Scholar] [CrossRef]

- Gręndzińska, J.; Hoffman, I.; Klimovský, D.; Malý, I.; Nemec, J. Four cases, the same story? The roles of the prime ministers in the V4 countries during the COVID crisis. Transylv. Rev. Adm. Sci. 2022, 2022, 28–44. [Google Scholar] [CrossRef]

- Lesáková, Ľ.; Vinczeová, M.; Kaščáková, A. Measures supporting entrepreneurship in Slovak SMEs in the most vulnerable industries in times of the COVID-19 pandemic. Ekon. A Manag. 2022, 25, 4–18. [Google Scholar] [CrossRef]

- MATYŠÁK—About Us. Available online: https://www.vinomatysak.sk/o-nas/ (accessed on 6 January 2023).

- Financial and Legal Data about Companies in One Place. Fin Stat. Available online: https://www.finstat.sk/ (accessed on 5 January 2023).

- Veselovská, L. Supply chain disruptions in the context of early stages of the global COVID-19 outbreak. Probl. Perskectivs Manag. 2020, 18, 490–500. [Google Scholar] [CrossRef]

- Pollák, F.; Markovič, P.; Világi, R. Selected Views on Eating Habits and Lifestyle Changes of Consumers During the COVID-19 Pandemic Through the Optics of Supply Chains. In Proceedings of the IDIMT 2022—Digitalization of Society, Business and Management in a Pandemic: 30th Interdisciplinary Information Management Talks, Prague, Czech Republic, 7–9 September 2022. [Google Scholar] [CrossRef]

- Leifman, H.; Dramstad, K.; Juslin, E. Alcohol consumption and closed borders—How COVID-19 restrictions have impacted alcohol sales and consumption in Europe. BMC Public Health 2022, 22, 692. [Google Scholar] [CrossRef] [PubMed]

- Aqueveque, C. Consumers’ preferences for low-priced wines’ packaging alternatives: The influence of consumption occasion, gender, and age. Br. Food J. 2023, 125, 781–793. [Google Scholar] [CrossRef]

- Gavurova, B.; Khouri, S.; Ivankova, V.; Kubak, M. Changes in Alcohol Consumption and Determinants of Excessive Drinking During the COVID-19 Lockdown in the Slovak Republic. Front. Public Health 2022, 9, 2357. [Google Scholar] [CrossRef] [PubMed]

- Gavurova, B.; Ivankova, V.; Kubak, M. Public health management in a crisis situation: Alcohol consumption in terms of socio-economic status. Pol. J. Manag. Stud. 2021, 24, 80–95. [Google Scholar] [CrossRef]

- Schwaiger, K.; Zehrer, A.; Braun, B. Organizational resilience in hospitality family businesses during the COVID-19 pandemic: A qualitative approach. Tour. Rev. 2022, 77, 163–176. [Google Scholar] [CrossRef]

- Lianos, C.; Ibanez, M.J.; Prado-Gasco, V.J. Job-demand and family business resources in pandemic context: How they influence burnout and job satisfaction. Front. Psychol. 2023, 13, 1061612. [Google Scholar] [CrossRef]

- Lianos, C.; Baier-Fuentes, H.; González-Serrano, M.H. Direct and indirect effects of SEWi, family human capital and social capital on organizational social capital in small family firms. Int. Entrep. Manag. J. 2022, 18, 1403–1418. [Google Scholar] [CrossRef]

- Edmondson, D.; Mathews, L. Are Business-to-Business Employees More Engaged or Burned Out Amid a Global Health Crisis: A Comparative Study. J. Bus.—Bus. Mark. 2022, 29, 87–98. [Google Scholar] [CrossRef]

- Huq, F.; Jones, V.; Hensler, D. A time series projection model of online seasonal demand for American wine and potential disruption in the supply channels due to COVID-19. Int. J. Wine Bus. Res. 2022, 34, 349–372. [Google Scholar] [CrossRef]

- Arimany-Serrat, N.; Farreras-Noguer, M.; Coenders, G. Financial resilience of Spanish wineries during the COVID-19 lockdown. Int. J. Wine Bus. Res. 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Sohn, S.; Seegebarth, B.; Kissling, M.; Sippel, T. Social Cues and the Online Purchase Intentions of Organic Wine. Foods 2020, 9, 643. [Google Scholar] [CrossRef]

- Kikuchi, J.; Nagao, R.; Nakazono, Y. Expenditure responses to the COVID-19 pandemic. Jpn. World Econ. 2023, 65, 101174. [Google Scholar] [CrossRef]

- Balatonyi, J.F. Getting married in times of COVID-19: Structure, agency, and individual decision making. Intersect. East Eur. J. Soc. Politics 2021, 7, 259–278. [Google Scholar] [CrossRef]

- Gomes, C.; Malheiros, C.; Campos, F.; Lima, S. COVID-19′s Impact on the Restaurant Industry. Sustainability 2022, 14, 11544. [Google Scholar] [CrossRef]

- Madeira, A.; Palrao, T.; Mendes, A. The impact of pandemic crisis on the restaurant business. Sustainability 2021, 13, 40. [Google Scholar] [CrossRef]

- Yost, E.; Kizildag, M.; Ridderstaat, J. Financial recovery strategies for restaurants during COVID-19: Evidence from the US restaurant industry. J. Hosp. Tour. Manag. 2021, 47, 408–412. [Google Scholar] [CrossRef]

- Králiková, A.; Kubát, P.; Ryglová, K. Visitors’ Happiness and Loyalty in the Moravian Wine Region. Eur. Countrys. 2021, 13, 750–767. [Google Scholar] [CrossRef]

- Garbarová, M.; Vartiak, L. Identification of Customer’s Preferences as One of the Main Activities of Destination Management. TEM J. 2022, 11, 159–163. [Google Scholar] [CrossRef]

- Strenitzerová, M.; Garbarová, M. Identification of the Barriers to Business in Slovakia. Commun.—Sci. Lett. Univ. Žilina 2017, 19, 56–60. [Google Scholar] [CrossRef]

- Balogh, J.; Mizik, T. Impacts of Marketing Strategy and Social Media Activity on the Profitability of Online Wine Shops: The Case of Hungary. Economies 2022, 10, 301. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Vineyard Location | Distance (km) |

|---|---|

| Grinava | 4 |

| Viničné | 8 |

| Chorvátsky Grob | 10 |

| Šenkvice | 11 |

| Hlohovec | 59 |

| Búč | 130 |

| Mužla | 130 |

| Vineyard Location | 2020 (kg) | 2021 (kg) | Difference between 2020 and 2021 (%) |

|---|---|---|---|

| Grinava | 259,220 | 226,773 | −12.52 |

| Viničné | 653,010 | 562,600 | −13.85 |

| Chorvátsky Grob | 391,830 | 311,700 | −20.45 |

| Šenkvice | 139,370 | 127,930 | −8.21 |

| Hlohovec | 364,650 | 368,460 | +1.00 |

| Búč | 206,850 | 180,861 | −12.56 |

| Mužla | 510,713 | 408,733 | −19.98 |

| Other areas | 682,006 | 416,739 | −38.89 |

| Total | 3,207,649 | 2,603,533 | −18.83 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Synák, F. Problems and Opportunities within the Wine Industry in Terms of the COVID-19 Pandemic. Agriculture 2023, 13, 731. https://doi.org/10.3390/agriculture13030731

Synák F. Problems and Opportunities within the Wine Industry in Terms of the COVID-19 Pandemic. Agriculture. 2023; 13(3):731. https://doi.org/10.3390/agriculture13030731

Chicago/Turabian StyleSynák, František. 2023. "Problems and Opportunities within the Wine Industry in Terms of the COVID-19 Pandemic" Agriculture 13, no. 3: 731. https://doi.org/10.3390/agriculture13030731

APA StyleSynák, F. (2023). Problems and Opportunities within the Wine Industry in Terms of the COVID-19 Pandemic. Agriculture, 13(3), 731. https://doi.org/10.3390/agriculture13030731