Payment Schemes in Conditional Cash Transfer Programs: The Case of 4Ps in the Davao Region, Philippines

Abstract

:1. Introduction

- (a)

- Assess the strengths and weaknesses of the different cash transfer schemes of 4Ps.

- (b)

- Estimate the differences in cost and time required to deliver cash assistance through the different 4Ps payment schemes.

- (c)

- Assess if a competitive procurement process (by way of bidding) of engaging Payment Service Providers (PSPs) is effective in securing the lowest price with the best service.

- (d)

- Identify indicators of outcome and cost efficiency for different payment schemes.

2. Institutional Background

2.1. Pantawid Pamilyang Pilipino Program (4Ps)

2.2. 4Ps Payment System

3. Perspectives on Cash Transfer Program Efficacy

3.1. Payment System of Cash Transfer Program

{kind=link}

| Delivery Agent | Delivery Method | |||||||

|---|---|---|---|---|---|---|---|---|

| Cash or Voucher | E-wallet | Bank Account | ||||||

| Direct (cash in envelopes or voucher) | Check or bank draft | Mobile phone | Smart card | Prepaid card | Debit card | Mobile phone | Smart card | |

| Aid Agency directly | Save the Children in Myanmar (Burma) | WFP (World Food Program in Syria) | Concern, Oxfam in Kenya | |||||

| Government | Kenya Hunger Safety Net (HSNP) | Indian and Pakistani governments | Kenya HSNP | |||||

| Bank | DRC in Chechnya | Red Cross in Indonesia | Concern in Malawi | |||||

| Post Office | Save the Children in Pakistan | Save the Children in Swaziland | Mercy Corps in Pakistan | |||||

| Micro-Finance institution | Action Aid in Myanmar (Burma) | |||||||

| Remittance company | Horn Relief in Somalia | |||||||

| Security company | WV in Lesotho | |||||||

| Local traders | Save the Children in Niger | Kenya HSNP | DRC ex-soldiers | |||||

3.2. Evaluation of Payment System of Cash Transfer Program

| Criteria | Assessment questions |

|---|---|

| Objectives | What are the key objectives of the program? |

| Delivery options and existing infrastructure | What delivery options are available in the area (banks, postal service, mobile operators)? Is there mobile phone coverage? What are the motivations of potential providers (e.g., Financial gain, social mission, image-boosting)? |

| Cost | What are the costs of different options for the agency (provider charges, staff, transport security and training costs)? What are the costs for the recipient (charges, travel costs, waiting time)? |

| Security | What are the security risks associated with each delivery option for the agency and the recipients? |

| Controls/risks | What are the key risks that need to be managed? What corruption risks are associated with each delivery option? What fiscal controls and standards are in place? |

| Human Resources | How many staffs are required for each option? |

| Speed | How long is it likely to take to get each delivery option and running? What are the regulatory requirements for the recipients in respect of each option? |

| Resilience | How resilient are the potential options in the face of possible disruptions to communication and infrastructure following disaster? How reliable and stable are potential commercial providers? |

| Scale | What is the target population, how large are the payments and how frequently will they be made? How will each delivery mechanism be likely to cope? |

| Flexibility | How flexibly can the different options adjust the timing and amount of payments? |

4. Empirical Strategy

4.1. Analytical Framework

| Cash Delivery Option | Advantages | Disadvantages |

|---|---|---|

| Direct delivery (cash in envelopes) | Speed, simplicity and cost Flexible if recipients move location. | Security and corruption risks. Often labor intensive, especially in terms of staff time. For recipients a lack of flexibility in when they receive cash and possible long waiting times |

| Delivery using bank accounts | Reduced workload for agency staff. Corruption and security risks may be reduced if institutions have strong control systems. Flexibility and convenience for recipients who can choose when to withdraw cash and avoid queues. Access to financial system for previously unbanked recipients | Time needed to negotiate roles, contractual terms and establish systems. Reluctance to set up accounts for small amounts of money. Bank charges may be expensive. Recipients may be unfamiliar with financial institutions and have some fears in dealing with them. Possible exclusion of people without necessary documentation and children. |

| Without accounts using checks | As above and can avoid delays that can be caused by having to verify transfers. | As bank accounts are not opened, recipients do not gain access to the banking system. |

| Delivery using sub-contracted parties (remittance companies) | Sub-contracted parties accept some responsibility for loss. Security risks for agency reduced. Remittance companies may have greater access than agencies to insecure areas. Recipients may be familiar with these types of systems. Flexibility and access—these systems may be near to where recipients live and may offer greater flexibility in receiving their cash. | The system may require greater monitoring for auditing purposes. Reduced control over distribution time frame. Credibility could be at risk if the transfer company cannot provide the money to the agreed time schedule. Recipients may be more removed from aid agency and so less able to complain if things go wrong. |

| Delivery via pre-paid cards or mobiles | As with banks, possible reduced corruption and security risks, reduced workload for agency staff, greater flexibility for recipients. Greater flexibility in where cash can be collected (e.g. Mobile Points of Sale, local traders). A mobile phone (individual or communal) can be provided at low cost to those who do not already have them. | Systems may take time and be complex to establish. Risks of agents or branches running out money. Costs and risks of new technology such as smart cards. Recipients may be unfamiliar with new systems. Form of identity required to use payment instrument depends on local regulations and may exclude some people. |

4.2. Data and Study Area

5. Results and Discussion

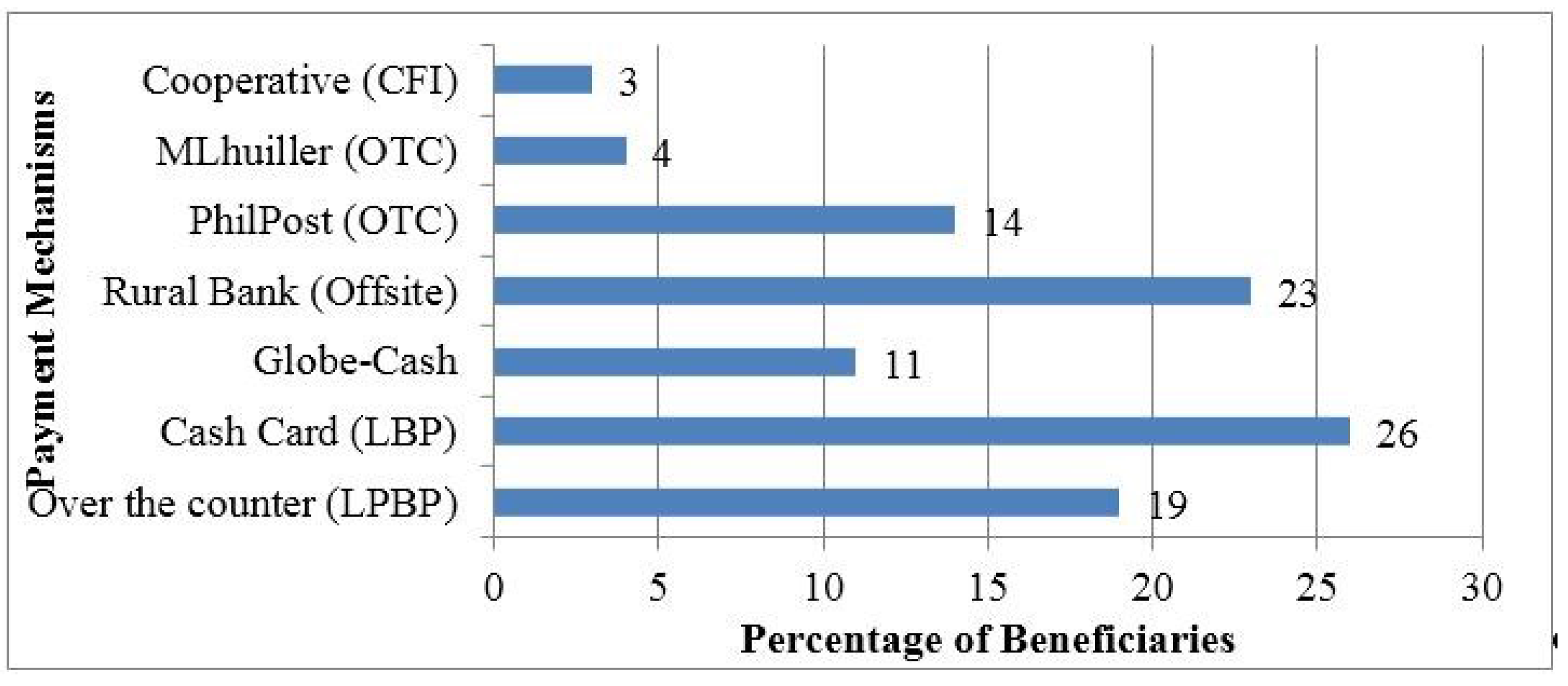

5.1. Comparison of Strengths and Weaknesses of Different Payment Schemes

| LBP (OTC or offsite) | LBP (CC) | Globe G-Cash | Rural Bank (offsite) | Coop Bank (offsite) | PhilPost (OTC) | MLhuiller (OTC) | |

|---|---|---|---|---|---|---|---|

| Year PSP Started | 2008 | 2009 | 2011 | 2011 | 2012 | 2012 | 2013 |

| Transaction Fees* | Php24 (US$0.50) | Php24 (US$0.50); Inter branch transaction Php20 (US$0.42) | Php75 (US$ 1.57) | Php50 (US$ 1.05) | Php50 (US$ 1.05) | Php50 (US$ 1.05) | Php42 (US $0.88) |

| Pay Points | Designated venue (s) | Any LBP branch in region 11 (11 branches) or ATMs (58) | Offsite areas providing OTC payments | Offsite areas providing OTC payments | Offsite areas providing OTC payments | PhilPost locations in region 11 (50) | MLhuiller locations in region 11 (41) |

| Payment Instruments | OTC | Cash Cards | G-Cash 4Ps Payment Slips (similar to ARs) | AR Form | AR Form | AR Form | AR Form |

| Payment Device | OTC Teller | ATM | G-cash Agent | OTC Teller | OTC Teller | Post Office Teller | Offsite Agents |

| Authentication Process | ID card | PIN | ID card | ID card | ID card | ID card | ID card |

5.2. Differences in Cost and Time Required to Deliver Cash Assistance and Competition of 4Ps Contracts to Deliver Cash Transfer

| Province | LBP (OTC) | LBP (CC) | Globe G-Cash | Rural Bank | Cooperative | Phil. Postal | MLhuillier |

|---|---|---|---|---|---|---|---|

| Davao Oriental | 8.95% | 9.33% | 7.01% | 74.26% | 0.00% | 0.40% | 0.05% |

| Davao del Norte | 6.93% | 20.37% | 2.66% | 53.30% | 0.01% | 15.19% | 1.53% |

| Davao del Sur | 11.97% | 24.74% | 17.16% | 8.60% | 8.04% | 29.01% | 0.48% |

| Compostela Valley | 6.28% | 18.44% | 17.30% | 49.53% | 0.00% | 8.22% | 0.22% |

5.3. Indicators of Outcome and Cost Efficiency

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A: Key Criteria for Assessing Cash Delivery Options—Viewpoint of Conduits

| Criteria | LBP (Over the Counter) | LBP (Cash Card) | PhilPost (Over the Counter) | Rural Banks (Over the Counter) | MLhuillier (OTC/Cash in Envelope) | Globe G-Cash (Cash in Envelope) | Cooperative (Cash in Envelope) | |

|---|---|---|---|---|---|---|---|---|

| Program Objective | Distribute the correct amount of benefits to the right people at the right time at a minimum cost | Yes, low cost | Yes, low Cost | Yes, medium cost | Yes, medium cost | Yes, medium cost | Yes, high cost | Yes, medium cost |

| Delivery Options and Existing Infrastructure | Six delivery options in the area and good mobile phone coverage | Infra- Limited | Infra-Limited to city centers | Infra-Present in all municipalities | Infra- None | Infra- Limited | Infra- High coverage | Infra- None |

| Costs | Operating cost | High cost | Low cost | High cost | High cost | High cost | High cost | High cost |

| Security/Control/ Risks | Monitoring/Auditing | Low risk | Low risk | High risk | High risk | High risk | High risk | High risk |

| Corruptions/ Lawless elements/Loss | High risk | Low risk | High risk | High risk | High risk | High risk | High risk | |

| Human Resources | Number of Staff Required | More | Less | More | More | More | More | More |

| Speed | Time for delivery | Longer time | Longer time | Shorter time | Shorter time | Shorter time | Shorter time | Shorter time |

| Resilience | Possible Disruption | Yes | No | Yes | Yes | Yes | No | Yes |

| Scale | Target Population | Assigned municipality | City centers and nearby areas | Each Municipality | Assigned municipality | Assigned municipality | Assigned municipality | Assigned municipality |

| Frequency of Payment | Bimonthly | Bimonthly | Bimonthly | Bimonthly | Bimonthly | Bimonthly | Bimonthly | |

| Flexibility | Timing | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Appendix B: Key Criteria for Assessing Cash Delivery Options: Viewpoint of Beneficiaries/Recipients

| Criteria | LBP (Over the Counter) | LBP (Cash Card) | PhilPost (Over the Counter) | Rural Banks (Over the counter) | Mlhuillier (OTC/Cash in Envelope) | Globe G-Cash (Cash in Envelope) | Cooperative (Cash in Envelope) | |

|---|---|---|---|---|---|---|---|---|

| Cost | Opportunity costs | |||||||

| (Long queues) | High | Low | High | High | High | High | High | |

| Transportation cost | Low | High | Low | Low | Low | Low | Low | |

| Security Risk | Lawless Elements | High | Low | High | High | High | High | High |

| Speed/Timeliness | In Terms of Accessibility | No | No | Yes | Yes | Yes | Yes | Yes |

| Flexibility | Collecting the benefits | No | Yes | No | No | No | No | No |

| Acceptability | Familiarity of Process | Yes | No | Yes | Yes | Yes | Yes | Yes |

| and types of payment | ||||||||

| schemes | ||||||||

Appendix C: Average Beneficiaries and Cities/Municipalities Served Per Payment Scheme

| Set | No. of Cities/Municipalities/Per Set | LBP (OTC) | LBP (CC) | Globe G-cash | Rural Bank | PhilPost | Mlhuillier | Coop |

|---|---|---|---|---|---|---|---|---|

| Set 1 | 3 | 4949 (3) | 6441 (3) | 3603 (2) | 4818 (3) | 75 (1) | 0 (0) | 0 (0) |

| Set 2 | 8 | 18,200 (8) | 29,036 (8) | 21,204 (6) | 10,657 (4) | 16,363 (4) | 0 (0) | 0 (0) |

| Set 3 | 14 | 5944 (14) | 7019 (12) | 1680 (4) | 1857 (8) | 409 (3) | 2 (0) | 0 (0) |

| Set 4 | 21 | 22,479 (12) | 27,566 (8) | 13,698 (11) | 21,439 (19) | 2816 (7) | 315 (6) | 2223 (1) |

| Set 5 | 36 | 13,946 (14) | 19,530 (16) | 0 (0) | 20,826 (26) | 9822 (17) | 6872 (15) | 228 (2) |

| Set 6 | 44 | 0 (0) | 3133 (16) | 0 (0) | 4219 (25) | 13,006 (24) | 3777 (16) | 1006 (1) |

References

- DFID. Social Transfers and Chronic Poverty: Emerging Evidence and the Challenge Ahead; Deparment for International Development: London and Glasgow, UK, 2005.

- Barrientos, A.; DeJong, J. Reducing Child Poverty with Cash Transfers: A sure Thing? Pol. Rev. 2006, 24, 537–552. [Google Scholar] [CrossRef]

- Farrington, J.; Slater, R. Introduction: Cash Transfers: Panacea for Poverty Reduction or Money Down the Drain? Dev. Pol. Rev. 2006, 24, 499–511. [Google Scholar] [CrossRef]

- Barca, V.; Hurrell, A.; MacAuslan, I.; Visram, A.; Willis, J. Paying Attention to Detail: How to Transfer Cash in Cash Transfers. Ent. Dev. Microfinance 2013, 24, 10–27. [Google Scholar] [CrossRef]

- Zimmerman, J.; Bohling, K. Striving for E-Payments at Scale. The Evolution of the Pantawid Pamilyang Pilipino Program in the Philippines; World Bank: Washington, DC, USA, 2014. [Google Scholar]

- DFID. Scoping Report on the Payment of Social Transfers through the Financial System; Bankable Frontier Associates: Boston, MA, USA, 2006. [Google Scholar]

- Fernandez, L.; Olfindo, R. Overview of the Philippines’ Conditional Cash Transfer Program: The Pantawid Pamilyang Pilipino Program (Pantawid Pamilya); World Bank: Manila, the Philippines, 2011. [Google Scholar]

- Bangsal, N.; Asuncion, R. Accountability Mechanisms in the Implementation of Condtional Cash Transfer Program (CCTs): Policy Brief; Congressional Policy, Budget and Research Department (CPBRD): Quezon City, Philippines, 2011.

- Harvey, P.; Haver, K.; Hoffman, J.; Murphy, B. Delivering Money: Cash Transfer Mechanisms in Emergencies; The Cash Learning Partnership (CaLP): London, UK, 2010. [Google Scholar]

- Devereux, S.; Vincent, K. Using Technology to Deliver Social Protection: Exploring Opportunities and Risks. Dev. Pract. 2010, 20, 367–379. [Google Scholar] [CrossRef]

- Murray, S.; Hove, F. Cheaper, Faster, Better? A Case Study of New Technologies in Cash Transfers from the Democratic Republic of Congo; Mercy Corps and Oxford Policy Management: Oxford, UK, 2014. [Google Scholar]

- Grosh, M.; del Ninno, C.; Tesline, E.; Ouerghi, A. From Protection to Promotion: The Design and Implementation of Effective Safety Nets; World Bank: Washington, DC, USA, 2007. [Google Scholar]

- Beswick, C. Distributing Cash Through Bank Accounts: Save the Children's Drought Response in Swaziland; FinMarkTrust: Marshalltown, South Africa, 2008. [Google Scholar]

- Forcier, N. Report on Cash Transfer Modalities for South Sudan. Available online: http://www.forcierconsulting.com/../uploads/2013/05/2012_Forcier-FAO-RSS-Report-on-Cash-Transfer (accessed on 8 February 2015).

- Nigenda, G.; Gonzalez-Robledo, J. Lessons Offered by Latin American Cash Transfer Programmes Mexico’s Oportunidades and Nicaraguas’ SPN: Implications for African countries; DFID Health Systems Response Centre: London, UK, 2005. [Google Scholar]

- Langhan, S.; Kilfoil, C.; Agar, J.; Murphy, B. Identification of Appropriate Alternative Delivery Mechanisms for the Cash Transfer in the Context of the Pilot Social Cash Transfer Scheme in Mchinji District, Malawi; UNICEF and Government of Malawi: Lilongwe, Malawi, 2010.

- O’ Brien, C. A Guide to Calculating the Cost of Delivering Cash Transfers in Humanitarian Emergencies with Reference to Case Studies in Kenya and Somalia; Oxford Policy Management: Oxford, UK, 2014. [Google Scholar]

- Carrillo, P.; Ponce Jarrín, J. Efficient Delivery of Cash Transfers to the Poor: Improving the Design of a Conditional Cash Transfer Program in Ecuador; Institute for International Economic Policy, 2007. Available online: https://www.gwu.edu/~iiep/assets/docs/papers/Carrillo_IIEPWP8.pdf (accessed on 10 March 2015).

- Bold, C.; Porteous, D.; Rotman, S. Social Cash Transfers and Financial Inclusion: Evidence from Four Countries; The Consultative Group to Assist the Poor (CGAP): Washington, DC, USA, 2012. [Google Scholar]

- Zimmerman, J.; Bohling, K.; Parker, S. Electronic G2P Payments: Evidence from Four Lower-Income Countries; The Consultative Group to Assist the Poor (CGAP): Washington, DC, USA, 2014. [Google Scholar]

- O’Brien, C.; Hove, F.; Smith, G. Factors Affecting the Cost-Efficiency of Electronic Transfers in Humanitarian Programmes; Oxford Policy Management: Oxford, UK, 2013. [Google Scholar]

- Oberländer, L.; Brossman, M. Electronic Delivery Methods of Social Cash Transfers. [Discussion Papers on Social Protection]. Available online: https://www.giz.de/expertise/downloads/giz2014-en-electronic-delivery-methods-of-social-cash-transfers.pdf (accessed on 26 February 2015).

- Chandy, L.; Kharas, H. The Innovation of Revolution and Its Implications for Development; Brookings Institution: Washington, DC, USA, 2012. [Google Scholar]

- Aker, J.; Boumnijel, R.; McClelland, A.; Tierney, N. Zap it to Me: The Short-Term Impacts of a Mobile Cash Transfer Program; Center for Global Development: Washington, DC, USA, 2011. [Google Scholar]

- CGAP. Striving for E-Payments at Scale: The Evolution of the Pantawid Pamilyang Pilipino Program in the Philippines; World Bank: Washington, DC, USA, 2013. [Google Scholar]

- Gusto, A.; Roque, E. Delivering Cash Grants to Indigenous Peoples Through Cash Cards Over-the-Counter Modalities: The Case of 4Ps Conditional Cash Transfer Program in Palawan, Philippines; Institute for Money Technology and Financial Inclusion (IMTFI): Irvine, CA, USA, 2012. [Google Scholar]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Catubig, M.C.; Villano, R.; Dollery, B. Payment Schemes in Conditional Cash Transfer Programs: The Case of 4Ps in the Davao Region, Philippines. Adm. Sci. 2015, 5, 240-259. https://doi.org/10.3390/admsci5040240

Catubig MC, Villano R, Dollery B. Payment Schemes in Conditional Cash Transfer Programs: The Case of 4Ps in the Davao Region, Philippines. Administrative Sciences. 2015; 5(4):240-259. https://doi.org/10.3390/admsci5040240

Chicago/Turabian StyleCatubig, Ma Cecilia, Renato Villano, and Brian Dollery. 2015. "Payment Schemes in Conditional Cash Transfer Programs: The Case of 4Ps in the Davao Region, Philippines" Administrative Sciences 5, no. 4: 240-259. https://doi.org/10.3390/admsci5040240

APA StyleCatubig, M. C., Villano, R., & Dollery, B. (2015). Payment Schemes in Conditional Cash Transfer Programs: The Case of 4Ps in the Davao Region, Philippines. Administrative Sciences, 5(4), 240-259. https://doi.org/10.3390/admsci5040240