Management Accounting and Control in Higher Education Institutions: A Systematic Literature Review

Abstract

1. Introduction

2. Theoretical Background

2.1. Management Accounting and Control

2.2. Main Theories Used in Management Accounting and Control Research

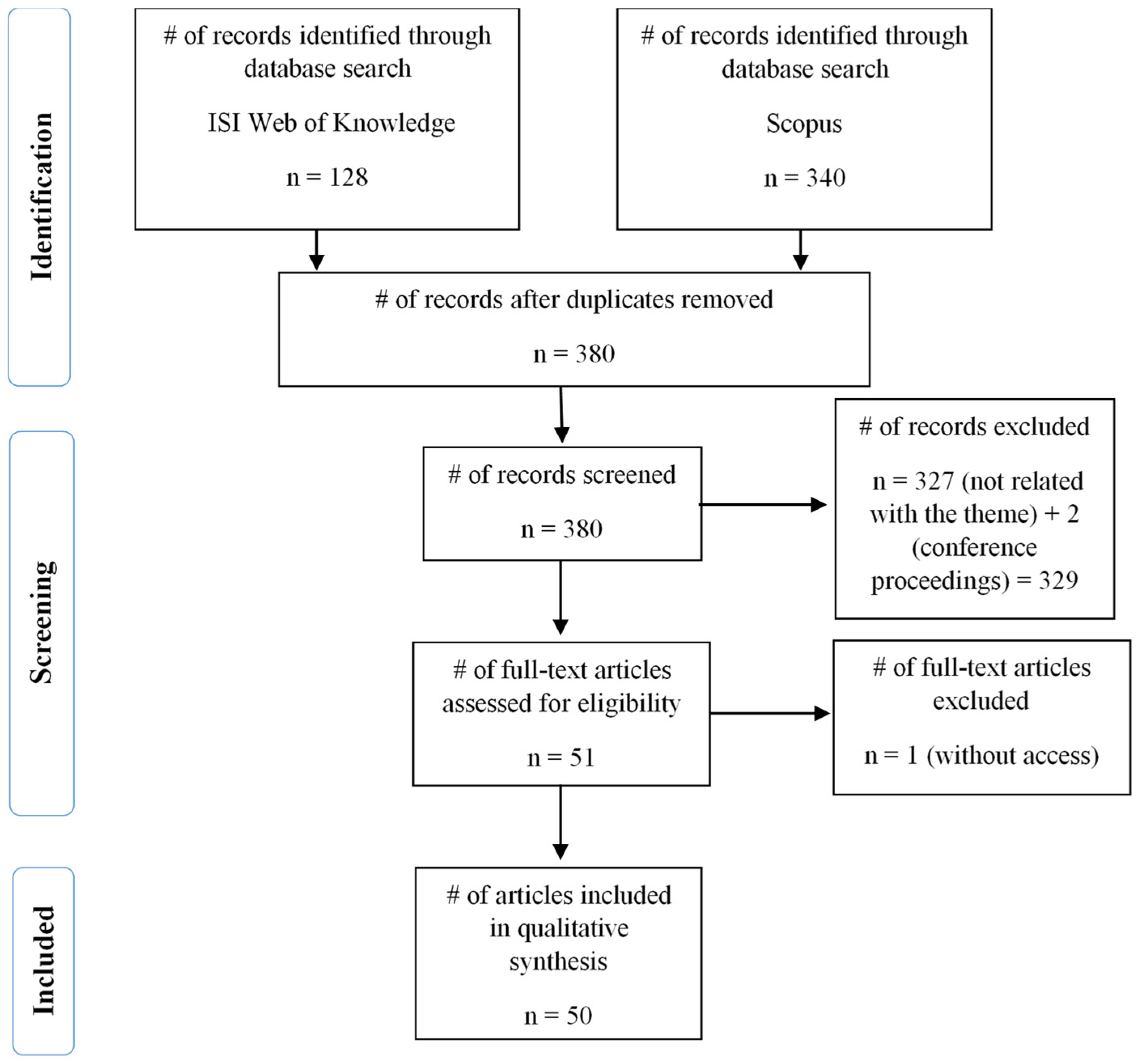

3. Methodology

4. Results

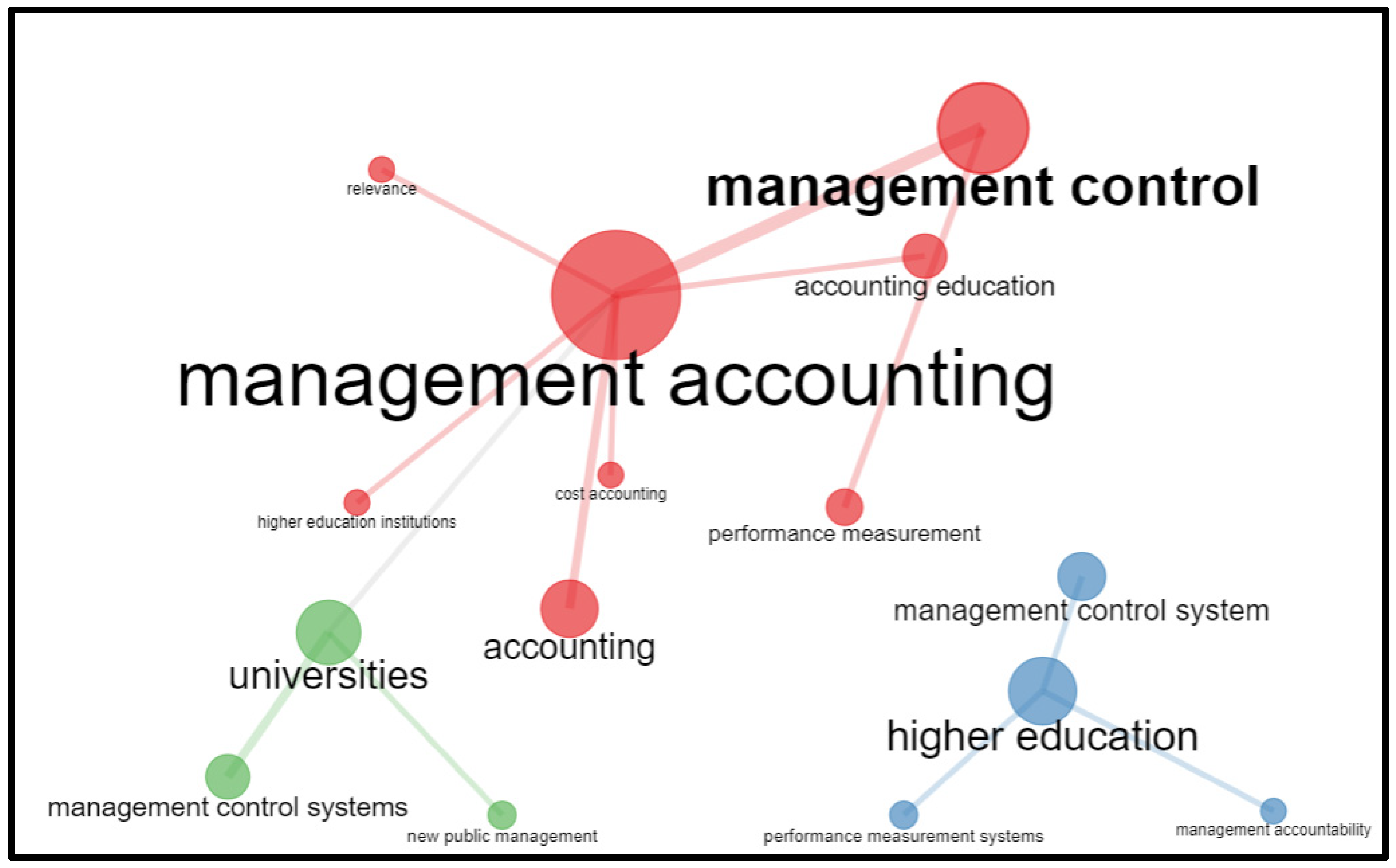

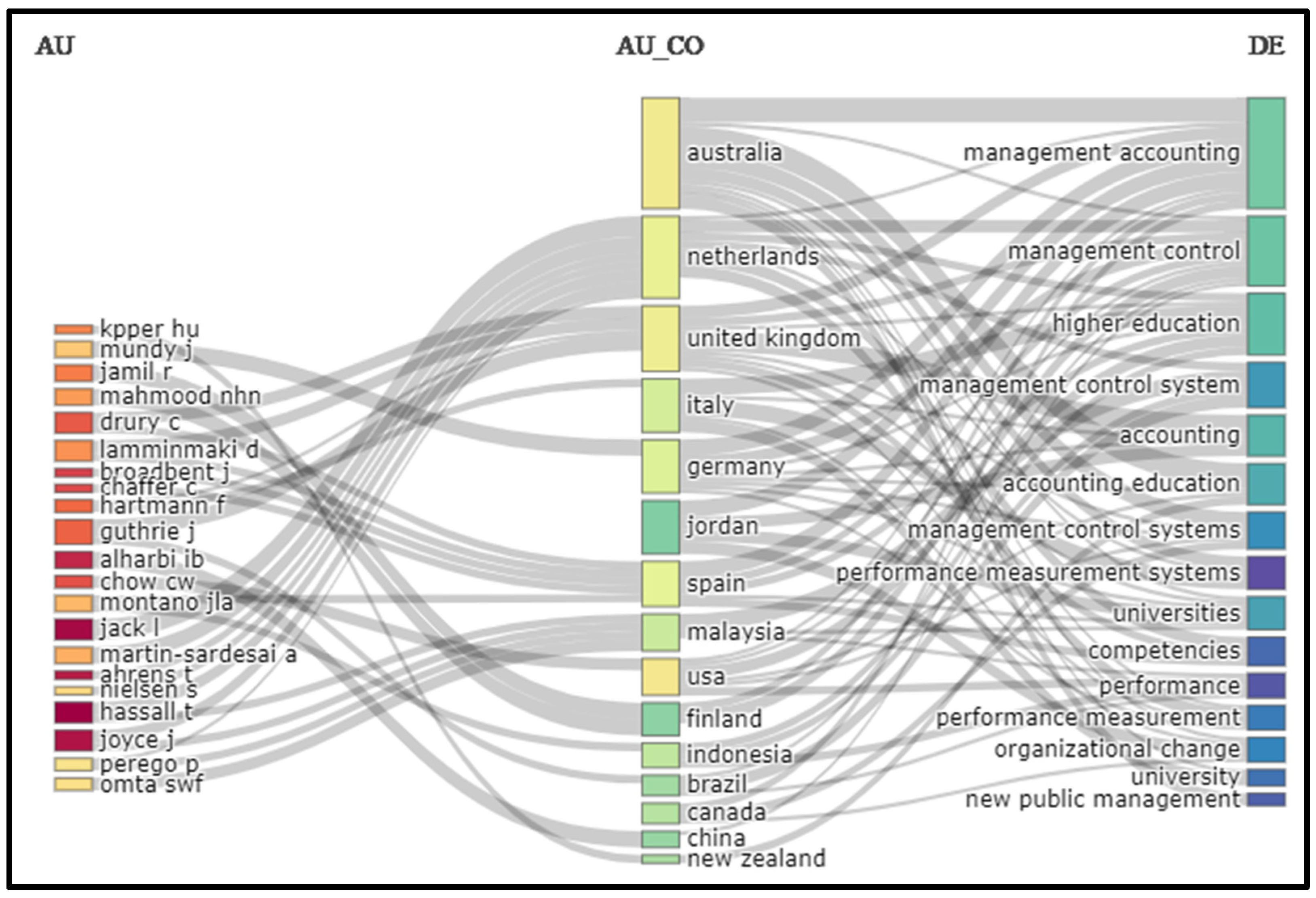

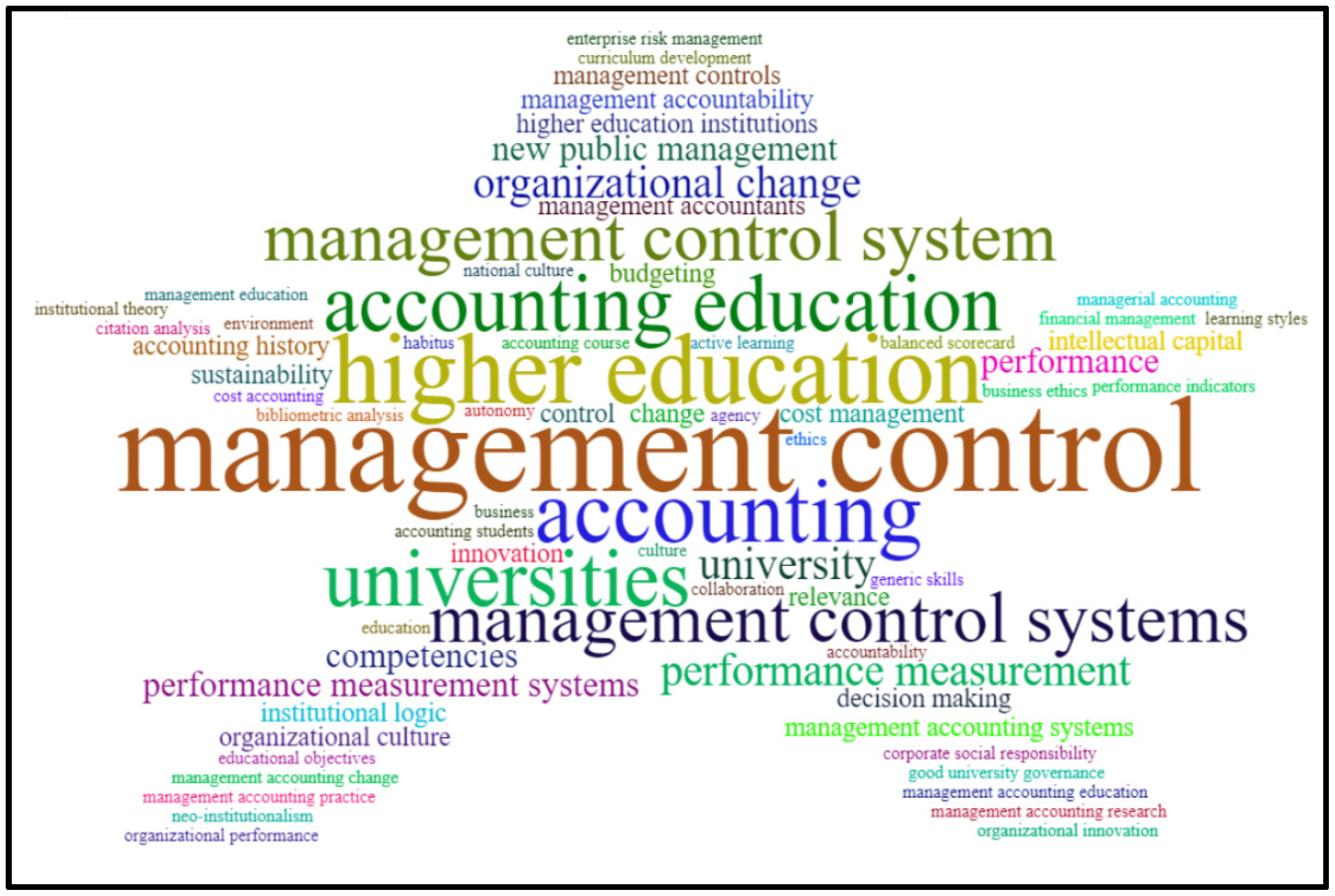

4.1. Main Topics Addressed in Studies on Management Accounting and Control in HEIs

Longitudinal Perspective

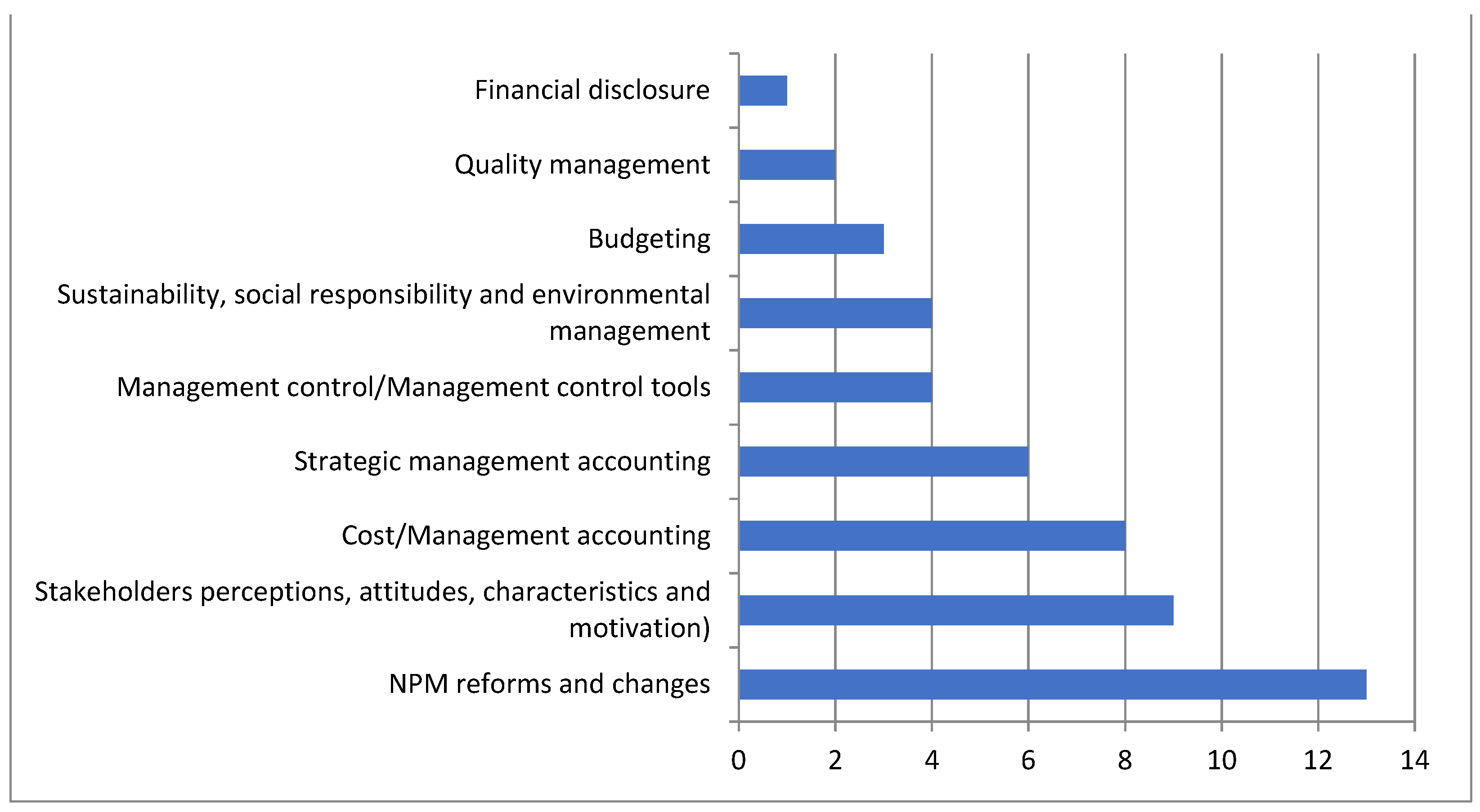

4.2. Main Results of Studies on Management Accounting and Control in HEIs

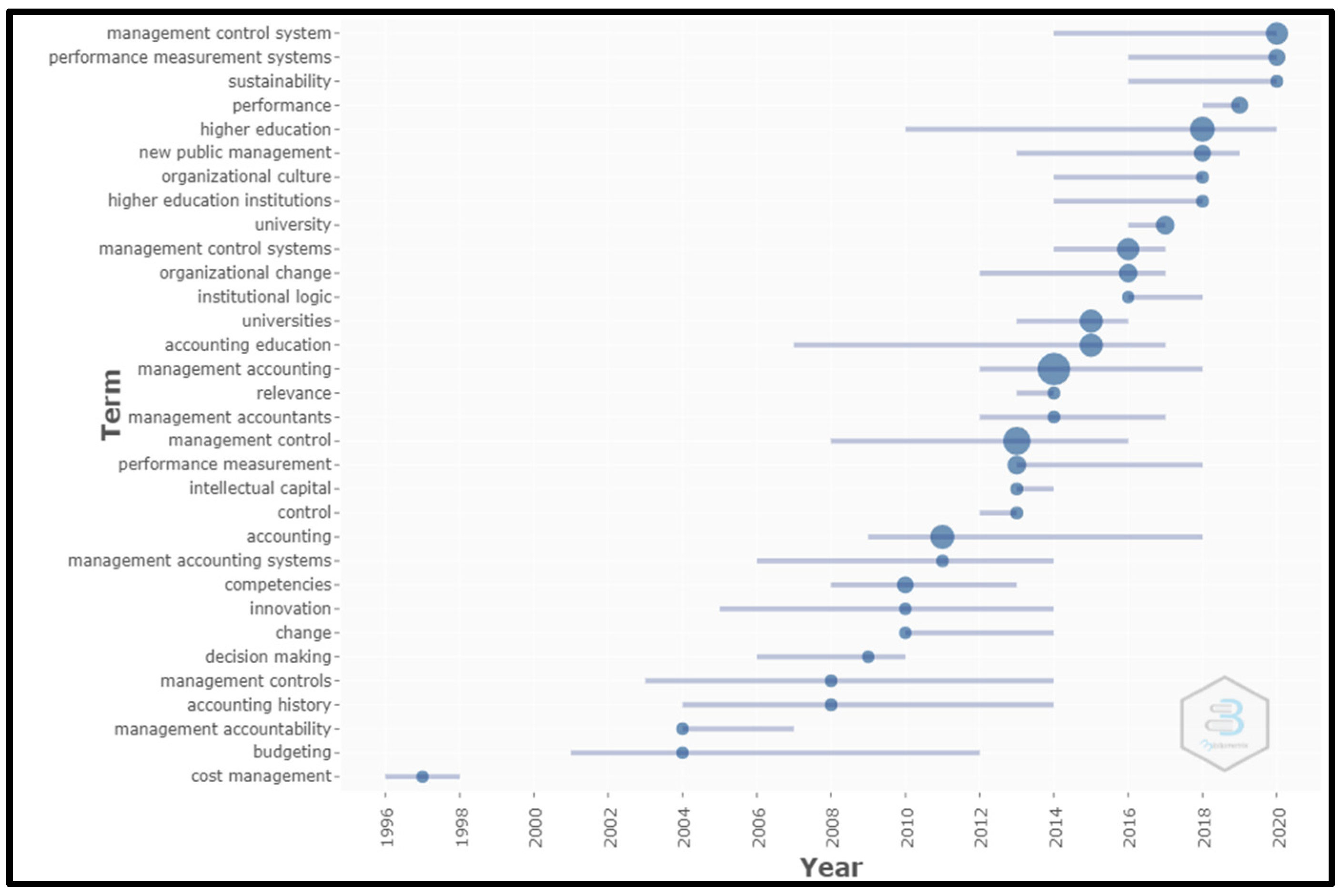

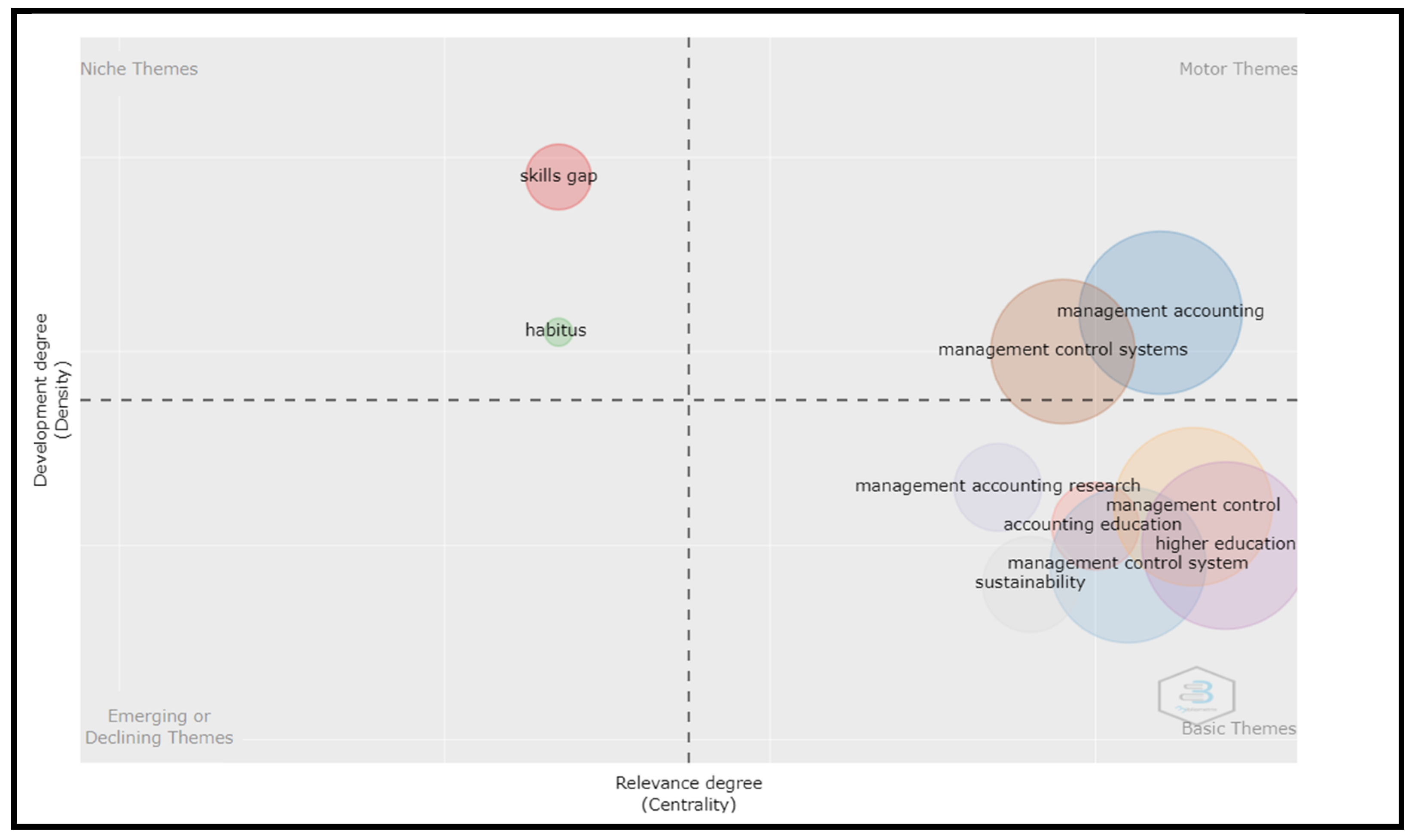

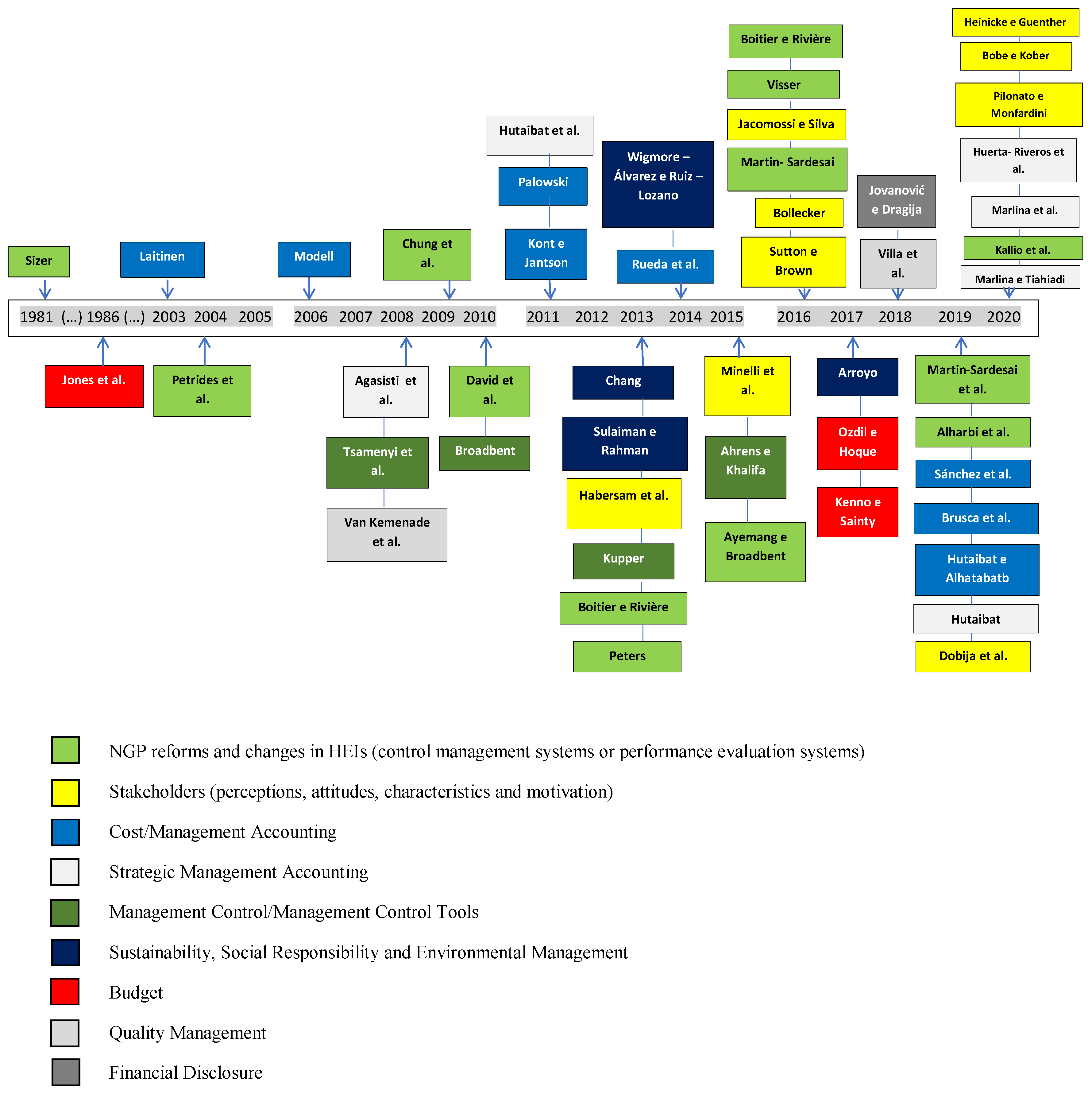

4.3. Thematic Evolution

4.4. Main Theories Addressed in Studies on Management Accounting and Control in HEIs

5. Some Reflections for Further Research and Concluding Remarks

- Addressing the extent to which negative impacts of performance management systems are due to the dysfunctions resulting from the actions of organizations or individuals. This is an important issue since these impacts may hamper quality research, also leading to rankings which do not truly depict the strength of the HEI;

- Better understanding the complexity of the reactions of academics towards management control systems based in academic rankings. This fact can potentially develop important values, which can be grounded on a more relational approach to management control;

- More empirical evidence is needed to prescribe practical implications to address the obligation to promote a sustainable higher education;

- More studies following the principles of authenticity, plausibility and criticality, mainly in cases where the researcher is a participant observer and a close relationship between him/her and the research subject can be questioned;

- More interpretive research on strategy and accounting in order to develop themes such as strategic costing modeling, accounting competitors and customer accounting. According to Hutaibat et al. (2011), strategic management accounting should be extended to other institutions to obtain a deeper comprehension of the phenomenon;

- Addressing the linkage between HEIs and industry in order to increase HEIS’ performance;

- Better understanding the impact of Deans’ characteristics on the use of MCS and performance measures, since they can greatly affect an HEI’s performance;

- Understanding how the actions undertaken by a presidential team can anticipate or change HEIs’ response to external demands. This is an important matter since stakeholders’ representation may change over time, affecting institutional demands. Consequently, HEIs’ strategic response should adapt to these changes;

- Assessing the impact of international organizations, such as rating and accreditation agencies, regarding the use of performance measures. In fact, several scholars as well as practitioners are still skeptical towards the credibility of those agencies, and consequently towards the use of the proposed measures;

- Assessing the role of other key players such as local authorities, ministries or healthcare organizations. By understanding the role played by these agents, HEIs can gain important insights about how control systems may be improved;

- Assessing the effects of power relations within an HEI, the potential conflicts between agents, as well as the motivational effects. Power exercises within an HEI can both promote collaboration or lead to the emergence of conflicts. Therefore, on the one hand it is crucial for these institutions to know how to overcome potential conflicts and, on the other hand, how to foster collaboration;

- Assessing the effects of innovation and organizational change on HEIs’ budgets. This is an important issue to be explored since changes in an HEI’s internal conditions, dynamics, as well as on the relationships between the different agents, can shape the budget model;

- Assessing the main barriers and drivers of organizational change, something which, for example, can potentially allow HEIs to better assess organizational and contextual factors behind the diversity of roles regarding the campus sustainability;

- Addressing the non-voluntary disclosure of sustainable practices. Nowadays, this is crucial since organizations need to be transparent. Their stakeholders increasingly wish to have a clear vision on how HEIs are managed, not only regarding their economic dimension, but also in relation to their social and environmental dimensions.

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Abba, Magaji, Lawan Yahaya, and Naziru Suleiman. 2018. Explored and Critique of Contingency Theory for Management Accounting Research. Journal of Accounting and Financial Management 4: 40–50. [Google Scholar]

- Acevedo, Rafael A., José María Rueda Rincón, and Neley Arcely Rueda. 2014. Contabilidad Gerencial y Toma de Decisiones Emergentes En La Universidad Politécnica Territorial Andrés Eloy Blanco de Barquisimeto, Estado Lara: Un Análisis Fenomenológico. Visión Gerencial 1: 7–26. [Google Scholar]

- Agasisti, Tommaso, Michela Arnaboldi, and Giovanni Azzone. 2008. Strategic Management Accounting in Universities: The Italian Experience. Higher Education 55: 1–15. [Google Scholar] [CrossRef]

- Agyemang, Gloria, and Jane Broadbent. 2015. Management Control Systems and Research Management in Universities: An Empirical and Conceptual Exploration. Accounting, Auditing & Accountability Journal 28: 1018–46. [Google Scholar]

- Ahrens, Thomas, and Rihab Khalifa. 2015. The Impact of Regulation on Management Control: Compliance as a Strategic Response to Institutional Logics of University Accreditation. Qualitative Research in Accounting & Management 12: 106–26. [Google Scholar]

- Al-Htaybat, Khaldoon, and Larissa von Alberti-Alhtaybat. 2013. Management accounting theory revisited: Seeking to increase research relevance. International Journal of Business and Management 8: 12. [Google Scholar]

- Arroyo, Paulina. 2017. A New Taxonomy for Examining the Multi-Role of Campus Sustainability Assessments in Organizational Change. Journal of Cleaner Production 140: 1763–74. [Google Scholar] [CrossRef]

- Bobe, Belete J., and Ralph Kober. 2020. University Dean Personal Characteristics and Use of Management Control Systems and Performance Measures. Studies in Higher Education 45: 235–57. [Google Scholar] [CrossRef]

- Boitier, Marie, and Anne Rivière. 2013. Freedom and Responsibility for French Universities: From Global Steering to Local Management. Accounting, Auditing & Accountability Journal 26: 616–49. [Google Scholar]

- Boitier, Marie, and Anne Rivière. 2016. Management Control Systems, Vectors of a Managerial Logic: Institutional Change and Conflicts of Logics at University. Comptabilite-Controle-Audit 22: 47–79. [Google Scholar] [CrossRef]

- Bollecker, Marc. 2016. The Adoption of Management Accounting at University: The Presence of Internal Cleavages in a Contradictory Institutional Demands Context. Accounting Auditing Control 22: 109–38. [Google Scholar]

- Broadbent, Jane. 2010. The UK Research Assessment Exercise: Performance Measurement and Resource Allocation. Australian Accounting Review 20: 14–23. [Google Scholar] [CrossRef]

- Brusca, Isabel, Margarita Labrador, and Vicente Condor. 2019. Management Accounting Innovations in Universities: A Tool for Decision Making or for Negotiation? Public Performance & Management Review 42: 1138–63. [Google Scholar]

- Chang, Huei-Chun. 2013. Environmental Management Accounting in the Taiwanese Higher Education Sector: Issues and Opportunities. International Journal of Sustainability in Higher Education 14: 133–45. [Google Scholar] [CrossRef]

- Chung, Tze Ki Jennie, Graeme L. Harrison, and Robert C. Reeve. 2009. Interdependencies in Organization Design: A Test in Universities. Journal of Management Accounting Research 21: 55–73. [Google Scholar] [CrossRef]

- Dobija, Dorota, Anna Maria Górska, Giuseppe Grossi, and Wojciech Strzelczyk. 2019. Rational and Symbolic Uses of Performance Measurement: Experiences from Polish Universities. Accounting, Auditing & Accountability Journal 32: 750–81. [Google Scholar]

- del Pino, Eulalia María, Ramón Murguía, and José Motenegro. 2018. Application of a diagnostic methodology for the change of organizational culture in higher education institutions. Revista Espacios 39: 1–9. [Google Scholar]

- El Filali, Yasmine Benabdelkrim, and Mohammed Saber Hassainate. 2018. The Contribution of Management Control to the Improvement of University Performance. Journal of North African Research in Business 2018: 842469. [Google Scholar] [CrossRef]

- Funck, Elin K., and Tom S. Karlsson. 2020. Twenty—five years of studying new public management in public administration: Accomplishments and limitations. Financial Accountability & Management 36: 347–75. [Google Scholar]

- Gong, Maleen Z., and Michael S. C. Tse. 2009. Pick, Mix or Match? A Discussion of Theories for Management Accounting Research. JABM: Journal of Accounting Business and Management 16: 54–66. [Google Scholar]

- Guenther, Thomas W., and Ulrike Schmidt. 2015. Adoption and Use of Management Controls in Higher Education Institutions. In Incentives and Performance. Berlin: Springer, pp. 361–78. [Google Scholar]

- Habersam, Michael, Martin Piber, and Matti Skoog. 2013. Knowledge Balance Sheets in Austrian Universities: The Implementation, Use, and Re-Shaping of Measurement and Management Practices. Critical Perspectives on Accounting 24: 319–37. [Google Scholar] [CrossRef]

- Hardan, Abdullah Salah, and Tareq Mohd Shatnawi. 2013. Impact of Applying the ABC on Improving the Financial Performance in Telecom Companies. International Journal of Business and Management 8: 48. [Google Scholar] [CrossRef]

- Heinicke, Xaver, and Thomas W. Guenther. 2020. The Role of Management Controls in the Higher Education Sector: An Investigation of Different Perceptions. European Accounting Review 29: 581–630. [Google Scholar] [CrossRef]

- Hiebl, Martin R. W. 2014. Upper Echelons Theory in management accounting and control Research. Journal of Management Control 24: 223–40. [Google Scholar] [CrossRef]

- Huerta-Riveros, Patricia C., Héctor G. Gaete-Feres, and Liliana M. Pedraja-Rejas. 2020. Dirección Estratégica, Sistema de Información y Calidad. El Caso de Una Universidad Estatal Chilena. Información Tecnológica 31: 253–66. [Google Scholar] [CrossRef]

- Hutaibat, Khaled. 2019. Accounting for Strategic Management, Strategising and Power Structures in the Jordanian Higher Education Sector. Journal of Accounting& Organizational Change 15: 430–52. [Google Scholar]

- Hutaibat, Khaled, and Zaidoon Alhatabat. 2020. Management Accounting Practices’ Adoption in UK Universities. Journal of Further and Higher Education 44: 1024–38. [Google Scholar] [CrossRef]

- Hutaibat, Khaled, Larissa von Alberti-Alhtaybat, and Khaldoon Al-Htaybat. 2011. Strategic Management Accounting and the Strategising Mindset in an English Higher Education Institutional Context. Journal of Accounting & Organizational Change 7: 358–90. [Google Scholar]

- Jacomossi, Fellipe Andre, and Marcia Zanievicz da Silva. 2016. Influence of Environmental Uncertainty in the Use of Management Control System in a Higher Education Institution/Influencia Da Incerteza Ambiental Na Utilizacao de Sistemas de Controle Gerencial Em Uma Instituicao de Ensino Superior. Revista de Gestao USP 23: 75–86. [Google Scholar] [CrossRef]

- Jansen, E. Pieter. 2018. Bridging the gap between theory and practice in management accounting: Reviewing the literature to shape interventions. Accounting, Auditing & Accountability Journal 31: 1486–509. [Google Scholar]

- Jiang, Darong. 2019. Management Accounting Literature Review—Based on the Development of Management Accounting Research in 2015–17. Modern Economy 10: 2315–34. [Google Scholar] [CrossRef]

- Johnson, H. Thomas, and Robert S. Kaplan. 1987. The Rise and Fall of Management Accounting. IEEE Engineering Management Review 15: 36–44. [Google Scholar] [CrossRef]

- Jones, Larry R., Fred Thompson, and William Zumeta. 1986. Reform of Budget Control in Higher Education. Economics of Education Review 5: 147–58. [Google Scholar] [CrossRef]

- Jovanović, Tatjana, and Martina Dragija. 2018. Application of the Accounting Information at Higher Education Institutions in Slovenia and Croatia-Preparation of Public Policy Framework. International Journal of Public Sector Performance Management 4: 452–66. [Google Scholar] [CrossRef]

- Kallio, Tomi J., Kirsi-Mari Kallio, and Annika Blomberg. 2020. From Professional Bureaucracy to Competitive Bureaucracy--Redefining Universities’ Organization Principles, Performance Measurement Criteria, and Reason for Being. Qualitative Research in Accounting & Management 17: 82–108. [Google Scholar]

- Kenno, Staci A., and Barbara Sainty. 2017. Revising the Budgeting Model: Challenges of Implementation at a University. Journal of Applied Accounting Research 18: 496–510. [Google Scholar] [CrossRef]

- Kont, Kate-Riin, and Signe Jantson. 2011. Activity-Based Costing (ABC) and Time-Driven Activity-Based Costing (TDABC): Applicable Methods for University Libraries? Evidence Based Library and Information Practice 6: 107–19. [Google Scholar] [CrossRef]

- Küpper, Hans-Ulrich. 2013. A Specific Accounting Approach for Public Universities. Journal of Business Economics 83: 805–29. [Google Scholar] [CrossRef]

- Laitinen, Erkki K. 2003. Future-Based Management Accounting: A New Approach with Survey Evidence. Critical Perspectives on Accounting 14: 293–323. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas G. Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter C. Gøtzsche, John P. A. Ioannidis, Mike Clarke, P. J. Devereaux, Jos Kleijnen, and David Moher. 2009. The PRISMA Statement for Reporting Systematic Reviews and Meta-Analyses of Studies That Evaluate Health Care Interventions: Explanation and Elaboration. Journal of Clinical Epidemiology 62: e1–34. [Google Scholar] [CrossRef]

- Marlina, Evi, and Bambang Tjahjadi. 2020. Strategic management accounting and university performance: A critical review. Academy of Strategic Management Journal 19: 1–5. [Google Scholar]

- Marlina, Evi, Hendri Ali Ardi, Siti Samsiah, Kirmizi Ritonga, and Amris Rusli Tanjung. 2020. Strategic Costing Models as Strategic Management Accountin Techniques at Private Universities in Riau, Indonesia. International Journal of Financial Research 11: 274–83. [Google Scholar] [CrossRef]

- Martin-Sardesai, Ann. 2016. Institutional Entrepreneurship and Management Control Systems. Pacific Accounting Review 28: 458–70. [Google Scholar] [CrossRef]

- Martin-Sardesai, Ann, James Guthrie, Stuart Tooley, and Sally Chaplin. 2019. History of Research Performance Measurement Systems in the Australian Higher Education Sector. Accounting History 24: 40–61. [Google Scholar] [CrossRef]

- Minelli, Eliana, Gianfranco Rebora, and Matteo Turri. 2015. Quest for Accountability: Exploring the Evaluation Process of Universities. Quality in Higher Education 21: 103–31. [Google Scholar] [CrossRef]

- Modell, Sven. 2006. Institutional and Negotiated Order Perspectives on Cost Allocations: The Case of the Swedish University Sector. European Accounting Review 15: 219–51. [Google Scholar] [CrossRef]

- Molina-Sanchez, Horacio, Antonio Ariza-Montes, Mar Ortiz-Gomez, and Antonio Leal-Rodriguez. 2019. The Subjective Well-Being Challenge in the Accounting Profession: The Role of Job Resources. International Journal of Environmental Research and Public Health 16: 3073. [Google Scholar] [CrossRef]

- Ozdil, Esin, and Zahirul Hoque. 2017. Budgetary Change at a University: A Narrative Inquiry. The British Accounting Review 49: 316–28. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 Statement: An Updated Guideline for Reporting Systematic Reviews. BMJ 372: 1–9. [Google Scholar] [CrossRef]

- Palowski, Henry T. 2011. Misinterpretation of the Strategic Significance of Cost Driver Analysis: Evidence from Management Accounting Theory and Practice. Ekonomika Regiona 2: 131. [Google Scholar] [CrossRef]

- Pelz, Michael. 2019. Can management accounting Be helpful for young and small companies? Systematic review of a paradox. International Journal of Management Reviews 21: 256–74. [Google Scholar] [CrossRef]

- Petrides, Lisa A., Sara I. McClelland, and Thad R. Nodine. 2004. Costs and Benefits of the Workaround: Inventive Solution or Costly Alternative. International Journal of Educational Management 18: 100–8. [Google Scholar] [CrossRef]

- Pilonato, Silvia, and Patrizio Monfardini. 2020. Performance Measurement Systems in Higher Education: How Levers of Control Reveal the Ambiguities of Reforms. The British Accounting Review 52: 100908. [Google Scholar] [CrossRef]

- Rashid, Tayyab, and Robert McGrath. 2020. Strengths-Based Actions to Enhance Wellbeing in the Time of COVID-19. International Journal of Wellbeing 10: 113–32. [Google Scholar] [CrossRef]

- Sánchez, Rosario del Río, Vanessa Rodriguez Cornejo, Teresa García-Valderrama, and Jaime Sanchez-Ortiz. 2019. Design of the activities map with the ABC cost model for the university departments. Cuadernos de Gestion 19: 159–84. [Google Scholar] [CrossRef]

- Scapens, Robert W. 2012. Institutional Theory and Management Accounting Research. Maandblad Voor Accountancy En Bedrijfseconomie 86: 401. [Google Scholar] [CrossRef]

- Schaltegger, Stefan, and Dimitar Zvezdov. 2015. Gatekeepers of Sustainability Information: Exploring the Roles of Accountants. Journal of Accounting and Organizational Change 11: 333. [Google Scholar] [CrossRef]

- Shields, Michael D. 2018. A Perspective on Management Accounting Research. Journal of Management Accounting Research 30: 1–11. [Google Scholar] [CrossRef]

- Sizer, John. 1981. Performance Assessment in Institutions of Higher Education under Conditions of Financial Stringency, Contraction and Changing Needs: A Management Accounting Perspective. Accounting and Business Research 11: 227–42. [Google Scholar] [CrossRef]

- Sulaiman, Maliah, and Noredah Abdul Rahman. 2013. Does the Environment Matter? Empirical Evidence from an Institution of Higher Learning in Malaysia. International Journal of Business & Society 14: 177–92. [Google Scholar]

- Sutton, Nicole C., and David A. Brown. 2016. The Illusion of No Control: Management Control Systems Facilitating Autonomous Motivation in University Research. Accounting & Finance 56: 577–604. [Google Scholar]

- Tranfield, David, David Denyer, and Palminder Smart. 2003. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review*. British Journal of Management 14: 207–22. [Google Scholar] [CrossRef]

- Tsamenyi, Mathew, Irvan Noormansyah, and Shahzad Uddin. 2008. Management Controls in Family-Owned Businesses (FOBs): A Case Study of an Indonesian Family-Owned University. Accounting Forum 32: 62–74. [Google Scholar] [CrossRef]

- Van Kemenade, Everard, Mike Pupius, and Teun W Hardjono. 2008. More Value to Defining Quality. Quality in Higher Education 14: 175–85. [Google Scholar] [CrossRef]

- Visser, Max. 2016. Management Control, Accountability, and Learning in Public Sector Organizations: A Critical Analysis. In Governance and Performance in Public and Non-Profit Organizations. Bingley: Emerald Group Publishing Limited. [Google Scholar]

- Wigmore-Álvarez, Amber, and Mercedes Ruiz-Lozano. 2014. The United Nations Global Compact Progress Reports as Management Control Instruments for Social Responsibility at Spanish Universities. Sage Open 4. [Google Scholar] [CrossRef]

- Yakhou, Mehenna, and Kevin Ulshafer. 2012. Adapting the Balanced Scorecard and Activity-Based Costing to Higher Education Institutions. International Journal of Management in Education 6: 258–72. [Google Scholar] [CrossRef]

- Xie, Jie. 2019. Review of chinese and foreign management accounting research based on management accounting research topics and research methods. Open Journal of Social Sciences 7: 107–19. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Theories | Authors |

|---|---|

| Institutional Theory | Ozdil and Hoque (2017) |

| Dobija et al. (2019) | |

| Modell (2006) | |

| Boitier and Rivière (2013) | |

| Bollecker (2016) | |

| Hutaibat and Alhatabat (2020) | |

| Minelli et al. (2015) | |

| Isomorphism Theory | Dobija et al. (2019) |

| Bollecker (2016) | |

| Agasisti et al. (2008) | |

| Brusca et al. (2019) | |

| Bourdieu’s Theory of Practice | Hutaibat et al. (2011) |

| Hutaibat (2019) | |

| Grounded Theory | Hutaibat et al. (2011) |

| Hutaibat (2019) | |

| Rational Choice Theory | Ozdil and Hoque (2017) |

| Self-Referential Theory | Agasisti et al. (2008) |

| Self-Determination Theory | Sutton and Brown (2016) |

| Negotiated Order | Modell (2006) |

| Contingency Theory | Hutaibat and Alhatabat (2020) |

| Cost Inducers Theory | Palowski (2011) |

| Organizational Control Theory | Minelli et al. (2015) |

| Professionalism Theory | Heinicke and Guenther (2020) |

| Upper Echelons Theory | Bobe and Kober (2020) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vale, J.; Amaral, J.; Abrantes, L.; Leal, C.; Silva, R. Management Accounting and Control in Higher Education Institutions: A Systematic Literature Review. Adm. Sci. 2022, 12, 14. https://doi.org/10.3390/admsci12010014

Vale J, Amaral J, Abrantes L, Leal C, Silva R. Management Accounting and Control in Higher Education Institutions: A Systematic Literature Review. Administrative Sciences. 2022; 12(1):14. https://doi.org/10.3390/admsci12010014

Chicago/Turabian StyleVale, José, Joana Amaral, Luís Abrantes, Carmem Leal, and Rui Silva. 2022. "Management Accounting and Control in Higher Education Institutions: A Systematic Literature Review" Administrative Sciences 12, no. 1: 14. https://doi.org/10.3390/admsci12010014

APA StyleVale, J., Amaral, J., Abrantes, L., Leal, C., & Silva, R. (2022). Management Accounting and Control in Higher Education Institutions: A Systematic Literature Review. Administrative Sciences, 12(1), 14. https://doi.org/10.3390/admsci12010014