Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review

Abstract

:1. Introduction

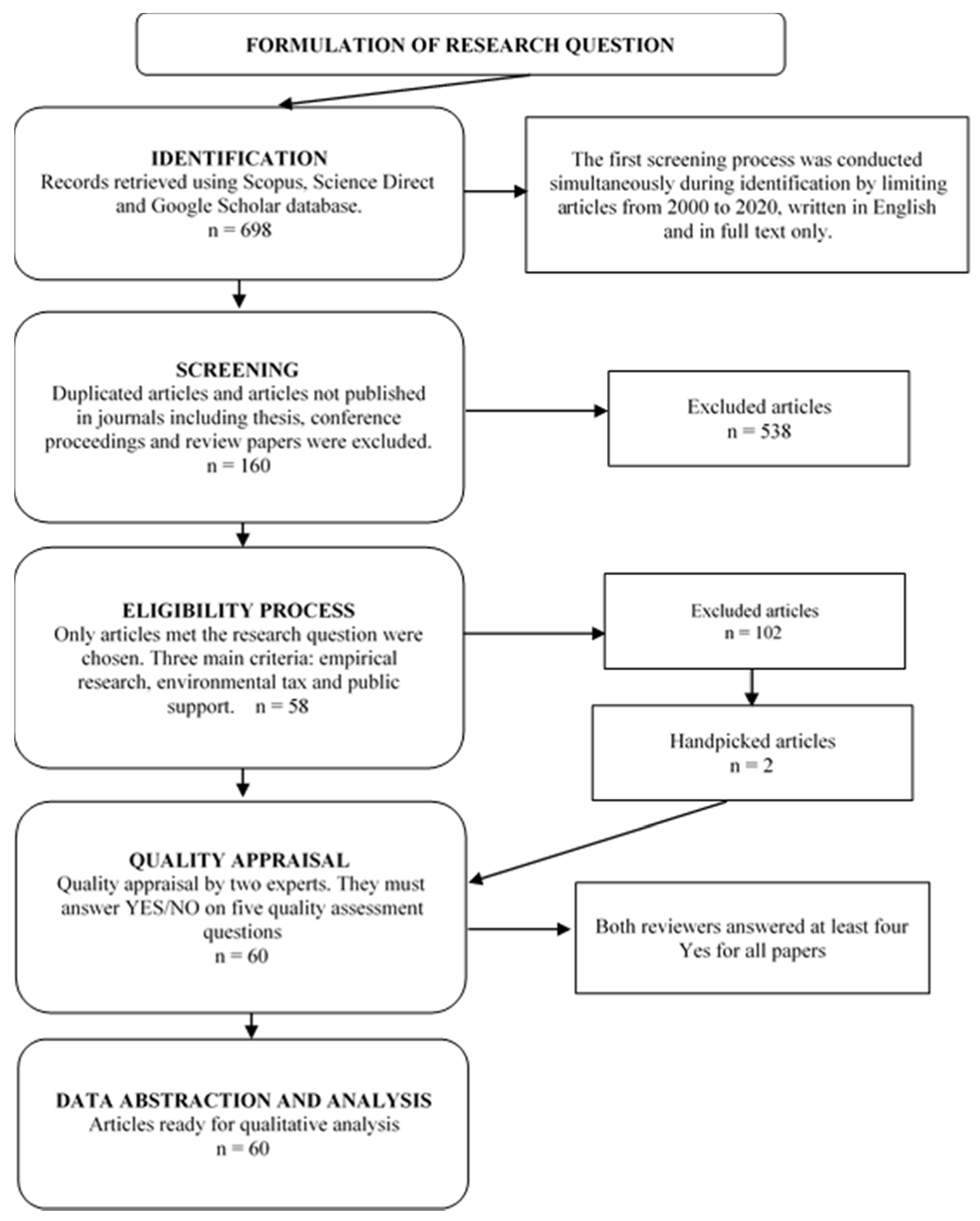

2. Methodology

2.1. Review Protocol and Research Question

2.2. Systematic Search Strategies

2.3. Quality Appraisal

2.4. Data Abstraction and Analysis

3. Results

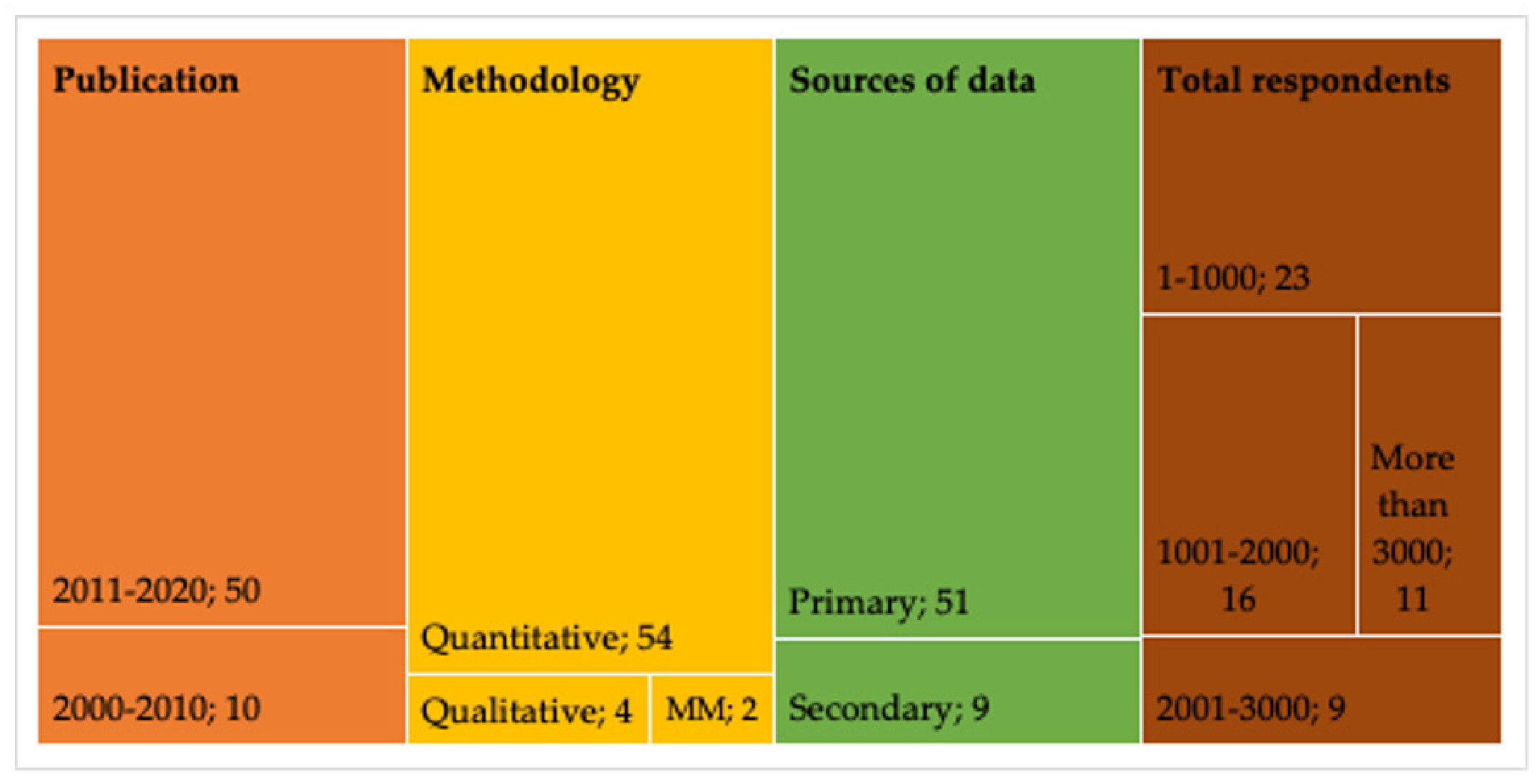

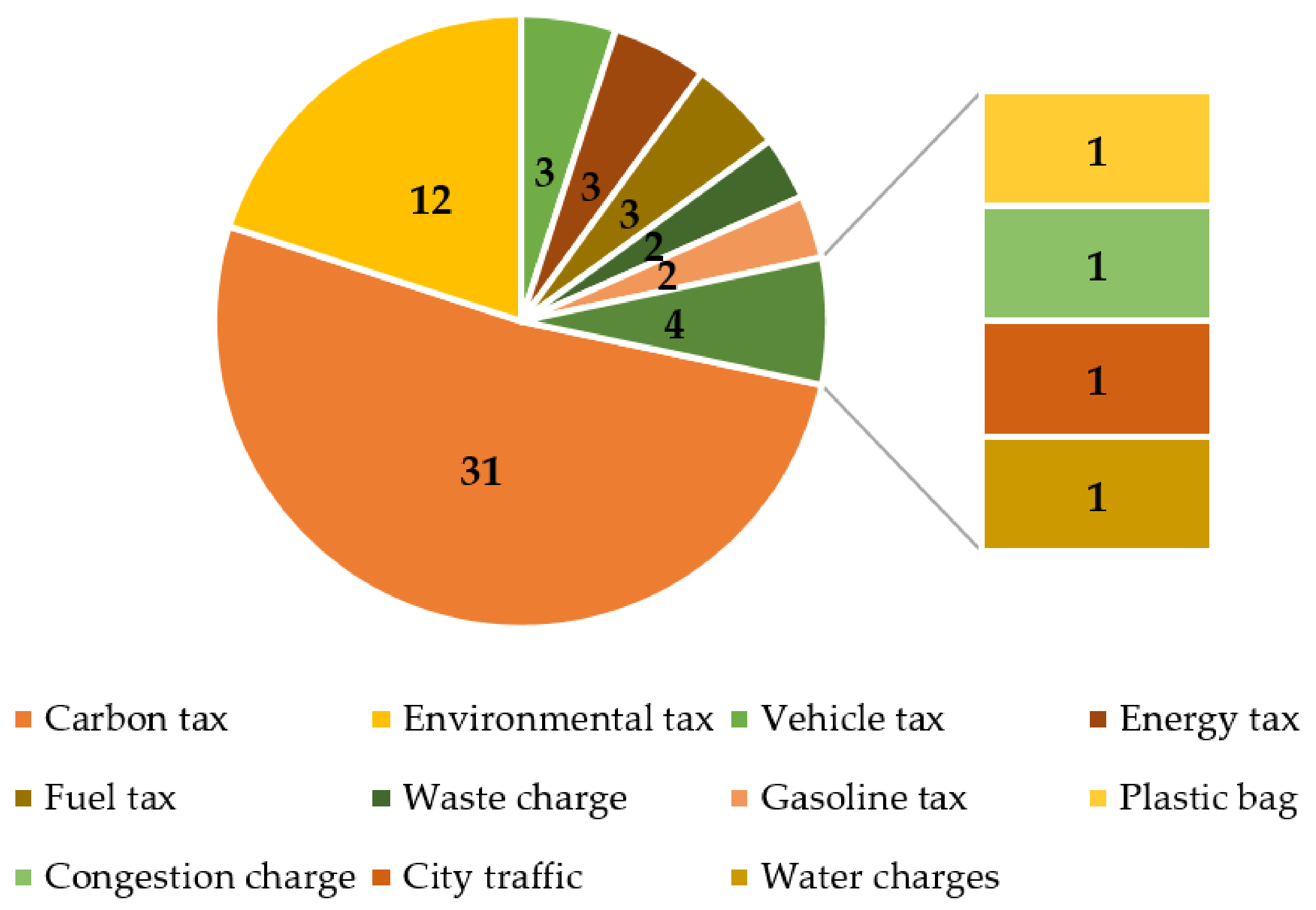

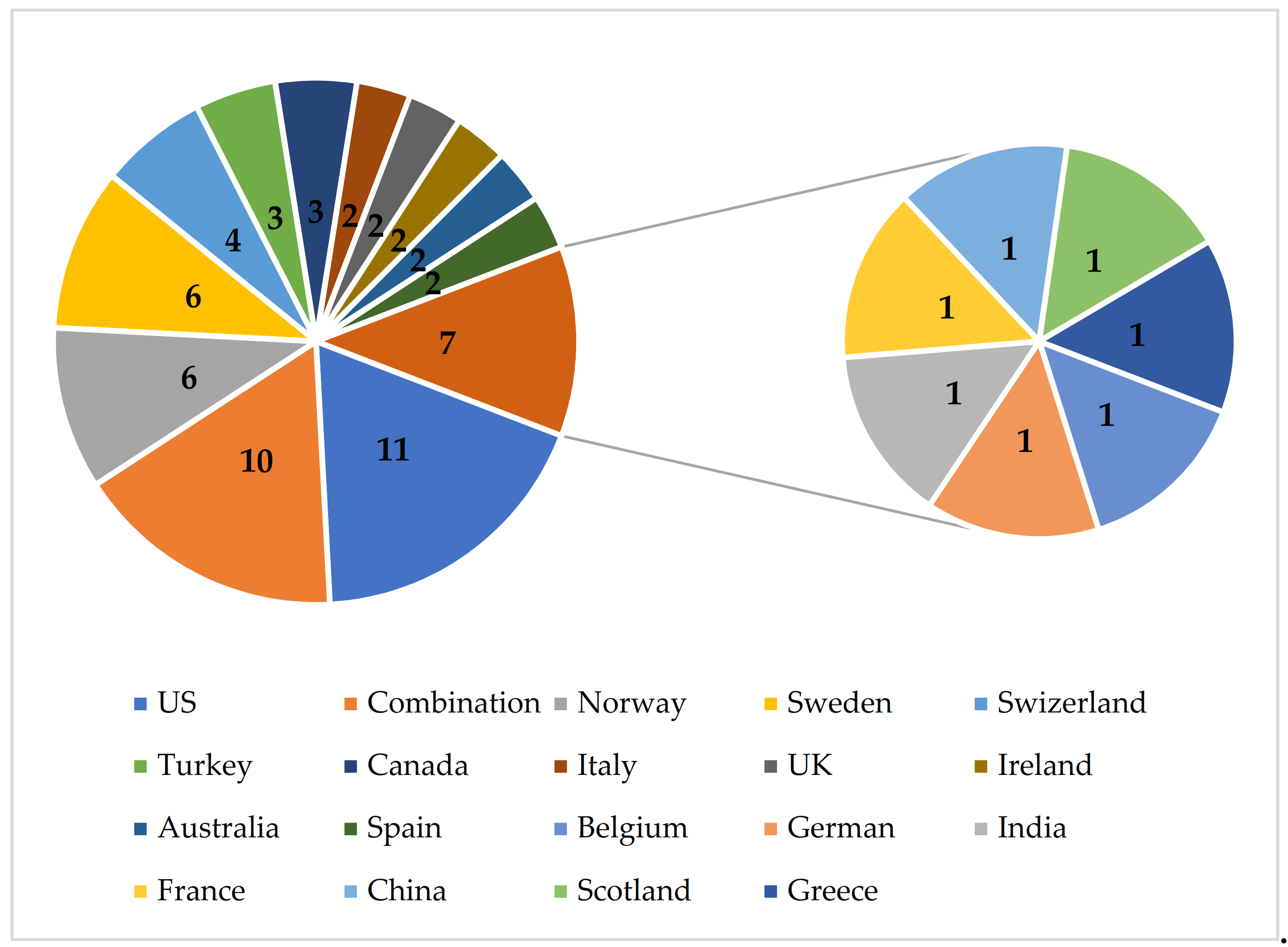

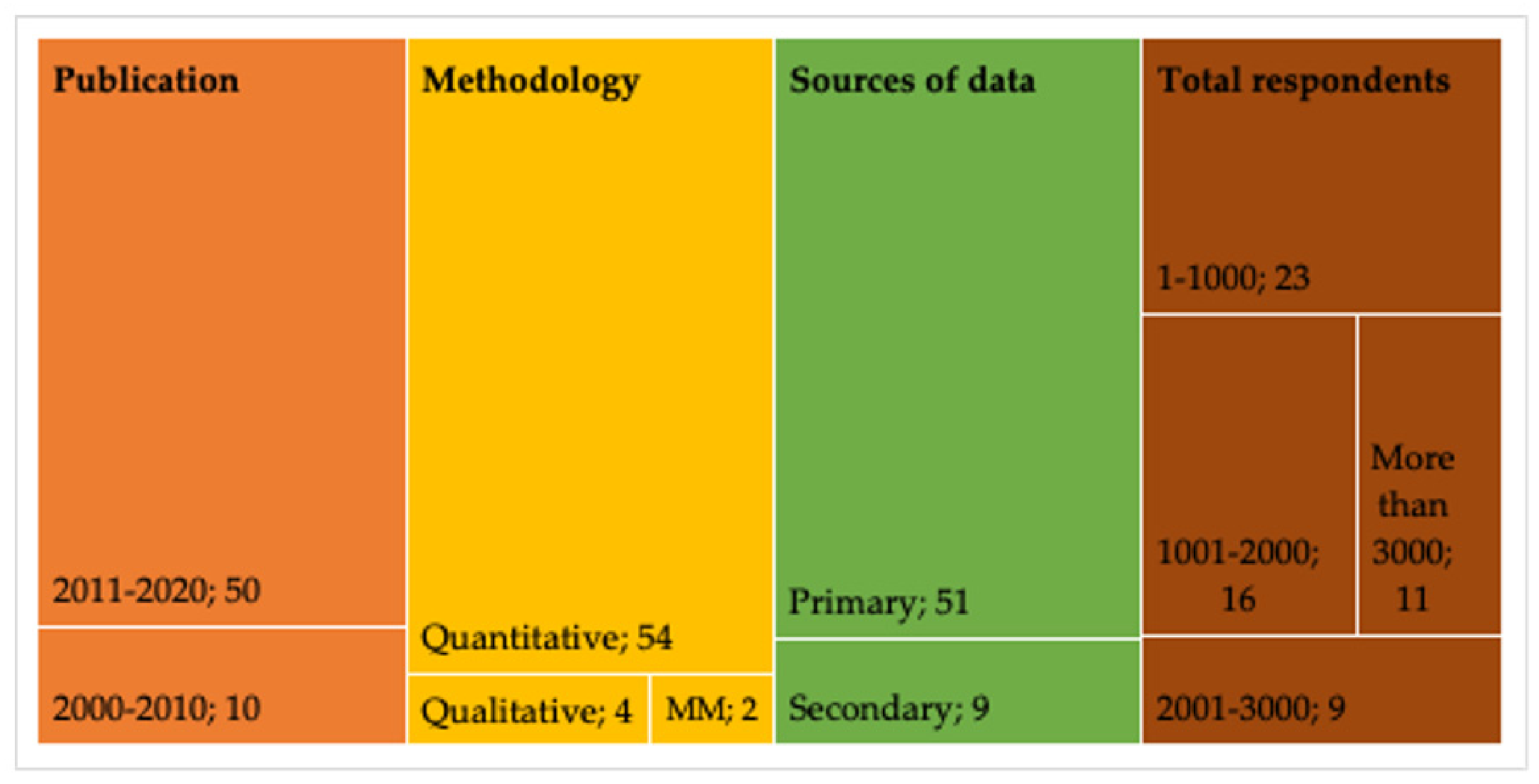

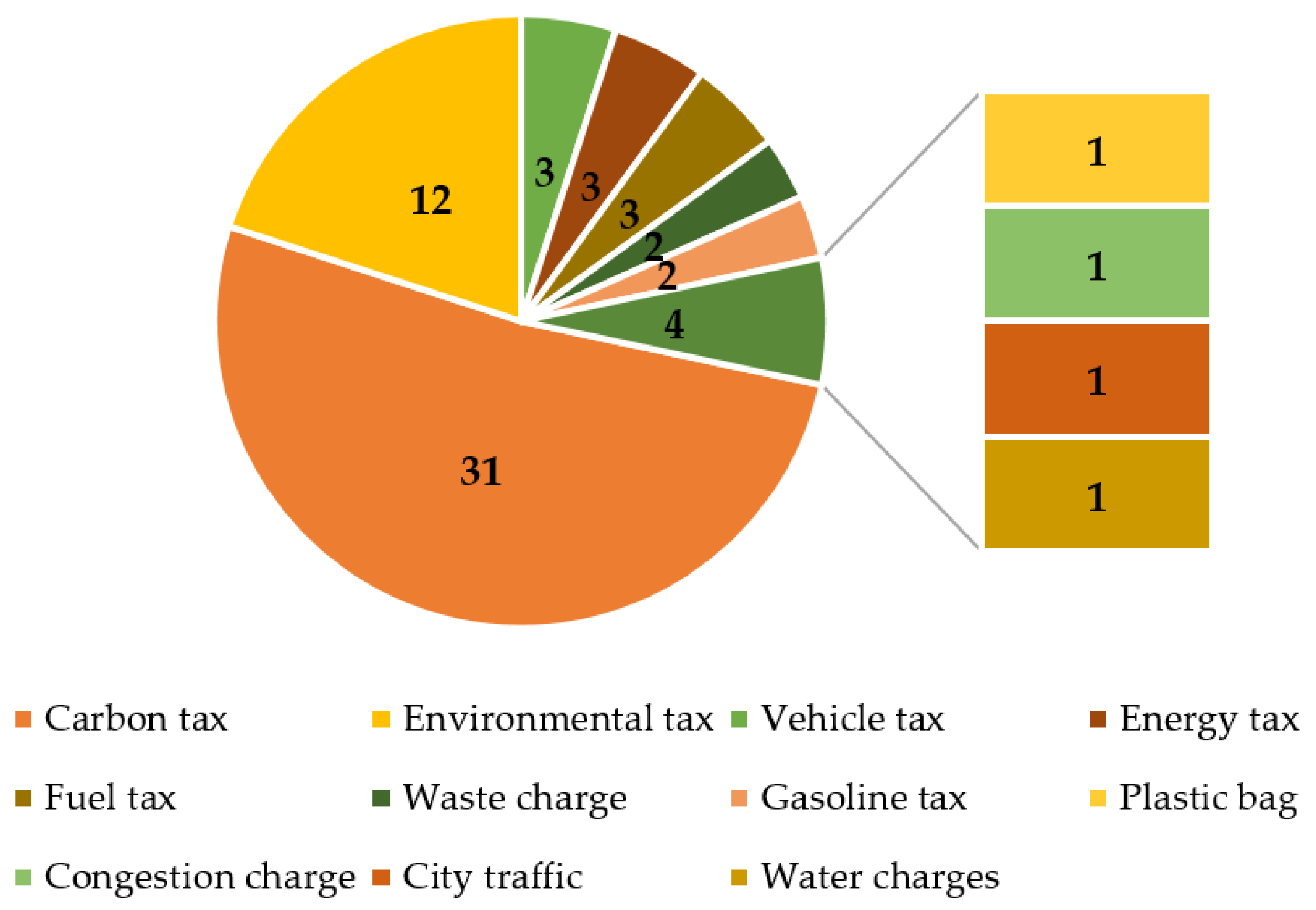

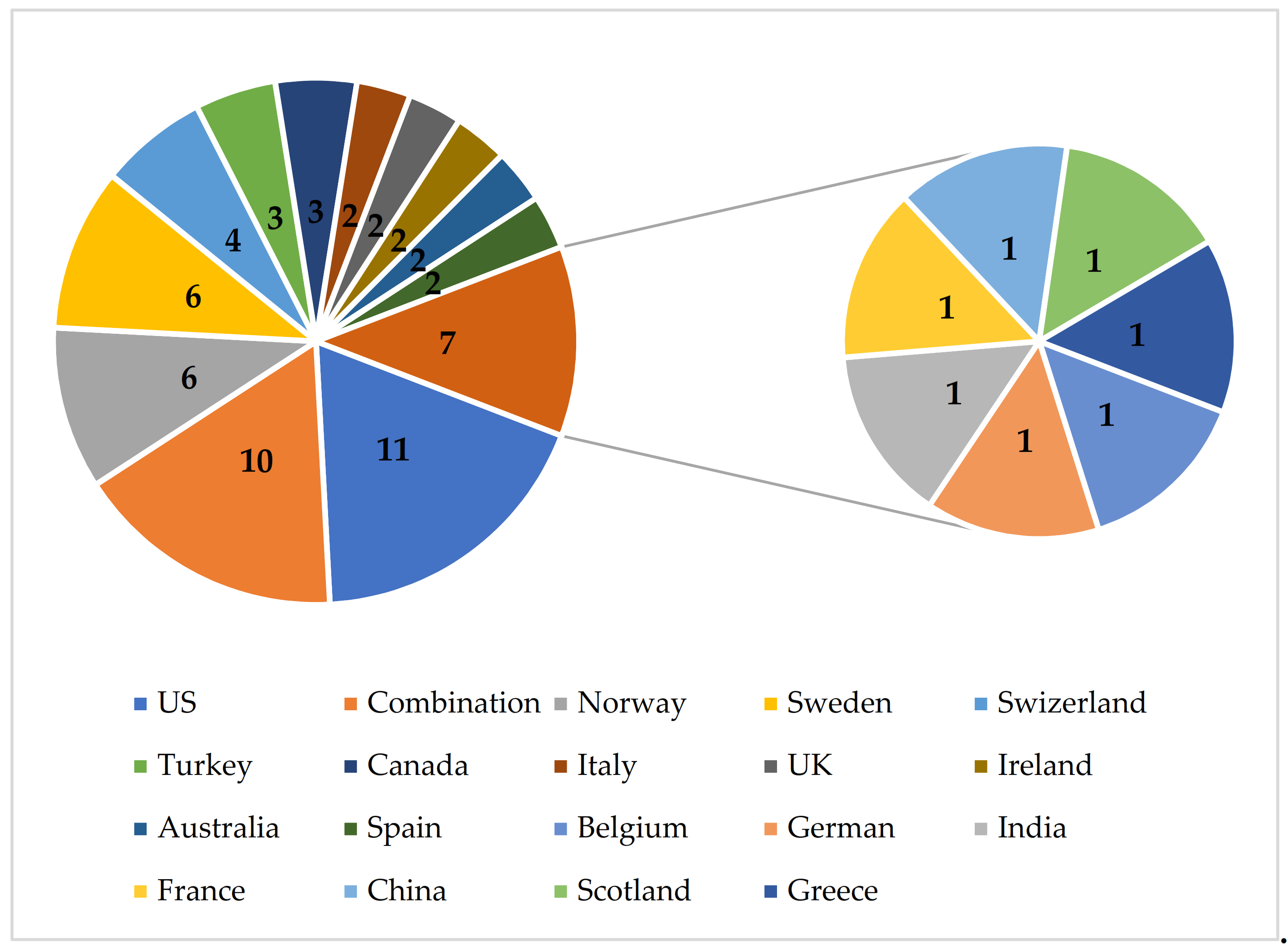

3.1. Overview of the Articles

3.2. Measuring of Public Acceptance

3.3. Themes and Sub-Themes for Factors That Influence Public Support

3.3.1. Policy

3.3.2. Governance

3.3.3. Personal Traits

3.3.4. Demographic

4. Discussions

4.1. Implications to the Policy and Practice

4.2. Suggestions for Future Research

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Theme | Policy | Governance | Personal Traits | Demographic | ||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sub-Theme | Use of Revenue | Effectiveness | Cost Distribution | Type of Policy | Information Dissemination | Tax Rate | Competitiveness | Experience | Exemption | Political Value Orientation | Trust | Efforts in Protecting Environment | QoG | Perceived Severity of Climate Change | Environmental Protection | Psychological | Social Sharing | Good Health | Actual Polluter | Visited Abroad | Location | Income | Gender | Education | Age | Energy Dependency | Household Size | Parenthood | Race | Employment | Religion | Religiosity | |

| 1 | Adaman et al. (2011) [39] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||

| 2 | Agrawal et al. (2010) [70] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||

| 3 | Alberini et al. (2018) [76] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 4 | Amdur et al. (2015) [71] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||

| 5 | Bachus et al. (2019) [75] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||

| 6 | Baranzini & Carrattini (2016) [35] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||

| 7 | Beiser-McGrath & Bernauer (2019) [40] | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||

| 8 | Bergquist et al. (2020) [16] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||

| 9 | Beuermann & Santarius (2006) [41] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| 10 | Birol & Das (2010) [77] | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||

| 11 | Bristow, et al. (2010) [50] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 12 | Brown & Johnstone (2014) [51] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||

| 13 | Bullock & Theodoridis (2017) [53] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 14 | Carattini et al. (2017) [10] | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||

| 15 | Clayton (2018) [67] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||

| 16 | Cherry et al. (2012) [44] | ✓ | ✓ | ||||||||||||||||||||||||||||||

| 17 | Cherry et al. (2014) [65] | ✓ | |||||||||||||||||||||||||||||||

| 18 | Convery et al. (2014) [42] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 19 | Davidovic et al. (2019) [33] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||

| 20 | Denstadli & Veisten (2020) [64] | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||

| 21 | Dolšak et al. (2020) [17] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 22 | Dounne & Fabre (2020) [18] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| 23 | Dreyer & Walker (2013) [48] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 24 | Duan et al. (2014) [73] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||

| 25 | Eliasson & Jonsson (2011) [79] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| 26 | Fairbrother (2017) [36] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||

| 27 | Fairbrother et al. (2019) [30] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||

| 28 | Feldman & Hart (2018) [36] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| 29 | Gevrek & Uyduranoglu (2015) [57] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 30 | Grimsrud et al. (2019) [58] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||

| 31 | Hammar & Jagers (2006) [68] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||

| 32 | Hammar & Jagers (2007) [49] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||

| 33 | Harring & Jagers (2013) [72] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| 34 | Heres et al. (2017) [45] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 35 | Hsu (2010) [78] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||

| 36 | Hsu et al. (2008) [56] | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||

| 37 | Jagers & Hammar (2009) [46] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 38 | Jagers et al. (2018) [61] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 39 | Kallbekken & Aasen (2010) [62] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 40 | Kallbekken & Sæælen (2011) [63] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||

| 41 | Kenny (2019) [74] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||

| 42 | Kim et al. (2013) [37] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| 43 | Kim & Shin (2015) [32] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 44 | Kotchen et al. (2017) [69] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||

| 45 | Lo et al. (2013) [43] | ✓ | ✓ | ||||||||||||||||||||||||||||||

| 46 | Long et al. (2020) [19] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||

| 47 | McLaughlin et al. (2019) [54] | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||

| 48 | Migheli (2018) [80] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 49 | Nastis & Mattas (2018) [34] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 50 | Nowlin et al. (2020) [20] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 51 | Rhodes et al. (2017) [47] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||

| 52 | Rotaris & Danielis (2019) [60] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||

| 53 | Rosentrater et al. (2013) [38] | ✓ | ✓ | ✓ | |||||||||||||||||||||||||||||

| 54 | Sælen & Kallbekken (2011) [59] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 55 | Savin et al. (2020) [22] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||

| 56 | Thalmann (2004) [55] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||

| 57 | Umit & Schaffer (2020) [29] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 58 | Uyduranoglu & Ozturk (2020) [21] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||

| 59 | Wicki et al. (2019) [31] | ✓ | ✓ | ✓ | ✓ | ||||||||||||||||||||||||||||

| 60 | Wicki et al. (2020) [23] | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||||||||||||||

| Total | 31 | 22 | 18 | 17 | 12 | 11 | 6 | 2 | 1 | 23 | 21 | 1 | 1 | 21 | 18 | 6 | 8 | 1 | 1 | 1 | 31 | 30 | 30 | 28 | 21 | 17 | 6 | 4 | 4 | 2 | 1 | 1 | |

References

- Fullerton, D.; Leicester, A.; Smith, S. Environmental Taxes. In Institute for Fiscal Studies (ed) Dimensions of Tax Design; Oxford University Press: Oxford, UK, 2010; pp. 428–549. [Google Scholar]

- OECD. Aligning Policies for a Low-Carbon Economy; OECD Publishing: Paris, France, 2015. [Google Scholar]

- United National Framework Convention on Climate Change (UNFCCC). Paris Agreement. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf. (accessed on 10 August 2021).

- Aldy, J.E.; Stavins, R.N. The Promise and Problems of Pricing Carbon: Theory and Experience. J. Environ. Dev. 2012, 21, 152–180. [Google Scholar] [CrossRef]

- OECD. Taxing Energy Use for Sustainable Development; OECD Publishing: Paris, France, 2021. [Google Scholar]

- Baranzini, A.; Caliskan, M.; Carattini, S. Economic Prescriptions and Public Responses to Climate Policy. SSRN Electron. J. 2014, 3, 1–19. [Google Scholar]

- OECD; World Bank. The FASTER Principles for Successful Carbon Pricing: An Approach Based on Initial Experience; OECD: Washington, DC, USA, 2015. [Google Scholar]

- Partnership for Market Readiness. Carbon Tax Guide: A Hand Book for Policy Makers; World Bank: Wanshington, DC, USA, 2017. [Google Scholar]

- Heine, D.; Black, S. Benefits beyond Climate: Environmental Tax Reform. In Fiscal Policies for Development and Climate Action; Wanshington, DC, USA, 2019; pp. 1–185. Available online: https://www.researchgate.net/publication/332135012_Benefits_beyond_Climate_Environmental_Tax_Reform (accessed on 8 October 2021).

- Carattini, S.; Baranzini, A.; Thalmann, P.; Varone, F.; Vöhringer, F. Green Taxes in a Post-Paris World: Are Millions of Nays Inevitable? Environ. Resour. Econ. 2017, 68, 97–128. [Google Scholar] [CrossRef] [Green Version]

- Haddaway, N.R.; Macura, B.; Whaley, P.; Pullin, A.S. ROSES Reporting Standards for Systematic Evidence Syntheses: Pro Forma, Flow-Diagram and Descriptive Summary of the Plan and Conduct of Environmental Systematic Reviews and Systematic Maps. Environ. Evid. 2018, 7, 1–8. [Google Scholar] [CrossRef]

- Okoli, C. A Guide to Conducting a Standalone Systematic Literature Review. Commun. Assoc. Inf. Syst. 2015, 37, 879–910. [Google Scholar] [CrossRef] [Green Version]

- Gusenbauer, M.; Haddaway, N.R. Which Academic Search Systems Are Suitable for Systematic Reviews or Meta-Analyses? Evaluating Retrieval Qualities of Google Scholar, PubMed, and 26 Other Resources. Res. Synth. Methods 2020, 11, 181–217. [Google Scholar] [CrossRef] [Green Version]

- Haddaway, N.R.; Collins, A.M.; Coughlin, D.; Kirk, S. The Role of Google Scholar in Evidence Reviews and Its Applicability to Grey Literature Searching. PLoS ONE 2015, 10, e0138237. [Google Scholar] [CrossRef] [Green Version]

- Shaffril, H.A.M.; Samsuddin, S.F.; Samah, A.A. The ABC of Systematic Literature Review: The Basic Methodological Guidance for Beginners. Qual. Quant. 2020, 55, 1319–1346. [Google Scholar] [CrossRef]

- Bergquist, P.; Mildenberger, M.; Stokes, L.C. Combining Climate, Economic, and Social Policy Builds Public Support for Climate Action in the US. Environ. Res. Lett. 2020, 15, 1–9. [Google Scholar] [CrossRef]

- Dolšak, N.; Adolph, C.; Prakash, A. Policy Design and Public Support for Carbon Tax: Evidence from a 2018 US National Online Survey Experiment. Public Adm. 2020, 98, 905–921. [Google Scholar] [CrossRef]

- Douenne, T.; Fabre, A. French Attitudes on Climate Change, Carbon Taxation and Other Climate Policies. Ecol. Econ. 2020, 169, 1–19. [Google Scholar] [CrossRef]

- Long, Z.; Axsen, J.; Kitt, S. Public Support for Supply-Focused Transport Policies: Vehicle Emissions, Low-Carbon Fuels, and ZEV Sales Standards in Canada and California. Transp. Res. Part A Policy Pract. 2020, 141, 98–115. [Google Scholar] [CrossRef]

- Nowlin, M.C.; Gupta, K.; Ripberger, J.T. Revenue Use and Public Support for a Carbon Tax. Environ. Res. Lett. 2020, 15, 1–11. [Google Scholar] [CrossRef]

- Uyduranoglu, A.; Ozturk, S.S. Public Support for Carbon Taxation in Turkey: Drivers and Barriers. Clim. Policy 2020, 20, 1175–1191. [Google Scholar] [CrossRef]

- Savin, I.; Drews, S.; Maestre-Andrés, S.; van den Bergh, J. Public Views on Carbon Taxation and Its Fairness: A Computational-Linguistics Analysis. Clim. Change 2020, 162, 2107–2138. [Google Scholar] [CrossRef]

- Wicki, M.; Huber, R.A.; Bernauer, T. Can Policy-Packaging Increase Public Support for Costly Policies? Insights from a Choice Experiment on Policies against Vehicle Emissions. J. Public Policy 2020, 40, 599–625. [Google Scholar] [CrossRef] [Green Version]

- Thomas, J.; Noel-Storr, A.; Marshall, I.; Wallace, B.; McDonald, S.; Mavergames, C.; Glasziou, P.; Shemilt, I.; Synnot, A.; Turner, T.; et al. Living Systematic Reviews: 2. Combining Human and Machine Effort. J. Clin. Epidemiol. 2017, 91, 31–37. [Google Scholar] [CrossRef] [Green Version]

- Petticrew, M.; Roberts, H. Systematic Reviews in the Social Sciences: A Practical Guide. Couns. Psychother. Res. 2006, 6, 304–305. [Google Scholar]

- Whittemore, R.; Knafl, K. The Integrative Review: Updated Methodology. J. Adv. Nurse 2005, 52, 546–553. [Google Scholar] [CrossRef]

- Flemming, K.; Booth, A.; Garside, R.; Tunçalp, Ö.; Noyes, J. Qualitative Evidence Synthesis for Complex Interventions and Guideline Development: Clarification of The Purpose, Designs and Relevant Methods. BMJ Glob. Health 2018, 4, 1–9. [Google Scholar] [CrossRef]

- Dresner, S.; Dunne, L.; Clinch, P.; Beuermann, C. Social and Political Responses to Ecological Tax Reform in Europe: An Introduction to the Special Issue. Energy Policy 2006, 34, 895–904. [Google Scholar] [CrossRef]

- Umit, R.; Schaffer, L.M. Attitudes Towards Carbon Taxes Across Europe: The Role of Perceived Uncertainty and Self-Interest. Energy Policy 2020, 140, 1–7. [Google Scholar] [CrossRef]

- Fairbrother, M.; Johansson Sevä, I.; Kulin, J. Political Trust and the Relationship between Climate Change Beliefs and Support for Fossil Fuel Taxes: Evidence from a Survey of 23 European Countries. Glob. Environ. Chang. 2019, 59, 1–15. [Google Scholar] [CrossRef]

- Wicki, M.; Fesenfeld, L.; Bernauer, T. In Search of Politically Feasible Policy-Packages for Sustainable Passenger Transport: Insights from Choice Experiments in China, Germany, and the USA. Environ. Res. Lett. 2019, 14, 1–17. [Google Scholar] [CrossRef]

- Kim, S.; Shin, W. Understanding American and Korean Students’ Support for Pro-Environmental Tax Policy: The Application of the Value–Belief–Norm Theory of Environmentalism. Environ. Commun. 2015, 11, 311–331. [Google Scholar] [CrossRef]

- Davidovic, D.; Harring, N.; Jagers, S.C. The Contingent Effects of Environmental Concern and Ideology: Institutional Context and People’s Willingness to Pay Environmental Taxes. Environ. Polit. 2019, 29, 674–696. [Google Scholar] [CrossRef] [Green Version]

- Nastis, S.A.; Mattas, K. Income Elasticity of Willingness-to-Pay for a Carbon Tax in Greece. Int. J. Glob. Warm. 2018, 14, 510–524. [Google Scholar] [CrossRef]

- Baranzini, A.; Carattini, S. Effectiveness, Earmarking and Labeling: Testing the Acceptability of Carbon Taxes with Survey Data. Environ. Econ. Policy Stud. 2016, 19, 197–227. [Google Scholar] [CrossRef] [Green Version]

- Feldman, L.; Hart, P.S. Climate Change as a Polarizing Cue: Framing Effects on Public Support for Low-Carbon Energy Policies. Glob. Environ. Chang. 2018, 51, 54–66. [Google Scholar] [CrossRef]

- Kim, J.; Schmöcker, J.D.; Fujii, S.; Noland, R.B. Attitudes towards Road Pricing and Environmental Taxation among US and UK Students. Transp. Res. Part A Policy Pract. 2013, 48, 50–62. [Google Scholar] [CrossRef] [Green Version]

- Rosentrater, L.D.; Sælensminde, I.; Ekström, F.; Böhm, G.; Bostrom, A.; Hanss, D.; O’Connor, R.E. Efficacy Trade-Offs in Individuals’ Support for Climate Change Policies. Environ. Behav. 2013, 45, 935–970. [Google Scholar] [CrossRef]

- Adaman, F.; Karalidotless, N.; Kumbaroĝlu, G.; Or, I.; Özkaynak, B.; Zenginobuz, Ü. What Determines Urban Households’ Willingness to Pay for CO2 Emission Reductions in Turkey: A Contingent Valuation Survey. Energy Policy 2011, 39, 689–698. [Google Scholar] [CrossRef]

- Beiser-McGrath, L.F.; Bernauer, T. Could Revenue Recycling Make Effective Carbon Taxation Politically Feasible? Sci. Adv. 2019, 5, 1–9. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Beuermann, C.; Santarius, T. Ecological Tax Reform in Germany: Handling Two Hot Potatoes at the Same Time. Energy Policy 2006, 34, 917–929. [Google Scholar] [CrossRef]

- Convery, F.; Dunne, L.; Joyce, D. Ireland’s Carbon Tax in the Context of the Fiscal Crisis. Cyprus Econ. Policy Rev. 2014, 8, 135–143. [Google Scholar]

- Lo, A.Y.; Alexander, K.S.; Proctor, W.; Ryan, A. Reciprocity as Deliberative Capacity: Lessons from a Citizen’s Deliberation on Carbon Pricing Mechanisms in Australia. Environ. Plan. C Gov. Policy 2013, 31, 444–459. [Google Scholar] [CrossRef] [Green Version]

- Cherry, T.L.; Kallbekken, S.; Kroll, S. The Acceptability of Efficiency-Enhancing Environmental Taxes, Subsidies and Regulation: An Experimental Investigation. Environ. Sci. Policy 2012, 16, 90–96. [Google Scholar] [CrossRef] [Green Version]

- Heres, D.R.; Kallbekken, S.; Galarraga, I. The Role of Budgetary Information in the Preference for Externality-Correcting Subsidies over Taxes: A Lab Experiment on Public Support. Environ. Resour. Econ. 2015, 66, 1–15. [Google Scholar] [CrossRef]

- Jagers, S.C.; Hammar, H. Environmental Taxation for Good and for Bad: The Effciency and Legitimacy of Sweden’s Carbon Tax. Environ. Polit. 2009, 18, 218–237. [Google Scholar] [CrossRef]

- Rhodes, E.; Axsen, J.; Jaccard, M. Exploring Citizen Support for Different Types of Climate Policy. Ecol. Econ. 2017, 137, 56–69. [Google Scholar] [CrossRef]

- Dreyer, S.J.; Walker, I. Acceptance and Support of the Australian Carbon Policy. Soc. Justice Res. 2013, 26, 343–362. [Google Scholar] [CrossRef] [Green Version]

- Hammar, H.; Jagers, S.C. What Is a Fair CO2 Tax Increase? On Fair Emission Reductions in the Transport Sector. Ecol. Econ. 2007, 61, 377–387. [Google Scholar] [CrossRef]

- Bristow, A.L.; Wardman, M.; Zanni, A.M.; Chintakayala, P.K. Public Acceptability of Personal Carbon Trading and Carbon Tax. Ecol. Econ. 2010, 69, 1824–1837. [Google Scholar] [CrossRef] [Green Version]

- Brown, Z.S.; Johnstone, N. Better the Devil You Throw: Experience and Support for Pay-as-You-Throw Waste Charges. Environ. Sci. Policy 2014, 38, 132–142. [Google Scholar] [CrossRef]

- Fairbrother, M. When Will People Pay to Pollute? Environmental Taxes, Political Trust and Experimental Evidence from Britain. Br. J. Polit. Sci. 2017, 49, 661–682. [Google Scholar] [CrossRef] [Green Version]

- Bullock, G.; Theodoridis, A.G. Addressing Concerns about Climate Policies: The Possibilities and Perils of Responsive Accommodation. Env. Polit. 2017, 26, 1079–1106. [Google Scholar] [CrossRef]

- McLaughlin, C.; Elamer, A.A.; Glen, T.; AlHares, A.; Gaber, H.R. Accounting Society’s Acceptability of Carbon Taxes: Expectations and Reality. Energy Policy 2019, 131, 302–311. [Google Scholar] [CrossRef]

- Thalmann, P. The Public Acceptance of Green Taxes: 2 Million Voters Express Their Opinion. Public Choice 2004, 119, 179–217. [Google Scholar] [CrossRef]

- Hsu, S.L.; Walters, J.; Purgas, A. Pollution Tax Heuristics: An Empirical Study of Willingness to Pay Higher Gasoline Taxes. Energy Policy 2008, 36, 3612–3619. [Google Scholar] [CrossRef]

- Gevrek, Z.E.; Uyduranoglu, A. Public Preferences for Carbon Tax Attributes. Ecol. Econ. 2015, 118, 186–197. [Google Scholar] [CrossRef] [Green Version]

- Grimsrud, K.M.; Lindhjem, H.; Sem, I.V.; Rosendahl, K.E. Public Acceptance and Willingness to Pay Cost-Effective Taxes on Red Meat and City Traffic in Norway. J. Environ. Econ. Policy 2019, 9, 251–268. [Google Scholar] [CrossRef]

- Sælen, H.; Kallbekken, S. A Choice Experiment on Fuel Taxation and Earmarking in Norway. Ecol. Econ. 2011, 70, 2181–2190. [Google Scholar] [CrossRef] [Green Version]

- Rotaris, L.; Danielis, R. The Willingness to Pay for a Carbon Tax in Italy. Transp. Res. Part D Transp. Environ. 2019, 67, 659–673. [Google Scholar] [CrossRef]

- Jagers, S.C.; Martinsson, J.; Matti, S. The Impact of Compensatory Measures on Public Support for Carbon Taxation: An Experimental Study in Sweden. Clim. Policy 2018, 19, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Kallbekken, S.; Aasen, M. The Demand for Earmarking: Results from a Focus Group Study. Ecol. Econ. 2010, 69, 2183–2190. [Google Scholar] [CrossRef]

- Kallbekken, S.; Sæælen, H. Public Acceptance for Environmental Taxes: Self-Interest, Environmental and Distributional Concerns. Energy Policy 2011, 39, 2966–2973. [Google Scholar] [CrossRef]

- Denstadli, J.M.; Veisten, K. The Flight Is Valuable Regardless of the Carbon Tax Scheme: A Case Study of Norwegian Leisure Air Travelers. Tour. Manag. 2020, 81, 1–12. [Google Scholar] [CrossRef]

- Cherry, T.L.; Kallbekken, S.; Kroll, S. The Impact of Trial Runs on the Acceptability of Environmental Taxes: Experimental Evidence. Resour. Energy Econ. 2014, 38, 84–95. [Google Scholar] [CrossRef]

- Doda, B.; Gennaioli, C.; Gouldson, A.; Grover, D.; Sullivan, R. Are Corporate Carbon Management Practices Reducing Corporate Carbon Emissions? Corp. Soc. Responsib. Environ. Manag. 2016, 23, 257–270. [Google Scholar] [CrossRef] [Green Version]

- Clayton, S. The Role of Perceived Justice, Political Ideology, and Individual or Collective Framing in Support for Environmental Policies. Soc. Justice Res. 2018, 31, 1–19. [Google Scholar] [CrossRef]

- Hammar, H.; Jagers, S.C. Can Trust in Politicians Explain Individuals’ Support for Climate Policy? The Case of CO2 Tax. Clim. Policy 2006, 5, 613–625. [Google Scholar] [CrossRef]

- Kotchen, M.J.; Turk, Z.M.; Leiserowitz, A.A. Public Willingness to Pay for a US Carbon Tax and Preferences for Spending the Revenue. Environ. Res. Lett. 2017, 12, 1–5. [Google Scholar] [CrossRef] [Green Version]

- Agrawal, A.W.; Dill, J.; Nixon, H. Green Transportation Taxes and Fees: A Survey of Public Preferences in California. Transp. Res. Part D Transp. Environ. 2010, 15, 189–196. [Google Scholar] [CrossRef]

- Amdur, D.; Dale, D.; Borick, C.; Rabe, B.G. Individual Discount Rates and Climate Change: Is Discount Rate Associated with Support for a Carbon Tax? Clim. Chang. Econ. 2015, 6, 1–14. [Google Scholar] [CrossRef]

- Harring, N.; Jagers, S.C. Should We Trust in Values? Explaining Public Support for pro-Environmental Taxes. Sustainability 2013, 5, 210–227. [Google Scholar] [CrossRef] [Green Version]

- Duan, H.X.; Lü, Y.L.; Li, Y. Chinese Public’s Willingness to Pay for CO2 Emissions Reductions: A Case Study from Four Provinces/Cities. Adv. Clim. Chang. Res. 2014, 5, 100–110. [Google Scholar] [CrossRef]

- Kenny, J. Environmentalism Undercover: The Environmental Dimension of Public Support for Domestic Water Charges. Elect. Stud. 2019, 62, 1–11. [Google Scholar] [CrossRef]

- Bachus, K.; Van Ootegem, L.; Verhofstadt, E. ‘No Taxation without Hypothecation’: Towards an Improved Understanding of the Acceptability of an Environmental Tax Reform*. J. Environ. Policy Plan. 2019, 21, 321–332. [Google Scholar] [CrossRef]

- Alberini, A.; Ščasný, M.; Bigano, A. Policy- v. Individual Heterogeneity in the Benefits of Climate Change Mitigation: Evidence from a Stated-Preference Survey. Energy Policy 2018, 121, 565–575. [Google Scholar] [CrossRef] [Green Version]

- Birol, E.; Das, S. Estimating the Value of Improved Wastewater Treatment: The Case of River Ganga, India. J. Environ. Manag. 2010, 91, 2163–2171. [Google Scholar] [CrossRef]

- Hsu, S.-L. The Politics and Psychology of Gasoline Taxes: An Empirical Study. Widener Law Rev. 2010, 26, 363–390. [Google Scholar]

- Eliasson, J.; Jonsson, L. The Unexpected “Yes”: Explanatory Factors behind the Positive Attitudes to Congestion Charges in Stockholm. Transp. Policy 2011, 18, 636–647. [Google Scholar] [CrossRef]

- Migheli, M. Brown Parents, Green Dads: Gender, Children, and Environmental Taxes. J. Clean. Prod. 2018, 180, 183–197. [Google Scholar] [CrossRef]

- Carattini, S.; Carvalho, M.; Fankhauser, S. Overcoming Public Resistance to Carbon Taxes. Wiley Interdiscip. Rev. Clim. Chang. 2018, 9, 1–26. [Google Scholar] [CrossRef] [Green Version]

- Organizational for Economic Co-Operation and Development (OECD). Government at a Glance; Organizational for Economic Cooperation and Development (OECD), OECD Publishing: Paris, France, 2019. [Google Scholar]

| Database | Search String |

|---|---|

| Scopus | TITLE-ABS-KEY ((“public accept*” OR “public choice” OR “public action*” OR “public support*” OR “public opinion” OR “public willingness” OR public response” OR “public perception*” OR “public resistance” OR “social response”) AND (“environment* tax*” OR “carbon tax*” OR “green tax*” OR “eco-tax*” OR “environment* charge*” OR “environment* tax reform” OR “tax reform”)) |

| Science Direct | TITLE-ABS-KEY ((“public acceptance” OR “public support” OR “public willingness” OR “public perception”) AND (“environmental tax” OR “carbon tax” OR “environmental tax reform” OR “environmental charges” OR “green tax”)) |

| Google Scholar | “Public acceptance” “environmental tax” |

| Theme | Sub-Theme |

|---|---|

| Policy | Type of policy, use of revenue, tax rate, exemption, experience, competitiveness, cost distribution, information dissemination, and effectiveness. |

| Governance | Political value orientation, trust in the government, efforts in protecting the environment, and quality of government (QoG). |

| Personal traits | Environmental protection attitude, perceived severity of climate change, psychological, social sharing, health, actual polluters and visited abroad. |

| Demographic | Income, age, education, gender, location, energy dependency, race, household size, employment, parenthood, religion, and religiosity. |

| Main theme | Policy | Governance | Personal Traits | Demographic |

|---|---|---|---|---|

| Sub-theme | Use of revenue Cost distribution Effectiveness Type of policy Tax rate Information Dissemination Competitiveness Experience Exemption | Political value orientation Trust Efforts in protecting the environment Quality of government | Perceived severity of climate change Environmental protection attitude Psychological Social sharing Good health Actual polluter Visited abroad | Location Income Gender Education Age Energy dependency Household size Parenthood Race Employment Religion Religiosity |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Muhammad, I.; Mohd Hasnu, N.N.; Ekins, P. Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review. Environments 2021, 8, 109. https://doi.org/10.3390/environments8100109

Muhammad I, Mohd Hasnu NN, Ekins P. Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review. Environments. 2021; 8(10):109. https://doi.org/10.3390/environments8100109

Chicago/Turabian StyleMuhammad, Izlawanie, Norfakhirah Nazihah Mohd Hasnu, and Paul Ekins. 2021. "Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review" Environments 8, no. 10: 109. https://doi.org/10.3390/environments8100109

APA StyleMuhammad, I., Mohd Hasnu, N. N., & Ekins, P. (2021). Empirical Research of Public Acceptance on Environmental Tax: A Systematic Literature Review. Environments, 8(10), 109. https://doi.org/10.3390/environments8100109