Does Property Return Affect Seller Behavior? An Empirical Study of China’s Real Estate Market

Abstract

1. Introduction

2. Data and Research Methodology

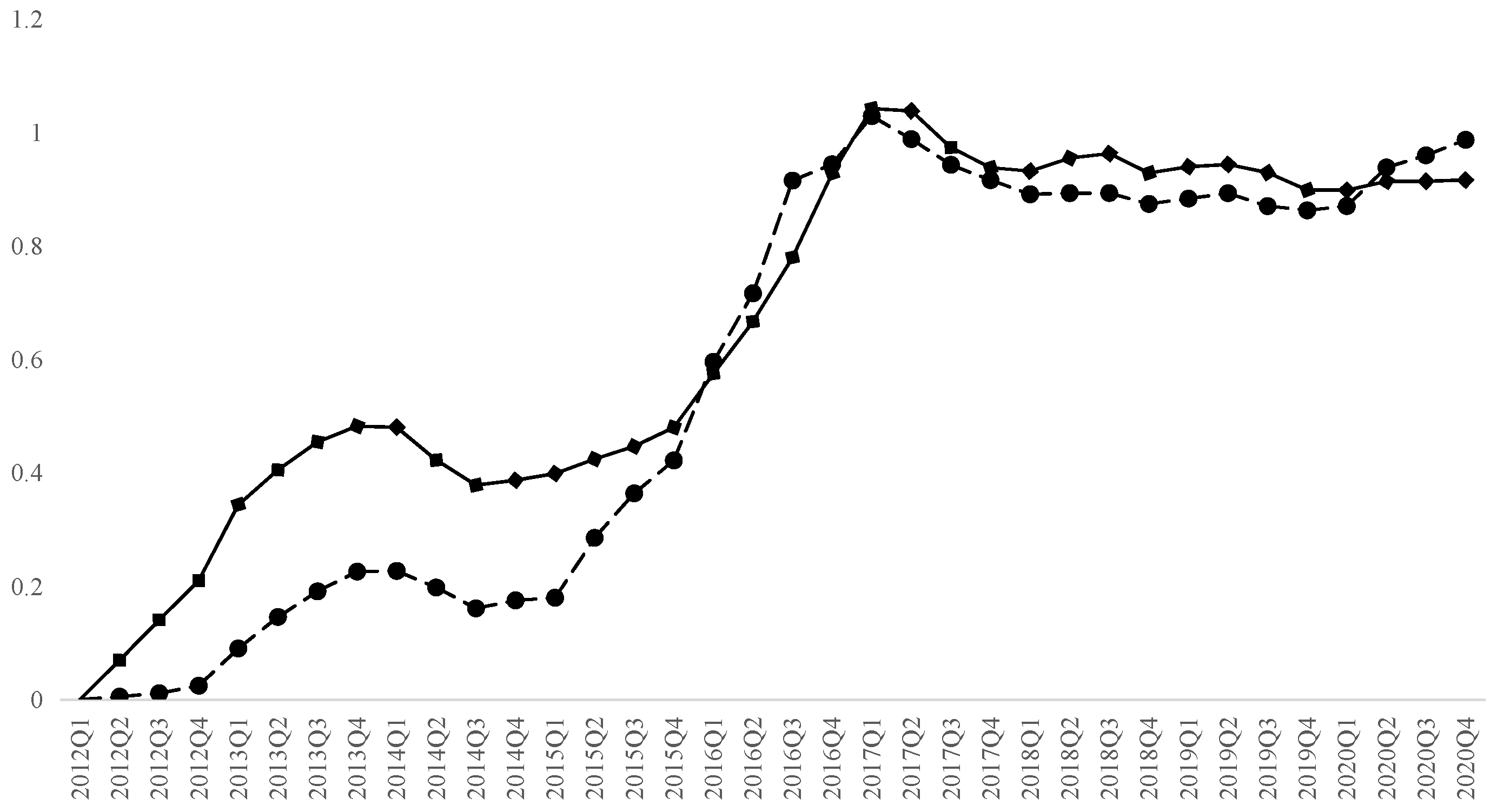

2.1. Data

2.2. Research Methodology

2.2.1. Return

2.2.2. Sell Propensity

2.2.3. Empirical Design

3. Empirical Results

3.1. Baseline Results

3.2. Robustness Analysis

3.2.1. Limiting the Scope of Purchase Dates

3.2.2. Removing Samples of Unreliable and Extreme Returns

3.2.3. Adjusting Expected Returns

3.2.4. Different Testing Methods

3.3. Heterogeneity Analysis

4. Further Analysis: Loss Aversion

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Shefrin, H.; Statman, M. The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence. J. Financ. 1985, 40, 777–790. [Google Scholar] [CrossRef]

- Odean, T. Are Investors Reluctant to Realize Their Losses. J. Financ. 1998, 53, 1775–1798. [Google Scholar] [CrossRef]

- Weber, M.; Camerer, C.F. The Disposition Effect in Securities Trading: An Experimental Analysis. J. Econ. Behav. Organ. 1998, 33, 167–184. [Google Scholar] [CrossRef]

- Genesove, D.; Mayer, C. Loss Aversion and Seller Behavior, pp. Evidence from the Housing Market. Q. J. Econ. 2001, 116, 1233–1260. [Google Scholar] [CrossRef]

- Locke, P.R.; Mann, S.C. Professional Trader Discipline and Trade Disposition. J. Financ. Econ. 2005, 76, 401–444. [Google Scholar] [CrossRef]

- Kumar, A. Hard-to-value Stocks, Behavioral Biases, and Informed Trading. J. Financ. Quant. Anal. 2009, 44, 1375–1401. [Google Scholar] [CrossRef]

- Hong, D.; Loh, R.; Warachka, M. Do Large Gains Make Willing Sellers? J. Financ. Quant. Anal. 2022, 57, 1486–1528. [Google Scholar] [CrossRef]

- Case, K.E.; Quigley, J.M.; Shiller, R.J. Wealth Effects Revisited 1975–2012. Crit. Financ. Rev. 2013, 2, 101–128. [Google Scholar] [CrossRef]

- Huang, Z. A Study of Household Finance in China. Ph.D. Thesis, Lingnan University, Hong Kong, China, 2013. [Google Scholar] [CrossRef]

- Xie, Y.; Jin, Y. Household Wealth in China. Chin. Sociol. Rev. 2015, 47, 203–229. [Google Scholar] [CrossRef] [PubMed]

- Ben-David, I.; Hirshleifer, D. Are Investors Really Reluctant to Realize Their Losses? Trading Responses to Past Returns and the Disposition Effect. Rev. Financ. Stud. 2012, 25, 2485–2532. [Google Scholar] [CrossRef]

- Engelhardt, G.V. Nominal Loss Aversion, Housing Equity Constraints, and Household Mobility: Evidence from the United States. J. Urban Econ. 2003, 53, 171–195. [Google Scholar] [CrossRef]

- Giglio, S.W.; Maggiori, M.; Stroebel, J. Very Long-Run Discount Rates. Q. J. Econ. 2015, 130, 1–53. [Google Scholar] [CrossRef]

- Shapira, Z.; Venezia, D.I. Patterns of Behavior of Professionally Managed and Independent Investors. J. Bank. Financ. 2011, 25, 1573–1587. [Google Scholar] [CrossRef]

- Feng, L.; Seasholes, M.S. Do Investor Sophistication and Trading Experience Eliminate Behavioral Biases in Financial Markets. Rev. Financ. 2005, 9, 205–351. [Google Scholar] [CrossRef]

- Vaarmets, T.; Liivamägi, K.; Talpsepp, T. How Does Learning and Education Help to Overcome the Disposition Effect? Rev. Financ. 2019, 23, 801–830. [Google Scholar] [CrossRef]

- Genesove, D.; Mayer, C. Equity and Time to Sale in the Real Estate Market. Am. Econ. Rev. 1997, 87, 255–269. [Google Scholar]

- Stein, J.C. Prices and Trading Volume in the Housing Market: A Model with Down-Payment Effects. Q. J. Econ. 1995, 110, 379–406. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect Theory: An Analysis of Decision under Risk. Econometrica 1979, 47, 263–292. [Google Scholar] [CrossRef]

- Barberis, N.; Xiong, W. Realization Utility. J. Financ. Econ. 2012, 104, 251–271. [Google Scholar] [CrossRef]

- Ingersoll, J.E.; Jin, L.J. Realization Utility with Reference-Dependent Preferences. Rev. Financ. Stud. 2013, 26, 723–767. [Google Scholar] [CrossRef]

- Case, K.E.; Shiller, R.J. The Behavior of Home Buyers in Boom and Post-Boom Markets; NBER Working Papers 2748; Federal Reserve Bank of Boston: Boston, MA, USA, 1998. [Google Scholar]

{kind=link}

| Variable | Description | Mean | SD | Max | Min |

|---|---|---|---|---|---|

| List price total | Total listing price | 411.680 | 280.571 | 8800 | 10 |

| List price | Listing price, unit: yuan/m2 | 49,780.204 | 24,229.086 | 199,901.039 | 10,000 |

| Price total | Total transaction price | 400.954 | 269.719 | 8000 | 12 |

| Price | Transaction price, unit: yuan/m2 | 48,530.386 | 23,486.200 | 199,924.242 | 10,000 |

| Size | House size, unit: m2 | 84.660 | 37.654 | 728 | 6 |

| Bedroom | Number of bedrooms | 2.034 | 0.779 | 9 | 1 |

| Living room | Number of living rooms | 1.163 | 0.504 | 6 | 0 |

| Bathroom | Number of bathrooms | 1.205 | 0.454 | 8 | 0 |

| Level1 | Level of the house. Two dummy variables to signify middle and high floors. Level1 represents middle floors, and Level2 represents higher floors. | 0.379 | 0.485 | 1 | 0 |

| Level2 | 0.329 | 0.470 | 1 | 0 | |

| Floor | Total floors of the building | 13.511 | 7.880 | 42 | 1 |

| South | Whether the direction of the house is south, 1 if yes, otherwise 0. | 0.773 | 0.419 | 1 | 0 |

| TOM | Time-on-the-market, the interval between transaction date and listing date. | 76.813 | 189.386 | 3509 | 1 |

| Variable | Description | Mean | SD | Max | Min |

|---|---|---|---|---|---|

| Log. of list price | Take the logarithm of the list price, unit: yuan/m2 | 10.988 | 0.410 | 12.398 | 9.302 |

| Size | House size, unit: m2 | 82.883 | 40.538 | 744.95 | 9.64 |

| Bedroom | Number of bedrooms | 2.076 | 0.812 | 9 | 1 |

| Living room | Number of living rooms | 1.095 | 0.437 | 5 | 0 |

| Bathroom | Number of bathrooms | 1.200 | 0.480 | 6 | 0 |

| Level1 | Level of the house. Two dummy variables to signify middle and high floors. Level1 represents middle floors, and Level2 represents higher floors. | 0.359 | 0.480 | 1 | 0 |

| Level2 | 0.314 | 0.464 | 1 | 0 | |

| Floor | Total floors of the building | 13.437 | 7.947 | 42 | 1 |

| South | Whether the direction of the house is south, 1 if yes, otherwise 0. | 0.791 | 0.407 | 1 | 0 |

| Mortgage | Denote 1 if the listed house is mortgaged, and 0 if not. | 0.299 | 0.458 | 1 | 0 |

| Distance | Distance between its residential project and Tiananmen Square, unit: kilometer | 14.735 | 10.595 | 111.297 | 0.418 |

| A: Results of control variables | |||||||

| Size | Level1 | Level2 | Floor | Bedroom | Livingroom | Bathroom | South |

| −0.003 | 0.010 | −0.007 | 0.001 | 0.030 | 0.012 | 0.015 | 0.048 |

| [−47.05] | [13.81] | [−7.22] | [0.63] | [21.29] | [12.15] | [6.41] | [25.58] |

| B: R2 distribution | |||||||

| Mean | P1 | P10 | P25 | P50 | P75 | P90 | P99 |

| 0.907 | 0.481 | 0.792 | 0.892 | 0.943 | 0.967 | 0.979 | 0.992 |

| Variable | Period t0 | Period t0 + 1 | ... | Period t − 1 | Period t |

|---|---|---|---|---|---|

| Sell propensity | 0 | 0 | ... | 0 | 1 |

| Unrealized return | ... | ||||

| Holding period | 0 | 1 | ... | t−1 | t |

| Housing attributes | Xi | Xi | ... | Xi | Xi |

| 0~2 Holding Years | 2~4 Holding Years | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Probit | OLS | OLS | Probit | OLS | OLS | |

| Loss | −0.035 *** | −0.035 *** | −0.047 *** | −0.025 *** | −0.017 *** | −0.020 *** |

| (0.007) | (0.008) | (0.009) | (0.004) | (0.004) | (0.005) | |

| Purchase Price | 0.017 | 0.018 | 0.058 ** | 0.021 *** | 0.019 *** | 0.031 ** |

| (0.012) | (0.012) | (0.023) | (0.007) | (0.006) | (0.012) | |

| LnTOM | −0.008 ** | −0.007 ** | −0.007 * | 0.002 | 0.002 | 0.001 |

| (0.003) | (0.003) | (0.004) | (0.002) | (0.002) | (0.002) | |

| Distance | −0.002 | −0.002 | −0.001 | −0.001 | ||

| (0.0062) | (0.002) | (0.001) | (0.001) | |||

| Hold Period | 0.066 *** | 0.069 *** | 0.076 *** | 0.034 *** | 0.028 *** | 0.031 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | |

| Mortgage | −0.073 *** | −0.069 *** | −0.068 *** | −0.033 *** | −0.030 *** | −0.037 *** |

| (0.006) | (0.005) | (0.007) | (0.003) | (0.003) | (0.003) | |

| Other Control Variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Street Fixed Effects | Yes | Yes | No | Yes | Yes | No |

| Project Fixed Effects | No | No | Yes | No | No | Yes |

| Sample Size | 35,389 | 36,724 | 36,549 | 59,202 | 61,829 | 61,778 |

| R2 | 0.167 | 0.255 | 0.269 | 0.215 | 0.343 | 0.349 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Probit | OLS | OLS | |

| Loss | −0.040 *** | −0.037 *** | −0.045 *** |

| (0.011) | (0.011) | (0.013) | |

| Control Variables | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes |

| Street Fixed Effects | Yes | Yes | No |

| Project Fixed Effects | No | No | Yes |

| Sample Size | 14,604 | 16,812 | 16,695 |

| R2 | 0.152 | 0.322 | 0.341 |

| Remove R2 < 0.8 Neighborhood Samples | Samples of Returns Inside the [−0.20, 0.20] Interval | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Probit | OLS | OLS | Probit | OLS | OLS | |

| Loss | −0.028 *** | −0.026 *** | −0.038 *** | −0.036 *** | −0.036 *** | −0.048 *** |

| (0.008) | (0.008) | (0.009) | (0.007) | (0.008) | (0.009) | |

| Control Variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Street Fixed Effects | Yes | Yes | No | Yes | Yes | No |

| Project Fixed Effects | No | No | Yes | No | No | Yes |

| Sample Size | 29,045 | 30,152 | 29,992 | 33,675 | 34,973 | 34,771 |

| R2 | 0.168 | 0.256 | 0.269 | 0.168 | 0.257 | 0.269 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Probit | OLS | OLS | |

| Loss | −0.024 *** | −0.023 *** | −0.035 *** |

| (0.007) | (0.007) | (0.008) | |

| Control Variables | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes |

| Street Fixed Effects | Yes | Yes | No |

| Project Fixed Effects | No | No | Yes |

| Sample Size | 43,529 | 44,852 | 44,720 |

| R2 | 0.153 | 0.233 | 0.242 |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| OLS | OLS | Exponential | Weibull | Cox | |

| Loss | 0.356 ** | 0.058 *** | −0.070 *** | −0.095 *** | −0.118 *** |

| (0.148) | (0.021) | (0.012) | (0.016) | (0.018) | |

| Control Variables | Yes | Yes | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes | Yes | Yes |

| Street Fixed Effects | No | No | Yes | Yes | Yes |

| Project Fixed Effects | Yes | Yes | No | No | No |

| Sample Size | 17,487 | 17,487 | 15,059 | 15,059 | 15,059 |

| Pseudo R2 | 0.336 | 0.267 | 0.004 |

| Mortgage | Project Popularity | |||

|---|---|---|---|---|

| Without a Mortgage | With a Mortgage | Unpopular | Popular | |

| (1) | (2) | (3) | (4) | |

| Loss | −0.033 *** | −0.045 *** | −0.015 | −0.045 *** |

| (0.008) | (0.013) | (0.012) | (0.009) | |

| Control Variables | Yes | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes | Yes |

| Street Fixed Effects | Yes | Yes | Yes | Yes |

| Sample Size | 26,055 | 9315 | 12,097 | 23,272 |

| Pseudo R2 | 0.154 | 0.236 | 0.187 | 0.168 |

| Listing Price Premium | Transaction Premium | |||||

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Loss | 0.036 *** | 0.037 *** | 0.031 *** | 0.032 *** | ||

| (0.003) | (0.003) | (0.004) | (0.004) | |||

| R | −0.526 *** | −0.446 *** | ||||

| (0.034) | (0.045) | |||||

| IMR | 0.021 | 0.035 | ||||

| (0.020) | (0.024) | |||||

| Control Variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Quarterly Fixed Effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Street Fixed Effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Sample Size | 17,505 | 16,975 | 17,505 | 7617 | 7484 | 7617 |

| R2 | 0.146 | 0.147 | 0.206 | 0.096 | 0.096 | 0.148 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, H.; Liang, L.; Sun, C. Does Property Return Affect Seller Behavior? An Empirical Study of China’s Real Estate Market. Behav. Sci. 2023, 13, 55. https://doi.org/10.3390/bs13010055

Li H, Liang L, Sun C. Does Property Return Affect Seller Behavior? An Empirical Study of China’s Real Estate Market. Behavioral Sciences. 2023; 13(1):55. https://doi.org/10.3390/bs13010055

Chicago/Turabian StyleLi, Hongfei, Limin Liang, and Chengjiu Sun. 2023. "Does Property Return Affect Seller Behavior? An Empirical Study of China’s Real Estate Market" Behavioral Sciences 13, no. 1: 55. https://doi.org/10.3390/bs13010055

APA StyleLi, H., Liang, L., & Sun, C. (2023). Does Property Return Affect Seller Behavior? An Empirical Study of China’s Real Estate Market. Behavioral Sciences, 13(1), 55. https://doi.org/10.3390/bs13010055