Trade Risk Society—Understanding Trade Policymaking in the 2020s

Abstract

1. Trade: Disrupted… and at Risk

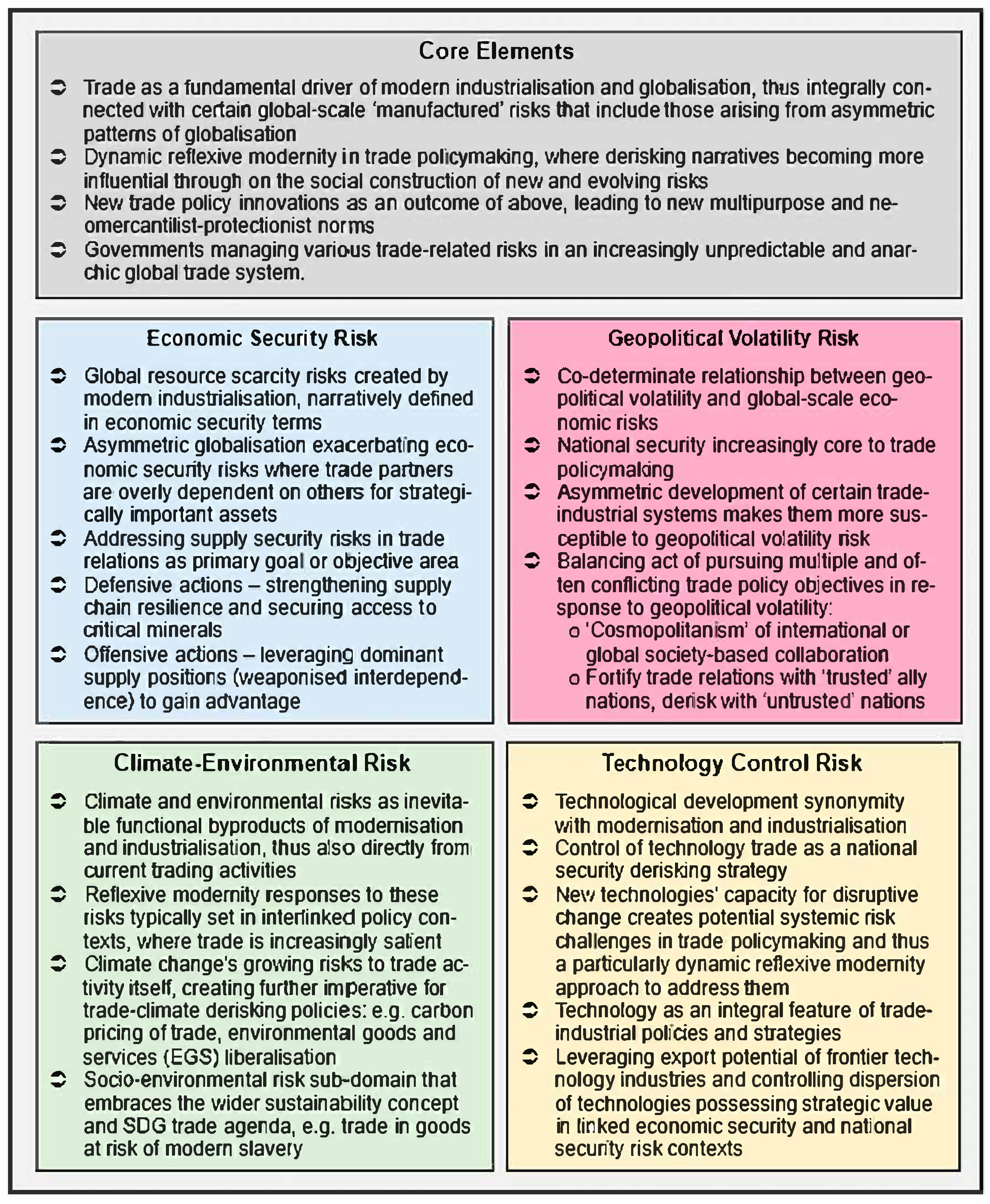

2. Trade Risk Society

2.1. Risk Society Theory and Trade

2.2. Towards a Trade Risk Society

3. Economic Security Risk

- ⮊

- Shortening supply of critical minerals as demand for them accelerates in frontier technology industries such as clean energy, advanced semiconductors, and digital infrastructures.

- ⮊

- COVID-19 pandemic disruptions to international supply chains generally and production of critical components, e.g., semiconductors.

- ⮊

- China’s growing dominance across supply chains in frontier technology industries, such as electric vehicles (EVs), solar energy, and batteries.

- ⮊

- Russia–Ukraine war and disruptions to energy, food, and other good supplies.

4. Geopolitical Volatility Risk

5. Climate–Environmental Risk

6. Technology Control Risk

7. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | In the 15-page official Strategy document, the word ‘risk’ is mentioned 77 times, mostly in connection with trade-related issues. |

| 2 | CSIS News, 20 December 2024, ‘Trump Trade 2.0’, www.csis.org/analysis/trump-trade-20 (accessed on 12 February 2025). |

| 3 | BBC News, 6 February 2025, ‘The tariff wars have begun: buckle up’, www.bbc.co.uk/news/articles/c8975dx1pe3o. Accessed on 12 February 2025. |

| 4 | BBC News, 1 February 2025, ‘China, Canada and Mexico vow swift response to Trump tariffs’, www.bbc.co.uk/news/articles/c627nx42xelo. Accessed on 12 February 2025. |

| 5 | Reuters, 12 March, ‘Canada announces C$29.8 billion in retaliatory tariffs on US’, www.reuters.com/world/americas/canada-announce-c298-bln-retaliatory-tariffs-us-2025-03-12. Accessed on 19 March 2025. |

| 6 | NPR News, 12 March 2025, ‘Automakers brace for higher costs as steel and aluminium tariffs kick in’, www.npr.org/2025/03/12/nx-s1-5325933/steel-aluminum-tariffs-autos. Accessed on 19 March 2025. |

| 7 | These new ‘reciprocal’ tariffs were presented by Trump as being half the import tariffs allegedly applied by trade partners on their own imports from the US but this transpired to be a misnomer. Instead, these announced new tariffs were calculated by taking the goods trade deficit (ignoring services trade) the US had with the partner country then dividing this by the US’ imported goods value total from that trade partner. Many countries targeted for higher-level tariffs did not apply any restrictions, tariffs or otherwise, on the US. BBC News, 3 April 2025, ‘Why Trump’s tariffs aren’t really reciprocal’, www.bbc.co.uk/news/videos/c14xldg3mjvo. Accessed on 5 April 2025; CSIS News, 3 April 2025, ‘Liberation Day Tariffs Explained’, www.csis.org/analysis/liberation-day-tariffs-explained. Accessed on 5 April 2025. |

| 8 | Where later in April 2025, the US applied a 145% tariff on most goods from China, who in turn applied a 125% tariff and other trade restrictions on targeted imports from the US. A partial de-escalation of tariff rates was later brokered between both sides the following month. |

| 9 | Guardian, 7 Jan 2025, ‘Trump refuses to rule out using military to take Panama Canal and Greenland’, www.theguardian.com/us-news/2025/jan/07/trump-panama-canal-greenland. Accessed on 9 January 2025. |

| 10 | Guardian, 17 Feb 2025, ‘What are Ukraine’s critical minerals—and why does Trump want them?’ www.theguardian.com/world/2025/feb/17/what-are-ukraines-critical-minerals-and-why-does-trump-want-them. Accessed on 19 March 2025; BBC News, 30 April 2025, ‘US and Ukraine sign long-awaited natural resources deal’, www.bbc.co.uk/news/articles/c5ypw7pn9q3o. Accessed on 5 May 2025. |

| 11 | The Diplomat, 11 July 2023, ‘China’s Transition from the Belt and Road to the Global Development Initiative’, https://thediplomat.com/2023/07/chinas-switch-from-the-belt-and-road-to-the-global-development-initiative. Accessed on 9 January 2025. |

| 12 | Bloomberg News, 9 January 2024, ‘Xi, Biden and the $10 Trillion Cost of War Over Taiwan’. www.bloomberg.com/news/features/2024-01-09/if-china-invades-taiwan-it-would-cost-world-economy-10-trillion?embedded-checkout=true. Accessed on 9 January 2025. |

| 13 | CSIS News, 30 April 2025, ‘Can Trump’s Reciprocal Trade Negotiations Make America Great Again?’, www.csis.org/analysis/can-trumps-reciprocal-trade-negotiations-make-america-great-again. Accessed on 5 May 2025. |

| 14 | East Asia Forum, 30 April 2025, ‘Making sense of Trump’s tariffs’, https://eastasiaforum.org/2025/04/30/making-sense-of-trumps-tariffs. Accessed on 5 May 2025. |

| 15 | For example, the annual WTO Public Forum events focused on these issues, www.wto.org/english/forums_e/public_forum23_e/public_forum23_e.htm. Accessed on 9 January 2025. |

| 16 | Ministry of Foreign Affairs and Trade (New Zealand): https://www.mfat.govt.nz/en/trade/free-trade-agreements/trade-and-climate/agreement-on-climate-change-trade-and-sustainability-accts-negotiations. Accessed on 9 January 2025. |

| 17 | The power to repeal the IRA lies with US Congress, not President Trump. Columbia Climate Law, 29 April 2025, ‘100 Days of Trump 2.0: The Inflation Reduction Act’, https://blogs.law.columbia.edu/climatechange/2025/04/29/100-days-of-trump-2-0-the-inflation-reduction-act. Accessed on 5 May 2025. |

| 18 | See www.tradeministersonclimate.org. Accessed on 9 January 2025. |

| 19 | ‘Creating Helpful Incentives to Produce Semiconductors’. |

| 20 | BBC News, 26 November 2023, ‘US bans sale of Huawei, ZTE tech amid security fears’. Available at: www.bbc.co.uk/news/world-us-canada-63764450. Accessed on 9 January 2025. |

| 21 | EAF, 19 February 2025, ‘How China is weaponising its dominance in critical minerals trade’, https://eastasiaforum.org/2025/02/19/how-china-is-weaponising-its-dominance-in-critical-minerals-trade. Accessed on 9 March 2025. |

| 22 | Tech Target News, 9 April 2025, ‘Trump puts stamp on CHIPS Act deals with new office’, www.techtarget.com/searchcio/news/366622293/Trump-puts-stamp-on-CHIPS-Act-deals-with-new-office. Accessed on 5 May 2025. |

| 23 | BBC News, 18 October 2023, ‘US-China chip war: Beijing unhappy at latest wave of US restrictions’, www.bbc.co.uk/news/business-67141987. Accessed on 14 October 2024. |

| 24 | BBC News, 30 June 2023, ‘Dutch to restrict chip equipment exports amid US pressure’, www.bbc.co.uk/news/business-66063594. Accessed on 14 October 2024. |

| 25 | Samsung was also approached around this time to establish a new semiconductor plant in the US. |

| 26 | Reuters, 8 August 2023, ‘Germany spends big to win $11 billion TSMC chip plant’, www.reuters.com/technology/taiwan-chipmaker-tsmc-approves-38-bln-germany-factory-plan-2023-08-08. Accessed on 14 October 2024. |

| 27 | Korea Herald, 24 January 2022, ‘Korea sets out own Chips Act, in less ambitious fashion’, www.koreaherald.com/view.php?ud=20220124000671. Accessed on 14 October 2024. |

| 28 | Reuters, 13 December 2022, ‘China readying $143 billion package for its chip firms in face of US curbs’, www.reuters.com/technology/china-plans-over-143-bln-push-boost-domestic-chips-compete-with-us-sources-2022-12-13. Accessed on 14 October 2024. |

| 29 | China Briefing, 20 July 2020, ‘What is the China Standards 2035 Plan and How Will it Impact Emerging Industries?’, www.china-briefing.com/news/what-is-china-standards-2035-plan-how-will-it-impact-emerging-technologies-what-is-link-made-in-china-2025-goals. Accessed on 14 October 2024. |

| 30 | See WTO Regional Trade Agreement Database at: https://rtais.wto.org. Accessed on 14 October 2024. |

| 31 | News Central Africa, 6 May 2025, ‘Lesotho’s Textile Sector Braces Up as Trump-Era Deadline Nears’, https://newscentral.africa/lesothos-textile-sector-braces-up-as-trump-era-deadline-nears. Accessed on 14 May 2025. |

References

- Adamchick, Julie, and Andres M. Perez. 2020. Choosing awareness over fear: Risk analysis and free trade support global food security. Global Food Security 26: 100445. [Google Scholar] [CrossRef] [PubMed]

- Arroniz, Ignacio, and Jonny Peters. 2022. How EU Trade Deals Can Increase Climate Action Developing Proactive Green Trade Approaches After the EU TSD Review. E3G Briefing Paper. London: E3G. [Google Scholar]

- Baršauskaitė, Ieva. 2024. Is the WTO Up to the Challenge of Prioritizing the Environment at MC13? Geneva: IISD. [Google Scholar]

- Batra, Amita. 2023. EU carbon tariffs are bad trade policy. East Asia Forum, July 27. [Google Scholar]

- Baumann, Zygmunt. 1997. Postmodernity and It’s Discontents. Cambridge: Polity Press. [Google Scholar]

- Beck, Ulrich. 1992. Risk Society: Towards a New Modernity. London: Sage. [Google Scholar]

- Beck, Ulrich. 1995. Ecological Politics in the Age of Risk. Cambridge: Polity. [Google Scholar]

- Beck, Ulrich. 1996. World Risk Society as Cosmopolitan Society? Ecological Questions in a Framework of Manufactured Uncertainties. Theory, Culture and Society 13: 1–32. [Google Scholar] [CrossRef]

- Beck, Ulrich. 2008. World at Risk. Cambridge: Polity. [Google Scholar]

- Beck, Ulrich. 2015. Emancipatory catastrophism: What does it mean to climate change and risk society? Current Sociology 63: 75–88. [Google Scholar] [CrossRef]

- Beck, Ulrich, and Edgar Grande. 2010. Varieties of second modernity: The cosmopolitan turn in social and political theory and research. British Journal of Sociology 61: 409–43. [Google Scholar] [CrossRef]

- Benson, Emily, and Catharine Mouradian. 2023. How Do the United States and Its Partners Approach Economic Security? Centre for Strategic and International Studies, November 8. [Google Scholar]

- Bilal, San. 2021. A European Economic Diplomacy in the Making. European Centre for Development Policy Management. Maastricht: ECDPM. [Google Scholar]

- Boudia, Soraya, and Nathalie Jas. 2007. Introduction: Risk and ‘Risk Society’ in Historical Perspective. History and Technology 23: 317–31. [Google Scholar] [CrossRef]

- Bronckers, Marco, and Giovanni Gruni. 2021. Retooling the Sustainability Standards in EU Free Trade Agreements. Journal of International Economic Law 24: 25–51. [Google Scholar] [CrossRef]

- Cao, Lansheng, Ming Gu, Ding Jin, and Changyan Wang. 2023. Geopolitical risk and economic security: Exploring natural resources extraction from BRICS region. Resources Policy 85: 103800. [Google Scholar] [CrossRef]

- Centre for International Knowledge on Development (CIKD). 2023. Progress Report on the Global Development Initiative 2023. Beijing: Centre for International Knowledge on Development. [Google Scholar]

- Chernilo, Daniel. 2021. One globalisation or many? Risk society in the age of the Anthropocene. Journal of Sociology 57: 12–26. [Google Scholar] [CrossRef]

- Curran, Dean. 2013. Risk society and the distribution of bads: Theorizing class in the risk society. British Journal of Sociology 64: 44–62. [Google Scholar] [CrossRef] [PubMed]

- Denney, David. 2005. Risk and Society. London: Sage. [Google Scholar]

- Dent, Christopher M. 2020. Brexit, Trump and trade: Back to a late 19th century future? Competition and Change 24: 338–57. [Google Scholar] [CrossRef]

- Dent, Christopher M. 2021. Trade, Climate and Energy: A New Study on Climate Action through Free Trade Agreements. Energies 14: 4363. [Google Scholar] [CrossRef]

- Dent, Christopher M. 2022. Neoliberal Environmentalism, Climate Interventionism and the Trade-Climate Nexus. Sustainability 14: 15804. [Google Scholar] [CrossRef]

- Dodds, Klaus. 2009. Geopolitics. London: Sage. [Google Scholar]

- Drinhausen, Katja, and Helena Legarda. 2022. Confident Paranoia: Xi’s “comprehensive national security” framework shapes China’s behaviour at home and abroad. Merics China Monitor 15: 2022. [Google Scholar]

- Dryzek, John S. 1995. Toward an Ecological Modernity. Contemporary Sociology 28: 231–42. [Google Scholar] [CrossRef]

- European Centre for International Political Economy (ECIPE). 2022. The New Wave of Defensive Trade Policy Measures in the European Union: Design, Structure, and Trade Effects. ECIPE Occasional Paper, No. 4. Brussels: ECIPE. [Google Scholar]

- European Commission. 2021. New Trade Strategy: An Open, Sustainable and Assertive Trade Policy. Brussels: European Commission. [Google Scholar]

- European Commission. 2023. European Economic Security Strategy. Brussels: European Commission. [Google Scholar]

- Evenett, Simon J. 2019. Protectionism, state discrimination, and international business since the onset of the global financial crisis. Journal of International Business Policy 2: 9–36. [Google Scholar] [CrossRef]

- Evenett, Simon J. 2022. Did COVID-19 Trigger a ‘New Normal’ in Trade Policy? Geneva: International Institute for Sustainable Development. [Google Scholar]

- Farrell, Henry, and Abraham L. Newman. 2019. Weaponized Interdependence: How Global Economic Networks Shape State Coercion. International Security 44: 42–79. [Google Scholar] [CrossRef]

- Gerstein, Daniel M., and Douglas C. Ligor. 2023. Economic Security and the U.S. Department of Homeland Security. Washington, DC: RAND Corporation. [Google Scholar]

- Giddens, Anthony. 1990. Consequences of Modernity. Cambridge: Polity. [Google Scholar]

- Gjesvik, Lars. 2023. Private Infrastructure in Weaponized Interdependence. Review of International Political Economy 30: 722–46. [Google Scholar] [CrossRef]

- Global Trade Alert. 2025. Global Trade Alert Database; St. Gallen. Available online: https://globaltradealert.org (accessed on 14 May 2025).

- Glosserman, Brad. 2023. Real Economic Security Demands Heretical Thinking. East Asia Forum, July 27. [Google Scholar]

- Hopkins, Antony G. 2003. Globalization in World History. New York: Norton. [Google Scholar]

- Hufbauer, Gary Clyde. 2023. Washington’s Turn to Neomercantilism. East Asia Forum, June 4. [Google Scholar]

- International Institute for Sustainable Development (IISD). 2023. We Need More Hybrid Trade and Environment Agreements. Geneva: IISD. [Google Scholar]

- Japanese Government. 2022. Economic Security Protection Act. Tokyo: Japanese Government. [Google Scholar]

- Keohane, Robert O., and Joseph S. Nye, Jr. 1973. Power and Interdependence. Survival 15: 158–65. [Google Scholar] [CrossRef]

- Kesselring, Sven. 2024. Contouring the Mobile Risk Society. Applied Mobilities 9: 248–68. [Google Scholar] [CrossRef]

- Kreps, Sarah, and Paul Timmers. 2022. Bringing Economics Back into EU and US Chips Policy. Washington, DC: Brookings Institute. [Google Scholar]

- Krummenacher, Pascal. 2023. International Trade and Artificial Intelligence: Is Trade Policy Ready for Chat GPT? Geneva: IISD. [Google Scholar]

- Labour Party. 2023. National Securonomics: National Security and Industrial Strategy. London: Labour Party. [Google Scholar]

- Lacy, Mark J. 2002. Deconstructing Risk Society. Environmental Politics 11: 42–62. [Google Scholar] [CrossRef]

- Lamp, Nicolas. 2023. Toward Multipurpose Trade Policy? How Competing Narratives About Globalization Are Reshaping International Trade Cooperation. Geneva: IISD. [Google Scholar]

- Lavery, Scott. 2023. Rebuilding the fortress? Europe in a changing world economy. Review of International Political Economy 31: 1–24. [Google Scholar] [CrossRef]

- Lee, Su-Hyun. 2022. ASEAN’s economic security and regional economic cooperation: Past, present, and future. Asian Journal of Comparative Politics 7: 10–28. [Google Scholar] [CrossRef]

- Lidskog, Rolf, and Jens O. Zinn. 2024. Reflexive Modernisation and Risk Society. In Elgar Encyclopaedia of Environmental Sociology. Edited by Christine Overdevest. Cheltenham: Edward Elgar. [Google Scholar]

- Lupton, Deborah. 1999. Risk. London: Routledge. [Google Scholar]

- Lydgate, Emily. 2022. Is the Golden Age of Free Trade Agreements Over? Brighton: UK Trade Policy Observatory. [Google Scholar]

- Marshall, Brent K. 1999. Globalisation, Environmental Degradation and Ulrich Beck’s Risk Society. Environmental Values 8: 253–75. [Google Scholar] [CrossRef]

- Mearsheimer, John J. 2021. The Inevitable Rivalry: America, China, and the Tragedy of Great Power Politics. Foreign Affairs 100: 48–58. [Google Scholar]

- Miller, Chris. 2022. Chip War: The Fight for the World’s Most Critical Technology. New York: Scribner. [Google Scholar]

- Murphy, Ben. 2022. Chokepoints: China’s Self-Identified Strategic Technology Import Dependencies. Washington, DC: Centre for Security and Emerging Technology. [Google Scholar]

- Mythen, Gabe. 2021. The Critical Theory of World Risk Society: A Retrospective Analysis. Risk Analysis 41: 533–43. [Google Scholar] [CrossRef]

- Mythen, Gabe, Adam Burgess, and Jamie K. Wardman. 2018. The Prophecy of Ulrich Beck: Signposts, for the Social Sciences. Journal of Risk Research 22: 96–100. [Google Scholar] [CrossRef]

- Nye, Joseph S. 2020. Power and Interdependence with China. The Washington Quarterly 43: 7–21. [Google Scholar] [CrossRef]

- Oatley, Thomas. 2021. Regaining relevance: IPE and a changing global political economy. Cambridge Review of International Affairs 34: 318–27. [Google Scholar] [CrossRef]

- Pangestu, Mari. 2023. Industrial policy not the right answer to securing critical minerals and the green transition. In East Asia Forum. Canberra: ANU Press. [Google Scholar]

- Papa, Mihaela, and Ravi Shankar Chaturvedi. 2023. BRICS and questions about the global order. East Asia Forum Quarterly 15: 21–25. [Google Scholar]

- Patunru, Arianto. 2023. Industrial Policy Makes a Comeback in East Asia. East Asia Forum Quarterly 15: 6–8. [Google Scholar]

- Pearson, Rebecca, and Douglas K. Bardsley. 2022. Applying complex adaptive systems and risk society theory to understand energy transitions. Environmental Innovation and Societal Transitions 42: 74–87. [Google Scholar] [CrossRef]

- Pigman, Geoffrey Allen. 2022. Negotiating Our Economic Future: Trade, Technology, and Diplomacy. Montreal: McGill-Queen’s University Press. [Google Scholar]

- Reeves, Jeffrey. 2024. Bidenomics in the Indo-Pacific: Strategic Implications. Washington Quarterly 47: 123–45. [Google Scholar] [CrossRef]

- Roberts, Anthea. 2023. From Risk to Resilience: How Economies Can Thrive in a World of Threats. Foreign Affairs. Available online: www.foreignaffairs.com/world/risk-resilience-economics (accessed on 14 October 2024).

- Rodrik, Dani. 2021. A Primer on Trade and Inequality. London: Institute for Fiscal Studies. [Google Scholar]

- Sheehan, Matt. 2022. Biden’s Unprecedented Semiconductor Bet. Washington, DC: Carnegie Endowment for International Peace. [Google Scholar]

- Sovacool, Benjamin K. 2025. The Low-Carbon Risk Society: Dilemmas of Risk–Risk Trade-offs in Energy Innovations, Transitions and Climate Policy. Risk Analysis 45: 78–107. [Google Scholar] [CrossRef] [PubMed]

- Starrs, Sean Kenji, and Julian Germann. 2021. Responding to the China challenge in techno-nationalism: Divergence between Germany and the United States. Development and Change 52: 1122–46. [Google Scholar] [CrossRef]

- Sundberg, Leif. 2024. Towards the Digital Risk Society: A Review. Human Affairs 34: 151–64. [Google Scholar] [CrossRef]

- Taleb, Nassim Nicholas. 2012. Antifragile: Things that Gain from Disorder. London: Penguin. [Google Scholar]

- Taylor-Gooby, Peter, and Jens O. Zinn, eds. 2006. Risk in Social Science. Oxford: OUP. [Google Scholar]

- Timmers, Paul. 2022. How Europe Aims to Achieve Strategic Autonomy for Semiconductors. Washington, DC: Brookings Institute. [Google Scholar]

- United Nations Conference on Trade and Development (UNCTAD). 2021. Climate Change, Green Recovery and Trade. Geneva: UNCTAD. [Google Scholar]

- United Nations Conference on Trade and Development (UNCTAD). 2024. Global Trade Update—December 2024. Geneva: UNCTAD. [Google Scholar]

- Villars Institute. 2024. Villars Framework for a Sustainable Global Trade System, Version 2.0. Villars: Villars Institute. [Google Scholar]

- World Economic Forum (WEF). 2024. Global Risks Report 2024. Davos: WEF. [Google Scholar]

- World Economic Forum (WEF). 2025. Global Risks Report 2025. Davos: WEF. [Google Scholar]

- World Trade Organisation (WTO). 2021a. Trade and Climate Change: The Carbon Content of International Trade. Geneva: WTO. [Google Scholar]

- World Trade Organisation (WTO). 2021b. Trade Policies Adopted to Address Climate Change. Geneva: WTO. [Google Scholar]

- World Trade Organisation (WTO). 2022. World Trade Report: Climate Change and International Trade. Geneva: WTO. [Google Scholar]

- Wu, Lunting. 2023. China’s Transition from the BRI to the GDI. The Diplomat, June 11. [Google Scholar]

- Zhang, Baohui. 2024. Hoping for the Best, Preparing for the Worst: China’s Varied Responses to US Strategic Competition. Journal of Contemporary China 33: 352–71. [Google Scholar] [CrossRef]

- Zhong, Jiarui, and Jiansuo Pei. 2023. Carbon border adjustment mechanism: A systematic literature review of the latest developments. Climate Policy 24: 228–42. [Google Scholar] [CrossRef]

- Zhou, Weihuan, Huiqin Jiang, and Zhe Chen. 2023. Trade vs. Security: Recent Developments of Global Trade Rules and China’s Policy and Regulatory Responses from Defensive to Proactive. World Trade Review 22: 193–211. [Google Scholar] [CrossRef]

{kind=link}

| Initiative | Status | Risk Domain Aspects | Overview |

|---|---|---|---|

| EU Economic Security Strategy | Launched June 2023 | Economic security Geopolitical volatility Technology control | Main priorities: 1. Promoting EU competitiveness. 2. Protecting the EU from economic security risks. 3. Partnering with the broadest possible range of countries who share the EU’s concerns or interests on economic security. |

| Japan Economic Security Protection Act | Launched May 2022 | Economic security Geopolitical volatility Technology control | Main themes: 1. Ensuring stable supplies of critical materials both domestically and internationally. 2. Stable provision of services using critical infrastructure. 3. Supporting the domestic development of critical technologies. 4 Strengthening Japan’s patent and technology export control system. |

| China Dual Circulation Strategy | Launched May 2020 | Economic security Geopolitical volatility Technology control | Main aim: Promoting China’s domestic market demand (internal circulation) and export market expansion (international circulation). Represents a shift more towards an import substitution approach where greater priority afforded to strengthening domestic consumption, production, and technological capabilities. |

| China Global Development Initiative (GDI) | Launched September 2021 | Economic security Geopolitical volatility Technology control | Eight priority areas: 1. Poverty reduction. 2. Food security. 3. Pandemic responses. 4. Financing for development. 5. Climate change and green development. 6. Industrialisation. 7. Digital economy. 8. Connectivity. As many as 60+ nations are GDI Group of Friends partners. First phase of 50 projects and over 1000 capacity-building programmes announced in September 2022. Trade policy aspects centre mainly on digital trade infrastructure (e.g., smart customs) and addressing supply chain disruptions. |

| US—Japan Critical Minerals Agreement | In force March 2023 | Economic security Climate–environmental Technology control | Main aims: 1. Strengthen and diversify critical minerals international supply chain trade links between both countries. 2. Promote adoption of battery technologies by formalising shared mutual commitments to facilitate trade and fair market competition in critical minerals. 3. Ensure robust environmental and labour standards in this trade. 4. Cooperate to ensure secure, sustainable, and equitable critical minerals supply chains. |

| Australia— US Climate, Critical Minerals and Clean Energy Transformation Compact | In force May 2023 | Economic security Climate–environmental Technology control | Main themes: 1. Coordinating supply chains, accelerating market development and investment to support the clean energy economy. 2. Supporting climate mitigation, adaptation, and resilience in the Indo-Pacific and beyond. |

| EU—US Critical Minerals Agreement | Negotiations from June 2023. Future tbc | Economic security Climate–environmental Technology control | Main themes: 1. Trade facilitation of critical minerals. 2. Cooperation on promoting higher environmental protection, international technical standards, and circular economy approaches in critical minerals production and trade. 3. Promotion of labour rights in the sector. 4. Strengthening sustainable and equitable supply chains through established common standards. |

| UK—US Critical Minerals Agreement | Negotiations from June 2023. Future tbc | Economic security Climate–environmental Technology control | Based on a similar agreement to the US–Japan equivalent above. |

| Indonesia—US Critical Minerals Agreement | Proposed in September 2023. Future tbc | Economic security Climate–environmental Technology control | Based on a similar agreement to the US–Japan equivalent above. |

| Minerals Security Partnership (MSP) US, EU, Canada, Australia, UK, France, Germany, Italy, Sweden, Finland, Norway, Japan, India, South Korea. | Launched June 2022. Future tbc | Economic security Climate–environmental Technology control | Main aim: Accelerate development of diverse and sustainable international trade of critical minerals and their supply chains through working with member governments and industry to facilitate targeted financial and diplomatic support for strategic projects. |

| Indo-Pacific Economic Framework (IPEF) US, Australia, Brunei, Fiji, India, Indonesia, Japan, South Korea, Malaysia, New Zealand, the Philippines, Singapore, Thailand, Vietnam | Negotiations from May 2022 but ended in 2025 by Trump 2.0 administration. Agreements reached on Pillars 2, 3 and 4 by 2024 | Geopolitical volatility Climate–environmental (Socio-environmental) Economic security | Four pillars: 1. Fair and resilient trade. 2. Supply chain resilience. 3. Clean energy, decarbonisation, and infrastructure. 4. Tax and anti-corruption. |

| EU New Trade Strategy | Launched February 2021 | Geopolitical volatility Economic security Climate–environmental (Socio-environmental) Technology control | Main objectives: 1. Green and digital transformation. 2. Shaping global rules for more sustainable and fairer globalisation. 3. Stricter enforcement of EU rights and trade interests. Pursued through six main policies: 1. Reform WTO. 2. Promote responsible and sustainable value chains. 3. Support digital transition and trade in services. 4. Strengthen EU’s regulatory impact globally. 5. Strengthen EU trade partnerships with neighbourhood and Africa. 6. Strengthen enforcement of EU trade agreements. |

| EU Anti-Coercion Instrument | In force October 2023 | Geopolitical volatility | Enables EU to respond to different forms of economic coercion. First seeks dialogue and engagement with third country perpetrators of economic coercion against the EU or any Member State. If this fails, appropriate countermeasures deployed against the perpetrator, including tariffs, restrictions on services trade, restricted access to public procurement markets. |

| Agreement on Climate Change, Trade and Sustainability (ACCTS) New Zealand (lead), Costa Rica, Fiji, Iceland, Norway, Switzerland | Negotiations concluded July 2024, signed November 2024 | Climate–environmental | Five trade rule areas: 1. Eco-labelling. 2. Environmental goods liberalisation. 3. Environmental services liberalisation. 4. Fossil fuel subsidy elimination and reform. 5. Legal and institutional mechanisms. Open to others to accede and gradually expand membership. |

| Singapore-Australia Green Economy Agreement (GEA) | In force January 2023 | Climate–environmental Technology control | Seventeen areas of action under six themes: Theme 1 (Trade and Investment) comprises six action areas: 1.1. Environmental goods liberalisation. 1.2. Environmental services liberalisation. 1.3. Non-trade barriers. 1.4. Green trade facilitation. 1.5. Environmentally sustainable government procurement. 1.6. Sustainable agriculture and food systems. Trade also covered under: 4.1. Cross-border green electricity trade. 4.2. Green shipping. 4.3. Sustainable aviation. 6.3. Eco-labelling. |

| UK-Singapore Green Economy Framework | In force March 2023 | Climate–environmental Technology control | Three pillars: 1. Green transport, especially decarbonising international maritime shipping and aviation cargo trade. 2. Low carbon energy and technologies, including certification, standards, and other regulations to facilitate climate-friendly trade. 3. Carbon markets and sustainable finance, including dialogue on carbon border adjustment mechanisms. |

| EU Carbon Border Adjustment Mechanism (CBAM) | In force May 2023 | Climate–environmental | First stage implementation from October 2023: CBAM introduced reporting obligations only on EU-based firms importing in six sectors: steel and iron, cement, aluminium, fertilisers, electricity and hydrogen. Second phase from January 2026: CBAM tariffs (or levies) will apply to imported products from all nations not linked to the EU’s Emissions Trading System or equivalent system. |

| EU Strategy for Sustainable and Circular Textiles | In force March 2022 | Climate–environmental | Includes trade policy measures on applying circular economy and sustainability regulations on EU textile imports and international supply chain trade, restrictions on exported textiles waste, eco-labelling of textile imports, and promoting sustainability in global trade of used textiles. |

| EU Deforestation Free Commodities directive | In force June 2023 | Climate–environmental | Traders importing certain commodities (or derived products from them) into EU market, or exports from it, obligated to prove non-sourcing from recently deforested land or have contributed to forest degradation. Examples of ‘forest risk’ commodities and products include beef, chocolate, furniture, palm oil, rubber, tyres. |

| EU-US Global Arrangement on Sustainable Steel and Aluminium | Negotiation from October 2021. Future tbc | Climate–environmental Economic security Technology control | Promoting decarbonised steel and aluminium production and trade while discouraging trade in high-carbon equivalents. |

| EU Corporate Sustainability Due Diligence directive | Proposed by European Commission in February 2022, awaiting approval | Climate–environmental (socio-environmental) | Main aim: Foster strong sustainable and responsible corporate behaviour throughout global value chain (GVC) trade. Requires EU-based companies to ‘identify and, where necessary, prevent, end or mitigate adverse impacts of their activities on human rights, such as child labour and exploitation of workers, and on the environment, for example pollution and biodiversity loss’ in GVC production and trade. |

| Indigenous Peoples Economic and Trade Cooperation Arrangement (IPETCA) Australia, Canada, New Zealand, Taiwan | In force December 2021 | Climate–environmental (socio-environmental) | Main aims: 1. Strengthen the inclusion of indigenous peoples into international trade activity. 2. Address indigenous trade issues more specifically. 3. Foster wider economic cooperation among indigenous communities in the Asia–Pacific region. |

| US Uyghur Forced Labor Prevention Act (UFLPA) | In force June 2022 | Climate–environmental (socio-environmental) | Prohibits the import of goods mined, produced, or manufactured partially or wholly in China’s Xinjiang Autonomous Region. |

| US CHIPS Act | In force August 2022 | Technology control Economic security Geopolitical volatility | Main aim: Expand national capacity in semiconductor manufacturing, research and development, jobs creation, and skills. Includes production subsidy support and reshoring investment incentives aimed at reducing import demand and boosting exports of US-made semiconductors while also exercising export controls on advanced microchips. |

| US Inflation Reduction Act (IRA) | In force August 2023 | Climate–environmental Technology control Economic security | Main aim: Enhance US economic competitiveness, technology and innovation capacity, and productivity in clean energy sectors, notably renewable electricity, low carbon manufacturing, environmental technology, transportation, and electric vehicles. Includes measures to reduce import demand, boost exports, and various homeshoring and friendshoring incentives. |

| US Trump 2.0 high- tariff protectionism | From February 2025 | Economic security Geopolitical volatility Technology control | Application of high-level tariffs on all the US’ major trade partners (most notably China, Canada, Mexico, and the EU) and also those countries with whom the US has high proportionate trade deficits with on a ‘reciprocal’ basis. Application of a 10 percent baseline universal tariff on all countries. |

| EU European Chips Act | In force July 2023 | Technology control Economic security Geopolitical volatility | Main aim: Strengthen EU capacity in semiconductor production, research and development, jobs, and skills base to achieve more strategic autonomy in the sector. Three pillars: 1. Support for ramping up technological capacity and innovation in advanced microchips. 2. Scaling up investments in production capacities. 3. Strengthen capacity to monitor and respond to future semiconductor supply crises. |

| Digital Economy Partnership Agreement (DEPA) Chile, New Zealand, Singapore | Original framework version entered force in January 2021. Protocol version in July 2023 | Technology control | Main aim: Create new rules for digital trade across various areas: digital products and innovation, data protection and management, digital identities and inclusion, SMEs, consumer trust, artificial intelligence, digital trade facilitation, and cooperation. Canada and South Korea negotiating accession from 2023. |

| UK—Singapore Digital Economy Agreement (UKSDEA) | In force June 2022 | Technology control | Three main goals: 1. Facilitate a more secure digital environment between both parties. 2. Enable trusted data flows. 3. Support end-to-end digital trade. |

| UK—Ukraine Digital Economy Agreement (UKUDEA) | Signed March 2023 | Technology control | Main areas: 1. Open and inclusive digital markets. 2. Data flows. 3. Consumer and business safeguards. 4. Digital trading systems. 5. Financial services. 6. Tech partnerships. |

| ASEAN Digital Economy Framework Agreement (DEFA) | Launched November 2023 | Technology control | Intention to develop a comprehensive roadmap across the Association of South East Asian Nations (ASEAN) regional bloc of ten nations to accelerate digital trade growth, enhancing interoperability and creating secure digital trade environments. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dent, C.M. Trade Risk Society—Understanding Trade Policymaking in the 2020s. Soc. Sci. 2025, 14, 338. https://doi.org/10.3390/socsci14060338

Dent CM. Trade Risk Society—Understanding Trade Policymaking in the 2020s. Social Sciences. 2025; 14(6):338. https://doi.org/10.3390/socsci14060338

Chicago/Turabian StyleDent, Christopher M. 2025. "Trade Risk Society—Understanding Trade Policymaking in the 2020s" Social Sciences 14, no. 6: 338. https://doi.org/10.3390/socsci14060338

APA StyleDent, C. M. (2025). Trade Risk Society—Understanding Trade Policymaking in the 2020s. Social Sciences, 14(6), 338. https://doi.org/10.3390/socsci14060338