A Hybrid Rule-Based Rough Set Approach to Explore Corporate Governance: From Ranking to Improvement Planning

Abstract

1. Introduction

2. Literature Review

2.1. Four Dimensions of Corporate Governance

- (1)

- Protecting shareholders’ rights and interests and treating shareholders equitably;

- (2)

- Enhancing board composition and operation;

- (3)

- Increasing information transparency;

- (4)

- Putting CSR (corporate social responsibility) into practice.

2.2. Rough Set Theory

2.3. Corporate Governance and Rough Set Theory

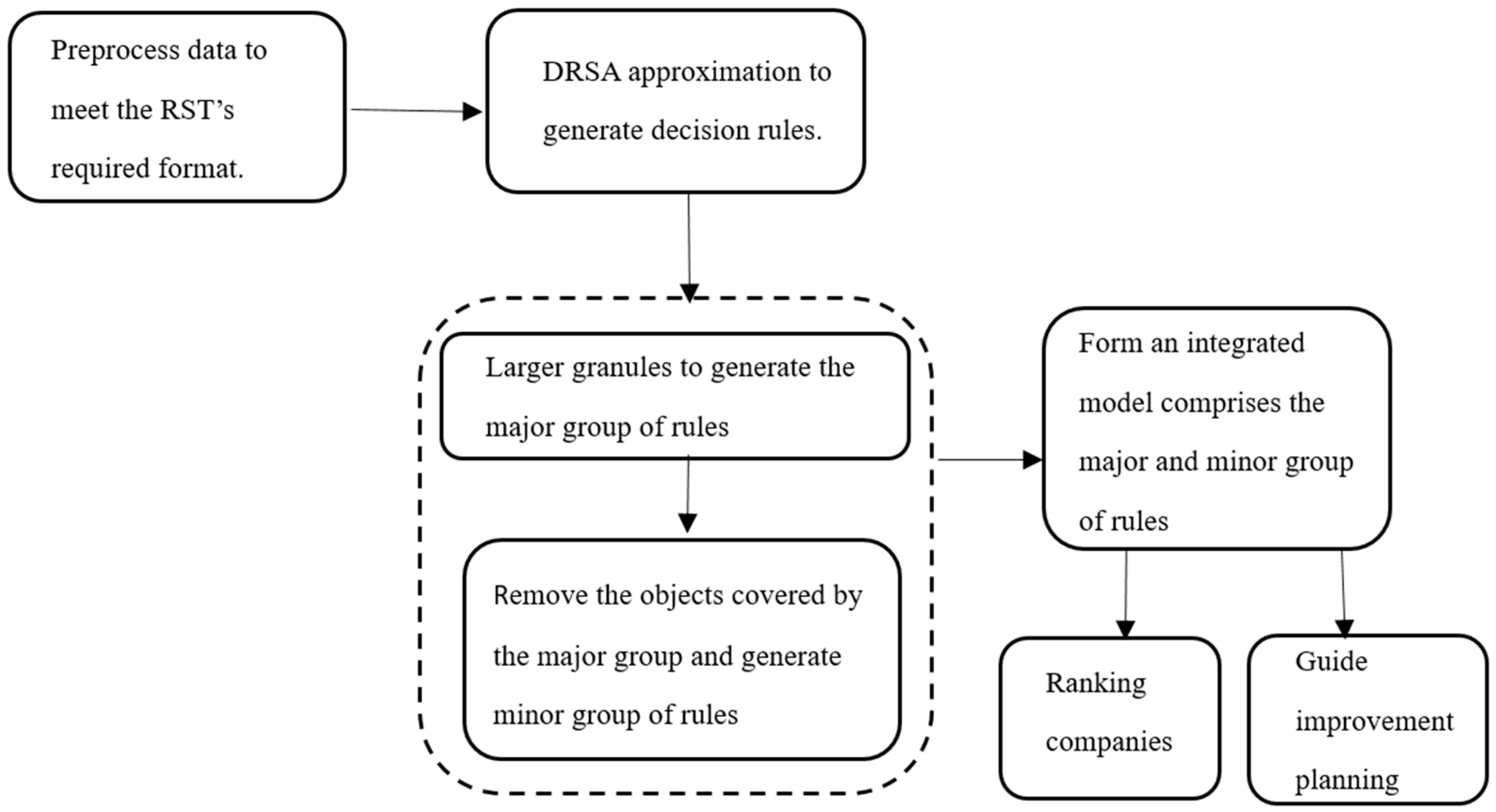

3. Multiple Rule-Based Decision-Making Model

3.1. Data Preprocessing

3.2. Rough Approximations

3.3. Rules Selection

3.4. Evaluate Sample Stocks

3.5. Research Limitations of MCDM Methods

3.6. Comparison with the DANP Approach

4. Discussion

4.1. Implications of the Critical Criteria

4.2. Improvement Planning

5. Conclusions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Conditions | Decision | Supports |

|---|---|---|

| (C11 2) | D Bad | 2 |

| (C3 1) and (C4 2) | D Bad | 2 |

| (C2 2) and (C8 1) | D Bad | 1 |

| (C2 1) and (C13 1) | D Bad | 1 |

| (C5 2) and (C12 2) | D Bad | 4 |

| (C6 1) and (C13 2) | D Bad | 3 |

| (C5 2) and (C13 2) | D Bad | 4 |

| (C13 2) | D Mid | 14 |

| (C1 1) | D Mid | 9 |

| (C12 2) | D Mid | 9 |

| (C8 2) | D Mid | 6 |

| (C4 1) and (C6 2) | D Mid | 3 |

| Conditions | Decision | Supports |

|---|---|---|

| (C2 1) and (C13 2) | D Vbad | 6 |

| (C3 1) and (C4 2) | D Vbad | 2 |

| (C2 2) and (C8 1) | D Vbad | 1 |

| (C5 2) and (C12 2) | D Vbad | 4 |

| (C13 2) | D Bad | 11 |

| (C12 2) | D Bad | 9 |

| (C1 1) | D Bad | 6 |

| (C11 2) | D Bad | 2 |

| (C4 1) and (C6 2) | D Bad | 3 |

| (C8 2) | D Good | 5 |

| Criteria | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TSMC | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 |

| Foxconn | 3 | 1 | 2 | 2 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 |

| Secom | 1 | 2 | 2 | 1 | 3 | 3 | 3 | 3 | 3 | 3 | 2 | 3 | 3 |

| Zinwell | 2 | 3 | 2 | 1 | 3 | 2 | 3 | 3 | 3 | 3 | 3 | 2 | 3 |

References

- Shleifer, A.; Vishny, R.W. A survey of corporate governance. J. Financ. 1997, 52, 737–783. [Google Scholar] [CrossRef]

- Naciti, V.; Cesaroni, F.; Pulejo, L. Corporate governance and sustainability: A review of the existing literature. J. Manag. Gov. 2021, 26, 55–74. [Google Scholar] [CrossRef]

- Md Nasir, N.A.; Hashim, H.A. Corporate governance performance and financial statement fraud: Evidence from Malaysia. J. Financ. Crime 2021, 28, 797–809. [Google Scholar] [CrossRef]

- Kabeyi, M.J.B. Corporate governance in manufacturing and management with analysis of governance failures at Enron and Volkswagen Corporations. Am. J. Oper. Manag. Inf. Syst. 2020, 4, 109–123. [Google Scholar]

- Panda, B.; Leepsa, N.M. Agency theory: Review of theory and evidence on problems and perspectives. Indian J. Corp. Gov. 2017, 10, 74–95. [Google Scholar] [CrossRef]

- Daily, C.M.; Dalton, D.R.; Rajagopalan, N. Governance through ownership: Centuries of practice, decades of research. Acad. Manag. J. 2003, 46, 151–158. [Google Scholar] [CrossRef]

- CGES. Available online: https://cgc.twse.com.tw/evaluationCorp/listEn (accessed on 10 January 2024).

- Huang, J.Y.; Shen, K.Y.; Shieh, J.C.; Tzeng, G.H. Strengthen financial holding companies’ business sustainability by using a hybrid corporate governance evaluation model. Sustainability 2019, 11, 582. [Google Scholar] [CrossRef]

- Pawlak, Z. Rough sets. Int. J. Comput. Inf. Sci. 1982, 11, 341–356. [Google Scholar] [CrossRef]

- Tzeng, G.H.; Shen, K.Y. New Concepts and Trends of Hybrid Multiple Criteria Decision Making; CRC Press: Boca Raton, FL, USA, 2017. [Google Scholar]

- Shen, K.Y.; Zavadskas, E.K.; Tzeng, G.H. Updated discussions on ‘Hybrid multiple criteria decision-making methods: A review of applications for sustainability issues’. Econ. Res.-Ekon. Istraživanja 2018, 31, 1437–1452. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behaviour, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Davis, J.H.; Schoorman, F.D.; Donaldson, L. Toward a stewardship theory of management. Acad. Manag. Rev. 1997, 22, 20–47. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Kao, T.H.; Wei, H.S. The effect of IFRS, information asymmetry and corporate governance on the quality of accounting information. Asian Econ. Financ. Rev. 2014, 4, 226. [Google Scholar]

- Ştefănescu, C.A. Disclosure and transparency in corporate governance codes-comparative analysis with prior literature findings. Procedia-Soc. Behav. Sci. 2011, 24, 1302–1310. [Google Scholar] [CrossRef]

- Laux, V. Corporate governance, board oversight, and CEO turnover. Found. Trends Account. 2014, 8, 1–73. [Google Scholar] [CrossRef]

- Baker, C.R.; Owsen, D.M. Increasing the role of auditing in corporate governance. Crit. Perspect. Account. 2002, 13, 783–795. [Google Scholar] [CrossRef]

- Jesover, F. Corporate governance in the Russian Federation: The relevance of the OECD principles on shareholder rights and equitable treatment. Corp. Gov. Int. Rev. 2001, 9, 79–88. [Google Scholar] [CrossRef]

- Deetz, S. Corporate governance, corporate social responsibility, and communication. In The Debate Over Corporate Social Responsibility; Oxford University Press: Oxford, UK, 2007; pp. 267–278. [Google Scholar]

- Harjoto, M.A.; Jo, H. Corporate governance and CSR nexus. J. Bus. Ethics 2011, 100, 45–67. [Google Scholar] [CrossRef]

- Shu, P.G.; Chiang, S.J. The impact of corporate governance on corporate social performance: Cases from listed firms in Taiwan. Pac.-Basin Financ. J. 2020, 61, 101332. [Google Scholar] [CrossRef]

- Singh, K.; Rastogi, S. Corporate governance and financial performance: Evidence from listed SMEs in India. Benchmarking Int. J. 2023, 30, 1400–1423. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A.; Vishny, R. Investor protection and corporate governance. J. Financ. Econ. 2000, 58, 3–27. [Google Scholar] [CrossRef]

- Adjaoud, F.; Ben-Amar, W. Corporate governance and dividend policy: Shareholders’ protection or expropriation? J. Bus. Financ. Account. 2010, 37, 648–667. [Google Scholar] [CrossRef]

- Schöndube-Pirchegger, B.; Schöndube, J.R. On the appropriateness of performance-based compensation for supervisory board members–an agency theoretic approach. Eur. Account. Rev. 2010, 19, 817–835. [Google Scholar] [CrossRef]

- Mrabure, K.O.; Abhulimhen-Iyoha, A. Corporate governance and protection of stakeholders rights and interests. Beijing Law Rev. 2020, 11, 292. [Google Scholar] [CrossRef]

- Naciti, V. Corporate governance and board of directors: The effect of a board composition on firm sustainability performance. J. Clean. Prod. 2019, 237, 117727. [Google Scholar] [CrossRef]

- Weisbach, M.S. Outside directors and CEO turnover. J. Financ. Econ. 1988, 20, 431–460. [Google Scholar] [CrossRef]

- Bhagat, S.; Black, B. The uncertain relationship between board composition and firm performance. Bus. Lawyer 1999, 54, 921–963. [Google Scholar] [CrossRef]

- Duru, A.; Iyengar, R.J.; Zampelli, E.M. The dynamic relationship between CEO duality and firm performance: The moderating role of board independence. J. Bus. Res. 2016, 69, 4269–4277. [Google Scholar] [CrossRef]

- Madhani, P.M. Diverse roles of corporate board: Review of various corporate governance theories. IUP J. Corp. Gov. 2017, 16, 7–28. [Google Scholar]

- Giovannini, R. Corporate governance, family ownership and performance. J. Manag. Gov. 2010, 14, 145–166. [Google Scholar] [CrossRef]

- Fung, B. The demand and need for transparency and disclosure in corporate governance. Univers. J. Manag. 2014, 2, 72–80. [Google Scholar] [CrossRef]

- Assidi, S. Voluntary disclosure and corporate governance: Substitutes or complements for firm value? Compet. Rev. Int. Bus. J. 2023, in press. [Google Scholar]

- Chan, S.H.; Creel, T.S.; Song, Q.; Yurova, Y.V. Does CSR reporting indicate strong corporate governance? Int. J. Account. Inf. Manag. 2021, 29, 27–42. [Google Scholar] [CrossRef]

- Jain, T.; Jamali, D. Looking inside the black box: The effect of corporate governance on corporate social responsibility. Corp. Gov. Int. Rev. 2016, 24, 253–273. [Google Scholar] [CrossRef]

- Okafor, A.; Adeleye, B.N.; Adusei, M. Corporate social responsibility and financial performance: Evidence from US tech firms. J. Clean. Prod. 2021, 292, 126078. [Google Scholar] [CrossRef]

- Nareswari, N.; Tarczyńska-Łuniewska, M.; Al Hashfi, R.U. Analysis of environmental, social, and governance performance in Indonesia: Role of ESG on corporate performance. Procedia Comput. Sci. 2023, 225, 1748–1756. [Google Scholar] [CrossRef]

- Pawlak, Z. Rough Sets: Theoretical Aspects of Reasoning about Data; Springer Science & Business Media: New York, NY, USA, 1991; Volume 9. [Google Scholar]

- Pawlak, Z.; Skowron, A. Rudiments of rough sets. Inf. Sci. 2007, 177, 3–27. [Google Scholar] [CrossRef]

- Greco, S.; Matarazzo, B.; Slowinski, R. Rough approximation by dominance relations. Int. J. Intell. Syst. 2002, 17, 153–171. [Google Scholar] [CrossRef]

- Błaszczyński, J.; Greco, S.; Matarazzo, B.; Szeląg, M. Dominance-Based Rough Set Approach: Basic Ideas and Main Trends. In Intelligent Decision Support Systems: Combining Operations Research and Artificial Intelligence-Essays in Honor of Roman Słowiński; Springer International Publishing: Cham, Switzerland, 2022; pp. 353–382. [Google Scholar]

- Shen, K.Y.; Tzeng, G.H. A decision rule-based soft computing model for supporting financial performance improvement of the banking industry. Soft Comput. 2015, 19, 859–874. [Google Scholar] [CrossRef]

- Shen, K.Y.; Tzeng, G.H. DRSA-based neuro-fuzzy inference systems for the financial performance prediction of commercial banks. Int. J. Fuzzy Syst. 2014, 16, 173. [Google Scholar]

- Liou, J.J.; Tzeng, G.H. A dominance-based rough set approach to customer behavior in the airline market. Inf. Sci. 2010, 180, 2230–2238. [Google Scholar] [CrossRef]

- Greco, S.; Matarazzo, B.; Slowinski, R. Rough sets methodology for sorting problems in presence of multiple attributes and criteria. Eur. J. Oper. Res. 2002, 138, 247–259. [Google Scholar] [CrossRef]

- García, F.; González-Bueno, J.; Guijarro, F.; Oliver, J. Forecasting the environmental, social, and governance rating of firms by using corporate financial performance variables: A rough set approach. Sustainability 2020, 12, 3324. [Google Scholar] [CrossRef]

- Wang, Z.; Li, H. Financial distress prediction of Chinese listed companies: A rough set methodology. Chin. Manag. Stud. 2007, 1, 93–110. [Google Scholar] [CrossRef]

- Karimi, T.; Hojati, A. Corporate sustainability assessment based on rough-grey set theory. J. Model. Manag. 2022, 17, 440–455. [Google Scholar] [CrossRef]

- Core, J.E.; Holthausen, R.W.; Larcker, D.F. Corporate governance, chief executive officer compensation, and firm performance. J. Financ. Econ. 1999, 51, 371–406. [Google Scholar] [CrossRef]

- Shen, Y.V.; Wang, W.; Zhou, F. Insider pledging in the US. J. Financ. Stab. 2021, 53, 100830. [Google Scholar] [CrossRef]

- Chi, Y.L. The agency costs of family ownership: Evidence from innovation performance. J. Bank. Financ. 2023, 148, 106737. [Google Scholar] [CrossRef]

- Ho, S.S.; Wong, K.S. A study of the relationship between corporate governance structures and the extent of voluntary disclosure. J. Int. Account. Audit. Tax. 2001, 10, 139–156. [Google Scholar] [CrossRef]

- Alfraih, M.M.; Almutawa, A.M. Voluntary disclosure and corporate governance: Empirical evidence from Kuwait. Int. J. Law Manag. 2017, 59, 217–236. [Google Scholar] [CrossRef]

- Eng, L.L.; Mak, Y.T. Corporate governance and voluntary disclosure. J. Account. Public Policy 2003, 22, 325–345. [Google Scholar] [CrossRef]

- Akhtaruddin, M.; Hossain, M.A.; Hossain, M.; Yao, L. Corporate governance and voluntary disclosure in corporate annual reports of Malaysian listed firms. J. Appl. Manag. Account. Res. 2009, 7, 1–19. [Google Scholar]

- Tadu, R.; Mukonya, S. Challenges of whistle blowing as a corporate governance control tool in the Zimbabwean banking sector during 2000–2008. J. Res. Bus. Econ. Manag. 2016, 6, 954–963. [Google Scholar]

- Drogalas, G.; Arampatzis, K.; Anagnostopoulou, E. The relationship between corporate governance, internal audit and audit committee: Empirical evidence from Greece. Corp. Ownersh. Control 2016, 14, 569–577. [Google Scholar] [CrossRef]

- Saaty, T.L. What is the Analytic Hierarchy Process? Springer: Berlin/Heidelberg, Germany, 1988; pp. 109–121. [Google Scholar]

- Saaty, T.L. Decision Making with Dependence and Feedback: The Analytic Network Process; RWS Publications: Pittsburgh, PA, USA, 1996; Volume 4922. [Google Scholar]

- Shen, Y.C.; Lin, G.T.; Tzeng, G.H. A novel multi-criteria decision-making combining Decision Making Trial and Evaluation Laboratory technique for technology evaluation. Foresight 2012, 14, 139–153. [Google Scholar] [CrossRef]

- Shen, K.Y.; Yan, M.R.; Tzeng, G.H. Combining VIKOR-DANP model for glamor stock selection and stock performance improvement. Knowl.-Based Syst. 2014, 58, 86–97. [Google Scholar] [CrossRef]

- Turley, S.; Zaman, M. The corporate governance effects of audit committees. J. Manag. Gov. 2004, 8, 305–332. [Google Scholar] [CrossRef]

- Ameer, R.; Ramli, F.; Zakaria, H. A new perspective on board composition and firm performance in an emerging market. Corp. Gov. Int. J. Bus. Soc. 2010, 10, 647–661. [Google Scholar] [CrossRef]

| Indicator | Description of the Indicators | Reference/Foundation |

|---|---|---|

| C1 | Ratio of remuneration of directors and supervisors to net profit before the distribution of dividends | [51]/Agency problem |

| C2 | The average ratio of pledges by directors, supervisors, and substantial shareholders | [52]/Agency problem |

| C3 | The proportion of seats held by government agencies or single-listed companies and their subsidiaries on the board of directors | Agency theory |

| C4 | Proportion of general manager (executive director) board members and spouse or second-degree relatives among board members | [53]/Agency problem |

| C5 | Independent directors put forward opinions on major proposals on the board of directors and deal with them | Agency theory |

| C6 | The company exposes the results of the resolution of the audit committee on the major proposals and the degree of disclosure of the company’s handling | [54]/Information asymmetry |

| C7 | The head of internal audit/auditor attends the board of directors and proposes the internal audit report to each supervisor and independent director | [54]/Agency theory |

| C8 | The company voluntarily discloses its financial forecast quarterly and without having any corrections ordered by the authority or having any demerits imposed by the TWSE | [35,54,55]/Information asymmetry |

| C9 | The company discloses long-term and short-term business development plans in its annual report | [55]/Information asymmetry |

| C10 | The company discloses the remuneration details of each director and supervisor in its annual report | [56]/Information asymmetry |

| C11 | The company website discloses information related to the company’s finances, business and corporate governance | [55,56]/Information asymmetry |

| C12 | The company proactively reveals the identity of interested parties and establishes communication channels and response methods | [57]/Information asymmetry and CSR |

| C13 | The company adopts and discloses in detail on its website a whistle blower system for company insiders and outsiders to report illegal behavior (including corruption) and unethical behavior | [58]/Information asymmetry, Stakeholder Theory, and CSR |

| Year | Object Numbers | Major Group’s Reclassification | Minor Group’s Reclassification |

|---|---|---|---|

| 2018 | 72 | 58.33% | 70.00% |

| 2019 | 86 | 68.61% | 60.94% |

| Rules | Conditions | Decision | Supports Weight | Weighted Supports |

|---|---|---|---|---|

| R1 | (C1 3), (C3 3), (C4 3), (C5 3), (C8 3), and (C13 3) | D G | 4 × 2 = 8 | 8% × 0.8 = 6.4% |

| R2 | (C4 3) and (C6 3) | D M | 18 | 18% × 0.8 = 14.4% |

| R3 | (C1 3), (C4 3), and (C12 3) | D M | 17 | 17% × 0.8 = 13.6% |

| R4 | (C3 3), (C6 3), (C11 3), and (C12 3) | D M | 14 | 14% × 0.8 = 11.2% |

| R5 | (C1 3), (C53), (C6 3), and (C12 3) | D M | 22 | 22% × 0.8 = 17.6% |

| R6 | (C1 3), (C2 3), (C6 3), and (C12 3) | D M | 21 | 21% × 0.8 = 16.8% |

| Rules | Conditions | Decision | Supports Weight | Weighted Supports |

|---|---|---|---|---|

| R7 | (C3 3), (C4 3), (C6 3), and (C8 3) | D VG | 1 × 3 = 3 | 23.08% × 0.2 = 4.62% |

| R8 | (C3 3), (C4 3), and (C6 3) | D G | 2 × 2 = 4 | 30.77% × 0.2 = 6.154% |

| R9 | (C1 3), (C3 3), and (C4 3) | D M | 3 | 23.08% × 0.2 = 4.62% |

| R10 | (C1 3), (C3 3), (C6 3), and (C12 3) | D M | 3 | 23.08% × 0.2 = 4.62% |

| Weighting | TSMC | Foxconn | Secom | Zinwell |

|---|---|---|---|---|

| (rank) | 100% (1st) | 66.26% (2nd) | 50.73% (3rd) | 22.05% (4th) |

| (rank) | 100% (1st) | 64.09% (2nd) | 48.80% (3rd) | 20.24% (4th) |

| (rank) | 100% (1st) | 61.93% (2nd) | 46.87% (3rd) | 18.43% (4th) |

| DANP Weights | TSMC | Foxconn | Secom | Zinwell | |

|---|---|---|---|---|---|

| C1 | 8.73% | 3 | 3 | 1 | 2 |

| C2 | 5.62% | 3 | 1 | 2 | 3 |

| C3 | 5.11% | 3 | 2 | 2 | 2 |

| C4 | 6.12% | 3 | 2 | 1 | 1 |

| C5 | 7.59% | 3 | 3 | 3 | 3 |

| C6 | 7.29% | 3 | 3 | 3 | 2 |

| C7 | 6.53% | 3 | 3 | 3 | 3 |

| C8 | 6.12% | 3 | 3 | 3 | 3 |

| C9 | 5.33% | 3 | 3 | 3 | 3 |

| C10 | 7.06% | 3 | 3 | 3 | 3 |

| C11 | 6.79% | 3 | 3 | 2 | 3 |

| C12 | 13.91% | 3 | 3 | 3 | 2 |

| C13 | 13.79% | 3 | 3 | 3 | 3 |

| Scores (ranking) | 2.5863 (1st) | 2.3615 (2nd) | 2.1140 (3rd) | 2.1134 (4th) |

| R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 | Sum | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| C1 | 6 (2nd) | ||||||||||

| C2 | 1 (5th) | ||||||||||

| C3 | 6 (2nd) | ||||||||||

| C4 | 6 (2nd) | ||||||||||

| C5 | 2 (4th) | ||||||||||

| C6 | 7 (1st) | ||||||||||

| C7 | 0 | ||||||||||

| C8 | 2 (4th) | ||||||||||

| C9 | 0 | ||||||||||

| C10 | 0 | ||||||||||

| C11 | 1 (5th) | ||||||||||

| C12 | 4 (3rd) | ||||||||||

| C13 | 2 (4th) |

| Secom | R1 | R2 | R3 | R4 | R5 | R6 |

|---|---|---|---|---|---|---|

| Change | 8% × 1/6 | 18% × 1/2 | 17% × 1/3 | 14% × 1/4 | 22% × 1/4 | 21% × 1/4 |

| Improved gap | 1.33% | 9.00% (1st) | 5.67% (2nd) | 3.50% | 5.50% (3rd) | 5.25% |

| Side effects | 8% × 1/6 = 1.33% | 17% × 1/3 = 5.67% |

| Secom | R7 | R8 | R9 | R10 |

|---|---|---|---|---|

| Change | 23.08% × 1/4 | 30.77% × 1/3 | 23.08% × 1/3 | 23.08 × 1/4 |

| Improved gap | 5.77% | 10.26% (1st) | 7.69% (2nd) | 5.77% |

| Side effects | +5.77% | +7.69% | +5.77% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shen, K.-Y. A Hybrid Rule-Based Rough Set Approach to Explore Corporate Governance: From Ranking to Improvement Planning. Axioms 2024, 13, 119. https://doi.org/10.3390/axioms13020119

Shen K-Y. A Hybrid Rule-Based Rough Set Approach to Explore Corporate Governance: From Ranking to Improvement Planning. Axioms. 2024; 13(2):119. https://doi.org/10.3390/axioms13020119

Chicago/Turabian StyleShen, Kao-Yi. 2024. "A Hybrid Rule-Based Rough Set Approach to Explore Corporate Governance: From Ranking to Improvement Planning" Axioms 13, no. 2: 119. https://doi.org/10.3390/axioms13020119

APA StyleShen, K.-Y. (2024). A Hybrid Rule-Based Rough Set Approach to Explore Corporate Governance: From Ranking to Improvement Planning. Axioms, 13(2), 119. https://doi.org/10.3390/axioms13020119