1. Introduction

The COVID-19 pandemic has disrupted many people’s finances. Managing personal financial planning is important at all times, but it becomes essential during a crisis such as the coronavirus pandemic [

1,

2,

3]. As the world continues to learn more about COVID-19, or the coronavirus, it is clear that the pandemic may impact several aspects of our lives. This provides opportunities to take stock of our current financial situation, and to establish habits that will strengthen our finances once the pandemic ends and the economy recovers, or to cope with the next economic downturn. In particular, there is an opportunity to establish better financial planning based on the last couple of months.

“Financial planning management” is a service provided by financial institutions to help high net-worth individuals protect and grow their wealth. This advanced investment advisory discipline involves providing a diverse range of services, such as financial planning, investment management, tax planning, and cash flow and debt management, based on client requirements. We are already starting to see some economic consequences, but the financially-induced stress caused by the uncertainty is less visible. Therefore, in the new world, across segments, income has vanished, reduced, or settled at a new low. “Family wealth management” is an investment advisory discipline that incorporates financial planning, investment portfolio management, and a number of aggregated financial services [

4,

5,

6]. “Private wealth management” is the term generally used to describe highly customized and sophisticated investment management and financial planning services that are delivered to high net-worth investors [

7,

8,

9]. In general, this includes advice on the use of trusts and other estate planning vehicles, business succession or stock option planning, and the use of hedging derivatives for large blocks of stock [

10,

11].

The coronavirus outbreak and reports of how it will impact the economy continue to dominate the news [

9,

12]. A key concern for many people is how to manage their finances amidst this global pandemic. Many questions arise, such as whether to make credit card bill payments now or to defer them for a couple of months; how to plan for the upcoming financial year in the wake of an uncertain economic scenario; or deciding on where to keep one’s savings in this uncertain market. In such circumstances, people must go back to basics and ensure they have a sound financial plan in place. Wealth management bank selection is composed of many interacting elements. Clients want wealth management supervisors to simply assist in overseeing their wealth, to best serve their family’s long-term needs. Therefore, wealth management supervisors should productively and viably plan clients’ time, manage budgets, meet due dates, and achieve clients’ expectations from other individuals on time. Wealth management supervisors continuously experience and overcome issues, and managers should look beyond their individual obligations. Regardless of where directors work, wealth management supervisors ought to be proficient with computer equipment and programs. A competitive attitude and enthusiasm for work are important, as well as the stamina to work long hours and exceed what is anticipated of them, compared with their co-workers and competitors [

13].

A case study of how customers select the most suitable wealth management bank was implemented, to demonstrate the proposed hybrid method. The results can provide informative and practical suggestions for evaluating and selecting a wealth bank. It is found that many companies tend to focus on compensation, and neglect service. In order to improve their service to clients and customers, providers must be constantly increasing their learning, as this will help them to try out new ways of satisfying customers’ demands to serve them better. The pandemic may change the nature of trust in online payments, for two reasons: the first is the aforementioned increase in fraud, while the second is the generally higher level of economic distress worldwide [

13,

14]. The COVID-19 pandemic is having a devastating impact on Taiwan’s economy. Many people have lost their jobs, businesses across the nation have closed or declared bankruptcy, and a major drop in the stock market has severely reduced many people’s savings and retirement investments [

15,

16,

17].

The field of wealth management bank evaluation is still relatively new, but has developed rapidly over the last decade. This paper demonstrates an integrated multiple-criteria decision-making (MCDM) technique that is appropriate for family financial planning, in order to develop a survey to assess and determine the most appropriate wealth management bank. We employed the decision-making trial and evaluation laboratory (DEMATEL) method to clarify the intertwined sub-criteria interrelationships within the complex structural hierarchy of the family financial planning problem. This paper proposes a novel hybrid method to cope with the various interdependence and feedback dimensions problem within the family financial planning problem. This proposed hybrid method can provide a better understanding of the interrelationship among the evaluation and selection dimensions, and solve a complex interacting family financial planning issue in order to enhance decision-making quality. Monetary experts should not just be highly numerate; they must be able to communicate their information with viable composing and introduction abilities. The personal skills required to succeed as a financial advisor involve understanding distinctive personality types, tuning in, asking appropriate questions, settling conflicts, teaching others, and counseling clients. When financial specialists trust their wealth management directors and supervisors, and feel that their managers respect them, then financial specialists can help clients to succeed. Financial experts should show their proficient abilities and information on prospects in their specialty markets, to demonstrate a total understanding of individual qualities, and riches administration bank proficient qualities.

2. Literature Review

As the world continues to learn more about COVID-19, or the novel coronavirus, it is clear that the pandemic may influence several aspects of our lives [

18]. It is necessary to address the present crisis by cooperating in the creation of new knowledge for a social purpose, as this has the capacity to renew the social license of financial organizations. The COVID-19 pandemic has squeezed budgets and resources, and it is becoming more evident that increased collaboration between universities, sector bodies, and industry will be required to drive the sector’s recovery. Over many months, COVID-19 has spread, infecting millions, and causing enormous social and financial disturbance. Very recently, COVID-19 has enabled a brief re-emergence of public and government trust in expertise. Overall, COVID-19 has presented a set of pressing social challenges, especially in family financial planning.

The selection of a wealth management bank involves numerous associated components. Therefore, a case study of the foremost appropriate wealth management bank was conducted, to develop the proposed crossover strategy, which provides insight and proposals for assessing and selecting a wealth management bank.

This section identifies the influential wealth management bank selection criteria, according to existing literature, and discusses the regions of scarcity in these studies.

2.1. Wealth Management Bank Image Perspective

The aspect of wealth management banks’ image can be divided into three categories: reputation, market share, and degree of internationalization.

2.1.1. Reputation

Corporate reputation has recently become a topic of considerable interest for the financial industry [

19,

20,

21,

22]. Corporate reputation is an important intangible asset that enables firms to establish customer relationships [

23,

24,

25,

26]; it also helps customers decide whether to buy services or not, when they cannot assess the quality before buying. Consequently, reputation is particularly important for service companies with predominantly intangible services [

27,

28,

29,

30,

31]. A good reputation is widely regarded as leading to better employee recruitment/retention, more favorable coverage by stock market analysts and the media, better relationships with regulating agencies, an enviable bargaining tool with source/vendor/partner/distributor networks, and a more saleable brand [

32].

2.1.2. Market Share

Market share is calculated by taking the company’s sales over a period and dividing it by the total industry sales over the same period [

33]. This metric is used to give a general idea of the size of a company within its market and against its competitors [

34,

35]. Market share refers to the percentage of the overall volume of business in a given market that is controlled by one company in relation to its competitors. Information on a firm’s relative market share—which indicates its competitive position—can be combined with information on the growth rate and attractiveness of the industry, to determine the best future positioning of the firm [

36,

37]. The attractiveness of an industry can be evaluated through industry analysis, which identifies the threats and opportunities facing competitors [

38]. The growth rate of an industry is assessed by measuring the trends in customer spending levels [

33,

39].

2.1.3. Degree of Internationalization

Research has shown that as firms increase the share of their operations abroad, thus, increasing their degree of internationalization, they experience higher levels of performance [

40,

41]. The degree of internationalization can be measured in terms of the share of total sales, assets, income, or employees located outside a company’s home country [

42]. Internationalization allows firms to learn about domestic markets from their international market experience, thereby improving performance [

43]. Operating in foreign jurisdictions allows firms to access factors at lower costs [

44,

45].

2.2. Customer Service Perspective

When customers are selecting the optimal wealth management bank, the service attitude, professional consultation service, and additional services must be taken into account.

2.2.1. Service Attitude

Success in business depends largely on cultivating an attitude of service and providing value to others [

46,

47]. Firms identify a need, and supply the solution for this need, instead of concentrating on the compensation or monetary aspect [

48,

49]. An attitude of service enables companies to truly and consistently exceed the client’s expectations, without having to consciously follow any process for doing so [

50,

51]. If financial service providers take the time to listen, make the effort to care, and show a willingness to be there to help, they will win customers for life [

52,

53].

2.2.2. Professional Consultation Services

Professional services provide clients with programs designed specifically for attorneys, paralegals, and other legal professionals [

54]. The development programs consist of on-site seminars, forums, conferences, lectures, and other formats that provide continuing legal education credits [

55]. An experienced team of trusted attorney consultants and a faculty group of subject-matter experts [

56] conducts these convenient, cost-effective, accredited courses.

2.2.3. Additional Services

Additional services include individual consultations involving budgeting, credit matters, estate planning, retirement planning, college funding, general investment subjects, and tax issues [

57].

2.3. Business Process and Product Perspective

In addition to satisfying the needs associated with the wealth management bank’s image and the customer service perspective when selecting the optimal wealth management bank, the business process and product perspective also need to be addressed.

2.3.1. Diversification of Financial Instruments

Diversification is a technique that reduces risk by allocating investments among various financial instruments, industries, and other categories [

58]. It aims to maximize return by investing in different areas that would each react differently to the same event. Most investment professionals agree that, although it does not guarantee against incurring loss, diversification is the most important component that achieves long-range financial goals while minimizing risk [

13,

59].

2.3.2. Transactional Safety

Transactional safety is one of the most significant concerns for both the shopper and the retailer during an online transaction [

60]. With the increase in online banking options and shopping sites that encourage the use of checking and credit card information, transaction security has become more important than ever before [

11]. As the internet grows and diversifies with options for online payments, false sites pose a constant threat to all computer users [

61]. Exchanging sensitive information without appropriate encryption technology or security measures can make a computer user or their identity particularly vulnerable. Online transactions take place at record speed, often faster than a standard credit card transaction or check processing. As providing personal data on the internet involves various risks, taking preventative action is a necessary part of ensuring online safety [

62].

2.3.3. Diversification of Transaction Modes

The diversification of transaction modes can help clients manage risk and reduce the volatility of an asset’s price movements [

63]. Nevertheless, irrespective of how diversified a client’s portfolio is, risk can never be completely eliminated. The risk associated with individual stocks can be reduced, but general market risks affect nearly every stock, so it is important to diversify among different asset classes [

64]. The key is to find a medium between risk and return; this ensures that clients achieve their financial goals, while still achieving a good night’s rest [

65,

66].

2.4. Managers’ Learning and Growth Perspective

The factors of managers’ required learning and growth can be divided into three categories: professional financial competence, educational background and training, and previous successful experiences.

2.4.1. Professional Financial Knowledge

Knowledge is defined as a generic quality referring to a person’s overall capacity, while competency refers to specific capabilities such as leadership, which comprise attitudes and skills [

67]. Knowledge is a complex multi-dimensional phenomenon defined as the ability of financial managers to practice safely and effectively, while fulfilling their professional responsibility within their scope of practice [

68,

69].

2.4.2. Educational Background and Training

Investigation of a financial manager’s educational background is one of the most important criteria for the employment selection process [

70,

71]. A thorough background investigation will yield job-relevant information concerning an individual’s past behavior, experience, education, performance, and other critical factors important in the overall selection process [

72]. This investigation is utilized in conjunction with other screening criteria, which are equally important in determining applicants that are best qualified to be financial managers [

73]. A manager’s background can influence investors who choose to pursue a performance degree at a higher education institution, rather than to continue training at professional private studios [

74].

2.4.3. Previous Successful Experiences

The practitioner’s experience may also influence information search activities. An individual with adequate professional experience might be a highly skilled technical manager with a wide repertoire of understanding, and who possesses exceptional abilities.

The above-mentioned theoretical models have contributed to our understanding of the evaluation of wealth management banks. Consequently, this study examines a set of potentially relevant factors based on past literature, and discusses the regions of scarcity in these studies.

3. Expert Interviews

This presentation is based on a report distributed to experts before their interviews. The objective was to recall knowledge and open a discussion. We wanted the experts to have a common understanding of the results before evaluating the wealth management bank. This analysis was conducted asynchronously with the experts. We collected empirical data from several key experts in different industries. Below, we discuss the research method—namely, expert interviews—in detail.

At the time of this work’s publication, COVID-19 is having a massive effect on the global economy [

75], even if this effect has not yet been felt in everyone’s household budgets. Irrespective of the current or future health effects of COVID-19, the pandemic has affected, and is likely to continue to affect, household finances for years to come [

18]. Having a plan, prioritizing spending, and using resources efficiently, will be key to people’s financial stability [

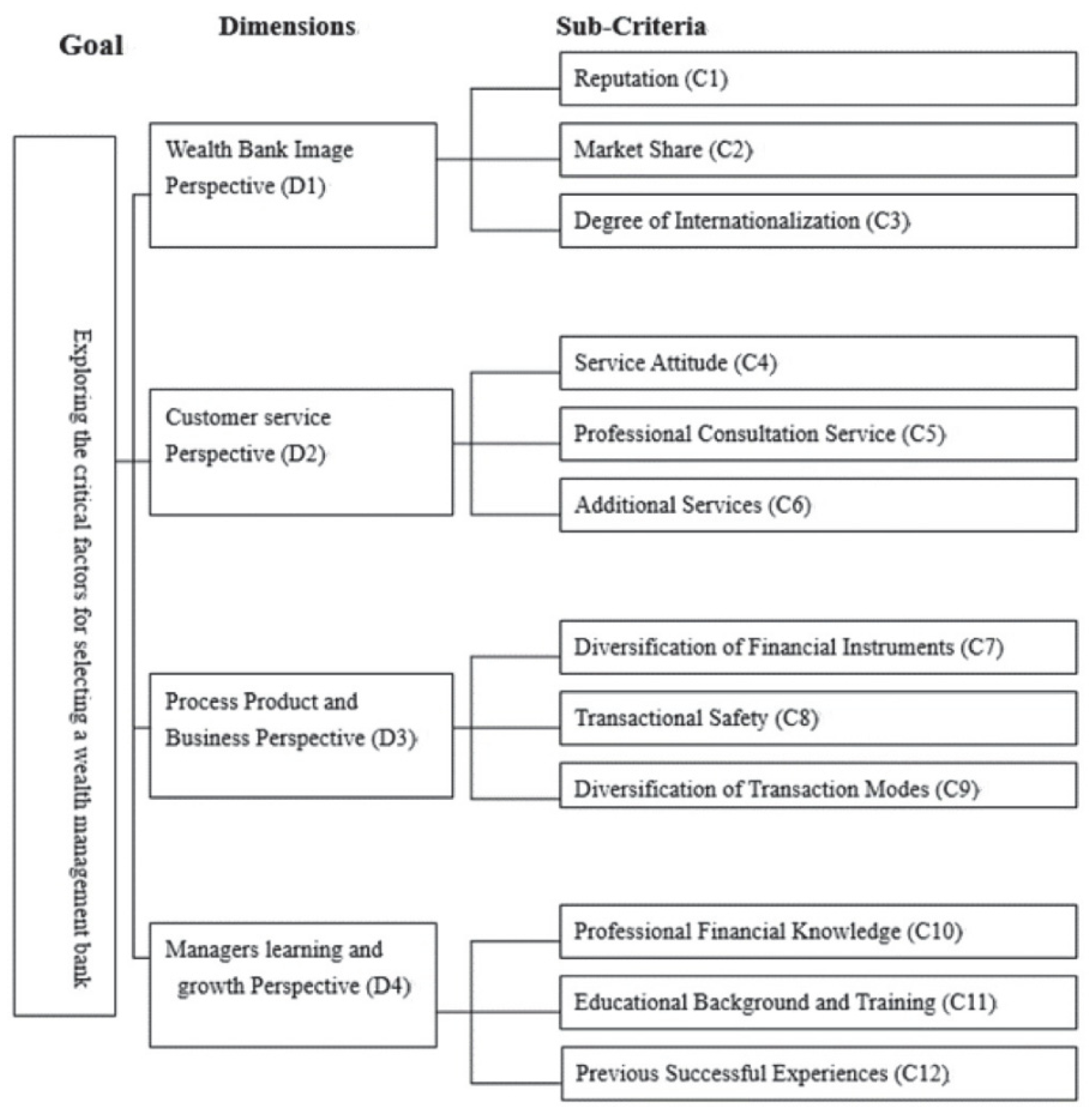

76]. The evaluation dimensions are: wealth management bank image perspective (D1), customer service perspective (D2), business process and product perspective (D3), and managers’ learning and growth perspective (D4). The evaluation criteria are: reputation (C1), market share (C2), degree of internationalization (C3), service attitude (C4), professional consultation service (C5), additional services (C6), diversification of financial instruments (C7), transactional safety (C8), diversification of transaction modes (C9), professional financial knowledge (C10), educational background and training (C11), and previous successful experiences (C12) (see

Figure 1).

Within the following sections, we describe the organizations where the specialists worked and the participants who provided the fundamental data, summarize the experts’ primary conclusions on all the topics, and then classify these opinions into four categories that were used as the basic system for the ensuing survey. In addition to answering the survey used in developing this assessment, the specialists provided their professional information and involvement in family financial planning, as well as a mechanical point of view.

Research Data Validation and Robustness

We constructed the assessment model using the literature review and interviews with specialists. In order to determine the suitable dimensions and criteria for each topic, this research interviewed experts to determine the suitable dimensions and criteria, based on our literature review. This research then summarized and constructed an evaluation model with the 4 dimensions and 12 criteria that were most suitable. In the sections that follow, this paper presents the experts’ information, and the interview themes that provided the basic information. We then summarize the experts’ main opinions about all themes, and classify these opinions into four categories that were adopted as the structural framework for the subsequent questionnaire (as

Appendix B). In addition to replying to the questionnaire for constructing this evaluation and selection model, the experts also provided their professional knowledge and experience. We interviewed these experts in their offices rather than off-site, in Taichung City and Changhua City in Taiwan (see

Table 1) [

77].

We used the DEMATEL information analysis method to effectively integrate the knowledge of the experts. DEMATEL helped us to develop a strategy by directly comparing the interrelationships of the key factors in the problem. The relations and the strength of influence among the key factors were obtained from the complex problems. DEMATEL turned the relations among the criteria into a clear structural model and dealt with a series of interrelations among the criteria. This paper discusses the key wealth management bank selection factors. However, given the high complexity and interrelations among the numerous factors, due to limited resources we allocated resources to the most critical key factors. All of the above tasks were compatible with DEMATEL’s characteristics.

4. Fuzzy Decision-Making Trial and Evaluation Laboratory (Fuzzy DEMATEL) Method

The multi-criteria decision-making method (MCDM) includes several techniques that allow the rating of various criteria, and then ranking them based on the opinions of industry experts [

78]. The MCDM method can significantly reduce the cost and time to create an appropriate framework for problem solving. To solve the managerial issue, the study applied the DEMATEL method [

79]. This method helps in gathering group knowledge to form a structural model, and in visualizing the casual relationship between sub-systems through a casual diagram. The judgment of decision-makers is often given as crisp (numerical) values. However, crisp values cannot adequately reflect vagueness in the real world. Thus, this study combined fuzzy logic and DEMATEL to address this issue.

This paper proposes a novel hybrid method to cope with the problem of various interdependence and feedback dimensions in wealth management bank selection. The proposed hybrid method is expected to provide a better understanding of the interrelationship between the evaluation and selection dimensions, and to clarify the complexly-interacting wealth management bank selection criteria, in order to enhance decision-making quality.

In reality, humans’ subjective cognition of abstract things is often vague and unquantifiable. This often distorts the true cognition of the respondent, even when using quantitative scales. The contribution of fuzzy logic theory is used in mathematical structure to express qualitative and quantitative data, to provide a realistic judgment [

80]; this enables decision-makers to define problems clearly and compare the data. Fuzzy theory means that an evaluation involves not just “yes” and “no,” but a concept of degree between “yes” and “no” [

81]. The linguistic variable of fuzzy theory was used as an experts’ scoring scale, to address the inconsistency of subjective cognition and draw the question answers closer to reality. Then, by using fuzzy numbers (FNs) represented by different linguistic variables, respondents chose the most appropriate meaning [

82,

83]. Next, through the defuzzification process, we transformed FNs into numerical values, and decision-making. Thus, we combined the traditional multi-attribute decision-making (MADM) method and fuzzy theory to solve the problem more appropriately [

84]. The structure of the proposed model is shown in

Figure 2.

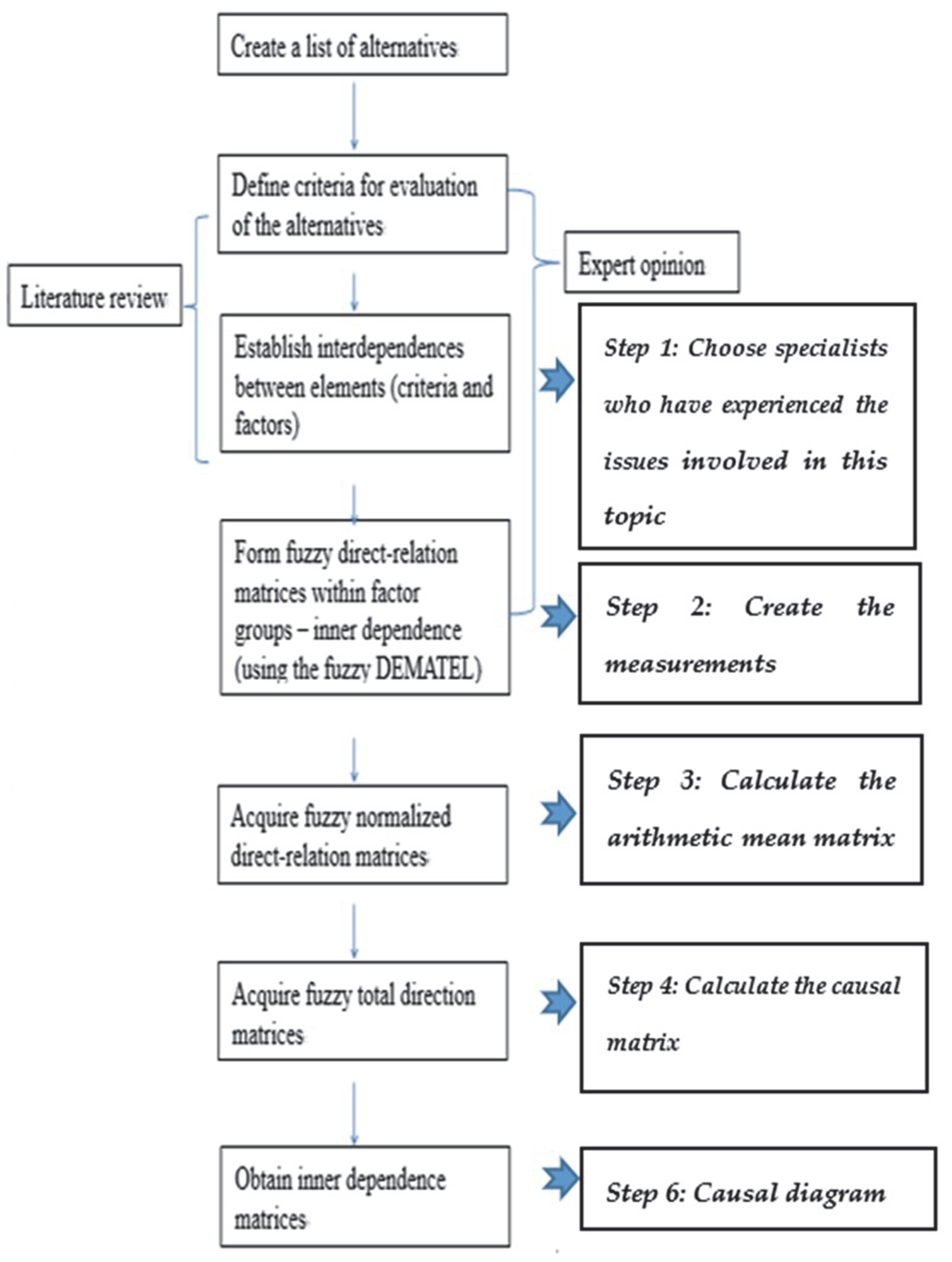

We obtained four dimensions and twelve criteria suitable for evaluating a wealth management bank [

85,

86]. The DEMATEL analysis steps were based on the research of Chou et al. [

87] and Chiang and Birtch [

86], among others. The analysis process was divided into six steps:

- (1)

Define the quality factor characteristics and establish an evaluation scale:

The evaluation scale for causal relations and a pairwise comparison of the quality factors was constructed by referring to the scale designed by Yue et al. [

88] and Büyüközkan and Göçer [

84], and adopting 0, 1, 2, 3, and 4 as the five levels of measurement;

- (2)

Obtain interdependent data for all factors using the expert opinion method:

The pairwise comparisons between any two factors are denoted by

and are given an integer score of 0–4, representing “No influence (0)”, “Low influence (1)”, “Medium influence (2)”, “High influence (3)”, and “Very high influence (4)”, respectively [

82,

83]. The matrix,

, is called the initial direct-relation matrix of expert,

;

- (3)

Calculate the arithmetic mean matrix:

Assuming that the number of factors is

, and the value is from

professionals who judge the factors based on the 0, 1, 2, 3, 4 five-level evaluation scale,

and

(

i = 1, 2, 3, …,

n;

j = 1, 2, 3, …,

n) represent the influence degree of factor

to the variable factor. All

from

experts are then added together, and averaged. The calculation formula to calculate the

arithmetic mean matrix [

89] is given below;

- (4)

Calculate direct/indirect matrix:

The direct/indirect relation matrix and the total-relation matrix illustrate the interrelated impact on each factor; the formula is as below. The normalized direct/relation matrix can be obtained as

[

80]:

- (5)

Utilize the direct/indirect matrix:

Let

be the quality of the given y factor for the direct/indirect matrix,

, and

i,

j = 1, 2, …,

n [

90]. Add the columns and the rows of the direct/indirect matrix,

; the formula is given below. It includes the direct and the indirect impact, which is the degree of the direct or the indirect impact on the other factors. Once the normalized direct-relation

is obtained, the total-relation matrix

can be calculated; it should be ensured that the convergence of

. The total-relation matrix is shown as Equations (2) and (3) [

81]:

- (6)

Causal diagram:

The causal diagram is depicted in two-dimensional graphics, where the total

is the horizontal axis, and the difference

is the vertical axis. This graphic can simplify the complex causal relation into an easily understandable visual structure and, therefore, allows the simple solution of the problems. When

is positive and located above the x axis, the quality factor, m, belongs to the type of cause, but if

is negative and located below the x axis, the quality factor belongs to the type of result [

81].

This paper identified and analyzed the critical factors in wealth management bank selection. A DEMATEL method was applied to analyze and classify these factors to help decision-makers explore the causal relationships among the identified factors. DEMATEL designs and arranges the structural model of a system with expert knowledge and is a rigorous tool to describe the structures of complex relations. This method can determine the interactions between factors according to their specific characteristics and transform the causality of the factors into a systematic structural model. An empirical study is presented below, to illustrate how wealth management bank selection criteria were applied to enhance their advantage.

5. Empirical Study

Maintaining financial health during this situation can be critically important. With a solid handle on finances, we will be better prepared for adverse events in the coming weeks and months. Following the case scenario, an evaluation model was developed for constructing a wealth management bank selection decision hierarchy. A typical hierarchy consists of at least three levels: the goal and the evaluation criteria. The empirical material for the study was collected in the fall and winter of 2021 with a questionnaire, which was followed by expert interviews.

5.1. Analysis of Direct and Indirect Impact of Main Aspects on Wealth Management Bank Evaluation

The main aspect was designed to identify the impact and the interrelations between the four aspects of wealth management bank image perspective, customer service perspective, business process and product perspective, and managers’ learning and growth perspective university technology transfer success. As there were four dimensions, the twenty 4 × 4 matrices are described in

Appendix A:

Step 1: Calculate the arithmetic mean matrix

We produced the preliminary arithmetic mean matrix.

Step 2: Normalize the arithmetic mean matrix.

We continually normalized the arithmetic mean matrix.

Step 3: Utilize the causal matrix.

Utilizing the causal matrix,

was calculated.

Step 4: Causal diagram.

We then produced the causal diagram by mapping a dataset of .

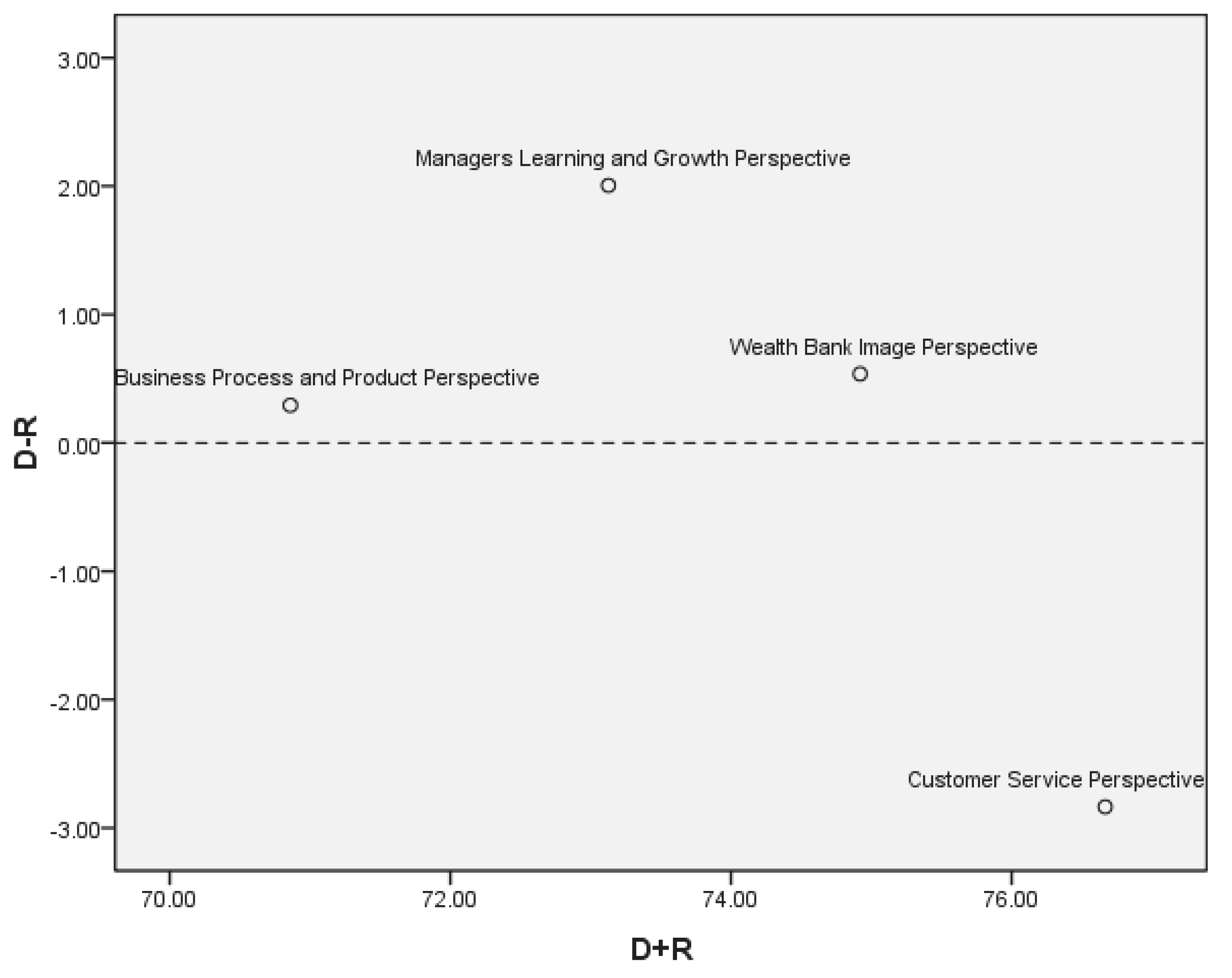

Table 2 explains the causal effects of four first-tier dimensions. The diagraph of these four dimensions is shown in

Figure 3. The wealth management bank image perspective, business process and product perspective, and managers’ learning and growth perspective were the key aspects, whereas customer service perspective was the net receiver. From

Figure 3, it appeared that managers’ learning and growth perspective was the most critical dimension. Moreover, the customer service perspective was affected by itself, as well as by wealth bank image perspective, business process and product perspective, and managers’ learning and growth perspective.

5.2. Analysis of Direct and Indirect Impact of Sub-Aspects of Wealth Management Bank Image Perspective on Wealth Management Bank Evaluation

From the wealth management bank image perspective, we will discuss the impact and interrelation between the three factors “Reputation,” “Market Share,” and “Degree of Internationalization,” on wealth management bank evaluation.

Step 1: Generating the decision-makers assessments matrix of wealth management bank image perspective.

To measure the relationships between the factors of wealth management bank image perspective, the experts were asked to make pairwise comparison sets, which were then obtained for the first-tier dimension of wealth management bank image Perspective,

, as follows:

Step 2: Normalizing the assessments matrix direct-relation matrix of wealth management bank image perspective.

We continually calculated the normalized direct-relation matrix for

:

Step 3: Calculate the causal matrix of wealth management bank image perspective.

Once the normalized direct-relation

was obtained, the total-relation matrix

could be calculated:

5.3. Analysis of Direct and Indirect Impact of Sub-Aspects of Customer Service Perspective on Wealth Management Bank Evaluation

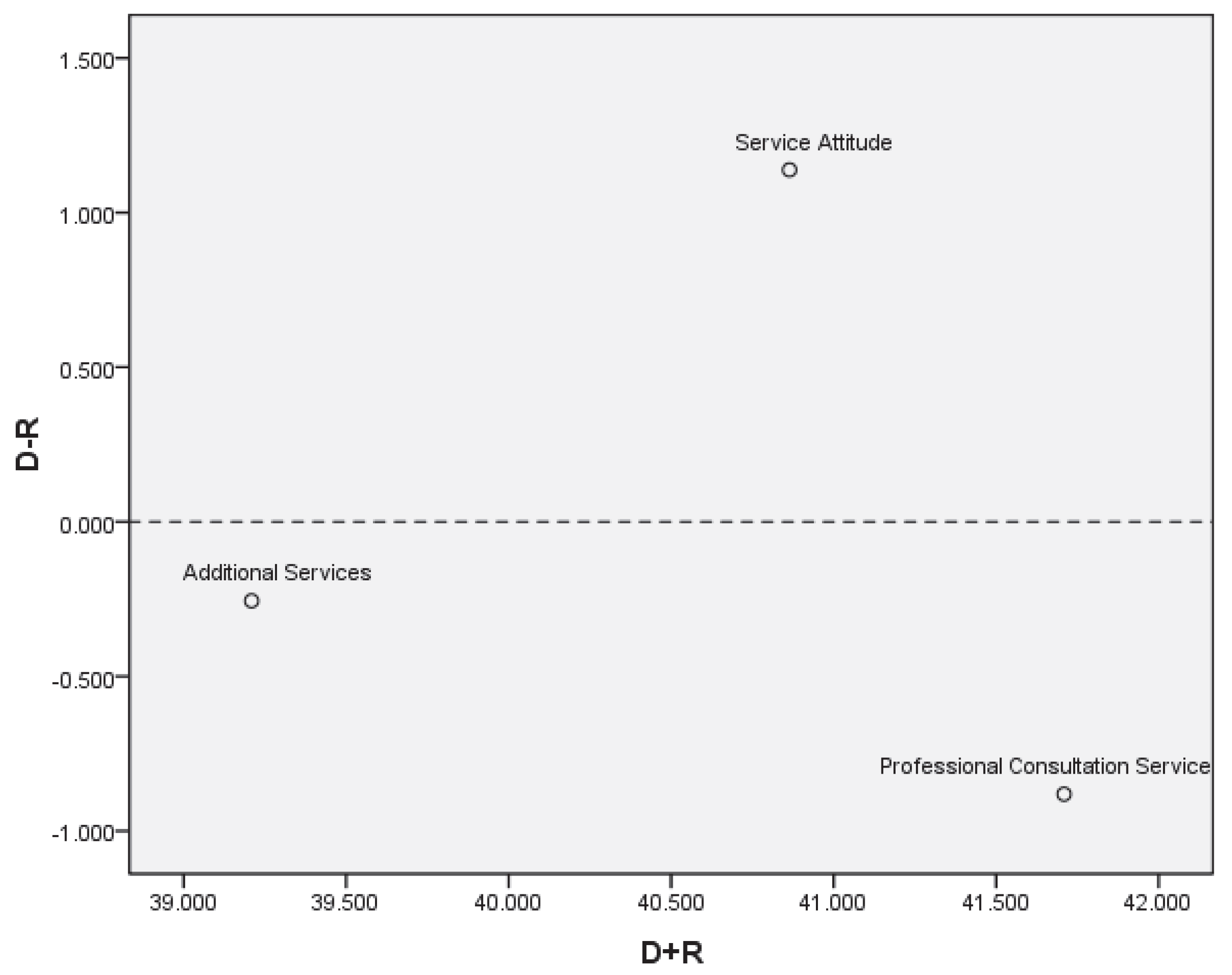

From the customer service perspective, we will discuss the impact and interrelation between the three factors “Service Attitude,” “Professional Consultation Service,” and “Additional Services,” on wealth management bank evaluation.

Step 1: Generate the decision-makers’ assessments matrix of customer service perspective.

To measure the relationships between the factors of customer service perspective, the experts were asked to make pairwise comparison sets, which were then obtained for the first-tier dimension of customer service perspective,

, as follows:

Step 2: Normalize the assessments matrix direct-relation matrix of customer service perspective.

We continually calculated the normalized direct-relation matrix for

:

Step 3: Calculate the causal matrix of customer service perspective.

Once the normalized direct-relation

was obtained, the total-relation matrix

could be calculated:

5.4. Analysis of Direct and Indirect Impact of Sub-Aspects of Business Process and Product Perspective on Wealth Management Bank Evaluation

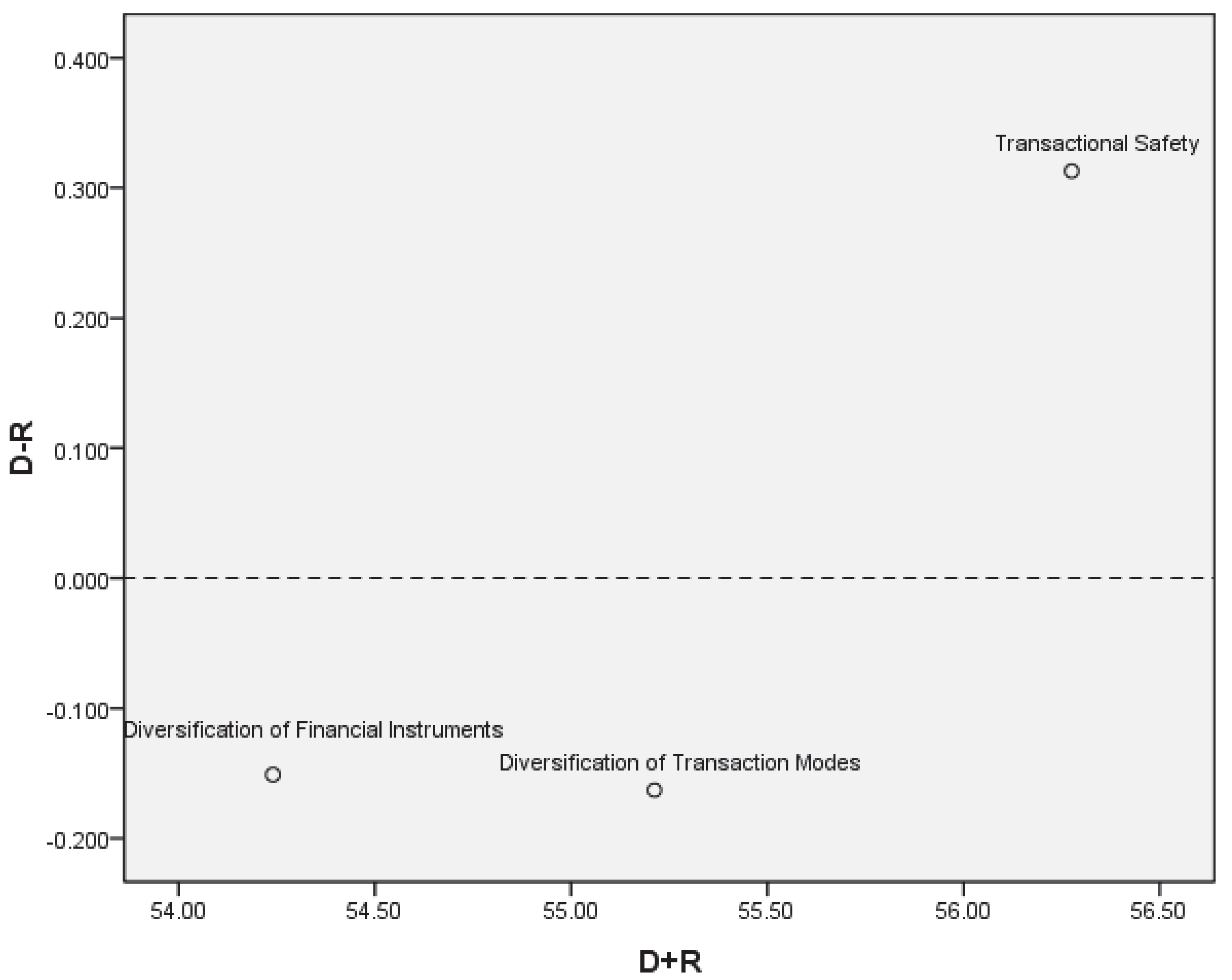

From the business process and product perspective, we will discuss the impact and interrelation between the three factors “Diversification of Financial Instruments”, “Transactional Safety”, and “Diversification of Transaction Modes”, on wealth management bank evaluation.

Step 1: Generate the decision-makers’ assessments matrix of business process and product perspective

To measure the relationships between the factors of business process and product perspective, the experts were asked to make pairwise comparison sets, which were then obtained for the first-tier dimension of business process and product perspective,

, as follows:

Step 2: Normalize the assessments matrix direct-relation matrix of business process and product perspective.

We continually calculated the normalized direct-relation matrix for

:

Step 3: Calculate the causal matrix of business process and product perspective.

Once the normalized direct-relation

was obtained, the total-relation matrix

could be calculated:

5.5. Analysis of Direct and Indirect Impact of Sub-Aspects of Managers’ Learning and Growth Perspective on Wealth Management Bank Evaluation

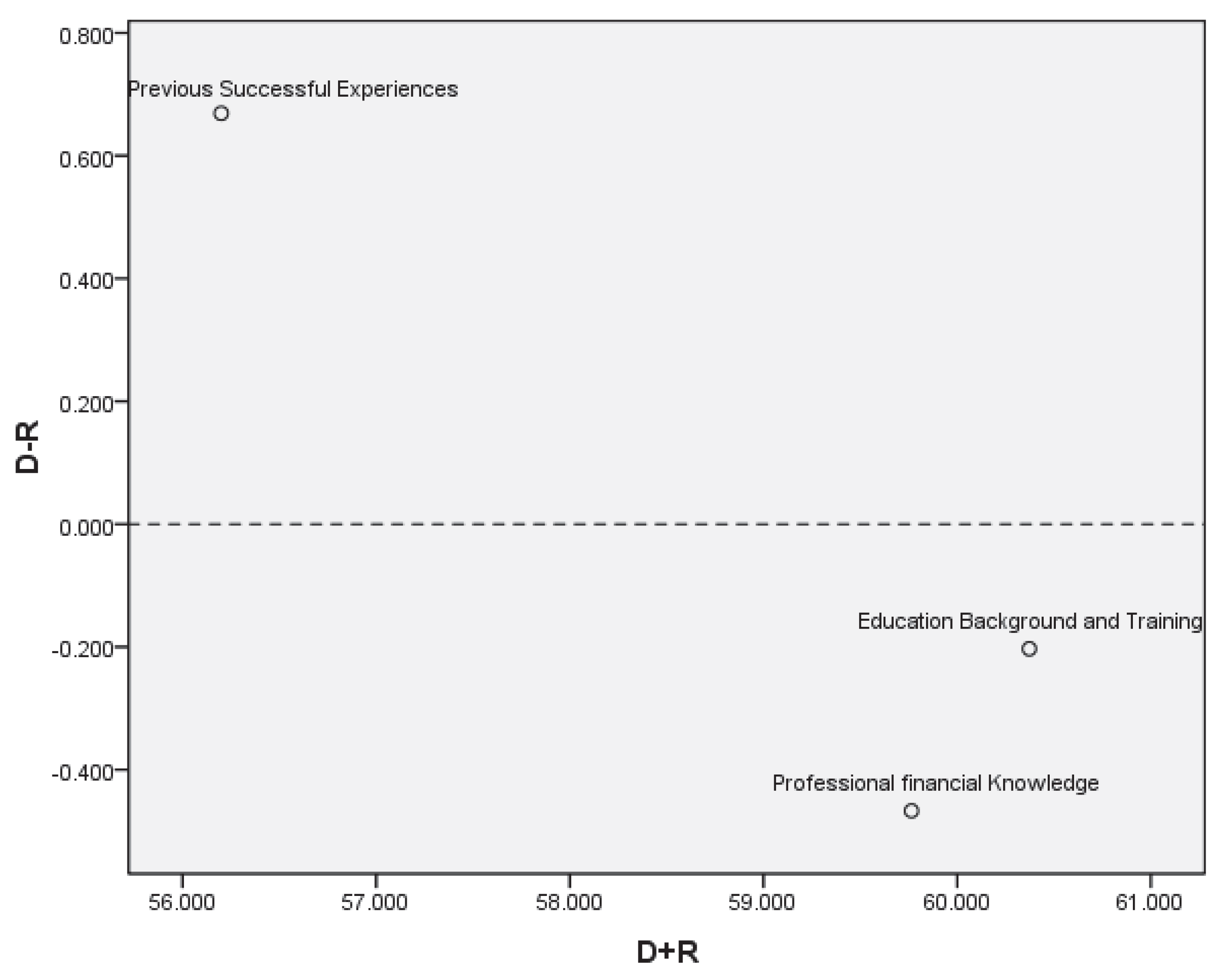

From the managers’ learning and growth perspective, we will discuss the impact and interrelation between the three factors “Professional financial Knowledge,” “Educational Background and Training,” and “Previous Successful Experiences,” on wealth management bank evaluation.

Step 1: Generate the decision-makers’ assessments matrix of managers’ learning and growth perspective.

To measure the relationships between the factors of managers’ learning and growth perspective, the experts were asked to make pairwise comparison sets, which were then obtained for the first-tier dimension of managers’ learning and growth,

, as follows:

Step 2: Normalize the assessments matrix direct-relation matrix of managers’ learning and growth perspective.

We continually calculated the normalized direct-relation matrix for

:

Step 3: Calculate the causal matrix of managers’ learning and growth perspective.

Once the normalized direct-relation

was obtained, the total-relation matrix

could be calculated:

5.6. Summary of the Causal Effects of the Criteria under Four Different Dimensions

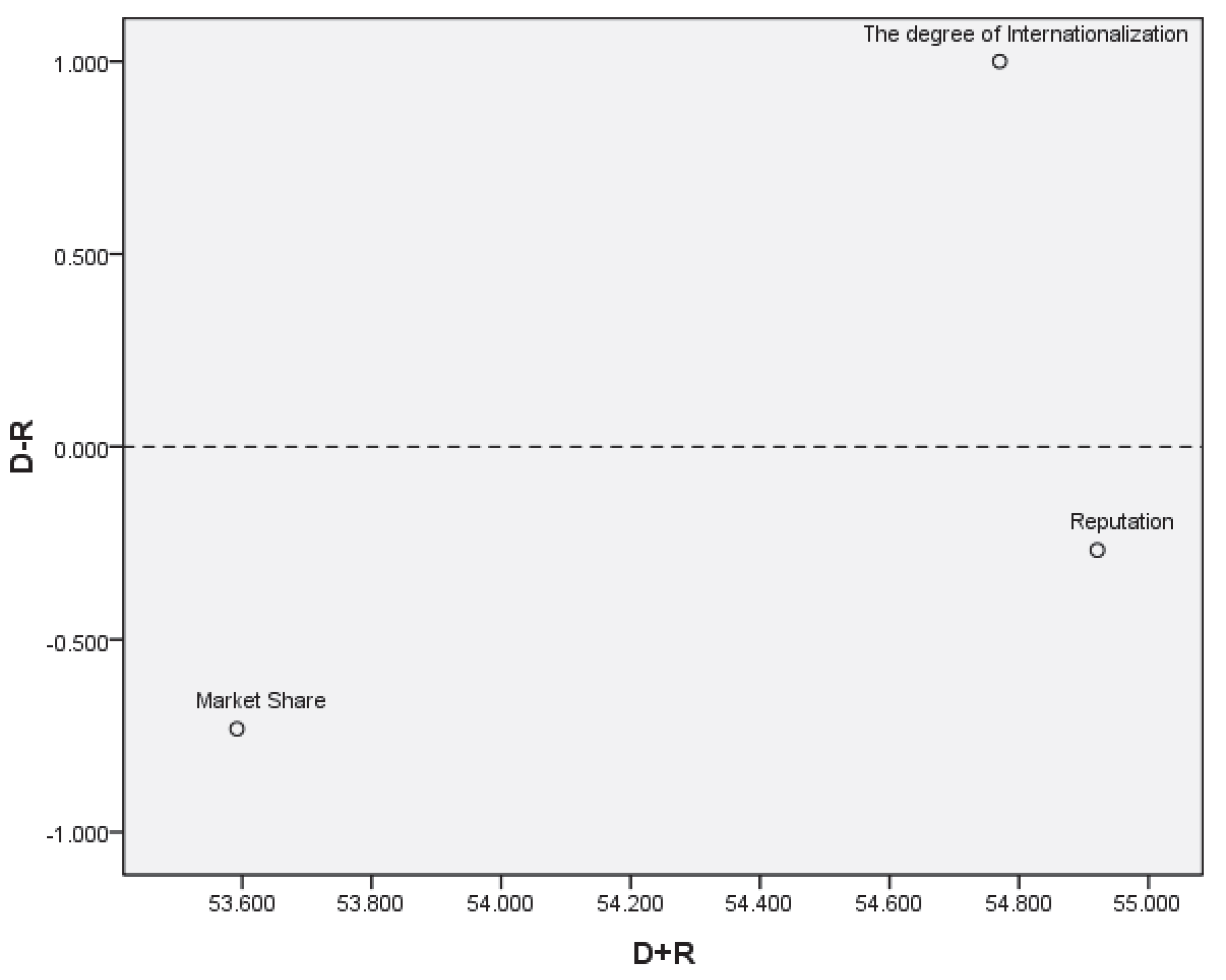

This paper summarizes causal effects of the criteria under four different dimensions, as shown in

Table 3. With respect to the wealth management bank image aspect, we will discuss the impact and interrelation in

Figure 4. The causal relationships among the four second-tier criteria of customer service perspective are shown in

Figure 4. The causal relationships among the three second-tier business process and product perspective criteria are shown in

Figure 5.

Figure 6 summarizes the causal relationships among the four second-tier managers’ learning and growth perspective criteria.

The data indicated that from the organizational culture aspect, degree of internationalization was the key factor for solving the core problems, which was the first factor that had to be considered. Moreover, reputation and market share were affected by degree of internationalization.

Figure 5 illustrates that service attitude was the net cause, whereas professional consultation service and additional services were the net receivers. We concluded that from the organizational structure and system aspect, “Service Attitude” was the key factor in solving the core problems, which was the first factor to be considered. Moreover, professional consultation service and additional services were affected by service attitude.

Figure 6 shows that transactional safety was the net cause, whereas diversification of financial instruments and diversification of transaction modes were the net receivers. It appeared that transactional safety was the most critical criterion. Moreover, diversification of financial instruments and diversification of transaction modes were affected by transactional safety.

Figure 7 shows that previous successful experiences was the net cause, whereas professional financial knowledge and educational background and training were the net receivers. This indicates that previous successful experiences was the most critical criterion. Moreover, professional financial knowledge and educational background and training were affected by previous successful experiences.

In this experimental study, we attempted to identify the major components of wealth management banks. Thus, we utilized wealth management banks as our case study. On the premise of the observational findings, we drew the following conclusions, with a few administrative implications. The experts believed that degree of internationalization was the strongest factor in wealth management bank choice, from the wealth management bank image perspective (D1). In terms of the customer service perspective (D2), we found that the service attitude was the foremost basic determinant. The specialists also demonstrated that transactional safety was a determinative component within the business process and product perspective (D3), and previous successful experience was a decisive factor within the managers’ learning and growth perspective (D4). The following section will illustrate the proposed crossover strategy, which provides insights and proposals for assessing and selecting a wealth management bank.

6. Conclusions and Remarks

The coronavirus outbreak and reports of how it will impact the economy continue to dominate the news. A key concern for many people is how to manage their finances amidst this global pandemic, and customers need to ensure that they have a sound financial plan in place. Wealth management bank selection is composed of many interacting elements, which were examined in this study by means of expert interviews.

The results indicated that the managers’ learning and growth perspective was the most influential factor. Thus, we concluded that financial professionals cannot just be numerate; they must also be able to communicate their knowledge with effective speaking, writing, and presentation skills [

91]. The people skills needed to succeed as a financial professional include understanding different personality types, listening, asking the right questions, resolving conflicts, educating others, and counseling clients. Managing relationships is a key competence for dealing with subordinates, co-workers, bosses, or people outside the company. If clients are to trust wealth managers, they must feel that these managers respect them. Investors will then want to help their wealth managers succeed, whether by speaking highly of them, promoting them, or signing them up as clients. In turn, financial professionals need the ability to market their professional skills and knowledge to prospects in their niche markets. While doing so, it is imperative for clients to have a complete understanding of both their own personal strengths, and those of the wealth management bank professional.

In the real situation of a family financial planning problem, the specific list of criteria used to evaluate family financial planning during formation varied based on the nature and context of the particular problem. Wealth managers will need to efficiently and effectively schedule their time, manage budgets, meet deadlines, and obtain what they need from other people on time, to complete the project successfully. Wealth management professionals will encounter problems in any job, and should be able to solve them; moreover, they must look beyond their own personal responsibilities. Regardless of where managers work, they need to be proficient with computer hardware and software, and able to quickly adopt new programs related to their job. A competitive personality, passion for work, and the stamina to work long hours, exceed expectations, and outperform co-workers and competitors, are crucial to success in finance. This helps the financial specialists overcome obstacles and obtain a large amount of data from various powerful components, utilizing expert information. These findings will support future research, as a useful reference for analysts to build family financial planning strategy models.

Wealth managers should communicate not only how much they know, but also how much they care, because “the clients’ most valuable asset and their biggest daily concern is not their monetary wealth, but their family.” Clients want to know that professionals can help them manage their money, to best provide for their family’s long-term needs [

92].

Diversification is a technique that reduces risk by allocating investments among various financial instruments, industries, and other categories. The aim is to maximize return by investing in different areas that would each react differently to the same event. Most investment professionals agree that although this does not guarantee against incurring loss, diversification is the most important component of achieving long-range financial goals while minimizing risk [

93].

Security is probably the most significant concern for both the shopper and the retailer during an online transaction. In reality, an online transaction is probably more secure than a card transaction in a shop or conducted over the telephone or by fax, as the information transmitted online is highly encrypted using complicated logarithm combinations. The transfer of the purchase details from the retailer’s site to the wealth management bank is conducted using an encrypted digitally signed protocol.

Ultimately, investors select a wealth management bank on the basis of the professionals’ work experience because they expect experienced financial managers to perform better. Prior experience is often used by employers as an expedient proxy for the knowledge and skill that contributes to performance. Prior work experience can also lead to habits, routines, and other cognitions and behaviors that may, or may not, be useful for performance when applied in a different context. Work experience may improve performance, but only indirectly via relevant knowledge and skill, because prior work experience provides the opportunity for individuals to acquire relevant knowledge and skill that can, in turn, enhance job performance. Managers can effectively manage in a cost-saving manner and thereby increase the competitive advantage of the wealth management bank. Using expert knowledge will help investors to reduce the interference caused by too much information among numerous influential factors.

As with any empirical research, this study has limitations. One was that the empirical data were collected in only one industry. Different industries have notable differences, and the research findings may, therefore, vary from one country to another. Furthermore, various countries have striking contrasts in terms of the utilization of versatile installments and administrations, and of mobile payments and services. In addition, the methodology of this study, namely, the fuzzy DEMATEL, also presents limitations in terms of the small sample size. Hence, future research can be conducted to test the adoption factors presented in this study using different methods and larger samples.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}