Modelling Dependency Structures of Carbon Trading Markets between China and European Union: From Carbon Pilot to COVID-19 Pandemic

Abstract

1. Introduction

2. Methods

2.1. GARCH Model

2.2. Copula Model

2.2.1. Basic Copula Theory

2.2.2. Copula Families

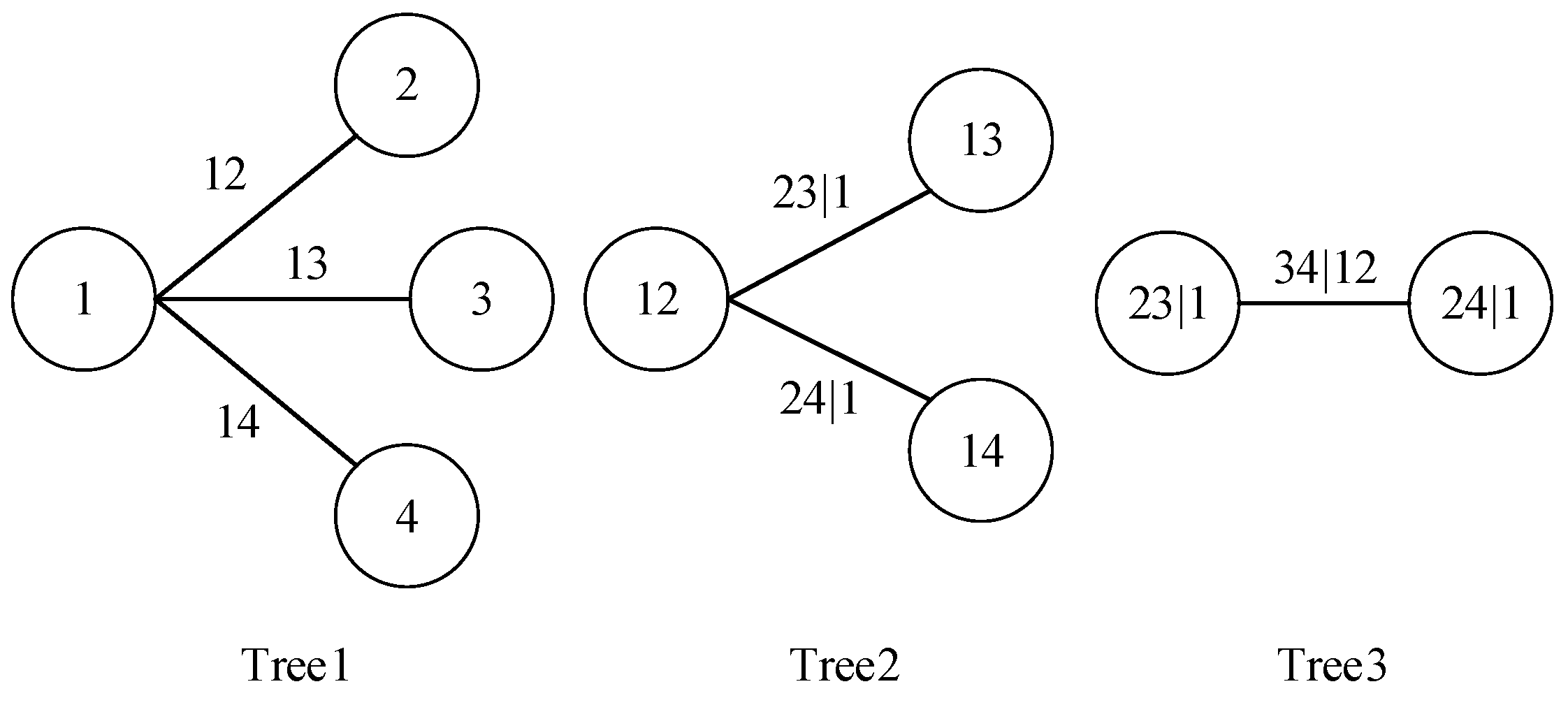

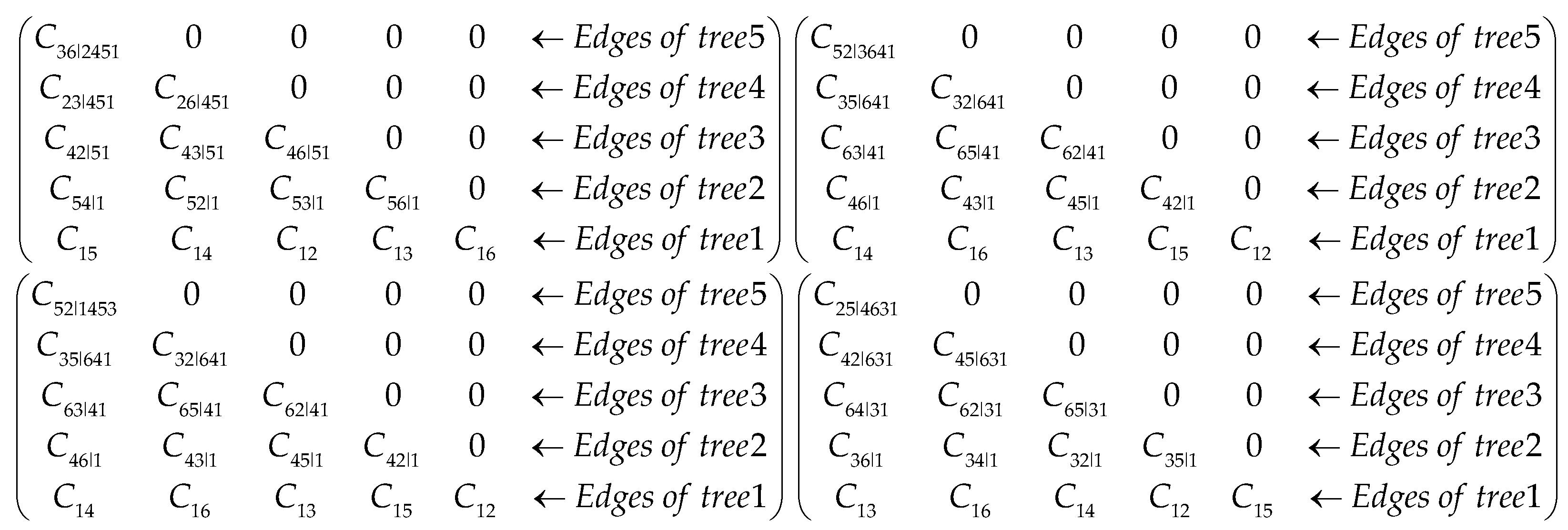

2.2.3. Canonical Vine (C-Vine) Copulas

2.2.4. Non-Linear Correlation and Tail Correlation Metrics

3. Empirical Models and Data

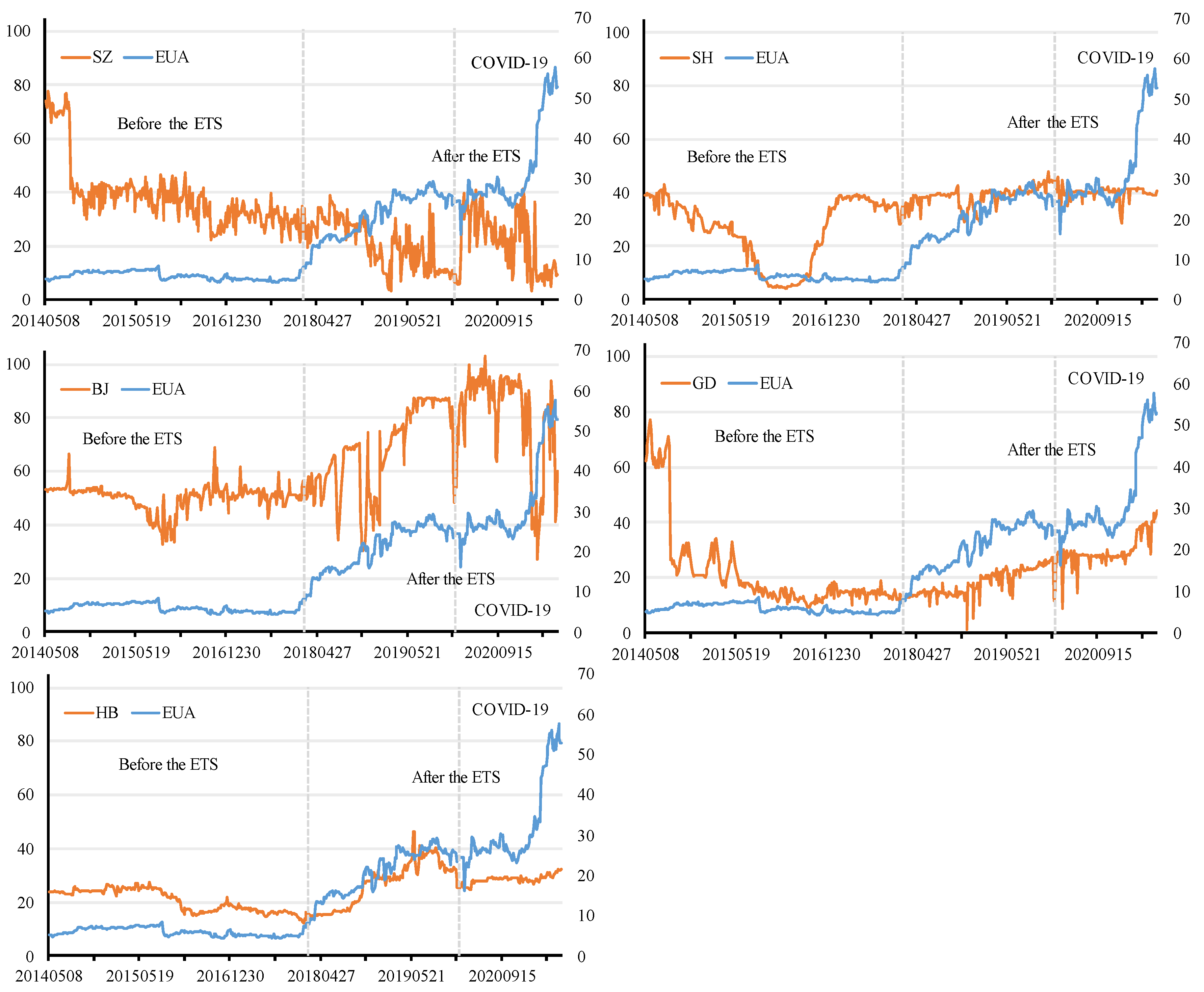

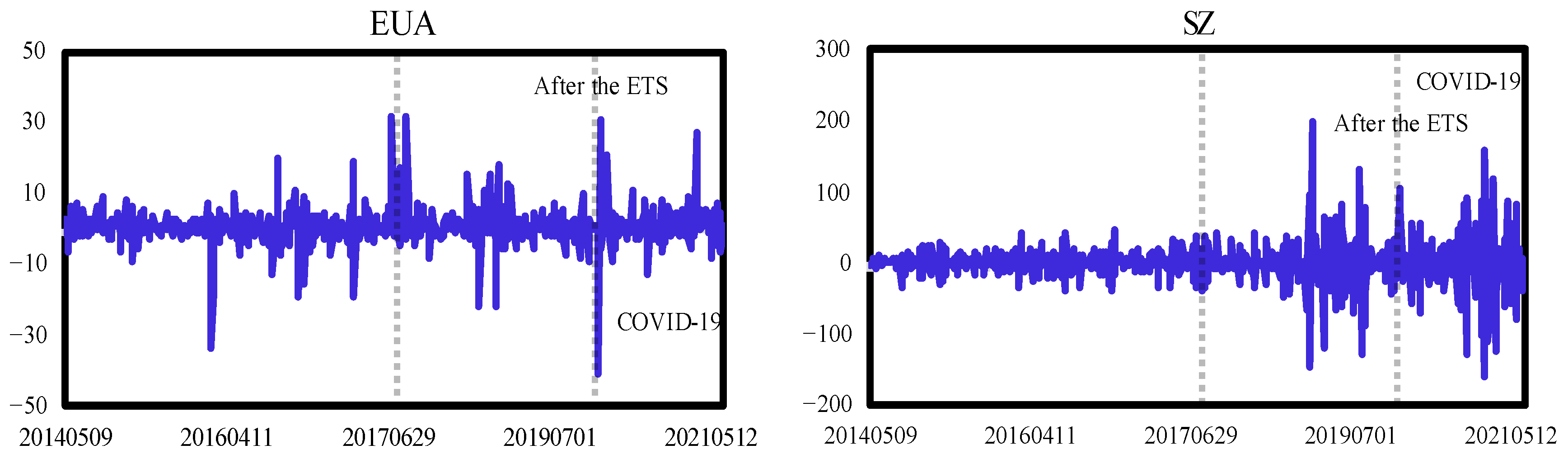

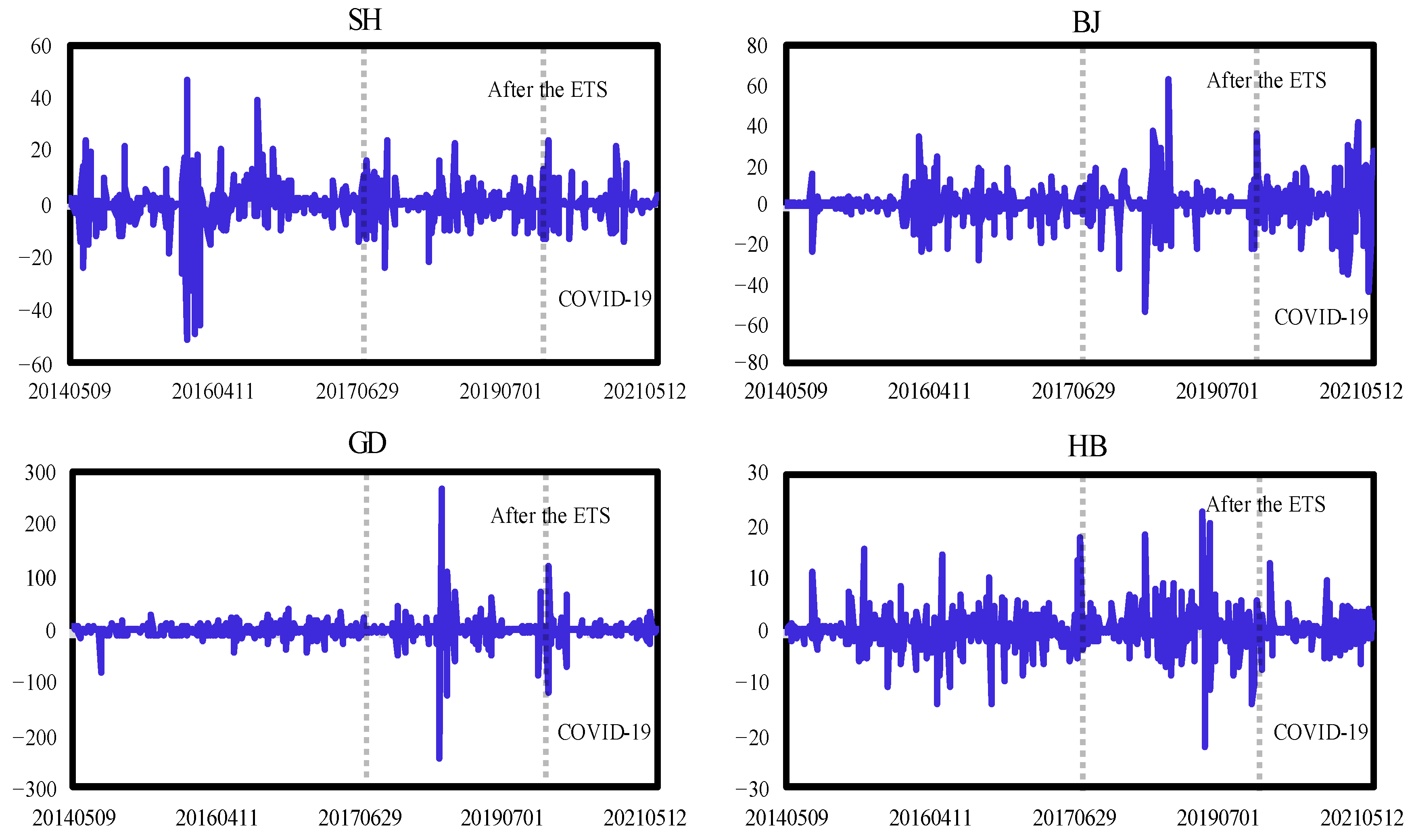

3.1. Data Description

3.2. Statistical Characteristics of the Carbon Price Return Series

3.3. Estimation Results of the Marginal Distribution

3.4. Estimation Results of C-Vine-Copula

3.4.1. Analysis of the Dependency between the Carbon Markets before and after the Launch of National ETS

3.4.2. Analysis of Dependencies between Carbon Markets before and after COVID-19

4. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Paris | Copula | Parameter 1 (SE) | Parameter 2 (SE) | Tau | Tail Dep | |

|---|---|---|---|---|---|---|

| Before the ETS | ||||||

| Tree 1 | EUA-HB | t | 0.01 (0.07) | 5.46 *** (1.99) | 0.00 | 0.04 |

| EUA-SH | t | 0.03 (0.06) | 5.09 *** (1.60) | 0.02 | 0.05 | |

| EUA-SZ | t | −0.13 ** (0.06) | 11.51 (9.02) | −0.08 | 0.00 | |

| EUA-BJ | N | 0.12 ** (0.06) | - | 0.07 | - | |

| EUA-GD | t | −0.17 *** (0.06) | 9.13 (5.81) | −0.11 | 0.00 | |

| Tree 2 | GD-HB|EUA | t | −0.04 (0.06) | 6.00 *** (2.20) | −0.02 | 0.03 |

| GD-SH|EUA | N | 0.08 (0.05) | - | 0.05 | - | |

| GD-SZ|EUA | C | 0.16 ** (0.07) | - | 0.07 | 0.01 L | |

| GD-BJ|EUA | C | 0.18 ** (0.07) | - | 0.08 | 0.02 L | |

| Tree 3 | BJ-HB|GD, EUA | J | 1.07 *** (0.05) | - | 0.04 | 0.09 U |

| BJ-SH|GD, EUA | BB7 | 1.00 *** (0.06) | 0.11 * (0.06) | 0.05 | 0.00 | |

| BJ-SZ|GD, EUA | N | −0.07 (0.06) | - | −0.04 | - | |

| Tree 4 | SZ-HB|BJ, GD, EUA | C | 0.13 ** (0.06) | - | 0.06 | 0.00 L |

| SZ-SH|BJ, GD, EUA | F | 0.24 (0.35) | - | 0.03 | - | |

| Tree 5 | SH-HB|SZ, BJ, GD, EUA | J | 1.06 *** (0.04) | - | 0.04 | 0.08 U |

| After the ETS | ||||||

| Tree 1 | EUA-HB | t | −0.04 (0.06) | 7.11 *** (2,75) | −0.02 | 0.02 |

| EUA-SH | t | −0.07 (0.06) | 6.41 *** (2.32) | −0.04 | 0.02 | |

| EUA-SZ | t | −0.02 (0.06) | 7.45 ** (3.36) | −0.02 | 0.02 | |

| EUA-BJ | F | −0.29 (0.43) | - | −0.03 | - | |

| EUA-GD | N | 0.04 (0.06) | - | 0.02 | - | |

| Tree 2 | BJ-SZ|EUA | F | 0.07 (0.51) | - | 0.01 | - |

| BJ-GD|EUA | t | −0.09 (0.15) | 5.11 ** (2.56) | −0.05 | 0.04 | |

| BJ-SH|EUA | C | 0.18 ** (0.07) | - | 0.08 | 0.02 L | |

| BJ-HB|EUA | N | 0.05 (0.09) | - | 0.03 | - | |

| Tree 3 | HB-SZ|BJ, EUA | F | −0.40 (0.08) | - | −0.04 | - |

| HB-GD|BJ, EUA | N | −0.05 (0.07) | - | −0.03 | - | |

| HB-SH|BJ, EUA | F | −0.78 * (0.42) | - | −0.09 | - | |

| Tree 4 | SH-SZ|HB, BJ, EUA | N | −0.03 (0.06) | - | −0.02 | - |

| SH-GD|HB, BJ, EUA | BB7 | 1.18 *** (0.12) | 0.02 (0.05) | 0.10 | 0.20 U | |

| Tree 5 | GD-SZ|SH, HB, BJ, EUA | C | 0.06 (0.05) | - | 0.03 | 0.00 L |

| Paris | Copula | Parameter 1 (SD) | Parameter 2 (SD) | Tau | Tail Dep | |

|---|---|---|---|---|---|---|

| Before COVID-19 | ||||||

| Tree 1 | EUA-SZ | C | 0.04 (0.07) | - | 0.02 | 0.00 L |

| EUA-GD | C | 0.07 (0.08) | - | 0.04 | 0.00 L | |

| EUA-SH | t | 0.05 (0.09) | 4.00 *** (1.27) | 0.03 | 0.09 | |

| EUA-HB | t | −0.09 (0.08) | 4.54 *** (1.68) | −0.05 | 0.05 | |

| EUA-BJ | G | 1.01 *** (0.06) | - | 0.01 | 0.01 U | |

| Tree 2 | BJ-SZ|EUA | F | −0.23 (0.66) | - | −0.03 | - |

| BJ-GD|EUA | t | 0.05 (0.02) | 4.51 * (2.39) | 0.03 | 0.07 | |

| BJ-SH|EUA | C | 0.25 ** (0.01) | - | 0.11 | 0.06 L | |

| BJ-HB|EUA | F | 0.64 (0.62) | - | 0.07 | - | |

| Tree 3 | HB-SZ|BJ, EUA | J | 1.03 *** (0.06) | - | 0.02 | 0.04 U |

| HB-GD|BJ, EUA | C | 0.00 (0.08) | - | 0.00 | - | |

| HB-SH|BJ, EUA | N | −0.12 (0.08) | - | −0.08 | - | |

| Tree 4 | SH-SZ|HB, BJ, EUA | N | −0.01 (0.08) | - | −0.01 | - |

| SH-GD|HB, BJ, EUA | J | 1.25 *** (0.13) | - | 0.12 | 0.26 U | |

| Tree 5 | GD-SZ|SH, HB, BJ, EUA | C | 0.11 (0.07) | - | 0.05 | 0.00 L |

| After COVID-19 | ||||||

| Tree 1 | EUA-SZ | t | −0.06 (0.10) | 5.46 * (3.06) | −0.04 | 0.03 |

| EUA-GD | C | 0.00 (0.10) | - | 0.00 | - | |

| EUA-SH | t | −0.20 * (0.10) | 10.43 (9.42) | −0.13 | 0.00 | |

| EUA-HB | t | 0.02 (0.11) | - | 0.01 | 0.01 | |

| EUA-BJ | t | −0.09 (0.09) | - | −0.06 | 0.00 | |

| Tree 2 | SH-GD|EUA | t | −0.09 (0.14) | - | −0.06 | 0.00 |

| SH-SZ|EUA | J | 1.26 *** (0.16) | - | 0.13 | 0.27 | |

| SH-BJ|EUA | F | 0.81 (0.66) | - | 0.09 | - | |

| SH-HB|EUA | F | −1.18 (0.75) | - | −0.13 | - | |

| Tree 3 | HB-GD|SH, EUA | G | 1.06 *** (0.10) | - | 0.06 | 0.08 U |

| HB-SZ|SH, EUA | F | −1.27 (0.61) | - | −0.14 | - | |

| HB-BJ|SH, EUA | F | −0.21 (0.63) | - | −0.02 | - | |

| Tree 4 | BJ-GD|HB, SH, EUA | F | −0.66 (0.64) | - | −0.07 | - |

| BJ-SZ|HB, SH, EUA | t | −0.01 (0.10) | - | −0.01 | 0.00 U | |

| Tree 5 | SZ-GD|BJ, HB, SH, EUA | F | 0.63 (0.63) | - | 0.07 | - |

References

- Rajalingam, M.; Srivastava, A. Rational hybrid analytical model for steel pipe rack quantification in oil & gas industries. Civ. Eng. J. 2020, 6, 649–658. [Google Scholar] [CrossRef]

- Zeng, S.H.; Jia, J.M.; Su, B.; Jiang, C.X.; Zeng, G.W. The volatility spillover effect of the European Union (EU) carbon financial market. J. Clean. Prod. 2021, 282, 124394. [Google Scholar] [CrossRef]

- Lin, B.; Chen, Y. Dynamic linkages and spillover effects between CET market, coal market and stock market of new energy companies: A case of Beijing CET market in China. Energy 2019, 172, 1198–1210. [Google Scholar] [CrossRef]

- Stoerk, T.; Dudek, D.J.; Yang, J. China’s national carbon emissions trading scheme: Lessons from the pilot emission trading schemes, academic literature, and known policy details. Clim. Policy 2019, 19, 472–486. [Google Scholar] [CrossRef]

- Wen, F.; Wu, N.; Gong, X. China’s carbon emissions trading and stock returns. Energy Econ. 2020, 86, 104627. [Google Scholar] [CrossRef]

- Sun, L.M.; Xiang, M.Q.; Shen, Q. A comparative study on the volatility of EU and China’s carbon emission permits trading markets. Phys. A 2020, 560, 125037. [Google Scholar] [CrossRef]

- Benkraiem, R.; Garfatta, R.; Lakhal, F.; Zorgati, I. Financial contagion intensity during the COVID-19 outbreak: A copula approach. Int. Rev. Financ. Anal. 2022, 81, 102136. [Google Scholar] [CrossRef]

- Liu, J.X.; Cheng, Y.N.; Li, X.Q.; Sriboonchitta, S. The role of risk forecast and risk tolerance in portfolio management: A case study of the Chinese financial sector. Axioms 2022, 11, 134. [Google Scholar] [CrossRef]

- Rupani, P.F.; Nilashi, M.; Abumalloh, R.A.; Asadi, S.; Samad, S.; Wang, S. Coronavirus pandemic (COVID-19) and its natural environmental impacts. Int. J. Environ. Sci. Technol. 2020, 17, 4655–4666. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.; Hu, Y.; Lucey, B.; Oxley, L. Aye Corona! The contagion effects of being named Corona during the COVID-19 pandemic. Financ. Res. Lett. 2021, 38, 101591. [Google Scholar] [CrossRef]

- Zhang, Y.; Sun, Y. The dynamic volatility spillover between European carbon trading market and fossil energy market. J. Clean. Prod. 2016, 112, 2654–2663. [Google Scholar] [CrossRef]

- Dhamija, A.K.; Yadav, S.S.; Jain, P.K. Volatility spillover of energy markets into EUA markets under EU ETS: A multi-phase study. Environ. Econ. Policy Stud. 2017, 20, 561–591. [Google Scholar] [CrossRef]

- Wu, Q.; Wang, M.; Tian, L. The market-linkage of the volatility spillover between traditional energy price and carbon price on the realization of carbon value of emission reduction behavior. J. Clean. Prod. 2020, 245, 118682. [Google Scholar] [CrossRef]

- Hanif, W.; Hernandez, J.A.; Mensi, W.; Kang, S.H.; Uddin, G.S.; Yoon, S.M. Nonlinear dependence and connectedness between clean/renewable energy sector equity and European emission allowance prices. Energy Econ. 2021, 101, 105409. [Google Scholar] [CrossRef]

- Chang, K.; Ye, Z.F.; Wang, W.H. Volatility spillover effect and dynamic correlation between regional emissions allowances and fossil energy markets: New evidence from China’s emissions trading scheme pilots. Energy 2019, 185, 1314–1324. [Google Scholar] [CrossRef]

- Reboredo, J.C. Volatility spillovers between the oil market and the European Union carbon emission market. Econ. Model 2014, 36, 229–234. [Google Scholar] [CrossRef]

- Zhu, B.Z.; Huang, L.Q.; Yuan, L.L.; Ye, S.X.; Wang, P. Exploring the risk spillover effects between carbon market and electricity market: A bidimensional empirical mode decomposition based conditional value at risk approach. Int. Rev. Econ. Financ. 2020, 67, 163–175. [Google Scholar] [CrossRef]

- Xu, L.; Wu, C.Y.; Qin, Q.D.; Lin, X.Y. Spillover effects and nonlinear correlations between carbon emissions and stock markets: An empirical analysis of China’s carbon-intensive industries. Energy Econ. 2022, 111, 106071. [Google Scholar] [CrossRef]

- Oestreich, A.M.; Tsiakas, I. Carbon emissions and stock returns: Evidence from the EU emissions trading scheme. J. Bank. Financ. 2015, 58, 294–308. [Google Scholar] [CrossRef]

- Hu, G.H.; Wu, H.Y.; Qiu, J.X. Dependence structure of carbon emission markets: Regular Vine approach. Chin. J. Popul. Resour. 2015, 25, 44–52. [Google Scholar]

- Arouri, M.E.H.; Jawadi, F.; Nguyen, D.K. Nonlinearities in carbon spot-futures price relationships during Phase II of the EU ETS. Econ. Model. 2012, 29, 884–892. [Google Scholar] [CrossRef]

- Zhao, L.L.; Wen, F.H.; Wang, X. Interaction among China carbon emission trading markets: Nonlinear Granger causality and time-varying effect. Energy Econ. 2020, 91, 104901. [Google Scholar] [CrossRef]

- Zhu, B.Z.; Zhou, X.X.; Liu, X.F.; Wang, H.F.; He, K.J.; Wang, P. Exploring the risk spillover effects among China’s pilot carbon markets: A regular vine copula-CoES approach. J. Clean. Prod. 2020, 242, 118455. [Google Scholar] [CrossRef]

- Mai, T.K.; Foley, A.M.; McAleer, M.; Chang, C.L. Impact of COVID-19 on returns-volatility spillovers in national and regional carbon markets in China. Renew. Sustain. Energy Rev. 2022, 169, 112861. [Google Scholar] [CrossRef]

- Fang, S.; Cao, G.X. Modelling extreme risks for carbon emission allowances—Evidence from European and Chinese carbon markets. J. Clean. Prod. 2021, 316, 128023. [Google Scholar] [CrossRef]

- Du, J.Z. Examining the Inter-relationship between RMB Markets. Procedia Comput. Sci. 2018, 139, 313–320. [Google Scholar] [CrossRef]

- Wu, C.C.; Chung, H.; Chang, Y.H. The economic value of co-movement between oil price and exchange rate using copula-based GARCH models. Energy Econ. 2012, 34, 270–282. [Google Scholar] [CrossRef]

- Benlagha, N. Dependence structure between nominal and index-linked bond returns: A bivariate copula and DCC-GARCH approach. Appl. Econ. 2014, 46, 3849–3860. [Google Scholar] [CrossRef]

- Min, A.; Czado, C. Bayesian inference for multivariate copulas using pair-copula constructions. J. Financ. Econom. 2010, 8, 511–546. [Google Scholar] [CrossRef]

- Embrechts, P.; McNeil, A.; Straumann, D. Correlation and Dependence in Risk Management: Properties and Pitfalls. Risk Manag. Value Risk Beyond 2002, 1, 176–223. [Google Scholar]

- So, M.K.; Yeung, C.Y. Vine-copula GARCH model with dynamic conditional dependence. Comput. Stat. Data Anal. 2014, 76, 655–671. [Google Scholar] [CrossRef]

- Bedford, T.; Cooke, R.M. Probability Density Decomposition for Conditionally Dependent Random Variables Modeled by Vines. Ann. Math. Artif. Intel. 2001, 32, 245–268. [Google Scholar] [CrossRef]

- Bedford, T.; Cooke, R.M. Vines: A New Graphical Model for Dependent Random Variables. Ann. Stat. 2002, 30, 1031–1068. [Google Scholar] [CrossRef]

- Brechmann, E.C.; Czado, C. Risk management with high-dimensional vine copulas: An analysis of the Euro Stoxx 50. Statist. Risk. Model 2013, 30, 307–342. [Google Scholar] [CrossRef]

- Song, Q.; Liu, J.X.; Sriboonchitta, S. Risk Measurement of Stock Markets in BRICS, G7, and G20: Vine Copulas versus Factor Copulas. Mathematics 2019, 7, 274. [Google Scholar] [CrossRef]

- Zhang, X.M.; Zhang, T.; Lee, C.C. The path of financial risk spillover in the stock market based on the R-vine-Copula model. Phys. A 2022, 600, 127470. [Google Scholar] [CrossRef]

- Jiang, C.X.; Li, Y.Q.; Xu, Q.F.; Liu, Y.Z. Measuring risk spillovers from multiple developed stock markets to China: A vine-copula-GARCH-MIDAS model. Int. Rev. Econ. Financ. 2021, 75, 386–398. [Google Scholar] [CrossRef]

- Joe, H. Asymptotic efficiency of the two-stage estimation method for copula-based models. J. Multivariate. Anal. 2005, 94, 401–419. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Bentes, S.R. On the stylized facts of precious metals’ volatility: A comparative analysis of pre-and during COVID-19 crisis. Phys. A Stat. Mech. Appl. 2022, 600, 127528. [Google Scholar] [CrossRef]

- Huang, J.J.; Lee, K.J.; Liang, H.M.; Lin, W.F. Estimating value at risk of portfolio by conditional copula-GARCH method. Insur. Math. Econ. 2009, 45, 315–324. [Google Scholar] [CrossRef]

- Sklar, A. Fonctions de Répartition à n Dimensions et Leurs Marges. Publ. Inst. Statist. Univ. Paris. 1959, 8, 229–231. [Google Scholar]

- Embrechts, P.; Lindskog, F.; McNeil, A. Modelling dependence with copulas and applications to risk management. In Handbook of Heavy Tailed Distributions in Finance; Rachev, S., Ed., Elsevier: Amsterdam, The Netherlands, 2003; pp. 25–26. [Google Scholar] [CrossRef]

- Patton, A.J. Modelling asymmetric exchange rate dependence. Int. Econ. Rev. 2006, 47, 527–556. [Google Scholar] [CrossRef]

- Frank, M.J. On the simultaneous associativity of F(x,y) and x+y−F(x,y). Aequ. Math. 1979, 19, 194–226. [Google Scholar] [CrossRef]

- Joe, H. Parametric families of multivariate distributions with given margins. J. Multivar. Anal. 1993, 46, 262–282. [Google Scholar] [CrossRef]

- Gumbel, E.J. Bivariate exponential distributions. J. Am. Stat. Assoc. 1960, 55, 698–707. [Google Scholar] [CrossRef]

- Clayton, D.G. A model for association in bivariate life tables and its application in epidemiological studies of familial tendency in chronic disease incidence. Biometrika 1978, 65, 141–152. [Google Scholar] [CrossRef]

- Ly, L.; Sriboonchitta, S.; Tang, J.C.; Wong, W.K. Exploring dependence structures among European electricity markets: Static and dynamic copula-GARCH and dynamic state-space approaches. Energy Rep. 2022, 8, 3827–3846. [Google Scholar] [CrossRef]

- Sriboonchitta, S.; Nguyen, H.T.; Wiboonpongse, A.; Liu, J.X. Modeling volatility and dependency of agricultural price and production indices of Thailand: Static versus time-varying copulas. Int. J. Approx. Reason. 2013, 54, 793–808. [Google Scholar] [CrossRef]

- Viviana, F. Copula-based measures of dependence structure in assets returns. Phys. A 2008, 387, 3615–3628. [Google Scholar] [CrossRef]

- Akaike, H. Information theory and an extension of the maximum likelihood principle. In Selected Papers of Hirotugu Akaike; Parzen, E., Tanabe, K., Kitagawa, G., Eds.; Springer: New York, NY, USA, 1998; pp. 199–213. [Google Scholar]

- Brechmann, E.C. Truncated and simplified regular vines and their applications. Ph.D. Thesis, Technische Universitaet Muenchen, Munich, Germany, 2010. [Google Scholar]

- Emmanouil, K.N.; Nikos, N. Extreme Value Theory and Mixed Canonical Vine Copulas on Modelling Energy Price Risks; Working Paper; NTNU: Trondheim, Norway, 2012. [Google Scholar]

- Tachibana, M. Relationship between stock and currency markets conditional on the US stock returns: A vine copula approach. J. Multinatl. Financ. Manag. 2018, 46, 75–106. [Google Scholar] [CrossRef]

- Wei, Z.; Kim, S.Y.; Kim, D.Y. Multivariate Skew Normal Copula for non-exchangeable dependence. Procedia Comput. Sci. 2016, 91, 141–150. [Google Scholar] [CrossRef]

- Schweizer, B.; Wolff, E. On nonparametric measures of dependence for random variables. Ann. Stat. 1981, 9, 879–885. [Google Scholar] [CrossRef]

- Qiu, Q.; Guo, S.Q. Analysis of regional trading market risks in carbon finance. Resour. Dev. Market. 2017, 2, 188–193. [Google Scholar]

| Mean | Med | Max | Min | SD | Skew | Kurt | ADF | LB-Q | ARCH-LM | J-B | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Before the ETS (2 April 2014 to 16 December 2017) | |||||||||||

| EUA | 0.16 | 0.00 | 31.61 | −33.44 | 5.06 | −0.44 | 13.76 | −6.44 ** | 11.71 * | 8.83 | 2304.30 *** |

| SZ | −0.27 | −0.24 | 44.60 | −40.48 | 13.64 | 0.03 | 1.12 | −8.71 ** | 54.75 *** | 22.94 * | 15.7630 *** |

| SH | −0.04 | 0.00 | 46.95 | −51.35 | 9.17 | −0.89 | 11.08 | −4.74 ** | 24.76 *** | 71.62 *** | 1527.30 *** |

| BJ | 0.01 | 0.00 | 34.56 | −28.31 | 6.67 | −0.10 | 5.88 | −9.87 ** | 30.49 *** | 84.72 *** | 421.70 *** |

| GD | −0.55 | −0.01 | 39.01 | −77.43 | 11.63 | −0.97 | 7.38 | −7.20 ** | 15.20 ** | 5.03 | 706.95 *** |

| HB | −0.14 | −0.21 | 17.57 | −13.84 | 3.67 | 0.65 | 5.10 | −6.13 ** | 10.05 | 19.56 * | 336.79 *** |

| After the ETS (17 December 2017 to 16 July 2021) | |||||||||||

| EUA | 0.67 | 0.22 | 31.65 | −41.32 | 6.07 | −0.01 | 13.92 | −6.67 ** | 6.95 | 14.53 | 2300.80 *** |

| SZ | −0.46 | −0.17 | 196.35 | −162.06 | 42.74 | 0.07 | 3.60 | −8.35 ** | 55.14 *** | 79.63 *** | 155.73 *** |

| SH | 0.05 | 0.00 | 24.09 | −23.64 | 6.06 | 0.32 | 3.69 | −8.50 ** | 18.85 ** | 64.09 *** | 168.03 *** |

| BJ | 0.04 | 0.35 | 62.99 | −54.39 | 12.07 | 0.05 | 5.16 | −7.65 ** | 6.26 | 39.27 *** | 318.21 *** |

| GD | 0.44 | 0.32 | 265.63 | −244.13 | 30.20 | 0.47 | 37.96 | −11.94 ** | 74.06 *** | 6.00 | 17,078.00 *** |

| HB | 0.26 | 0.07 | 22.68 | −22.35 | 4.27 | 0.47 | 7.72 | −6.54 ** | 16.50 ** | 71.74 *** | 718.68 *** |

| Mean | Med | Max | Min | SD | Skew | Kurt | ADF | LB-Q | ARCH-LM | J-B | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Before COVID-19 (18 December 2017 to 31 December 2019) | |||||||||||

| EUA | 0.65 | 0.21 | 31.65 | −22.10 | 5.40 | 0.87 | 9.40 | −6.04 ** | 5.59 | 7.81 | 667.34 *** |

| SZ | −1.07 | −0.69 | 196.35 | −147.26 | 37.30 | 0.41 | 6.65 | −6.45 ** | 41.43 *** | 63.67 *** | 329.43 *** |

| SH | 0.16 | 0.01 | 23.77 | −23.64 | 6.16 | 0.06 | 3.57 | −5.82 ** | 13.45 ** | 22.32 ** | 94.52 *** |

| BJ | 0.15 | 0.35 | 62.99 | −54.39 | 11.13 | 0.46 | 9.60 | −7.76 ** | 12.94 ** | 14.71 | 679.97 *** |

| GD | 0.45 | 0.25 | 265.63 | −244.13 | 34.95 | 0.48 | 32.75 | −11.54 ** | 43.68 *** | 3.91 | 7802.40 *** |

| HB | 0.31 | 0.13 | 22.68 | −22.35 | 5.04 | 0.36 | 5.71 | −6.07 ** | 11.37 ** | 39.11 *** | 243.18 *** |

| After COVID-19 (1 January 2020 to 16 July 2021) | |||||||||||

| EUA | 0.70 | 0.31 | 30.87 | −41.32 | 7.01 | −0.64 | 14.51 | −4.75 ** | 9.21 * | 5.62 | 1016.10 *** |

| SZ | 0.50 | 2.62 | 157.62 | −162.06 | 50.16 | −0.18 | 1.32 | −8.45 ** | 29.84 *** | 35.32 *** | 9.52 *** |

| SH | −0.11 | −0.02 | 24.09 | −14.72 | 5.92 | 0.77 | 3.83 | −6.46 ** | 7.53 | 49.10 *** | 82.85 *** |

| BJ | −0.14 | 0.35 | 41.36 | −44.64 | 13.44 | −0.31 | 1.31 | −5.07 ** | 5.51 | 30.35 *** | 10.67 *** |

| GD | 0.41 | 0.38 | 122.95 | −118.82 | 20.99 | 0.10 | 19.06 | −10.84 ** | 36.57 *** | 0.17 | 1736.60 *** |

| HB | 0.18 | 0.00 | 12.56 | −7.14 | 2.71 | 0.87 | 4.28 | −6.09 ** | 14.65 ** | 6.07 | 103.81 *** |

| EUA | SZ | SH | BJ | GD | HB | |

|---|---|---|---|---|---|---|

| Before the ETS | ||||||

| 0.136 (1.318) | −0.010 (−0.046) | 0.051 (0.259) | −0.031 (−0.818) | −0.576 ** (−1.987) | −0.1207 (−1.5031) | |

| 0.839 *** (7.788) | 0.117 (1.017) | 0.208 (0.559) | 0.341 *** (4.004) | 0.866 *** (14.541) | 0.3486 * (1.7973) | |

| −0.898 *** (−11.07) | −0.652 *** (−7.273) | −0.263 (−0.720) | −0.754 *** (−14.531) | −0.931 *** (−23.767) | −0.5373 *** (−3.1335) | |

| 2.766 *** (1.561) | 38.327 ** (2.247) | 3.005 (0.701) | 0.726 * (1.907) | 0.624 (0.564) | 2.313 * (1.710) | |

| 0.294 (1.717) | 0.440 ** (2.471) | 0.223 (1.575) | 0.452 *** (5.160) | 0.000 (0.000) | 0.586 *** (3.444) | |

| 0.705 * (6.539) | 0.415 *** (2.929) | 0.776 *** (3.270) | 0.547 *** (7.657) | 0.998 *** (258.868) | 0.4134 *** (3.103) | |

| 2.679 *** (6.614) | 4.660 *** (3.184) | 2.571 *** (6.802) | 3.221 *** (10.192) | 3.008 *** (7.529) | 2.982 *** (7.644) | |

| Log Likelihood | −776.840 | −1094.306 | −910.867 | −788.050 | −1072.289 | −708.530 |

| AIC | 5.481 | 7.701 | 6.419 | 5.560 | 7.548 | 5.004 |

| After the ETS | ||||||

| 0.2927 (1.5831) | −0.3993 (−0.9552) | 0.0504 (0.6447) | 0.2575 (1.6373) | 0.6521 *** (3.9178) | 0.1266 (1.5472) | |

| 0.5309 * (1.7602) | 0.1290 (1.1770) | −0.0290 (−0.1986) | −0.3787 (−0.9173) | −0.1397 (−1.2428) | 0.2444 * (1.7600) | |

| −0.5849 ** (−2.0432) | −0.6901 *** (−7.9853) | −0.2795 ** (−1.9372) | 0.3025 (0.7052) | −0.3655 *** (−2.4946) | −0.4889 *** (−4.3270) | |

| 0.1325 (0.3122) | 67.3125 * (1.7400) | 3.5917 *** (3.3980) | 1.1349 (1.2763) | 40.4564 ** (2.5465) | 1.4791 (1.0746) | |

| 0.0020 (0.1802) | 0.3641 *** (3.5845) | 0.8556 *** (5.0966) | 0.4171 *** (5.4491) | 0.8010 *** (3.7382) | 0.4970 *** (3.6056) | |

| 0.9970 *** (319.4716) | 0.6349 *** (7.7451) | 0.1434 ** (2.1148) | 0.5819 *** (7.9922) | 0.1980* (1.4737) | 0.5020 *** (3.2861) | |

| 2.3601 *** (17.4461) | 3.8608 *** (4.9929) | 2.8252 *** (13.2582) | 3.2452 *** (10.8275) | 2.4369 *** (18.6968) | 3.1149 *** (7.9993) | |

| Log Likelihood | −812.3930 | −1342.6590 | −779.2891 | −966.5379 | −1026.1220 | −714.4188 |

| AIC | 5.8528 | 9.6404 | 5.6164 | 6.9538 | 7.3794 | 5.1530 |

| EUA | SZ | SH | BJ | GD | HB | |

|---|---|---|---|---|---|---|

| Before COVID-19 | ||||||

| 0.1044 (0.2339) | −0.4071 (0.5098) | 0.1134 (0.1244) | 0.2981 ** (0.1384) | 0.5883 *** (0.1488) | 0.2532 (0.2162) | |

| −0.8796 *** (0.0763) | 0.0310 (0.2454) | −0.0468 (0.2233) | −0.5355 ** (0.2121) | 0.0797 (0.1140) | −0.7748 *** (0.1943) | |

| 0.9240 *** (0.0554) | −0.5766 ** (0.2310) | −0.3145 (0.2202) | 0.4605 ** (0.2249) | −0.7152 *** (0.1005) | 0.8087 *** (0.1673) | |

| 2.2543 (1.7493) | 71.0614 * (40.2515) | 5.3587 ** (2.5041) | 1.8210 * (1.0958) | 21.6148 (16.2651) | 4.2006 (2.7023) | |

| 0.1069 (0.0842) | 0.4436 *** (0.1578) | 0.7522 *** (0.2234) | 0.5121 *** (0.1355) | 0.4360 *** (0.1532) | 0.573 ** (0.2486) | |

| 0.8388 *** (0.0639) | 0.5554 *** (0.1067) | 0.2468 ** (0.1240) | 0.4869 *** (0.0933) | 0.5630 *** (0.1956) | 0.426 *** (0.1468) | |

| 2.5449 *** (0.3796) | 3.2428 *** (0.5764) | 2.8666 *** (0.3272) | 2.555 *** (0.1716) | 2.4728 *** (0.2043) | 3.2133 *** (0.6917) | |

| Log Likelihood | −477.4436 | −778.2724 | −496.439 | −529.1808 | −645.2967 | −475.2599 |

| AIC | 5.6993 | 9.2385 | 5.9228 | 6.3080 | 7.6741 | 5.6736 |

| After COVID-19 | ||||||

| 0.4248 (0.3238) | −0.3455 (1.4400) | −0.1327 *** (0.0211) | 0.0806 (0.6318) | 0.6640 *** (0.2276) | 0.0595 (0.0723) | |

| 0.3740 (0.4237) | 0.1234 (0.1677) | 0.9633 *** (0.0082) | −0.7511 *** (0.1701) | −0.1990 (0.1438) | 0.0700 (0.1945) | |

| −0.4497 (0.4060) | −0.6754 *** (0.1214) | −1.0000 *** (0.0024) | 0.8390 *** (0.1287) | −0.3729 ** (0.1701) | −0.4258 *** (0.1477) | |

| 0.1183 (2.2655) | 152.4128 (245.6283) | 1.4005 *** (0.5300) | 5.4548 (4.7713) | 29.0942 * (17.4163) | 1.1436 (0.9136) | |

| 0.0000 (0.0315) | 0.2898 (0.1871) | 0.9990 *** (0.2441) | 0.3982 ** (0.1556) | 0.8014 ** (0.3803) | 0.7657 ** (0.3310) | |

| 0.9990 *** (0.0428) | 0.6598 *** (0.2154) | 0.0000 (0.0088) | 0.6008 *** (0.1358) | 0.1976 (0.1239) | 0.2333 (0.1947) | |

| 2.4435 ** (1.0165) | 5.6228 *** (4.6862) | 2.8528 *** (0.2913) | 32.3070 (78.3328) | 2.3974 *** (0.2040) | 3.1404 *** (0.5656) | |

| Log Likelihood | 6.1231 | 10.321 | 5.0838 | 7.6978 | 6.9685 | 4.4099 |

| AIC | −329.7686 | −560.6668 | −272.609 | −416.3775 | −376.2652 | −235.543 |

| Paris | Copula | Parameter 1 (SE) | Parameter 2 (SE) | Tau | Tail Dep | |

|---|---|---|---|---|---|---|

| Before the ETS | ||||||

| Tree 1 | EUA-HB | t | 0.01 (0.07) | 5.46 *** (1.99) | 0.00 | 0.04 |

| EUA-SH | t | 0.03 (0.06) | 5.09 *** (1.60) | 0.02 | 0.05 | |

| EUA-SZ | t | −0.13 ** (0.06) | 11.51 (9.02) | −0.08 | 0.00 | |

| EUA-BJ | N | 0.12 ** (0.06) | - | 0.07 | - | |

| EUA-GD | t | −0.17 *** (0.06) | 9.13 (5.81) | −0.11 | 0.00 | |

| Tree 2 | GD-HB|EUA | t | −0.04 (0.06) | 6.00 *** (2.20) | −0.02 | 0.03 |

| GD-SH|EUA | N | 0.08 (0.05) | - | 0.05 | - | |

| GD-SZ|EUA | C | 0.16 ** (0.07) | - | 0.07 | 0.01 L | |

| GD-BJ|EUA | C | 0.18 ** (0.07) | - | 0.08 | 0.02 L | |

| After the ETS | ||||||

| Tree 1 | EUA-HB | t | −0.04 (0.06) | 7.11 *** (2,75) | −0.02 | 0.02 |

| EUA-SH | t | −0.07 (0.06) | 6.41 *** (2.32) | −0.04 | 0.02 | |

| EUA-SZ | t | −0.02 (0.06) | 7.45 ** (3.36) | −0.02 | 0.02 | |

| EUA-BJ | F | −0.29 (0.43) | - | −0.03 | - | |

| EUA-GD | N | 0.04 (0.06) | - | 0.02 | - | |

| Tree 2 | BJ-SZ|EUA | F | 0.07 (0.51) | - | 0.01 | - |

| BJ-GD|EUA | t | −0.09 (0.15) | 5.11 ** (2.56) | −0.05 | 0.04 | |

| BJ-SH|EUA | C | 0.18 ** (0.07) | - | 0.08 | 0.02 L | |

| BJ-HB|EUA | N | 0.05 (0.09) | - | 0.03 | - | |

| Paris | Copula | Parameter 1 (SD) | Parameter 2 (SD) | Tau | Tail dep | |

|---|---|---|---|---|---|---|

| Before COVID-19 | ||||||

| Tree 1 | EUA-SZ | C | 0.04 (0.07) | - | 0.02 | 0.00 L |

| EUA-GD | C | 0.07 (0.08) | - | 0.04 | 0.00 L | |

| EUA-SH | t | 0.05 (0.09) | 4.00 *** (1.27) | 0.03 | 0.09 | |

| EUA-HB | t | −0.09 (0.08) | 4.54 *** (1.68) | −0.05 | 0.05 | |

| EUA-BJ | G | 1.01 *** (0.06) | - | 0.01 | 0.01 U | |

| Tree 2 | BJ-SZ|EUA | F | −0.23 (0.66) | - | −0.03 | - |

| BJ-GD|EUA | t | 0.05 (0.02) | 4.51 * (2.39) | 0.03 | 0.07 | |

| BJ-SH|EUA | C | 0.25 ** (0.01) | - | 0.11 | 0.06 L | |

| BJ-HB|EUA | F | 0.64 (0.62) | - | 0.07 | - | |

| After COVID-19 | ||||||

| Tree 1 | EUA-SZ | t | −0.06 (0.10) | 5.46 * (3.06) | −0.04 | 0.03 |

| EUA-GD | C | 0.00 (0.10) | - | 0.00 | - | |

| EUA-SH | t | −0.20 * (0.10) | 10.43 (9.42) | −0.13 | 0.00 | |

| EUA-HB | t | 0.02 (0.11) | - | 0.01 | 0.01 | |

| EUA-BJ | t | −0.09 (0.09) | - | −0.06 | 0.00 | |

| Tree 2 | SH-GD|EUA | t | −0.09 (0.14) | - | −0.06 | 0.00 |

| SH-SZ|EUA | J | 1.26 *** (0.16) | - | 0.13 | 0.27 | |

| SH-BJ|EUA | F | 0.81 (0.66) | - | 0.09 | - | |

| SH-HB|EUA | F | −1.18 (0.75) | - | −0.13 | - | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, M.; Liu, H.; Liu, J.; Chen, C.; Li, Z.; Wang, B.; Sriboonchitta, S. Modelling Dependency Structures of Carbon Trading Markets between China and European Union: From Carbon Pilot to COVID-19 Pandemic. Axioms 2022, 11, 695. https://doi.org/10.3390/axioms11120695

Zhang M, Liu H, Liu J, Chen C, Li Z, Wang B, Sriboonchitta S. Modelling Dependency Structures of Carbon Trading Markets between China and European Union: From Carbon Pilot to COVID-19 Pandemic. Axioms. 2022; 11(12):695. https://doi.org/10.3390/axioms11120695

Chicago/Turabian StyleZhang, Mingzhi, Hongyu Liu, Jianxu Liu, Chao Chen, Zhaocheng Li, Bowen Wang, and Songsak Sriboonchitta. 2022. "Modelling Dependency Structures of Carbon Trading Markets between China and European Union: From Carbon Pilot to COVID-19 Pandemic" Axioms 11, no. 12: 695. https://doi.org/10.3390/axioms11120695

APA StyleZhang, M., Liu, H., Liu, J., Chen, C., Li, Z., Wang, B., & Sriboonchitta, S. (2022). Modelling Dependency Structures of Carbon Trading Markets between China and European Union: From Carbon Pilot to COVID-19 Pandemic. Axioms, 11(12), 695. https://doi.org/10.3390/axioms11120695