Global Potential of Rare Earth Resources and Rare Earth Demand from Clean Technologies

Abstract

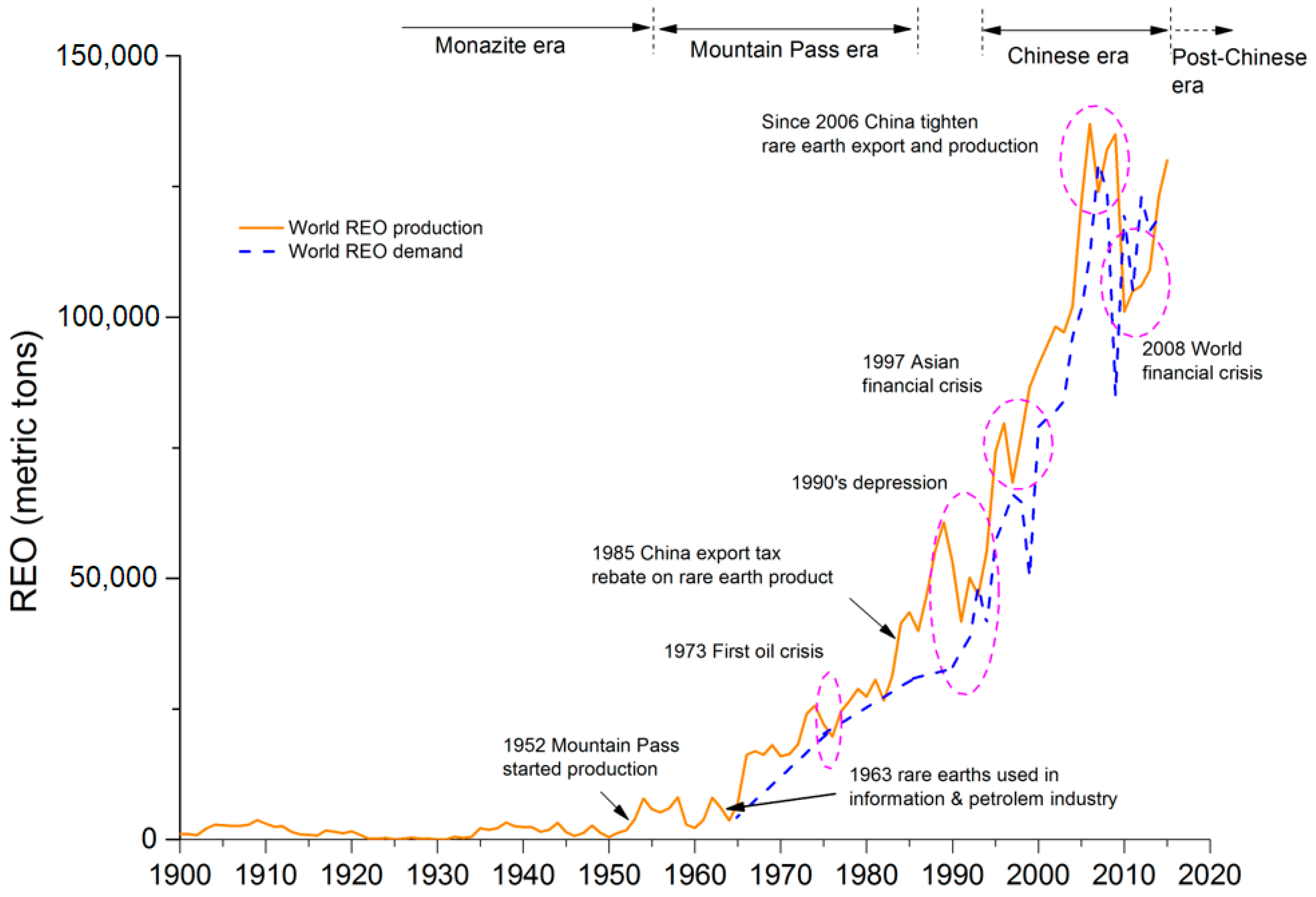

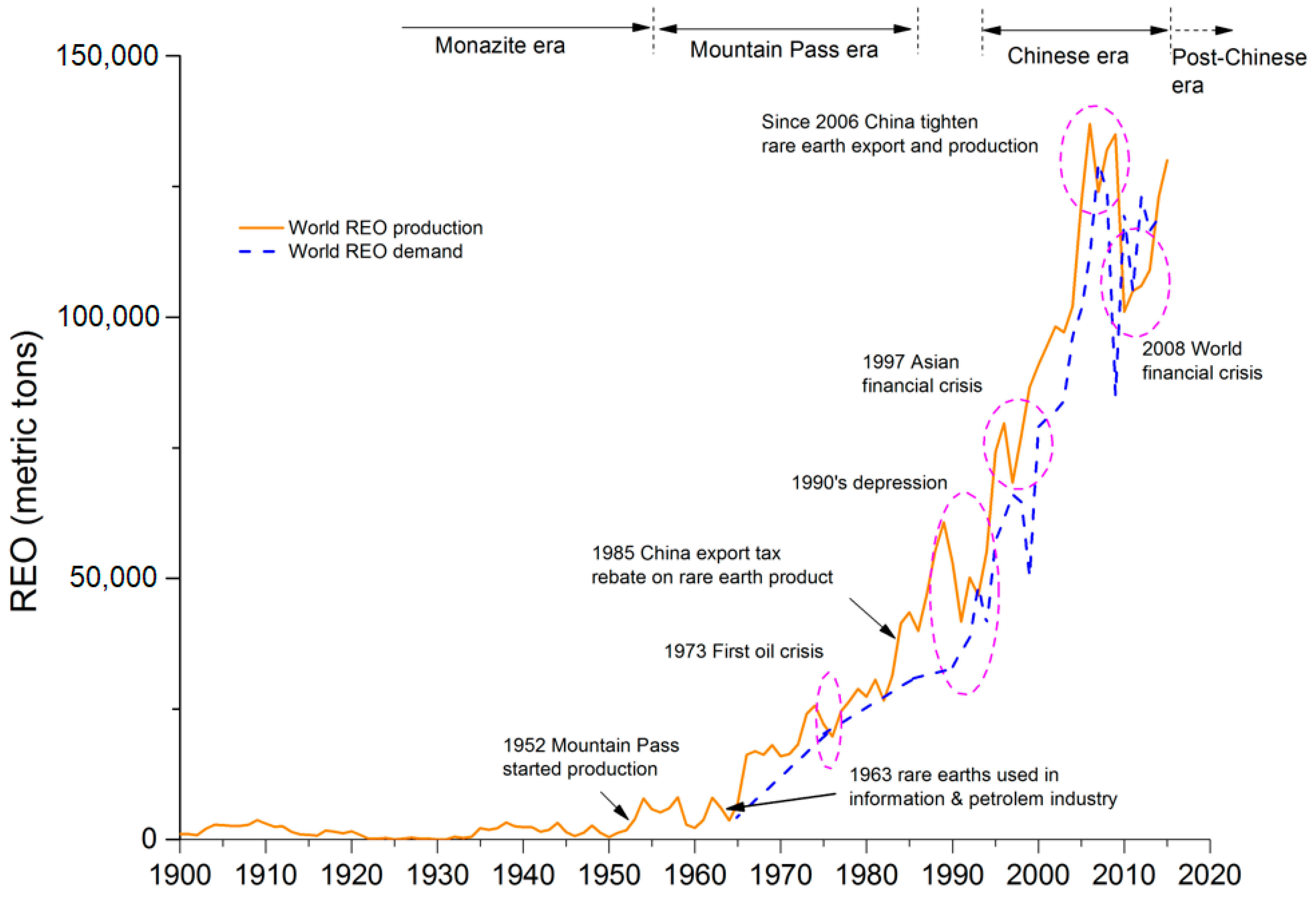

:1. Introduction

2. Methodology

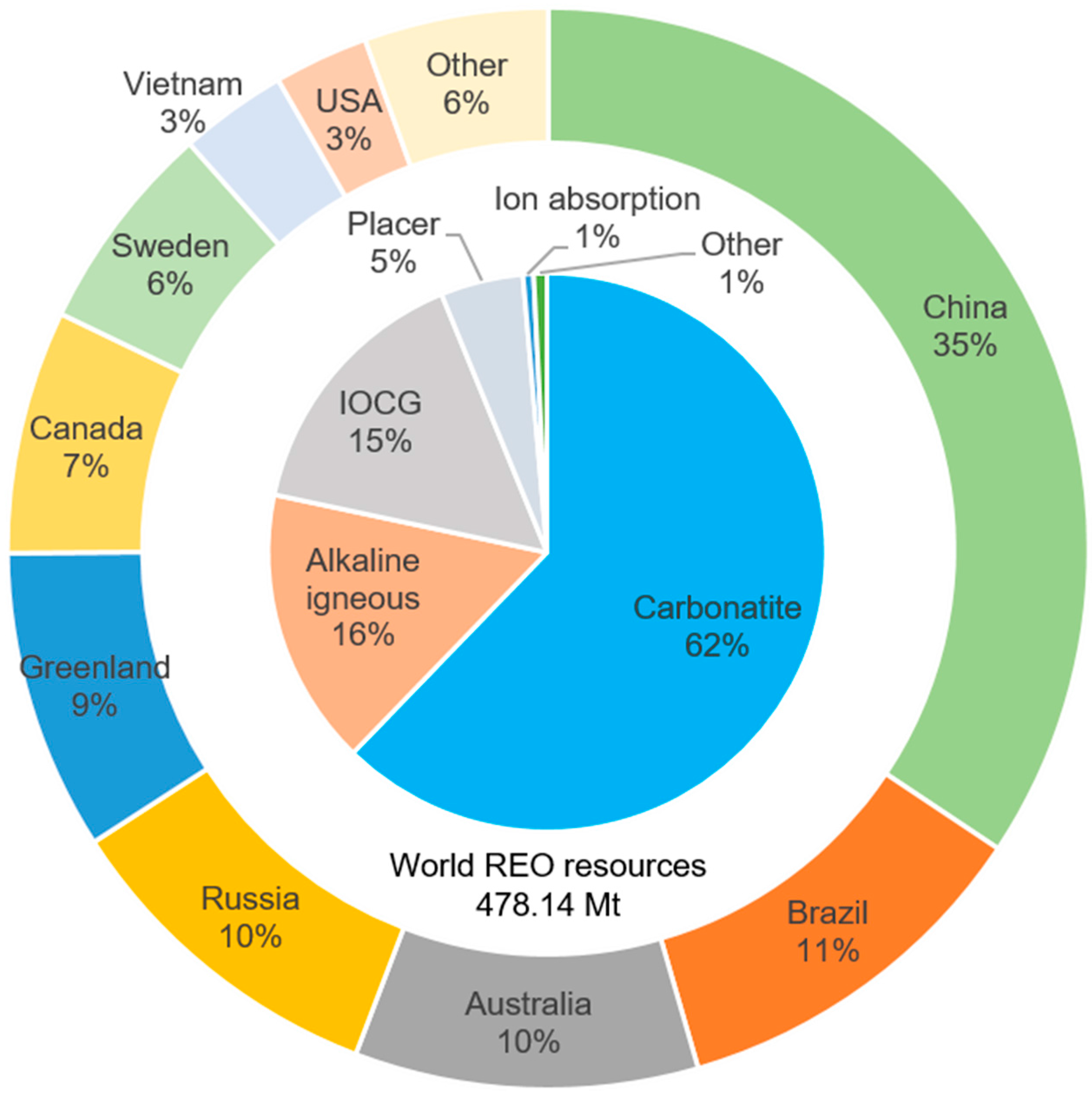

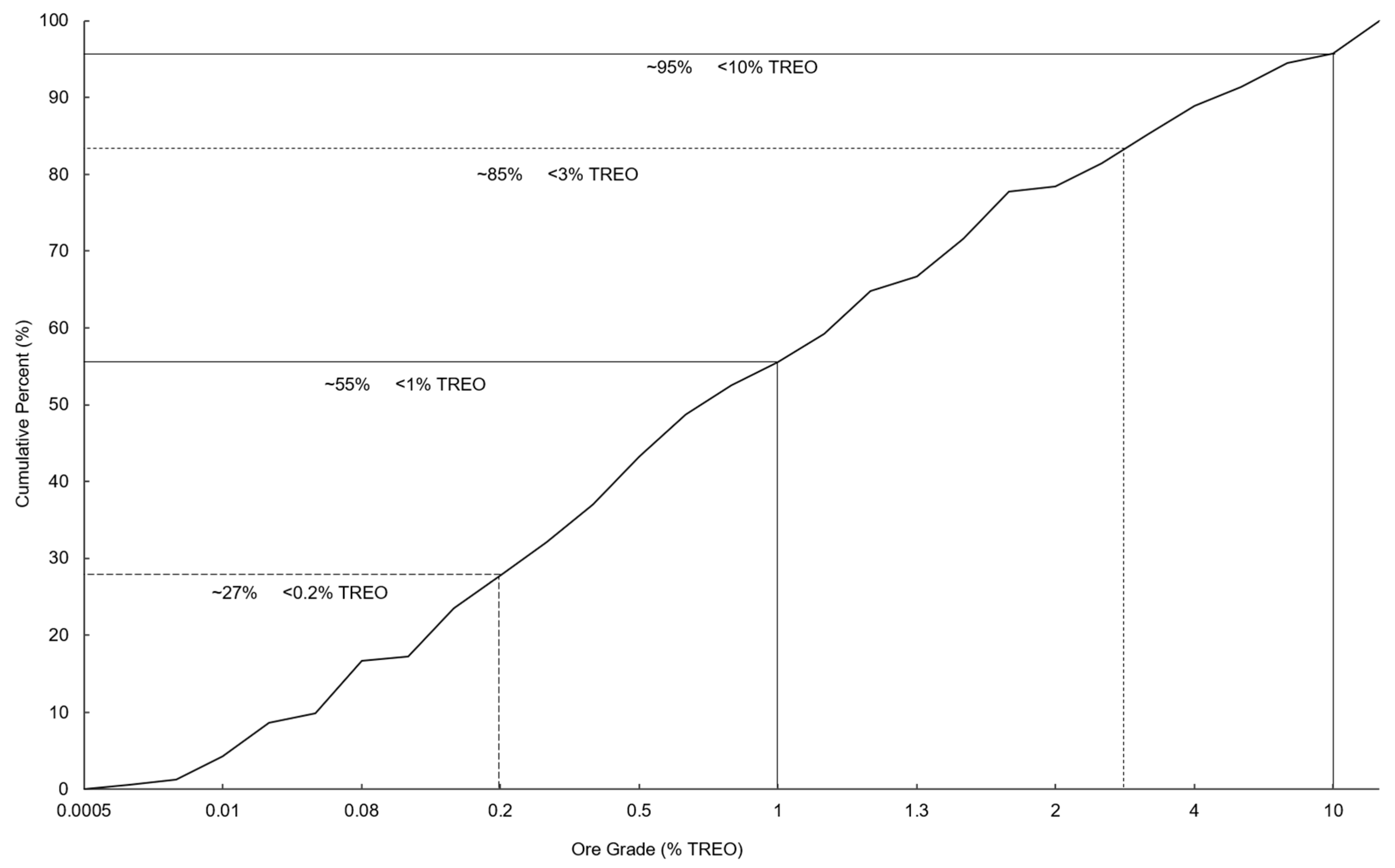

2.1. Identification of Global Rare Earth Resources

2.2. Rare Earths in Clean Technologies

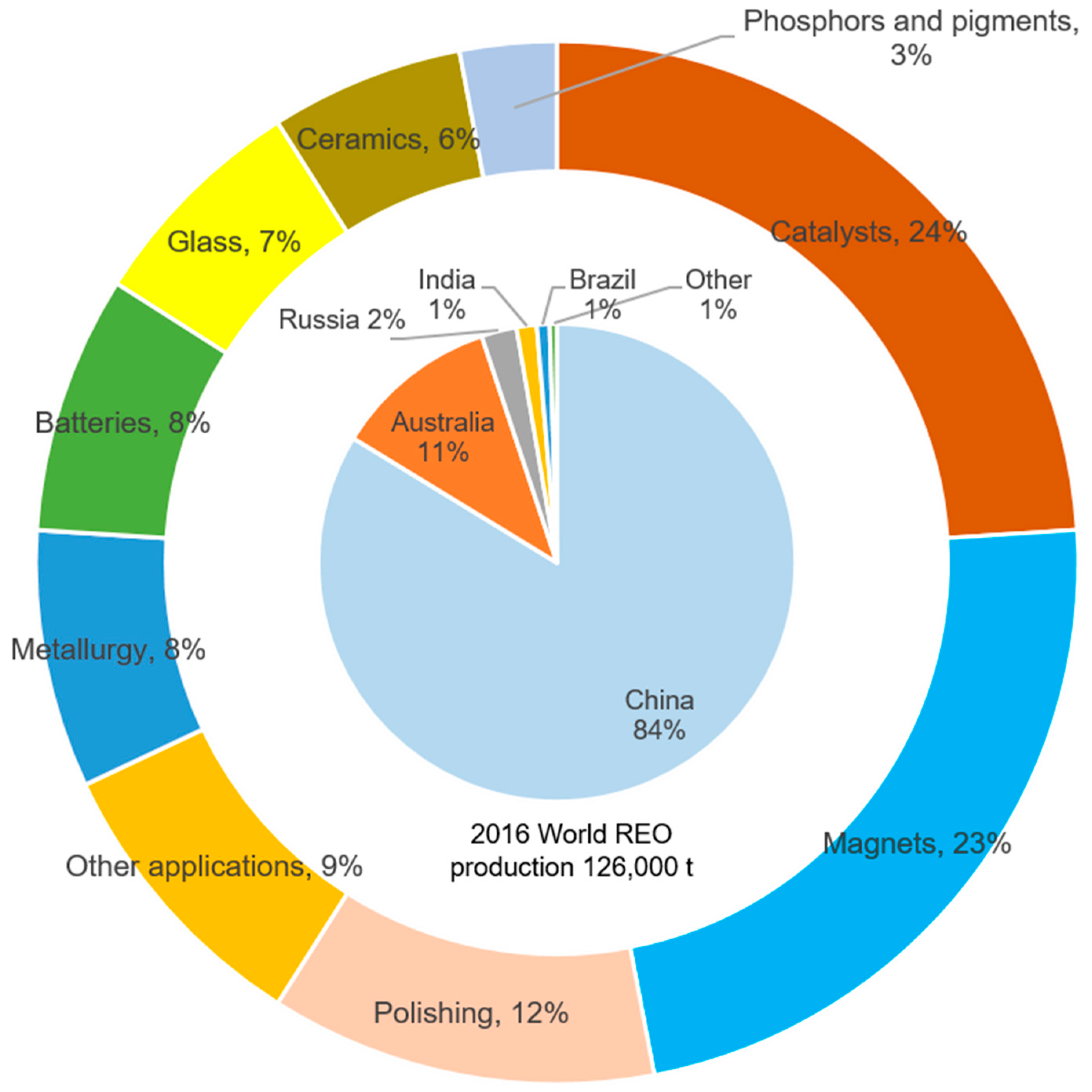

3. Results and Discussion

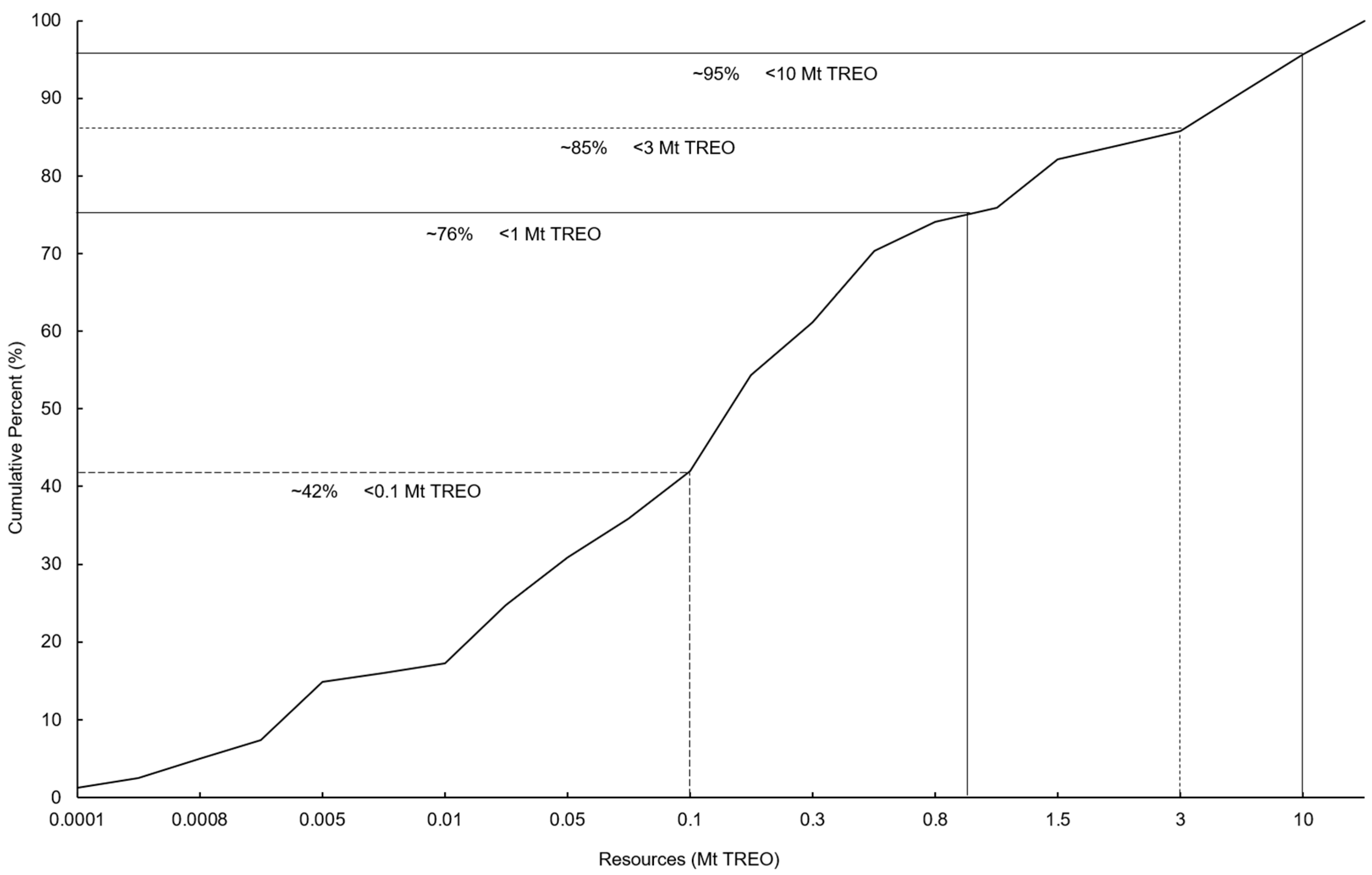

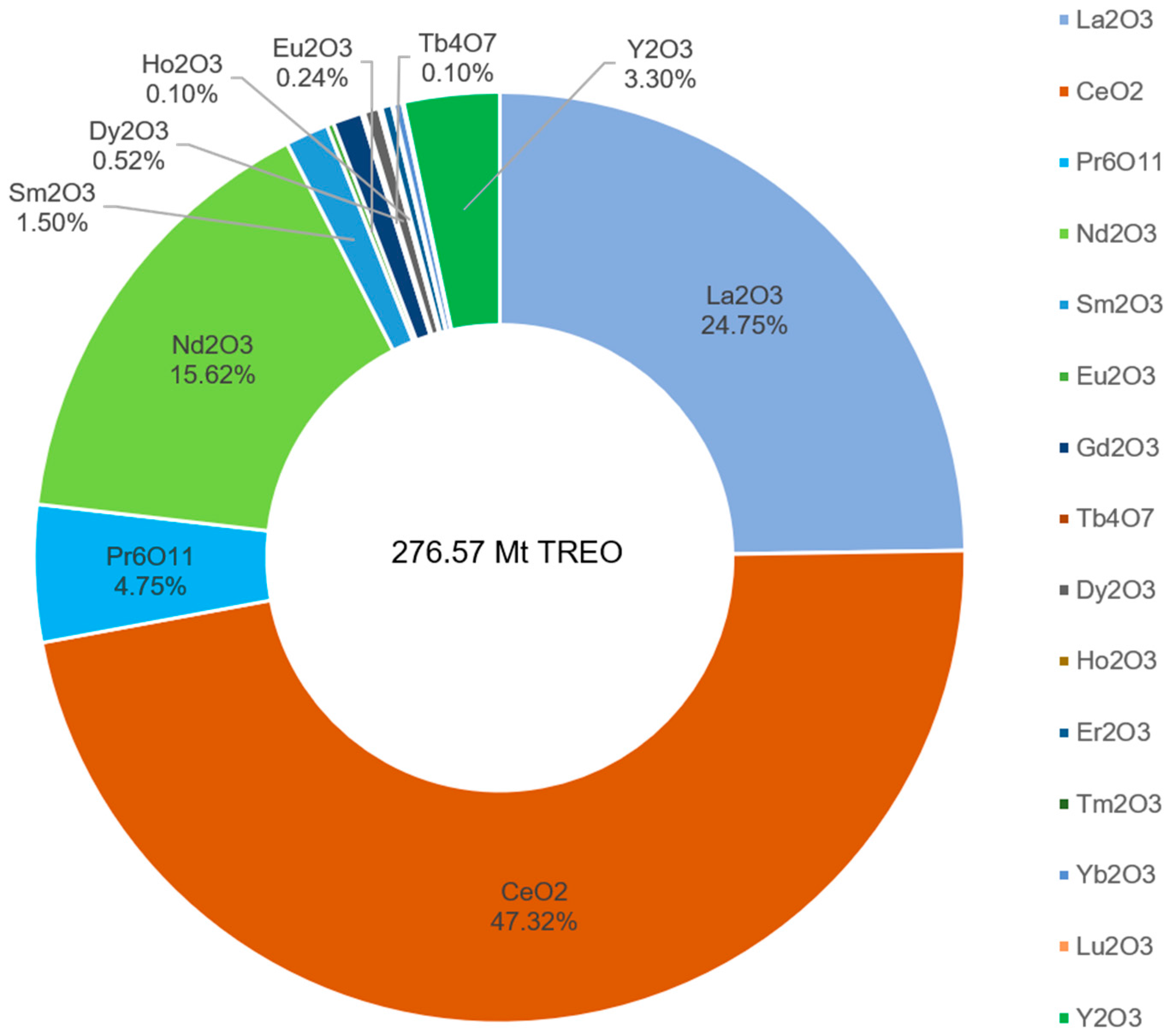

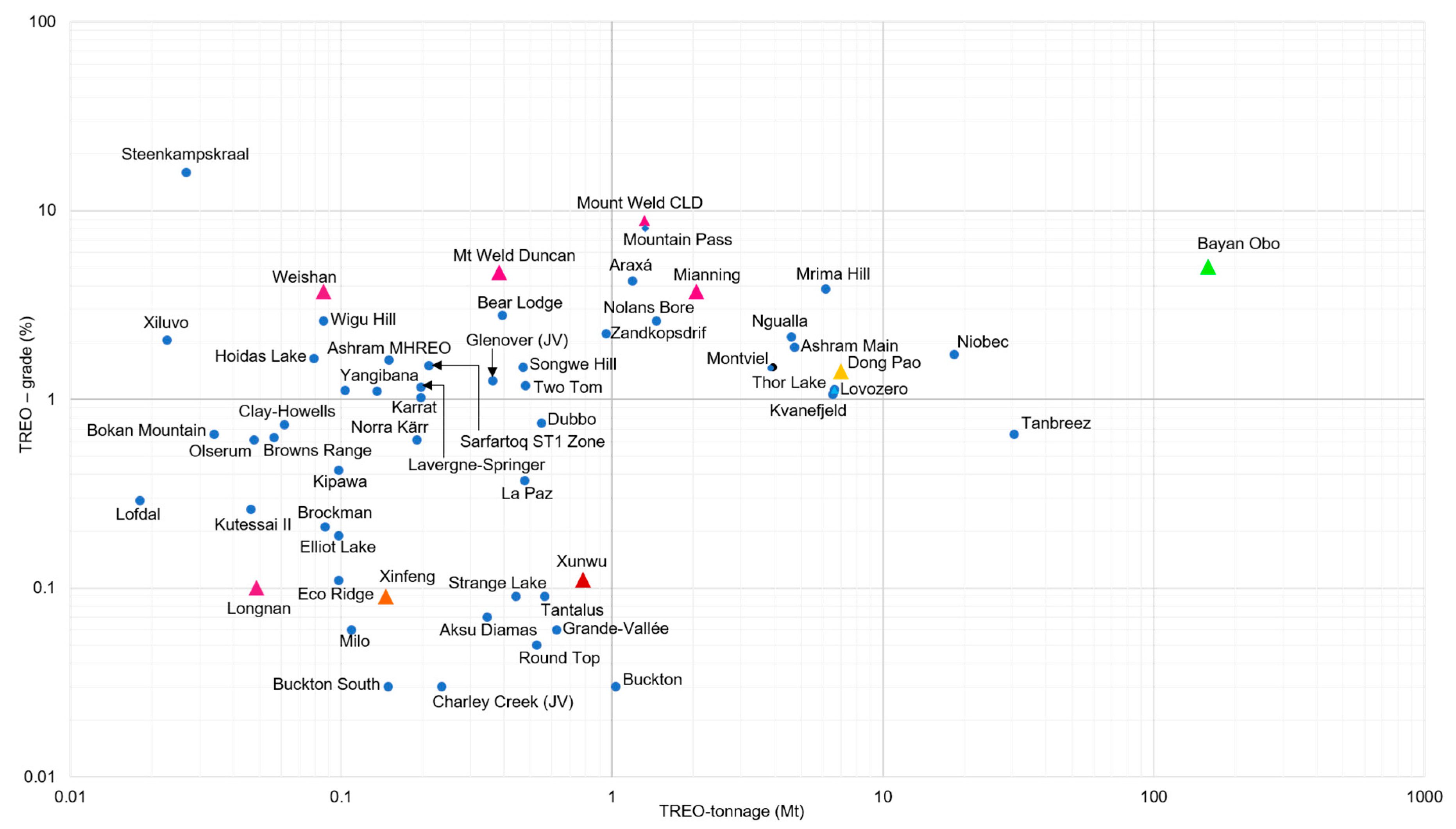

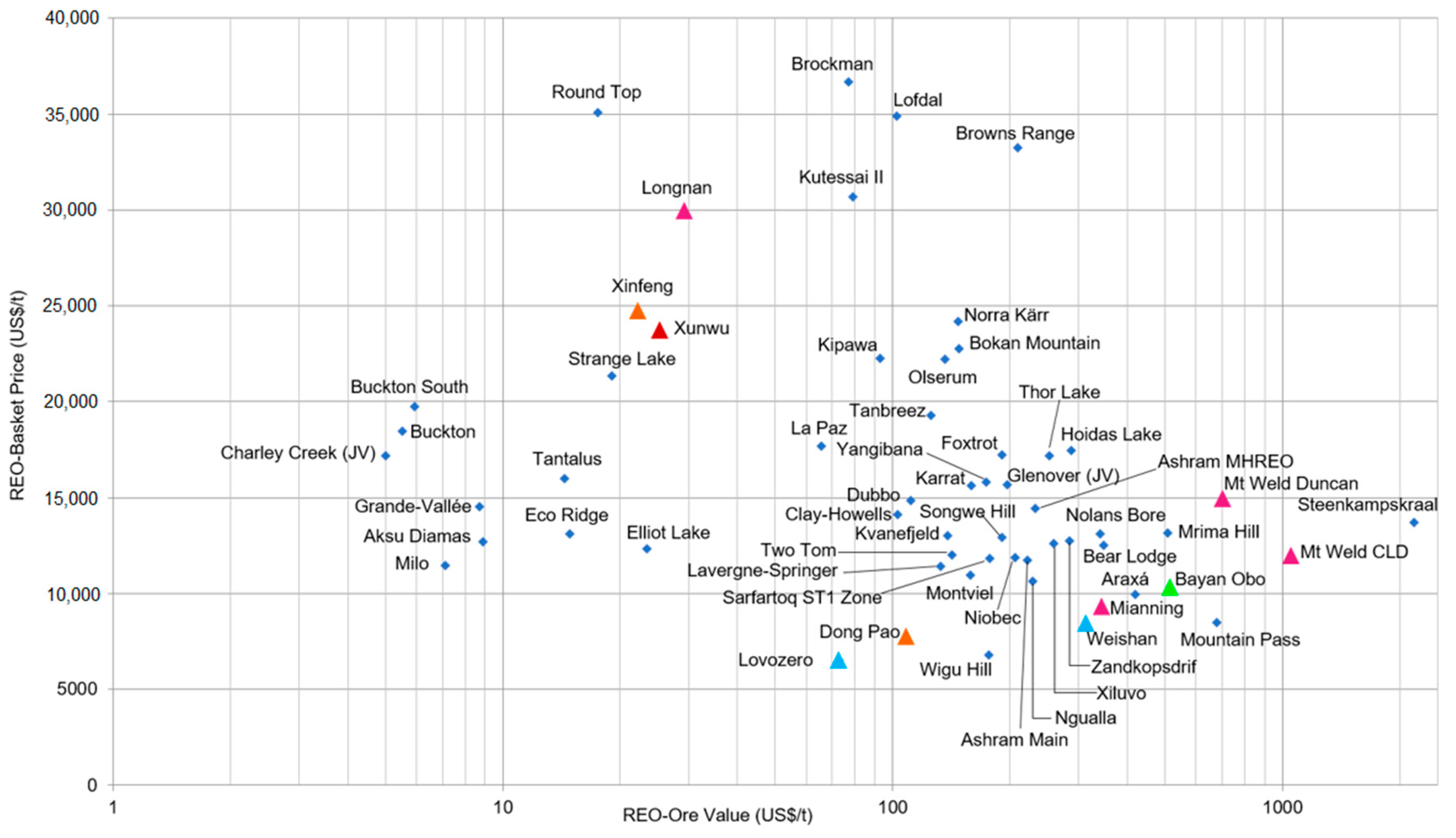

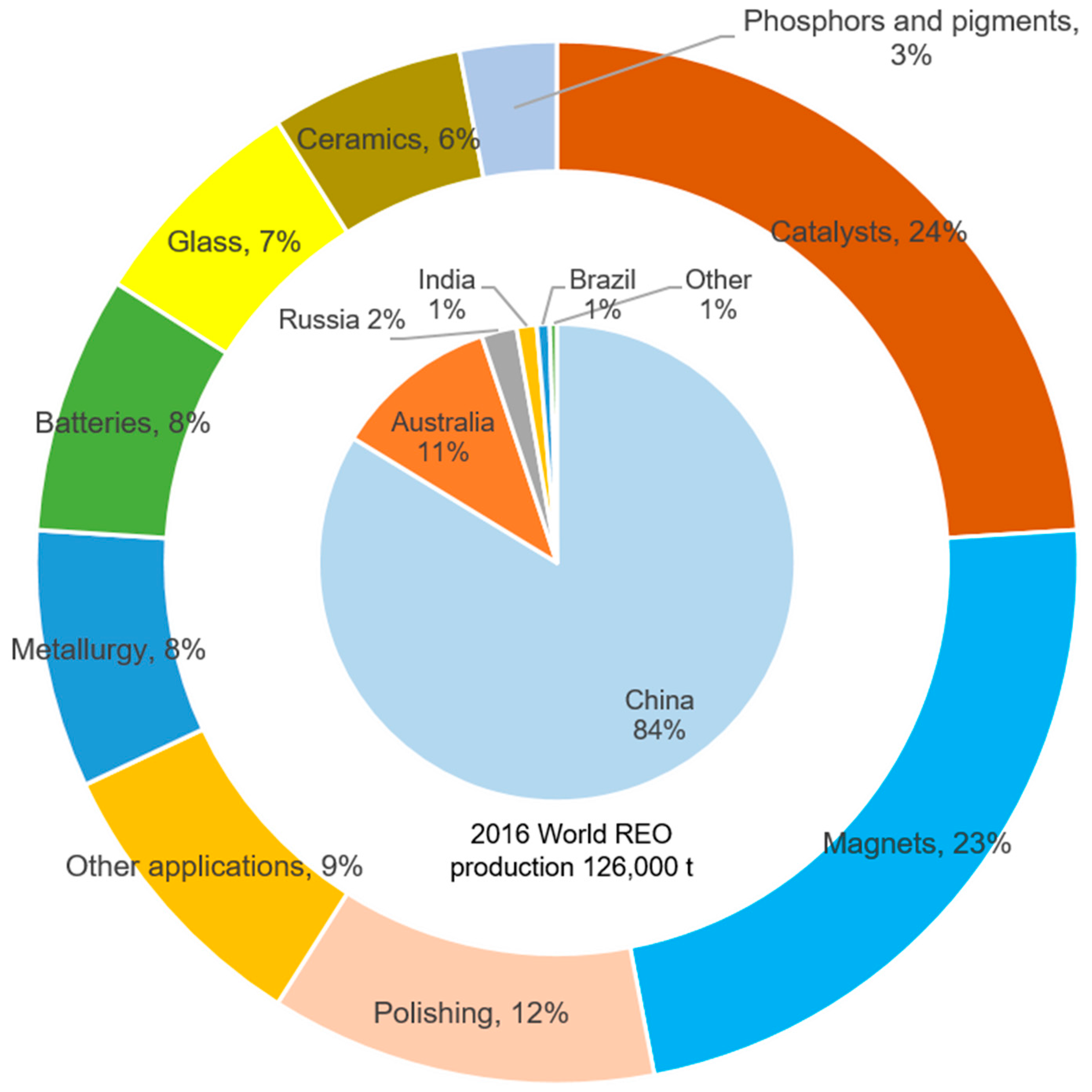

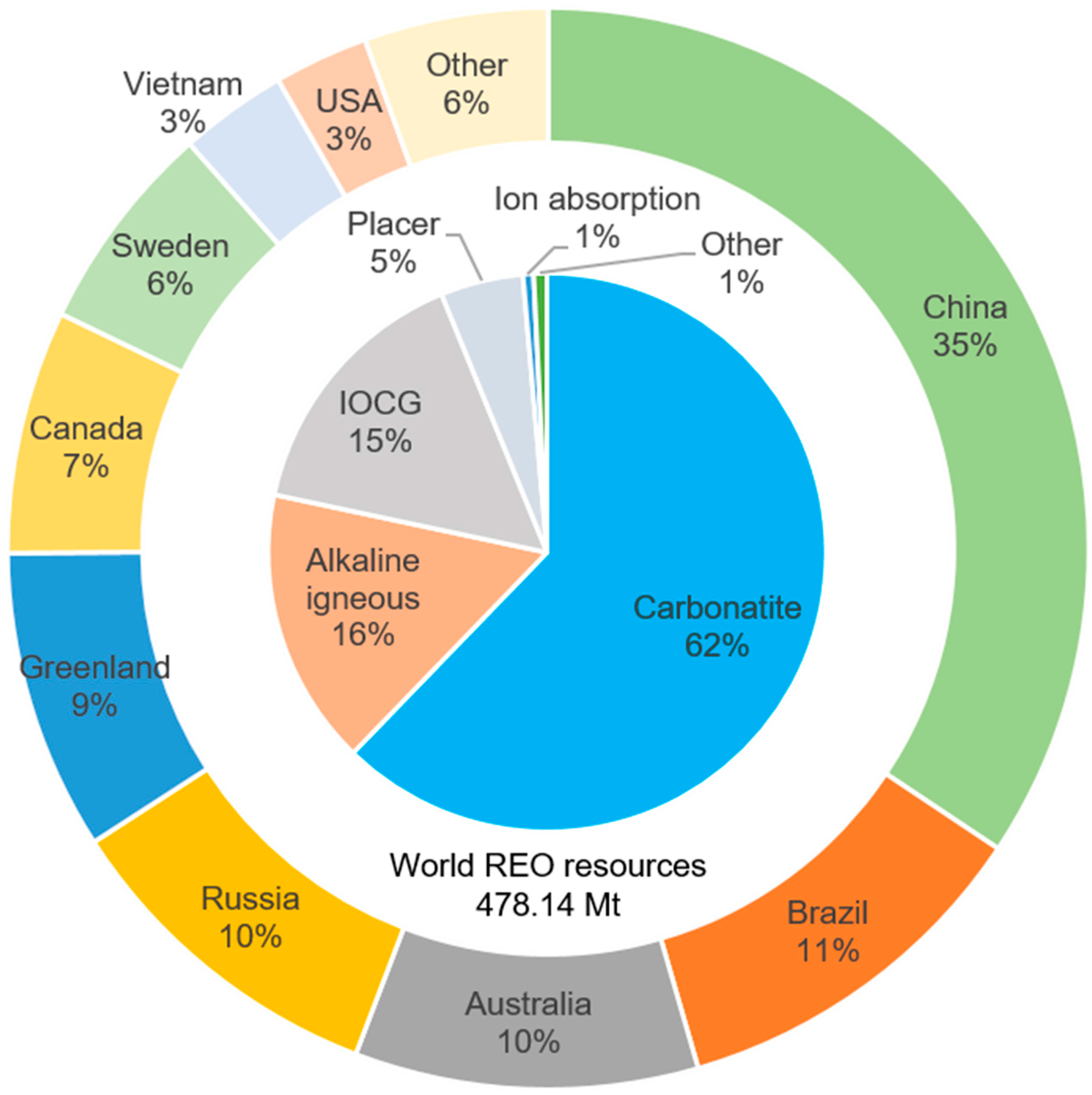

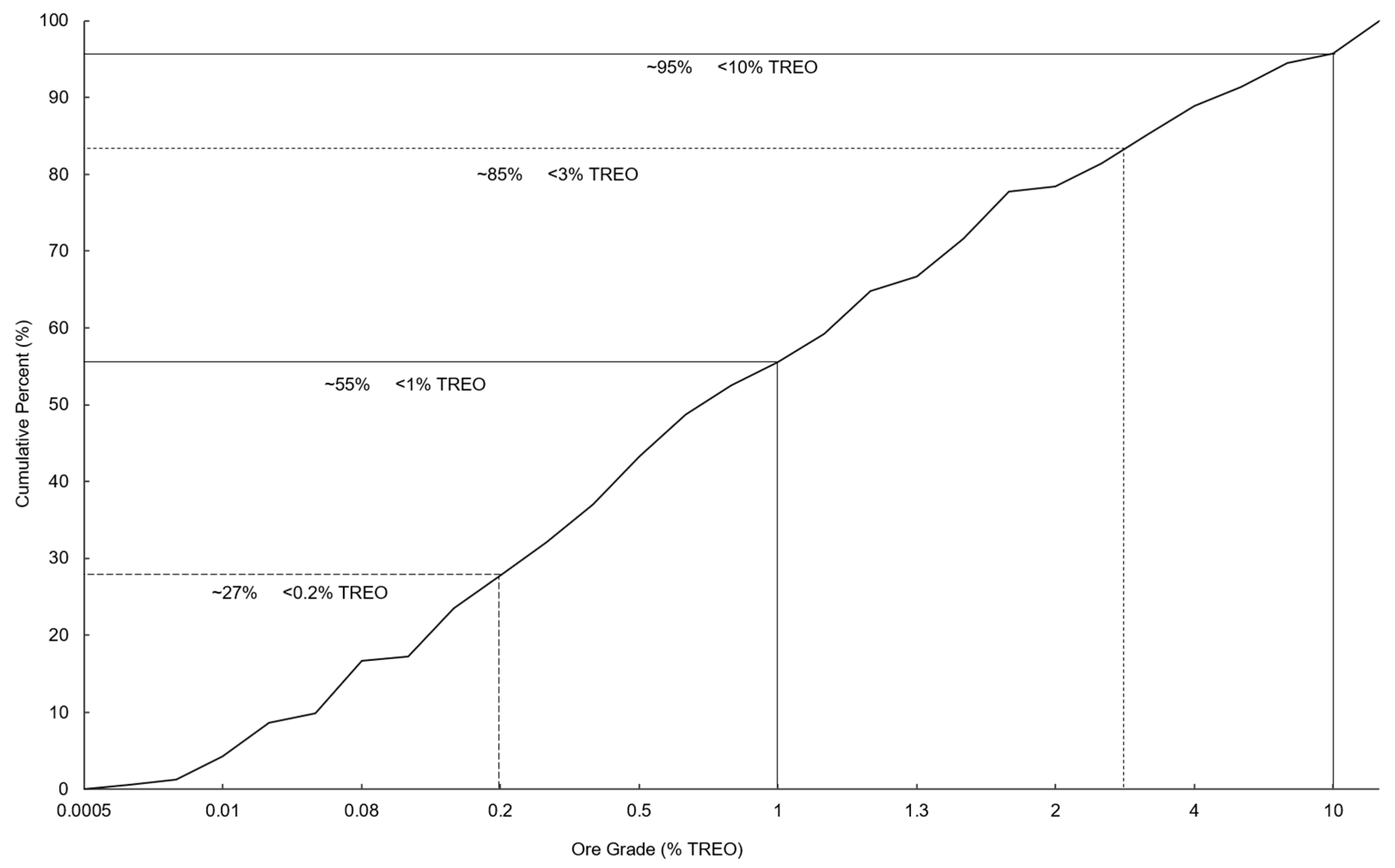

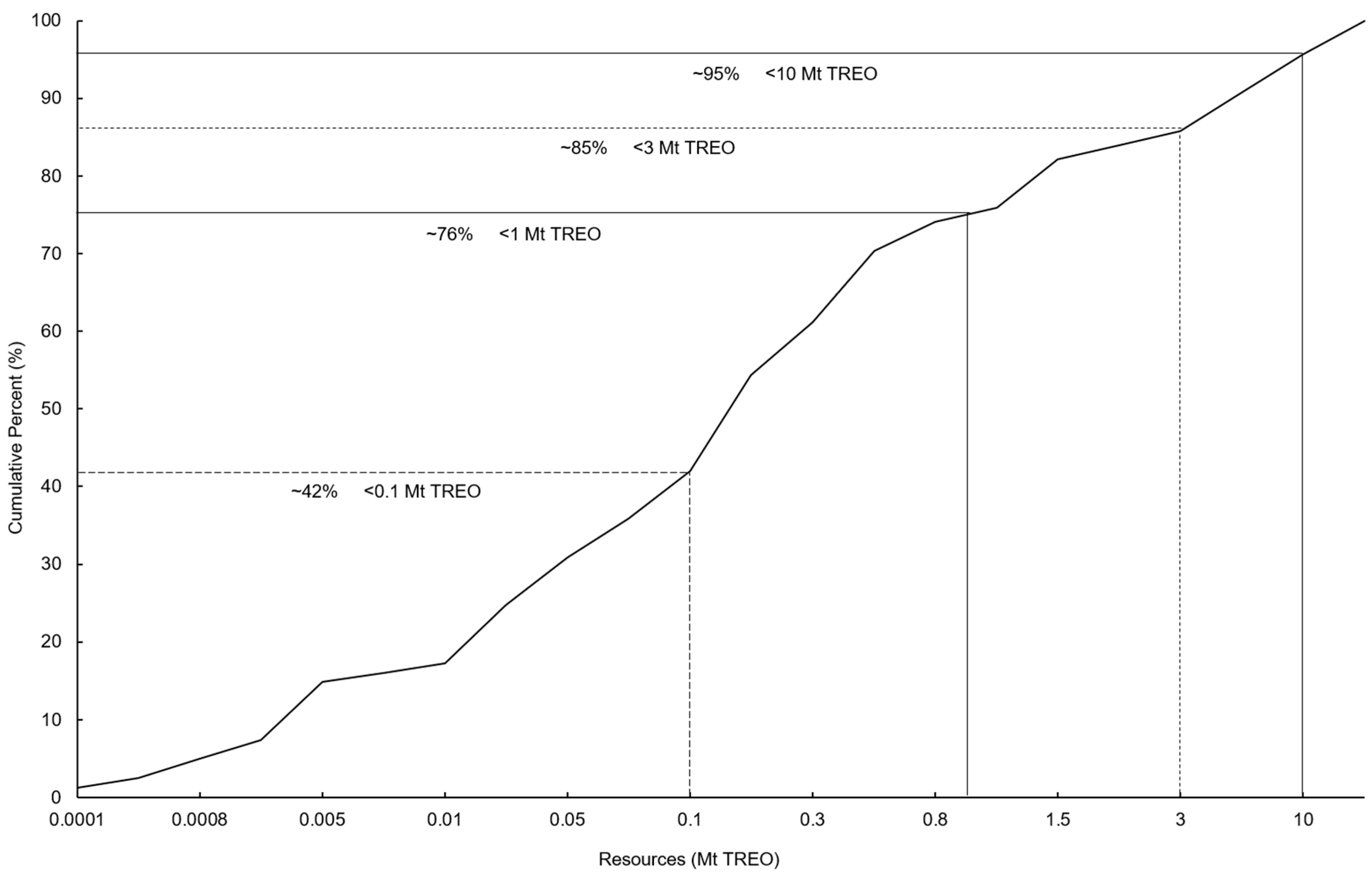

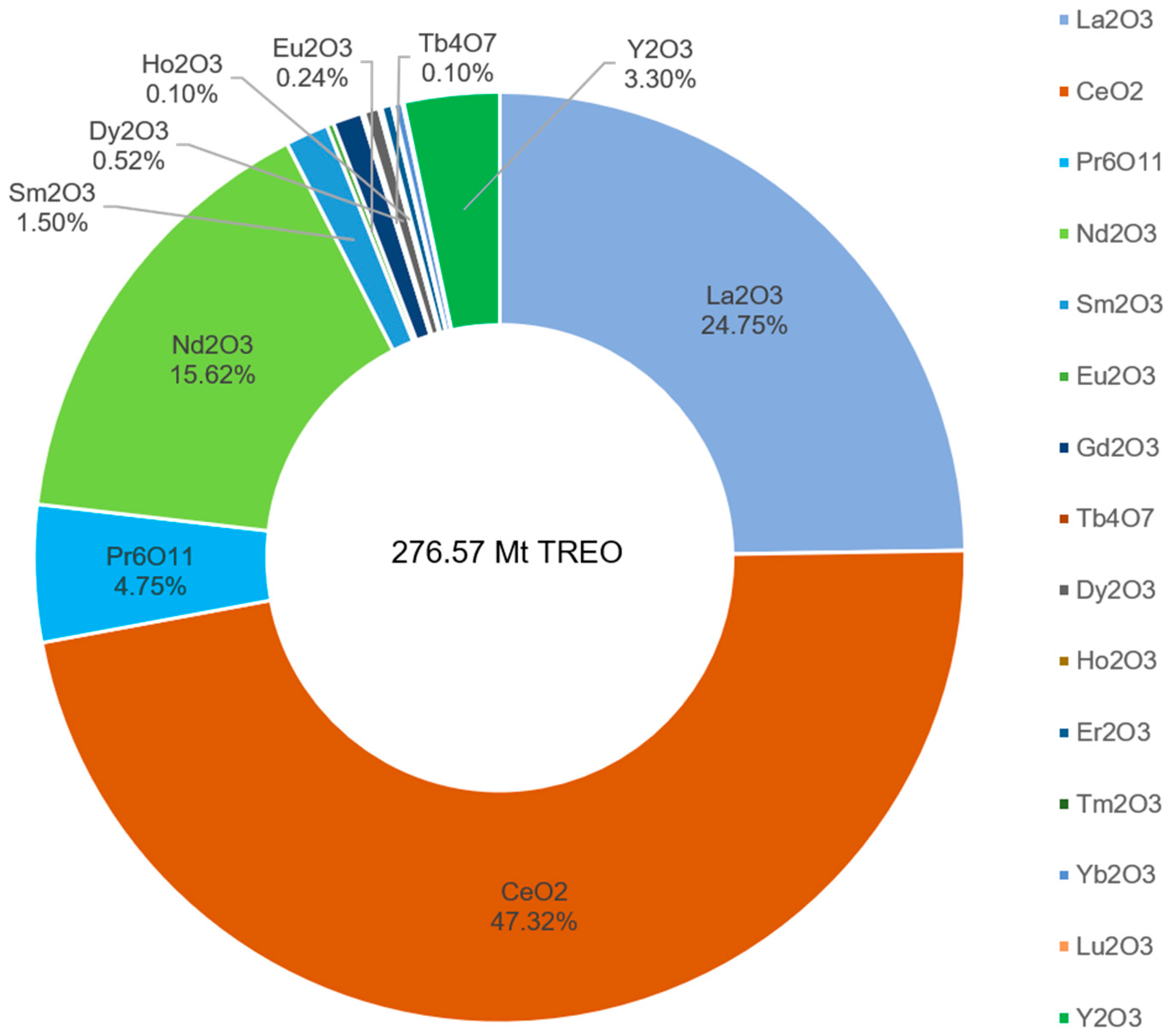

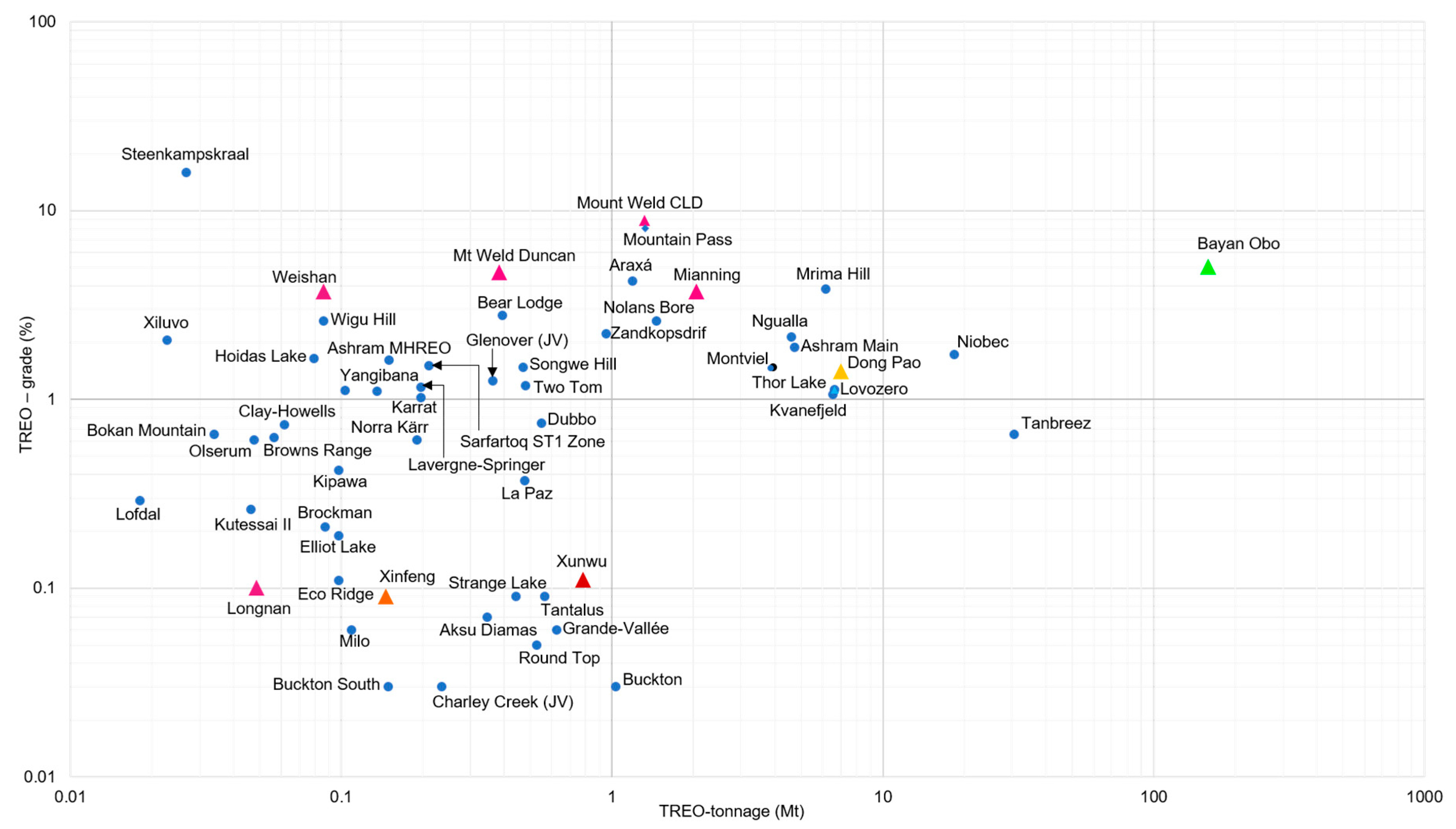

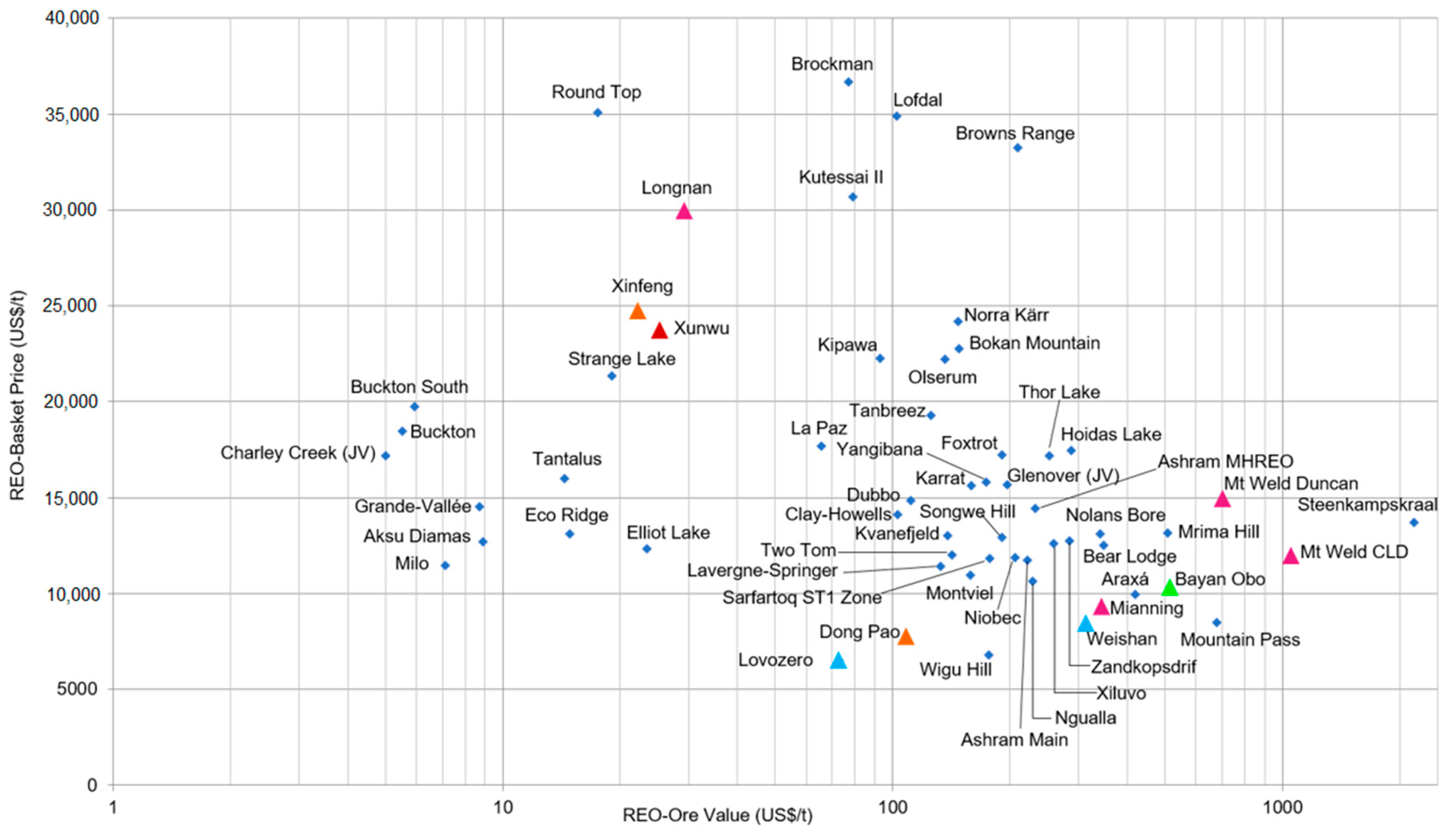

3.1. Global Potential of Rare Earth Resources

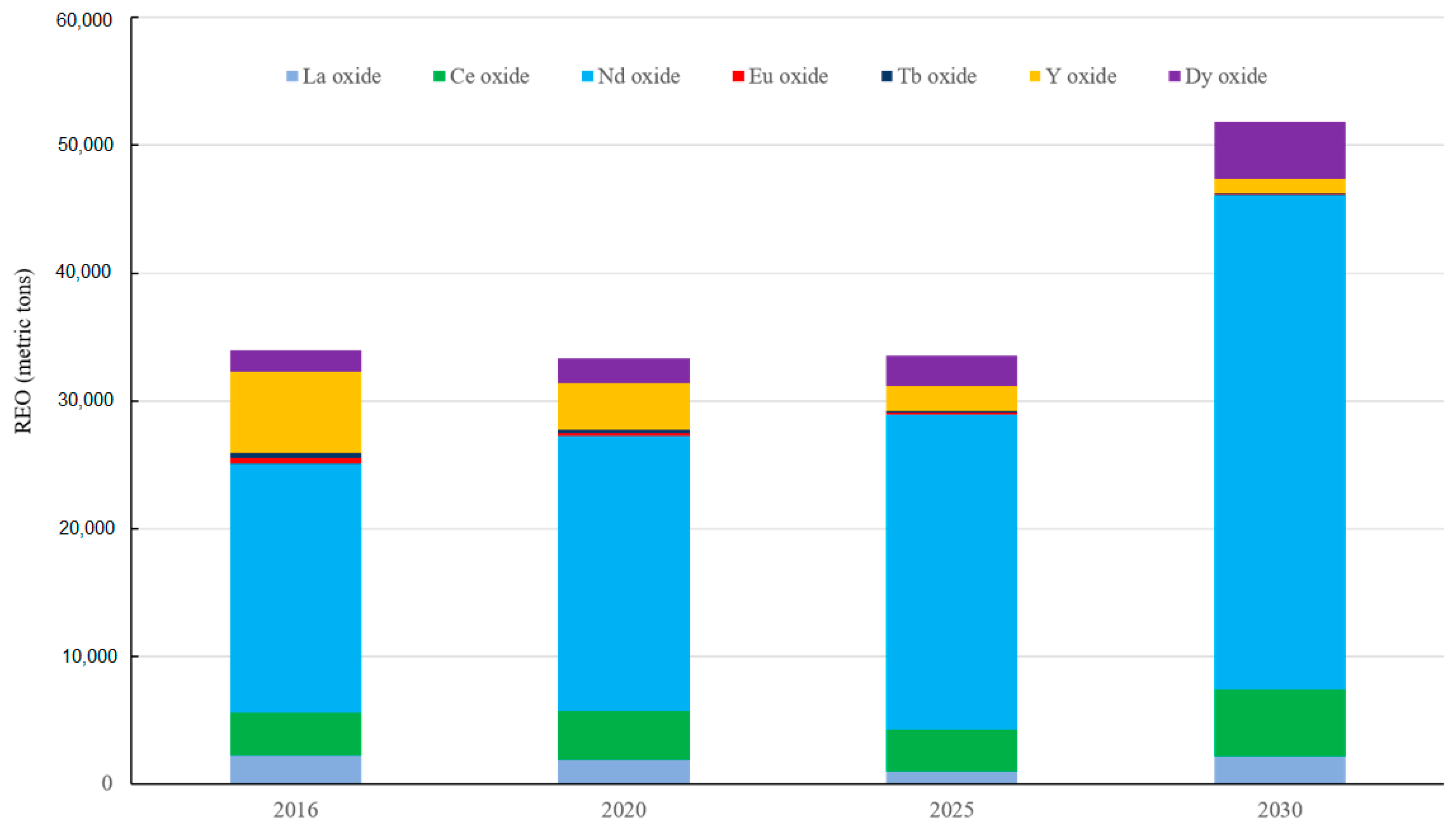

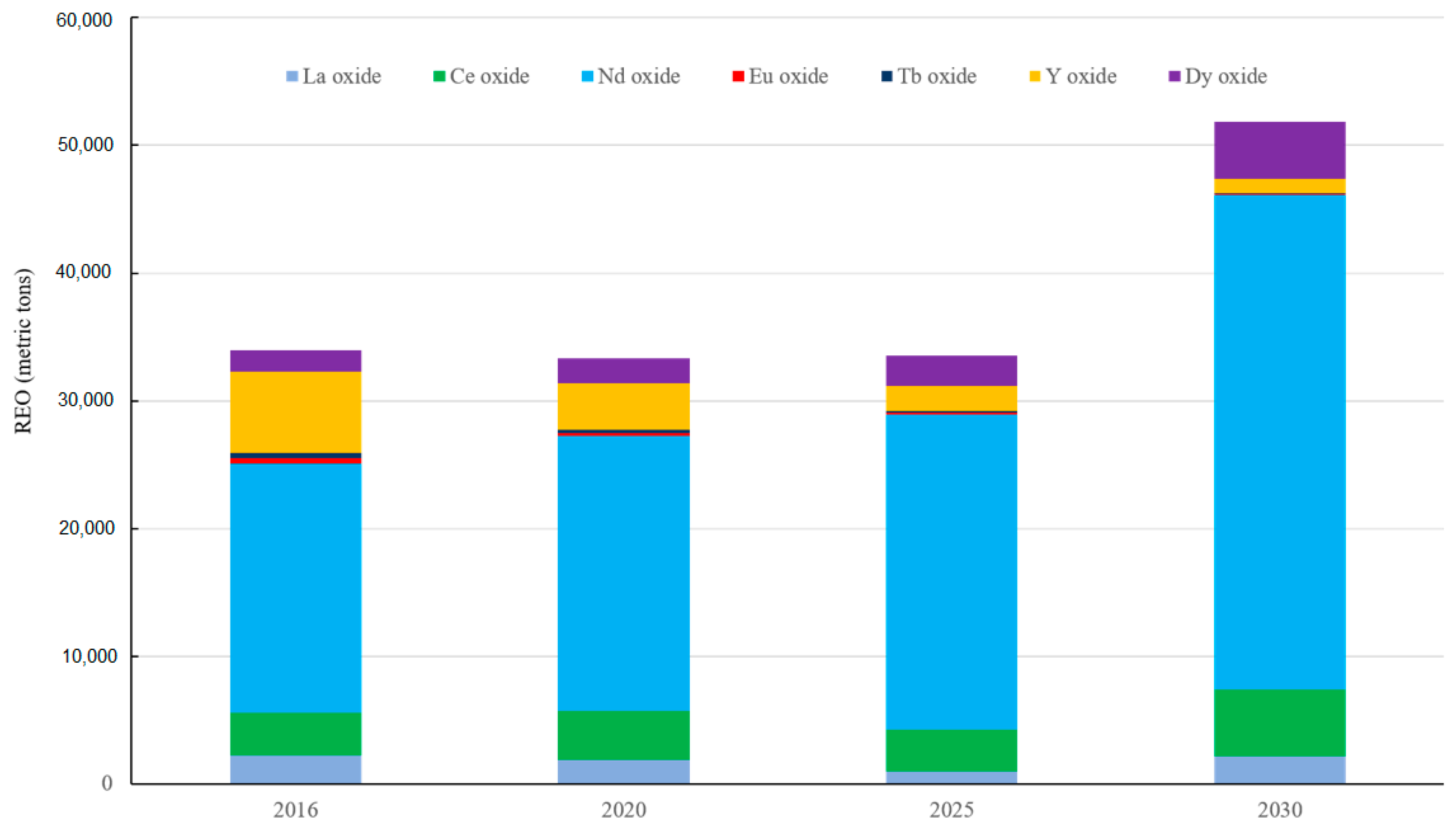

3.2. Rare Earth Demand from Clean Technologies

4. Conclusions

Supplementary Materials

Author Contributions

Conflicts of Interest

References

- Klinger, J.M. A historical geography of rare earth elements: From discovery to the atomic age. Extr. Ind. Soc. 2015, 2, 572–580. [Google Scholar] [CrossRef]

- U.S. Department of Energy. Critical Materials Strategy. Available online: https://energy.gov/sites/prod/files/piprod/documents/cms_dec_17_full_web.pdf (accessed on 1 August 2017).

- Zhou, B.; Li, Z.; Zhao, Y.; Zhang, C.; Wei, Y. Rare Earth Elements Supply vs. Clean Energy Technologies: New Problems to Solve. Gospod. Surowcami Miner. 2016, 32, 29–44. [Google Scholar] [CrossRef]

- Tukker, A. Rare earth elements supply restrictions: Market failures, not scarcity, hamper their current use in high-tech applications. Environ. Sci. Technol. 2014, 48, 9973–9974. [Google Scholar] [CrossRef] [PubMed]

- Alonso, E.; Sherman, A.M.; Wallington, T.J.; Everson, M.P.; Field, F.R.; Roth, R.; Kirchain, R.E. Evaluating rare earth element availability: A case with revolutionary demand from clean technologies. Environ. Sci. Technol. 2012, 46, 3406–3414. [Google Scholar] [CrossRef] [PubMed]

- Humphries, M. Rare Earth Elements: The Global Supply Chain. Available online: https://fas.org/sgp/crs/natsec/R41347.pdf (accessed on 6 July 2017).

- Nomenclature of Inorganic Chemistry IUPAC Recommendations 2005. Available online: http://old.iupac.org/publications/books/rbook/Red_Book_2005.pdf (accessed on 9 August 2017).

- U.S. Geological Survey. The Rare-Earth Elements—Vital to Modern Technologies and Lifestyles. Available online: https://pubs.usgs.gov/fs/2014/3078/pdf/fs2014-3078.pdf (accessed on 9 June 2017).

- U.S. Geological Survey. Minerals Year Book—Rare Earths. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/mcs-2014-raree.pdf (accessed on 1 February 2017).

- The Information Office of the State Council of China. Situation and Policies of China’s Rare Earth Industry. Available online: http://english.gov.cn/archive/white_paper/2014/08/23/content_281474983043156.htm (accessed on 1 October 2016).

- CROSSLAND Uranium Mines Ltd. Charley Creek Rare Earths Project Scoping Study Results. Available online: http://www.crosslanduranium.com.au/uploads/resources/ASX_Release_Charley_Ck_scoping_Study_15_Apr_13_Final.pdf (accessed on 15 June 2017).

- Gagnon, G.; Rousseau, G.; Camus, Y.; Gagné, J. NI 43-101 Technical Report Preliminary Economic Assessment Ashram Rare Earth Deposit for Commerce Resources Corp. Available online: https://www.commerceresources.com/assets/docs/reports/2015-01-07_GG-PEA-Report.pdf (accessed on 20 March 2017).

- U.S. Geological Survey. Minerals Year Book—Rare Earths. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/mcs-2015-raree.pdf (accessed on 9 February 2017).

- Kingsnorth, D. Can China’s Rare Earths Dynasty Survive? Available online: http://investorintel.com/wp-content/uploads/2013/09/DJK-China-IM-Sept-2013-V3.pptx (accessed on 9 December 2016).

- Su, W. Economic Analysis and Policy Research of Rare Earth Industry in China; China Financial & Economic Publishing House: Beijing, China, 2009; ISBN 9787509513361. (In Chinese) [Google Scholar]

- Development of a Sustainable Exploitation Scheme for Europe’s Rare Earth Ore Deposits. Available online: http://promine.gtk.fi/documents_news/promine_final_conference/8_50_PASPALIARIS_EURARE_project_promine.pdf (accessed on 9 July 2017).

- Rudnick, R.L.; Gao, S. Composition of the continental crust. In Treatise on Geochemistry; Rudnick, R.L., Holland, H.D., Turekian, K.K., Eds.; Elsevier Pergamon: Oxford, UK, 2003; Volume 3, pp. 1–7. ISBN 0-08-043751-6. [Google Scholar]

- Liu, H. Rare Earths: Shades of Grey. Can China Continue to Fuel Our Global Clean and Smart Future. Available online: http://chinawaterrisk.org/wp-content/uploads/2016/07/CWR-Rare-Earths-Shades-Of-Grey-2016-ENG.pdf (accessed on 9 July 2017).

- Kanazawa, Y.; Kamitani, M. Rare earth minerals and resources in the world. J. Alloys Compd. 2006, 408–412, 1339–1343. [Google Scholar] [CrossRef]

- Goodenough, K.M.; Schilling, J.; Jonsson, E.; Kalvig, P.; Charles, N.; Tuduri, J.; Deady, E.A.; Sadeghi, M.; Schiellerup, H.; Müller, A.; et al. Europe’s rare earth element resource potential: An overview of REE metallogenetic provinces and their geodynamic setting. Ore Geol. Rev. 2016, 72, 838–856. [Google Scholar] [CrossRef]

- Long, K.R.; Van Gosen, B.S.; Foley, N.K.; Cordier, D. The Principal Rare Earth Elements Deposits of the United States. Available online: https://pubs.usgs.gov/sir/2010/5220/ (accessed on 16 July 2017).

- U.S. Geological Survey. Minerals Year Book—Rare Earths. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/mcs-2017-raree.pdf (accessed on 1 February 2017).

- U.S. Geological Survey. Minerals Year Book—Rare Earths. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/mcs-2011-raree.pdf (accessed on 11 May 2017).

- Kingsnorth, D. Rare Earths: Is Supply Critical in 2013? Available online: http://investorintel.com/wp-content/uploads/2013/08/AusIMM-CMC-2013-DJK-Final-InvestorIntel.pdf (accessed on 19 August 2016).

- Dutta, T.; Kim, K.H.; Uchimiya, M.; Eilhann, E.K.; Jeon, B.H.; Deep, A.; Yun, S.T. Global demand for rare earth resources and strategies for green mining. Environ. Res. 2016, 150, 182–190. [Google Scholar] [CrossRef] [PubMed]

- Rollat, A.; Guyonnet, D.; Planchon, M.; Tuduri, J. Prospective analysis of the flows of certain rare earths in Europe at the 2020 horizon. Waste Manag. 2016, 49, 427–436. [Google Scholar] [CrossRef] [PubMed]

- Weng, Z.; Jowitt, S.M.; Mudd, G.M.; Haque, N. A detailed assessment of global rare earth element resources: Opportunities and challenges. Econ. Geol. 2015, 110, 1925–1952. [Google Scholar] [CrossRef]

- Orris, G.J.; Grauch, R.I. Rare Earth Element Mines, Deposits, and Occurrences. Available online: https://pubs.usgs.gov/of/2002/of02-189/ (accessed on 8 June 2017).

- Van Gosen, B.S.; Verplanck, P.L.; Long, K.R.; Gambogi, J.; Robert, R.; Seal, I.I. The Rare-Earth Elements: Vital to Modern Technologies and Lifestyles (No. 2014–3078). Available online: https://pubs.usgs.gov/fs/2014/3078/pdf/fs2014-3078.pdf (accessed on 16 July 2017).

- Zaitsev, V.A.; Kogarko, L.N. Sources and Perspectives of REE in the Lovozero Massif (Kola Peninsula, Russia). Available online: http://meetingorganizer.copernicus.org/EMC2012/EMC2012-290.pdf (accessed on 23 March 2017).

- Global Wind Energy Outlook 2016. Available online: http://www.gwec.net/publications/global-wind-energy-outlook/global-wind-energy-outlook-2016/ (accessed on 10 August 2017).

- Lighting the Way: Perspectives on the Global Lighting Market. Available online: https://www.mckinsey.de/files/Lighting_the_way_Perspectives_on_global_lighting_market_2012.pdf (accessed on 10 August 2017).

- Executive Summary: Electric Bicycles Li-Ion and SLA E-Bikes: Drivetrain, Motor, and Battery Technology Trends, Competitive Landscape, and Global Market Forecasts. Available online: http://www.pedegoelectricbikes.com/wp-content/uploads/2016/07/MF-EBIKE-16-Executive-Summary-w-Pedego.pdf (accessed on 10 August 2017).

- Global EV Outlook 2017. Available online: https://www.iea.org/publications/freepublications/publication/GlobalEVOutlook2017.pdf (accessed on 10 August 2017).

- Battery Market Development for Consumer Electronics, Automotive, and Industrial. Available online: http://www.rechargebatteries.org/wp-content/uploads/2015/01/Avicenne-market-review-Nive-2014.pdf (accessed on 25 July 2017).

- Globalization of the Auto Industry-The Race for Competitive Advantage via Global Scale. Available online: https://ipc.mit.edu/sites/default/files/documents/00-012.pdf (accessed on 10 July 2017).

- BP Energy Outlook 2017 edition. Available online: https://www.bp.com/content/dam/bp/pdf/energy-economics/energy-outlook-2017/bp-energy-outlook-2017.pdf (accessed on 9 July 2017).

- Ku, A.Y.; Setlur, A.A.; Loudis, J. Impact of light emitting diode adoption on rare earth element use in lighting: Implications for yttrium, europium, and terbium demand. Electrochem. Soc. Interface 2015, 24, 45–49. [Google Scholar] [CrossRef]

- Report on Critical Raw Materials for the EU, Critical Raw Materials Profiles. Available online: https://ec.europa.eu/growth/sectors/raw-materials/specific-interest/critical_en (accessed on 10 August 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Wind Power (MW) | Lighting | Electric Vehicles | Batteries | Catalytic Converter | |||

|---|---|---|---|---|---|---|---|---|

| LFL | CFL | LED | Electric Cars | Electric Bicycles | NiMH Batteries | |||

| (Million Cps) | (Car) | (Battery) | (Million Cars) | |||||

| 2016 | 63,350 | 2142 | 2903 | 2675 | 750,000 | 35,000,000 | 580,125 | 95 |

| 2020 | 79,005 | 1604 | 1491 | 4828 | 2,140,0000 | 35,500,000 | 1,251,900 | 100 |

| 2025 | 76,810 | 1116 | 662 | 5874 | 7,953,375 | 36,200,000 | 715,803 | 111 |

| 2030 | 107,488 | 776 | 294 | 7146 | 29,530,323 | 37,000,000 | 2,657,729 | 117 |

| Application | La (kg) | Ce (kg) | Nd (kg) | Eu (kg) | Tb (kg) | Dy (kg) | Y (kg) |

|---|---|---|---|---|---|---|---|

| Wind turbines (/WM) | 120 | 12 | |||||

| Electric vehicles (/motor) | 0.45 | 0.075 | |||||

| Electric bicycles (/motor) | 0.038 | 0.031 | |||||

| NiMH battery (/battery) | 0.61 | 0.86 | 0.255 | ||||

| CFL (/bulb) | 0.0000765 | 0.00018 | 0.0000405 | 0.000045 | 0.000558 | ||

| LFL (/bulb) | 0.000462 | 0.000137 | 0.0000945 | 0.000105 | 0.0013 | ||

| LED (/bulb) | 0.0000004 | 0.000005 | |||||

| Catalytic converter (/auto) | 0.02 |

| Scenario | Year | Nd | Eu | Tb | Dy | TREO |

|---|---|---|---|---|---|---|

| Current | 2012 | 21,669 | 367 | 348 | 1362 | 131,100 |

| 3% annual growth rate | 2020 | 27,449 | 464 | 440 | 1725 | 166,073 |

| 2025 | 31,821 | 538 | 511 | 2000 | 192,524 | |

| 2030 | 36,890 | 624 | 592 | 2318 | 223,189 | |

| 5% annual growth rate | 2020 | 32,014 | 542 | 514 | 2012 | 193,694 |

| 2025 | 40,860 | 692 | 656 | 2568 | 247,208 | |

| 2030 | 52,149 | 883 | 837 | 3277 | 315,507 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, B.; Li, Z.; Chen, C. Global Potential of Rare Earth Resources and Rare Earth Demand from Clean Technologies. Minerals 2017, 7, 203. https://doi.org/10.3390/min7110203

Zhou B, Li Z, Chen C. Global Potential of Rare Earth Resources and Rare Earth Demand from Clean Technologies. Minerals. 2017; 7(11):203. https://doi.org/10.3390/min7110203

Chicago/Turabian StyleZhou, Baolu, Zhongxue Li, and Congcong Chen. 2017. "Global Potential of Rare Earth Resources and Rare Earth Demand from Clean Technologies" Minerals 7, no. 11: 203. https://doi.org/10.3390/min7110203

APA StyleZhou, B., Li, Z., & Chen, C. (2017). Global Potential of Rare Earth Resources and Rare Earth Demand from Clean Technologies. Minerals, 7(11), 203. https://doi.org/10.3390/min7110203