Short Value Chains in Food Production: The Role of Spatial Proximity for Economic and Land Use Dynamics

Abstract

:1. Introduction

2. Conceptual Framework

2.1. Value Creation in Food Production

2.1.1. The Spatial Perspective

2.1.2. Regional Value Creation

2.2. Spatial Proximity and Land-Use

2.2.1. Neoclassical Arguments

2.2.2. Relational Arguments

3. Material and Methods

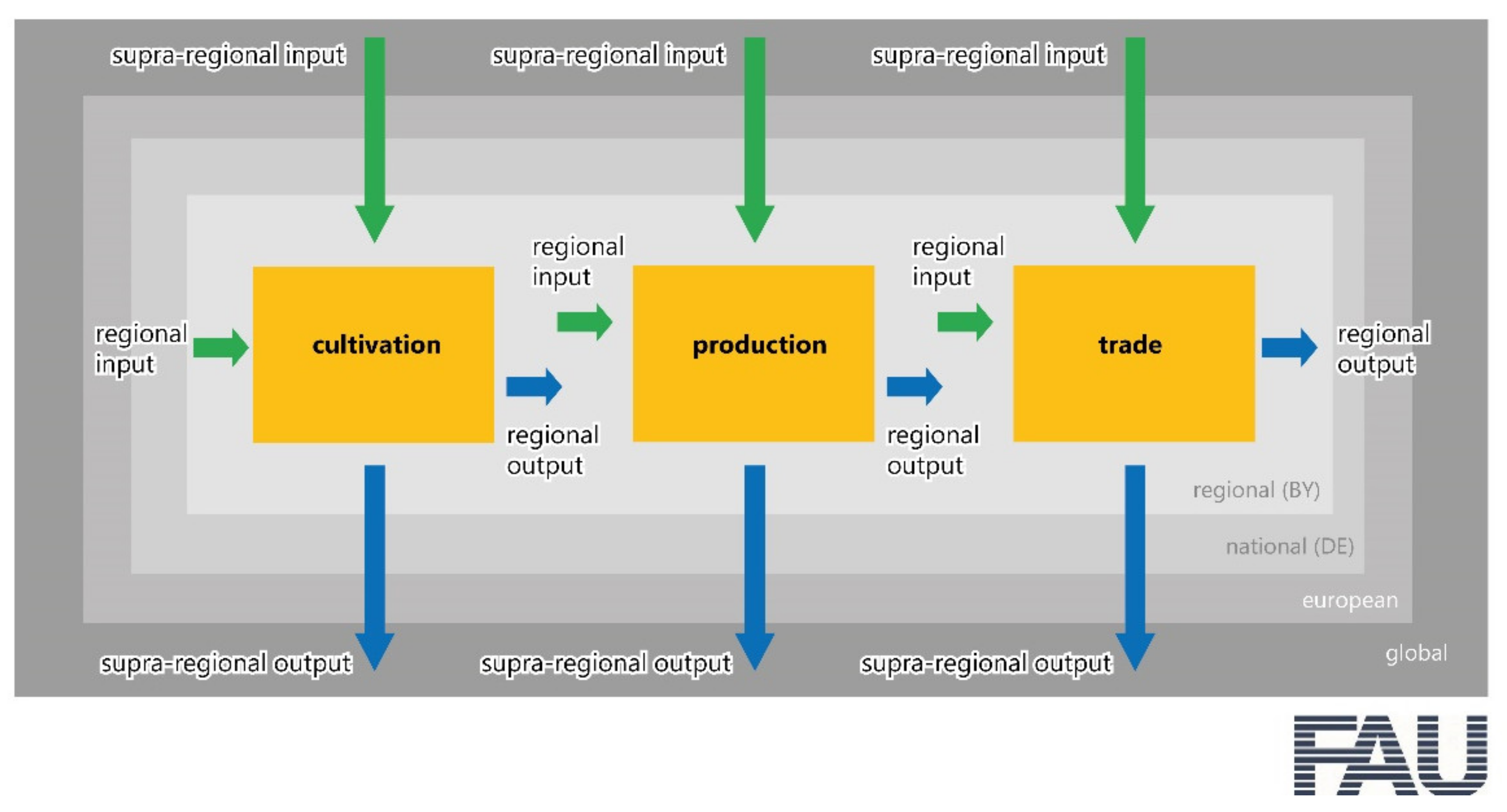

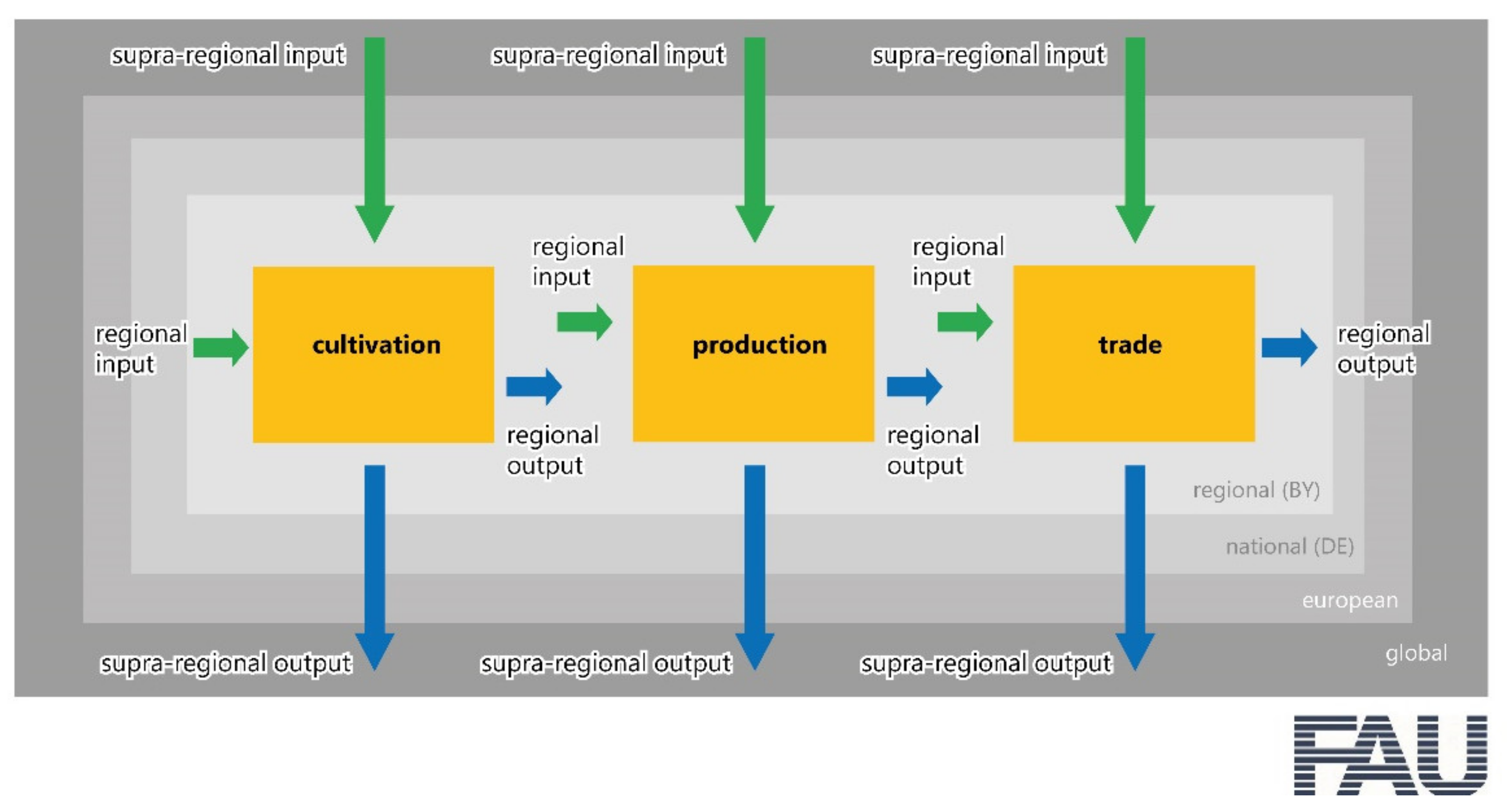

3.1. Operationalisation and Value Creation Mapping

3.2. Data Base and Quality

3.3. Expert Interviews

- Inputs and sales: differentiation of spatial scales (regional, national and international inputs and sales), shares and origin as well as destination of the purchased inputs and sales

- Value creation variables: share of intermediate inputs and gross value creation in total sales; components with highest share within intermediate consumption and gross value creation

- Market trend: assessment of the variability and trends of sales prices in Bavaria/Germany, current average sales price per product, reasons for dynamics

- Employment: proportion of employees subject to social security contributions, part time employees and seasonal employees

- Spatial relations: role of proximity to a previous or subsequent stage of the value chain

4. Results

4.1. The Spatial Dimension of Value Creation

4.1.1. Overview

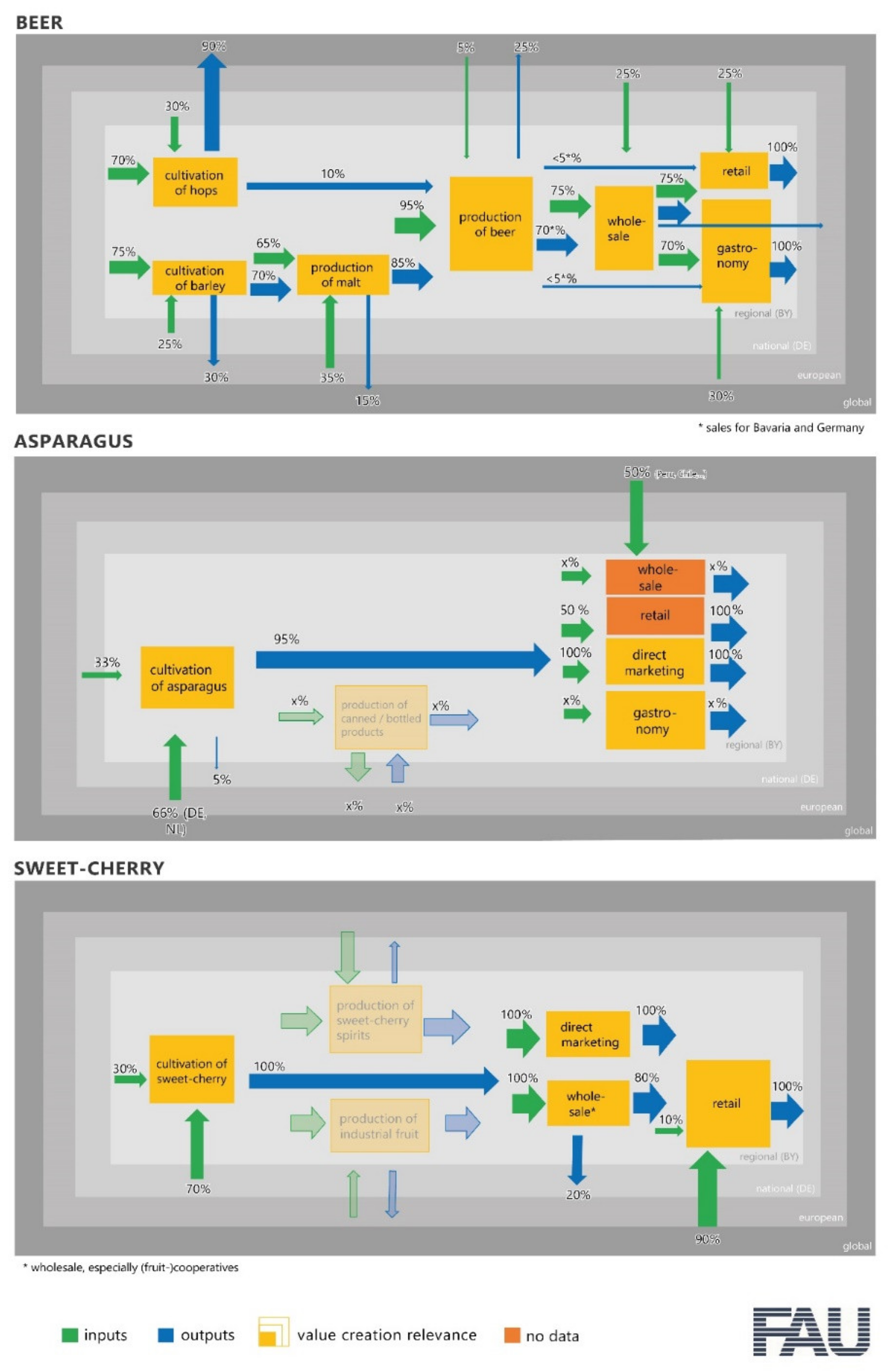

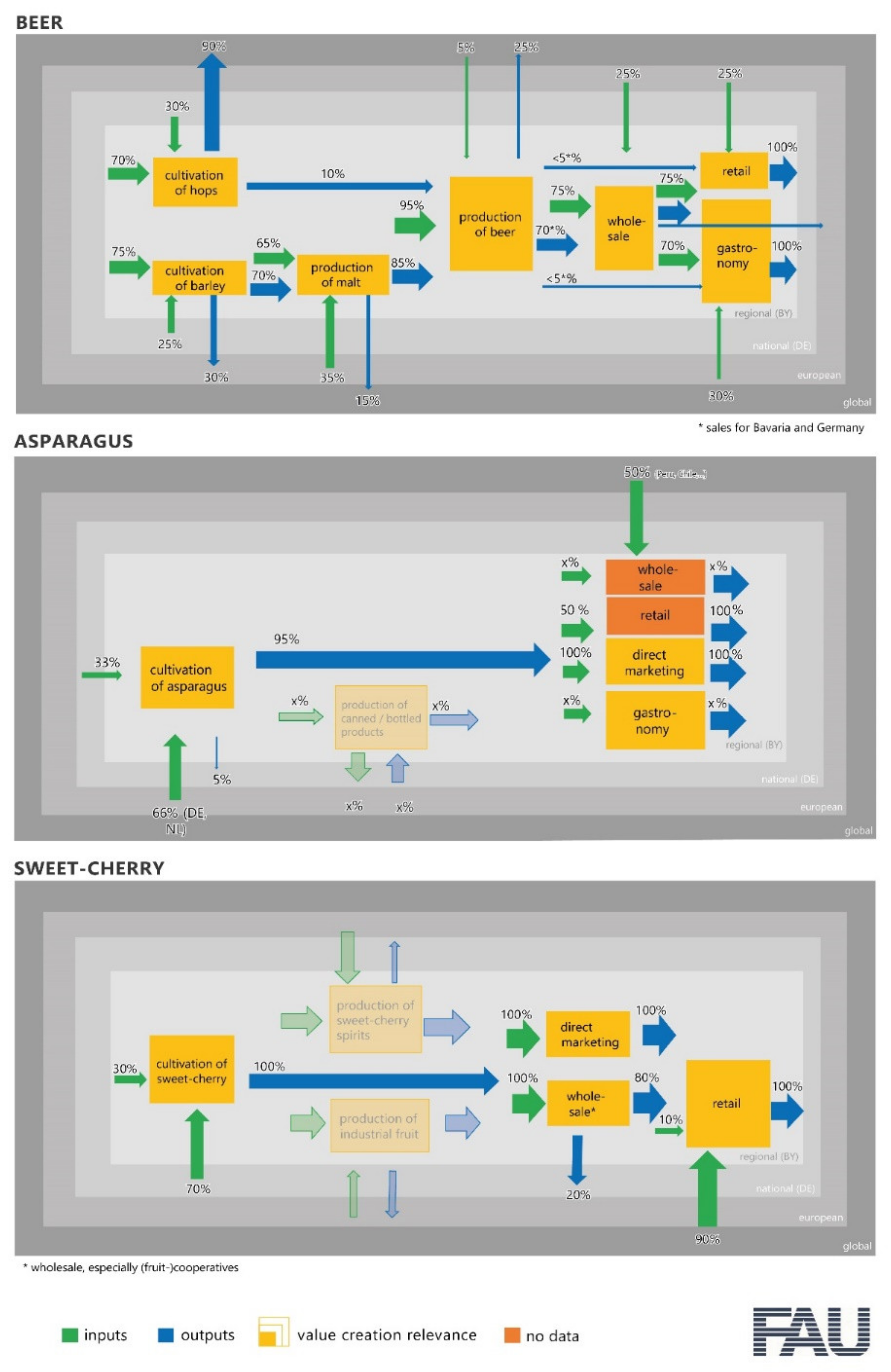

4.1.2. Beer

4.1.3. Asparagus

4.1.4. Sweet Cherry

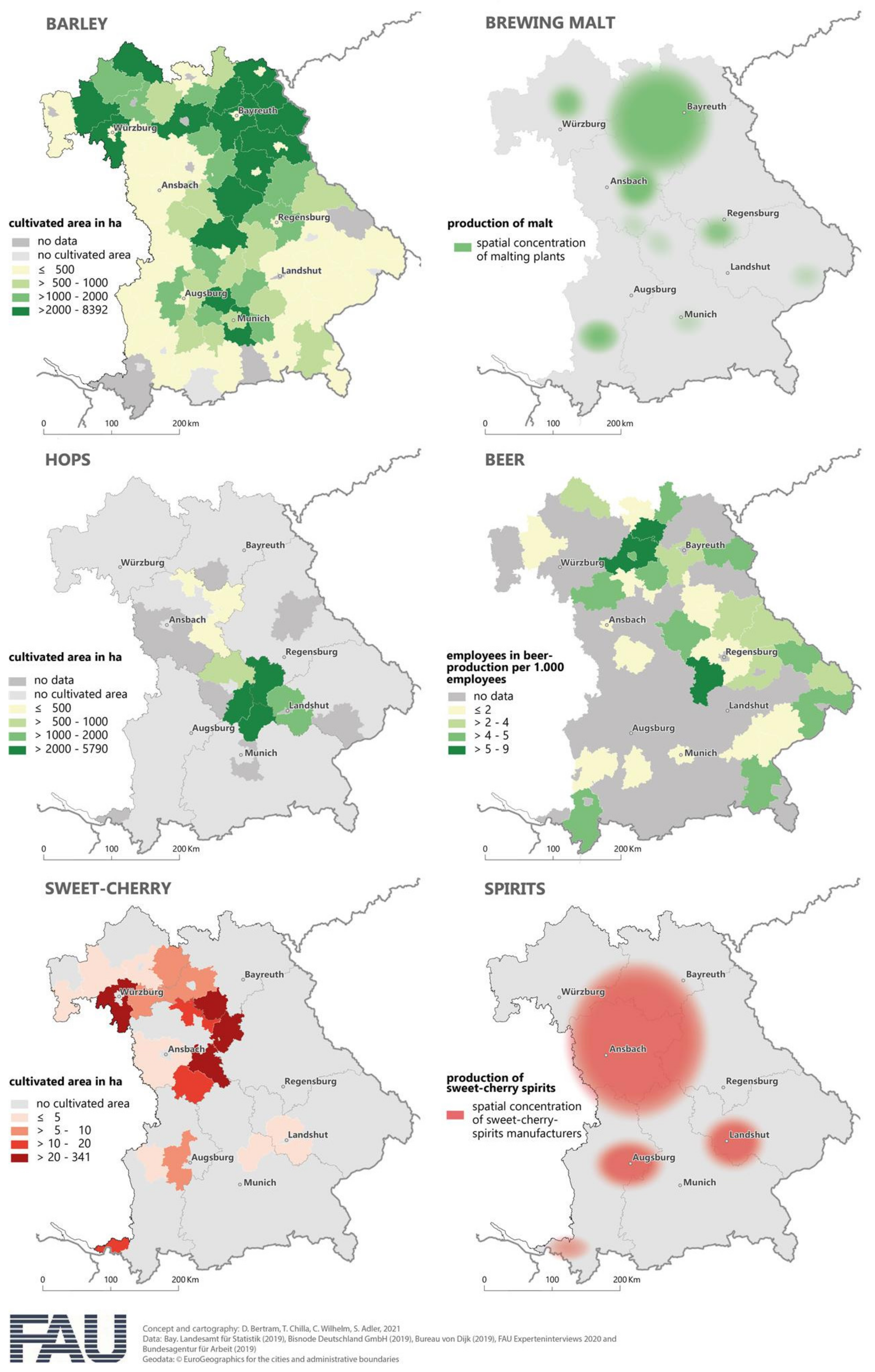

4.2. Localised Activities and Land Use Patterns

4.2.1. Overview

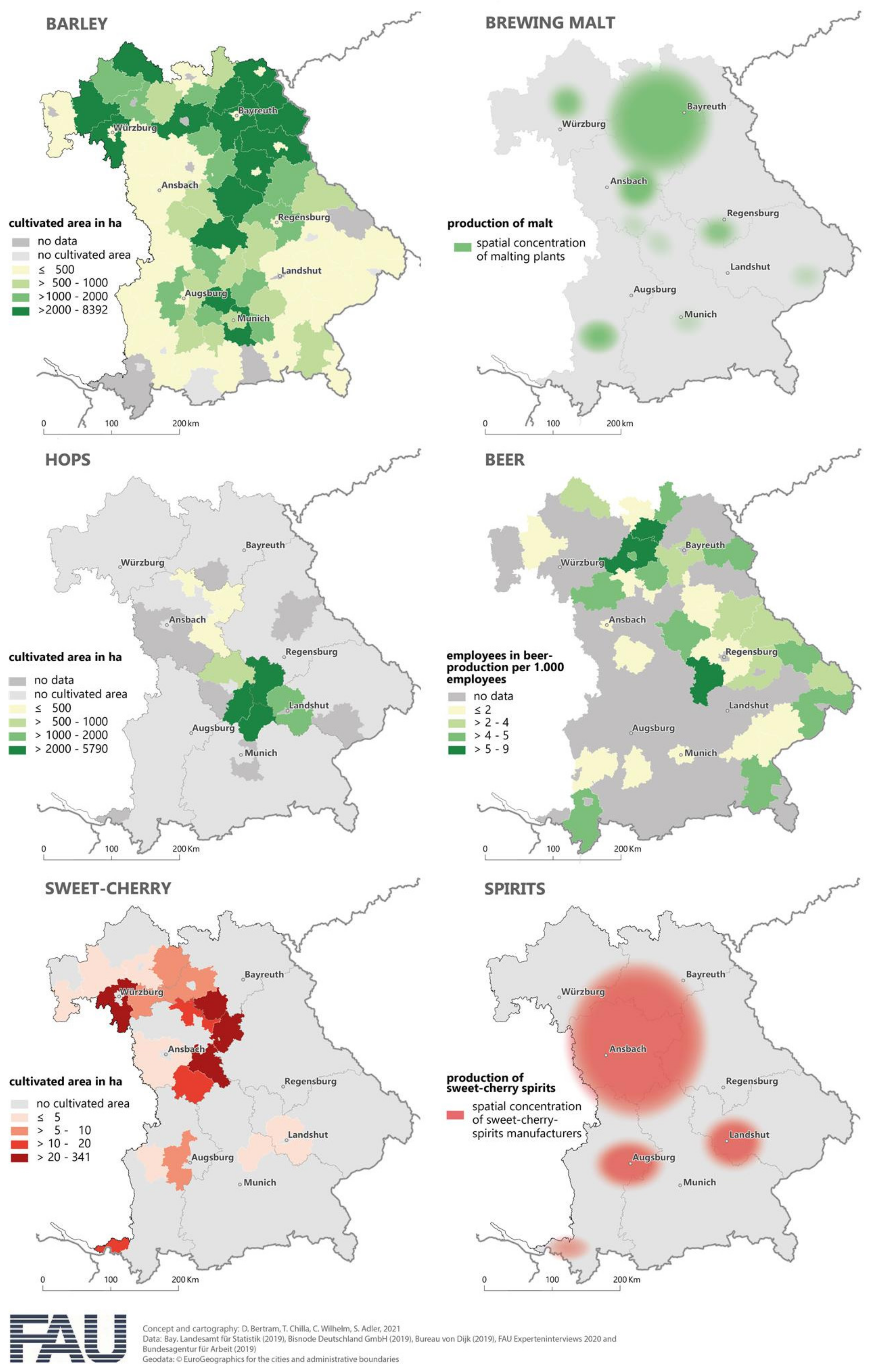

4.2.2. Beer

4.2.3. Asparagus

4.2.4. Sweet Cherry

5. Discussion

5.1. The Role of Proximity

5.2. Explanations

5.2.1. Beer

5.2.2. Asparagus

5.2.3. Sweet Cherry

5.3. Positioning of the Findings: Lessons Learned and Limitations

6. Conclusions and Outlook

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Gomes, E.; Abrantes, P.; Banos, A.; Rocha, J.; Buxton, M. Farming under urban pressure: Farmers’ land use and land cover change intentions. Appl. Geogr. 2019, 102, 58–70. [Google Scholar] [CrossRef]

- Egidi, G.; Halbac-Cotoara-Zamfir, R.; Cividino, S.; Quaranta, G.; Salvati, L.; Colantoni, A. Rural in Town: Traditional Agriculture, Population Trends, and Long-Term Urban Expansion in Metropolitan Rome. Land 2020, 9, 53. [Google Scholar] [CrossRef] [Green Version]

- Pazúr, R.; Lieskovský, J.; Bürgi, M.; Müller, D.; Lieskovský, T.; Zhang, Z.; Prishchepov, A.V. Abandonment and Recultivation of Agricultural Lands in Slovakia—Patterns and Determinants from the Past to the Future. Land 2020, 9, 316. [Google Scholar] [CrossRef]

- García-Martín, M.; Quintas-Soriano, C.; Torralba, M.; Wolpert, F.; Plieninger, T. Landscape Change in Europe. In Sustainable Land Management in a European Context; Human-Environment Interactions; Weith, T., Barkmann, T., Gaasch, N., Rogga, S., Strauß, C., Zscheischler, J., Eds.; Springer International Publishing: Basel, Switzerland, 2021; Volume 8, pp. 17–37. [Google Scholar] [CrossRef]

- Kneafsey, M.; Maye, D.; Holloway, L.; Goodman, M.K. Geographies of Food: An Introduction; Bloomsbury Publishing: London, UK, 2021. [Google Scholar]

- Cadillo-Benalcazar, J.J.; Renner, A.; Giampietro, M. A multiscale integrated analysis of the factors characterizing the sustainability of food systems in Europe. J. Environ. Manag. 2020, 271, 110944. [Google Scholar] [CrossRef] [PubMed]

- Mastronardi, L.; Marino, D.; Cavallo, A.; Giannelli, A. Exploring the Role of Farmers in Short Food Supply Chains: The Case of Italy. Int. Food Agribus. Manag. Rev. 2015, 18, 109–130. [Google Scholar] [CrossRef]

- Perito, M.A.; Coderoni, S.; Russo, C. Consumer Attitudes towards Local and Organic Food with Upcycled Ingredients: An Italian Case Study for Olive Leaves. Foods 2020, 9, 1325. [Google Scholar] [CrossRef]

- Melkonyan, A.; Gruchmann, T.; Lohmar, F.; Kamath, V.; Spinler, S. Sustainability assessment of last-mile logistics and distribution strategies: The case of local food networks. Int. J. Prod. Econ. 2020, 228, 107746. [Google Scholar] [CrossRef]

- Ditlevsen, K.; Denver, S.; Christensen, T.; Lassen, J. A taste for locally produced food—Values, opinions and sociodemographic differences among ‘organic’ and ‘conventional’ consumers. Appetite 2020, 147, 104544. [Google Scholar] [CrossRef]

- Bryła, P. Regional Ethnocentrism on the Food Market as a Pattern of Sustainable Consumption. Sustainability 2019, 11, 6408. [Google Scholar] [CrossRef] [Green Version]

- Kissinger, M.; Sussmann, C.; Dorward, C.; Mullinix, K. Local or global: A biophysical analysis of a regional food system. Renew. Agric. Food Syst. 2019, 34, 523–533. [Google Scholar] [CrossRef]

- Slámová, M.; Belčáková, I. The Role of Small Farm Activities for the Sustainable Management of Agricultural Landscapes: Case Studies from Europe. Sustainability 2019, 11, 5966. [Google Scholar] [CrossRef] [Green Version]

- Toma, I.; Redman, M.; Czekaj, M.; Tyran, E.; Grivins, M.; Sumane, S. Small-scale farming and food security—Policy perspectives from Central and Eastern Europe. Glob. Food Secur. 2021, 29, 100504. [Google Scholar] [CrossRef]

- Rivera, M.; Guarín, A.; Pinto-Correia, T.; Almaas, H.; Mur, L.A.; Burns, V.; Czekaj, M.; Ellis, R.; Galli, F.; Grivins, M.; et al. Assessing the role of small farms in regional food systems in Europe: Evidence from a comparative study. Glob. Food Secur. 2020, 26, 100417. [Google Scholar] [CrossRef]

- Béné, C. Resilience of local food systems and links to food security—A review of some important concepts in the context of COVID-19 and other shocks. Food Sec. 2020, 12, 805–822. [Google Scholar] [CrossRef]

- Thilmany, D.; Canales, E.; Low, S.A.; Boys, K. Local Food Supply Chain Dynamics and Resilience during COVID-19. Appl. Econ. Perspect. Policy 2021, 43, 86–104. [Google Scholar] [CrossRef]

- Hobbs, J.E. Food supply chains during the COVID-19 pandemic. Can. J. Agric. Econ. Rev. Can. D’agroeconomie 2020, 68, 171–176. [Google Scholar] [CrossRef] [Green Version]

- Rizou, M.; Galanakis, I.M.; Aldawoud, T.M.S.; Galanakis, C.M. Safety of foods, food supply chain and environment within the COVID-19 pandemic. Trends Food Sci. Technol. 2020, 102, 293–299. [Google Scholar] [CrossRef]

- Gardi, C.; Panagos, P.; van Liedekerke, M.; Bosco, C.; de Brogniez, D. Land take and food security: Assessment of land take on the agricultural production in Europe. J. Environ. Plan. Manag. 2015, 58, 898–912. [Google Scholar] [CrossRef]

- Ritala, P.; Tidström, A. Untangling the value-creation and value-appropriation elements of coopetition strategy: A longitudinal analysis on the firm and relational levels. Scand. J. Manag. 2014, 30, 498–515. [Google Scholar] [CrossRef]

- Schiereck, D.; Gaar, E.; Kammlott, C.; Engel, A. Ein Buchhaltungsbasiertes Konzept zur Quantifizierung Regionaler Wertschöpfung in der Lebensmittelwirtschaft; Publications of Darmstadt Technical University: Darmstadt, Germany, 2020. [Google Scholar]

- Van der Borgh, M.; Cloodt, M.; Romme, A.G.L. Value creation by knowledge-based ecosystems: Evidence from a field study. RD Manag. 2012, 42, 150–169. [Google Scholar] [CrossRef]

- Ilbery, B.; Maye, D. Alternative (Shorter) Food Supply Chains and Specialist Livestock Products in the Scottish–English Borders. Environ. Plan. A 2005, 37, 823–844. [Google Scholar] [CrossRef]

- De Roest, K.; Menghi, A. Reconsidering ‘Traditional’ Food: The Case of Parmigiano Reggiano Cheese. Sociol. Rural. 2000, 40, 439–451. [Google Scholar] [CrossRef]

- Ricciotti, F. From value chain to value network: A systematic literature review. Manag. Rev. Q. 2020, 70, 191–212. [Google Scholar] [CrossRef]

- García, E.; Mendez, A. Mañana Today: A Long View of Economic Value Creation in Latin America. Glob. Policy 2021, 12, 410–413. [Google Scholar] [CrossRef]

- Tokatli, N.; Kizilgün, Ö. Upgrading in the Global Clothing Industry: Mavi Jeans and the Transformation of a Turkish Firm from Full-Package to Brand-Name Manufacturing and Retailing. Econ. Geogr. 2004, 80, 221–240. [Google Scholar] [CrossRef]

- Song, D.-W.; Parola, F. Strategising port logistics management and operations for value creation in global supply chains. Int. J. Logist. Res. Appl. 2015, 18, 189–192. [Google Scholar] [CrossRef]

- Langford, N.J. From Global to Local Tea Markets: The Changing Political Economy of Tea Production within India’s Domestic Value Chain. Dev. Chang. 2021. [Google Scholar] [CrossRef]

- Feyaerts, H.; van den Broeck, G.; Maertens, M. Global and local food value chains in Africa: A review. Agric. Econ. 2020, 51, 143–157. [Google Scholar] [CrossRef]

- Trienekens, J.; van Velzen, M.; Lees, N.; Saunders, C.; Pascucci, S. Governance of market-oriented fresh food value chains: Export chains from New Zealand. Int. Food Agribus. Manag. Rev. 2018, 21, 249–268. [Google Scholar] [CrossRef]

- Aubry, C.; Kebir, L. Shortening food supply chains: A means for maintaining agriculture close to urban areas? The case of the French metropolitan area of Paris. Food Policy 2013, 41, 85–93. [Google Scholar] [CrossRef]

- Mundler, P.; Laughrea, S. The contributions of short food supply chains to territorial development: A study of three Quebec territories. J. Rural. Stud. 2016, 45, 218–229. [Google Scholar] [CrossRef]

- Elghannam, A.; Mesias, F.J.; Escribano, M.; Fouad, L.; Horrillo, A.; Escribano, A.J. Consumers’ Perspectives on Alternative Short Food Supply Chains Based on Social Media: A Focus Group Study in Spain. Foods 2020, 9, 22. [Google Scholar] [CrossRef] [Green Version]

- Thomé, K.M.; Cappellesso, G.; Ramos, E.L.A.; de Lima Duarte, S.C. Food Supply Chains and Short Food Supply Chains: Coexistence conceptual framework. J. Clean. Prod. 2021, 278, 123207. [Google Scholar] [CrossRef]

- Charatsari, C.; Kitsios, F.; Lioutas, E.D. Short food supply chains: The link between participation and farmers’ competencies. Renew. Agric. Food Syst. 2020, 35, 643–652. [Google Scholar] [CrossRef]

- Chiffoleau, Y.; Dourian, T. Sustainable Food Supply Chains: Is Shortening the Answer? A Literature Review for a Research and Innovation Agenda. Sustainability 2020, 12, 9831. [Google Scholar] [CrossRef]

- Kneafsey, M.; Venn, L.; Schmutz, U.; Balasz, B.; Trenchard, L.; Eyden-Wood, T.; Bos, E.; Sutton, G.; Blackett, M.; Santini, F.; et al. Short Food Supply Chains and Local Food Systems in the EU: A State of Play of Their Socio Economic Characteristics; European Commission: Brussels, Belgium; Joint Research Centre: Ispra, Italy; Institute for Prospective Technological Studies: Seville, Spain, 2013. [Google Scholar] [CrossRef]

- Mundler, P.; Jean-Gagnon, J. Short food supply chains, labor productivity and fair earnings: An impossible equation? Renew. Agric. Food Syst. 2020, 35, 697–709. [Google Scholar] [CrossRef]

- Dupuis, E.M.; Goodman, D. Should we go “home” to eat?: Toward a reflexive politics of localism. J. Rural. Stud. 2005, 21, 359–371. [Google Scholar] [CrossRef]

- Duram, L.; Oberholtzer, L. A geographic approach to place and natural resource use in local food systems. Renew. Agric. Food Syst. 2010, 25, 99–108. [Google Scholar] [CrossRef] [Green Version]

- Ostrom, M. Everyday Meanings of “Local Food”: Views from Home and Field. Community Dev. 2006, 37, 65–78. [Google Scholar] [CrossRef]

- Cvijanović, D.; Ignjatijević, S.; Vapa, T.J.; Cvijanović, V. Do Local Food Products Contribute to Sustainable Economic Development? Sustainability 2020, 12, 2847. [Google Scholar] [CrossRef] [Green Version]

- Marsden, T.; Banks, J.; Bristow, G. Food Supply Chain Approaches: Exploring their Role in Rural Development. Sociol. Rural. 2000, 40, 424–438. [Google Scholar] [CrossRef]

- Renting, H.; Marsden, T.K.; Banks, J. Understanding Alternative Food Networks: Exploring the Role of Short Food Supply Chains in Rural Development. Environ. Plan. A 2003, 35, 393–411. [Google Scholar] [CrossRef] [Green Version]

- Barham, E. Translating terroir: The global challenge of French AOC labeling. J. Rural. Stud. 2003, 19, 127–138. [Google Scholar] [CrossRef]

- Mancini, M.C.; Menozzi, D.; Donati, M.; Biasini, B.; Veneziani, M.; Arfini, F. Producers’ and Consumers’ Perception of the Sustainability of Short Food Supply Chains: The Case of Parmigiano Reggiano PDO. Sustainability 2019, 11, 721. [Google Scholar] [CrossRef] [Green Version]

- Chilla, T.; Fink, B.; Balling, R.; Reitmeier, S.; Schober, K. The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension. Sustainability 2020, 12, 5503. [Google Scholar] [CrossRef]

- Blake, M.K.; Mellor, J.; Crane, L. Buying Local Food: Shopping Practices, Place, and Consumption Networks in Defining Food as “Local”. Ann. Assoc. Am. Geogr. 2010, 100, 409–426. [Google Scholar] [CrossRef]

- Cushing, N. Counting the food miles of sugar in early colonial Australia. Food Foodways 2020, 28, 195–214. [Google Scholar] [CrossRef]

- Morris, C.; Buller, H. The local food sector: A preliminary assessment of its form and impact in Gloucestershire. Br. Food J. 2003, 105, 559–566. [Google Scholar] [CrossRef]

- Jarzębowski, S.; Bourlakis, M.; Bezat-Jarzębowska, A. Short Food Supply Chains (SFSC) as Local and Sustainable Systems. Sustainability 2020, 12, 4715. [Google Scholar] [CrossRef]

- Feagan, R. The place of food: Mapping out the ‘local’ in local food systems. Prog. Hum. Geogr. 2007, 31, 23–42. [Google Scholar] [CrossRef] [Green Version]

- Kwil, I.; Piwowar-Sulej, K.; Krzywonos, M. Local Entrepreneurship in the Context of Food Production: A Review. Sustainability 2020, 12, 424. [Google Scholar] [CrossRef] [Green Version]

- Kurznack, L.; Schoenmaker, D.; Schramade, W. A model of long-term value creation. J. Sustain. Financ. Investig. 2021, 1–19. [Google Scholar] [CrossRef]

- Signori, S.; San-Jose, L.; Retolaza, J.L.; Rusconi, G. Stakeholder Value Creation: Comparing ESG and Value Added in European Companies. Sustainability 2021, 13, 1392. [Google Scholar] [CrossRef]

- Brozović, D.; D’Auria, A.; Tregua, M. Value Creation and Sustainability: Lessons from Leading Sustainability Firms. Sustainability 2020, 12, 4450. [Google Scholar] [CrossRef]

- Esposito, P.; Brescia, V.; Fantauzzi, C.; Frondizi, R. Understanding Social Impact and Value Creation in Hybrid Organizations: The Case of Italian Civil Service. Sustainability 2021, 13, 4058. [Google Scholar] [CrossRef]

- Ritala, P.; Albareda, L.; Bocken, N. Value creation and appropriation in economic, social, and environmental domains: Recognizing and resolving the institutionalized asymmetries. J. Clean. Prod. 2021, 290, 125796. [Google Scholar] [CrossRef]

- Bowman, C.; Ambrosini, V. Value Creation Versus Value Capture: Towards a Coherent Definition of Value in Strategy. Br. J. Manag. 2000, 11, 1–15. [Google Scholar] [CrossRef]

- Sadovska, V.; Ekelund Axelson, L.; Mark-Herbert, C. Reviewing Value Creation in Agriculture—A Conceptual Analysis and a New Framework. Sustainability 2020, 12, 5021. [Google Scholar] [CrossRef]

- Sjödin, D.; Parida, V.; Jovanovic, M.; Visnjic, I. Value Creation and Value Capture Alignment in Business Model Innovation: A Process View on Outcome-Based Business Models. J. Prod. Innov. Manag. 2020, 37, 158–183. [Google Scholar] [CrossRef] [Green Version]

- Grabs, J.; Ponte, S. The evolution of power in the global coffee value chain and production network. J. Econ. Geogr. 2019, 19, 803–828. [Google Scholar] [CrossRef]

- Dicken, P. The Roepke Lecture in Economic Geography Global-Local Tensions: Firms and States in the Global Space-Economy. Econ. Geogr. 1994, 70, 101. [Google Scholar] [CrossRef]

- Gereffi, G.; Korzeniewicz, M. Commodity chains and global capitalism. In Studies in the Political Economy of the World-System; Greenwood Press: Westport, CT, USA, 1994. [Google Scholar]

- Bair, J.; Werner, M. Commodity Chains and the Uneven Geographies of Global Capitalism: A Disarticulations Perspective. Environ. Plan. A 2011, 43, 988–997. [Google Scholar] [CrossRef] [Green Version]

- Dicken, P.; Kelly, P.F.; Olds, K.; Wai-Chung Yeung, H. Chains and networks, territories and scales: Towards a relational framework for analysing the global economy. Glob. Netw. 2001, 1, 89–112. [Google Scholar] [CrossRef]

- Coe, N.M.; Hess, M.; Yeung, H.W.-C.; Dicken, P.; Henderson, J. ‘Globalizing’ regional development: A global production networks perspective. Trans. Inst. Br. Geogr. 2004, 29, 468–484. [Google Scholar] [CrossRef]

- Coe, N.M.; Yeung, H.W.-C. (Eds.) Global Production Networks. Theorizing Economic Development in an Interconnected World; Oxford University Press: Oxford, UK, 2015. [Google Scholar]

- Yeung, H.W. Regional worlds: From related variety in regional diversification to strategic coupling in global production networks. Reg. Stud. 2021, 55, 989–1010. [Google Scholar] [CrossRef]

- Alford, M.; Visser, M.; Barrientos, S. Southern actors and the governance of labour standards in global production networks: The case of South African fruit and wine. Environ. Plan. A 2021, 0308518X2110333. [Google Scholar] [CrossRef]

- Dannenberg, P.; Braun, B.; Kulke, E. The paradox of formalization and informalization in South-North value chains. DIE ERDE-J. Geogr. Soc. Berl. 2016, 147, 173–186. [Google Scholar] [CrossRef]

- Malak-Rawlikowska, A.; Majewski, E.; Wąs, A.; Borgen, S.O.; Csillag, P.; Donati, M.; Freeman, R.; Hoàng, V.; Lecoeur, J.-L.; Mancini, M.C.; et al. Measuring the Economic, Environmental, and Social Sustainability of Short Food Supply Chains. Sustainability 2019, 11, 4004. [Google Scholar] [CrossRef] [Green Version]

- Lopez-Morales, E. Gentrification by Ground Rent Dispossession: The Shadows Cast by Large-Scale Urban Renewal in Santiago de Chile. Int. J. Urban Reg. Res. 2011, 35, 330–357. [Google Scholar] [CrossRef]

- Swyngedouw, E. Rent and landed property. In The Elgar Companion to Marxist Economics; Edward Elgar Publishing: Cheltenham, UK, 2012. [Google Scholar]

- Andreucci, D.; García-Lamarca, M.; Wedekind, J.; Swyngedouw, E. “Value Grabbing”: A Political Ecology of Rent. Capital. Nat. Soc. 2017, 28, 28–47. [Google Scholar] [CrossRef]

- Smith, N. Gentrification and the Rent Gap. Ann. Assoc. Am. Geogr. 1987, 77, 462–465. [Google Scholar] [CrossRef]

- Krijnen, M. Beirut and the creation of the rent gap. Urban Geogr. 2018, 39, 1041–1059. [Google Scholar] [CrossRef]

- Wachsmuth, D.; Weisler, A. Airbnb and the rent gap: Gentrification through the sharing economy. Environ. Plan. A 2018, 50, 1147–1170. [Google Scholar] [CrossRef]

- Wang, K.-C. The art of rent: The making of edamame monopoly rents in East Asia. Environ. Plan. E Nat. Space 2020, 3, 624–641. [Google Scholar] [CrossRef]

- Clark, E. The Rent Gap Re-examined. Urban Stud. 1995, 32, 1489–1503. [Google Scholar] [CrossRef]

- Slater, T. Clarifying Neil Smith’s Rent Gap Theory of Gentrification. Tracce Urbane 2017, 1, 83–101. [Google Scholar] [CrossRef]

- Guiomar, N.; Godinho, S.; Pinto-Correia, T.; Almeida, M.; Bartolini, F.; Bezák, P.; Biró, M.; Bjørkhaug, H.; Bojnec, Š.; Brunori, G.; et al. Typology and distribution of small farms in Europe: Towards a better picture. Land Use Policy 2018, 75, 784–798. [Google Scholar] [CrossRef]

- O’Callaghan, J.R. Land Use: The Interaction of Economics, Ecology and Hydrology, 1st ed.; Chapman & Hall: London, UK, 1996. [Google Scholar]

- Alonso, W. (Ed.) Location and Land Use: Toward a General Theory of Land Rent; Publications of the Joint Center for Urban Studies of the Massachusetts Institute of Technology and Harvard University; Harvard University Press: Cambridge, CA, USA, 1964. [Google Scholar] [CrossRef]

- Wójcik-Leń, J.; Sobolewska-Mikulska, K.; Sajnóg, N.; Leń, P. The idea of rational management of problematic agricultural areas in the course of land consolidation. Land Use Policy 2018, 78, 36–45. [Google Scholar] [CrossRef]

- Colsaet, A.; Laurans, Y.; Levrel, H. What drives land take and urban land expansion? A systematic review. Land Use Policy 2018, 79, 339–349. [Google Scholar] [CrossRef]

- Fujita, M.; Krugman, P. When is the economy monocentric?: Von Thünen and Chamberlin unified. Reg. Sci. Urban Econ. 1995, 25, 505–528. [Google Scholar] [CrossRef]

- Meyfroidt, P.; Roy Chowdhury, R.; de Bremond, A.; Ellis, E.C.; Erb, K.-H.; Filatova, T.; Garrett, R.D.; Grove, J.M.; Heinimann, A.; Kuemmerle, T.; et al. Middle-range theories of land system change. Glob. Environ. Chang. 2018, 53, 52–67. [Google Scholar] [CrossRef]

- De Roest, K.; Ferrari, P.; Knickel, K. Specialisation and economies of scale or diversification and economies of scope? Assessing different agricultural development pathways. J. Rural. Stud. 2018, 59, 222–231. [Google Scholar] [CrossRef]

- Farhauer, O.; Kröll, A. Das Cluster- und Netzwerkkonzept. In Standorttheorien: Regional-Und Stadtökonomik in Theorie Und Praxis; Farhauer, O., Kröll, A., Eds.; Springer Gabler: Wiesbaden, Germany, 2013; pp. 145–189. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage, Agglomeration Economies, and Regional Policy. Int. Reg. Sci. Rev. 1996, 19, 85–90. [Google Scholar] [CrossRef]

- Genosko, J. Networks, innovative milieux and globalization: Some comments on a regional economic discussion. Eur. Plan. Stud. 1997, 5, 283–297. [Google Scholar] [CrossRef]

- Calignano, G.; Fitjar, R.D.; Kogler, D.F. The core in the periphery? The cluster organization as the central node in the Apulian aerospace district. Reg. Stud. 2018, 52, 1490–1501. [Google Scholar] [CrossRef]

- Ron, A.B.; Jan, G. Lambooy. Evolutionary economics and economic geography. J. Evol Econ. 1999, 9, 411–429. [Google Scholar] [CrossRef]

- Broekel, T.; Boschma, R. The cognitive and geographical structure of knowledge links and how they influence firms’ innovation performance. Reg. Stat. 2016, 6, 3–26. [Google Scholar] [CrossRef]

- Miguelez, E.; Moreno, R. Networks, Diffusion of Knowledge, and Regional Innovative Performance. Int. Reg. Sci. Rev. 2017, 40, 331–336. [Google Scholar] [CrossRef] [Green Version]

- Dümmler, P.; Thierstein, A. Identifying and Managing Clusters—Evidence from Switzerland. In Entrepreneurship, Spatial Industrial Clusters and Inter-Firm Networks—Uddevalla Symposium; Routledge: London, UK, 2003. [Google Scholar]

- Glückler, J. Geography of Reputation: The City as the Locus of Business Opportunity. Reg. Stud. 2007, 41, 949–961. [Google Scholar] [CrossRef] [Green Version]

- Gergaud, O.; Livat, F.; Rickard, B.; Warzynski, F. Evaluating the net benefits of collective reputation: The case of Bordeaux wine. Food Policy 2017, 71, 8–16. [Google Scholar] [CrossRef]

- Howells, J.R.L. Tacit Knowledge, Innovation and Economic Geography. Urban Stud. 2002, 39, 871–884. [Google Scholar] [CrossRef]

- Pérez-Luño, A.; Alegre, J.; Valle-Cabrera, R. The role of tacit knowledge in connecting knowledge exchange and combination with innovation. Technol. Anal. Strateg. Manag. 2019, 31, 186–198. [Google Scholar] [CrossRef]

- Boschma, R. Editorial: Role of Proximity in Interaction and Performance: Conceptual and Empirical Challenges. Reg. Stud. 2005, 39, 41–45. [Google Scholar] [CrossRef]

- Šūmane, S.; Kunda, I.; Knickel, K.; Strauss, A.; Tisenkopfs, T.; Des Rios, I.I.; Rivera, M.; Chebach, T.; Ashkenazy, A. Local and farmers’ knowledge matters! How integrating informal and formal knowledge enhances sustainable and resilient agriculture. J. Rural. Stud. 2018, 59, 232–241. [Google Scholar] [CrossRef]

- Fang, L.; Drucker, J. How Spatially Concentrated Are Industrial Clusters?: A Meta-analysis. J. Plan. Lit. 2021, 088541222110129. [Google Scholar] [CrossRef]

- Perraton, J.; Tarrant, I. What does tacit knowledge actually explain? J. Econ. Methodol. 2007, 14, 353–370. [Google Scholar] [CrossRef]

- Isaksen, A. Regional Clusters Building on Local and Non-Local Relationships: A European Comparison. In Proximity, Distance and Diversity; Routledge: London, UK, 2017; pp. 129–151. [Google Scholar] [CrossRef]

- Sternberg, R.; Litzenberger, T. Regional clusters in Germany--their geography and their relevance for entrepreneurial activities. Eur. Plan. Stud. 2004, 12, 767–791. [Google Scholar] [CrossRef]

- Belussi, F. New perspectives on the evolution of clusters. Eur. Plan. Stud. 2018, 26, 1796–1814. [Google Scholar] [CrossRef]

- Bellandi, M.; Propris, L.D.; Vecciolini, C. Effects of learning, unlearning and forgetting on path development: The case of the Macerata-Fermo footwear industrial districts. Eur. Plan. Stud. 2021, 29, 259–276. [Google Scholar] [CrossRef]

- Chapain, C.; Sagot-Duvauroux, D. Cultural and creative clusters—A systematic literature review and a renewed research agenda. Urban Res. Pract. 2020, 13, 300–329. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Grant, R.M. The Resource-Based Theory of Competitive Advantage: Implications for Strategy Formulation. Calif. Manag. Rev. 1991, 33, 114–135. [Google Scholar] [CrossRef] [Green Version]

- Kamasak, R. The contribution of tangible and intangible resources, and capabilities to a firm’s profitability and market performance. Eur. J. Manag. Bus. Econ. 2017, 26, 252–275. [Google Scholar] [CrossRef] [Green Version]

- Quélin, B. Core competencies, R&D management and partnerships. Eur. Manag. J. 2000, 18, 476–487. [Google Scholar]

- Pechlaner, H.; Fischer, E.; Hammann, E.-M. Leadership and Innovation Processes—Development of Products and Services Based on Core Competencies. J. Qual. Assur. Hosp. Tour. 2006, 6, 31–57. [Google Scholar] [CrossRef]

- Malmberg, A.; Maskell, P. An Evolutionary Approach to Localized Learning and Spatial Clustering. Handb. Evol. Econ. Geogr. 2010, 391–405. [Google Scholar]

- Vanhaverbeke, W. Realizing new regional core competencies: Establishing a customer-oriented SME network. Entrep. Reg. Dev. 2001, 13, 97–116. [Google Scholar] [CrossRef]

- Keeble, D. Collective Learning Processes in European High-Technology Milieux. In High-Technology Clusters, Networking and Collective Learning in Europe; Routledge: London, UK, 2017; pp. 199–229. [Google Scholar] [CrossRef]

- Lawson, C. Collective Learning, System Competences and Epistemically Significant Moments. In High-Technology Clusters, Networking and Collective Learning in Europe; Routledge: London, UK, 2017; pp. 182–198. [Google Scholar] [CrossRef]

- Rivera, L.; Sheffi, Y.; Knoppen, D. Logistics clusters: The impact of further agglomeration, training and firm size on collaboration and value added services. Int. J. Prod. Econ. 2016, 179, 285–294. [Google Scholar] [CrossRef]

- Purcell, S.W.; Crona, B.I.; Lalavanua, W.; Eriksson, H. Distribution of economic returns in small-scale fisheries for international markets: A value-chain analysis. Mar. Policy 2017, 86, 9–16. [Google Scholar] [CrossRef]

- Flanagan, D.J.; Lepisto, D.A.; Ofstein, L.F. Coopetition among nascent craft breweries: A value chain analysis. J. Small Bus. Entrep. Dev. 2018, 25, 2–16. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Topic | Sources |

|---|---|

| Agricultural area und land use |

|

| Input Costs (cultivation stage) |

|

| Agricultural returns |

|

| Employment and business |

|

| Processing |

|

| Sales and trades |

|

| Proximity … | Market Trend | Land Use Trend | |

|---|---|---|---|

| Beer | …of hop, barley, malting plants, breweries, “Proximity for export“ | Stable to positive (due to strategy internationalization of regional specificity and export growth) | Stable |

| Asparagus | …of cultivation and sales “Field to plate proximity“ | Positive (due to technological development) | Positive |

| Sweet cherry | …of cultivation, distillery and sales “tree-to-plate-and-glass-proximity“ | Negative (decreasing competitiveness due to lacking innovation/adaptation) | Stable to negative |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bertram, D.; Chilla, T.; Wilhelm, C. Short Value Chains in Food Production: The Role of Spatial Proximity for Economic and Land Use Dynamics. Land 2021, 10, 979. https://doi.org/10.3390/land10090979

Bertram D, Chilla T, Wilhelm C. Short Value Chains in Food Production: The Role of Spatial Proximity for Economic and Land Use Dynamics. Land. 2021; 10(9):979. https://doi.org/10.3390/land10090979

Chicago/Turabian StyleBertram, Dominik, Tobias Chilla, and Carola Wilhelm. 2021. "Short Value Chains in Food Production: The Role of Spatial Proximity for Economic and Land Use Dynamics" Land 10, no. 9: 979. https://doi.org/10.3390/land10090979

APA StyleBertram, D., Chilla, T., & Wilhelm, C. (2021). Short Value Chains in Food Production: The Role of Spatial Proximity for Economic and Land Use Dynamics. Land, 10(9), 979. https://doi.org/10.3390/land10090979