3.2. Location, Size, Age, and Objectives of the Facility

Among the 140 identified structures, most aquaponic activities took place in France (37.1%, n = 52), followed by Belgium (10.7%, n = 15), Germany, and the UK (7.8%, n = 11 each) for a total of 25 countries.

Our panel of respondents was representative of the geographic distribution of the total number of structures, with 41.3% (

n = 19) of respondents in France, followed by Belgium (19.6%,

n = 9). Germany, Sweden, The Netherlands, and the United Kingdom had 4.3% (

n = 2) respondents each. Austria, Czechia, Greece, Italy, Lithuania, Portugal, Slovakia, Slovenia, Spain, and Swiitzerland had one respondent each. The fact that this study was mainly conducted in English and French and was partially delivered through local networks could explain the high participation of French and Belgian entities. However, the distribution of the aquaponic systems identified here reflects the findings of previous studies [

26].

Despite the promotion of the benefits of aquaponic systems in urban environments [

39], it was surprising to notice that aquaponic systems were very evenly distributed among urban (30.4%,

n = 14), peri-urban (34.8%,

n = 16), and rural (34.8%,

n = 16) areas. Different markets apply to these different zones, suggesting a high degree of variability in the design and management of aquaponic systems.

Among the 46 entities, 13.0% (

n = 6) were non-profit. The education sector, including primary and secondary schools, training centers, universities, and research centers represented 26.1% (

n = 12) of the entities. The remaining 60.9% (

n = 28) combined production, retail, and consulting activities and will be regarded as “professionals” henceforth. Professional activities clearly increased compared to previous studies. In a study conducted in 2016, only 19.1% of the respondents identified themselves as commercial structures, 51.4% were educational structures, and 14.7% were NPOs [

26].

The oldest aquaponics system of our panel was created in 2009 (

Figure 2). Half of our panel created its aquaponics system between 2011 and 2017. Interestingly, 15 systems were created in 2018. The first two professional systems were created in 2012 in the United Kingdom and Spain. The third and fourth professional systems were created in 2015, one in France and one in Belgium. Professional aquaponic systems started appearing in higher numbers after 2015. This may reveal that many new professional aquaponics entities were created after 2015 or were an artefact in the representativeness of our panel, as new entities may be more motivated than older ones to contribute to such studies.

The survey investigated the main purposes of the entities (

Figure 3). The commercial aspect and financial gain were very important in all projects. This is particularly interesting, because it contrasts with the result of the survey by Turnšek et al. [

21], where only 36% of the respondents claimed choosing aquaponics for “having a higher economic potential”. The main differences between the panels were that (i) our panel only includes infrastructure with actual aquaponic systems, (ii) the panel of Turnšek et al. [

21] included early enthusiasts who invested time and money in aquaponic activities, and (iii) the study by Turnšek et al. [

21] was conducted in 2017, whereas the present study was conducted in 2019–2020. This reveals that the respondent’s conviction for financially viable aquaponic activities was lower in previous studies. “Innovative food production systems” and “Environmental durability” were important or very important for, respectively, 93.5% (

n = 43) and 95.7% (

n = 44) of the respondents. Then came, by decreasing order of importance, “Research and development”, “Improve food nutritional quality and taste”, “Local consumption”, “Subsistence (food security)”, “Recreation”, “Consultancy”, and “Social integration”. This is in accordance with the observations of Turnšek et al. [

21]. “Customary land use” was not a main concern for the majority of the respondents: 63.0% (

n = 29). This is a surprising result as it was previously understood that aquaponics was particularly adapted to areas not suitable for other food production techniques, for example, polluted areas, cities, and rooftops [

11,

40].

3.3. Design, Production, and Techniques

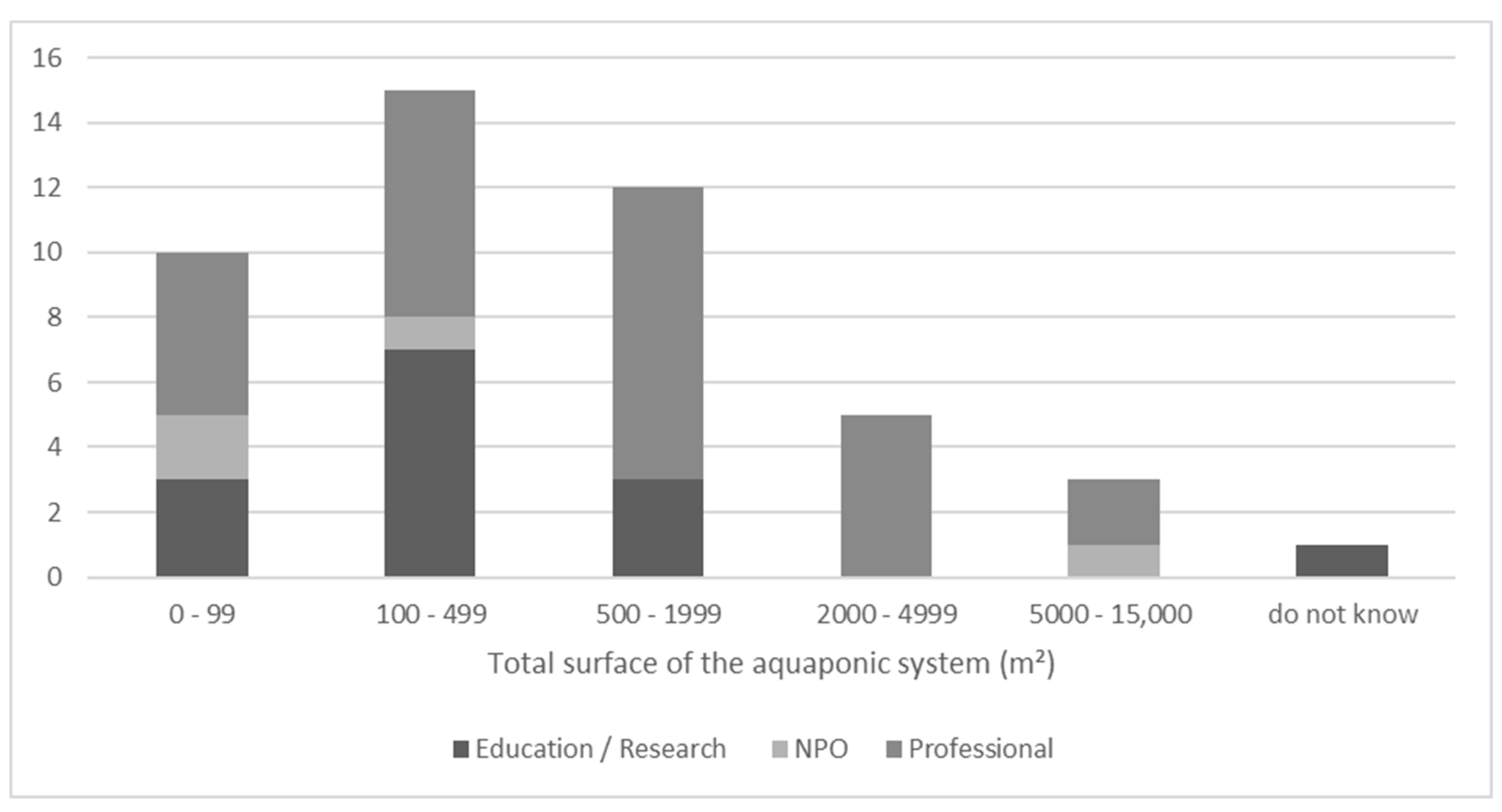

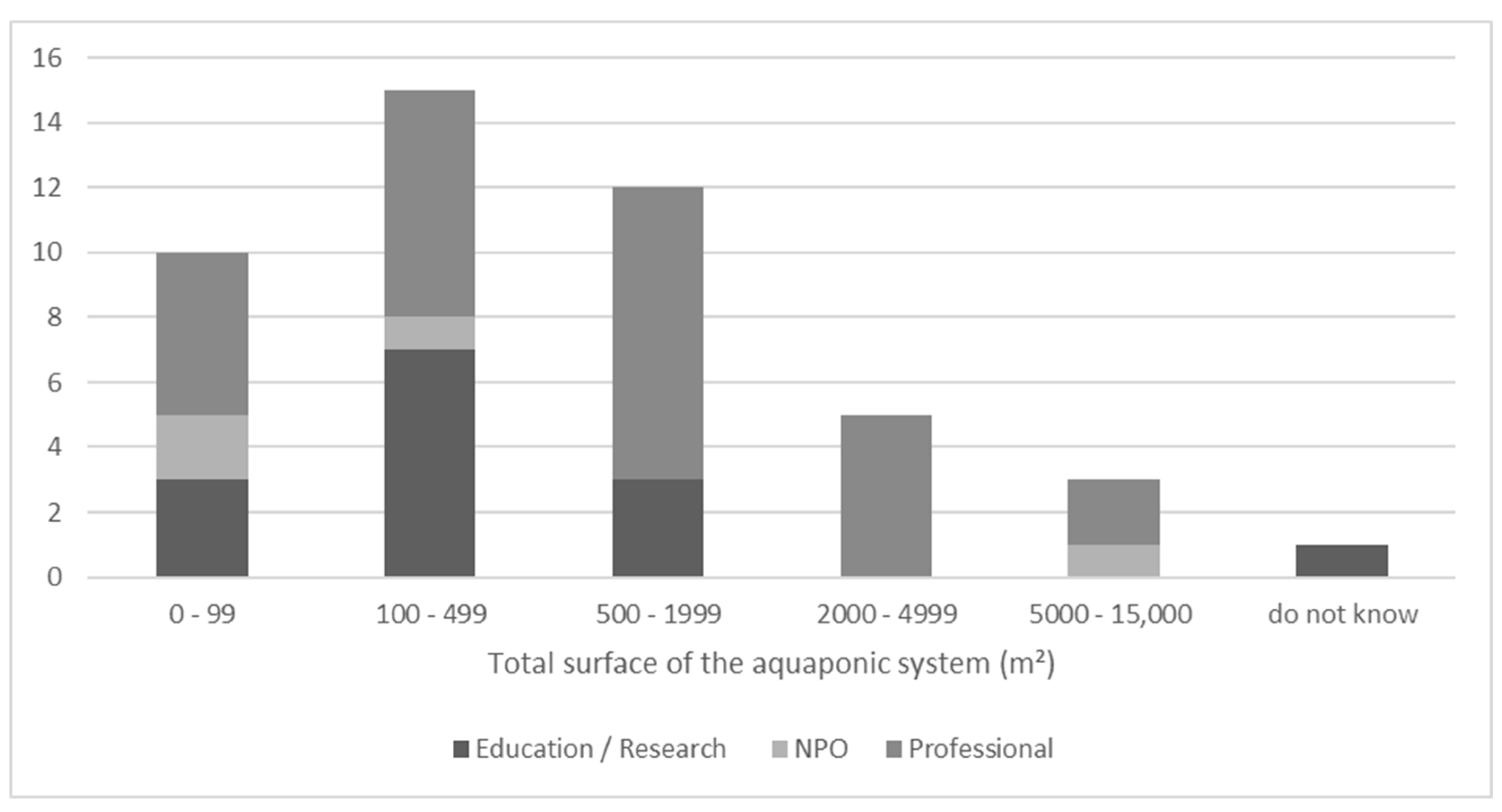

The aquaponic facilities of this study ranged from 8 m

2 to 14,000 m

2. To more appropriately reflect the data, the systems were classified in the following size categories: 0–99 m

2, 100–499 m

2, 500–1999 m

2, 2000–4999 m

2, and 5000–15,000 m

2 (

Figure 4). The most represented classes were 100–499 m

2, 500–1999 m

2, and 0–100 m

2. They represented 32.6% (

n = 15), 26.1% (

n = 12), and 21.7% (

n = 10) of the systems, respectively. Systems with a total surface greater than 2000 m

2 represented only 17.4% of the panel (

n = 8). One entity did not provide its total surface. The average size of the facilities was much bigger than in previous studies where aquaponics facilities ranged between 1 and 1600 m

2, and the majority were smaller than 100 m

2 [

26]. This indicates a significant increase in the sizes of aquaponic facilities between 2014 and 2020.

The area dedicated to plant production ranged from 4 to 12,000m

2, and the volume of water in the RAS ranged from 1 to 5000 m

3. The correlation between the area dedicated to plant production and the volume of water in the RAS was not significant. This reflects the variability of the plant-production-area-to-RAS-water-volume ratio (0.02–50) and further demonstrates the heterogeneous nature of professional aquaponic systems. Surprisingly, no significant statistical correlation was found between total area, plant production area, or RAS water volume and the activity of the structure (Professional vs. NPO vs. Education/research), suggesting that the size of the aquaponic system is not defined by the main activity of the structure. Among the 46 entities, 47.8% (

n = 22) also produced vegetables in soil, 13.0% (

n = 6) produced insects, and 13.0% (

n = 6) produced mushrooms. This shows that entities using aquaponics tend to diversify their production. A very wide range of systems was observed. Most companies designed and built their own systems (67.4%,

n = 31), some had systems designed by consultants (28.3%,

n = 13), and only two systems were bought in a kit (4.3%). These results are in line with previous findings on European systems [

26].

About one third of the systems (30.4%,

n = 14) were coupled, about one third (37%,

n = 17) were decoupled, and about one third (32.6%,

n = 15) were hybrid systems, including both coupled and decoupled loops. There was no significant correlation between the coupling type and the system size or the date of creation of the system. Similarly, the coupling type seemed evenly distributed between the size and the activity of the structure (Professional vs. NPO vs. Education/research). The increase of decoupled systems compared to previous studies is easily explained by its advantage in terms of risk management and increased yields [

10]. Nevertheless, among the 11 most recent systems (operating after 2018), only three of them were coupled, hinting to a global trend towards more decoupled systems but still with an interest in coupled systems in 2018.

RASs were located in cold greenhouses (37.0%, n = 17), inside buildings (34.8%, n = 16), heated greenhouses (17.4%, n = 8), and outdoors (8.7%, n = 4). One answer of RAS location was “other”. A few RASs were located on rooftops: two in a cold rooftop greenhouse, one in a heated rooftop greenhouse, and two outside on a terrace. Most of the aquaponics producers used greenhouses for plant production, including cold greenhouses (47.8%, n = 22) or heated greenhouses (34.8%, n = 16); the others grew plants in buildings (17.4%, n = 8) or simply outdoors (10.9%, n = 5). Five entities (10.8%) were growing plants in different locations.

Most respondents (71.7%, n = 33) used city water, 43.5% (n = 20) used rain water, and 26.1% (n = 12) used well water. Among them, 47.8% (n = 22) combined different sources of water. No significant correlation between the water source and the size of the system was identified.

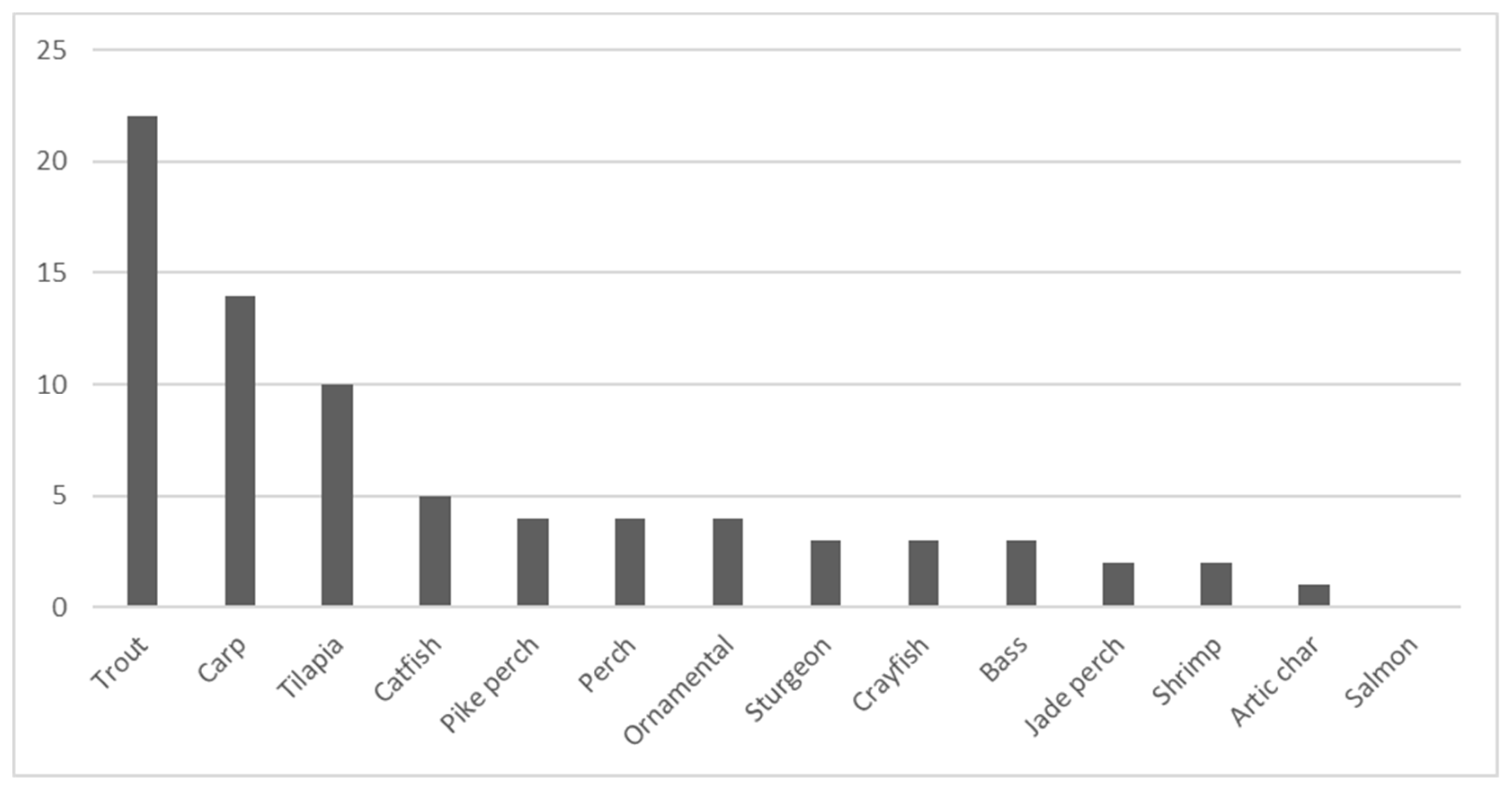

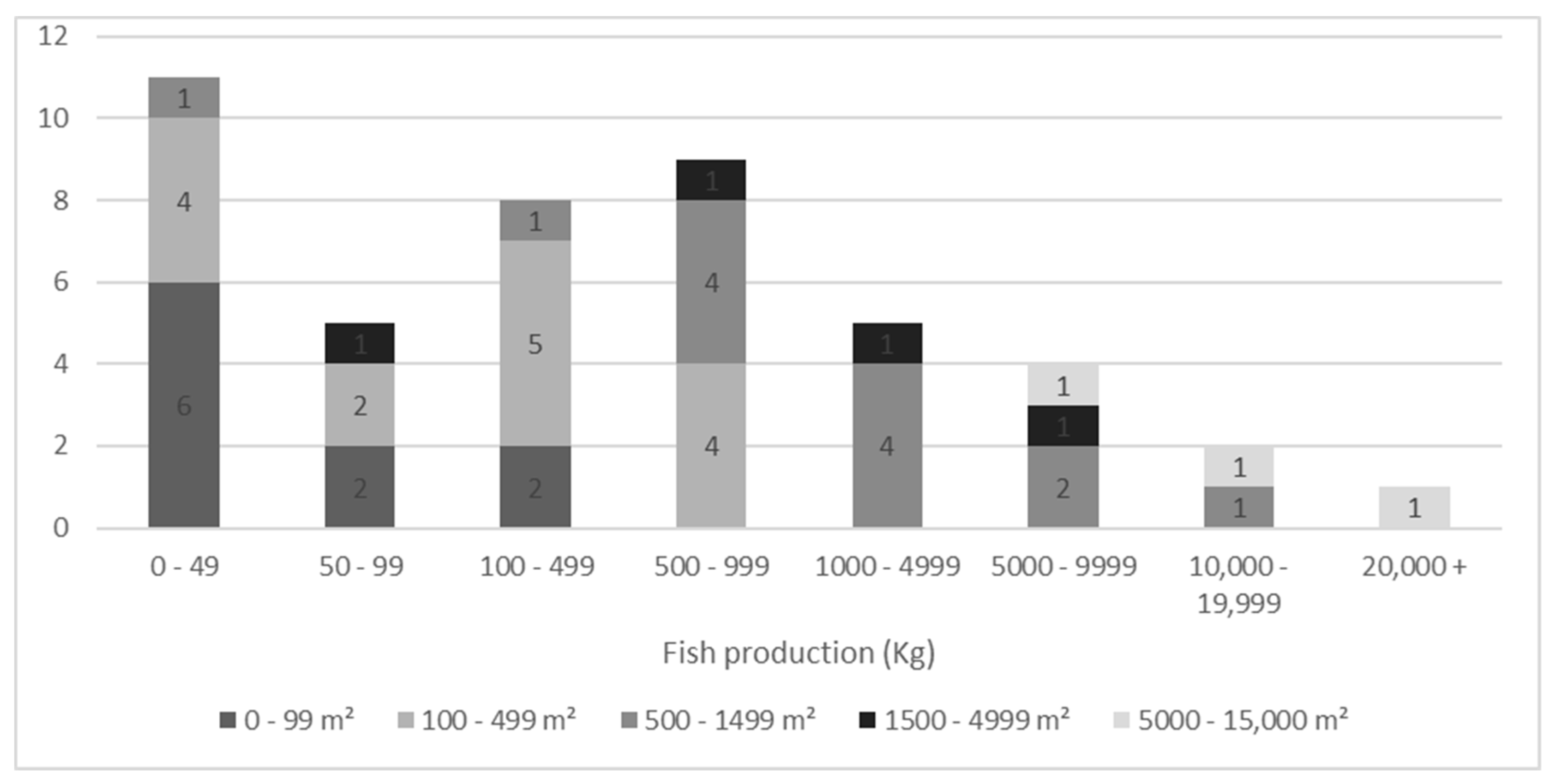

The most popular fish produced in the systems was trout, followed by carp and tilapia, present in 47.8% (

n = 22), 30.4% (

n = 14,) and 21.7% (

n = 10) of the systems, respectively (

Figure 5). An important proportion of systems (45.7%,

n = 21) reared more than one fish species. This result is very different from Villarroel et al. [

26] where the prevalent species were tilapia (27%), catfish (10%), ornamental fish (8%), and trout (7%). The decrease in occurrence of tilapia and catfish may be associated with a lack of consumer interest in these species on the European market and due to invasive species as well as breeding regulations in certain European countries. The range of annual fish production was wide, with 26% (

n = 12) of the respondents producing 1–49 kg of fish per year, and only one farm had an annual production of 20,000 kg of fish (

Figure 6).

Several interesting trends were noticed in the technical aspects of fish production. The two most represented mechanical filters were sedimentation filters and drum filters, found in 50.0% (n = 23) and 39.1% (n = 18) of the systems, respectively. Media beds were present in 8.7% (n = 4) of the systems, and 6.5% (n = 3) of the respondents claimed to use no filter. Some systems (15.2%, n = 7) were equipped with a combination of different filters. As for biofiltration, most of the respondents used moving beds or media beds (63.0%, n = 29 and 37.0%, n = 17, respectively). Others used bead filters (4.3%, n = 2) or other types of biofilters (8.7%, n = 4). A combination of biofilters was present in 17.4% (n = 8) of the systems. Pure-oxygen and UV filters were present in respectively 82.6% (n = 38) and 56.5% (n = 26) of the systems, suggesting increasing implementation of technology and a trend towards intensified production. Few systems (8.7%, n = 4) had a biofloc unit. Concerning the feed, the respondents were using pellet feeds based on animal proteins (80,4%, n = 37), pellets including insect proteins (17.4%, n = 8), 100% vegetal feed pellets (23.9%, n = 11), and live feed (8.7%, n = 4). A combination of feed types was used in 28.3% (n = 13) of the systems.

The management of fish sludge was also investigated in the study. Most respondents (78.3%, n = 36) claimed that they used fish sludge for soil amendment in agriculture (45.7%, n = 21) and/or in their hydroponic system (45.7%, n = 21). Among them, 32.6% (n = 15) used sludge for both soil and hydroponic production. Some respondents (13.0%, n = 6) did not reuse the sludge, and 8.7% (n = 4) did not know how the sludge could be used. The most popular sludge treatment was aerobic mineralization (37.0%, n = 17), followed by anaerobic mineralization and vermicomposting (10.9%, n = 5 each). Two respondents used sludge for biogas production, one respondent used sludge as soil compost, and 10.9% (n = 5) did not know how it was treated.

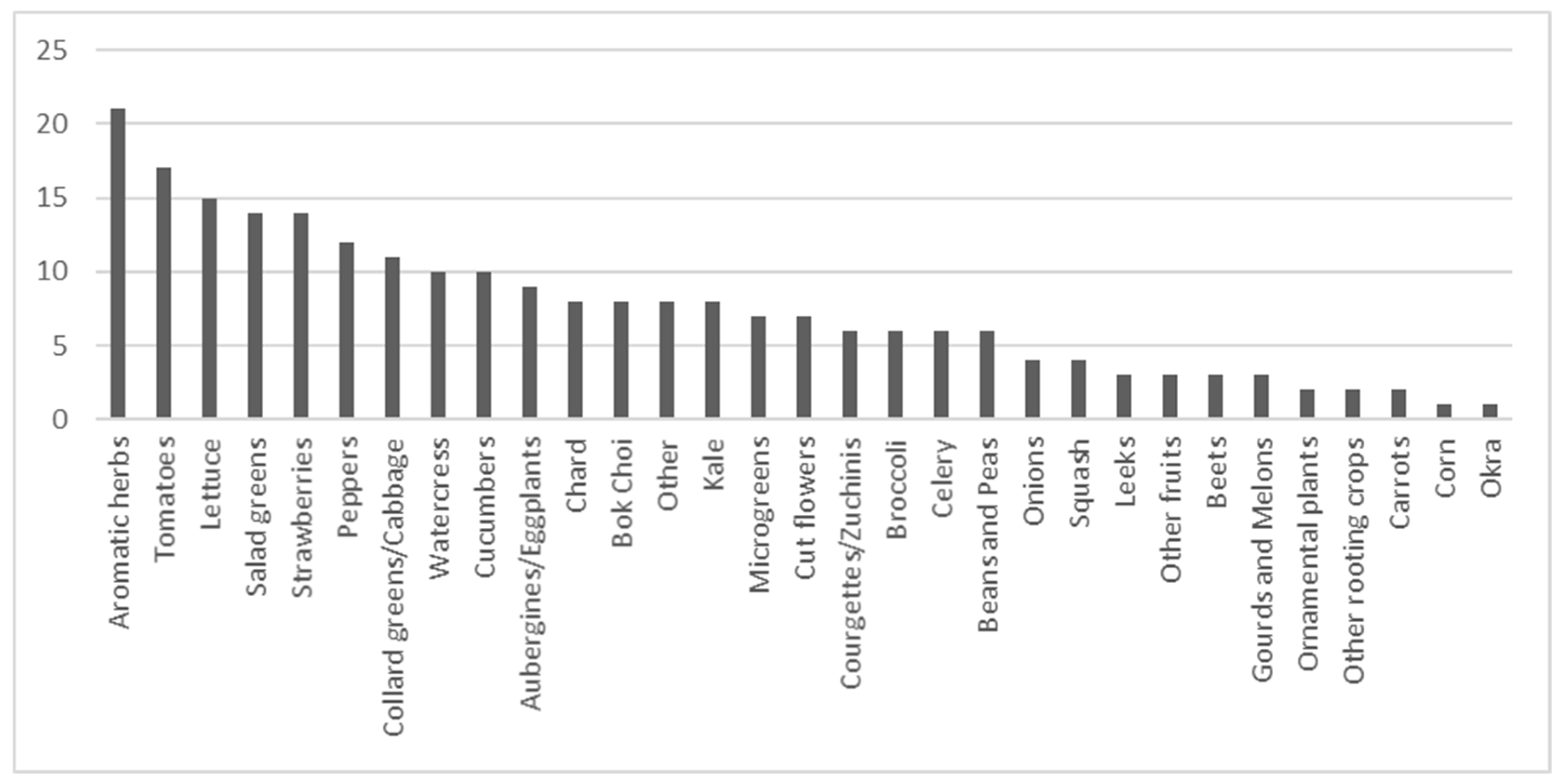

Thirty-one varieties of plants were identified in the present survey (

Figure 7). Contrary to fish, where three species were prevalent, numerous vegetable species were well represented. Six species were present in more than 25% of the entities and 20 were present in more than 10% of the entities. Aromatic herbs, tomatoes, and lettuce were the most represented plants and were present in 45.7% (

n = 21), 37.0% (

n = 17), and 32.6% (

n = 15) of the entities, respectively. The number of species per system ranged from 1 to 33, and 32.6% (

n = 15) of the structures produced fewer than three vegetable species, 39.1% (

n = 18) produced three to nine vegetable species, and 28.3% (

n = 13) produced 10–33 vegetable species. Again, no significant correlation emerged between the number of species and the type of organization. Large aquaponic systems with low or very large numbers of species were found, and small systems with low or very large numbers of species were also observed. The high variability of these parameters in the data further demonstrates the complexity and diversity of current aquaponic farms. The range of annual plant production followed that of fish production: 15.2% of the systems (

n = 7) produced 1–49 kg of vegetables per year, whereas 8.7% (

n = 4) produced more than 20,000 kg of vegetables per year (

Figure 8).

The most common hydroponic production systems were rafts, media beds, NFT, drip systems, and were present in 69.6% (n = 32), 43.4% (n = 20), 15.2% (n = 17), and 30.4% (n = 14) of the entities, respectively. Vertical towers, ebb-and-flow, and wicking beds were less represented (15.2% (n = 7), 4.3% (n = 2), and 2.2% (n = 1), respectively). Most entities (63.0%, n = 29) were combining different production systems. The structures equipped with rafts had a significantly higher number of species than those with no raft (p = 0.007). The systems where high numbers of species (>13 species) were grown all had rafts. This reflects the adequacy of rafts to a wide range of plant species. Heated greenhouses harbored a significantly lower number of species (p = 0.02) than cold greenhouses did, maybe because heated greenhouses are generally used to grow fruit vegetables (tomatoes, eggplants, peppers), hence, a more restricted number of species. Moreover, heated greenhouses require more energy and a higher investment, so that entities would tend to intensify production of a few species to reach a certain economy of scale. No significant association between the type of production system and the size of the aquaponics facilities was identified. Artificial light was present in 32.6% (n = 15) of the structures. Most structures (65.2%, n = 30) had an automated monitoring system. Moreover, half of the entities (50.0%, n = 23) utilized monitoring systems within both fish and plant production, again highlighting the implementation of high-tech equipment.

3.4. Business Model

The business questions were answered by 84.8% (n = 39) of the 46 respondents. Among them, 58.7% of the entities (n = 27) declared that they had had clients in the last 12 months, versus 26.1% (n = 12) who declared that they had had no clients. The following sections of this article focus on the 27 entities that had had clients and in thus a commercial activity. Among them, 22 described themselves as aquaculturists/horticulturists/aquaponists, three were NPOs and two were schools. The commercial activities taking place in schools may reveal the importance of commercialization of aquaponic training programs.

In order to get a better understanding of the business strategies of the respondents, the type of offe and the targeted customer segments were investigated for the 27 commercial entities. Only 18.5% (

n = 5) had one type of offer (product), whereas the others offered a combination of products, services, or R&D (

Table 1). Most of the entities (96.3%,

n = 26) offered products, 74.1% (

n = 20) offered services, and 37.0% (

n = 10) performed research and development. Services included—but were not limited to—training, visits and consultancy. As for the targeted customer segment, few entities (25.9%,

n = 7) had only one type of segment, and the others combined different segments. In fine, 92.6% (

n = 25) of the companies had B2B activities, 81.5% (

n = 22) had B2C activities, and 11.1% (

n = 3) had R&D activities. Commercial European aquaponic structures appear to be mainly opting for the production of products and services and directly targeting end customers as well as companies. One explanation of this diversity would be that most of the entities are quite recent (2018), and are attempting to reach different markets. The coming years will give insight on whether commercial strategies will remain broad or will be focused on certain key segments.

The data gathered in this study show no clear trends in the companies’ business models and reflect the diverse nature of the production systems themselves. There is a high degree of variability within markets depending on the nature, size, and location of commercial aquaponic farms. Furthermore, as most farms were established in the last 5 years, commercial strategies are yet to be standardized.

Specific attention was paid to the motivations of the respondents to initiate or participate in their organization. The three most representative answers were (i) “to develop full-time professional activity” (ii) “to produce food” (iii) “by passion”, closely followed by “reducing CO2 emissions”. These four statements were of certain importance for more than 66.7% (n = 18) of the respondents. This underlines the respondents’ belief that commercial aquaponics can be profitable and sustainable.

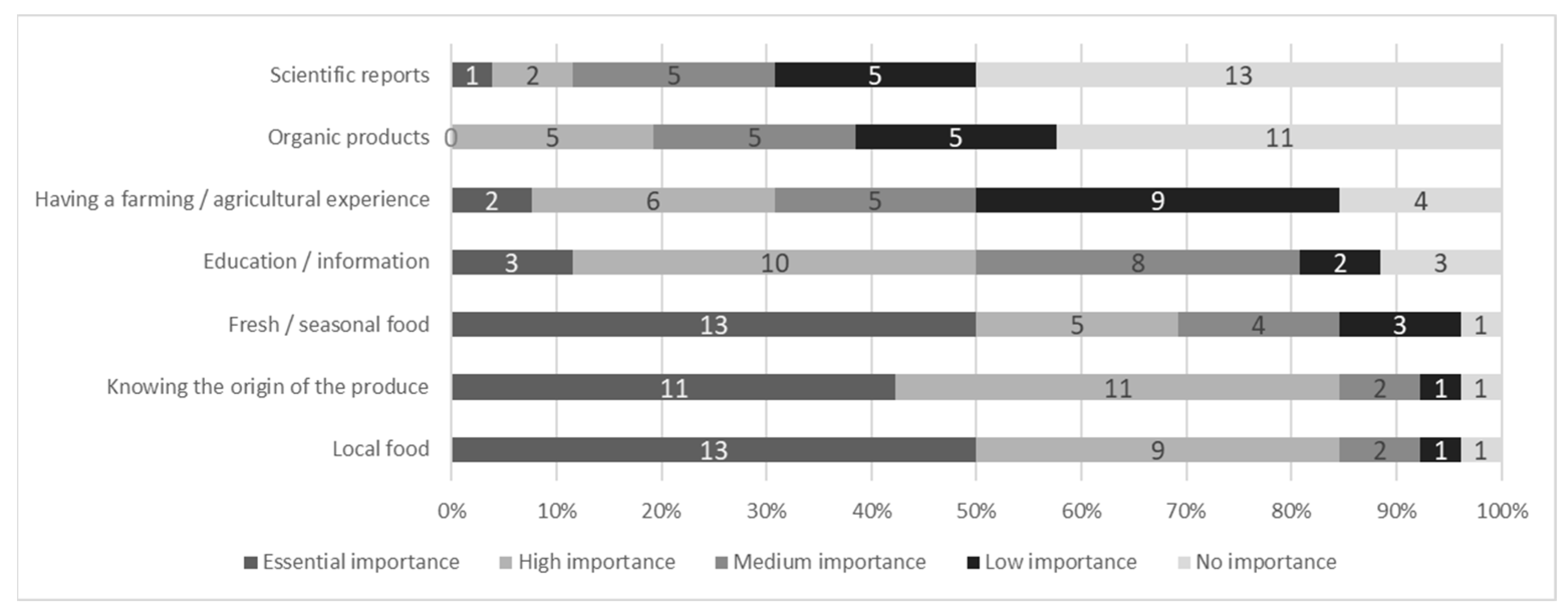

The survey investigated the clients’ expectations by asking the producers what the expectation of their clients were (

Figure 9). Since the respondents were the producers themselves—not the clients—the data and conclusion presented in this paragraph need to be taken with caution. The two greatest expectations were “having local food” and “knowing the origin of the product”. These two points were regarded of high importance for 81.5% (

n = 22) of the respondents. The third most important point was “having fresh and seasonal products” and was of high importance for 66.7% (

n = 18) of the respondents. These results are in accordance with the observation and conclusions made by Turnšek et al. [

21], who reported that aquaponics consumers were willing to pay a premium price for aquaponics products free of antibiotics, pesticides, and herbicides, connected with local producers, but not because of aquaponics as a production system in itself. Consequently, this reveals that the customer base of the respondents is mainly interested in sustainable and local farming.

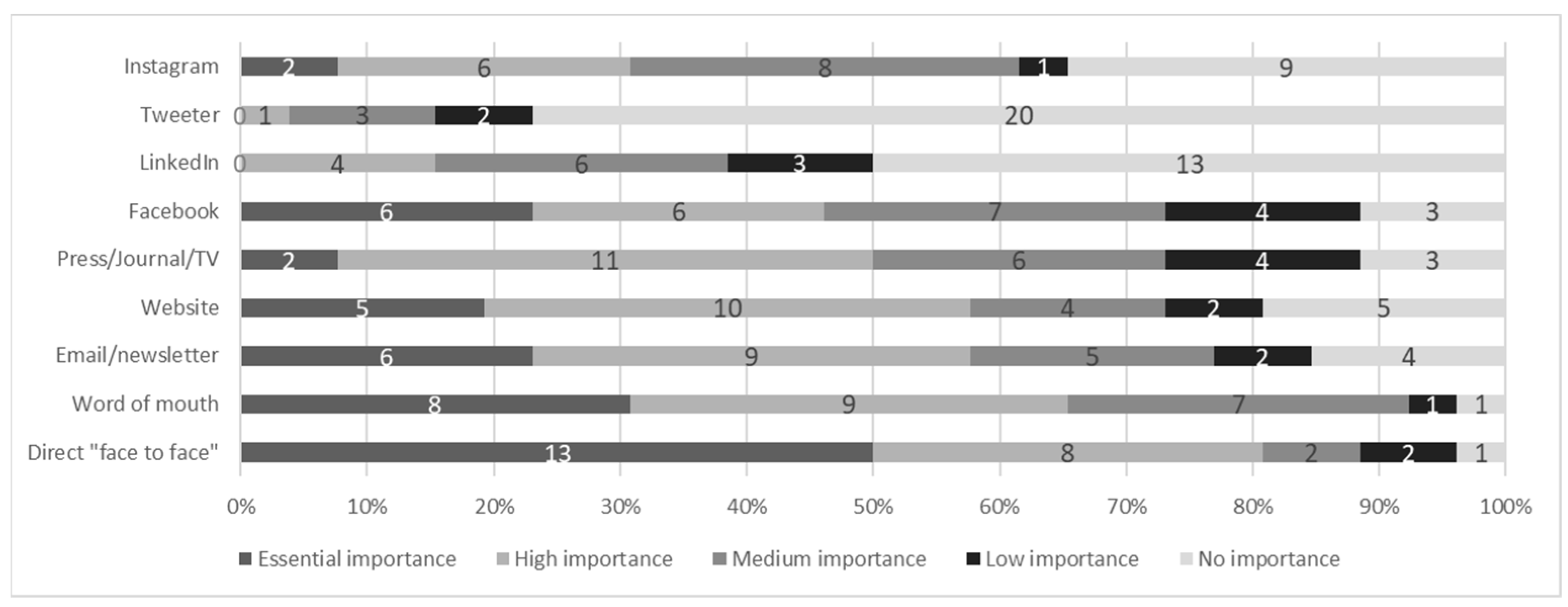

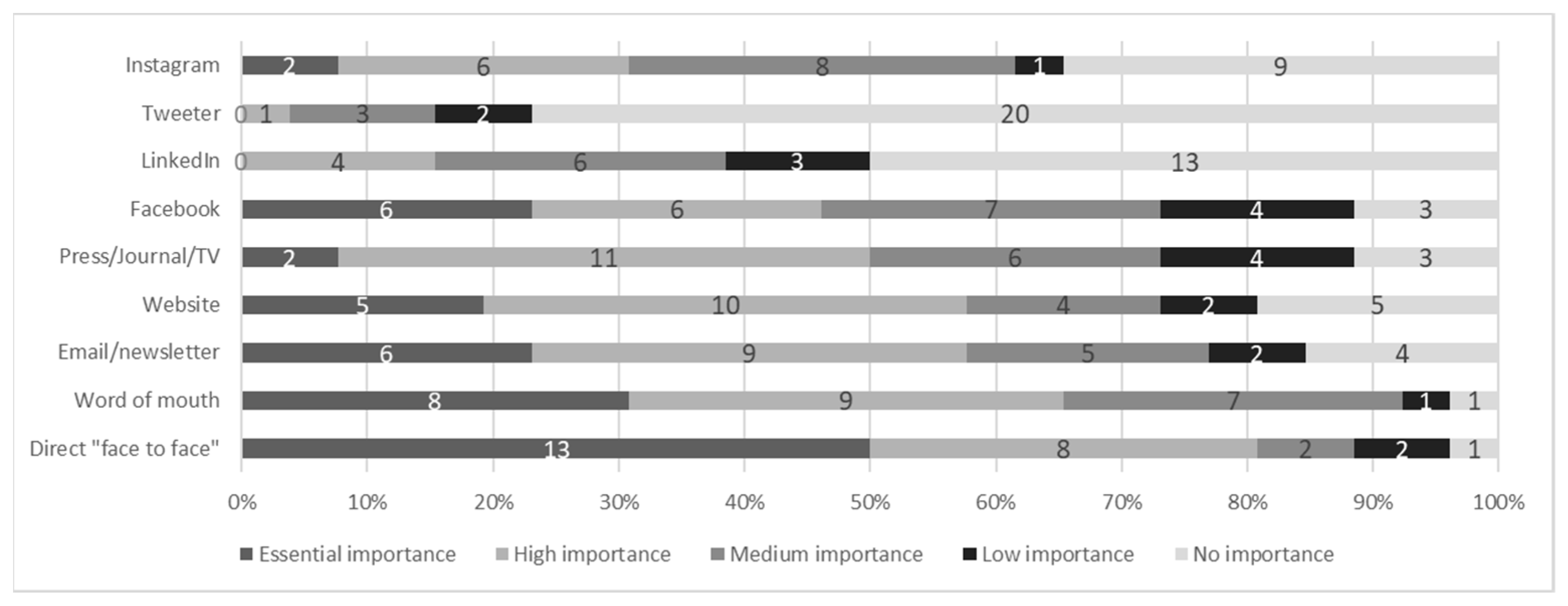

The two most popular communication channels were direct communication (“Face to face”) and/or by word of mouth, which was of high importance for 77.8% (

n = 21) and 63.0% (

n = 17) of the respondents, respectively (

Figure 10). Emails, newsletters, and websites were of high importance for 55.6% of the respondents (

n = 15). Traditional communication channels such as the press/journals/TV were also well represented with at least a high importance for 48.1% of the respondents (

n = 13). Among the social networks, Facebook had a certain prevalence, but others such as LinkedIn, Twitter, and Instagram were poorly represented. Consequentially, it makes sense that direct communication and word of mouth are important communication media in a sector where food locality and knowing the origin of the produce are major customer expectations. Communication channels could change if the size and production of aquaponics farms continue to increase. Bigger aquaponic farms may indeed have to find other, larger customer segments.

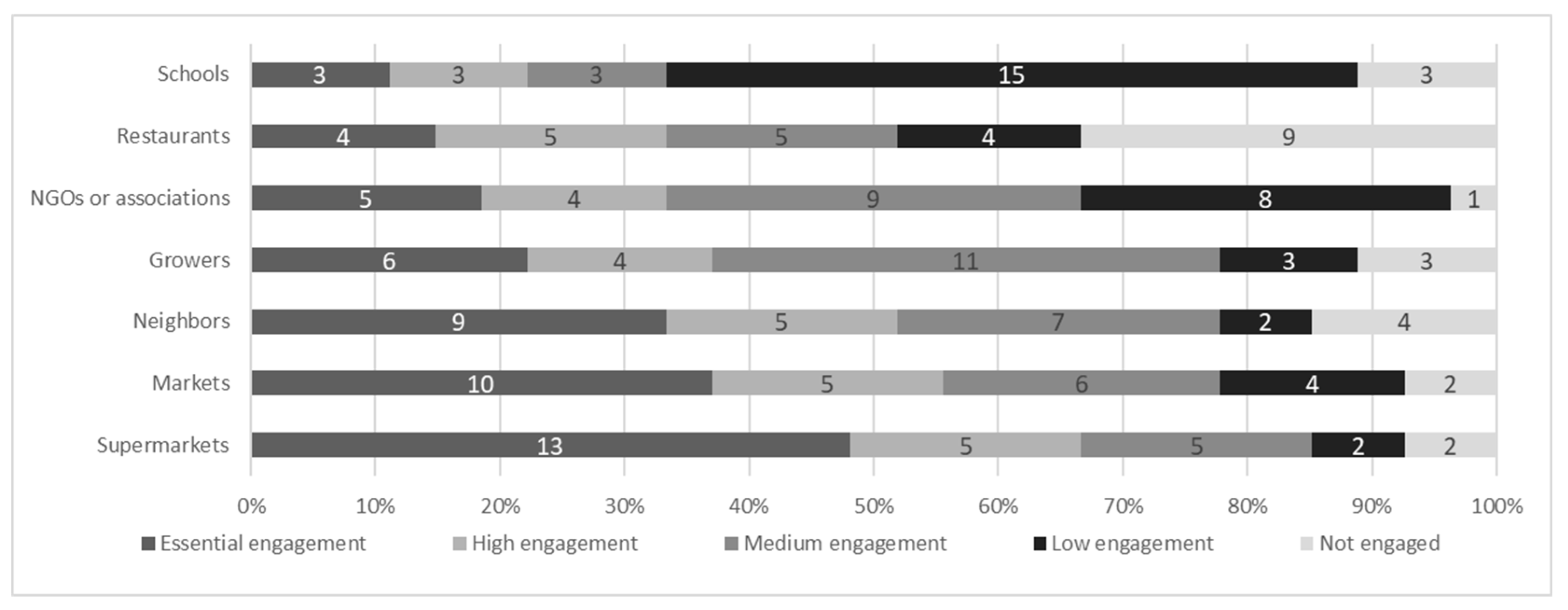

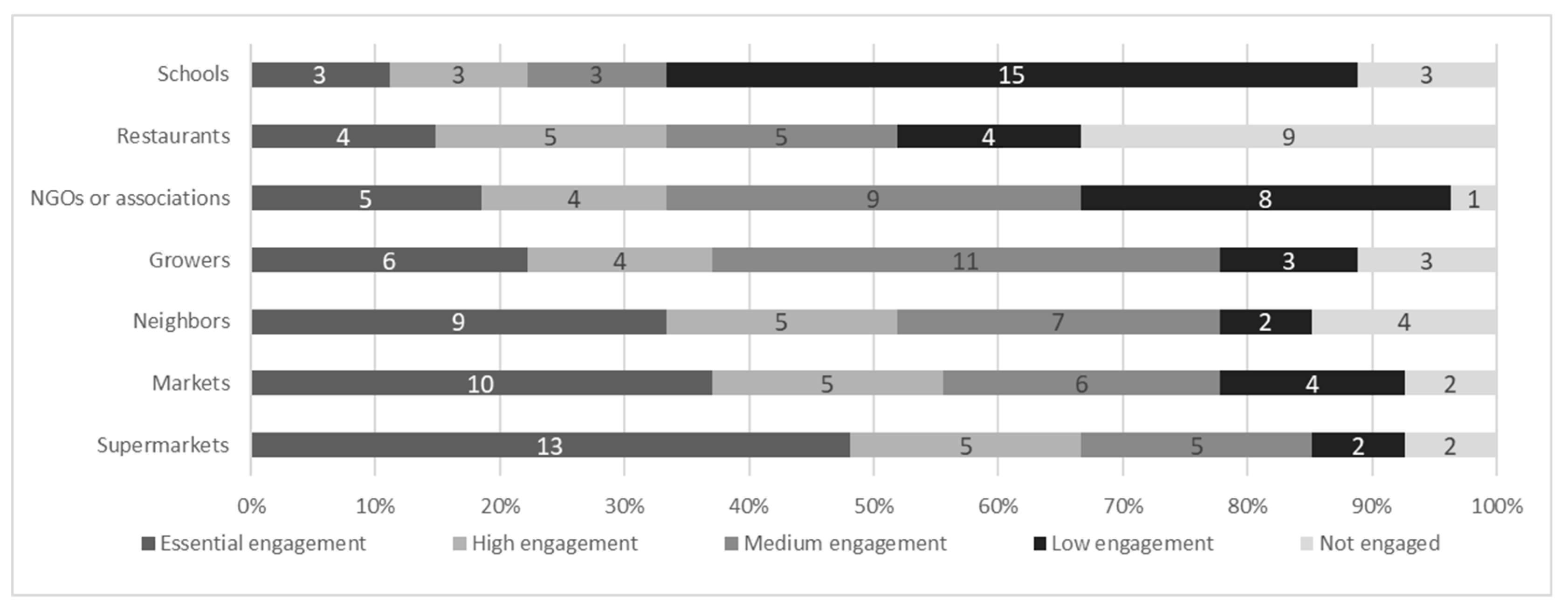

The survey also investigated stakeholder engagement and competition (

Figure 11 and

Figure 12). According to the respondents, the three most engaged stakeholders were supermarkets, markets, and neighbors with at least a high engagement representing 66.7% (

n = 18), 55.6% (

n = 15), and 51.9% (

n = 14) of the entities, respectively. Having clients as main stakeholders reveals that commercial relationships are an essential support for the aquaponic sector and suggests that aquaponics producers may be important economic actors. Most of the respondents did not feel a sense of competition: only a few answered this question (51.9%,

n = 14), and among them, the proportion of respondents who declared being under high or very high competition was low. The biggest competitors, for whom competition was of high importance or more were small growers (28.5%,

n = 4), supermarkets (21.4%,

n = 3), and markets (14.3%,

n = 2).

To evaluate the investment cost of each system, the respondents were invited to select a range of initial investments and write the exact investment cost if the data was available (

Table 2). Most of the respondents (96.3%,

n = 26) provided a range of initial investment, whereas 40.7% (

n = 11) provided the exact investment.

Table 2 shows that the investment range was variable in each size category. Entities with investments higher than 1,000,000 € were (i) a heated rooftop greenhouse and (ii) the largest aquaponic system of this study, which also produced in a heated greenhouse. Entities with investments ranging from 500,000 to 999,999 € generally produced indoors. The systems with more technological or energy-demanding components (large RAS water volume, indoor, or heated greenhouses) required the highest investments. Yet, the system with the lowest investment was a 100 m

2 heated rooftop greenhouse. The other investment range categories included various types of aquaponic systems. Eleven respondents provided their exact investment costs. The investment cost per square meter was calculated based on their data. Four of the 11 structures had investment costs ranging from 44 €/m

2 to 93 €/m

2 and produced their vegetables in a cold greenhouse. Four of the 11 structures had investment costs ranging from 150 €/m

2 to 313 €/m

2 and had a heated greenhouse for vegetable production. Two had investment costs of 694 €/m

2 and 714 €/m

2; an indoor system, and very small system (less than 20 m

2), respectively. One system—the heated rooftop greenhouse with investment higher than 1,000,000 €—had an investment cost of 1175 €/m

2. Investments ranged from 44 to 93 €/m

2 for an aquaponic systems with a non-heated greenhouse, 150 to 313 €/m

2 for aquaponic systems with a heated greenhouse, and more than 700 €/m

2 for indoor systems. These investments per area can increase drastically in specific cases, for example, in very small systems that do not benefit from the economy of scale or in rooftop greenhouses which can lead to extra costs associated with accessibility during the construction and/or security measures due to their specific location.

When it comes to employment, the aquaponics sector appeared to rely both on paid and unpaid labor via volunteers or interns (

Table 3 and

Table 4). The ratio between paid and unpaid labor was variable with some structures predominantly relying on paid labor, whereas the opposite was true for other structures. On average, however, there was less unpaid labor than paid labor. The high degree of unpaid labor underlines the attractability of aquaponics. Nevertheless, the important role played today by unpaid workers illustrates that the workload of these farms is higher than their ability to pay their workforce. This coincides with previous papers raising concerns about the economic viability of commercial aquaponic farms.

Seventeen respondents (63.0%) declared that the company made profits in the last 12 months, whereas seven others acknowledged having made no profit within the same time frame. Among them, one was an NPO, and most of them (n = 6) started their activity after 2018. At the time of the survey, these companies had not yet gone through a full production cycle. Among the 10 respondents who declared having made no profit, four launched their activity in 2018.

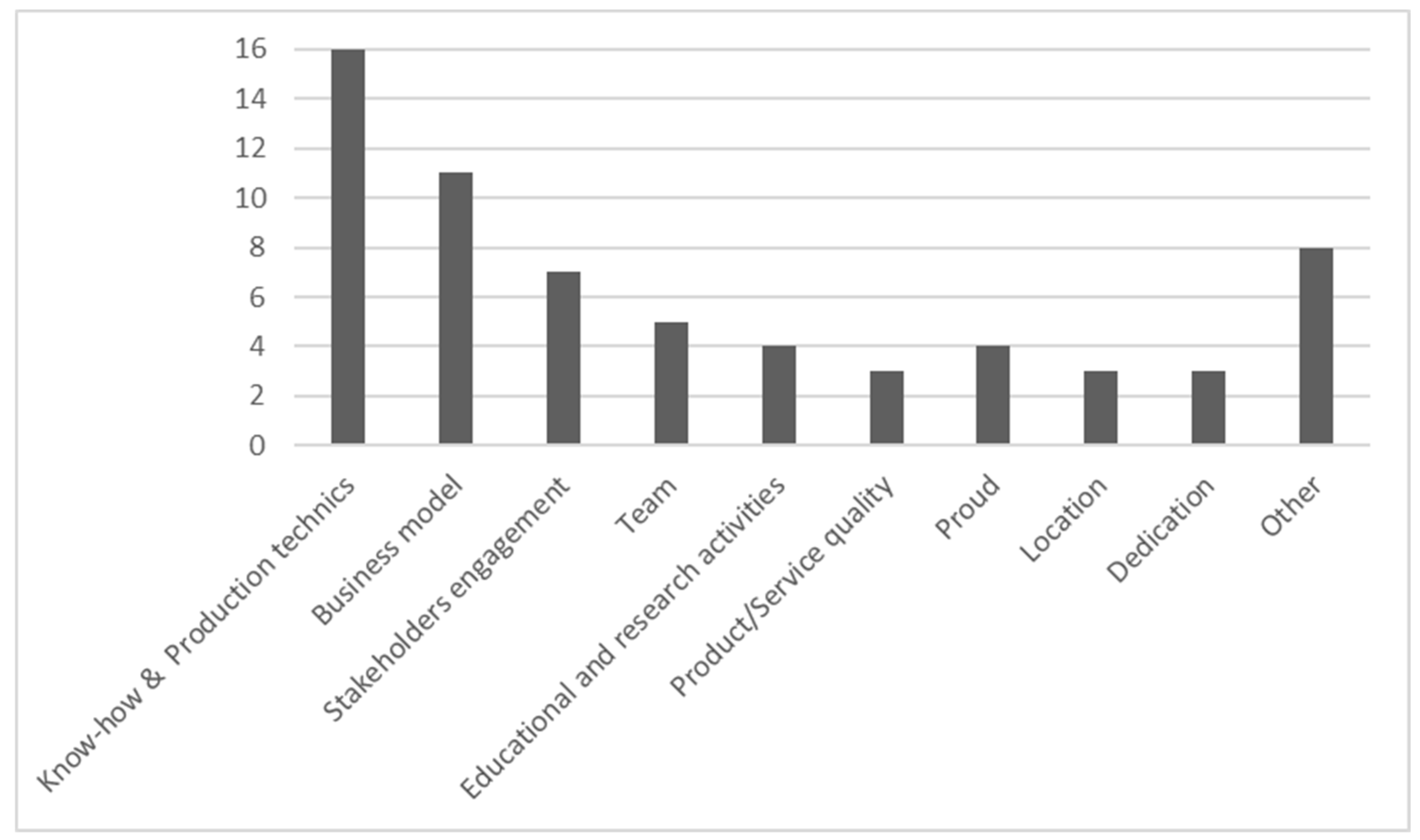

The participants were asked to identify three of the most important success factors and three of the most significant challenges faced by their companies. Twenty-five respondents provided success factors and 17 provided challenges (

Figure 13 and

Figure 14). The top success factor, identified by 64.0% of the respondents (

n = 16), was knowledge and production techniques, followed by the business model and stakeholder engagement at 44.0% (

n = 11) and 28% (

n = 7), respectively. The two major challenges were general production and successful business models, mentioned by 52.9% (

n = 9) and 47.1% (

n = 8) of the respondents, respectively. The challenges are similar to the success factors and reveal that even “success factors” are still subject to challenges and improvement. However, these results contrast with the obstacles identified by Turnšek et al. [

21] which were investment costs and unexpected regulations at 33% and 21%, respectively. Other obstacles such as the lack of skilled labor (11%), and competition on market prices (10%) were identified by the respondents. This may indicate that the investment costs and unexpected regulations are not as much of a challenge anymore, as previously stated by other studies.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}