Abstract

The recent financial crisis highlighted the need for a strong emphasis on the effectiveness of board risk oversight practices. Good corporate governance upholds effective risk management, which in turn ensures the flexibility to reply to unpredicted threats and take benefit of opportunities. Thus, risk management affords corporate resilience that engenders competitive advantage due to the capacity to circumvent, deter, defend, react, and adjust to any kind of disturbance, besides recovering quickly. Guaranteeing that the board is prepared and adequately resilient to deal with a crisis circumstance is a crucial part of good governance. By employing a data set of companies listed in Romania, this paper analyzes whether boards of directors influence risk management. We measure boards by means of size, independence, diversity, establishment of Consultative Committees, as well as CEO duality, gender, age, and tenure. Based on ten financial ratios, we develop two risk indicators regarding shareholders’ wealth and short-term risk, alongside a global business failure risk tool, by means of principal component analysis. Furthermore, the output of the multivariate regression analysis show that CEO gender, the size of the board, and Audit Committee negatively influence business failure risk.

1. Introduction

The concept of resilience has emerged as a reaction of current iterative and growing strong economic crises [1]. Organizational resilience is viewed as the power of the company to foresee, undergo, adjust, and flourish in the aftermath of disruptive circumstances [2]. Consequently, resilience can be seen when a company is able to uphold above-average returns even after absorbing the shocks of the competing setting [3], and is thus an approach to risk management. In fact, the reply of companies to fast transformations and shocks is crucial for economic development [4]. According to the study by Hamilton [5], enterprise resilience empowers the company to constantly identify and mitigate the risks, therefore acting as an early warning tool. Therewith, resilient enterprises employ sustainable strategies aiming to register long-term performance [6]. Also, strategic resilience was depicted as the response of the company to replace and fit the strategies according to shocks from outside environment [7]. By means of resilience are underlined the firm skills to preserve social and intellectual resources, apart from operational integrity, that are vital to the long-run success of organizations [8]. Besides, groups show greater organizational resilience relative to unaffiliated firms due to an efficiency effect which supports the idea that groups have greater incentives to reorganize and are more efficient through market transition, as well as a cumulativeness effect which argues that groups hold higher resources and skills to exploit the new opportunities given by the market expansion [9].

A company should certify that there exists a balance between the management incentives and shareholder concerns in order to generate long-term value. In this sense, corporate governance is an essential device for bringing into line the beliefs corresponding to principals and agents, also promoting responsibility. Besides, corporations are not solitary entities, being a share of a wide-ranging system that comprises the entire society, as well as the environment. Even if some of the companies are keen to fulfill the needs of stakeholders, their undertakings call for the consumption of huge quantities of natural resources. As such, corporations should lessen harmful effects on the environment, at the same time creating long-term sustainable shareholder value. Therewith, the board of directors should integrate environmental, social, and governance aspects within the fundamental decision-making practices, thereby benefiting from remarkable opportunities on behalf of innovation and growth, whereas any rebuff might cause major risks. Specifically, the companies that disregard sustainability are expected to face disputes with regulators, stockholders, or non-governmental organizations that undermine their reputation due to suspicious functioning practices. On the contrary, a resilient organization establishes transparency and sets oversight for CEOs and boards to manage enterprise risks, in order to reduce losses and to maintain shareholder value. Thus, resilience supports the companies not only to live on during a crisis period, but also to reach their essential goals, due to its capability to catch opportunities.

Further, the research of Tait and Loosemore [10] underlined that sound corporate governance is related to higher levels of organizational resilience ensuing from the reputational and financial benefits of better transparency, market value, investor attractiveness, and organizational performance. Liang et al. [11] noticed that the fundamental corporate governance indicators towards business failure examination were board composition and ownership structure. In fact, the internal controls (including shareholder structure, board features, external overseeing, and management remuneration) are considered as the primary factors that reveal and hinder poor performance, scandals, and frauds, whereas if these governance mechanisms fail, then the external controls (comprising the legislative regulations, mergers and acquisitions market, and manufacturing market rivalry) are likely to intrude into corporate control, at least in well-functioning finance and stock markets. Fich and Slezak [12] stated two corporate governance viewpoints which may enlighten the eventual occurrence of business failure. Mainly, well-known scandals (such as Enron and WorldCom) showed that financial statements could be handled in order to conceal the genuine financial condition. Hence, corporate governance takes responsibility over vigorous financial reporting. Moreover, bankruptcy depends on the ability of management towards dealing with challenging financial situations.

Managers should be aware that unexpected situations could happen whenever, which in turn place their organization at risk of failure. As such, building resilience is strategically advisable, but also costly, thus becoming a process of harmonizing costs compared to prospective risks [8]. In addition, the adaptability of corporations reveals their capacity to amend their undertakings as an answer to variations within the outside setting. A company should anticipate hints of change from the outside, decrypt them, and speedily proceed to enhance or reinvent its business model. Corporations that surpass crisis periods are those entities that show sufficient flexibility to adjust to fluctuating situations. Likewise, the adaptability and flexibility of corporate governance, sustained by a supervisory framework is a precondition for enhanced corporate performance. Furthermore, even sustainability demands for adaption towards the ecological, social, and economic changes across time.

The current empirical investigation aims to explore the link between corporate governance features and the risk of failure related to the companies listed in Romania. This research adds new perspectives to the literature since, from our knowledge, there is no previous evidence towards the link between characteristics of a board of directors and risk management on the Bucharest Stock Exchange (BSE). Likewise, a comprehensive global business failure risk tool (GBFRT) was developed, by the side of two risk indicators for shareholders’ wealth and short-term risk, by employing multidimensional data analysis techniques. Furthermore, several characteristics related to CEOs were considered. In addition, the results drawn from this paper reveal practical usefulness for investors, as well as policy makers, within the investment activity.

The remainder of the study proceeds as follows. The second section analyzes prior literature, strongly debated especially for the US market, drawing the research hypotheses. The third section presents the database, selected variables, as well as employed quantitative methods, whilst the fourth section exhibits and discusses the empirical evidence. The final section of the manuscript set out the concluding remarks and provides future research avenues.

2. Related Literature and Hypotheses Design

As long as the roles of CEO and Board Chair are not divided, the agency theory predicts that firm performance is poor since the oversight and control of the CEO are imperiled. Contrariwise, the conjunction of CEO-Board Chair functions is supported by stewardship theory that emphasizes that there is a unity of command, which positively influences firm performance. According to Hambrick and D’Aveni [13], corporations within which the same individual holds both the CEO and Chair of the Board positions reveal a greater tendency to go bankrupt. In case of an independent Chairman, Jensen [14] highlighted that the board will be more effective and the Chairman will have no conflicts of interest. Further, a high quality monitoring will be ensured in case of an independent Chairman, showing a lesser likelihood of organizational failure [15].

Based on these assertions, the first tested hypothesis was:

Hypothesis 1 (H1).

CEO duality negatively influences business failure risk.

Croson and Gneezy [16] stated that men consider risky situations as challenges instead of threats, which causes increased risk tolerance. Contrariwise, Bliss and Potter [17] found that females assume higher risk than men. Likewise, Adams and Funk [18] documented that women directors are more oriented towards risk taking than male directors. Berger et al. [19] suggested that female directors are less skilled compared to male directors, and found that the increase of women directors is positively linked to risk, but this outcome was not significant.

Considering the above-mentioned, the second tested hypothesis was:

Hypothesis 2 (H2).

Women CEOs negatively influence business failure risk.

Younger managers are concerned about career, therefore showing more risk-aversion, which determines excessive conservatism in investment policies [20]. In fact, younger managers do not have reputations as high quality managers, hence being confronted with greater labor market scrutiny in case of a bad investment decision, which could significantly diminish future career opportunities. Bucciol and Miniaci [21] explored a representative sample of US households and stated that risk tolerance declines with age and increases with wealth. Serfling [22] showed that the age of CEO is negatively associated with risk, thereby providing evidence suggesting that corporations expect older (younger) CEOs to take fewer (more) risks, which implies that CEO and firm risk preferences are aligned.

Based on these statements, the third tested hypothesis was:

Hypothesis 3 (H3).

Older CEOs negatively influence business failure risk.

Commonly, longer tenure emphasizes higher risk aversion due to larger private benefits from control related with higher managerial power, as well as more undiversified human capital investment. Hence, longer tenure entails greater managerial power and entrenchment [23], whilst entrenched managers may take fewer risks to protect their private benefits from control. Chen and Zheng [24] found a positive impact of CEO tenure on risk-taking, inconsistent with considering tenure primarily as a measure of human capital investment. Also, Ferrero-Ferrero et al. [25] suggested that generational diversity promote sustainability within businesses.

Based on these considerations, the fourth tested hypothesis was:

Hypothesis 4 (H4).

Longer CEO tenure negatively influences business failure risk.

Yermack [26] emphasized the effectiveness of smaller boards since there are fewer problems with regard to communication and coordination. On the contrary, Uzun et al. [27] claimed the lack of correlation between the size of the board and corporate fraud. Wang [28] found that corporations with smaller boards register a higher future risk. Further, Wang and Hsu [29] noticed a negative and non-linear link between the size of the board and the occurrence of operational risk events.

Considering the above-mentioned, the fifth tested hypothesis was:

Hypothesis 5 (H5).

Larger boards negatively influence business failure risk.

Heslin and Donaldson [30] noticed that executive directors would increase risk, whilst non-executive directors would decrease risk. During the financial crisis, Minton et al. [31] emphasized that financially literate independent boards exhibited a risk-taker stance. Shrivastava and Addas [32] found the prevalence of policies towards climate change and environment in companies with a higher ratio of independent directors. In addition, according to Post et al. [33], a higher share of independent directors will drive to the establishment of sustainability-themed alliances.

Based on these considerations, the sixth tested hypothesis was:

Hypothesis (H6).

Board independence negatively influences business failure risk.

Based on an investigation of 150 papers, Byrnes et al. [34] concluded that women tend to follow an approach of less engagement with risk taking. Thus, women are less overconfident than men. According to Beckmann and Menkoff [35], female fund managers avoid risk, their confidence being lower than in case of men. Additionally, a directive was proposed which established that at least 40% of non-executive board positions should be held by women [36]. Also, Post et al. [33] contended that a higher female representation on a board lead to the foundation of sustainability-themed alliances, whereas Ben-Amar et al. [37] found an improvement of disclosure on voluntary climate change in companies showing greater women ratio on boards.

Based on these assertions, the seventh tested hypothesis was:

Hypothesis (H7).

The presence of women on boards negatively influences business failure risk.

The board of directors is responsible for decision-making processes, corporate performance, and value creation, elements that bear risks. In addition, the CEO is accountable for setting the strategy regarding risk management, as well as for the policies established by the board. Board committees are created to serve the board with wise resolutions within particular fields, along with supervision of their fulfilment. However, the board may delegate the risk oversight responsibility to a particularly intended committee such as Risk Management Committee. Otherwise, the Audit Committee might implicitly take on this duty. For instance, amongst the requirements for listing on the New York Stock Exchange is that the Audit Committee is liable for risk monitoring. Instead, the Australian Stock Exchange guidelines claim that risk oversight is the assignment of the full board. Klein [38] asserted an inverse link between Audit Committee independence (AC) and earnings management, whereas Bedard et al. [39] noticed that the financial knowledge on the Audit Committee mitigated earnings management. Bliss et al. [40] found a positive link between combined CEO-chairman roles and audit fees, thus arguing that auditors perceive higher inherent risk within a corporation where CEO duality prevails. Sun and Liu [41] asserted that a great effectiveness of the Audit Committee may restrict risk-taking behavior.

Based on the above assertions, the eighth tested hypothesis was:

Hypothesis (H8).

The establishment of Consultative Committees negatively influences business failure risk.

3. Data and Research Methodology

3.1. Database and Variables

We have selected all the companies listed on the BSE in 2013, namely 104 companies. Subsequently, we removed from the initial sample the financial services companies due to specific reporting regulations, the companies from the unlisted and international tier, as well as the companies that did not make available financial statements. Hence, the final database comprises 69 companies.

Table 1 presents the variables. Several elements were selected out of annual financial statements, which will be employed towards global business failure risk tool development, variables related to corporate governance specific features, as well as firm-level controls. The annual financial statements depict the data source related to financial indicators, whereas corporate governance measures were collected from the companies’ website.

Table 1.

Variables presentation.

3.2. Empirical Research Methods

The GBFRT will be designed by means of the principal components analysis (PCA). In fact, PCA aims to lessen a wide suite of variables into a dense set of constructs-entitled principal components, which largely explain the variance in the former variables. Besides dimensionality mitigation, PCA attempts to uncover latent shapes in the data, as well as the connected variables. However, the basic procedure is as follows: (i) data standardization; (ii) computation of the covariance/correlation matrix, across its eigenvectors and eigenvalues; (iii) ordering the eigenvectors from highest to lowest consistent to the eigenvalues; (iv) disregarding the components of minor significance and achieving the novel data [42].

In an algebraic view, principal components are linear combinations of the ten selected variables towards developing the GBFRT (, , …, ), whereas in a geometric setting, the linear combinations depict the choice of a new coordinate frame achieved by rotating the primary system with , , …, as the coordinate axes. Hence, the new axes signify the ways with the most fluctuation, while ensuring a straightforward and more parsimonious exhibition of the covariance pattern. Thus, the vector of variables picked out in order to substantiate the GBFRT, = (, , …, ), shows the correlation matrix ρ which registers ten eigenvalues ≥ ≥ … ≥ 0 [43].

Thereby, the liner combinations are exposed below:

Further, the linear combinations show the variances and covariances as follows:

In fact, this shows the following ten principal components:

signifies the first principle component, which depicts the linear combination X that maximizes Var(X) under the condition that = 1;

signifies the second principle component, which depicts the linear combination X that maximizes Var(X) under the conditions that = 1, as well as Cov(sX, X) = 0;

…

signifies the tenth principle component, which depicts the linear combination X that maximizes Var(X) under the conditions that = 1, as well as Cov(X, X) = 0.

Subsequently, we will regress GBFRT, as substantiated by means of PCA, on corporate governance measures and control variables:

where Y is separately depicted by the retained principal components and GBFRT, X is the vector of characteristics related to corporate governance, and Z is the vector of firm controls. In addition, the index i depicts the company, is the intercept, and are parameters, and is the error term.

4. Findings

4.1. Summary Statistics

Summary statistics for all the selected variables are exhibited in Table 2. By considering the sixth principle out of the BSE Corporate Governance Code [44] with respect to board independence, we notice the potential shortcoming of biased decisions within the boardroom inasmuch as the mean percentage of external directors is only 40.55%. Moreover, even if the Romanian guidelines towards good corporate governance [45] assert that the independent directors should register at least a quarter of all directors (Recommendation 16), in mean (37.04%), this reference is fulfilled. Likewise, in mean (16.75%), no balance is registered between women and men on boards. In addition, high standard deviations regarding the variables taken from annual financial statements emphasize the higher exposure to risk of listed companies on the BSE. The higher standard deviation related to short-term assets reveals issues regarding corporate liquidity, which may exert a substantial effect on operational efficiency, as well as on profitability. As such, troubles regarding short-term liabilities represent a hindrance for business success. Moreover, higher standard deviations regarding CEO tenure support that long tenure CEOs are concerned about sustainability aims, whilst short tenure CEOs may be related to business failure.

Table 2.

Statistical summary of observations.

The correlation coefficients between selected variables for GBFRT development are shown in Table 3. Therefore, we notice several strong correlation coefficients. In fact, the individual significance of the selected variables is mitigated, also being redundant in information. Hereafter, by employing PCA, the primary data is expressed via data with lesser size, but which suitably summarizes the original data.

Table 3.

The correlations between variables.

4.2. Global Business Failure Risk Development

The variances corresponding to the principal components, signifying the eigenvalues related to the correlation matrix are presented in Table 4. Thus, the relevance of the eigenvalues is given by the fact that it shows how much variance lies in the examined data.

Table 4.

The variances of the principal components.

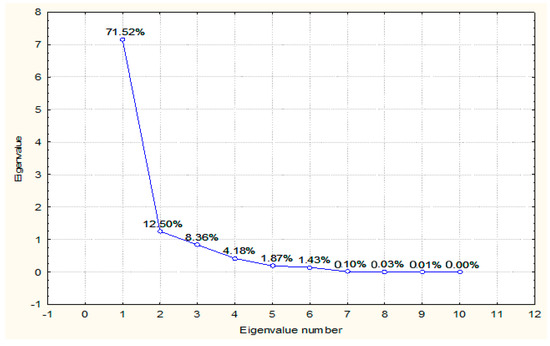

The first eigenvector of the correlation matrix describes the first principal component which explains the greatest possible variance in the dataset, the second principal component explains most of the remaining variance, whereas every following component explains as much of the remaining variance as possible. Additionally, the components are presented in a decreasing order of the associated variances. Thereby, the first principal component accounts for 71.51927% of data variation and the second principal component accounts for 12.50444% of data variation. Consequently, the first two principal components account for 84.0237% of the total variation in the dependency structure of the ten selected variables. Figure 1 illustrates the scree plot, proposed by Cattell [46], which graphically reveals the variance expounded by every component. We assert that the curve begins to flatten out after the second eigenvalue, proving a clear cut-off between the second and the third principal component.

Figure 1.

Scree plot—eigenvalues of correlation matrix. Source: Authors’ own work.

However, according to the rule of thumb suggested by Kaiser [47], the components registering eigenvalues greater than one unit will be kept. Consequently, we will retain two principal components.

The factor-loading matrix is conveyed in Table 5 and shows the correlations between the observed variables and components.

Table 5.

Factor pattern.

Thus, the first component registers large negative loadings for and , while the second principal component registers the highest loadings on and . Hence, we will consider the first principal component an indicator that measures the risk related to shareholders’ wealth (RSWI) and the second principal component an indicator which emphasizes short-term risk (STRI).

Table 6 discloses the eigenvectors of the correlation matrix. In fact, each eigenvector comprises the coefficients of the linear equation for a certain component. Afterwards, we have computed the component scores by multiplying the loadings with the original variables.

Table 6.

Eigenvectors of correlation matrix.

Further, our aim is to substantiate a global business failure risk tool based on the two retained components. Initially, we will compute coefficients of importance (CI) for both of the components, as follows:

As such, = 71.51927/84.0237, whereas = 12.50444/84.0237, hence resulting = 0.85118 and = 0.14882.

Subsequently, the values of the GBFRT for the companies from our sample will be acquired based on the following formula:

Accordingly, we will employ GBFRT, as well as RSWI and STRI as explanatory variables within the regression framework.

4.3. Regression Analyses

The estimations towards the influence of CEO characteristics (in terms of duality, gender, age, and tenure) on business failure risk, by means of multivariate regressions, are exhibited in Table 7.

Table 7.

The impact of CEO characteristics on business failure risk.

We notice that CEO gender negatively influence RSWI (model 1) and GBFRT (model 3), therefore H2 is statistically validated. Within our selected sample, only nine CEOs are women, thus emphasizing the barriers of females towards accession to top management. In addition, board size negatively influences only STRI (model 2), H5 being partially statistically validated. We acknowledge that, in mean, the boards of selected companies comprise four members. Accordingly, Yermack’s [26] assertion is sustained, since smaller boards are more effective.

As regards, CEO duality, CEO age, as well as CEO tenure, we could not statistically validate any relationship. Consequently, H1, H3, H4 are rejected. Moreover, we acknowledge a mixed influence of firm size on business failure risk: negative (model 1 and model 3) and positive (model 2).

The econometric output regarding the effect of board independence (accounting for the percentage of non-executive and independent directors on board) on business failure risk is pointed out in Table 8. The estimations support the lack of any statistically significant association between board independence and business failure risk; thus H6 was rejected. In addition, the negative influence of board size on STRI is reinforced (model 2 and model 5). In addition, we identified that the establishment of an Audit Committee negatively influence STRI (model 2 and model 5); therefore H8 was statistically validated for AC. We found that 31 companies from our sample established AC. In fact, we expect a decrease of earnings management being reinforced Bedard et al. [39]. Regarding firm-level control variables, the mixed influence of firm size is reconfirmed.

Table 8.

The impact of board independence on business failure risk.

The empirical findings related to the effect of board diversity (particularly women on boards, board size, and Consultative Committees) on business failure risk are provided in Table 9. Thus, we could not statistically validate the link between board gender diversity, as measured by the percentage of female directors on board, and business failure risk. Therefore, H7 is rejected. Furthermore, the negative influence of board size and AC is reinforced (model 2). Thus, we strengthen the mixed relationship between firm size and business failure risk.

Table 9.

The impact of board diversity on business failure risk.

As regards the standard errors of the estimated regressions within the research, we notice a low estimated variance of the residuals.

5. Conclusions

This paper explored the link between CEO characteristics (duality, gender, age, and tenure), board characteristics (size, independence, diversity, Consultative Committees), and risk management for the companies listed in Romania. We have employed principal components analysis for ten indicators out of annual financial statements, with only two principal components retained that explain 84.0237% of data variation and which signify risk indicators regarding shareholders’ wealth and short-term risk. Moreover, based on the retained principal components, a global business failure risk tool was developed. Subsequently, by applying a regression approach, the empirical findings revealed statistically significant negative relationships between CEO gender, board size, Audit Committee, and business failure risk. However, it should be considered that the relationships are not robust to all specifications. In fact, the research limitations are depicted by the reduced sample size, as well as having only one year of investigation. As future research avenues, we aim to develop a business failure risk indicator by considering neural network architecture.

Corporate governance is regularly regarded as a device aiming to secure shareholder wealth against opportunistic managers. In fact, dilemma takes place when management seeks private benefits instead of long-term sustainability. However, the board of directors should be aware of risks and opportunities of the corporations, whilst sustainability concerns should be considered as part of their daily responsibilities. Therefore, boards are in charge of reinforcing governance tools, alongside risk management and internal control, as well as operating consistently with the doctrines of social responsibility. In the context of contemporary global challenges, boards of directors should consider the requisite to nominate highly skilled members showing varied qualifications, viewpoints, and knowledge. Male and female representation on boards, with diverse geographical membership, proficiency, and competence could set the suitable partnership that integrates conceptions, cleverness, and solutions to design and accomplish the successful path in order to enhance shareholder value. However, boards with narrowed perspectives are not able to reflect towards potential the companies could have within the worldwide market. Accordingly, boards comprising members which have kindred training will be unfruitful on carrying out corporate sustainability strategies that are fundamental to the company and its forthcoming progress. As trustworthy corporate citizens, the companies are expected to reply to the demands of society, as well as maintaining unaltered the natural environment on which rely current and subsequent generations. A good corporate governance cannot prevail if the companies are not providing a balance of social, economic, and environmental concerns, which represent the frame of sustainable development. Furthermore, the accountability and engagement with respect to sustainability could be emphasized by incorporating sustainability concerns within board committees’ charters. In addition, as a driver of investor confidence and employee trustworthiness, sustainability reporting should evolve forward to become a mainstream business practice.

Author Contributions

These authors contributed equally to this work. All authors read and approved the final manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Pal, R.; Torstensson, H.; Mattila, H. Antecedents of organizational resilience in economic crises-an empirical study of Swedish textile and clothing smes. Int. J. Prod. Econ. 2014, 147, 410–428. [Google Scholar] [CrossRef]

- Markman, G.M.; Venzin, M. Resilience: Lessons from banks that have braved the economic crisis—And from those that have not. Int. Bus. Rev. 2014, 23, 1096–1107. [Google Scholar] [CrossRef]

- Teixeira, E.D.; Werther, W.B. Resilience: Continuous renewal of competitive advantages. Bus. Horiz. 2013, 56, 333–342. [Google Scholar] [CrossRef]

- Williams, N.; Vorley, T. Economic resilience and entrepreneurship: Lessons from the Sheffield City region. Entrep. Reg. Dev. 2014, 26, 257–281. [Google Scholar] [CrossRef]

- Hamilton, B.A. Redefining the Corporate Governance Agenda—From Risk Management to Enterprise Resilience. 2004. Available online: https://www.boozallen.com/content/dam/boozallen/media/file/138022.pdf (accessed on 24 January 2017).

- Sabatino, M. Economic crisis and resilience: Resilient capacity and competitiveness of the enterprises. J. Bus. Res. 2016, 69, 1924–1927. [Google Scholar] [CrossRef]

- Hamel, G.; Valikangas, L. The quest for resilience. Harv. Bus. Rev. 2003, 81, 52–63. [Google Scholar] [PubMed]

- Lampel, J.; Bhalla, A.; Jha, P.P. Does governance confer organisational resilience? Evidence from UK employee owned businesses. Eur. Manag. J. 2014, 32, 66–72. [Google Scholar] [CrossRef]

- Castellacci, F. Institutional voids or organizational resilience? Business groups, innovation, and market development in Latin America. World Dev. 2015, 70, 43–58. [Google Scholar] [CrossRef]

- Tait, P.; Loosemore, M. The corporate governance of Australian listed construction companies. Australas. J. Constr. Econ. Build. 2009, 9, 7–16. [Google Scholar] [CrossRef]

- Liang, D.; Lu, C.C.; Tsai, C.F.; Shih, G.A. Financial ratios and corporate governance indicators in bankruptcy prediction: A comprehensive study. Eur. J. Oper. Res. 2016, 252, 561–572. [Google Scholar] [CrossRef]

- Fich, E.M.; Slezak, S.L. Can corporate governance save distressed firms from bankruptcy? An empirical analysis. Rev. Quant. Financ. Account. 2008, 30, 225–251. [Google Scholar] [CrossRef]

- Hambrick, D.C.; D’Aveni, R.A. Top team deterioration as part of the downward spiral of large corporate bankruptcies. Manag. Sci. 1992, 38, 1445–1466. [Google Scholar]

- Jensen, M.C. The modern industrial-revolution, exit, and the failure of internal control-systems. J. Financ. 1993, 48, 831–880. [Google Scholar] [CrossRef]

- Matolcsy, Z.; Stocks, D.; Wright, A. Do independent directors add value? Aust. Account. Rev. 2004, 14, 33–40. [Google Scholar] [CrossRef]

- Croson, R.; Gneezy, U. Gender differences in preferences. J. Econ. Lit. 2009, 47, 448–474. [Google Scholar] [CrossRef]

- Bliss, R.T.; Potter, M.E. Mutual fund managers: Does gender matter? J. Bus. Econ. Stud. 2002, 8, 1–15. [Google Scholar]

- Adams, R.B.; Funk, P. Beyond the glass ceiling: Does gender matter? Manag. Sci. 2012, 58, 219–235. [Google Scholar] [CrossRef]

- Berger, A.N.; Kick, T.; Schaeck, K. Executive board composition and bank risk taking. J. Corp. Financ. 2014, 28, 48–65. [Google Scholar] [CrossRef]

- Holmstrom, B. Managerial incentive problems: A dynamic perspective. Rev. Econ. Stud. 1999, 66, 169–182. [Google Scholar] [CrossRef]

- Bucciol, A.; Miniaci, R. Household portfolios and implicit risk preference. Rev. Econ. Stat. 2011, 93, 1235–1250. [Google Scholar] [CrossRef]

- Serfling, M.A. Ceo age and the riskiness of corporate policies. J. Corp. Financ. 2014, 25, 251–273. [Google Scholar] [CrossRef]

- Hermalin, B.E.; Weisbach, M.S. Endogenously chosen boards of directors and their monitoring of the CEO. Am. Econ. Rev. 1998, 88, 96–118. [Google Scholar]

- Chen, D.; Zheng, Y. Ceo tenure and risk-taking. Glob. Bus. Financ. Rev. 2014, 19, 1–27. [Google Scholar] [CrossRef]

- Ferrero-Ferrero, I.; Fernandez-Izquierdo, M.A.; Munoz-Torres, M.J. Integrating sustainability into corporate governance: An empirical study on board diversity. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 193–207. [Google Scholar] [CrossRef]

- Yermack, D. Higher market valuation of companies with a small board of directors. J. Financ. Econ. 1996, 40, 185–211. [Google Scholar] [CrossRef]

- Uzun, H.; Szewczyk, S.H.; Varma, R. Board composition and corporate fraud. Financ. Anal. J. 2004, 60, 33–43. [Google Scholar] [CrossRef]

- Wang, C.-J. Board size and firm risk-taking. Rev. Quant. Financ. Account. 2012, 38, 519–542. [Google Scholar] [CrossRef]

- Wang, T.W.; Hsu, C. Board composition and operational risk events of financial institutions. J. Bank. Financ. 2013, 37, 2042–2051. [Google Scholar] [CrossRef]

- Heslin, P.; Donaldson, L. An organizational portfolio theory of board composition. Corp. Gov. Int. Rev. 1999, 7, 81–88. [Google Scholar] [CrossRef]

- Minton, B.A.; Taillard, J.P.; Williamson, R. Financial expertise of the board, risk taking, and performance: Evidence from bank holding companies. J. Financ. Quant. Anal. 2014, 49, 351–380. [Google Scholar] [CrossRef]

- Shrivastava, P.; Addas, A. The impact of corporate governance on sustainability performance. J. Sustain. Financ. Invest. 2014, 4, 21–37. [Google Scholar] [CrossRef]

- Post, C.; Rahman, N.; McQuillen, C. From board composition to corporate environmental performance through sustainability-themed alliances. J. Bus. Ethics 2015, 130, 423–435. [Google Scholar] [CrossRef]

- Byrnes, J.P.; Miller, D.C.; Schafer, W.D. Gender differences in risk taking: A meta-analysis. Psychol. Bull. 1999, 125, 367–383. [Google Scholar] [CrossRef]

- Beckmann, D.; Menkoff, L. Will women be women? Analyzing the gender difference among financial experts. Kyklos 2008, 61, 364–384. [Google Scholar] [CrossRef]

- European Commission. Proposal for a Directive of the European Parliament and of the Council on Improving the Gender Balance among Non-Executive Directors of Companies Listed on Stock Exchanges and Related Measures. 2012. Available online: http://www.europa-nu.nl/id/vjno4j3jwvzz/proposal_for_a_directive_of_the_european (accessed on 24 January 2017).

- Ben-Amar, W.; Chang, M.; McIlkenny, P. Board gender diversity and corporate response to sustainability initiatives: Evidence from the carbon disclosure project. J. Bus. Ethics 2015. [Google Scholar] [CrossRef]

- Klein, A. Audit committee, board of director characteristics, and earnings management. J. Account. Econ. 2002, 33, 375–400. [Google Scholar] [CrossRef]

- Bedard, J.; Chtourou, S.M.; Courteau, L. The effect of audit committee expertise, independence, and activity on aggressive earnings management. Audit. J. Pract. Theory 2004, 23, 13–35. [Google Scholar] [CrossRef]

- Bliss, M.A.; Muniandy, B.; Majid, A. Ceo duality, audit committee effectiveness and audit risks: A study of the Malaysian market. Manag. Audit. J. 2007, 22, 716–728. [Google Scholar] [CrossRef]

- Sun, J.; Liu, G.P. Audit committees’ oversight of bank risk-taking. J. Bank. Financ. 2014, 40, 376–387. [Google Scholar] [CrossRef]

- Han, J.; Kamber, M. Data Mining: Concepts and Techniques, 2nd ed.; Morgan Kaufmann Publishers: San Francisco, CA, USA, 2006. [Google Scholar]

- Jolliffe, I.T. Principal Component Analysis, 2nd ed.; Springer: New York, NY, USA, 2002. [Google Scholar]

- Bucharest Stock Exchange. Bucharest Stock Exchange Corporate Governance Code. 2008. Available online: http://www.ecgi.org/codes/documents/bucharest_se_code_jan2009_en.pdf (accessed on 24 January 2017).

- Bucharest Stock Exchange. Guide for Implementing the Corporate Governance Code. 2010. Available online: http://www.bvb.ro/info/Rapoarte/Diverse/Ghid%20GC_Ed1_martie%202010.pdf (accessed on 24 January 2017).

- Cattell, R.B. The scree test for the number of factors. Multivar. Behav. Res. 1966, 1, 245–276. [Google Scholar] [CrossRef] [PubMed]

- Kaiser, H.F. The application of electronic computers to factor analysis. Educ. Psychol. Meas. 1960, 20, 141–151. [Google Scholar] [CrossRef]

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).