Managing Sustainability of Fennoscandian Forests and Their Use by Law and/or Agreement: For Whom and Which Purpose?

Abstract

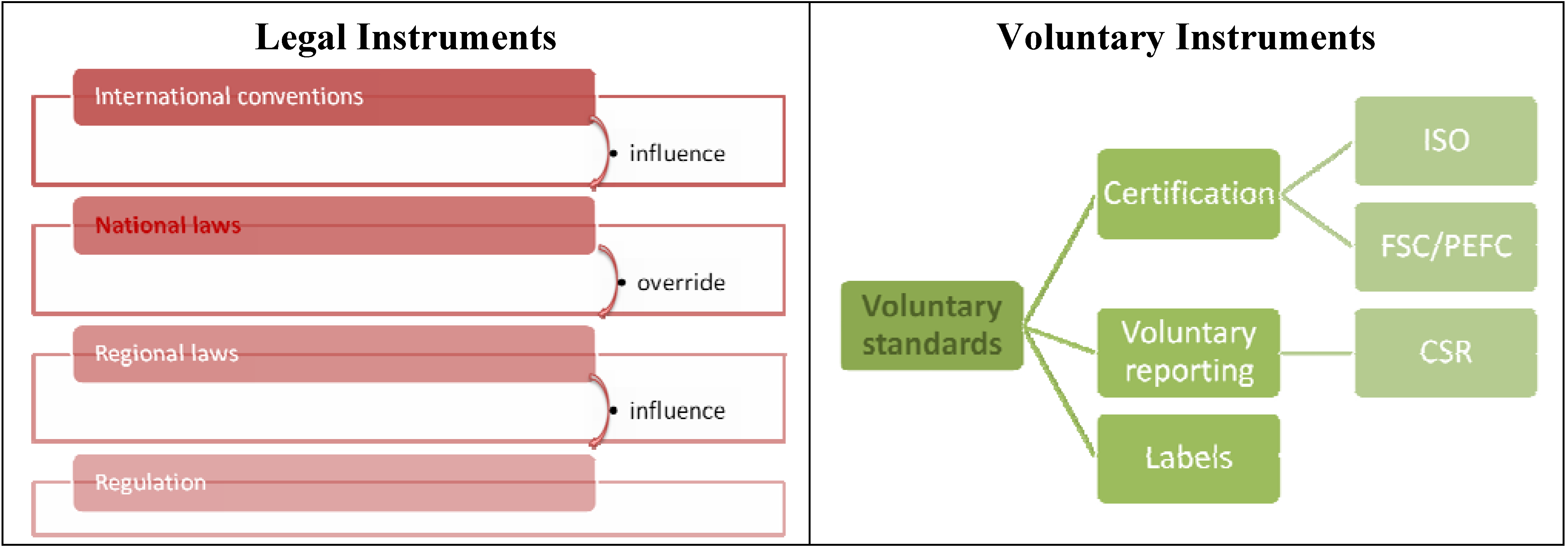

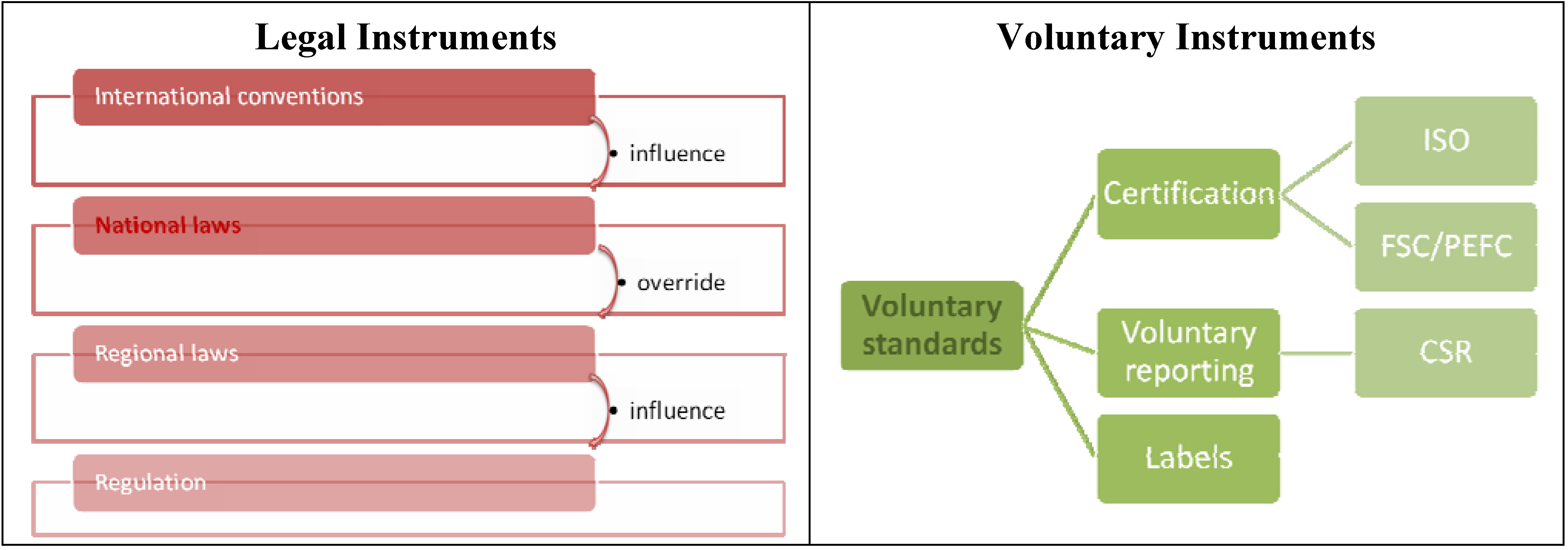

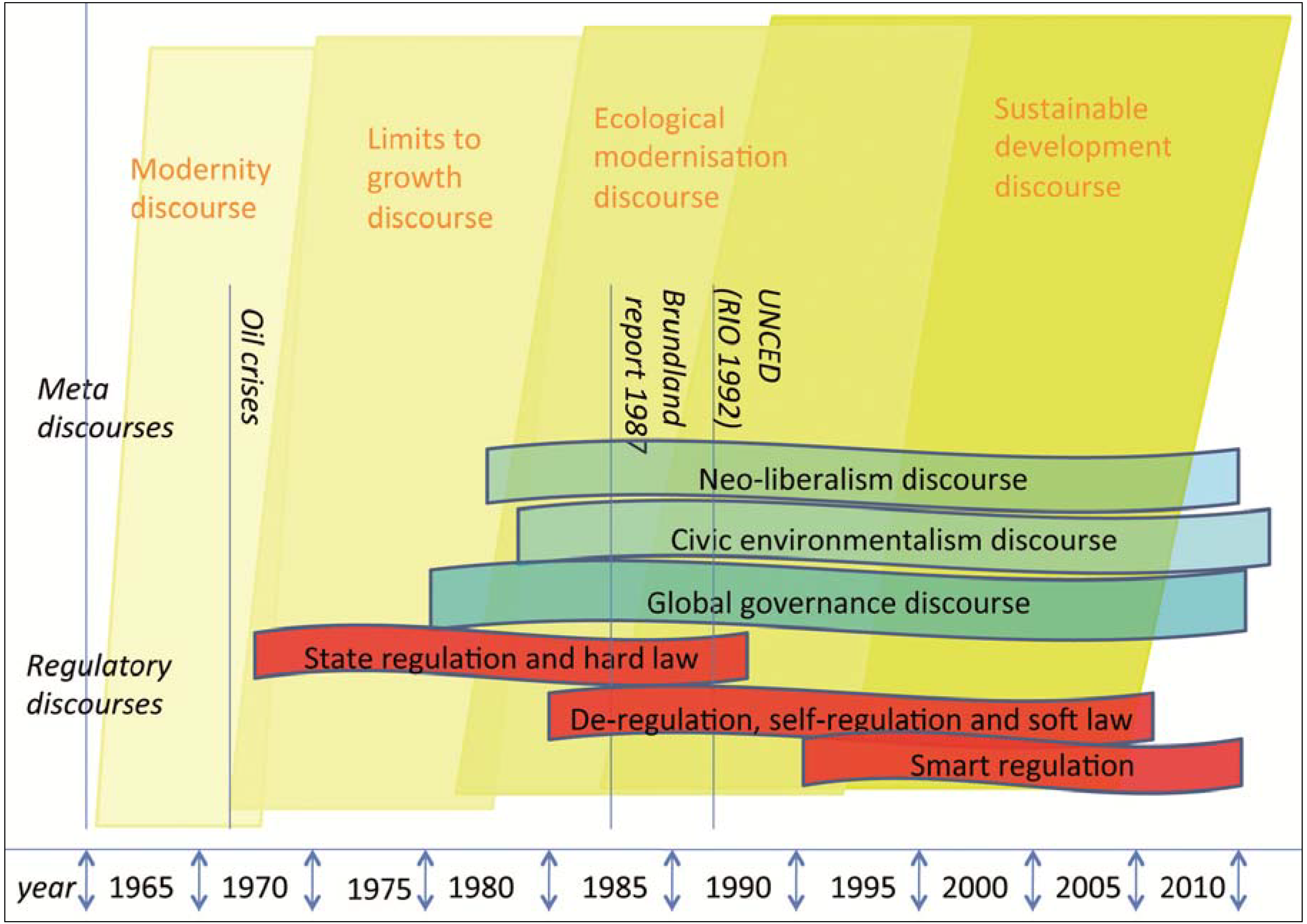

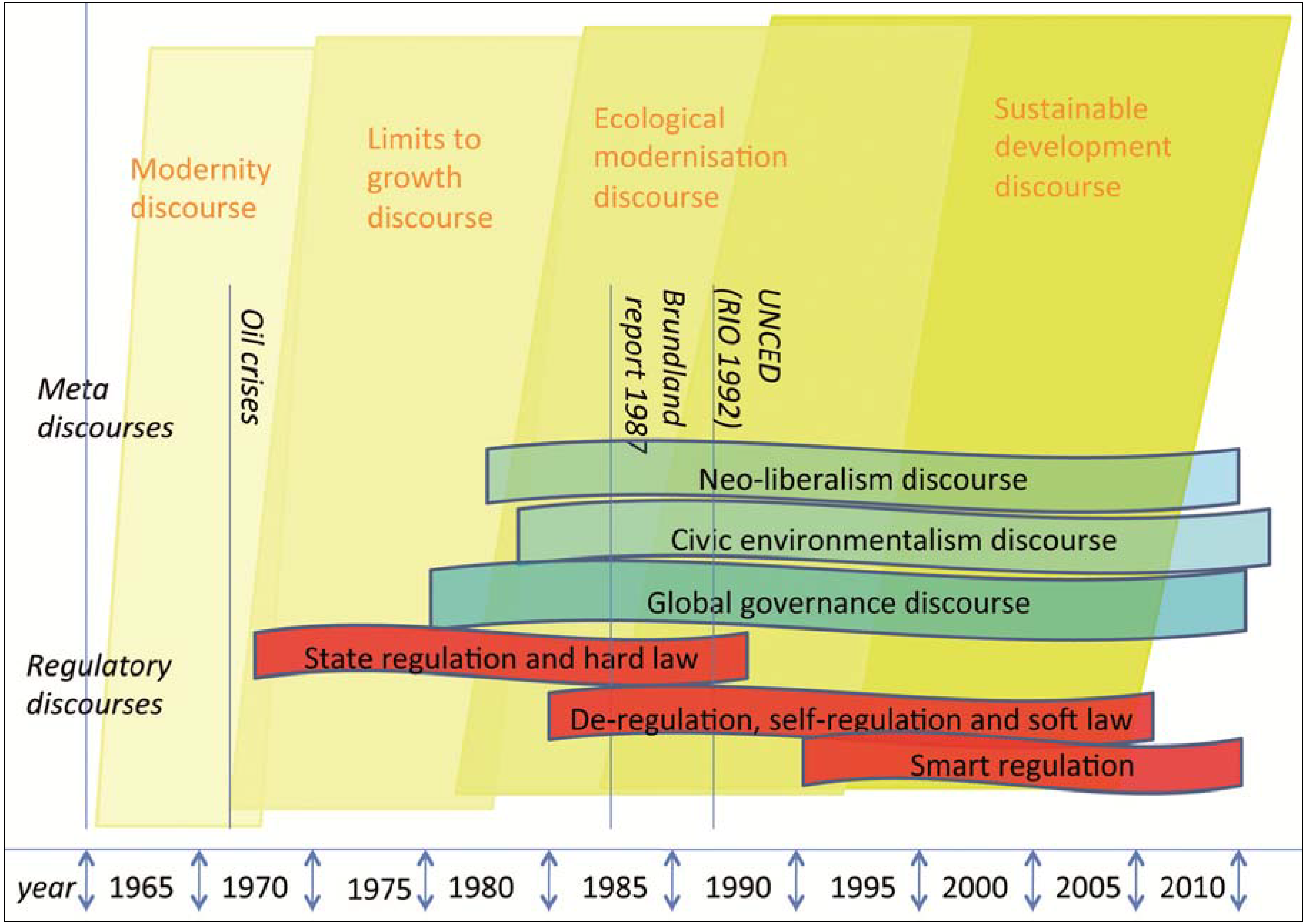

:1. Introduction

- (a)

- Hard international legal instruments with a forest-related mandate and sanctions (such as the Convention on Biological Diversity (CBD) and United Nations Framework Convention on Climate Change (UNFCCC));

- (b)

- Growing body of soft international law focused on forests, which are not legally binding or not followed by sanctions for non-fulfilment, such as the Non-Legally Binding Instrument (NLBI) [26] and other decisions of the United Forum on Forests (UNFF), IPF/IFF (Intergovernmental Panel on Forests (IPF) and the Intergovernmental Forum on Forests (IFF)) proposals for action, the Forest Principles and Chapter 11 of Agenda 21 [24,27];

- (c)

- Voluntary private sector regulation, such as the FSC (Forest Stewardship Council) principles for forest management [28].

Aim of this Paper

2. Material and Methods

- (1)

- Voluntary instruments are classified into two instrument categories: instruments with regulatory power, like certification and voluntary standards, and voluntary, non-regulatory instruments like CSR and SIA (see Table 1). Instrument categories are understood as a grouping of instruments following similar concepts. Instruments are means of implementing defined measures, concepts or ideas.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Instrument category | Instrument | Approach to represent instrument |

|---|---|---|

| Voluntary and regulatory instruments | Voluntary standards (ISO) | ISO14040: LCA |

| Certification | FSC Certification | |

| Voluntary and non-regulatory instruments | CSR reporting | CSR (IKEA) |

| Reporting on Sustainability impacts (SIA) | SIA (ToSIA) |

- (2)

- To give more tangible examples, for each instrument a representative approach is described in the following steps:

- Background of the instrument

- Approaches used within this instrument with a discourse of

- ○

- Definition and implementation: Details about the approach and its historic background are given. The aspects of sustainability it targets are described with details about the scope of the assessment (system boundary).

- ○

- Strengths: Strengths are presented based on empirical observations, experiences from practice and literature.

- ○

- Weaknesses: Weaknesses are presented based on empirical observations, experiences from practice and literature.

- ○

- Suitability and actors: The suitability to assess or prove the sustainability assessment of a product, processes, or code of conduct) are clarified and potential actors for whom this approach or instrument is suitable are described.

- (3)

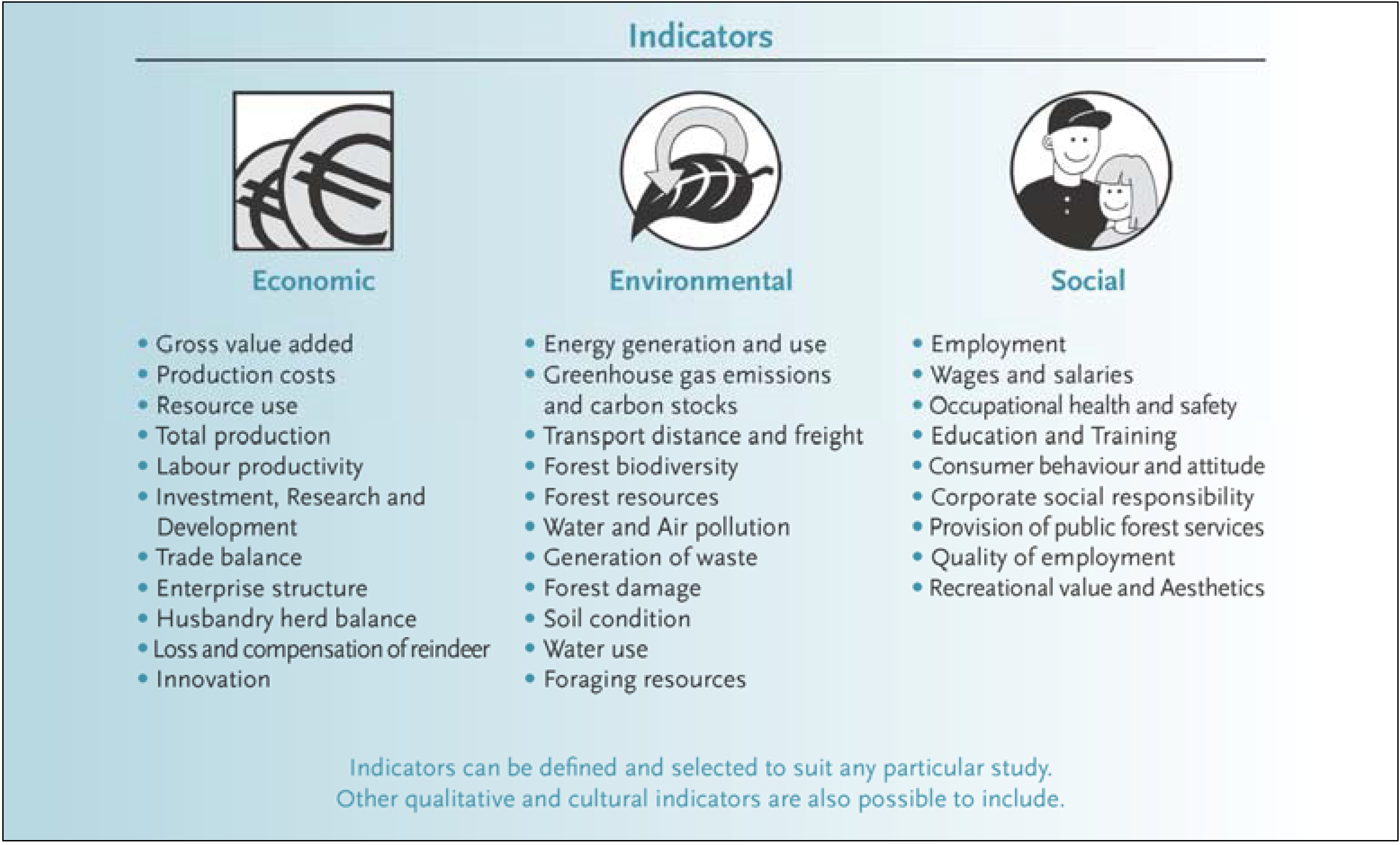

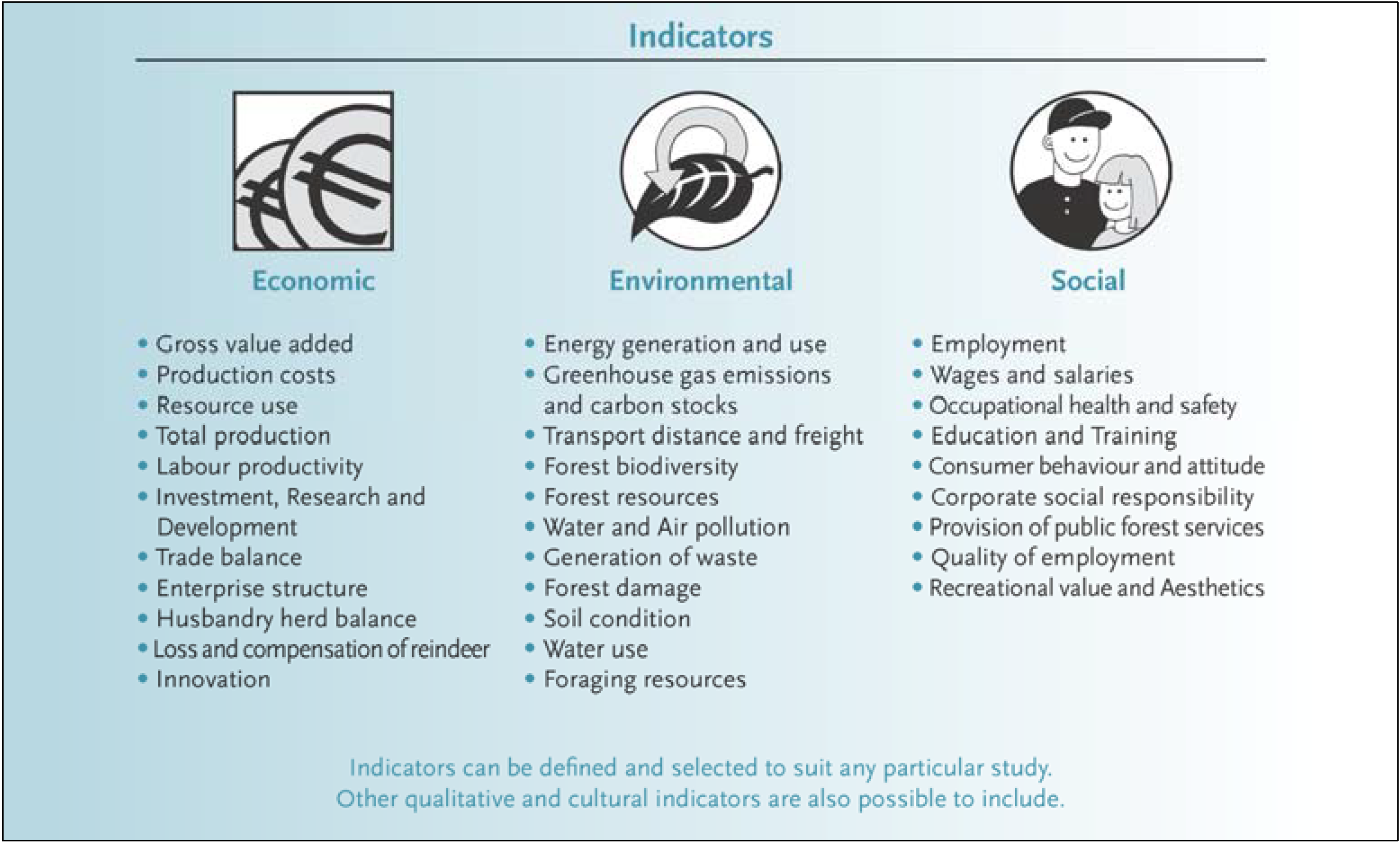

- The focus is on approaches as a way of dealing with certain concepts, rather than on specifically defined methods or tools. The reason behind is that for some instruments only recommended approaches exist. The detailed method or tools to implement them can be developed by the companies applying it. After the individual and detailed descriptions for each instrument and approach, they are assessed comparatively with respect to the sustainability dimensions each one covers (Section 3.3.). The traditional separation into economic, environmental and social aspects of sustainability turned out to be too simplistic and instead we used: work place, human rights, community, market place, environment and economy. These categories were chosen based on ISO26000 categories for social responsibility, supplemented with the dimension of economy. Each category is divided in sub-aspects which it covers. These sub-aspects are described and calculated by a set of indicators which each approach uses. For better analysis these indicators were condensed to a limited number of representative main indicators per sustainability dimension, as described in detail in Table 2.

| Sustainability dimension | Indicators |

|---|---|

| Workplace | Workforce profile |

| Safety and health | |

| Equal opportunity | |

| Work satisfaction/perception. Attractive employer | |

| Staff development | |

| Human rights | Human rights |

| Anti-force and child labour | |

| Indigenous rights | |

| National/international rights conformance | |

| Stakeholder perception | |

| Community | Local community impacts |

| Anti-corruption /transparency | |

| Public perception of company (Company brand) | |

| Marketplace | Customer perception |

| Product safety | |

| Advertising and product recognition (Product brand) | |

| Environment | Resource and Environment |

| Consumption | |

| Emission | |

| Waste/recycling | |

| Low environmental Impact | |

| Landuse and protection of biodiversity | |

| Economy | Costs |

| Gross value added | |

| Investment |

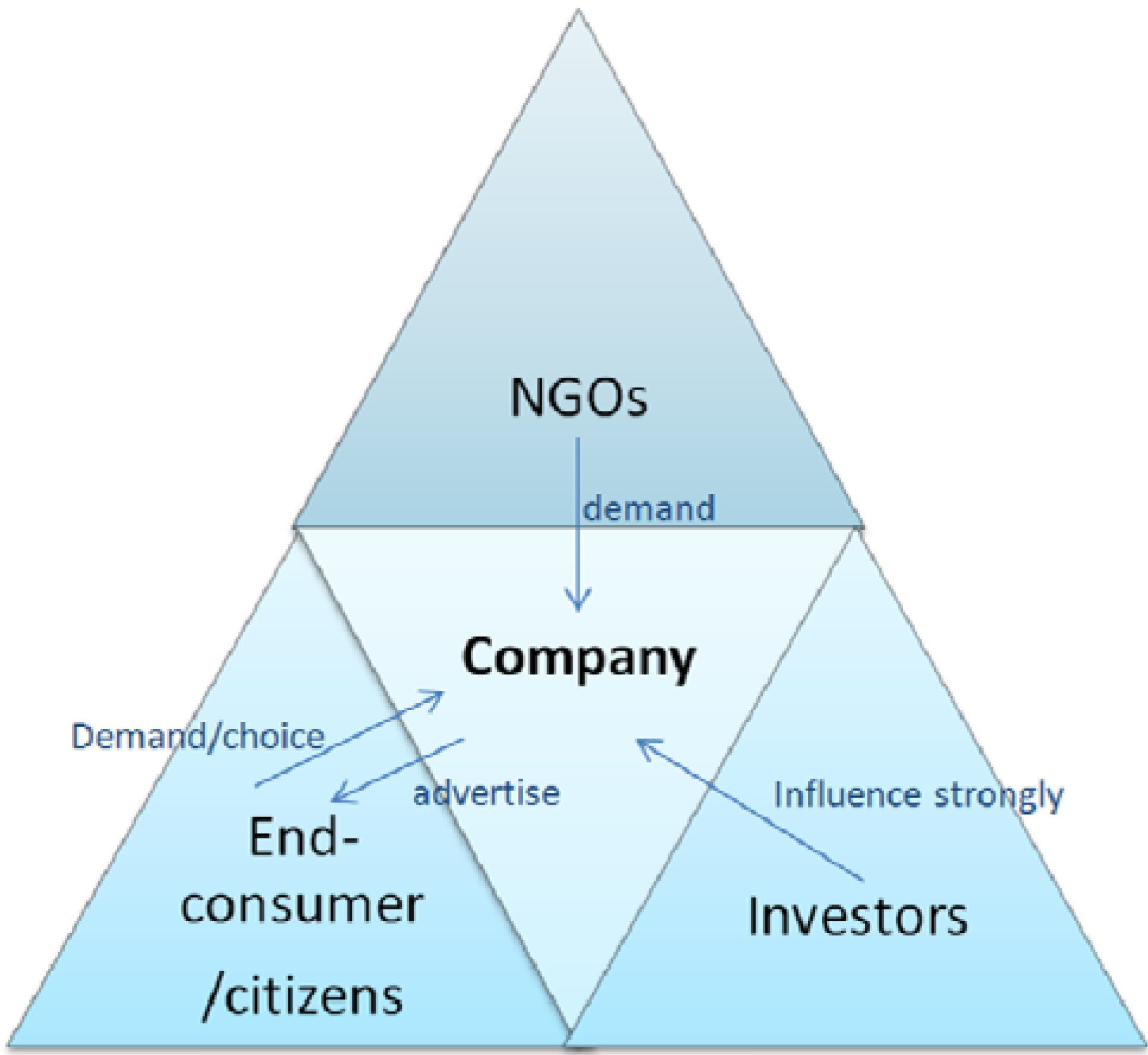

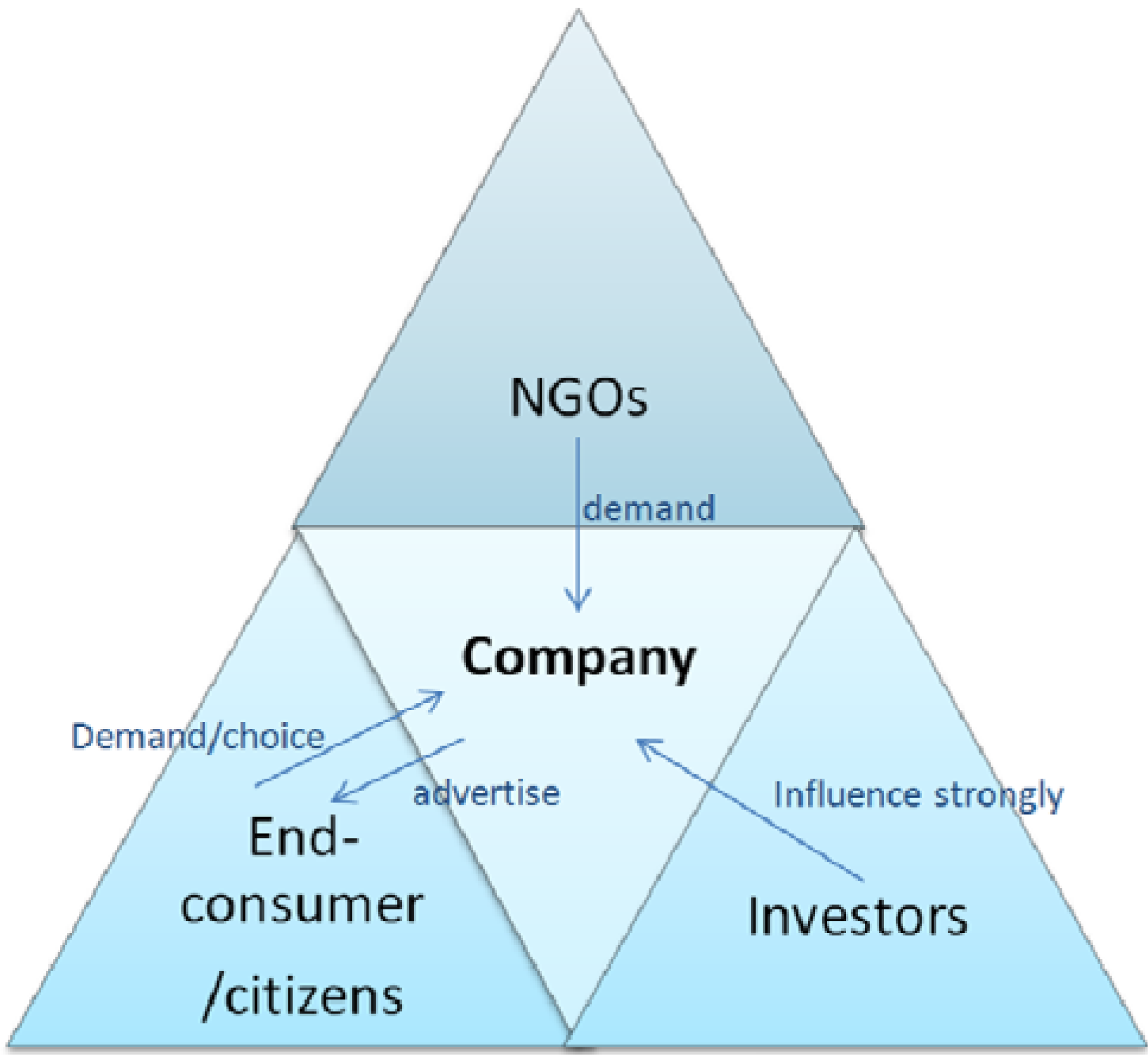

Roles and Interaction of Actors:

- ‐

- Investors have an interest in high and stable returns on investments, while minimizing risks. Risks for a company can take different forms such as the volatility of global and local markets, prices of raw materials, but most important are reputational risks and operational risks with regards to the fulfilment of environmental obligations [34,35]. Adherence to more strict regulations and initiative in good governance and production are usually investor driven. Investors are influential, as companies are dependent on their investments, and often major investors are represented in the decision making body of a company.

- ‐

- NGOs (non-governmental organisations) are one of the external drivers demanding high standards and responsible treatment of the natural environment in the name of public interest. Thus, their demands and activities link directly to publicity, and in consequence, to financial risks related to the production environment of companies. NGOs are important actors influencing the use and development of both legal and voluntary instruments [24,36].

- ‐

- Business customers, end-users and citizens, are important driving forces for company practices and markets. Companies anticipating a market premium may offer end customers products with an eco-friendly reputation. The end users i.e., the public, are usually in a national setting which relates to certain regional or national legislation and standards. The purchasing of public contracts may have a significant environmental or social impact. Therefore, purchases with public money are regulated by the EU directive 2004/18 [37]. In recent years, customers have also become more aware and active in demanding product safety, and ethical production practices. Market competition drives companies to respond to customer demands in a forward acting and informative matter [37].

3. Results: Sustainability Assessments in Voluntary Instruments

3.1. Standards Replace Legislation

3.2. Voluntary Instruments with Regulatory Power: Certification and Voluntary Standards

3.2.1. Approaches Used in Voluntary, Regulatory Instruments: FSC Certification

3.2.1.1. Definition and Implementation of Standards and Certification, and Example from FSC

3.2.1.2. Strengths

3.2.1.3. Weaknesses

3.2.1.4. Suitability and Actors

3.2.2. Approaches Used in Voluntary, Regulatory Instrument: ISO Standard 14040 on Life Cycle Analysis (LCA)

3.2.2.1. Definition and Implementation, and an Example from ISO14040

- (1)

- Goal and scope definition

- (2)

- Inventory analysis, and

- (3)

- Impact assessment, referring to certain impact categories as e.g., Global Warming Potential and Acidification.

3.2.2.2. Strengths

3.2.2.3. Weaknesses

3.2.2.4. Suitability and Actors

3.3. Voluntary, Non-Regulatory Instruments: CSR and Other Reporting Practices in the Industry

- Principle 1: Support and respect the protection of internationally proclaimed human rights.

- Principle 2: Make sure that they are not complicit in human rights abuses.

- Principle 3: The freedom of association and the effective recognition of the right to collective bargaining.

- Principle 4: the elimination of all forms of forced and compulsory labour.

- Principle 5: the effective abolition of child labour.

- Principle 6: the elimination of discrimination in employment and occupation.

- Principle 7: Support a precautionary approach to environmental challenges.

- Principle 8: Undertake initiatives to promote environmental responsibility.

- Principle 9: Encourage the development and diffusion of environmentally friendly technologies.

- Principle 10: Businesses should work against corruption in all its forms, including extortion and bribery.

3.3.1. Approaches Used in Voluntary Reporting: Cooperate Social Responsibility (CSR)

3.3.1.1. Definition and Implementation, an Example from IKEA

3.3.1.2. Strengths

3.3.1.3. Weaknesses

3.3.1.4. Suitability and Actors

3.3.2. Approaches Used in Voluntary Reporting: SIA Approach

3.3.2.1. Definition and Implementation, Example of ToSIA

3.3.2.2. Strengths

3.3.2.3. Weaknesses

3.3.2.4. Suitability and Actors

3.4. Comparison of Voluntary Instruments on the Covered Sustainability Dimensions

| CSR | CSR | ISO 26000:2010 | Forest Management Standard | ISO 14000-family | SIA |

|---|---|---|---|---|---|

| Global Reporting Initiative (1997) | UN Global Compact (1999) | ISO 26000 on Social Responsibility | FSC | 14000 on Environmental Management | Sustainability Impact Assessment |

| Sustainability dimension: Work place | |||||

| GRI: Labour practices and decent work | UN GC: Labour Standards | Labour practices 6.4 | Principle 4, Principle 8 | ISO Reporting: Workplace | Social indicators |

| Sustainability dimension: Human rights | |||||

| GRI: Human rights | UN GC: Human Rights | Human rights 6.3 | Principle 1, Principle 3 | ISO Reporting: Human rights | (potential) |

| Sustainability dimension: Community | |||||

| GRI: Society | UN GC: Transparency/Anti-corruption | Fair operating practices 6.6, Community involvement and development 6.8 | Principle 2, Principle 4, Principle 5, Principle 8 | ISO Reporting: Community | (potential) |

| Sustainability dimension: Market place | |||||

| GRI: Product responsibility | Consumer issues 6.7 | Principle 9 | ISO Reporting: Marketplace | (potential) | |

| Sustainability dimension: Environment | |||||

| UN GC: Environment | The environment 6.5 | Principle 6, Principle 8 | ISO Reporting: Environment | Environmental indicators | |

| Sustainability dimension: Economy | |||||

| Economic indicators | |||||

4. Discussion and Conclusion: Summary of Suitability and Trends of Introduced Approaches

4.1. In Short—Which Approach is Suitable for Which Purpose?

- ■ For comparative, operations- and management-related questions (=processes) with a clear system boundary, SIA is suitable.

- ■ While for stand-alone, product related assessments which need to cover a wide range of the lifecycle of the product itself and the raw materials and facilities to produce this product, LCA is suitable (=Environmental Product Declaration).

- ■ A company’s code of conduct in terms of sustainable behaviour can so far only be assessed through CSR, and the contents thereof have to be defined by the company itself. ISO 26000 gives merely guidelines for assessment.

4.2. Why Are Voluntary Instruments Gaining More Ground and Getting More Important for Sustainable Management?

4.3. How Does SIA Add Value to above Approaches, and What Are Development Trends for Voluntary Instruments?

Abbreviations

| CBD | Convention on Biological Diversity |

| CERES | Coalition for Environmentally Responsible Economies |

| CSR | Cooperate Social Responsibility |

| EIA | Environmental Impact Assessment |

| EMS | Environmental Management Systems |

| EUTR | European Timber Regulation |

| FLEGT | Forest Law Enforcement, Governance and Trade |

| FSC | Forest Stewardship Council |

| GFEP | Global Panel of Forest Experts |

| GRI | Global Reporting Initiative |

| IA | Impact Assessment |

| ISO | International Standard Organisation |

| ITTO | International Tropical Timber Organisation |

| NFP | National Forestry Programme |

| NGO | Non-Governmental Organisation |

| PEFC | Programme for the Endorsement of Forest Certification |

| RFP | Regional Forest Programme |

| SEA | Strategic Environmental Assessment |

| SIA | Sustainability Impact Assessment |

| SME | small- to medium-sized enterprise |

| STG | Standard Trading Group |

| ToSIA | Tool for Sustainability Impact Assessment |

| UNCED | United Nations Conference on Environment and Development |

| UNEP | United Nations Environment Programme |

| UNFCCC | United Nations Framework Convention on Climate Change |

| VPA | Voluntary Partnership Agreement |

| WCED | World Commission on Environmental and Development |

Acknowledgments

Conflicts of Interest

Appendix

| Categories | Aspects |

|---|---|

| ISO Reporting: Marketplace | Customer complaints about products and services |

| Advertising complaints upheld | |

| Complaints about late payment of bills | |

| Upheld cases of anti-competitive behaviour | |

| Customer satisfaction levels | |

| Customer retention | |

| Provision for customers with special needs | |

| Average time to pay bills to suppliers | |

| Customer loyalty measures | |

| Recognising and catering for diversity in advertising and product labelling | |

| Social impact, cost or benefits, of the company’s core products and services | |

| Cash value of company support as % of pre-tax profit | |

| Estimated combined value of staff company time, gifts in kind and management costs | |

| Individual value of staff time, gifts in kind and management costs | |

| ISO Reporting: Environment | Overall energy consumption |

| Water usage | |

| Quantity of waste produced by weight | |

| Upheld cases of prosecution for environmental offences | |

| CO2/greenhouse gas emissions | |

| Other emissions (e.g., Ozone, Radiation, SOx, NOx etc.) | |

| Use of recycled material | |

| Percentage of waste recycled | |

| Net CO2 contribution made | |

| Environmental impact over the supply chain | |

| Environmental impact, benefits or costs, of companies core products and services | |

| Any upheld non-compliances with domestic human rights legislation | |

| Existence of confidential grievance procedures for workers | |

| Wage rates | |

| ISO Reporting: Workplace | Workforce profile: gender, race, disability, age |

| Workforce profile compared to the community profile for travel to work area: gender, race, disability, age | |

| Staff absenteeism | |

| Number of legal non-compliances on health, safety, equal opportunities legislation | |

| Number of staff grievances | |

| Upheld cases of corrupt or unprofessional behaviour | |

| Number of recordable incidents (fatal and non-fatal) including sub-contractors | |

| Staff turnover | |

| Value of training and development provided to staff | |

| Pay and conditions compared against local equivalent averages | |

| Impact evaluations of the effects of downsizing, restructuring etc. | |

| Perception measures of the company by its employees | |

| ISO Reporting: Community | Project progress and achievement measures |

| Leverage of other resources | |

| Impact evaluations carried out on community programmes | |

| Perception measures of the company as a good neighbour | |

| ISO Reporting: Human rights | Progress measures against adherence to stated business principles on human rights as stated by law and international human rights standards |

| Proportion of suppliers and partners screened for human rights compliance | |

| Proportion of suppliers and partners meeting the company’s expected standards on human rights | |

| Proportion of company’s managers meeting the company's standards on human rights within their area of operation |

References

- Carlowitz, H.C.V. Sylvicultura Oeconomica: Anweisung zur Wilden Baum-Zucht; (in German). Braun: Leipzig, Germany, 1713. [Google Scholar]

- World Commission on Environment and Development (Brundtland Commission). Our Common Future; Oxford University Press: Oxford, UK, 1987; p. 383. [Google Scholar]

- Dietz, S.; Neumayer, E. Weak and strong sustainability in the SEEA: Concepts and measurement. Ecol. Econ. 2007, 61, 617–626. [Google Scholar]

- Cabeza-Gutés, M. The concept of weak sustainability. Ecol. Econ. 1996, 17, 147–156. [Google Scholar] [CrossRef]

- Rennings, K.; Wiggering, H. Steps towards indicators of sustainable development: Linking economic and ecological concepts. Ecol. Econ. 1997, 20, 25–36. [Google Scholar]

- World Commission on Environment and Development (WCED). Our Common Future: United Nations World Commission on Environment and Development (Chaired by Gro Brundtland); Oxford University Press: London, UK, 1987. [Google Scholar]

- European Commission. Impact Assessment Guidelines, SEC 791. Available online: http://ec.europa.eu/governance/impact/docs/SEC2005_791_IA%20guidelines_annexes.pdf (accessed on 27 November 2011).

- European Commission. Communication from the Commission on Impact Assessment; Commission of the European Communities: Brussels, Belgium, 2002. [Google Scholar]

- Tscherning, K.; König, B.; Schößer, B.; Helming, K.; Sieber, S. Ex-Ante Impact Assessments (IA) in the European Commission—An Overview. In Sustainability Impact Assessment of Land Use Changes; Helming, K., Pérez-Soba, M., Tabbush, P., Eds.; Springer: Berlin, Gremany, 2008; pp. 17–33. [Google Scholar]

- Helming, K.; Diehl, K.; Bach, H.; Dilly, O.; König, B.; Kuhlman, T.; Perez-Soba, M.; Sieber, S.; Tabbush, P.; Tscherning, K.; et al. Ex-ante impact assessment of policies affecting land use—Part A: Analytical framework. Ecol. Soc. 2011, 16, No. 27. [Google Scholar]

- Gasparatos, A.; Scolobig, A. Choosing the most appropriate sustainability assessment tool. Ecol. Econ. 2012, 80, 1–7. [Google Scholar] [CrossRef]

- Lindner, M.; Suominen, T.; Palosuo, T.; Garcia-Gonzales, J.; Verweij, P.; Zudin, S.; Päivinen, R. ToSIA—A tool for sustainability impact assessment of forest-wood-chains. Ecol. Model. 2010, 221, 2197–2205. [Google Scholar] [CrossRef]

- Vanclay, F. Conceptualising social impacts. Environ. Impact Assess. Rev. 2002, 22, 183–211. [Google Scholar] [CrossRef]

- Forest Stewardship Council (FSC). FSC Principles and Criteria for Forest Stewardship; FSC-STD-01-001 (version 4-0) EN; FSC: Bonn, Germany, 2002; p. 13. [Google Scholar]

- GRI (Global Reporting Initiative). Available online: www.globalreporting.org (accessed on 10 November 2013).

- International Organisation for Standardisation (ISO). ISO 14040:2006: Environmental management—Life cycle assessment—Principles and framework. Available online: www.iso.org/iso/home/standards/management-standards/iso14000.htm (accessed on 10 November 2013).

- Ness, B.; Urbel-Piirsalu, E.; Anderberg, S.; Olsson, L. Categorising tools for sustainability assessment. Ecol. Econ. 2007, 60, 498–508. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. An overview of sustainability assessment methodologies (Review). Ecol. Indic. 2009, 9, 189–212. [Google Scholar] [CrossRef]

- European Council; European Parliament. Regulation (EU) No 995/2010 of the European Parliament and of the Council. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2010:295:0023:0034:EN:PDF (accessed on 12 November 2013).

- UNEP/IUC. The Kyoto Protocol to the Convention on Climate Change; NFCCC Climate Change Secreteriat: Chatelaine, Switzerland, 1998; p. 34. [Google Scholar]

- Bjorheden, R. Drivers behind the development of forest energy in Sweden. Biomass Bioenerg. 2006, 30, 289–295. [Google Scholar] [CrossRef]

- Borja, A.; Bricker, S.B.; Dauer, D.M.; Demetriades, N.T.; Ferreira, J.G.; Forbes, A.T.; Hutchings, P.; Jia, X.; Kenchington, R.; Marques, J.C.; et al. Overview of integrative tools and methods in assessing ecological integrity in estuarine and coastal systems worldwide. Mar. Pollut. Bull. 2008, 56, 1519–1537. [Google Scholar] [CrossRef]

- Stoate, C.; Báldi, A.; Beja, P.; Boatman, N.D.; Herzon, I.; van Doorn, A.; de Snoo, G.R.; Rakosy, L.; Ramwell, C. Ecological impacts of early 21st century agricultural change in Europe—A review. J. Environ. Manag. 2009, 91, 22–46. [Google Scholar]

- Rayner, J.; Buck, A.; Katila, P. (Eds.) Embracing complexity: Meeting the challenges of international forest governance. IUFRO World Ser. 2010, 28, 1–172.

- Humphreys, D. The global politics of forest conservation since the UNCED. Environ. Polit. 1996, 5, 231–256. [Google Scholar] [CrossRef]

- United Nations Forum on Forests (UNFF). Developing a Non-Legally Binding Instrument on All Types of Forests; Note by the Secretariat, E/CN.18/AC.1/2006/2. UNFF: New York, NY, USA, 2006. Available online: http://www.un.org/esa/forests/pdf/aheg/nlbi/Secretariat_note_NLBI_E.pdf (accessed on 13 November 2013).

- Pülzl, H.; Rametsteiner, E. Grounding international modes of governance into national forest programmes. For. Policy Econ. 2002, 4, 259–268. [Google Scholar] [CrossRef]

- Humphreys, D. The evolving forest regime. Glob. Environ. Chang. 1999, 9, 251–254. [Google Scholar]

- Thornber, K.; Louver, D.; Bass, S. Certification: Barriers to Benefits: A Discussion of Equity Implications; Discussion Paper; European Forest Institute: Joensuu, Finland, 1999. [Google Scholar]

- Humphreys, D. (Ed.) Forest Politics: The Evolution of International Cooperation; Earthscan Publications Ltd.: Oxford, UK, 1996.

- Rametsteiner, E.; Simula, M. Forest certification—an instrument to promote sustainable forest management? J. Environ. Manag. 2003, 67, 87–98. [Google Scholar] [CrossRef]

- Upton, C.B.S. (Ed.) The Forest Certification Handbook; Earthscan Publications Ltd.: Oxford, UK, 1995; p. 219.

- Northern ToSIA project. Available online: www.northerntosia.org (accessed on 13 November 2013).

- Freidberg, S. Calculating sustainability in supply chain capitalism. Econ. Soc. 2013, 42, 571–596. [Google Scholar]

- Busch, L. Standards: Recipes for Reality; MIT Press: Cambridge, MA, USA, 2011. [Google Scholar]

- Krasner, S.-D. Structural causes and regime consequences: Regimes as intervening variables. Int. Organ. 1982, 36, 185–205. [Google Scholar]

- European Parliament and European Commission. Directive 2004/18/EC of the European Parliament and of the Council of 31 March 2004 on the Coordination of Procedures for the Award of Public Works Contracts, Public Supply Contracts and Public Service Contracts. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2004:134:0114:0240:EN:PDF(accessed (accessed on 10 November 2013).

- Razman, M.R.; Yusoff, S.S.A.; Suhor, S.; Ismail, R.; Abdul Aziz, A.; Khalid, K.A.T. Environmental sustainability in the Basel Convention 1989 by adopting the principle of transboundary liability towards protection to the consumer. Soc. Sci. (Pak.) 2012, 7, 446–451. [Google Scholar]

- Cargill, C.F. Information Technology Standardization: Theory, Process, and Organizations; Digital Press: Clifton, NJ, USA, 1989; p. 17. [Google Scholar]

- Bonino, M.J.; Spring, M.B. Standards as change agents in the information technology market. Comput. Standard. Interfac. 1999, 20, 279–289. [Google Scholar]

- Pajunen, K.; Maunula, M. Internationalisation: A co-evolutionary perspective. Scand. J. Manag. 2008, 24, 247–258. [Google Scholar]

- Bernstein, S.; Cashore, B. Can non-state global governance be legitimate? An analytical framework. Regul. Gov. 2007, 1, 347–371. [Google Scholar]

- Berg, S. Drivkrafterna Miljöproblem blir en Global Fråga (The driving forces behind environmental problems are a global issue). Skog och Forskning 1998, 2, 6–11. [Google Scholar]

- Berg, S. Vad händer Internationellt (What happens internationally). Skog och Forskning 1998, 2, 36–40. [Google Scholar]

- Fletcher, R. A holistic approach to internationalisation. Int. Bus. Rev. 2001, 10, 25–49. [Google Scholar]

- Nationalencyklopedin. Standardisering (Standardisation); Bokförlaget Bra Böcker AB: Höganäs, Sweden, 1995; Volume 17, pp. 195–196. [Google Scholar]

- Swedish Standards Institute (SIS). Miljöledningssystem—Allmän vägledning för Principer, System och stödjande Metoder Environmental Management Systems—General Guidelines on Principles, Systems and Support Techniques, in (ISO 14004:2004); Swedish Standards Institute (SIS): Stockholm, Sweden, 2010. [Google Scholar]

- Swedish General Standards Institute (STG). Miljöledningssystem—Kravspecifikation Med vägledning för användning (ISO 14001:1996) (Environmental Management Systems—Specification with Guidance for Use (ISO 14001:1996); STG: Stockholm, Sweden, 1996. [Google Scholar]

- International Organisation for Standardisation (ISO). ISO 26000:2010 Guidance on Social Responsibility; Swedish Standards Institute (SIS): Stockholm, Sweden, 2010. [Google Scholar]

- Diermeier, D.; van Mieghem, J.A. Voting with your pocketbook: A stochastic model of consumer boycotts. Math. Comp. Model. 2008, 48, 1497–1509. [Google Scholar]

- Spiegel, D. Plünderer im Norden. Der Spiegel. 1993, 1993, 244–247. [Google Scholar]

- Mikkilä, M. Observing corporate social performance empirically through the acceptability concept: A global study. Corp. Soc. Responsib. Environ. Manag. 2005, 12, 183–196. [Google Scholar]

- Swedish Standard Institute (SIS). Standards promote the common good. Available online: www.sis.se/en/content/about-sis/SIS--Organization/Standards-promote-the-common-good/ (accessed on 10 November 2013).

- Cashore, B.; Auld, G.; Lawson, J.; Newsom, D. The future of non-state authority on Canadian staples industries: Assessing the emergence of forest certification. Policy Soc. 2007, 26, 71–91. [Google Scholar]

- Santaniello, F.; Koetz, B.; Cappelli, A. Environmental changes: Monitoring land cover changes in the Siberian region of Komi: Estimate of the vegetation trend using remote sensing. Proceedings of the First Sentinel 2 Preparatory Symposium, Rome, Italy, 23–27 April 2012; Available online: www.s2symposium.org (accessed on 10 November 2013).

- Support study for development of the non-legislative acts provided for in the Regulation of the European Parliament and of the Council laying down the obligations of operators who place timber and timber products on the market. Available online: http://ec.europa.eu/environment/forests/pdf/EUTR-Final_Report.pdf (accessed on 10 November 2013).

- European Commission. COM (2003) 251: Communication from the Commission to the Council and the European Parliament—Forest Law Enforcement, Governance and Trade (FLEGT)—Proposal for an EU action plan. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:52003DC0251:EN:HTML (accessed on 13 November 2013).

- DIRECTIVE 2009/28/EC of the European Parliament and of the Council of 23 Aril 20029 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=Oj:L:2009:140:0016:0062:en:PDF (accessed on 13 December 2013).

- Carroll, A.B. Corporate social responsibility: Evolution of a definitional construct. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Vergalli, S.; Poddi, L.; Comincioli, N. Does Corporate Social Responsibility Affect The Performance of Firms? Available online: http://www.feem.it/userfiles/attach/2012724152104NDL2012-053.pdf (accessed on 10 November 2013).

- World Business Council for Sustainable Development (WBCSD). Available online: www.wbcsd.org (accessed on 13 November 2013).

- UN Global Compact. Available online: www.unglobalcompact.org/ (accessed on 10 November 2013).

- Chen, S.B.P. Is corporate responsibility converging? A comparison of corporate responsibility reporting in the USA, UK, Australia, and Germany. J. Bus. Ethics 2009, 87, 299–317. [Google Scholar] [CrossRef]

- Raditya, D.A. Case Studies of Corporate Social Responsibility (CSR) in Forest Products Companies—and Customer’s Perspectives. Ph.D. Thesis, Sveriges Landbruksuniversitet (SLU), Umeå, Sweden, 2009. [Google Scholar]

- IKEA Group. IKEA Way on Purchasing Home Furnishing Products; Code of Conduct. IKEA Supply AG: Delft, The Netherlands, 2002. Available online: http://www.ikea.com/ms/nl_BE/about_ikea/pdf/IWAY_purchasing_home_furnishing_products.pdf (accessed on 13 December 2013).

- General Assembly of the United Nations (UN). Universal Declaration of Human Rights. Available online: www.un.org/en/documents/udhr/history.shtml (accessed on 10 November 2013).

- International Labour Association (ILO). Declaration on Fundamental Principles and Rights at Work. Available online: www.ilo.org/declaration/thedeclaration/lang--en/index.htm (accessed on 10 November 2013).

- General Assembly of the UN. Report on the United Nations Conference on Environment and Development. Available online: http://sustainabledevelopment.un.org/index.php?menu=1130 (accessed on 10 December 2013).

- Bartley, T. Institutional emergence in an era of globalization: The rise of transnational private regulation of labor and environmental conditions. Am. J. Sociol. 2007, 113, 297–351. [Google Scholar] [CrossRef]

- Tekle, Y.; Tuomasjukka, D.; Van Brusselen, J.; Tuomasjukka, T. A Sourcebook for the Development of VPA Impact Monitoring; EFI and EU FLEGT: Barcelona, Spain, 2013; forthcoming. [Google Scholar]

- Lindner, M.; Werhahn-Mees, W.; Suominen, T.; Vötter, D.; Pekkanen, M.; Zudin, S.; Roubalova, M.; Kneblik, P.; Brüchert, F.; Valinger, E.; et al. Conducting sustainability impact assessments of forestry-wood chains—examples of ToSIA applications. Eur. J. For. Res. 2012, 2012, 21–34. [Google Scholar]

- Palosuo, T.; Suominen, T.; Werhahn-Mees, W.; Garcia-Gonzales, J.; Lindner, M. Assigning results of the Tool for Sustainability Impact Assessment (ToSIA) to products of a forest-wood-chain. Ecol. Model. 2010, 221, 2215–2225. [Google Scholar] [CrossRef]

- Päivinen, R.; Lindner, M.; Rosén, K.; Lexer, M.J. A concept for assessing sustainability impacts of forestry-wood chains. Eur. J. For. Res. 2012. [Google Scholar] [CrossRef]

- Berg, S.; Fischbach, J.; Brüchert, F.; Poissonnet, M.; Pizzirani, S.; Varet, A.; Sauter, U. Towards assessing the sustainability of European logging operations. Eur. J. For. Res. 2012, 131, 81–94. [Google Scholar] [CrossRef]

- EFORWOOD Deliverable PD0.0.16: Manual for Data Collection for Regional and European Cases—UPDATE 3 September 2008; Berg, S. (Ed.) Skogforsk: Uppsala, Sweden, 2008; p. 110.

- Wolfslehner, B.; Brüchert, F.; Fischbach, J.; Rammer, W.; Becker, G.; Lindner, M.; Lexer, M. Exploratory multi-criteria analysis in sustainability impact assessment of forest-wood chains: the example of a regional case study in Baden-Württemberg. Eur. J. For. Res. 2012, 2012, 47–56. [Google Scholar]

- Prokofieva, I.; Lucas, B.; Thorsen, B.J.; Carlsen, K. Monetary Values of Environmental and Social Externalities for the Purpose of Cost-Benefit Analysis in the EFORWOOD Project; EFI Technical Report; European Forest Institute: Joensuu, Finland, 2011. [Google Scholar]

- Tuomasjukka, D.; Lindner, M.; Edwards, D. A concept for testing decision support tools in participatory processes applied to the ToSIA tool. Challenges 2013, 4, 34–55. [Google Scholar] [CrossRef]

- Weidema, B.P. The intergration of economic and social aspects in life cycle impact assessment. Int. J. Life Cycle Assess. 2006, 11, 89–96. [Google Scholar] [CrossRef]

- Berg, S.; Valinger, E.; Lind, T. Forestry and Reindeer Husbandry in Northern Sweden—The Malå Case Study in The Northern ToSIA Research Project. In Presented at Dubrovnik Conference on Sustainable Development of Energy, Water and Environment Systems, Dubrovnik, Croatia, 25–30 September 2011.

- Cafaupe Poca, M.; Valbuena, R.; Tuomasjukka, D.; Packalén, P. Evaluating the Potential of Airborne Laser Scanning (ALS) for Sustainability Impact Assessment with ToSIA Tool. Proceedings of GeoMundus, conference on Geosciences, Geoinformation and the Environment, Lisbon, Portugal, 9–11 November 2012; Available online: http://geomundus.org/2012/index.php/program/publications.html (accessed on 10 November 2013).

- Korvenranta, M. Metsähakkeen Hyödyntämisen Työllistävä Vaikutus KITEELLÄ ToSIA-Työkalulla ja Paikkatietomenetelmillä Arvioituna. Bachelor Thesis, Itä-Suomen yliopisto (UEF), Joensuu, Finland, 2011. [Google Scholar]

- Vötter, D.; Berg, S.; Lindner, M.; Kolström, M. Sustainability in Northern forests-related livelihood (Northern ToSIA). Proceedings of “The Spirit of Place”, Nordland, Norway, 1–3 August 2009; Available online: http://norwegianjournaloffriluftsliv.com/doc/Diana_Votter_-_Sustainability_in_Northern_forests-related_livelihood.pdf (accessed on 10 November 2013).

- Edwards, D.; Jensen, F.S.; Marzano, M.; Mason, B.; Pizzirani, S.; Schelhaas, M.J. A theoretical framework to assess the impacts of forest management on the recreational value of European forests. Ecol. Indic. 2011, 11, 81–89. [Google Scholar] [CrossRef]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Tuomasjukka, D.; Berg, S.; Lindner, M. Managing Sustainability of Fennoscandian Forests and Their Use by Law and/or Agreement: For Whom and Which Purpose? Sustainability 2014, 6, 18-49. https://doi.org/10.3390/su6010018

Tuomasjukka D, Berg S, Lindner M. Managing Sustainability of Fennoscandian Forests and Their Use by Law and/or Agreement: For Whom and Which Purpose? Sustainability. 2014; 6(1):18-49. https://doi.org/10.3390/su6010018

Chicago/Turabian StyleTuomasjukka, Diana, Staffan Berg, and Marcus Lindner. 2014. "Managing Sustainability of Fennoscandian Forests and Their Use by Law and/or Agreement: For Whom and Which Purpose?" Sustainability 6, no. 1: 18-49. https://doi.org/10.3390/su6010018

APA StyleTuomasjukka, D., Berg, S., & Lindner, M. (2014). Managing Sustainability of Fennoscandian Forests and Their Use by Law and/or Agreement: For Whom and Which Purpose? Sustainability, 6(1), 18-49. https://doi.org/10.3390/su6010018