Policy Instruments towards a Sustainable Waste Management

Abstract

:1. Introduction

- Waste generated per capita is in absolute decline.

- Energy recovery is limited to non-recyclable materials.

- Landfilling is virtually eliminated.

- High quality material recycling is ensured.

2. Methods

2.1. Introduction

- 0:

- Reference scenario, assuming developments in accordance with official forecasts made in 2008

- 1:

- Global sustainability, assuming globalization and strong political control over the environment and natural resources.

- 2:

- Global markets, assuming globalization and weak political control over the environment and natural resources.

- 3:

- Regional markets, assuming regionalization and weak political control over the environment and natural resources.

- 4:

- European sustainability, assuming regionalization and strong political control over the environment and natural resources.

{kind=link}

{kind=link}

| Policy instrument | Economic assessment | Environmental assessment | Assessment of social acceptance |

|---|---|---|---|

| Climate tax on waste incineration | X | X | |

| Including waste in the green certificate system for electricity production | X | X | |

| Compulsory recycling of recyclable materials | (X) | (X) | |

| Tradable Recycling Credits | X | ||

| Weight-based tax on incineration of waste | (X) | (X) | |

| Weight-based waste collection fee | X | X | X |

| Developed recycling systems | X | ||

| Tax on virgin raw materials | X | X | |

| Advertisements on request only | X | X | |

| Differentiated VAT | X | X | |

| Environmentally differentiated waste fee | X | ||

| Information to household and enterprises | X | ||

| Mandatory labeling of goods containing hazardous substances | X |

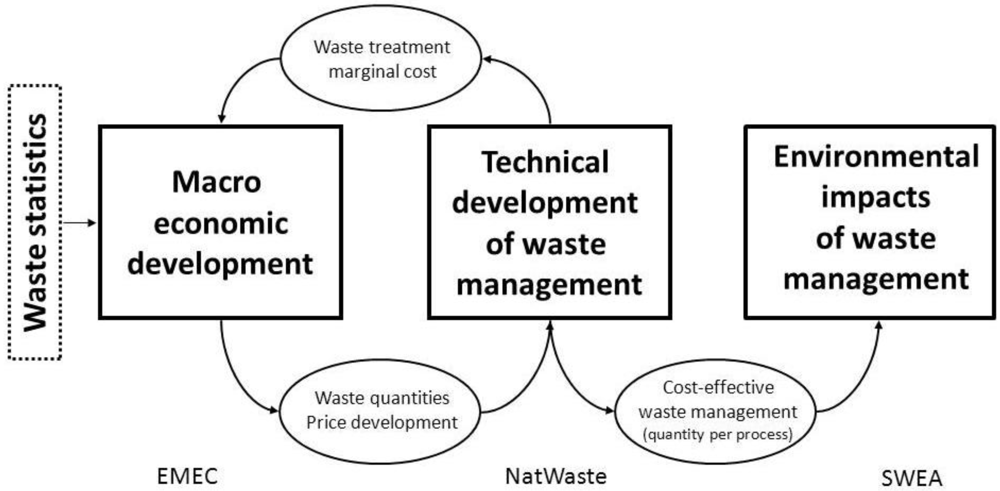

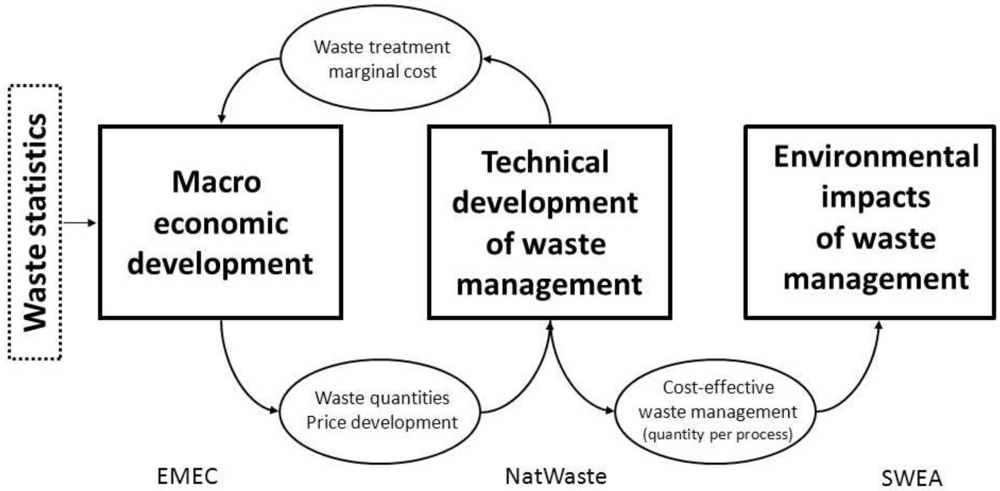

2.2. Integrated Approach for Quantitative Analysis

- The Environmental Medium term Economic model (EMEC) is a computable general equilibrium (CGE) model of the Swedish economy [26]. The EMEC model has been extended in order to analyze the relation between economic activity and waste generation. Data on waste quantities has been compiled and assigned to different economic activities and different sectors [23]. In the model, the waste generation of households and firms depend on their respective economic activities and is sensitive to changes in the price of goods and services. The waste-management costs are assumed to affect the total cost of utilizing goods and services. Hence, households and firms incorporate waste-management performance into their decisions [24]. The waste generation is directly or indirectly influenced by changes in government policies, e.g., tax policies [27].

- NatWaste is a systems engineering model of the Swedish waste management system [28,29]. Based on cost optimization, NatWaste calculates the cost-effective mix of technologies for managing Swedish waste. The cost-effective mix is the set of technologies that gives the lowest total economic costs (excluding external environmental costs and private consumers’ time) on the basis of the conditions defined for the analysis. Among the most influencing conditions are the choice of treatment technologies defined for each waste type (including their unit costs and performance) as well as the scenarios.

- Swedish Waste management Environmental Assessment (SWEA) is a life cycle assessment (LCA) model of the Swedish waste-management system [30]. LCA is a tool for assessing the potential environmental impacts of a product or a service (e.g., [31]), in this case waste management. Since a life-cycle perspective is used, credit is given to useful products, materials and energy carriers produced in the waste-management system that can replace products produced from virgin raw materials, in line with established LCA methodology for waste management (e.g., [32,33]). In addition, SWEA includes the reductions in material production of material that follows from waste-prevention efforts. This allows the model to account for the environmental benefits of waste prevention. SWEA has been implemented in the Simapro software [34] and for Life Cycle Impact Assessment the Recipe methodology [35] was used together with Cumulative energy demand [36] and Cumulative exergy demand [37].

2.3. Qualitative Assessment

- (i)

- if the instrument matched the individual’s / household’s environmental commitment;

- (ii)

- the perceived social fairness of the instrument;

- (iii)

- if the policy instrument would affect the individuals or households directly or indirectly (i.e., through other stakeholders, such as landlords);

- (iv)

- how the policy instruments would interact, or be in conflict, with fundamental cultural categories and practices [43];

- (v)

- if the instrument would conform or not with the users' general understanding [47] of the waste system’s task and function (e.g., to be a community service that minimizes environmental impact), and

- (vi)

- the (un)certainty of the message conveyed through the policy instrument (uncertainty regarding environmental impact; the benefit of oneself doing something and uncertainty about what others are doing, i.e., social uncertainty).

3. Evaluation of Policy Instruments

3.1. Climate Tax on Waste Incineration

3.1.1. Description and Assumptions

3.1.2. Results of the Evaluation

3.2. Including Waste in Green Certificates for Electricity Production

3.2.1. Description and Assumptions

3.2.2. Results of the Evaluation

3.3. Compulsory Recycling of Recyclable Materials

3.3.1. Description and Assumptions

3.3.2. Results of the Evaluation

- -

- Paper: 1386 ktonne (+90%)

- -

- Metals: 263 ktonne (+14%)

- -

- Plastics: 980 ktonne (+398%)

- -

- Glass: 91 ktonne (+26%)

- -

- Rubber: 63 ktonne (+394%)

- -

- Gypsum: 615 ktonne (+81%)

- -

- Textiles: 205 ktonne (+801%)

3.4. Tradable-Recycling-Credits

3.4.1. Description and Assumptions

3.4.2. Results of the Evaluation

3.5. Weight-based Tax on Incineration of Waste

3.5.1. Description and Assumptions

3.5.2. Results of the Evaluation

3.6. Weight-based Waste Collection Fee

3.6.1. Description and Assumptions

- an economic incentive to reduce the quantity of residual waste though prevention, recycling, or irregular or illegal waste treatment, and

- raised attention to waste-management issues that, at least temporarily, can result in waste prevention and increased recycling.

- All reduction in residual waste is due to prevention of waste with the same composition as the average residual waste.

- All reduction in residual waste is due to an increase in source separation for home composting (50%) and materials recycling (50%).

- All reduction in residual waste is due to illegal treatment: e.g. burning of combustible waste in private stoves or dumping of food and garden waste in the forest.

3.6.2. Results of the Evaluation

3.7. Developed Recycling Systems

3.7.1. Description and Assumptions

3.7.2. Results of the Evaluation

3.8. Tax on Virgin Raw Materials

3.8.1. Description and Assumptions

- A 10 SEK/ton tax on non-renewable materials (excluding fossil raw materials and plastics) extracted or imported and then used in Sweden.

- A tax on all fossil raw materials similar to the one currently applied on household heating oil (3804 SEK /m3) and an associated 5000 SEK/ton tax on imported plastics.

3.8.2. Results of the Evaluation

3.9. Advertisements on Request Only

3.9.1. Description and Assumptions

3.9.2. Results of the Evaluation

3.10. Differentiated VAT

3.10.1. Description and Assumptions

3.10.2. Results of the Evaluation

3.11. Environmentally Differentiated Waste Fees

3.11.1. Description and Assumptions

3.11.2. Results of the Evaluation

3.12. Improved Information

3.12.1. Description and Assumptions

- Procedural information, telling for example how, where, and when people should hand over source separated or non-separated waste.

- Declarative or norm-activating information, aiming at giving people motivation why they should source separate and the effects of source separation.

3.12.2. Results of the Evaluation

- Information should be combined with other instruments, for example to make way for other policy instruments.

- Information should be adjusted for each recipient group.

- Information can be given in the form of feedback.

- Information should be conveyed by a credible source.

- Information should rely on ethical norms of what people should do.

- In Sweden, the environmental awareness is generally high. Declarative information is then less important, but it is necessary for groups with low environmental awareness.

3.13. Mandatory Labeling of Goods Containing Hazardous Substances

3.13.1. Description and Assumptions

3.13.2. Results of the Evaluation

- The consumers themselves decide if they want to contribute to a better environment when shopping.

- If there are alternatives, the consumers will have the possibility to avoid products containing hazardous substances.

- Consumers without an active interest in environmental issues can still be prone to avoid exposing themselves and their family to hazardous substances. This is likely to make negative environmental labeling (of hazardous substances) more effective than positive environmental labeling (eco-labeling).

- The system must be mandatory. A voluntary system can lead to confusion if a lot of products and trademarks are not included.

- It is easier for a manufacturer to accept an eco-labeling system.

- There are examples when the labeling can lead to confusion, e.g., if a product has both positive and negative environmental properties.

4. Discussion

4.1. Development of Policy Instruments towards Implementation

4.1.1. Compulsory Recycling of Recyclable Materials

4.1.2. Weight-Based Waste Fee in Combination with Information and Developed Collection Systems

4.1.3. Mandatory Labeling of Products Containing Hazardous Chemicals

4.1.4. Advertisements on Request only and Other Waste Minimization Measures

4.1.5. Differentiated VAT and Subsidies for Some Services

4.1.6. Information

4.2. New Ideas for Policy Instruments

4.2.1. A General (Raw) Materials Tax

4.2.2. Re-Use Certificates

4.2.3. Bringing down Transaction Costs

4.2.4. Requirement of Design for Recycling

4.2.5. Tax on Hazardous Substances

4.2.6. Deposit and Refund Systems

4.2.7. A broader Landfill Tax

4.2.8. Required Storing of Plastics that Cannot be Recycled

4.2.9. Increased Control and Monitoring by Authorities

4.2.10. Waste Minimization in Enterprises (Industrial Waste-plan Requirements)

4.3. Choosing and Combining Policy Instruments

- The material in question cannot be recycled. Technological development is supported to find recycling possibilities with environmental improvements. A tax on virgin raw materials is introduced to stimulate the development of technology and market for recycling.

- Recycling of the material is possible but markets are not established. Further technological development is supported as well as tools to establish markets: for example, information systems, certifications, procurement requirements, waste brokers, and requirements for design for recycling.

- A market has been established. A requirement to recycle is introduced together with other policy tools that support the supply of recyclable materials.

5. Conclusions

Acknowledgments

Conflict of Interest

References and Notes

- European Commission, Roadmap to a Resource Efficient Europe; COM (2011) 571 Final; European Commission: Brussels, Belgium, 2011.

- Rockström, J.; Steffen, W.; Noone, K.; Persson, Å.; Chapin, III, F.S.; Lambin, E.F.; Lenton, T.M.; Scheffer, M.; Folke, C.; Schellnhuber, H.J.; et al. A safe operating space for humanity. Nature 2009, 461, 472–475. [Google Scholar]

- Swedish EPA, Steg på vägen. Fördjupad utvärdering av miljömålen 2012(Step by Step. In Depth Evaluation of Environmental Objectives 2012); Report 6500; Swedish EPA: Stockholm, Sweden, 2012.

- Ambell, C.; Björklund, A.; Ljunggren Söderman, M. Potential för ökad materialåtervinning av hushållsavfall och industriavfall (Potential for Increased Material Recycling of Household Waste and Industrial Waste); TRITA-INFRA-FMS 2010:4; KTH Samhällsplanering: Stockholm, Sweden, 2010. [Google Scholar]

- Bernstad, A.; La Cour Jansen, J.; Aspegren, H. Life cycle assessment of a household solid waste source separation programme: A Swedish case study. Waste Manage. Res. 2011, 29, 1027–1042. [Google Scholar] [CrossRef]

- Björklund, A.; Finnveden, G. Life cycle assessment of a national policy proposal—The case of a proposed waste incineration tax. Waste Manage. 2007, 27, 1046–1058. [Google Scholar] [CrossRef]

- European Environment Agency (EEA), The Road from Landfilling to Recycling: Common Destination, Different Routes; European Environment Agency: Copenhagen, Denmark, 2007; ISBN 978-92-9167-930-0.

- Pires, A.; Martinho, G.; Chang, N-B. Solid waste management in European countries: A review of systems analysis techniques. J. Environ. Manage. 2011, 92, 1033–1050. [Google Scholar] [CrossRef]

- Gentil, E.; Clavreul, J.; Christensen, T.H. Global warming factor of municipal solid waste management in Europe. Waste Manage. Res. 2009, 27, 850–860. [Google Scholar] [CrossRef]

- EU, Directive 2008/98/EC of the European Parliament and of the Council of 19 November 2008 on Waste and Repealing Certain Directives; European Commission: Brussels, Belgium, 2008.

- Swedish Government, Svenska miljömål—preciseringar av miljökvalitetsmålen och en första uppsättning etappmål (SwedishEnvironmental Objectives—Clarifications of the Envrionmental objectIves and a First Set of Milestones); Ds 2012:23; Regeringskansliet: Stockholm, Sweden, 2012.

- Swedish Waste Management, Svensk avfallshantering 2010 (Swedish waste management 2010); Swedish Waste Management: Malmö, Sweden, 2011.

- Ljunggren Söderman, M. Assessment of Policy Instruments for Waste Prevention. In Presentation at the ISWA Beacon Conference on Waste Prevention and Recycling, Vienna, Austria, 2011; ISWA: Vienna, Austria, 2011. [Google Scholar]

- Swedish EPA, Avfall i Sverige 2010 (Waste in Sweden 2010); Report 6520; Swedish EPA: Stockholm, Sweden, 2012.

- Swedish EPA, Från avfallshantering till resurshushållning. Sveriges avfallsplan 2012–2017 (From Waste Management to Resource Management. Waste plan of Sweden 2012–2017); Swedish EPA: Stockholm, Sweden, 2012.

- Von Borgstede, C.; Andersson, K. Environmental information—Explanatory factors for information behavior. Sustainability 2010, 2, 2785–2798. [Google Scholar] [CrossRef]

- Henriksson, G.; Åkesson, L.; Ewert, S. Uncertainty regarding waste handling in everyday life. Sustainability 2010, 2, 2799–2813. [Google Scholar] [CrossRef]

- Swedish District Heating Association. 2012. Available online: http://www.svenskfjarrvarme.se/Statistik--Pris/Fjarrvarme/Energitillforsel/ (accessed on 14 November 2012).

- Towards Sustainable Waste Management. 2013. Available online: http://www.hallbaravfallshantering.se (accessed on 21 February 2013).

- Bisaillon, M.; Finnveden, G.; Noring, M.; Stenmarck, Å.; Sundberg, J.; Sundqvist, J.-O.; Tyskeng, S. Nya styrmedel inom avfallsområdet? (New Policy Measures for Waste Management?); Miljöstrategisk analys—fms, ISSN 1652-5442, TRITA-INFRA-FMS 2009:7; KTH Royal Institute of Technology: Stockholm, Sweden, 2009. [Google Scholar]

- Finnveden, G.; Bisaillon, M.; Noring, M.; Stenmarck, Å.; Sundberg, J.; Sundqvist, J.-O.; Tyskeng, S. Developing and evaluating new policy instruments for sustainable waste management. Int. J. Environ. Sust. Develop. 2012, 11, 19–31. [Google Scholar] [CrossRef]

- Dreborg, K.-H.; Tyskeng, S. Framtida förutsättningar för en hållbar avfallshantering—Övergripande omvärldsscenarier samt referensscenario(Future conditions for a sustainable waste management—General environment scenarios and reference scenario); Miljöstrategisk analys—fms, TRITA-INFRA-FMS 2008:6; KTH Royal Institute of Technology: Stockholm, Sweden, 2008. [Google Scholar]

- Sjöström, M.; Östblom, G. Future Waste Scenarios for Sweden Based on a CGE-model; Working Paper no. 109; National Institute of Economic Research: Stockholm, Sweden, 2009. [Google Scholar]

- Östblom, G.; Ljunggren Söderman, M.; Sjöström, M. Analysing Future Waste Generation—Soft Linking a Model for Waste Management with a CGE-model for Sweden; Working paper no. 118; National Institute of Economic Research: Stockholm, Sweden, 2010. [Google Scholar]

- Ljunggren Söderman, M.; Björklund, A.; Eriksson, O.; Forsfält, T.; Stenmarck, Å.; Sundqvist, J.-O. Policy Instruments for a More Sustainable Waste Management; Presentation at LCM 2011; Berlin, Germany, 2011. Available online: http://www.lcm2011.org (accessed on 21 February 2013).

- Östblom, G.; Berg, C. The EMEC model: Version 2.0; Working Paper no. 96; National Institute of Economic Research: Stockholm, Sweden, 2006. [Google Scholar]

- Forsfält, T. Samhällsekonomiska effekter av två styrmedel för minskade avfallsmängder (Socioeconomic impacts of two policy measures towards reduced waste amounts); Specialstudie nr 26; National Institute of Economic Research: Stockholm, Sweden, 2011. [Google Scholar]

- Ljunggren, M. Modelling national solid waste management. Waste Manage. Res. 2000, 18, 525–537. [Google Scholar]

- Ljunggren Söderman, M. Ekonomisk analys av nya styrmedel för hanteringen av svenskt avfall(Economic Analysis of New Policy Measures for Management of Swedish Waste); Report B 2021; IVL Swedish Environmental Research Institute: Stockholm, Sweden, 2011. [Google Scholar]

- Arushanyan, Y.; Björklund, A.; Eriksson, O.; Finnveden, G.; Ljunggren-Söderman, M.; Sundqvist, J.-O.; Stenmarck, Å. Environmental Assessment of Waste Policy Instruments in Sweden; 2013; in progress. [Google Scholar]

- ISO, ISO 14040 International Standard. In Environmental Management—Life Cycle Assessment —Principles and Framework; International Organisation for Standardization: Geneva, Switzerland, 2006.

- Clift, R.; Doig, A.; Finnveden, G. The Application of Life Cycle Assessment to Integrated Solid Waste management, Part I—Methodology; Process Safety and Environmental Protection 2000, 78, 279–287. [CrossRef]

- Finnveden, G.; Hauschild, M.; Ekvall, T.; Guinée, J.; Heijungs, R.; Hellweg, S.; Koehler, A.; Pennington, D.; Suh, S. Recent developments in Life Cycle Assessment. J. Environ. Manage. 2009, 91, 1–21. [Google Scholar] [CrossRef]

- Pré, Simapro 7 Professional Version 7.3.2. Pre Consultants: Amersfoort, The Netherlands, 2011.

- Goedkoop, M.; Heijungs, R.; Huijbregts, M.; De Scryver, A.; Sruijs, J.; van Zelm, R. ReCiPe 2008, Report 1: Characterization; Ministry of VROM: The Hague, The Netherlands, 2009. [Google Scholar]

- Frischknecht, R.; Jungbluth, N.; Althaus, H.; Doka, G.; Dones, R.; Hellweg, S.; Hischier, R. Implementation of Life Cycle Impact Assessment Methods; Swiss Center for Life Cycle Inventories: Duebendorf, Switzerland, 2007. [Google Scholar]

- Bösch, M.; Hellweg, S.; Huijbregts, M.; Frischknecht, R. Applying cumulative exergy demand (CExD) indicators to the ecoinvent database. Int. J. Life Cycle Ass. 2006, 12, 181–190. [Google Scholar]

- Ekvall, T. Key methodological issues for life cycle inventory analysis of paper recycling. J. Clean. Prod. 1999, 7, 281–294. [Google Scholar] [CrossRef]

- Wene, C.-O. Exploring and Mapping: A Comparison of the IEA-MARKAL and CEC-EFOM Technical Energy System Models and the ANL Electric Utility Model; Technical report BNL-52224; Brookhaven National Lab.: Upton, NY, USA, 1989. [Google Scholar]

- Sahlin, J.; Ekvall, T.; Bisaillon, M.; Sundberg, J. Introduction of a waste incineration tax: Effects on the Swedish waste flows. Resour. Conserv. Recy. 2007, 51, 827–846. [Google Scholar] [CrossRef]

- Blomberg, J.; Söderholm, P. The economics of secondary aluminium supply: An econometric analysis based on European data. Resour. Conserv. Recy. 2009, 53, 455–463. [Google Scholar] [CrossRef]

- Ekvall, T.; Sahlin, J.; Sundberg, J. Effects of Policy Instruments on Waste Intensities; Report B1939; IVL Swedish Environmental Research Institute: Stockholm, Sweden, 2010. [Google Scholar]

- Henriksson, G.; Åkesson, L.; Ewert, S. Uncertainty regarding waste handling in everyday life. Sustainability 2010, 2, 2799–2813. [Google Scholar] [CrossRef]

- Andersson, M.; von Borgstede, C.; Eriksson, O.; Guath, M.; Henriksson, G.; Sundqvist, J.-O.; Åkesson, L. Hållbar avfallshantering—utvärdering av styrmedel från psykologiskt och etnologiskt perspektiv (Sustainable Waste Management—Evaluation of Policy Measures from an Psychological and Ethnologivcal Perspective); TRITA-INFRA-FMS: 2011:5; KTH Royal Institute of Technology: Stockholm, Sweden, 2011. [Google Scholar]

- Andersson, M.; Eriksson, O.; von Borgstede, C. The effects of environmental management systems on source separation in the work and home settings. Sustainability 2012, 4, 1292–1308. [Google Scholar] [CrossRef]

- Geertz, C. The Interpretation of Cultures; Basic Books: New York, NY, USA, 1973. [Google Scholar]

- Gram-Hanssen, K. Practice Theory and the Green Energy Consumer. In Presentation at ESA Conference 3–6 September 2007 in Glasgow, Research Network on the Sociology of Consumption, 2007; ESA: Paris, France, 2007. [Google Scholar]

- Ekvall, T.; Sundqvist, J.-O.; Hemström, K.; Jensen, C. Stakeholder Analysis of Incineration Tax, Raw Material Tax, and Weight-based Waste Fee; Draft report; IVL Swedish Environmental Research Institute: Stockholm, Sweden, 2011. [Google Scholar]

- Söderholm, P.; Ekvall, T. Material Markets in the Presence of Secondary and Primary Production: Important Interactions and Policy Impacts, 2012; Draft version.

- Söderholm, P. Taxing Virgin Natural Resources: Lessons from Aggregates Taxation in Europe. Resour. Conserv. Recy. 2011, 55, 911–922. [Google Scholar] [CrossRef]

- Olofsson, M.; Sahlin, J.; Ekvall, T.; Sundberg, J. Driving forces for import of waste for energy recovery in Sweden. Waste Manage. Res. 2005, 23, 3–12. [Google Scholar] [CrossRef]

- Bergek, A.; Jacobsson, S. Are tradable green certificates a cost-efficient policy driving technical change or a rent-generating machine? Lessons from Sweden 2003–2008. Energ. Policy 2010, 38, 1255–1271. [Google Scholar] [CrossRef]

- Swedish Waste Management, National Survey of Analyses of Composition of Household’s Solid Waste; Report U 2011:4; Swedish Waste Management: Malmö, Sweden, 2011.

- Massachusetts Department of Environment Protection, Massachusetts 2010–2020. Solid Waste Master Plan. Pathway to Zero Waste; Massachusetts Department of Environment Protection: Boston, MA, USA, 2010.

- Gerlat, A. Mandatory Organics Recycling to Become Law in Vermont. 2012. Available online: http://waste360.com/state-and-local/mandatory-organics-recycling-become-law-vermont (accessed on 14 November 2012).

- Metro Vancouver. Banned and Prohibited Materials. 2012. Available online: http://www.metrovancouver.org/services/solidwaste/disposal/Pages/bannedmaterials.aspx (accessed on 14 November 2012).

- Ahlroth, S.; Finnveden, G. Ecovalue08—A new valuation set for environmental systems analysis tools. J. Clean. Prod. 2011, 19, 1994–2003. [Google Scholar] [CrossRef]

- Arushanyan, Y.; Finnveden, G. Ban on incineration, weighting gf.xlsx; Spread-sheet Data, 20120222, Stockholm, Sweden, 2012; Unpublished.

- Nilsson, H. Förpacknings- och tidningsinsamlingen AB, Stockholm, Sweden. Personal communication, 13 December 2011. [Google Scholar]

- Profu, Tillgång och efterfrågan på behandlingskapacitet för brännbart och övrigt organiskt avfall. Underlag till Sveriges nationella avfallsplan 2011—Del 1. (Supply and Demand for Treatment Capacity of Combustible and Other Organic Waste. Data for Sweden’s National Waste Plan 2011—Part 1), Profu: Mölndal, Sweden, 1 April 2011.

- Fischer, J. Massachusetts Department of Environment Protection, Boston, MA, USA. Personal Communication, 22 February 2012. [Google Scholar]

- O’Doherty, R.; Bailey, I.; Colins, A. Regulatory failure via market evolution: The case of UK packaging recycling. Environ. Plann. C Govern. Pol. 2003, 21, 579–595. [Google Scholar] [CrossRef]

- Matsueda, N.; Nagase, Y. An economic analysis of the packaging waste recovery note system in the UK. Resour. Energy Econ. 2012, 34, 660–679. [Google Scholar]

- Edjemo, T.; Söderholm, P. Steel Scrap Markets in Europe and the USA. Miner. Energ. 2008, 23, 57–73. [Google Scholar] [CrossRef]

- Weitzman, M. Prices vs. Quantities. Rev. Econ. Stud. 1974, 41, 447–491. [Google Scholar]

- Björklund, A.; Finnveden, G. Life cycle assessment of a national policy proposal—The case of a proposed waste incineration tax. Waste Manage. 2007, 27, 1046–1058. [Google Scholar] [CrossRef]

- SOU, Skatt i retur (Tax in return); SOU 2009:12, Fritzes: Stockholm, Sweden, 2009.

- Dahlén, L.; Lagerkvist, A. Pay as you throw: Strengths and weaknesses of weight-based billing in household waste collection systems. Waste Manage. 2010, 30, 23–31. [Google Scholar] [CrossRef]

- Hage, O.; Sandberg, K.; Söderholm, P.; Berglund, C. Household Plastic Waste Collection in Swedish Municipalities: A Spatial-Econometric Approach. In Proceedings of The 16th Annual Conference of the European Association of Environmental and Resource Economists (EAERE), Gothenburg, Sweden, 25–28 June 2008; EAERE: Venice, Italy, 2008. [Google Scholar]

- Hedman, B.; Näslund, M.; Nilsson, C.; Marklund, S. Emissions of polychlorinated Dibenzodioxins and Dibenzofurans and Polychlorinated Biphenyls from uncontrolled burning of garden and domestic waste (Backyard Burning). Environ. Sci. Technol. 2005, 39, 8790–8796. [Google Scholar] [CrossRef]

- Schmidt, L.; Sjöström, J.; Palm, D.; Ekvall, T. Viktbaserad avfallstaxa—Vart tar avfallet vägen? (Weight-Based Waste Tariff—Where does the Waste Go?); Report B 2054; IVL Swedish Environmental Research Institute: Stockholm, Sweden, 2012. [Google Scholar]

- Sterner, T.; Bartelings, H. Household waste management in a Swedish Municipality: Determinants of waste disposal, Recycling and composting. Environ. Resour. Econ. 1999, 13, 473–491. [Google Scholar] [CrossRef]

- Fullerton, D.; Kinnaman, T.C. Garbage, Recycling and Illicit Burning or Dumping. J. Environ. Econ. Manag. 1995, 29, 78–91. [Google Scholar] [CrossRef]

- Walls, M.; Palmer, K. Upstream pollution, Downstream waste disposal, And the design of comprehensive environmental policies. J. Environ. Econ. Manag. 2001, 41, 94–108. [Google Scholar] [CrossRef]

- Environmental Policy and Household Behavior: Sustainability and Everyday Life; Söderholm, P. (Ed.) Earthscan: London, UK, 2010.

- Thøgersen, J. Monetary incentives and environmental concern. Effects of a differentiated garbage fee. J. Consum. Policy 1994, 17, 407–443. [Google Scholar] [CrossRef]

- Kinnaman, T.C. Policy Watch: Examining the Justification for Residential Recycling. J. Econ. Perspec. 2006, 20, 219–232. [Google Scholar] [CrossRef]

- Swedish EPA, System för insamling av hushållsavfall i materialströmmar(System for collection of household waste in material streams); Report 5942; Swedish EPA: Stockholm, Sweden, 2009.

- Palmer, K.; Sigman, H.A.; Walls, M. The Cost of Reducing Municipal Solid Waste. J. Environ. Econ. Manag. 1997, 33, 128–150. [Google Scholar] [CrossRef]

- Ljunggren Söderman, M.; Björklund, A. Konsumtion, produktion och framtida avfall—effekter på miljö och ekonomi (Consumption, Production and Future Waste-Effects on the Environment and Economy). Presentation at the conference Avfall i nytt fokus, Borås, Sweden. 2010. Available online: http://www.hallbaravfallshantering.se/ (accessed on 21 February 2013).

- Brekke, K.A.; Kipperberg, G.; Nyborg, K. Social interaction in responsibility ascription: The case of household recycling. Land Econ. 2010, 86, 766–784. [Google Scholar]

- Bruvoll, A.; Nyborg, K. The cold shiver of not giving enough: On the social cost of recycling campaigns. Land Econ. 2004, 80, 539–549. [Google Scholar] [CrossRef]

- Cela, E.; Kaneko, S. Determining the effectiveness of the Danish packaging tax policy: The case of paper and paperboard and packaging imports. Resour. Conserv. Recy. 2011, 55, 836–841. [Google Scholar] [CrossRef]

- Rouw, M.; Worrell, E. Evaluating the impacts of packaging policy in The Netherlands. Resour. Conserv. Recy. 2011, 55, 483–492. [Google Scholar] [CrossRef]

- Monomaivibool, V.; Vassanadumrongdee, S. Extended Producer Responsibility in Thailand. Prospects for Policies on Waste Electrical and Electronic Equipment. J. Ind. Ecol. 2011, 15, 185–205. [Google Scholar] [CrossRef]

- Mayers, K.; Peagam, R.; France, C.; Basson, L.; Clift, R. Redesigning the Camel: The European WEEE directive. J. Ind. Ecol. 2011, 15, 4–8. [Google Scholar] [CrossRef]

- Lindhqvist, T. Policies for waste batteries: Learning from experience. J. Ind. Ecol. 2010, 14, 537–540. [Google Scholar] [CrossRef]

- Cleary, J. Life cycle assessments of wine and spirit packaging at the product and municipal scale: A Toronto, Canada case study. J. Clean. Prod. 2013, in press. [Google Scholar]

- Gentil, E.; Gallo, D.; Christensen, T.H. Environmental evaluation of municipal waste prevention. Waste Manage. 2011, 31, 2371–2379. [Google Scholar] [CrossRef]

- Ljunggren Söderman, M.; Davidsson, H.; Jensen, C.; Palm, D.; Stenmarck, Å. Goda exempel på förebyggande av avfall från kommuner (Good Examples of Waste Prevention in Municipalities); Report U 2011:5; Swedish Waste Management: Malmö, Sweden, 2011. [Google Scholar]

- Salhofer, S.; Obersteiner, G.; Schneider, F.; Lebersorger, S. Potential for the prevention of municipal solid waste. Waste Manage. 2008, 28, 245–259. [Google Scholar] [CrossRef]

- Nicolli, F.; Johnstone, N.; Söderholm, P. Resolving Failures in Recycling Markets: The Role of Technological Innovation. Environ. Econ. Policy Stud. 2012, 14, 261–288. [Google Scholar] [CrossRef]

- Watkins, G.; Husgafvel, R.; Pajunen, N.; Dahl, O.; Heiskanen, K. Overcoming institutional barriers in the development of novel process industry residue based symbiosis product—Case study at the EU level. Miner. Eng. 2013, 41, 31–40. [Google Scholar] [CrossRef]

- Fullerton, D.; Wu, W. Policies for Green Design. J. Environ. Econ. Manag. 1998, 25, 242–256. [Google Scholar]

- Calcott, P.; Walls, M. Waste, Recycling, and ‘Design for Environment’: Roles for Markets and Policy Instruments. Resour. Energ. Econ. 2005, 27, 283–305. [Google Scholar]

- Johansson, J.G.; Björklund, A.E. Reducing lifecycle environmental impact of waste electrical and electronic equipment recycling. J. Ind. Ecol. 2010, 14, 258–269. [Google Scholar] [CrossRef]

- Söderholm, P. Economic Instruments in Chemicals Policy: Past Experiences and Prospects for Future Use; TemaNord 2009:565; Nordic Council of Ministers: Copenhagen, Denmark, 2009. [Google Scholar]

- Tyskeng, S.; Finnveden, G. Comparing energy use and environmental impacts of recycling and incineration. J. Environ. Eng. 2010, 136, 744–748. [Google Scholar] [CrossRef]

- Nakatani, J.; Fujii, M.; Moriguchi, Y.; Hirao, M. Life-cycle assessment of domestic and transboundary recycling of post-consumer PET bottles. Int. J. Life Cycle Ass. 2010, 15, 590–597. [Google Scholar] [CrossRef]

- Profu, Evaluating Waste Incineration as Treatment and Energy Recovery Method from an Environmental Point of View; Report on behalf of CEWEP (Confederation of European Waste-to-Energy Plants), Final Version, 13 May 2004, Profu: Mölndal, Stockholm, 2004.

- Eriksson, O.; Finnveden, G. Plastic waste as a fuel—CO2-neutral or not? Energ. Environ. Sci. 2009, 2, 907–914. [Google Scholar] [CrossRef]

- Damon, M.; Sterner, T. Policy Instruments for sustainable development at Rio + 20. J. Environ. Develop. 2012, 21, 143–151. [Google Scholar] [CrossRef]

- Henriksson, G.; Börjesson Rivera, M.; Åkesson, L. Environmental policy instruments seen as negotiations. In Negotiating Environmental Conflicts: Local communities, global policies (published within the series Kulturanthropologie Notizen, vol. 81); Goethe Universität: Frankfurt am Main, Germany, 2012. [Google Scholar]

- Hajer, M.A. A Frame in the Fields: Policymaking and the Reinvention of Politics. In Deliberative Policy Analysis: Understanding Governance in the Network Society; Hajer, M.A., Wagenaar, H., Eds.; Cambridge University Press: Cambridge, UK, 2003; pp. 88–110. [Google Scholar]

- Henriksson, G. What did the Trial Mean for Stockholmers? In Congestion Taxes in City Traffic: Lessons Learnt from the Stockholm Trial; Gullberg, A., Isaksson, K., Eds.; Nordic Academic Press: Lund, Sweden, 2009; pp. 235–294. [Google Scholar]

- Shove, E.; Walker, G. Governing transistions in the sustainability of everyday life. Res. Policy 2010, 39, 471–476. [Google Scholar] [CrossRef]

- Gulliver, P.H. Anthropological contributions to the study of negotiations. Negotiation J. 1988, 4, 247–255. [Google Scholar] [CrossRef]

- Worster, D. Nature’s Economy. A History of Ecological Ideas, 2nd ed; Cambridge University Press: Cambridge, UK, 1996. [Google Scholar]

- Ostrom, E. Coping with tragedies of the commons. Annu. Rev. Polit. Sci. 1999, 2, 493–535. [Google Scholar] [CrossRef]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Finnveden, G.; Ekvall, T.; Arushanyan, Y.; Bisaillon, M.; Henriksson, G.; Gunnarsson Östling, U.; Söderman, M.L.; Sahlin, J.; Stenmarck, Å.; Sundberg, J.; et al. Policy Instruments towards a Sustainable Waste Management. Sustainability 2013, 5, 841-881. https://doi.org/10.3390/su5030841

Finnveden G, Ekvall T, Arushanyan Y, Bisaillon M, Henriksson G, Gunnarsson Östling U, Söderman ML, Sahlin J, Stenmarck Å, Sundberg J, et al. Policy Instruments towards a Sustainable Waste Management. Sustainability. 2013; 5(3):841-881. https://doi.org/10.3390/su5030841

Chicago/Turabian StyleFinnveden, Göran, Tomas Ekvall, Yevgeniya Arushanyan, Mattias Bisaillon, Greger Henriksson, Ulrika Gunnarsson Östling, Maria Ljunggren Söderman, Jenny Sahlin, Åsa Stenmarck, Johan Sundberg, and et al. 2013. "Policy Instruments towards a Sustainable Waste Management" Sustainability 5, no. 3: 841-881. https://doi.org/10.3390/su5030841

APA StyleFinnveden, G., Ekvall, T., Arushanyan, Y., Bisaillon, M., Henriksson, G., Gunnarsson Östling, U., Söderman, M. L., Sahlin, J., Stenmarck, Å., Sundberg, J., Sundqvist, J.-O., Svenfelt, Å., Söderholm, P., Björklund, A., Eriksson, O., Forsfält, T., & Guath, M. (2013). Policy Instruments towards a Sustainable Waste Management. Sustainability, 5(3), 841-881. https://doi.org/10.3390/su5030841