“Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future

Abstract

:1. Introduction

2. Corporate Financial Performance

3. Corporate Social Performance (CSP)

3.1. The Concept of CSP

{kind=link}

| Authors | Definition of CSP | CSP Dimensions |

|---|---|---|

| Carroll [39] | The articulation and interaction between (a) different categories of social responsibilities; (b) specific issues relating to such responsibilities; and (c) the philosophies of the answers | Definition of Corporate Social Responsibility Levels: economic, legal, ethical, discretionary Philosophy of Responsiveness Stances: responsive, defensive, accommodative, proactive Social Issues involved e.g., Consumerism; Environment; Discrimination; Product safety; Safety at work; Shareholding |

| Wartick and Cochran [42] | “The underlying interaction among the principles of social responsibility, the process of social responsiveness and the policies developed to address social issues” (p. 758) | Corporate Social Responsibilities Levels: economic, legal, ethical, discretionary Corporate Social Responsiveness Stances: responsive, defensive, accommodative, proactive Social Issues Management Approach: Identification; Analysis; Response |

| Wood [41] | “A Business organization’s configuration of principles of social responsibility, processes of social responsiveness, and policies, programs, and observable outcomes as they relate to the firm’s societal relationship”(p. 693) | Principles of Corporate Social Responsibility Levels: Institutional, Organizational and Individual Processes of Corporate Social Responsiveness Includes: Environmental Assessment and Analysis; Stakeholder Managements; Issues Management Outcomes of Corporate Behavior Combines: Societal Impacts; Corporate Social Programs and Policies |

| Clarkson [43] | The ability to manage and satisfy the different corporate stakeholders | This model identifies specific problems for each of the main stakeholder categories it distinguishes: Employees; Owners/Shareholders; Consumers; Suppliers; State; Stakeholders; Competitors |

3.2. Measurement Approaches to CSP

| Type of Measurement | Suitability in terms of the SP-concept | Characteristics/Problems | Mode of production |

|---|---|---|---|

| Contents of annual reports | A measurement that is more symbolic than substantive (discourse) and which contains no reference to the construct’s varying dimensions | Subjective measurement that can be easily manipulated | By the company |

| Pollution indicators | Measures just one of the construct’s dimensions (its environmental aspects) | An objective measurement but does not apply to all firms | By an entity that is external to the company |

| Questionnaire based surveys | Depends on what measurements have been suggested. Can be a very good fit with the concept but actors’ perceptions remain a priority in such measurements | Perceptual measurement that can be manipulated depending on how it is administered | By a researcher who uses questionnaires to gather info directly from the company |

| Corporate Reputation indicators | Overlapped with Corporate Reputation enables a measurement of overall CSP but is still relatively ambiguous | Perceptual measurement Halo effects | By an entity that is external to the company |

| Data produced by “measurement entities” | Multidimensional measurement, with the extent of a theoretical model’s “fit” depending on the operational modes and benchmarks that agencies are using | Depends on the agencies’ operational mode. Halo effects | By an entity that is external to the company |

| Measure | Dimensions | Judge | Source |

|---|---|---|---|

| Fortune | Eight attributes of reputation | Financial analyst, senior executives and outside managers | Griffin and Mahon [79] |

| KLD | Five attributes of CSR focusing on key stakeholder relation, including topics with which companies have recently experienced external pressures | External audiences | Waddock and Grave [22] |

| TRI | Qualitative measure of companies’ environmental discharge to water, air and landfill, and disposal of hazardous waste | No external judge needed, companies themselves give the data | Griffin and Mahon [79] |

| Corporate Philanthropy | Quantitative measure of companies philanthropy, how much | No external judge needed, companies themselves give the data | Griffin and Mahon [79] |

| Best Corporate Citizen | Three-year average shareholder return and six social measures: company’s influence on customer, employee, community, environment, minorities, and non US stakeholders | Social investment research firm | Murphy [80] |

| Dimension | Strength | Concern |

|---|---|---|

| Community Issues | -Generous Giving -Innovating Giving -Community consultation/Engagement -Strong aboriginal Relationship | -Lack of Consultation/Engagement -Breach of Covenant -Weak aboriginal relation |

| Diversity Workplace | -Strong Employment Equity Program -Women on board of directors -Women in senior management -Work/family benefit -Minority/women contracting | -Lack of employment equity initiative -Employment equity Controversies |

| Employee relations | -Positive union relation -Exceptional benefit -Workforce management policies -Cash profit sharing -Employee ownership/Involvement | -Poor union relation -Safety problem -Workforce reduction -Inadequate benefits |

| Environmental Performance | -Environmental management strength -Exceptional environment planning and impact assessment -Environmentally sound resource use -Environmental impact reduction -Beneficial product and service | -Environment management concern -Inadequate environmentalplanning or impact assessment -Unsound resource use -Poor compliance record -Substantial emissions/discharges -Negative impact of operation -Negative impact of products |

| International | -Community relations -Employee relations -Environment -Sourcing practice | -Poor community relations -Poor employee relations -Poor environmental management/performance -Human rights -Burma -Sourcing practice |

| Product and Business Practice | -Beneficial products and services -Ethical Business Practice | -Product safety -Pornography -Marketing practices -Illegal business practices |

| Other | -Limited compensation -Confidential proxy voting -Ownership in companies | -Excessive compensation -Dual-class share structure -Ownership in other Companies |

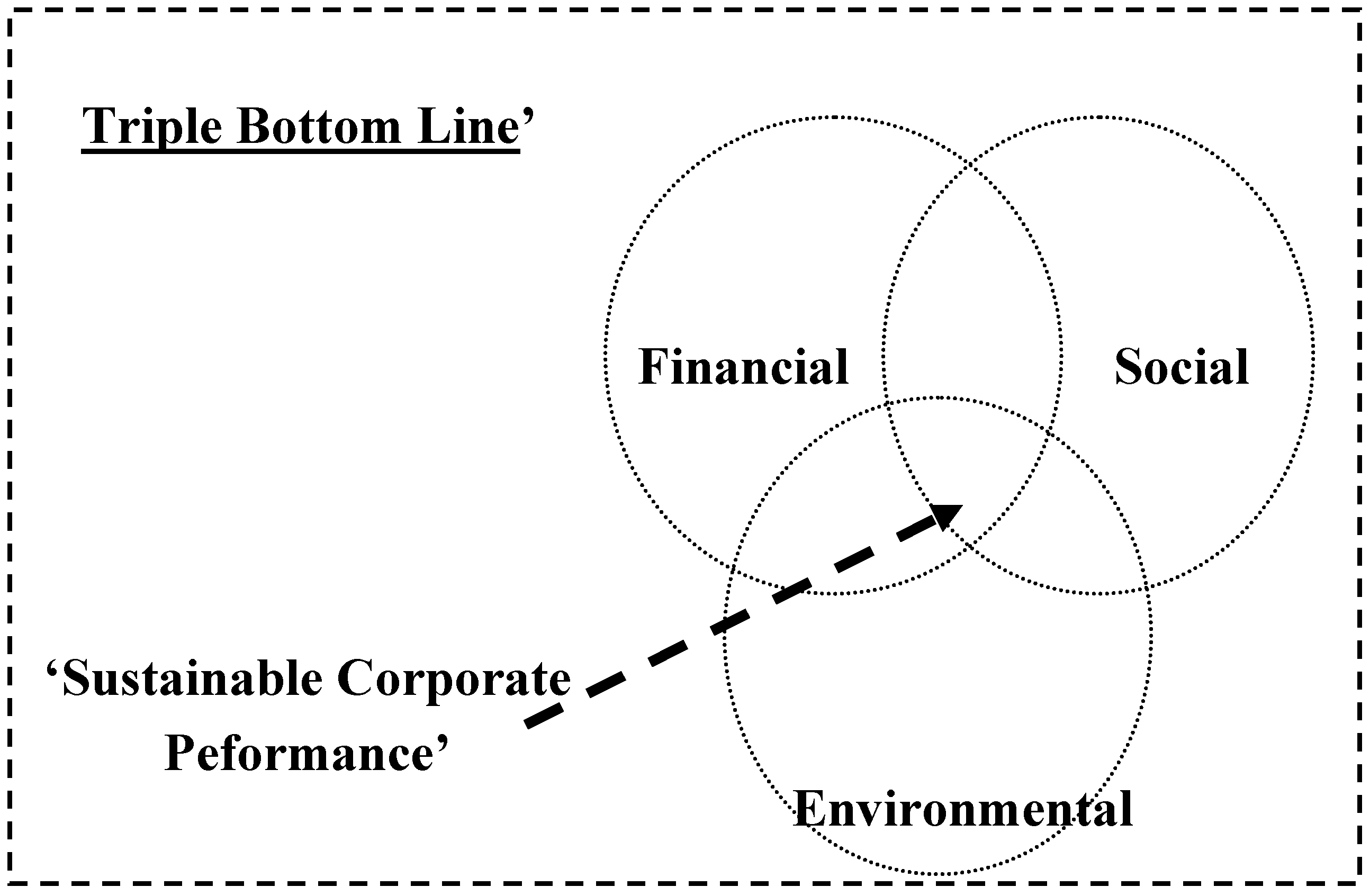

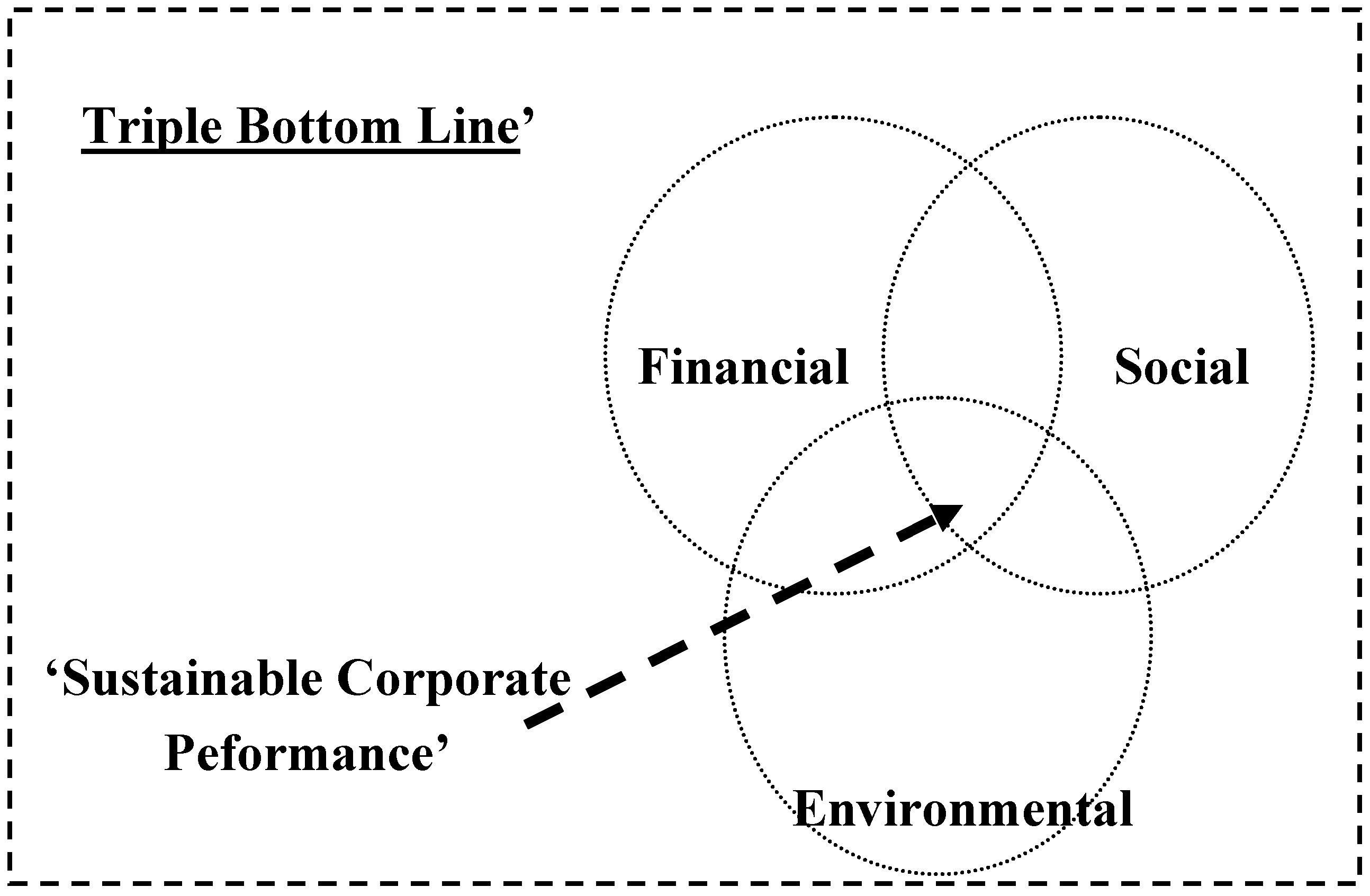

4. Triple Bottom Line as Sustainable Corporate Performance

5. A Proposition for the Future

Acknowledgments

References

- Daft, R.L. Management; Dryden Press: Chicago, IL, USA, 1991. [Google Scholar]

- Lenz, R.T. Environmental strategy, organization structure and performance: Pattern in one industry. Strateg. Manage. J. 1980, 1, 209–226. [Google Scholar] [CrossRef]

- Venktrakaman, N.; Ramanugan, V. Measurement of business performance in strategy research: A comparative of approach. Acad. Manage. Rev. 1986, 11, 801–814. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. The balanced scorecard: Measures that drive performance. Harvard Bus. Rev. 1992, January–February, 71–80. [Google Scholar]

- Simons, R. Levers of Control: How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business School Press: Boston, MA, USA, 1995. [Google Scholar]

- Simons, R. Performance Measurement and Control System for Implementing Strategy: Text and Cases; Prentice Hall: Old Tappan, NJ, USA, 2000. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concept, evidence, and implications. Acad. Manage. Rev. 1995, 20, 65–91. [Google Scholar]

- Simons, R. Accounting control systems and business strategy: An empirical analysis. Account. Organ. Soc. 1987, 12, 357–374. [Google Scholar] [CrossRef]

- Govindarajan, V.; Fisher, J. Strategy, control system and resource sharing: Effect on business-unit performance. Acad. Manage. J. 1990, 33, 259–285. [Google Scholar] [CrossRef]

- Govindarajan, V. A contingency approach to a strategy implementation at the business-unit level: Integrating an administrative mechanism with strategy. Acad. Manage.J. 1988, 31, 838–853. [Google Scholar] [CrossRef]

- Liao, Y.S. Business strategy and performance: The role of human resource management control. Pers. Rev. 2005, 34, 294–309. [Google Scholar] [CrossRef]

- Azumi, K.; Hage, J. Organization System; Heath and Company Lexington: Washington, DC, USA, 1972. [Google Scholar]

- Gul, F.A. The effect of management accounting system and environment uncertainty on small business managers’ performance. Account. Bus. Res. 1992, 22, 57–61. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Morris, D. The impact of structure, environment, and interdependency on the perceived usefulness of management accounting system. Account. Rev. 1986, 61, 16–35. [Google Scholar]

- Abernethy, M.A.; Brownell, P. The role of budgets in organizations facing strategic change: An exploratory study. Account. Organ. Soc. 1999, 24, 189–204. [Google Scholar] [CrossRef]

- Davila, T. An empirical study on the drivers of management control systems’ design in new product development. Account. Organ. Soc. 2000, 25, 383–409. [Google Scholar] [CrossRef]

- Marginson, D.E. Management control system and their effect on strategy formation at middle-management level: Evidence from a UK organization. Strate. Manage. J. 2002, 23, 1019–1031. [Google Scholar]

- Salmon, S.; Joiner, T. How integrative management accounting information and role ambiguity influence managerial performance. In Proceedings of the 19th Australia and New Zealand Academy of Management Conference: Engaging the Multiple Contexts of Management, Canberra, Australia, 7–10 December 2005.

- Coenders, G.; Bisbe, J.; Saris, W.E.; Batista-Foguet, J.M. Moderating Effects of Management Control Systems and Innovation on Performance. Simple Methods for Correcting the Effects of Measurement Error for Interaction Effects in Small Samples; Working Papers of the Department of Economics, University of Girona: Girona, Spain, 2003. [Google Scholar]

- Alexander, J.W.; Alan, R.W. The fit between technology and structure as predictor of performance. Acad. Manage. J. 1985, 28, 844–859. [Google Scholar] [CrossRef] [PubMed]

- Langfield-Smith, K. Management control systems and strategy: A critical review. Account. Organ. Soc. 1997, 22, 207–232. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.M. The corporate social performance-financial performance link. Strateg. Manage. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Dean, K.L. The chicken and the egg revisited: Ties between corporate social performance and the financial bottom line. Acad. Manage. Exec. 1988, 2, 99–100. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A Meta analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar]

- Cochran, P.L.; Wood, R.A. Corporate social performance and financial performance. Acad. Manage. J. 1984, 27, 42–56. [Google Scholar] [CrossRef]

- Shane, P.B.; Spicer, B.H. Market response to environmental information produced outside the firm. Account. Rev. 1983, 58, 521–538. [Google Scholar]

- Preston, L.E. Analyzing corporate social performance: Methods and results. J. Contemp. Bus. 1978, 7, 135–150. [Google Scholar]

- Vance, S. Are socially responsible firms good investment risks? Manage. Rev. 1975, 64, 18–24. [Google Scholar]

- Simerly, R.L. Corporate social performance and firms’ financial performance: An alternative perspective. Psychol. Rep. 1994, 75, 1091–1103. [Google Scholar]

- Pava, M.L.; Krausz, J. The association between corporate social-responsibility and financial performance: The paradox of social cost. J. Bus. Ethics 2002, 15, 321–357. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employee. Acad. Manage. J. 1996, 40, 658–672. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manage. J. 1997, 40, 534–559. [Google Scholar]

- Mahoney, L.S.; Roberts, R.W. Corporate social performance, financial performance and institutional ownership in Canadian Firms. Account. Forum 2007, 31, 233–253. [Google Scholar] [CrossRef]

- Stanwick, P.A.; Stanwick, S.D. The relationship between corporate social performance and organizational size, financial performance, and environmental performance: An empirical examination. J. Bus. Ethics 1998, 17, 195–204. [Google Scholar] [CrossRef]

- Moore, G. Corporate social and financial performance: An investigation in the UK supermarket industry. J. Bus. Ethics 2001, 34, 299–315. [Google Scholar] [CrossRef]

- Reimann, B.C. Organizational effectiveness and management’s public values: A canonical analysis. Acad. Manage. J. 1975, 18, 224–241. [Google Scholar] [CrossRef]

- Wartick, S.L. How issues management contributes to corporate performance. Business Forum 1988, 13, 16–22. [Google Scholar]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manage. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate social performance. Acad. Manage. Rev. 1979, 4, 497–506. [Google Scholar]

- Carroll, A.B. Corporate social responsibility: Evolution of a definitional construct. Bus. Soc. 1999, 33, 268–295. [Google Scholar] [CrossRef]

- Wood, D.J. Corporate social performance revisited. Acad. Manage. Rev. 1991, 16, 691–718. [Google Scholar]

- Wartick, S.L.; Cochran, P.L. The evolution of the corporate social performance model. Acad. Manage. Rev. 1985, 10, 758–769. [Google Scholar]

- Clarkson, M.B.E. A stakeholder framework for analyzing and evaluating corporation social performance. Acad. Manage. Rev. 1995, 20, 92–117. [Google Scholar]

- Gerde, V.W.; Wokutch, R. 25 years and going strong: A content analysis of the first 25 years of the social issues in management division proceedings. Bus. Soc. 1988, 37, 414–446. [Google Scholar] [CrossRef]

- Igalens, J.; Gond, J.P. Measuring corporate social performance in France: A critical and empirical analysis of ARESE data. J. Bus. Ethics 2005, 56, 131–148. [Google Scholar] [CrossRef]

- Anderson, G.J.; Frankle, A.W. Voluntary social reporting: An iso-beta portfolio analysis. Account. Rev. 1980, 55, 467–486. [Google Scholar]

- Gray, R.H.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Gray, R.H.; Kouhy, R.; Lavers, S. Constructing a research database of social and environmental reporting by UK companies: A methodological note. Account. Audit. Account. J. 1995, 8, 78–101. [Google Scholar]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Adams, C. Harte The changing portrayal of the employment of women in British bank and retail companies: Corporate annual reports. Account. Organ. Soc. 1998, 23, 781–812. [Google Scholar] [CrossRef]

- Spencer, B.A.; Taylor, S.G. A Within and Between Analysis of the relationship between corporate social responsibility and financial performance. Akron Bus. Econ. Rev. 1987, 18, 7–18. [Google Scholar]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manage. J. 1988, 3, 854–872. [Google Scholar] [CrossRef]

- Fombrun, C.; Shanley, M. What’s in a name? Reputation building and corporate strategy. Acade. Manage. J. 1990, 33, 233–258. [Google Scholar] [CrossRef]

- Brown, B.; Perry, S. Removing the financial performance halo from fortune’s most admired companies. Acad. Manage. J. 1994, 37, 1346–1359. [Google Scholar] [CrossRef]

- Brown, B.; Susan Perry, S. Halo-removed residuals of Fortune’s responsibility to the community and environment: A decade of data. Bus. Soc. 1995, 34, 199–215. [Google Scholar] [CrossRef]

- Simerly, R.L. Institutional ownership, corporate social performance, and firms’ financial performance. Psychol. Rep. 1995, 77, 515–525. [Google Scholar] [CrossRef]

- Sharfman, M. A concurrent validity study of the KLD Social Performance Ratings data. J. Bus. Ethics 1996, 15, 287–296. [Google Scholar] [CrossRef]

- Belkaoui, A. The impact of the disclosure of the environmental effects of organizational behavior on the market. Finan. Manage. 1976, 5, 26–31. [Google Scholar] [CrossRef]

- Chen, K.H.; Metcalf, R.W. The relationship between pollution control record and financial indicators revisited. Account. Rev. 1980, 55, 168–177. [Google Scholar]

- Shane, P.B.; Spicer, B.H. Market response to environmental information produced outside the firm. Account. Rev. 1983, 58, 521–538. [Google Scholar]

- Wartick, S.L. How issues management contributes to corporate performance. Bus. Forum 1988, 13, 16–22. [Google Scholar]

- Stark, A. What’s the matter with business ethics? Harvard Bus. Rev. 1993, 71, 38–48. [Google Scholar]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, A.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acade. Manage. J. 1985, 28, 446–463. [Google Scholar]

- Ingram, R.W.; Frazier, K.B. Environmental performance and corporate disclosure. J. Account. Res. 1980, 18, 614–622. [Google Scholar] [CrossRef]

- O’Neill, H.M.; Saunders, C.B.; McCarthy, A.D. Board members, corporate social responsiveness and profitability: Are tradeoffs necessary? J. Bus. Ethics 1980, 8, 353–357. [Google Scholar] [CrossRef]

- Hansen, G.S.; Wernerfelt, B. Determinants of firm performance: The relative importance of economic and organizational factors. Strateg. Manage. J. 1989, 10, 399–411. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Science Quart. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Itkonen, L. Corporate Social Responsibility and Financial Performance; Institute of Strategy and International Business: Hilsinki, Finland, 2003. [Google Scholar]

- Frederick, W.C.; Post, E.J.; Davis, K. Business and Society: Corporate Strategy, Public Policy, and Ethics; McGraw-Hill International Edition: Singapore, 1992. [Google Scholar]

- Atkinson, A.A.; Waterhouse, J.H.; Wells, R.B. A stakeholder approach to strategic performance measurement. Sloan Manage. Rev. 1997, 38, 25–37. [Google Scholar]

- Nickols, F. The Stakeholder Scorecard a Stakeholder-based Approach to Keeping Score. 2000. Available online: http://home.att.net/~nickols/articles.htm (accessed on 21 December 2008).

- The Triple Bottom Line: Does It All Add Up? Henriques, A.; Richardson, J. (Eds.) Earthscan: London, UK, 2004.

- Elkington, J. Towards the sustainable corporation: Win-win-win business strategies for Sustainable Corporationable Development. Calif. Manage. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- O’Donovan, G. The social bottom line. Aust. CPA 2002, 72, 66–69. [Google Scholar]

- Hubbard, G. Sustainable organisation performance: Towards a practical measurement system. Monash Bus. Rev. 2006, 2, 25–29. [Google Scholar] [CrossRef]

- Colbert, B.A.; Kurucz, E.C. Three conceptions of triple bottom line business sustainability and the role for HRM. Hum. Resour. Plan. 2007, 30, 21–29. [Google Scholar]

- Climate Change 2007: The Physical Science Basis—Summary for Policymakers; IPCC WGI Fourth Assessment Report; Intergovernmental Panel on Climate Change (IPCC): Geneva, Switzerland, 2007.

- Svensson, G. Anti-Climate Change Management (ACCM)—“Business-as-Usual” or “Out-of-the-Box? Manage. Decis. 2008, 46, 92–105. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Murphy, E.; Verschoor, C. Best corporate citizens have better financial performance. Strateg. Financ. 2002, 83, 20–22. [Google Scholar]

© 2010 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Fauzi, H.; Svensson, G.; Rahman, A.A. “Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future. Sustainability 2010, 2, 1345-1360. https://doi.org/10.3390/su2051345

Fauzi H, Svensson G, Rahman AA. “Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future. Sustainability. 2010; 2(5):1345-1360. https://doi.org/10.3390/su2051345

Chicago/Turabian StyleFauzi, Hasan, Goran Svensson, and Azhar Abdul Rahman. 2010. "“Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future" Sustainability 2, no. 5: 1345-1360. https://doi.org/10.3390/su2051345

APA StyleFauzi, H., Svensson, G., & Rahman, A. A. (2010). “Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future. Sustainability, 2(5), 1345-1360. https://doi.org/10.3390/su2051345