_Li.png)

CSR and Corporate Sustainability: Theoretical and Empirical Approaches Based on Data Science in Spanish Tourism Companies

Abstract

1. Introduction

- It provides an updated and detailed view of the theoretical fields of CSR and CS in tourism, evaluating the shift in research focus from CSR to CS. In the context of sustainable tourism, this is essential because a solid theoretical understanding can promote coherent changes that reduce ambiguity in academia and the implementation of business practices [15].

- It increases scientific knowledge about how Spanish tourism companies approach the theory of CSR and CS. Recent studies, such as those by Koh [19] and Back [7], highlight the need for more longitudinal and sectoral studies. These are useful for evaluating evolution over time and identifying the importance different subsectors attribute to sustainability.

2. Literature Review

2.1. Evolution of CSR and CS in Tourism

2.2. Application of Data Science in CSR and CS Reports

3. Research Questions and Hypotheses

4. Research Methodology

4.1. Methodology Applicable to the Theoretical Approach of the Computational Literature Review

4.1.1. Establishing the Conceptual Objective

4.1.2. Review Planning

4.1.3. Selection of Computational Techniques

4.1.4. Data Processing

- Tokenization: The text was divided into meaningful units, called tokens, which can be words or phrases. During this process, non-informative elements, such as punctuation marks, special characters, and whitespace, were removed to focus the analysis on relevant terms.

- Stop word removal: Common grammatical terms, such as articles, prepositions, and conjunctions, were excluded, as they do not contribute analytical value in the context of topic modeling and text classification.

- Lowercasing: All terms were converted to lowercase to ensure uniform representation and avoid inconsistencies caused by capitalization differences.

- Lemmatization: Words were reduced to their base or root form, unifying morphological variants of the same concept and minimizing the dispersion of textual data.

4.1.5. Content Analysis

4.1.6. Validation and Synthesis of Results

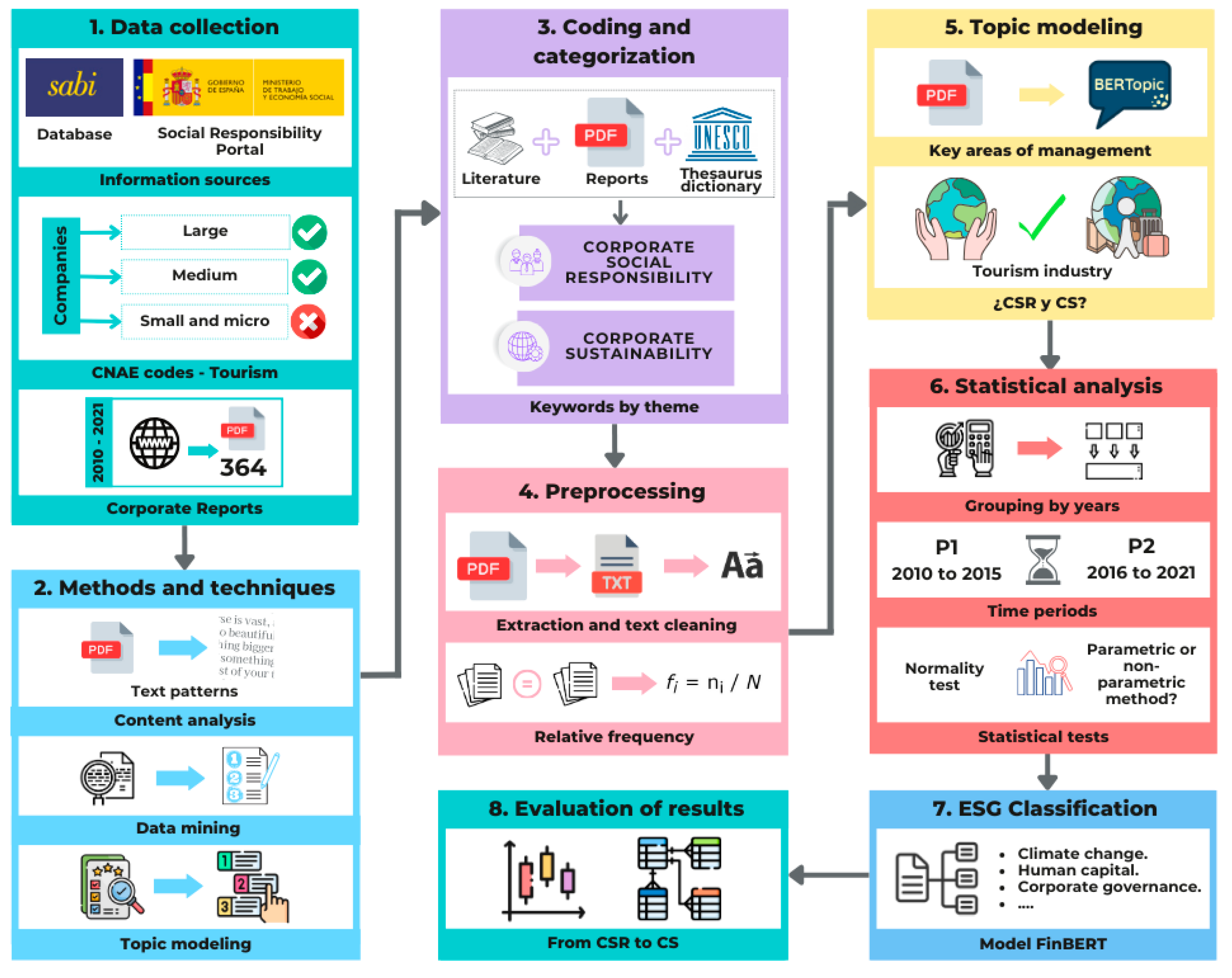

4.2. Methodology Applicable to the Empirical Approach of the Review of Corporate Reports from Spanish Tourism Companies

4.2.1. Data Collection

4.2.2. Methods and Techniques of Investigation

4.2.3. Coding and Categorization

- Theoretical grounding in previous studies: The process began with relevant research such as that of Karen [93], Palazzo and Scherer [94], and Van Marrewijk [20], which identify recurring terms in the literature regarding CSR and CS. These references provided a robust initial framework for identifying keywords, particularly in an interdisciplinary context like tourism.

- Supplementation with the UNESCO Thesaurus: Concepts related to “social responsibility” and “sustainable development” from the UNESCO Thesaurus [95] were incorporated. This thesaurus offers a controlled and structured list of terms used in international research, ensuring broad and up-to-date coverage of concepts, while minimizing biases associated with the use of individual sources.

- Contextual validation for Spanish companies: To adapt the keywords to the Spanish business context, a qualitative analysis of the collected reports was conducted, identifying specific terms used by companies in their corporate reports. This analysis enriched the initial categorization with terminology specific to the local context, resulting in a categorized framework that integrates both international academic perspectives and Spanish business practices.

4.2.4. Preprocessing

- Conversion and redundancy removal: PDF files were converted to the TXT format, and non-analytical elements such as headers, footers, and watermarks were removed.

- Text cleaning and normalization: Non-informative patterns, such as symbols, numbers, and isolated characters, were removed, and all text was converted to lowercase to unify the representation of terms and avoid inconsistencies.

- Stop word removal and lemmatization: Stop words, such as articles, prepositions, and conjunctions, which do not contribute analytical value, were eliminated. Additionally, lemmatization was performed to reduce words to their base or root form, unifying morphological variants and improving the semantic coherence of the data.

- Adjustment using relative frequency: To ensure comparability between documents of different lengths, the relative frequency method [97] was applied. Absolute word frequencies were adjusted to the total size of the text by dividing the absolute frequency of each pattern or word by the total number of words in the document, as proposed by Salinas and Martínez [98]. This approach has proven effective in previous research [76], particularly when document sizes vary considerably.

4.2.5. Topic Modeling Based on the BERTopic Approach

4.2.6. Statistical Analysis of the Data

4.2.7. Classification Under ESG Criteria

5. Results

5.1. Results of the Theoretical Approach: Computational Literature Review

5.2. Results of the Empirical Approach: Analysis of Corporate Reports from Tourism Companies

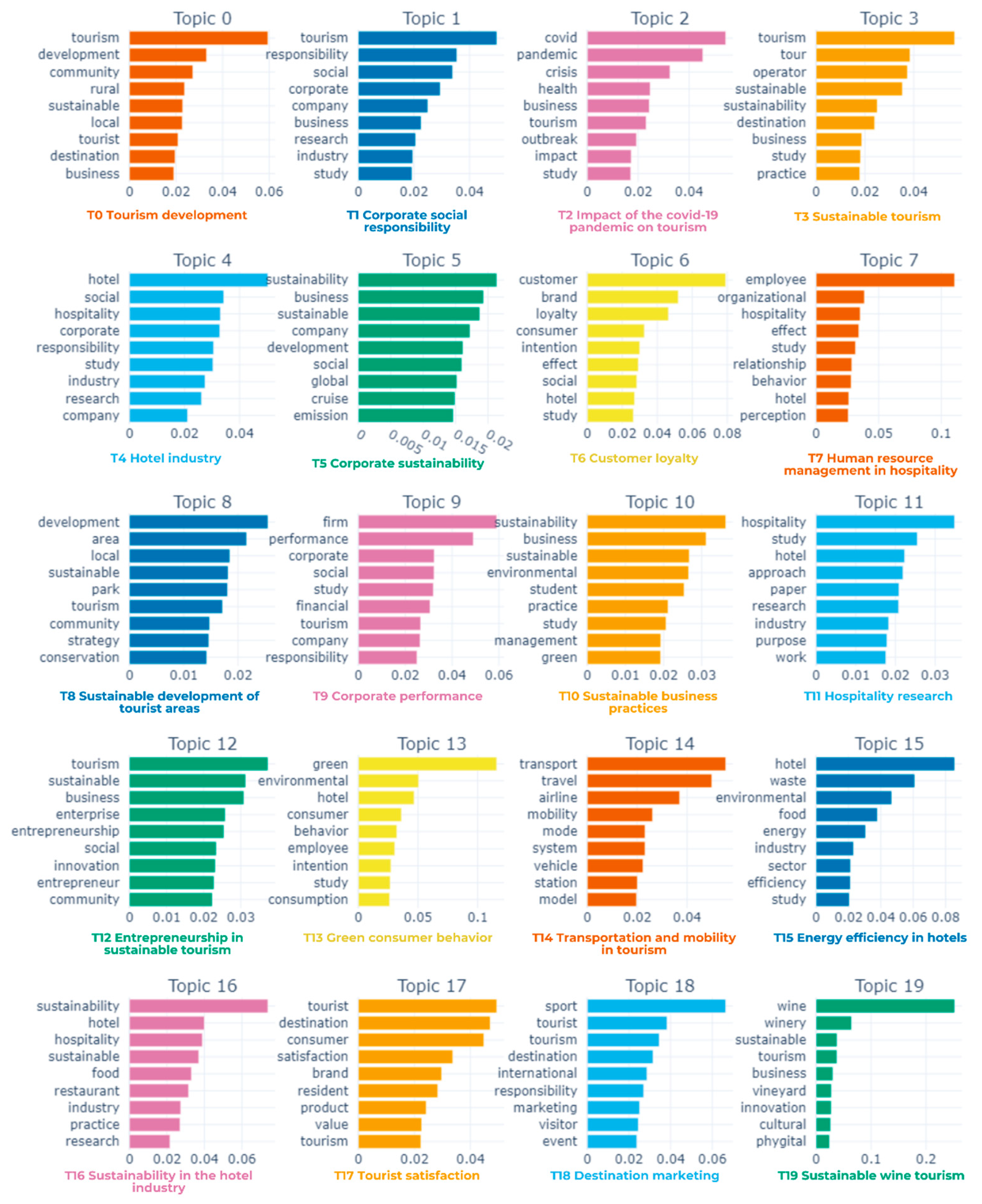

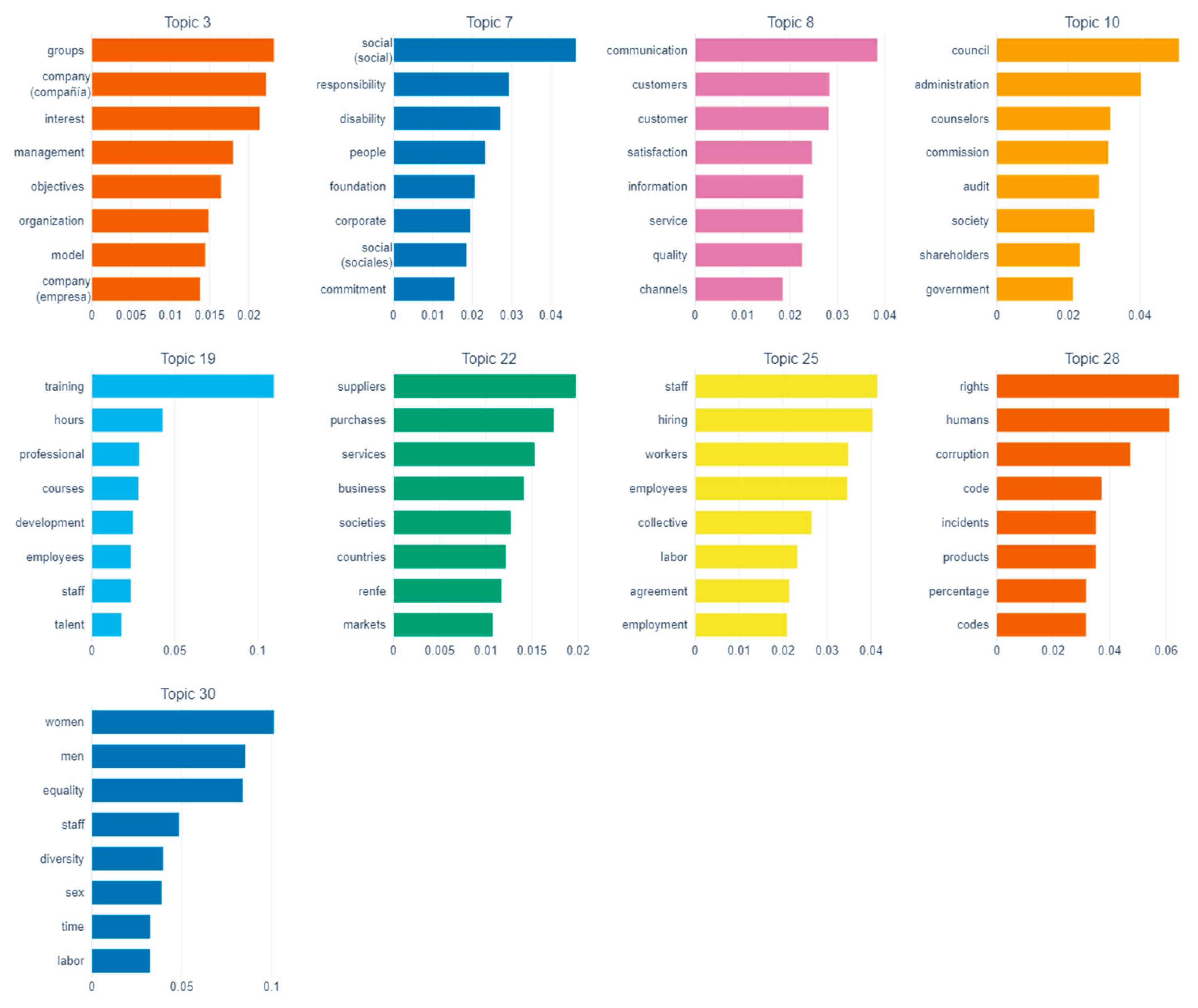

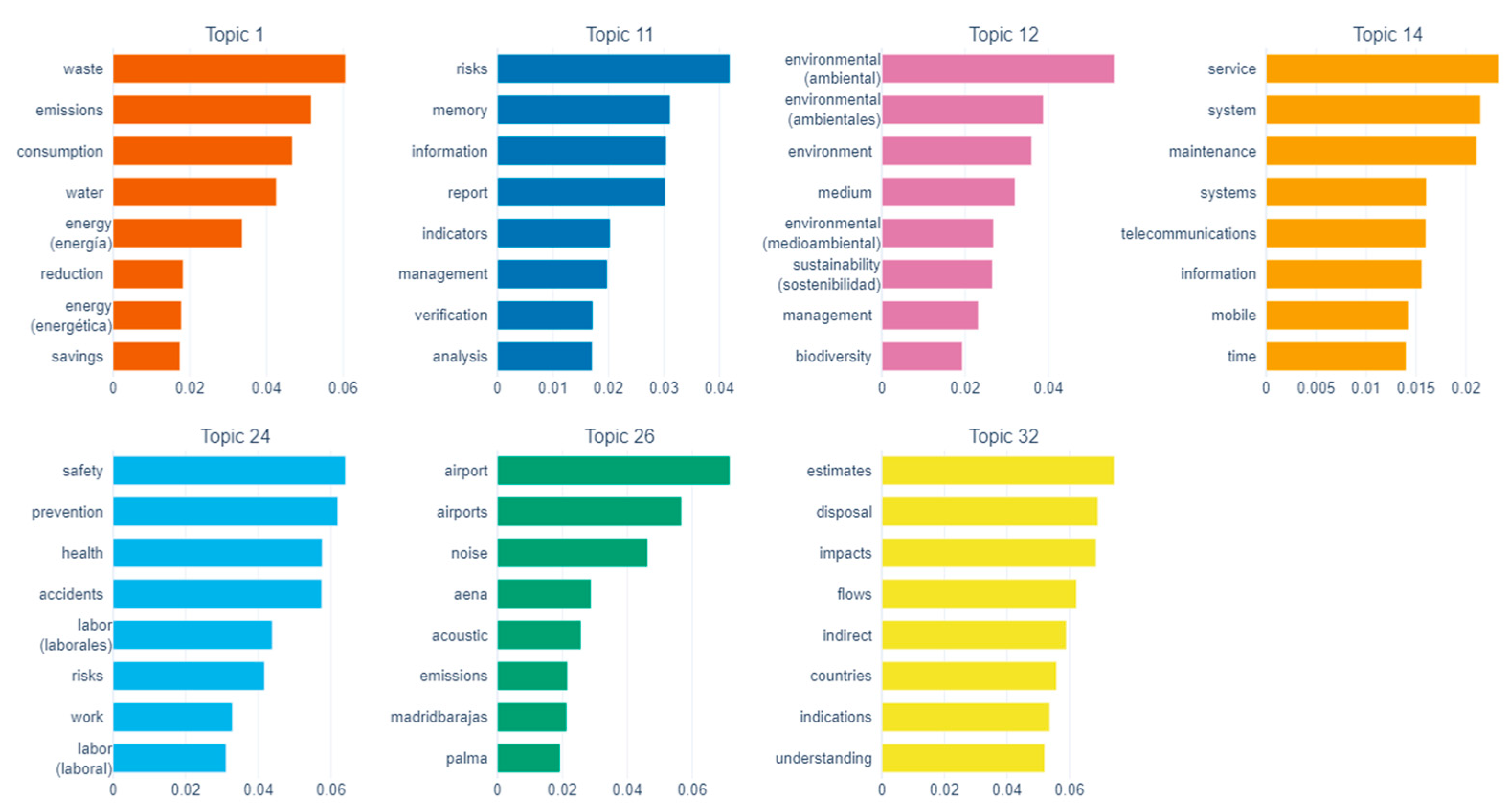

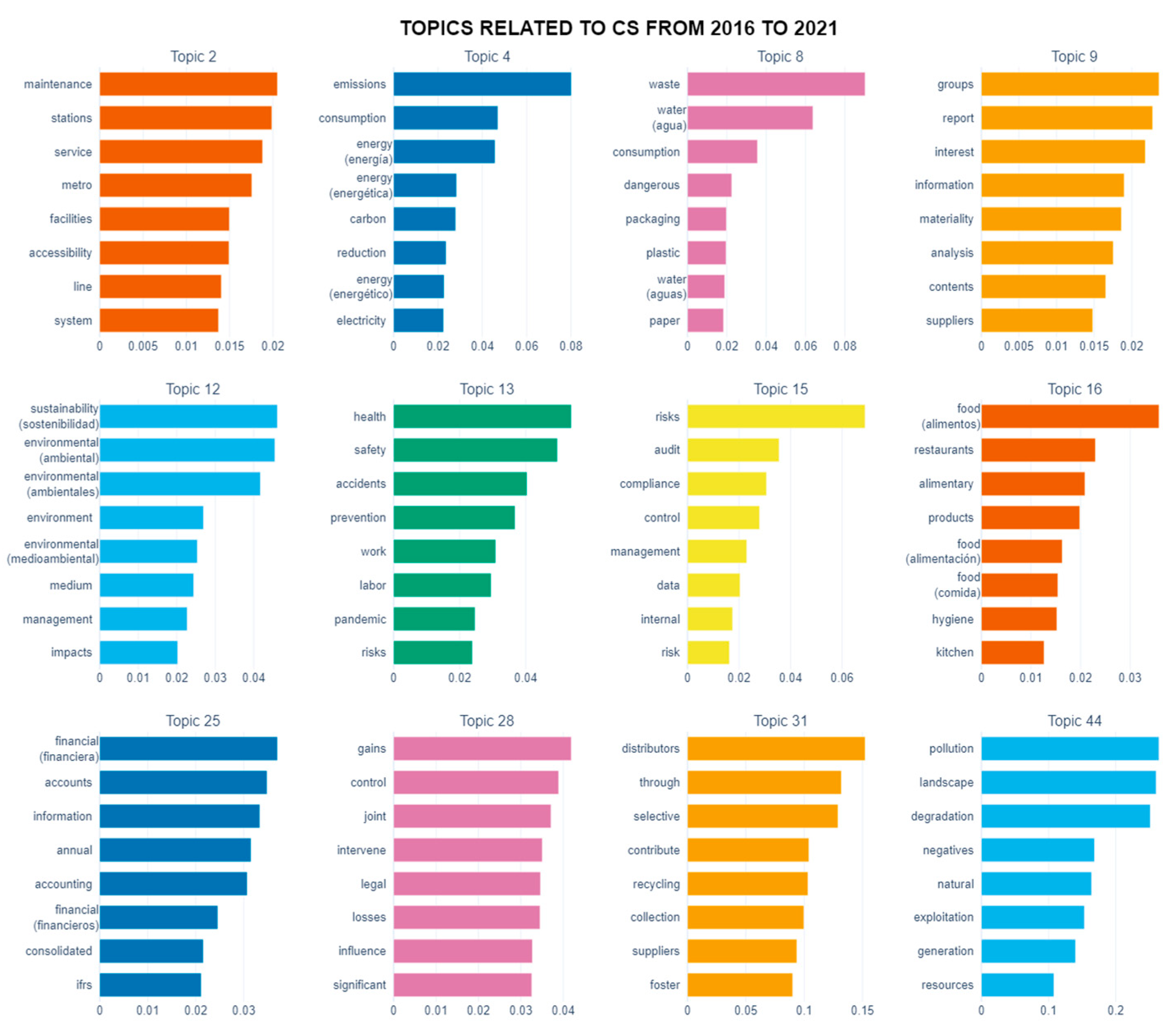

5.2.1. Topic Modeling with the BERTopic Approach

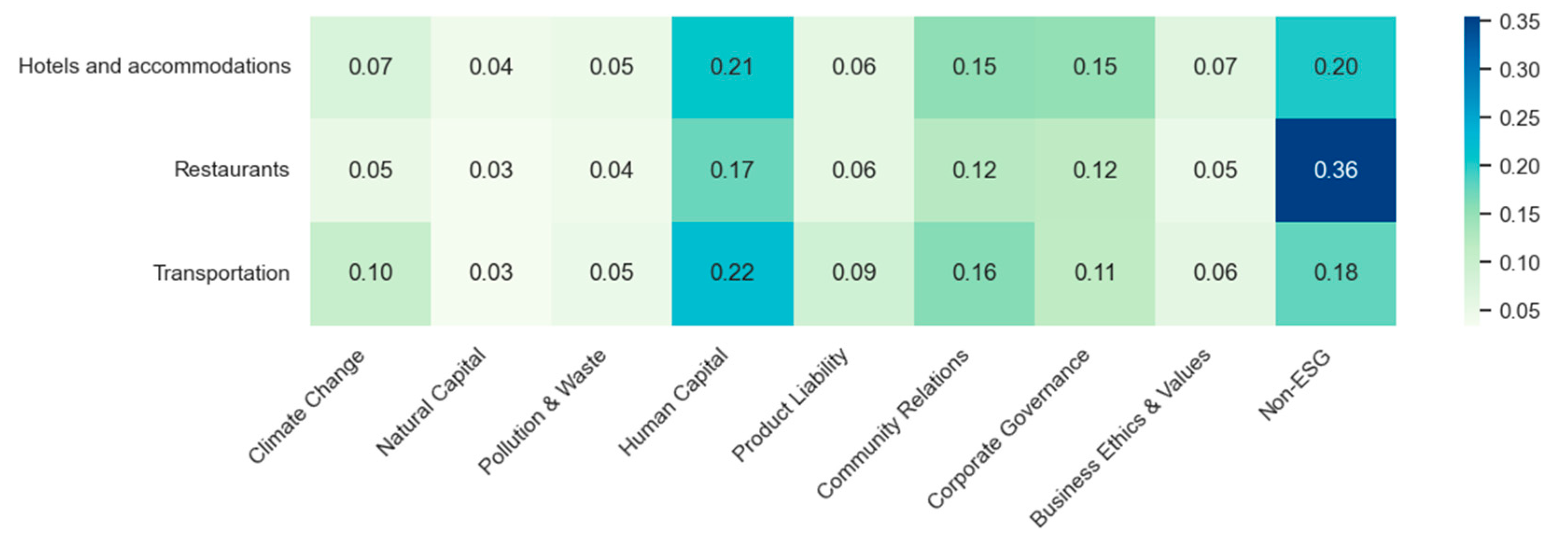

5.2.2. Key Areas of CSR and CS Management

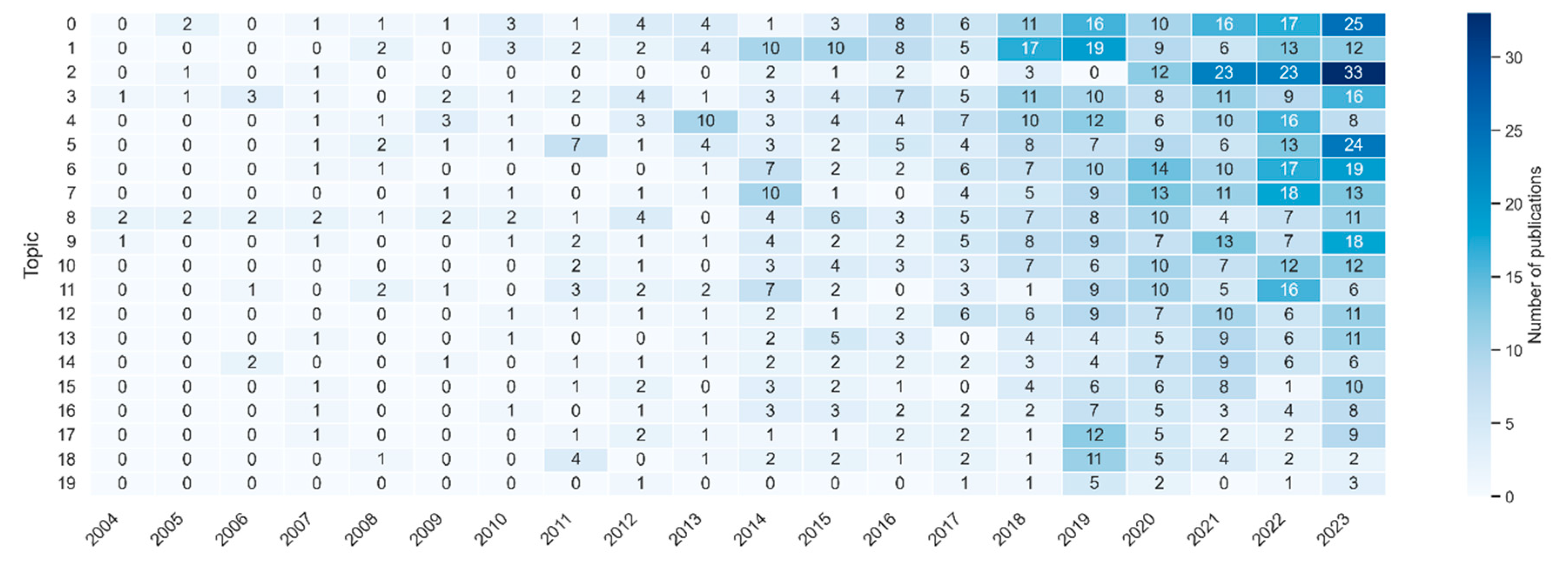

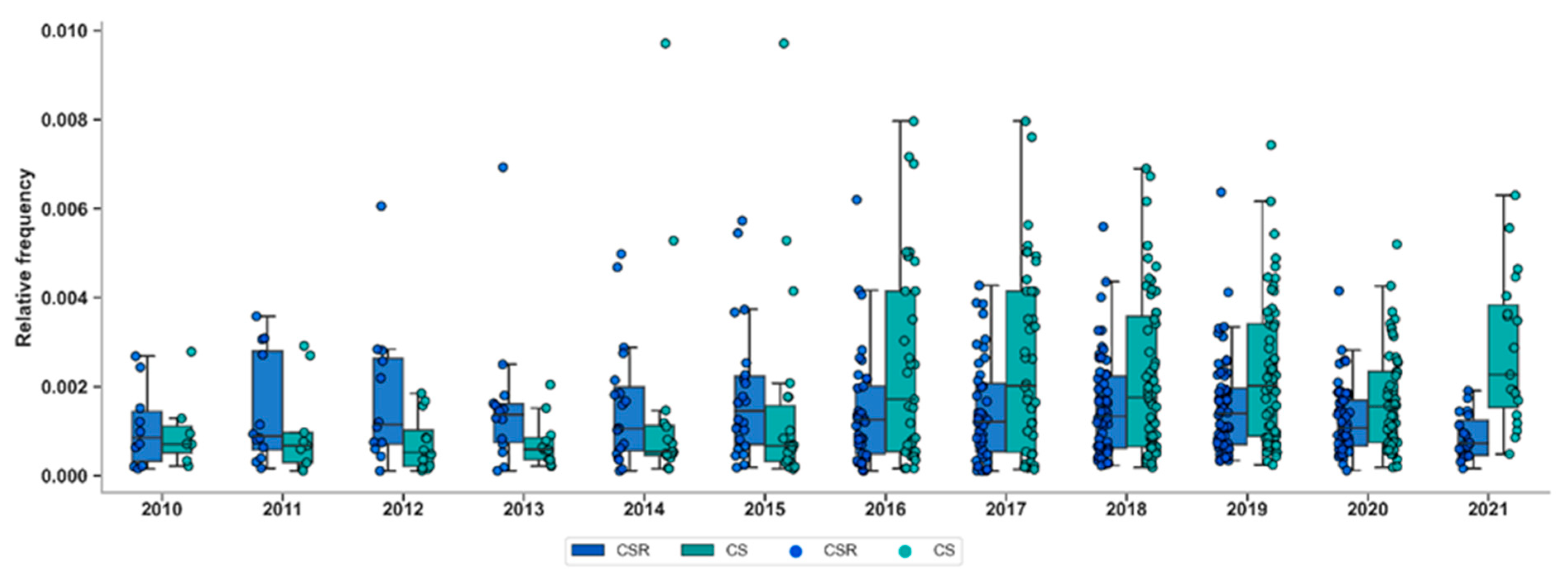

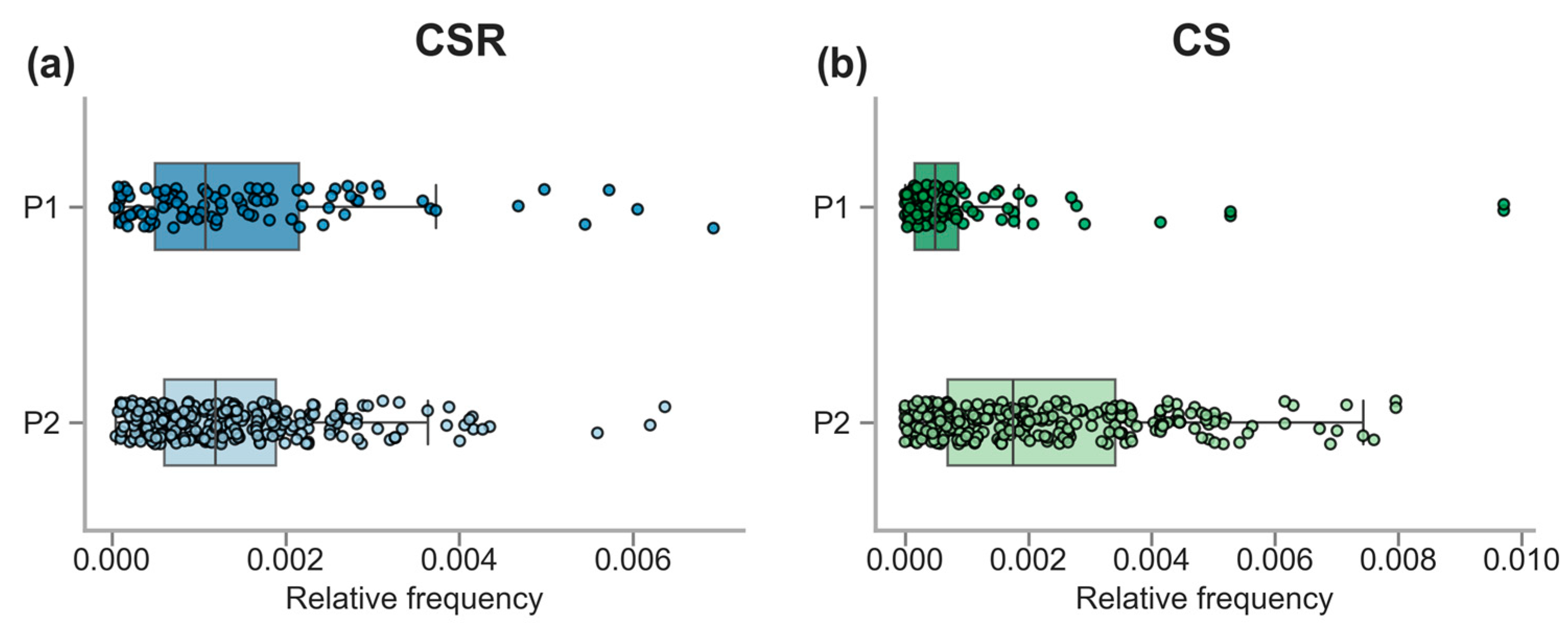

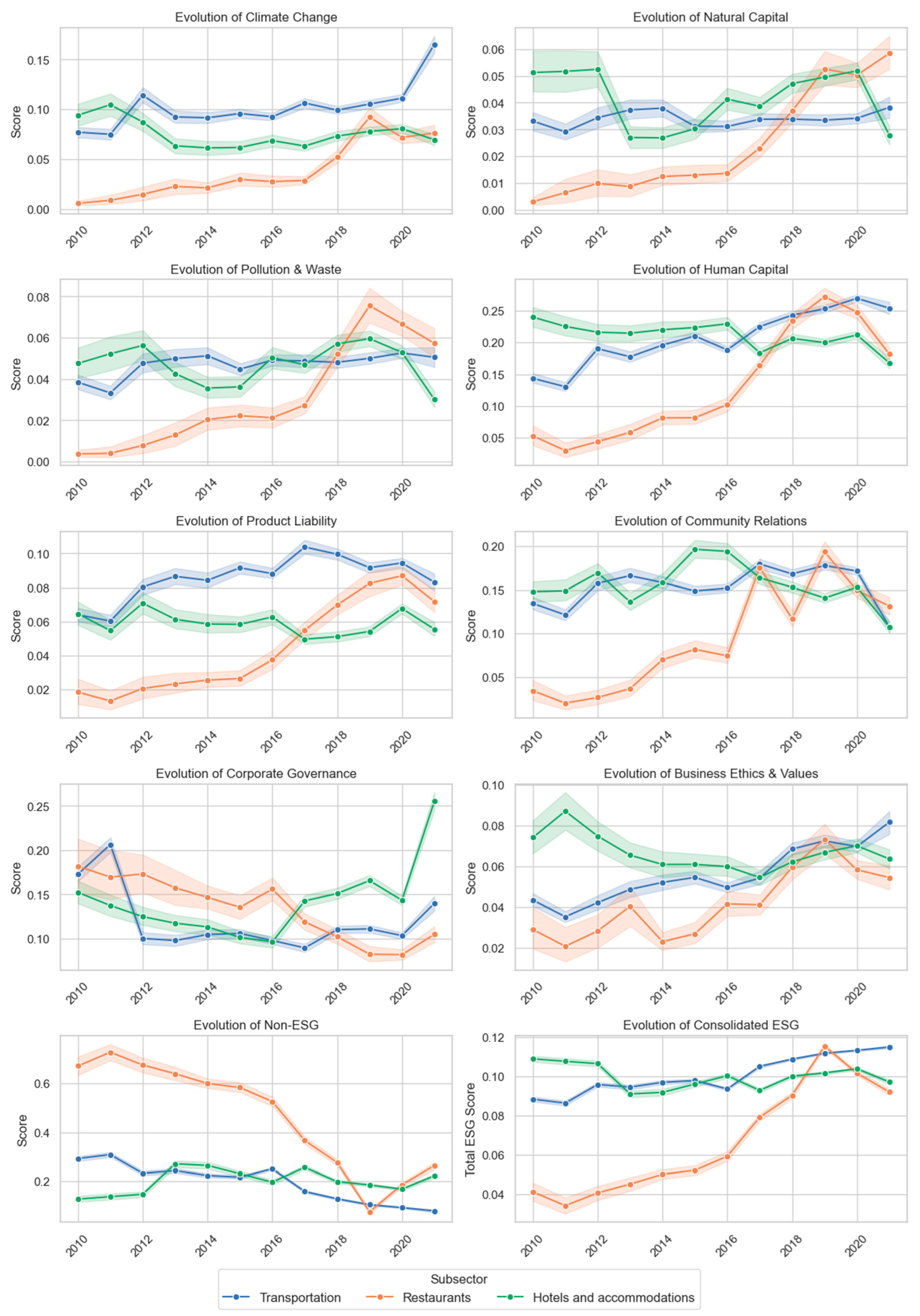

5.2.3. Descriptive Statistical Analysis

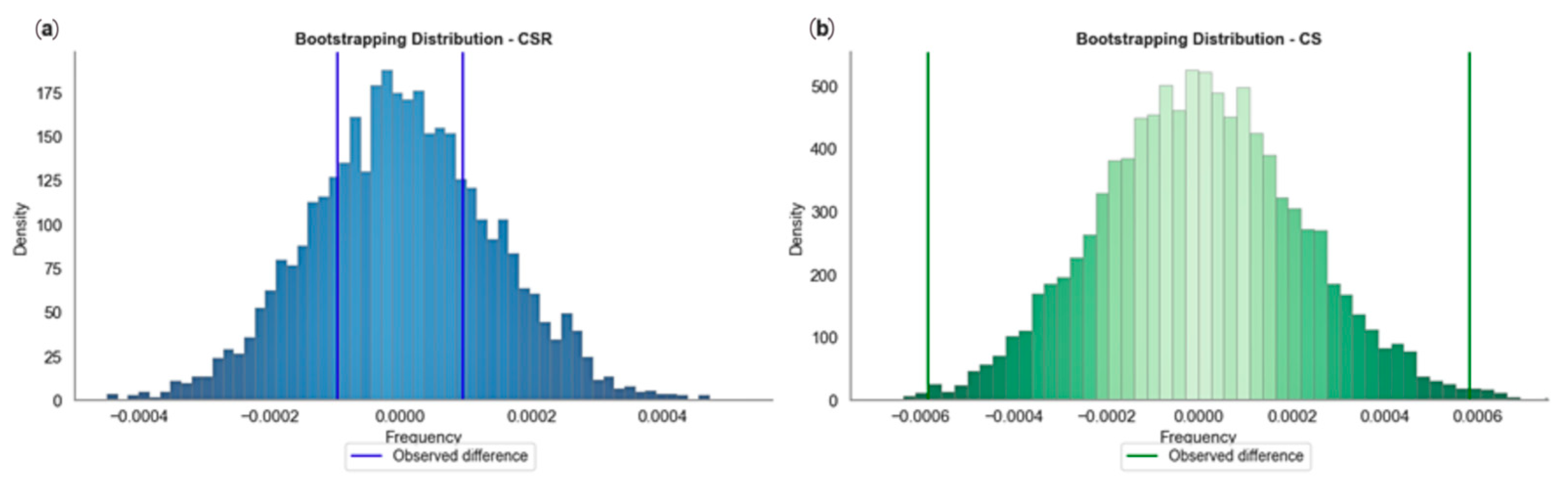

5.2.4. Normality and Bootstrapping Tests

- H1: “There is a significant change over time in the category ’corporate social responsibility’ observed through the words used in corporate reports of tourism companies” is rejected, as no statistically significant differences were observed between P1 and P2.

- H2: “There is a significant change over time in the category ’corporate sustainability’ observed through the words used in corporate reports of tourism companies” is accepted, given the significant increase observed in this category.

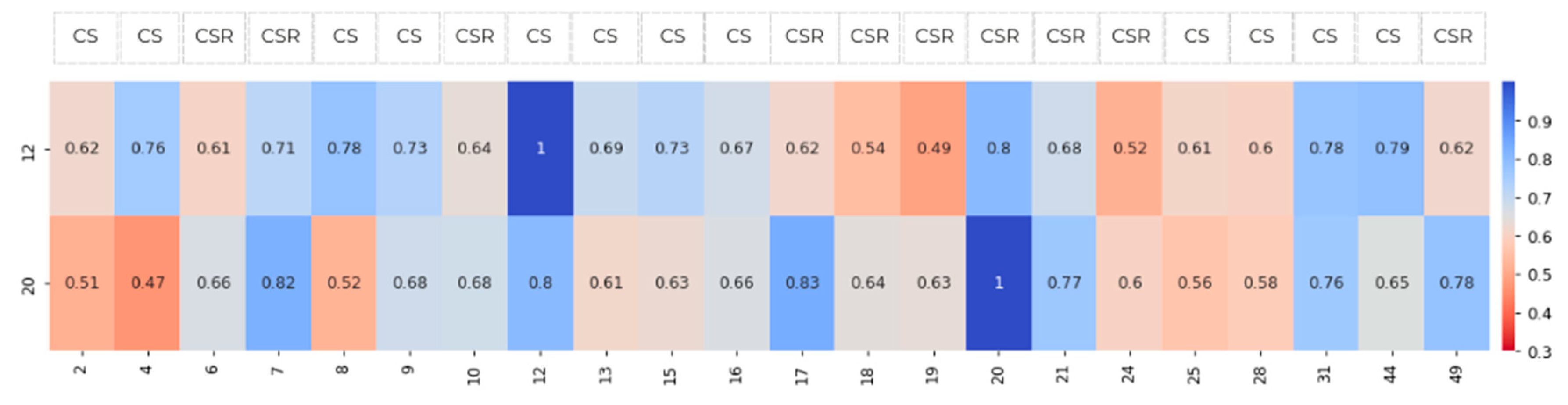

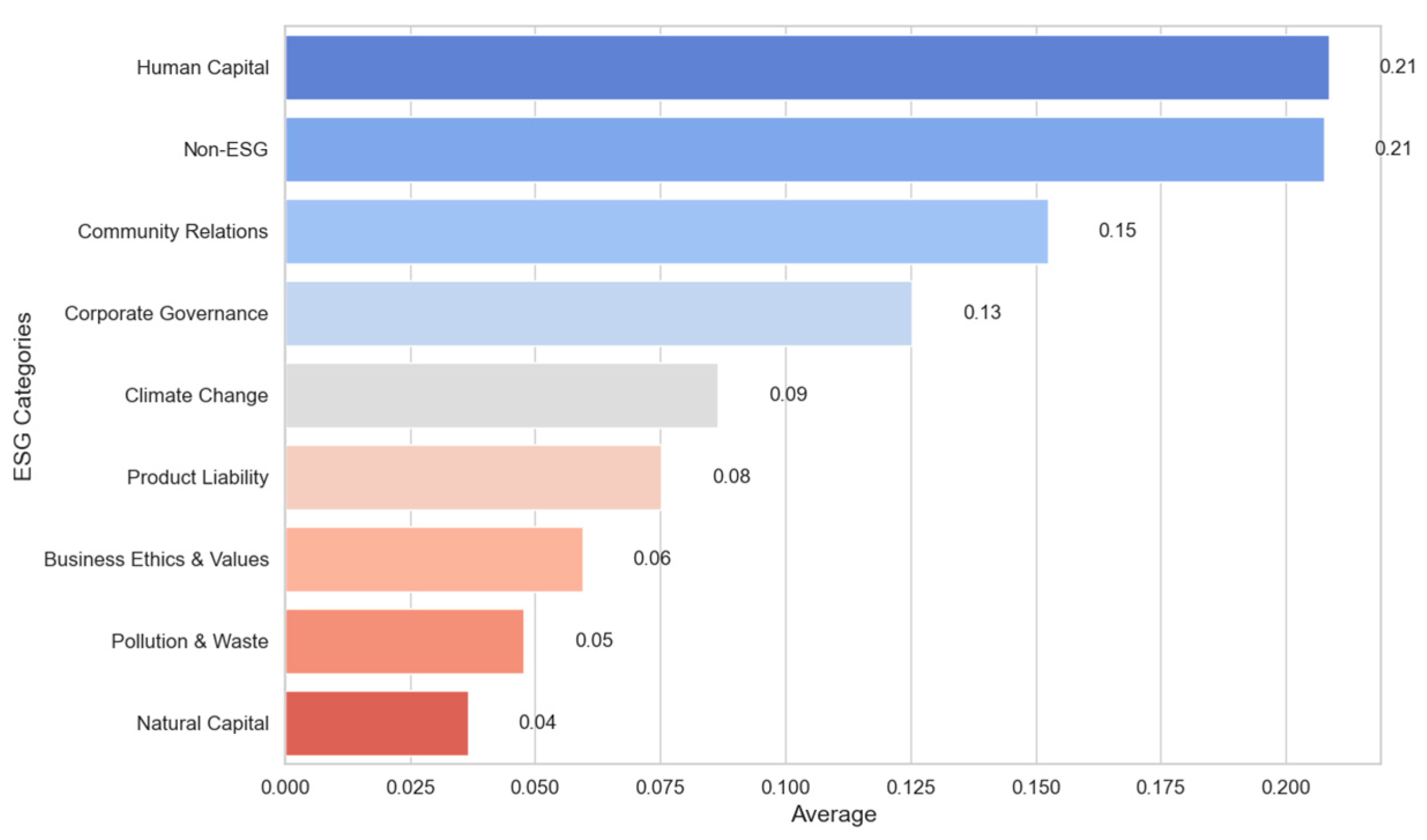

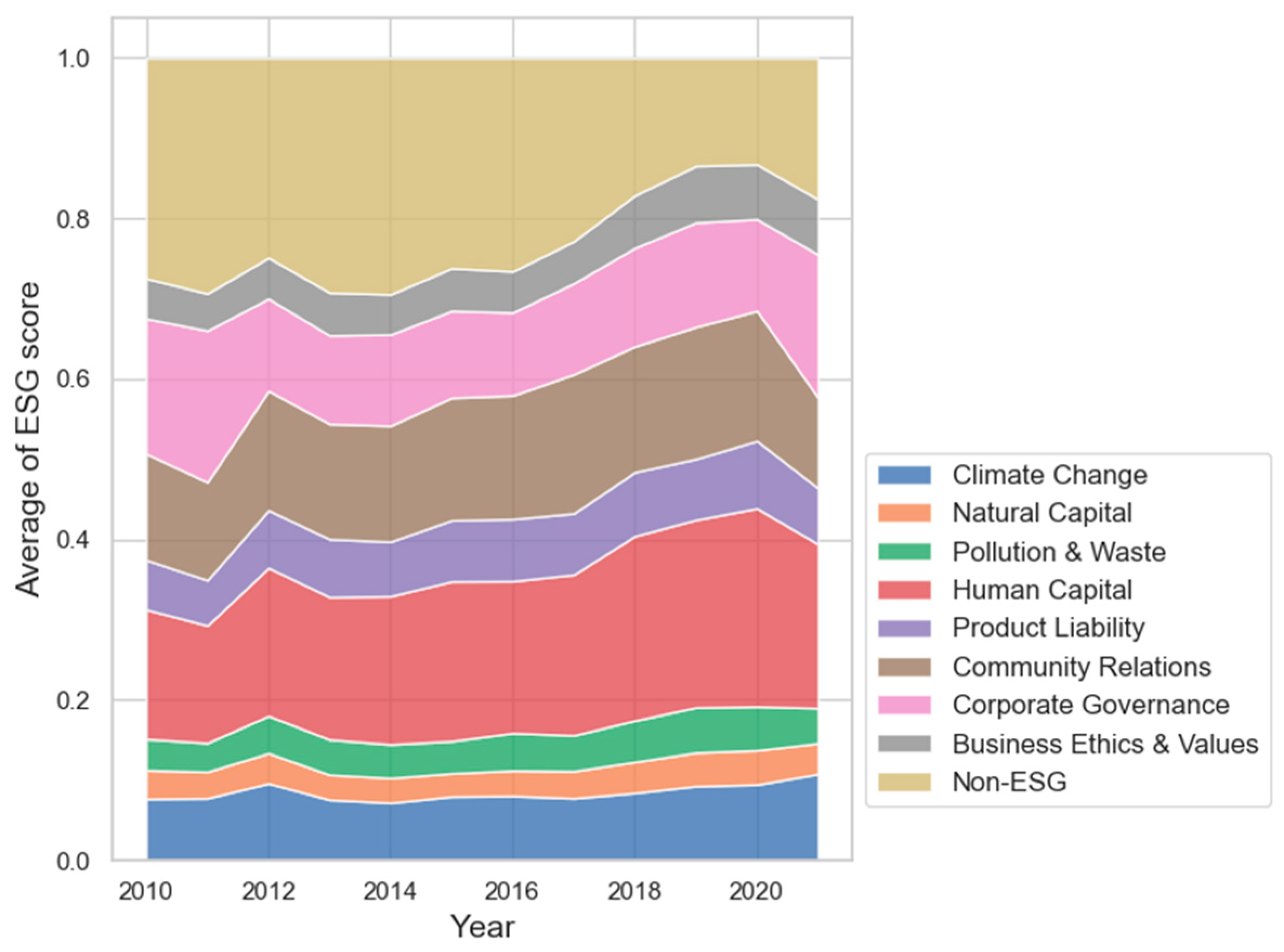

5.2.5. Importance of ESG Criteria in Spanish Tourism Companies

6. Conclusions

6.1. Conclusions Regarding the Theoretical Approach: Computational Literature Review

6.2. Conclusions Regarding the Empirical Approach: Review of Corporate Reports of Tourism Companies in Spain

6.3. Limitations and Future Lines of Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Lee, S.; Yeon, J.; Song, H.J. Current status and future perspective of the link of corporate social responsibility–corporate financial performance in the tourism and hospitality industry. Tour. Econ. 2022, 29, 1703–1735. [Google Scholar] [CrossRef]

- Font, X.; Walmsley, A.; Cogotti, S.; McCombes, L.; Häusler, N. Corporate social responsibility: The disclosure-performance gap. Tour. Manag. 2012, 33, 1544–1553. [Google Scholar] [CrossRef]

- Font, X.; Lynes, J. Corporate social responsibility in tourism and hospitality. J. Sustain. Tour. 2018, 26, 1027–1042. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability: Separate pasts, common futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef]

- Sheehy, B.; Farneti, F. Corporate social responsibility, sustainability, sustainable development and corporate sustainability: What is the difference, and does it matter? Sustainability 2021, 13, 5965. [Google Scholar] [CrossRef]

- Lu, H. The ‘legalisation’ of corporate social responsibility: Hong Kong experience on ESG reporting. Asia Pac. Law Rev. 2016, 24, 123–148. [Google Scholar] [CrossRef]

- Back, K.J. ESG for the hospitality and tourism research: Essential demanded research area for all. Tour. Manag. 2024, 105, 104954. [Google Scholar] [CrossRef]

- Legendre, T.S.; Ding, A.; Back, K.J. A bibliometric analysis of the hospitality and tourism environmental, social, and governance (ESG) literature. J. Hosp. Tour. Manag. 2024, 58, 309–321. [Google Scholar] [CrossRef]

- Grosbois, D. Corporate social responsibility reporting by the global hotel industry: Commitment, initiatives and performance. Int. J. Hosp. Manag. 2012, 31, 896–905. [Google Scholar] [CrossRef]

- Medrado, L.; Jackson, L.A. Corporate nonfinancial disclosures: An illuminating look at the corporate social responsibility and sustainability reporting practices of hospitality and tourism firms. Tour. Hosp. Res. 2015, 16, 116–132. [Google Scholar] [CrossRef]

- Diwan, H.; Amarayil Sreeraman, B. From financial reporting to ESG reporting: A bibliometric analysis of the evolution in corporate sustainability disclosures. Environ. Dev. Sustain. 2023, 26, 13769–13805. [Google Scholar] [CrossRef]

- Uyar, A.; Köseoglu, M.A.; Kılıç Karamahmutoğlu, M.; Mehraliyev, F. Thematic structure of sustainability reports of the hospitality and tourism sector: A periodical, regional, and format-based analysis. Curr. Issues Tour. 2020, 24, 2602–2627. [Google Scholar] [CrossRef]

- Mastercard; Turespaña. Expectativas y Comportamiento de los Viajeros Europeos en Materia de Sostenibilidad. 2023. Available online: https://www.tourspain.es/es/notas-prensa-turismo/espana-mejores-destinos-turisticos-viajeros-sostenibles/ (accessed on 25 September 2024).

- Google; Deloitte. Viajeros y Destinos NextGen: Nuestra Visión Sobre la Transformación del Sector Turístico. 2024. Available online: https://perspectivas.deloitte.com/l/915781/2024-06-11/t9wxf/915781/17180970624JfWZbST/20240305_Viajeros_Destinos_NextGen_Google.pdf (accessed on 25 September 2024).

- Miller, G.; Twining-Ward, L. Monitoring for a Sustainable Tourism Transition: The Challenge of Developing and Using Indicators; CABI Publishing: Wallingford, UK, 2005. [Google Scholar] [CrossRef]

- Egger, R. Applied Data Science in Tourism: Interdisciplinary Approaches, Methodologies, and Applications. In Tourism on the Verge; Springer: Cham, Switzerland, 2022. [Google Scholar]

- Mariani, M.; Baggio, R. Big data and analytics in hospitality and tourism: A systematic literature review. Int. J. Contemp. Hosp. Manag. 2022, 34, 231–278. [Google Scholar] [CrossRef]

- Mariani, M.; Baggio, R.; Fuchs, M.; Höepken, W. Business intelligence and big data in hospitality and tourism: A systematic literature review. Int. J. Contemp. Hosp. Manag. 2018, 30, 3514–3554. [Google Scholar] [CrossRef]

- Koh, Y. The industry-academia gap on the corporate governance issues in tourism and hospitality: A critical review and future research suggestions. J. Travel Tour. Mark. 2024, 41, 3–19. [Google Scholar] [CrossRef]

- Van Marrewijk, M. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Lechuga Sancho, M.P.; Martín-Navarro, A.; Ramos-Rodríguez, A.R. Information Systems Management Tools: An Application of Bibliometrics to CSR in the Tourism Sector. Sustainability 2020, 12, 8697. [Google Scholar] [CrossRef]

- Madanaguli, A.; Srivastava, S.; Ferraris, A.; Dhir, A. Corporate social responsibility and sustainability in the tourism sector: A systematic literature review and future outlook. Sustain. Dev. 2022, 30, 447–461. [Google Scholar] [CrossRef]

- Aragon-Correa, J.A.; Martin-Tapia, I.; de la Torre-Ruiz, J. Sustainability issues and hospitality and tourism firms’ strategies: Analytical review and future directions. Int. J. Contemp. Hosp. Manag. 2015, 27, 498–522. [Google Scholar] [CrossRef]

- Sánchez-Camacho, C.; Carranza, R.; Martín-Consuegra, D.; Díaz, E. Evolution, trends and future research lines in corporate social responsibility and tourism: A bibliometric analysis and science mapping. Sustain. Dev. 2022, 30, 462–476. [Google Scholar] [CrossRef]

- Wut, T.M.; Xu, J.; Wong, S.M.H. Timing and congruence effects of corporate social responsibility practices on social media crises in the tourism industry. J. Hosp. Tour. Technol. 2023, 14, 154–171. [Google Scholar] [CrossRef]

- Martínez, P.; Rodríguez del Bosque, I. Sustainability Dimensions: A Source to Enhance Corporate Reputation. Corp. Reput. Rev. 2014, 17, 239–253. [Google Scholar] [CrossRef]

- Martínez, P.; Rodríguez del Bosque, I. CSR and customer loyalty: The roles of trust, customer identification with the company and satisfaction. Int. J. Hosp. Manag. 2013, 35, 89–99. [Google Scholar] [CrossRef]

- Yoopetch, C.; Nimsai, S.; Kongarchapatara, B. Bibliometric Analysis of Corporate Social Responsibility in Tourism. Sustainability 2023, 15, 668. [Google Scholar] [CrossRef]

- Tuan, L.T.; Rajendran, D.; Rowley, C.; Khai, D.C. Customer value co-creation in the business-to-business tourism context: The roles of corporate social responsibility and customer empowering behaviors. J. Hosp. Tour. Manag. 2019, 39, 137–149. [Google Scholar] [CrossRef]

- Andreu Pinillos, A.; Fernández Fernández, J.L. De la RSC a la sostenibilidad corporativa: Una evolución necesaria para la creación de valor. Harv. Deusto Bus. Rev. 2011, 207, 5–21. [Google Scholar]

- Burbano, V.C.; Delmas, M.A.; Cobo, M.J. The Past and Future of Corporate Sustainability Research. Organ. Environ. 2023, 37, 133–158. [Google Scholar] [CrossRef]

- Serafeim, G. Social-impact efforts that create real value. Harv. Bus. Rev. 2020, 1–20. [Google Scholar]

- David, L.K.; Wang, J.; Angel, V.; Luo, M. China’s ESG scorecard: A predictive machine learning model. Corp. Soc. Responsib. Environ. Manag. 2024, 31, 3468–3486. [Google Scholar] [CrossRef]

- Hanson, D.; Usa, J.F.; Koller, T.; Jiang, B.; Raj, R.; Tarasoff, J.; Capital, G.L.; Mccormack, J.; Park, A.; Ravenel, C.; et al. ESG Investing in Graham & Doddsville. J. Appl. Corp. Financ. 2013, 25, 20–31. [Google Scholar] [CrossRef]

- Kumar, V.; Srivastava, A. Trends in the thematic landscape of corporate social responsibility research: A structural topic modeling approach. J. Bus. Res. 2022, 150, 26–37. [Google Scholar] [CrossRef]

- Yu, J.; Chiriko, A.Y.; Kim, S.; Moon, H.G.; Choi, H.; Han, H. ESG management of hotel brands: A management strategy for benefits and performance. Int. J. Hosp. Manag. 2025, 125, 103998. [Google Scholar] [CrossRef]

- Zhang, D.; Liu, L. Does ESG Performance Enhance Financial Flexibility? Evidence from China. Sustainability 2022, 14, 11324. [Google Scholar] [CrossRef]

- Chen, C.D.; Su, C.H.J.; Chen, M.H. Are ESG-committed hotels financially resilient to the COVID-19 pandemic? An autoregressive jump intensity trend model. Tour. Manag. 2022, 93, 104581. [Google Scholar] [CrossRef] [PubMed]

- Cohen, R.; Kennedy, P. Global Sociology; Bloomsbury Publishing: London, UK, 2017. [Google Scholar]

- Henderson, J.C. Corporate social responsibility and tourism: Hotel companies in Phuket, Thailand, after the Indian Ocean tsunami. Int. J. Hosp. Manag. 2007, 26, 228–239. [Google Scholar] [CrossRef]

- Gössling, S.; Peeters, P. Assessing tourism’s global environmental impact 1900–2050. J. Sustain. Tour. 2025, 23, 639–659. [Google Scholar] [CrossRef]

- Sørensen, F.; Bærenholdt, J.O. Tourist practices in the circular economy. Ann. Tour. Res. 2020, 85, 103027. [Google Scholar] [CrossRef]

- Strippoli, R.; Gallucci, T.; Ingrao, C. Circular economy and sustainable development in the tourism sector—An overview of the truly-effective strategies and related benefits. Heliyon 2024, 10, e36801. [Google Scholar] [CrossRef]

- Gül, H.; Çağatay, S.; Gartner, W.C. Fossil fuel and resource use impacts of raw material substitution and recycling in tourism sector in Türkiye: Evidence from circular economy adjusted input-output matrix. Curr. Issues Tour. 2024, 1–20. [Google Scholar] [CrossRef]

- García, C.; Herrero, B.; Morillas-Jurado, F. The impact of the environmental, social and governance dimensions of sustainability on firm risk in the hospitality and tourism industry. Corp. Soc. Responsib. Environ. Manag. 2024, 31, 2783–2800. [Google Scholar] [CrossRef]

- Alonso-Muñoz, S.; Torrejón-Ramos, M.; Medina-Salgado, M.S.; González-Sánchez, R. Sustainability as a building block for tourism—Future research: Tourism Agenda 2030. Tour. Rev. 2023, 78, 461–474. [Google Scholar] [CrossRef]

- Sharma, A.; Nunkoo, R.; Rana, N.P.; Dwivedi, Y.K. On the intellectual structure and influence of tourism social science research. Ann. Tour. Res. 2021, 91, 103142. [Google Scholar] [CrossRef]

- Nunkoo, R.; Sharma, A.; Rana, N.P.; Dwivedi, Y.K.; Sunnassee, V.A. Advancing sustainable development goals through interdisciplinarity in sustainable tourism research. J. Sustain. Tour. 2023, 31, 735–759. [Google Scholar] [CrossRef]

- Rasoolimanesh, S.M.; Ramakrishna, S.; Hall, C.M.; Esfandiar, K.; Seyfi, S. A systematic scoping review of sustainable tourism indicators in relation to the sustainable development goals. J. Sustain. Tour. 2023, 31, 1497–1517. [Google Scholar] [CrossRef]

- Girella, L.; Zambon, S.; Rossi, P. Reporting on sustainable development: A comparison of three Italian small and medium-sized enterprises. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 981–996. [Google Scholar] [CrossRef]

- Miralles-Quiros, M.D.M.; Miralles-Quiros, J.L.; Arraiano, I.G. Are Firms that Contribute to Sustainable Development Valued by Investors? Corp. Soc. Responsib. Environ. Manag. 2017, 24, 71–84. [Google Scholar] [CrossRef]

- Hsu, C.W.; Lee, W.H.; Chao, W.C. Materiality analysis model in sustainability reporting: A case study at Lite-On Technology Corporation. J. Clean. Prod. 2013, 57, 142–151. [Google Scholar] [CrossRef]

- Kumar, D. Role of corporate sustainability disclosures in moderating the impact of country-level uncertainties on tourism sector firms’ risk. J. Sustain. Tour. 2024, 32, 1287–1306. [Google Scholar] [CrossRef]

- Johann, M. CSR Strategy in Tourism during the COVID-19 Pandemic. Sustainability 2022, 14, 3773. [Google Scholar] [CrossRef]

- Zientara, P.; Adamska, J.; Bąk, M. What do tourism and hospitality companies convey about labor union relations in their CSR reports? A conceptual model and empirical findings. J. Sustain. Tour. 2024, 1–24. [Google Scholar] [CrossRef]

- Gajjar, T.; Okumus, F. Diversity management: What are the leading hospitality and tourism companies reporting? J. Hosp. Mark. Manag. 2018, 27, 905–925. [Google Scholar] [CrossRef]

- Quintás, M.A.; Martínez-Senra, A.I.; García-Pintos, A. Is the hotel industry really committed to the environment? Answering using the business models framework. Serv. Bus. 2023, 17, 395–428. [Google Scholar] [CrossRef]

- Geerts, M.; Dooms, M. An analysis of the CSR portfolio of cruise shipping lines. Res. Transp. Bus. Manag. 2022, 45, 100615. [Google Scholar] [CrossRef]

- Di Vaio, A.; Varriale, L.; Lekakou, M.; Pozzoli, M. SDGs disclosure: Evidence from cruise corporations’ sustainability reporting. Corp. Gov. 2023, 23, 845–866. [Google Scholar] [CrossRef]

- Di Vaio, A.; Hassan, R.; D’amore, G.; Dello Strologo, A. Digital Technologies for Sustainable Waste Management On-Board Ships: An Analysis of Best Practices from the Cruise Industry. IEEE Trans. Eng. Manag. 2024, 71, 12715–12728. [Google Scholar] [CrossRef]

- Yoon, J.; Han, S.; Lee, Y.; Hwang, H. Text Mining Analysis of ESG Management Reports in South Korea: Comparison with Sustainable Development Goals. SAGE Open 2023, 13, 21582440231202896. [Google Scholar] [CrossRef]

- Antons, D.; Breidbach, C.F.; Joshi, A.M.; Salge, T.O. Computational Literature Reviews: Method, Algorithms, and Roadmap. Organ. Res. Methods 2021, 26, 107–138. [Google Scholar] [CrossRef]

- Mortenson, M.J.; Vidgen, R. A computational literature review of the technology acceptance model. Int. J. Inf. Manag. 2016, 36, 1248–1259. [Google Scholar] [CrossRef]

- Grootendorst, M. MaartenGr/BERTopic: Fix Embedding Parameter. 2021. Available online: https://zenodo.org/records/4430182 (accessed on 6 August 2023).

- Deerwester, S.; Dumais, S.T.; Furnas, G.W.; Landauer, T.K.; Harshman, R. Indexing by latent semantic analysis. J. Am. Soc. Inf. Sci. 1990, 41, 391–407. [Google Scholar]

- Blei, D.M.; Ng, A.Y.; Jordan, M.I. Latent Dirichlet Allocation. J. Mach. Learn. Res. 2003, 3, 993–1022. [Google Scholar]

- Wallach, H.M. Topic Modeling: Beyond Bag-of-Words. In Proceedings of the ICML ’06: 23rd International Conference on Machine Learning, Pittsburgh, PA, USA, 25–29 June 2006; Association for Computing Machinery: New York, NY, USA, 2006; pp. 977–984. [Google Scholar]

- Grootendorst, M. BERTopic: Neural topic modeling with a class-based TF-IDF procedure. arXiv 2022, arXiv:2203.05794. [Google Scholar] [CrossRef]

- Uysal, A.K.; Gunal, S. The impact of preprocessing on text classification. Inf. Process. Manag. 2014, 50, 104–112. [Google Scholar] [CrossRef]

- Wang, Z.; Chen, J.; Chen, J.; Chen, H. Identifying interdisciplinary topics and their evolution based on BERTopic. Scientometrics 2023, 129, 7359–7384. [Google Scholar] [CrossRef]

- Douglas, T.; Capra, L.; Musolesi, M. A Computational Linguistic Approach to Study Border Theory at Scale. In Proceedings of the ACM on Human-Computer Interaction, 8(CSCW1), New York, NY, USA, 23 April 2024. [Google Scholar] [CrossRef]

- Kim, K.; Kogler, D.F.; Maliphol, S. Identifying interdisciplinary emergence in the science of science: Combination of network analysis and BERTopic. Humanit. Soc. Sci. Commun. 2024, 11, 1–15. [Google Scholar] [CrossRef]

- Kendall, M.G. Rank Correlation Methods, 4th ed.; Charles Griffin: London, UK, 1975. [Google Scholar]

- Mann, H.B. Nonparametric Tests Against Trend. Econometrica 1945, 13, 245. [Google Scholar] [CrossRef]

- Ning, X.; Yim, D.; Khuntia, J. Online sustainability reporting and firm performance: Lessons learned from text mining. Sustainability 2021, 13, 1069. [Google Scholar] [CrossRef]

- Landrum, N.E.; Ohsowski, B. Identifying Worldviews on Corporate Sustainability: A Content Analysis of Corporate Sustainability Reports. Bus. Strategy Environ. 2018, 27, 128–151. [Google Scholar] [CrossRef]

- Einwiller, S.A.; Carroll, C.E. Negative disclosures in corporate social responsibility reporting. Corp. Commun. 2020, 25, 319–337. [Google Scholar] [CrossRef]

- Ellili, N.O.D.; Nobanee, H. Impact of economic, environmental, and corporate social responsibility reporting on financial performance of UAE banks. Environ. Dev. Sustain. 2022, 25, 3967–3983. [Google Scholar] [CrossRef]

- Torelli, R.; Balluchi, F.; Furlotti, K. The materiality assessment and stakeholder engagement: A content analysis of sustainability reports. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 470–484. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; dos Santos, P.; Kensah, D. A Review of Dutch Corporate Sustainable Development Reports. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 321–339. [Google Scholar] [CrossRef]

- Campopiano, G.; de Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-family Firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Gatti, L.; Seele, P. Evidence for the prevalence of the sustainability concept in European corporate responsibility reporting. Sustain. Sci. 2014, 9, 89–102. [Google Scholar] [CrossRef]

- SABI. Sistema de Análisis de Balances Ibéricos. Último Acceso a La Web. 2022. Available online: https://sabi.informa.es/ (accessed on 6 August 2023).

- Branco, M.C.; Rodrigues, L.L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of corporate social responsibility disclosure ratings by Spanish listed firms. J. Bus. Ethics 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Khan, H. The effect of corporate governance elements on corporate social responsibility (CSR) reporting: Empirical evidence from private commercial banks of Bangladesh. Int. J. Law Manag. 2010, 52, 82–109. [Google Scholar]

- Ministerio de Trabajo y Economía Social. El Portal de la Responsabilidad Social. 2022. Available online: https://www.mites.gob.es/es/rse/ (accessed on 6 August 2023).

- Pizzi, S.; Caputo, A.; Corvino, A.; Venturelli, A. Management research and the UN sustainable development goals (SDGs): A bibliometric investigation and systematic review. J. Clean. Prod. 2020, 276, 124033. [Google Scholar] [CrossRef]

- Rosato, P.F.; Caputo, A.; Valente, D.; Pizzi, S. 2030 Agenda and Sustainable Business Models in Tourism: A Bibliometric Analysis. In Ecological Indicators; Elsevier: Amsterdam, The Netherlands, 2021; Volume 121. [Google Scholar] [CrossRef]

- Witten, I.; Frank, E.; Hall, M.A. Data Mining: Practical Machine Learning Tools and Techniques, 3rd ed.; Morgan Kaufmann: Burlington, MA, USA, 2011. [Google Scholar]

- Huang, A.; Wang, H.; Yang, Y. FinBERT: A Large Language Model for Extracting Information from Financial Text. Contemp. Account. Res. 2022, 40, 806–841. [Google Scholar] [CrossRef]

- Vives Varela, T.; Hamui Sutton, L. La codificación y categorización en la teoría fundamentada, un método para el análisis de los datos cualitativos. Investig. Educ. Médica 2021, 10, 97–104. [Google Scholar] [CrossRef]

- Karen, P. Corporate sustainability, citizenship and social responsibility reporting: A website study of 100 model corporations. J. Corp. Citizsh. 2008, 32, 63–78. [Google Scholar]

- Palazzo, G.; Scherer, A.G. Corporate legitimacy as deliberation: A communicative framework. J. Bus. Ethics 2006, 66, 71–88. [Google Scholar] [CrossRef]

- UNESCO. Tesauro de la UNESCO. 2022. Available online: https://vocabularies.unesco.org/ (accessed on 6 August 2023).

- García, S.; Ramírez-Gallego, S.; Luengo, J.; Herrera, F. Big Data: Preprocesamiento y calidad de datos. Novática 2016, 237, 17–23. [Google Scholar]

- Muller, C. Estadística Lingüística; Gredos S.A.: Madrid, Spain, 1973. [Google Scholar]

- Salinas, C.M.; Martínez, G.E.S. Hacia una normalización de la frecuencia de los corpus CREA y CORDE. Rev. Signos 2015, 48, 307–331. [Google Scholar] [CrossRef]

- D’Agostino, R.; Pearson, E.S. Tests for Departure from Normality. Empirical Results for the Distributions of b2 and √b1. Biometrika 1973, 60, 613–622. [Google Scholar] [CrossRef]

- Efron, B. Bootstrap methods: Another look at the Jackknife. Ann. Stat. 1979, 7, 1–26. [Google Scholar] [CrossRef]

- Srijiranon, K.; Lertratanakham, Y.; Tanantong, T. A Hybrid Framework Using PCA, EMD and LSTM Methods for Stock Market Price Prediction with Sentiment Analysis. Appl. Sci. 2022, 12, 10823. [Google Scholar] [CrossRef]

- Sinha, A.; Kedas, S.; Kumar, R.; Malo, P. SEntFiN 1.0: Entity-aware sentiment analysis for financial news. J. Assoc. Inf. Sci. Technol. 2022, 73, 1314–1335. [Google Scholar] [CrossRef]

- Gao, Y.; Zheng, W.; Wang, Y. Sectoral risk contagion and quantile network connectedness on Chinese stock sectors after the COVID-19 outbreak. China Financ. Rev. Int. 2023, in press. [Google Scholar] [CrossRef]

- Arami, M.; Balina, S.; Chang, V.; Kim, J.; Kim, H.-S.; Choi, S.-Y. Forecasting the S&P 500 Index Using Mathematical-Based Sentiment Analysis and Deep Learning Models: A FinBERT Transformer Model and LSTM. Axioms 2023, 12, 835. [Google Scholar] [CrossRef]

- Xiao, Q.; Ihnaini, B. Stock trend prediction using sentiment analysis. PeerJ Comput. Sci. 2023, 9, e1293. [Google Scholar] [CrossRef]

- Unlu, A.; Truong, S.; Tammi, T.; Lohiniva, A.L. Exploring Political Mistrust in Pandemic Risk Communication: Mixed-Method Study Using Social Media Data Analysis. J. Med. Internet Res. 2023, 25, e50199. [Google Scholar] [CrossRef]

- Unlu, A.; Truong, S.; Sawhney, N.; Sivelä, J.; Tammi, T. Tracing the dynamics of misinformation and vaccine stance in Finland amid COVID-19. Inf. Commun. Soc. 2024, 28, 193–217. [Google Scholar] [CrossRef]

- Fedorova, E.; Iasakova, P. The impact of climate change news on the US stock market. J. Risk Financ. 2024, 25, 293–320. [Google Scholar] [CrossRef]

- Sahu, A.K.; Debata, B.; Dash, S.R. Manager sentiment, policy uncertainty, ESG disclosure and firm performance: A large language model in corporate landscape. Int. J. Account. Inf. Manag. 2024, 32, 858–882. [Google Scholar] [CrossRef]

- Lane, B.; Kastenholz, E. Rural tourism: The evolution of practice and research approaches—Towards a new generation concept? J. Sustain. Tour. 2015, 23, 1133–1156. [Google Scholar] [CrossRef]

- Sigala, M. Tourism and COVID-19: Impacts and implications for advancing and resetting industry and research. J. Bus. Res. 2020, 117, 312–321. [Google Scholar] [CrossRef] [PubMed]

- Budeanu, A.; Miller, G.; Moscardo, G.; Ooi, C.S. Sustainable tourism, progress, challenges and opportunities: An introduction. J. Clean. Prod. 2016, 111, 285–294. [Google Scholar] [CrossRef]

- Cannas, R.; Argiolas, G.; Cabiddu, F. Fostering corporate sustainability in tourism management through social values within collective value co-creation processes. J. Sustain. Tour. 2019, 27, 139–155. [Google Scholar] [CrossRef]

- Sakshi Shashi Cerchione, R.; Bansal, H. Measuring the impact of sustainability policy and practices in tourism and hospitality industry. Bus. Strategy Environ. 2020, 29, 1109–1126. [Google Scholar] [CrossRef]

- Han, H.; Yu, J.; Lee, J.S.; Kim, W. Impact of hotels’ sustainability practices on guest attitudinal loyalty: Application of loyalty chain stages theory. J. Hosp. Mark. Manag. 2019, 28, 905–925. [Google Scholar] [CrossRef]

- de Lange, D.; Dodds, R. Increasing sustainable tourism through social entrepreneurship. Int. J. Contemp. Hosp. Manag. 2017, 29, 1977–2002. [Google Scholar] [CrossRef]

- Dyah Utami, D.; Dhewanto, W.; Dwi Lestari, Y.; Teknologi Bandung, I.; Aparicio, S. Rural tourism entrepreneurship success factors for sustainable tourism village: Evidence from Indonesia. Cogent Bus. Manag. 2023, 10, 2180845. [Google Scholar] [CrossRef]

- Vecchio, R.; Annunziata, A.; Bouzdine-Chameeva, T. How to promote sustainable wine tourism: Insights from Italian and French young adults. Ann. Tour. Res. Empir. Insights 2024, 5, 100137. [Google Scholar] [CrossRef]

- Martínez-Falcó, J.; Sánchez-García, E.; Marco-Lajara, B.; Millán-Tudela, L.A. Wine Tourism as a Catalyst for Sustainable Performance: The Mediating Role of Corporate Legitimacy and Green Innovation. Agribusiness 2024, early view. [Google Scholar] [CrossRef]

- Huang, S. A comprehensive science mapping of tourism and hospitality research: Tribes, territories and networks. J. Hosp. Leis. Sport Tour. Educ. 2025, 36, 100523. [Google Scholar] [CrossRef]

- Sánchez-Franco, M.J.; Rey-Moreno, M. Do travelers’ reviews depend on the destination? An analysis in coastal and urban peer-to-peer lodgings. Psychol. Mark. 2022, 39, 441–459. [Google Scholar] [CrossRef]

- Harrington, R.J.; Ottenbacher, M.C. Strategic management: An analysis of its representation and focus in recent hospitality research. Int. J. Contemp. Hosp. Manag. 2011, 23, 439–462. [Google Scholar] [CrossRef]

- Wang, C.; Xu, H.; Li, G. The corporate philanthropy and legitimacy strategy of tourism firms: A community perspective. J. Sustain. Tour. 2018, 26, 1124–1141. [Google Scholar] [CrossRef]

- Ruiz-Ortega, M.J.; Córcoles-Muñoz, M.M.; Parra-Requena, G.; García-Villaverde, P.M. Sustainability orientation and sustainability performance in response to hostile environments in cultural tourism destinations. Int. J. Tour. Cities 2023, 9, 974–994. [Google Scholar]

- Bilbao-Terol, A.; Arenas-Parra, M.; Cañal-Fernández, V.; Obam-Eyang, P.N. Multi-criteria analysis of the GRI sustainability reports: An application to Socially Responsible Investment. J. Oper. Res. Soc. 2018, 69, 1576–1598. [Google Scholar] [CrossRef]

- Zhang, J. Impacts of the emissions policies on tourism: An important but neglected aspect of sustainable tourism. J. Hosp. Tour. Manag. 2021, 47, 453–461. [Google Scholar] [CrossRef]

- Lin, M.S.; Zhang, H.; Luo, Y.; Li, Y. Environmental, social, and governance (ESG) measurement in the tourism and hospitality industry: Views from a developing country. J. Travel Tour. Mark. 2024, 41, 154–168. [Google Scholar] [CrossRef]

- Lee, S.; Ham, S.; Yeon, J.; Lee, M. ESG themes of the restaurant industry: A comparison between full-service and limited-service restaurants. J. Travel Tour. Mark. 2024, 41, 20–34. [Google Scholar] [CrossRef]

- Pérez Cañizares, P. “Corporate Sustainability” or “Corporate Social Responsibility”? A Comparative Study of Spanish and Latin American Companies’ Websites. Bus. Prof. Commun. Q. 2021, 84, 361–385. [Google Scholar] [CrossRef]

- Rhou, Y.; Singal, M. A review of the business case for CSR in the hospitality industry. Int. J. Hosp. Manag. 2020, 84, 102330. [Google Scholar] [CrossRef]

- Kaur, P.; Talwar, S.; Madanaguli, A.; Srivastava, S.; Dhir, A. Corporate social responsibility (CSR) and hospitality sector: Charting new frontiers for restaurant businesses. J. Bus. Res. 2022, 144, 1234–1248. [Google Scholar] [CrossRef]

- Yildiz, F.; Dayi, F.; Yucel, M.; Cilesiz, A. The Impact of ESG Criteria on Firm Value: A Strategic Analysis of the Airline Industry. Sustainability 2024, 16, 8300. [Google Scholar] [CrossRef]

- Sim, M.; Kim, H. Measurement validation of a consumer-driven environmental, social, and governance (ESG) index for the airline industry. J. Sustain. Tour. 2024, 33, 474–499. [Google Scholar] [CrossRef]

- Madanaguli, A.; Dhir, A.; Kaur, P.; Srivastava, S.; Singh, G. Environmental sustainability in restaurants. A systematic review and future research agenda on restaurant adoption of green practices. Scand. J. Hosp. Tour. 2022, 22, 303–330. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Category | Topic | ||

|---|---|---|---|

| C0 | Corporate Social Responsibility | T1 | Corporate social responsibility |

| C1 | Corporate Sustainability | T5 | Corporate sustainability |

| T10 | Sustainable business practices | ||

| C2 | Sustainable Tourism and Development | T0 | Tourism development |

| T3 | Sustainable tourism | ||

| T8 | Sustainable development of tourist areas | ||

| T12 | Entrepreneurship in sustainable tourism | ||

| T19 | Sustainable wine tourism | ||

| C3 | Hospitality and Hotel Management | T4 | Hotel industry |

| T7 | Human resource management in hospitality | ||

| T11 | Hospitality research | ||

| T16 | Sustainability in the hotel industry | ||

| T15 | Energy efficiency in hotels | ||

| C4 | Customers and Marketing | T6 | Customer loyalty |

| T17 | Tourist satisfaction | ||

| T13 | Green consumer behavior | ||

| T18 | Destination marketing | ||

| C5 | Corporate Performance | T9 | Corporate performance |

| C6 | COVID-19 Pandemic | T2 | Impact of the COVID-19 pandemic on tourism |

| C7 | Transportation and Mobility | T14 | Transportation and mobility in tourism |

| Topic | Trend | p-Value | Tau |

|---|---|---|---|

| Corporate Social Responsibility | Not significant | 0.788 | 0.089 |

| Corporate Sustainability | Increasing | 0.004 | 0.733 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bernal Salazar, M.F.; Baraibar-Diez, E.; Collado-Agudo, J. CSR and Corporate Sustainability: Theoretical and Empirical Approaches Based on Data Science in Spanish Tourism Companies. Sustainability 2025, 17, 2768. https://doi.org/10.3390/su17062768

Bernal Salazar MF, Baraibar-Diez E, Collado-Agudo J. CSR and Corporate Sustainability: Theoretical and Empirical Approaches Based on Data Science in Spanish Tourism Companies. Sustainability. 2025; 17(6):2768. https://doi.org/10.3390/su17062768

Chicago/Turabian StyleBernal Salazar, Maria Fernanda, Elisa Baraibar-Diez, and Jesús Collado-Agudo. 2025. "CSR and Corporate Sustainability: Theoretical and Empirical Approaches Based on Data Science in Spanish Tourism Companies" Sustainability 17, no. 6: 2768. https://doi.org/10.3390/su17062768

APA StyleBernal Salazar, M. F., Baraibar-Diez, E., & Collado-Agudo, J. (2025). CSR and Corporate Sustainability: Theoretical and Empirical Approaches Based on Data Science in Spanish Tourism Companies. Sustainability, 17(6), 2768. https://doi.org/10.3390/su17062768