Environmental Dependence and Economic Vulnerability in Rural Nepal

Abstract

1. Introduction

2. Materials and Methods

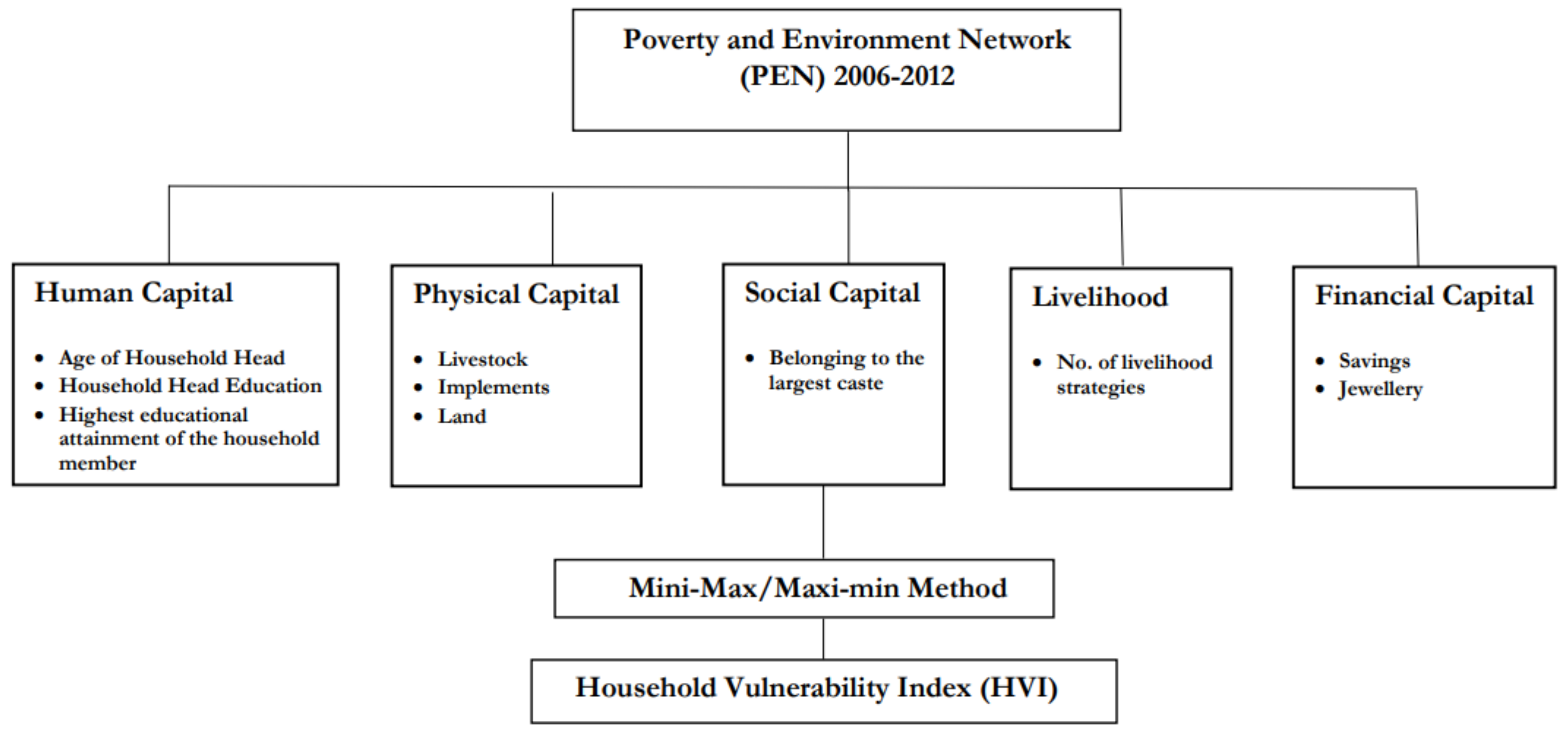

2.1. Household Vulnerability Index

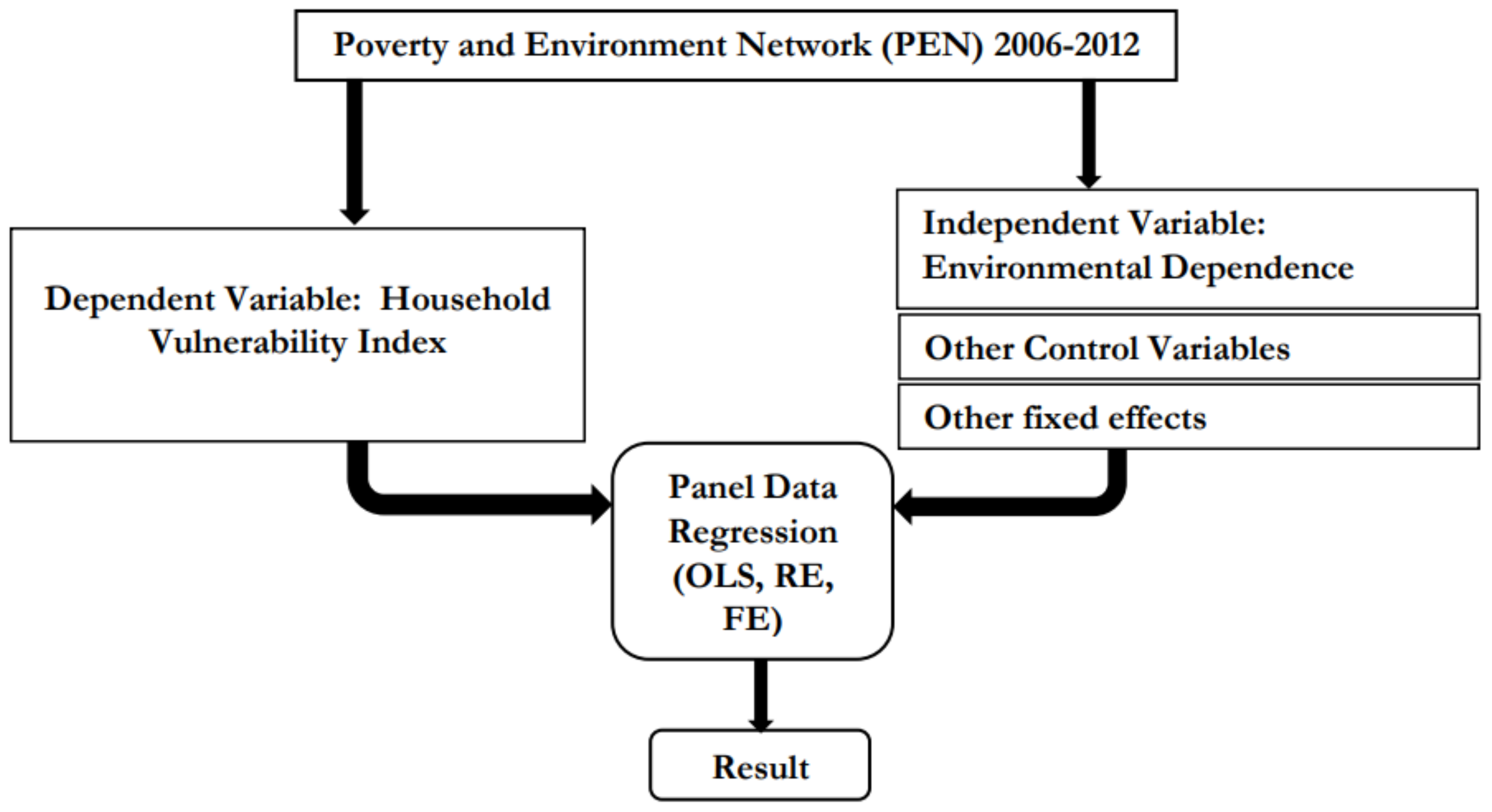

2.2. Household Vulnerability and Environmental Dependence

2.3. Sources of Data and Variables Used

3. Results and Discussion

3.1. Nature of the Household Vulnerability

3.2. Environmental Dependence and Vulnerability

3.3. Discussion

4. Conclusions and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B. Diagnostic Test Results

Appendix B.1. Lagrange Multiplier Test-(Honda) Time Effects Test

Appendix B.2. F Test for Individual Effects

Appendix B.3. Lagrange Multiplier Test-(Breusch-Pagan)

Appendix B.4. Hausman Test

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Model | Time FE Test | BP-LM Test | Hausman Test | |||

|---|---|---|---|---|---|---|

| Normal | p-Value | Chi² | p-Value | Chi² | p-Value | |

| 1 | 16.731 | 2.2 | 11.208 | 0.0008 | 0.9993 | 0.3175 |

| 2 | 16.741 | 2.2 | 11.141 | 0.0008 | 0.9938 | 0.6084 |

| 3 | 16.828 | 2.2 | 7.670 | 0.0056 | 4.4754 | 0.2145 |

| 4 | 16.864 | 2.2 | 0.277 | 0.5989 | 3.8450 | 0.4274 |

| 5 | 17.081 | 2.2 | 1.504 | 0.2201 | 8.4915 | 1.0000 |

| 6 | 14.916 | 2.2 | 1.504 | 0.2201 | 7.8704 | 1.0000 |

| 7 | 14.930 | 2.2 | 1.504 | 0.2201 | 3.2437 | 1.0000 |

| Year | 2006 | 2009 | 2012 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| District | Chitwan | Kaski | Mustang | Chitwan | Kaski | Mustang | Chitwan | Kaski | Mustang |

| Human Capital | |||||||||

| hhh_age | 50.36 (14.15) | 50.14 (14.57) | 52.89 (13.52) | 52.13 (13.75) | 52.00 (13.39) | 54.12 (13.78) | 52.24 (17.20) | 53.52 (13.71) | 55.24 (14.17) |

| hhh_edu | 3.08 (4.06) | 6.29 (4.97) | 3.05 (3.98) | 2.93 (4.06) | 6.07 (5.23) | 2.94 (3.78) | 2.91 (4.33) | 6.91 (5.07) | 2.90 (4.08) |

| max_hh_edu | 8.44 (3.91) | 10.76 (2.90) | 7.64 (3.32) | 9.70 (3.63) | 11.18 (3.94) | 8.04 (3.93) | 9.89 (4.44) | 11.91 (4.03) | 8.22 (3.87) |

| Physical Capital | |||||||||

| implements | 4660.32 (11,275.51) | 14,057.03 (16,860.40) | 10,360.32 (19,629.35) | 10,153.80 (23,970.96) | 30,700.04 (46,128.42) | 15,135.16 (25,508.99) | 22,165.29 (38,089.26) | 48,959.03 (70,582.61) | 21,466.58 (27,566.06) |

| livestock | 18,532.68 (15,428.31) | 26,573.08 (20,411.58) | 80,387.77 (224,589.10) | 43,936.83 (39,679.86) | 35,690.11 (35,760.04) | 56,165.26 (178,639.73) | 38,993.71 (34,330.39) | 34,635.85 (39,306.64) | 34,114.52 (39,335.73) |

| land | 2027.47 (6367.27) | 1187.00 (1013.02) | 2940.39 (2789.36) | 915.91 (765.38) | 1491.41 (2060.26) | 2235.09 (3738.40) | 1041.46 (1136.88) | 1374.96 (2253.95) | 1921.22 (1892.77) |

| Social Capital | |||||||||

| hh_caste | 0.58 (0.50) | 0.89 (0.32) | 0.49 (0.50) | 0.66 (0.48) | 0.98 (0.14) | 0.58 (0.50) | 0.50 (0.50) | 0.86 (0.50) | 0.59 (0.42) |

| Financial Capital | |||||||||

| bank_saving | 879.58 (2661.50) | 9663.83 (26,812.59) | 31,897.65 (79,933.66 ) | 1911.63 (6126.69) | 11,937.72 (31,025.90) | 24,536.06 (59,338.85) | 11,953.55 (31,763.88) | 25,410.64 (66,932.36) | 48,051.24 (104,495.00) |

| jewellery | 0.00 (0.00) | 0.00 (0.00) | 31,662.91 (67,846.57) | 4396.88 (6965.54) | 20,485.87 (16,594.27) | 38,598.35 (79,440.96) | 21,477.20 (23,620.48) | 51,605.95 (48,463.66) | 54,132.35 (112,328.06) |

| Livelihood | |||||||||

| n_livelihoods | 4.81 (0.97) | 4.72 (0.91) | 4.56 (0.93) | 4.93 (1.02) | 4.74 (0.91) | 5.11 (0.84) | 4.60 (0.98) | 4.78 (0.90) | 4.60 (0.98) |

| Household Vulnerability | |||||||||

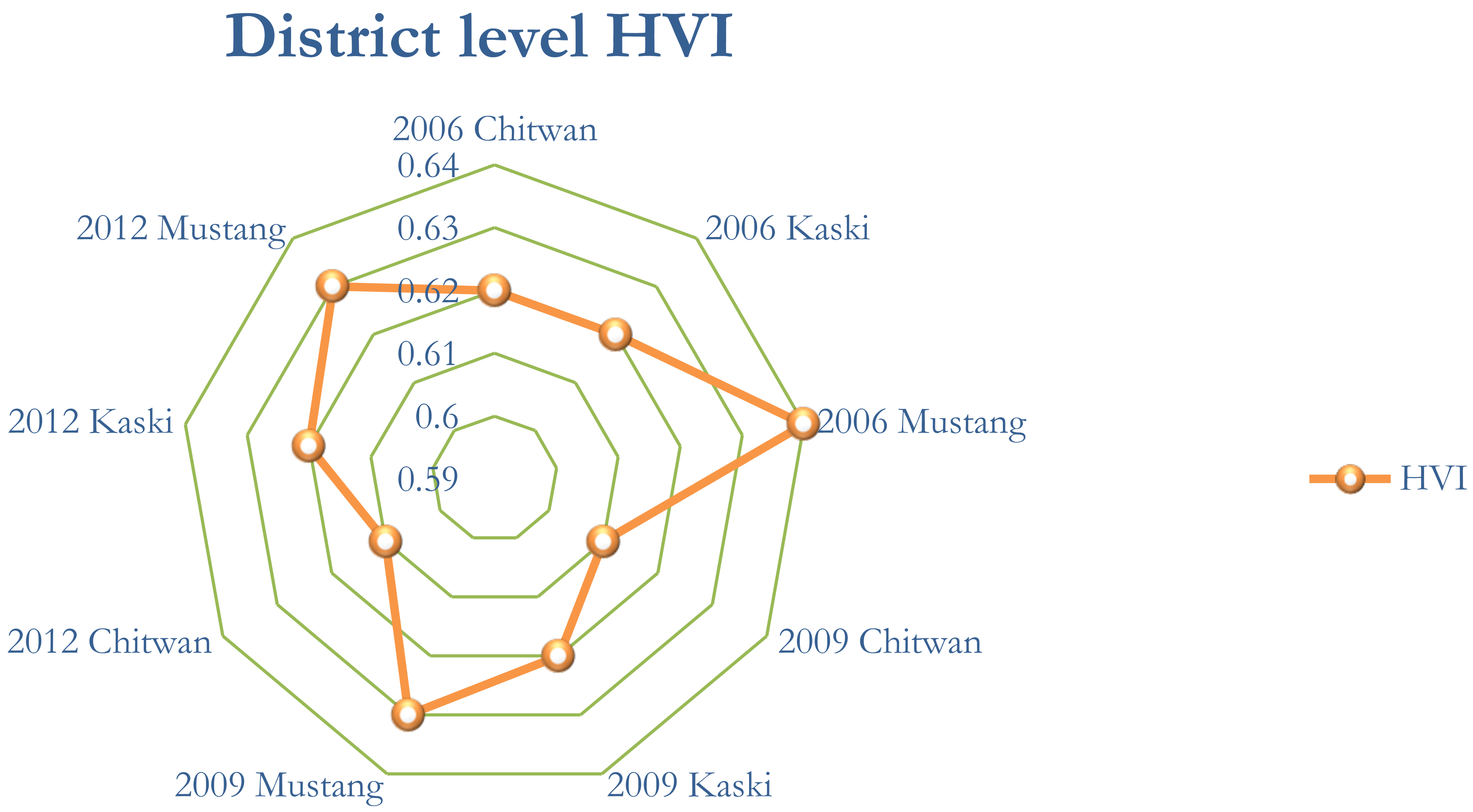

| HVI | 0.61 (0.05) | 0.62 (0.04) | 0.64 (0.05) | 0.61 (0.05) | 0.62 (0.04) | 0.63 (0.05) | 0.61 (0.05) | 0.62 (0.05) | 0.63 (0.05) |

| Year/ District | 2006 | 2009 | 2012 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Chainpur | Hemja | Kunjo | Lete | Chainpur | Hemja | Kunjo | Lete | Chainpur | Hemja | Kunjo | Lete | |

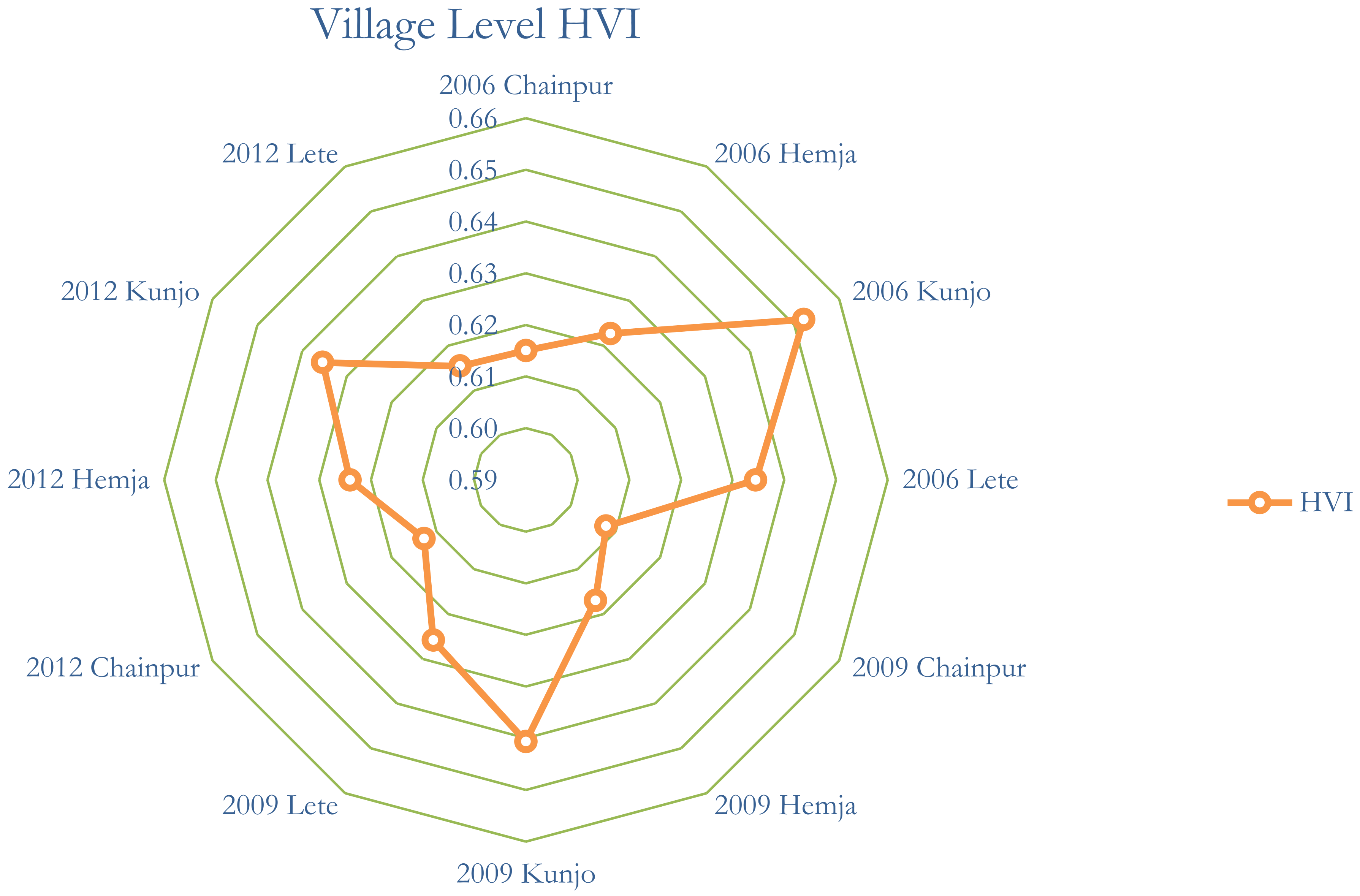

| HVI | 0.62 (0.05) | 0.62 (0.04) | 0.65 (0.04) | 0.63 (0.05) | 0.61 (0.05) | 0.62 (0.04) | 0.64 (0.04) | 0.63 (0.05) | 0.61 (0.05) | 0.62 (0.05) | 0.64 (0.05) | 0.62 (0.05) |

| Dependent Variable: Household Vulnerability | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Env. Dependence | 0.108 *** | 0.141 *** | 0.141 *** | 0.141 *** |

| (0.013) | (0.014) | (0.014) | (0.014) | |

| Dependency ratio | 0.009 *** | 0.009 *** | 0.009 *** | |

| (0.003) | (0.003) | (0.003) | ||

| Shock | 0.0002 | 0.0002 | 0.0002 | |

| (0.004) | (0.004) | (0.004) | ||

| Debt | −0.004 ** | −0.004 ** | −0.004 ** | |

| (0.002) | (0.002) | (0.002) | ||

| Constant | 0.683 *** | 0.694 *** | 0.694 *** | |

| (0.007) | (0.008) | (0.008) | ||

| Year-fixed effects | No | Yes | Yes | Yes |

| District-fixed effects | No | Yes | Yes | Yes |

| VDC-fixed effects | Yes | Yes | Yes | Yes |

| Observations | 1245 | 1245 | 1245 | 1245 |

| 0.049 | 0.183 | 0.183 | 0.174 | |

| Adjusted | 0.048 | 0.177 | 0.177 | 0.168 |

| Dependent Variable: Household Vulnerability | |||||||

|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| Env. Dependence | 0.106 *** | 0.104 *** | 0.103 *** | 0.128 *** | 0.131 *** | 0.131 *** | 0.140 *** |

| (0.014) | (0.014) | (0.014) | (0.014) | (0.014) | (0.014) | (0.014) | |

| Dependency ratio | 0.009 *** | 0.009 *** | 0.008 ** | 0.008 ** | 0.008 ** | 0.009 *** | |

| (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | ||

| Shock | 0.005 | 0.005 | 0.005 | 0.005 | 0.0002 | ||

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |||

| Debt | −0.006 *** | −0.004 * | −0.004 * | −0.004 ** | |||

| (0.001) | (0.002) | (0.002) | (0.002) | ||||

| Year-fixed effects | No | No | No | No | Yes | Yes | Yes |

| District-fixed effects | No | No | No | No | No | Yes | Yes |

| VDC-fixed effects | No | No | No | No | No | No | Yes |

| Observations | 1245 | 1245 | 1245 | 1245 | 1245 | 1245 | 1245 |

| 0.047 | 0.053 | 0.054 | 0.075 | 0.076 | 0.076 | 0.174 | |

| Adjusted | 0.044 | 0.050 | 0.050 | 0.071 | 0.071 | 0.071 | 0.168 |

| Variable | Description | Expected Sign (+/−) |

|---|---|---|

| HH head’s educational attainment | HH head’s educational attainment enhances access to information, improves decision-making, and increases income opportunities, enabling better risk management and resilience, thereby reducing household vulnerability [27,29,60,61]. | Higher educational level (−) |

| Highest educational attainment by an HH member | Family members with higher education levels contribute to increased HH income, improved access to resources and better adaptive capacity, thereby reducing overall household vulnerability [28,29,37]. | Maximum (−) |

| Implements Value | The total value of implements (Cars, Trucks, Motorbike, Plough, etc.) reflects household assets that enhance mobility, productivity, and income opportunities, reducing vulnerability by improving resilience and market access [27,61]. | Higher Value (−) |

| Livestock Value | Total value of livestock (all types) in Rs. serves as a key household asset, providing income, food security, and a financial safety net, thereby reducing vulnerability and enhancing resilience [28,60]. | Higher Value (−) |

| Land area | The total area of land owned by the household (sq. m) represents a crucial asset that supports livelihood, food security, and income generation, enhancing economic stability and reducing vulnerability [28,61]. | Greater land area (−) |

| HH Caste | Households belonging to the largest caste in the village (=1) indicate social positioning and access to community resources, networks, and opportunities, potentially reducing vulnerability through social capital and support systems [28,62]. | Largest caste (−) |

| Bank saving | Household savings in banks or recognized financial institutions enhance financial security, facilitate access to credit, and improve resilience to economic shocks, reducing household vulnerability [63]. | Greater saving (−) |

| Jewellery | Household savings in the form of non-productive assets serve as a financial reserve, providing liquidity during emergencies, but with limited income-generating potential compared to productive assets [64]. | Greater value (−) |

| Livelihood | The count of livelihoods of the household represents the household’s economic diversification. A higher number of income sources enhances financial stability, reduces dependency on a single sector, and improves resilience to economic shocks, thereby lowering vulnerability [28,37]. | Diversified (−) |

| Variable | Description | Expected Sign (+/−) |

|---|---|---|

| Environmental Dependence | The ratio of Environmental Income to Total Income of the Household Reflects a household’s reliance on natural resources for livelihood. Higher environmental dependence is expected to increase household vulnerability, as it indicates greater exposure to environmental risks, resource depletion, and economic instability, making households more susceptible to shocks [8,65]. | Greater dependence (+) |

| Dependency Ratio | Ratio of Dependent to Working Adult Members of the Household Represents the economic burden on working members. A higher dependency ratio increases household vulnerability by straining resources, limiting savings, and reducing the household’s ability to cope with financial shocks [29,34,66,67]. | Higher ratio (−) |

| Debt | Total Household Debt (Rs.) Indicates financial obligations that may constrain household resources. Higher debt levels increase vulnerability by reducing disposable income, limiting investment in productive assets, and heightening financial stress during economic shocks [68]. | Higher value of debt (−) |

| Shock | Indicates whether the household has faced adverse events. Experiencing shocks increases vulnerability by disrupting income, depleting assets, and weakening the household’s ability to recover and build resilience [61,69,70]. | Experienced shock (+) |

References

- Jaszczak, A.; Kristianova, K.; Vaznonienė, G.; Žukovskis, J. Phenomenon of abandoned villages and its impact on transformation of rural landscapes. Manag. Theory Stud. Rural. Bus. Infrastruct. Dev. 2018, 40, 467–480. [Google Scholar] [CrossRef]

- World Bank. Rural Population (% of Total Population). 2021. Available online: https://data.worldbank.org/indicator/SP.RUR.TOTL.ZS (accessed on 4 February 2025).

- United Nations. World Urbanization Prospects 2018. 2018. Available online: https://population.un.org/wup (accessed on 4 February 2025).

- Acharya, B.R. Dimension of rural development in Nepal. Dhaulagiri J. Sociol. Anthropol. 2008, 2, 181–192. [Google Scholar] [CrossRef]

- FAO; IFAD; UNICEF; WFP; WHO. The State of Food Security and Nutrition in the World 2021: Transforming Food Systems for Food Security, Improved Nutrition and Affordable Healthy Diets for All; FAO: Rome, Italy, 2021. [Google Scholar]

- Gemenne, F. The Impacts of Migration for Adaptation and Vulnerability. 2022. Available online: https://www.delmi.se/media/l4acp0cq/delmi-research-overview-2022_2-webb.pdf (accessed on 4 February 2025).

- Pelser, A.J.; Chimukuche, R.S. Climate Change, Rural Livelihoods, and Human Well-Being: Experiences from Kenya. In Vegetation Dynamics, Changing Ecosystems and Human Responsibility; IntechOpen: London, UK, 2022. [Google Scholar] [CrossRef]

- Angelsen, A.; Jagger, P.; Babigumira, R.; Belcher, B.; Hogarth, N.J.; Bauch, S.; Börner, J.; Smith-Hall, C.; Wunder, S. Environmental income and rural livelihoods: A global-comparative analysis. World Dev. 2014, 64, S12–S28. [Google Scholar] [CrossRef]

- United Nations. Rural Population Left Behind by Uneven Global Economy. 2019. Available online: https://press.un.org/en/2019/gaef3521.doc.htm (accessed on 4 February 2025).

- Lazarte-Hoyle, A. Understanding the Drivers of Rural Vulnerability Towards Building Resilience, Promoting Socio-Economic Empowerment and Enhancing the Socio-Economic Inclusion of Vulnerable, Disadvantaged and Marginalized Populations for an Effective Promotion of Decent Work in Rural Economies; International Labour Organization: Geneva, Switzerland, 2017. [Google Scholar]

- McNamara, K.E.; Olson, L.L.; Rahman, M.A. Insecure hope: The challenges faced by urban slum dwellers in Bhola Slum, Bangladesh. Migr. Dev. 2016, 5, 1–15. [Google Scholar] [CrossRef]

- Tacoli, C.; Mcgranahan, G. Urbanisation, Rural-Urban Migration and Urban Poverty; Human Settlements Group, International Institute for Environment and Development: London, UK, 2015. [Google Scholar]

- Artuso, M. State of the World’s Cities 2010/11–Bridging the Urban Divide, by UN Habitat; Earthscan: London, UK, 2011; ISBN 978-1-84971-176-0. [Google Scholar]

- Nawrotzki, R.; Hunter, L.; Dickinson, T.W. Natural resources and rural livelihoods: Differences between migrants and non-migrants in Madagascar. Demogr. Res. 2012, 26, 661–700. [Google Scholar] [CrossRef]

- Angelsen, A.; Wunder, S. Exploring the forest-poverty link. CIFOR Occas. Pap. 2003, 40, 1–20. [Google Scholar]

- Emeru, G.M.; Fikire, A.H.; Beza, Z.B. Determinants of urban households’ livelihood diversification strategies in North Shewa Zone, Ethiopia. Cogent Econ. Financ. 2022, 10, 2093431. [Google Scholar] [CrossRef]

- Amevenku, F.; Asravor, R.; Kuwornu, J.K. Determinants of livelihood strategies of fishing households in the volta Basin, Ghana. Cogent Econ. Financ. 2019, 7, 1595291. [Google Scholar] [CrossRef]

- Chambers, R.; Conway, G. Sustainable Rural Livelihoods: Practical Concepts for the 21st Century; Institute of Development Studies: Falmer, UK, 1992. [Google Scholar]

- DfID. Sustainable Livelihoods Guidance Sheets; DFID: London, UK, 1999; Volume 445, p. 710. [Google Scholar]

- Ellis, F. Rural Livelihood Diversity in Developing Countries: Evidence and Policy Implications. In Natural Resource Perspectives; Overseas Development Institute: London, UK, 1999; Volume 40, pp. 1–10. [Google Scholar]

- Scoones, I. Livelihoods perspectives and rural development. In Critical Perspectives in Rural Development Studies; Routledge: London, UK, 2013; pp. 159–184. [Google Scholar]

- Chambers, R. Editorial introduction: Vulnerability, coping and policy. IDS Bull. 1989, 20, 1–7. [Google Scholar] [CrossRef]

- Calvo, C.; Dercon, S. Measuring Individual Vulnerability; University of Oxford: Oxford, UK, 2005. [Google Scholar]

- Chambers, R. Vulnerability, coping and policy (editorial introduction). IDS Bull. 2006, 37, 33–40. [Google Scholar] [CrossRef]

- Fang, Y.p.; Zhao, C.; Rasul, G.; Wahid, S.M. Rural household vulnerability and strategies for improvement: An empirical analysis based on time series. Habitat Int. 2016, 53, 254–264. [Google Scholar] [CrossRef]

- Gaisie, E.; Han, S.S.; Kim, H.M. Complexity of resilience capacities: Household capitals and resilience outcomes on the disaster cycle in informal settlements. Int. J. Disaster Risk Reduct. 2021, 60, 102292. [Google Scholar] [CrossRef]

- Zhang, H.; Zhao, Y.; Pedersen, J. Capital assets framework for analysing household vulnerability during disaster. Disasters 2020, 44, 687–707. [Google Scholar] [CrossRef]

- Antwi-Agyei, P.; Dougill, A.J.; Fraser, E.D.; Stringer, L.C. Characterising the nature of household vulnerability to climate variability: Empirical evidence from two regions of Ghana. Environ. Dev. Sustain. 2013, 15, 903–926. [Google Scholar] [CrossRef]

- Rahman, M.M.; Arif, M.S.I.; Hossain, M.T.; Almohamad, H.; Al Dughairi, A.A.; Al-Mutiry, M.; Abdo, H.G. Households’ vulnerability assessment: Empirical evidence from cyclone-prone area of Bangladesh. Geosci. Lett. 2023, 10, 26. [Google Scholar] [CrossRef]

- Notenbaert, A.; Karanja, S.N.; Herrero, M.; Felisberto, M.; Moyo, S. Derivation of a household-level vulnerability index for empirically testing measures of adaptive capacity and vulnerability. Reg. Environ. Chang. 2013, 13, 459–470. [Google Scholar] [CrossRef]

- Aksha, S.K.; Juran, L.; Resler, L.M.; Zhang, Y. An analysis of social vulnerability to natural hazards in Nepal using a modified social vulnerability index. Int. J. Disaster Risk Sci. 2019, 10, 103–116. [Google Scholar] [CrossRef]

- Shahi, P.R.; Shreezal, G. Estimating Households’ Vulnerability to Poverty. Econ. J. Nepal 2020, 43, 17–35. [Google Scholar]

- Bista, R.B. Grasping Climate Vulnerability in Western Mountainous Nepal: Applying Climate Vulnerability Index. Proc. Forum Soc. Econ. 2019, 50, 553–568. [Google Scholar] [CrossRef]

- Gerlitz, J.Y.; Macchi, M.; Brooks, N.; Pandey, R.; Banerjee, S.; Jha, S.K. The multidimensional livelihood vulnerability index–an instrument to measure livelihood vulnerability to change in the Hindu Kush Himalayas. Clim. Dev. 2017, 9, 124–140. [Google Scholar] [CrossRef]

- UNDP. Human development report 2007/8. Fighting climate change: Human solidarity in a divided world. In Fighting Climate Change: Human Solidarity in a Divided World (November 27, 2007); UNDP-HDRO Human Development Report; UNDP: New York, NY, USA, 2007. [Google Scholar]

- Karunarathne, A.Y.; Lee, G. Developing a multi-facet social vulnerability measure for flood disasters at the micro-level assessment. Int. J. Disaster Risk Reduct. 2020, 49, 101679. [Google Scholar] [CrossRef]

- Huynh, L.T.M.; Stringer, L.C. Multi-scale assessment of social vulnerability to climate change: An empirical study in coastal Vietnam. Clim. Risk Manag. 2018, 20, 165–180. [Google Scholar] [CrossRef]

- Dumenu, W.K.; Takam Tiamgne, X. Social vulnerability of smallholder farmers to climate change in Zambia: The applicability of social vulnerability index. SN Appl. Sci. 2020, 2, 1–16. [Google Scholar] [CrossRef]

- Walelign, S.Z.; Smith-Hall, C.; Rayamajhi, S.; Chhetri, B.B. A unique environmental augmented household-level livelihood panel dataset from Nepal. Data Brief 2022, 42, 108168. [Google Scholar] [CrossRef]

- Larsen, H.O.; Rayamajhi, S.; Chhetri, B.B.K.; Charlery, L.C.; Gautam, N.; Khadka, N.; Puri, L.; Rutt, R.L.; Shivakoti, T.; Thorsen, R.S. The role of environmental incomes in rural Nepalese livelihoods 2005–2012: Contextual information. IFRO Doc. 2014, 4. [Google Scholar]

- Honda, Y. A size correction to the Lagrange multiplier test for heteroskedasticity. J. Econom. 1988, 38, 375–386. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. The Lagrange multiplier test and its applications to model specification in econometrics. Rev. Econ. Stud. 1980, 47, 239–253. [Google Scholar] [CrossRef]

- Meador, J.E.; Skerratt, S. On a unified theory of development: New institutional economics & the charismatic leader. J. Rural Stud. 2017, 53, 144–155. [Google Scholar] [CrossRef]

- Haggblade, S.; Hazell, P.; Reardon, T. The Rural Non-farm Economy: Prospects for Growth and Poverty Reduction. World Dev. 2010, 38, 1429–1441. [Google Scholar] [CrossRef]

- Joshi, S.; Timsina, J.; Shrestha, R. Agricultural productivity and its impact on rural livelihoods in Nepal’s Tarai region. Agric. Syst. 2013, 125, 52–63. [Google Scholar] [CrossRef]

- Shrestha, S.; Ghimire, B.; Thapa, G. Vulnerability and coping strategies in remote mountain areas: Evidence from rural Nepal. Environ. Dev. 2017, 24, 14–23. [Google Scholar] [CrossRef]

- Adger, W.N. Vulnerability. Glob. Environ. Change 2006, 16, 268–281. [Google Scholar] [CrossRef]

- Turner, B.L.; Kasperson, R.E.; Matson, P.A.; McCarthy, J.J.; Corell, R.W.; Christensen, L.; Eckley, N.; Kasperson, J.X.; Luers, A.; Martello, M.L.; et al. A framework for vulnerability analysis in sustainability science. Proc. Natl. Acad. Sci. USA 2003, 100, 8074–8079. [Google Scholar] [CrossRef]

- Berkes, F.; Ross, H. Community resilience: Toward an integrated approach. Soc. Nat. Resour. 2013, 26, 5–20. [Google Scholar] [CrossRef]

- Paudel, N.S.; Ojha, H.; Kanel, K. Community Forestry in Nepal: A Platform for Public Deliberation or Technocratic Hegemony? Int. For. Rev. 2008, 10, 303–311. [Google Scholar]

- Barbier, E.B. Poverty, Development, and Environment. Environ. Dev. Econ. 2010, 15, 635–660. [Google Scholar] [CrossRef]

- Carter, M.R.; Barrett, C.B. The Economics of Poverty Traps and Persistent Poverty: An Asset-Based Approach. J. Dev. Stud. 2006, 42, 178–199. [Google Scholar] [CrossRef]

- Dercon, S. Income Risk, Coping Strategies, and Safety Nets. World Bank Res. Obs. 2002, 17, 141–166. [Google Scholar] [CrossRef]

- Antriyandarti, E.; Barokah, U.; Rahayu, W.; Herdiansyah, H.; Ihsannudin, I.; Nugraha, F.A. The Economic Security of Households Affected by the COVID-19 Pandemic in Rural Java and Madura. Sustainability 2024, 16, 2091. [Google Scholar] [CrossRef]

- Dasgupta, P.; Shaw, R.; Sahu, S. Climate Change and Household Debt in Rural India. Environ. Econ. Policy Stud. 2022, 24, 1–22. [Google Scholar]

- Pillai, V.; Nayar, K.R. Dependency ratios and welfare loss: Effects of caregiving on mental health in low-income households. Health Econ. 2022, 31, 749–763. [Google Scholar] [CrossRef]

- Chandran, S.; Chatterjee, S. Economic dependency ratio as a dimension of poverty and vulnerability. Int. J. Soc. Econ. 2021, 48, 1677–1694. [Google Scholar]

- Walker, T.; Kawasoe, Y.; Shrestha, J. Risk and Vulnerability in Nepal: Findings from the Household Risk and Vulnerability Survey; World Bank: Washington, DC, USA, 2019. [Google Scholar]

- Bhandari, S.; Shrestha, S. Food Insecurity and Compound Environmental Shocks in Nepal. Int. J. Environ. Res. Public Health 2020, 17, 9243. [Google Scholar] [CrossRef]

- Wang, M.; Li, M.; Jin, B.; Yao, L.; Ji, H. Does livelihood capital influence the livelihood strategy of herdsmen? Evidence from western China. Land 2021, 10, 763. [Google Scholar] [CrossRef]

- Nguyen, T.T.; Do, T.L.; Bühler, D.; Hartje, R.; Grote, U. Rural livelihoods and environmental resource dependence in Cambodia. Ecol. Econ. 2015, 120, 282–295. [Google Scholar] [CrossRef]

- Alha, A. The other side of caste as social capital. Soc. Change 2018, 48, 575–588. [Google Scholar] [CrossRef]

- Newman, C.; Tarp, F.; Van Den Broeck, K. Social Capital, Network Effects, and Savings in Rural V ietnam. Rev. Income Wealth 2014, 60, 79–99. [Google Scholar] [CrossRef]

- Noerhidajati, S.; Purwoko, A.B.; Werdaningtyas, H.; Kamil, A.I.; Dartanto, T. Household financial vulnerability in Indonesia: Measurement and determinants. Econ. Model. 2021, 96, 433–444. [Google Scholar] [CrossRef]

- Charlery, L.; Walelign, S.Z. Assessing environmental dependence using asset and income measures: Evidence from Nepal. Ecol. Econ. 2015, 118, 40–48. [Google Scholar] [CrossRef]

- Pathak, S.; Panta, H.K.; Bhandari, T.; Paudel, K.P. Flood vulnerability and its influencing factors. Nat. Hazards 2020, 104, 2175–2196. [Google Scholar] [CrossRef]

- Sam, A.S.; Kumar, R.; Kächele, H.; Müller, K. Quantifying household vulnerability triggered by drought: Evidence from rural India. Clim. Dev. 2017, 9, 618–633. [Google Scholar] [CrossRef]

- Ramprasad, V. Debt and vulnerability: Indebtedness, institutions and smallholder agriculture in South India. J. Peasant Stud. 2019, 46, 1286–1307. [Google Scholar] [CrossRef]

- Barua, S.; Banerjee, A. Impact of Climatic Shocks on Household Well-being: Evidence from Rural Bangladesh. Asia-Pac. J. Rural Dev. 2020, 30, 89–112. [Google Scholar] [CrossRef]

- Gautam, N.P.; Raut, N.K.; Chhetri, B.B.K.; Raut, N.; Rashid, M.H.U.; Ma, X.; Wu, P. Determinants of poverty, self-reported shocks, and coping strategies: Evidence from rural Nepal. Sustainability 2021, 13, 1790. [Google Scholar] [CrossRef]

| Variables | Construct |

|---|---|

| HHH_age | Household head age in years |

| HHH_edu | Education attainment of household head |

| Max_hh_edu | Highest educational attainment by a household member |

| Durables | Total monetary value of durables goods such as: Car; Trucks; Motorbike; Plough etc. owned by the household (in NRs.) |

| Livestock | Total value of livestock (of all types) in Rs. |

| Land | Total area of land owned by the household in sq. m |

| HH_caste | Household belonging to the biggest caste in the village (=1) |

| Bank_saving | Households savings kept in banks or other recognized financial institutions |

| Jewellery | Households’ saving in the form of non-productive assets, such as Jewellery. |

| N_livelihoods | Count of livelihoods of the households |

| Variables | Construct |

|---|---|

| env_dependence | This environmental dependence variable is considered one of the key factors contributing to household vulnerability. It is measured as the ratio of environmental income to the total income of each household. |

| dependency_ratio | The ratio of total dependent family members to working adult members in the household is calculated. The dependent group includes children under 15 years and senior citizens over 60 years. |

| debt | The amount of outstanding debt of a household, measured in rupees. |

| shock | The survey asks about various shocks experienced by the household, including crop failure, illness, the loss of an adult family member, land dispossession, livestock depletion, loss of other assets, unemployment, and expenses from significant social events. This is a binary indicator, where 1 represents a household experiencing shocks and 0 otherwise. |

| Year/ District | 2006 | 2009 | 2012 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Chitwan | Kaski | Mustang | Chitwan | Kaski | Mustang | Chitwan | Kaski | Mustang | |

| HVI | 0.62 (0.05) | 0.62 (0.04) | 0.64 (0.05) | 0.61 (0.05) | 0.62 (0.04) | 0.63 (0.05) | 0.61 (0.05) | 0.62 (0.05) | 0.63 (0.05) |

| Year | 2006 | |||

|---|---|---|---|---|

| District | Chitwan | Kaski | Mustang | Mustang |

| VDC | Chainpur | Hemja | Kunjo | Lete |

| HVI | 0.62 (0.05) | 0.62 (0.04) | 0.64 (0.05) | 0.64 (0.05) |

| env_dependence | 0.13 (0.19) | 0.16 (0.20) | 0.40 (0.23) | 0.29 (0.23) |

| dependency_ratio | 0.66 (0.62) | 0.73 (0.76) | 0.88 (0.85) | 0.69 (0.63) |

| debt | 12,234.42 (19,246.56) | 25,896.24 (47,371.72) | 17,792.57 (19,055.29) | 31,217.37 (69,576.58) |

| shock | 1.75 (1.66) | 0.55 (1.07) | 2.48 (1.24) | 1.97 (1.2) |

| Year | 2009 | |||

| HVI | 0.61 (0.05) | 0.62 (0.04) | 0.64 (0.04) | 0.63 (0.05) |

| env_dependence | 0.14 (0.23) | 0.13 (0.15) | 0.19 (0.30) | 0.21 (0.59) |

| dependency_ratio | 0.58 (0.56) | 0.63 (0.63) | 0.77 (0.64) | 0.68 (0.69) |

| debt | 18,249.69 (36,642.37) | 46,654.49 (72,705.08) | 14,887.21 (16,156.9) | 20,616.94 (41,324.71) |

| shock | 0.24 (0.65) | 0.59 (0.96) | 0.65 (1.00) | 1.16 (1.14) |

| Year | 2012 | |||

| HVI | 0.61 (0.05) | 0.62 (0.05) | 0.64 (0.05) | 0.62 (0.05) |

| env_dependence | 0.15 (0.20) | 0.14 (0.25) | 0.78 (3.16) | 0.27 (0.25) |

| dependency_ratio | 0.51 (0.60) | 0.53 (0.57) | 0.77 (0.82) | 0.49 (0.56) |

| debt | 37,221.48 (87,094.30) | 64,572.68 (133,587.15) | 24,507.84 (33,242.18) | 19,864.55 (27,238.68) |

| shock | 0.77 (1.01) | 0.31 (0.66) | 0.35 (0.72) | 0.24 (0.59) |

| Dependent Variable: Household Vulnerability | |||||||

|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| Env. Dependence | 0.108 *** | 0.106 *** | 0.104 *** | 0.129 *** | 0.132 *** | 0.131 *** | 0.141 *** |

| (0.013) | (0.013) | (0.013) | (0.014) | (0.014) | (0.014) | (0.014) | |

| Dependency ratio | 0.010 *** | 0.010 *** | 0.008 *** | 0.009 *** | 0.008 ** | 0.009 *** | |

| (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | ||

| Shock | 0.009 ** | 0.009 ** | 0.009 ** | 0.005 | 0.0002 | ||

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |||

| Debt | −0.006 *** | −0.004 * | −0.004 * | −0.004 ** | |||

| (0.001) | (0.002) | (0.002) | (0.002) | ||||

| Constant | 0.683 *** | 0.678 *** | 0.675 *** | 0.667 *** | 0.665 *** | 0.675 *** | 0.694 *** |

| (0.007) | (0.007) | (0.007) | (0.007) | (0.008) | (0.009) | (0.008) | |

| Year-fixed effects | No | No | No | No | Yes | Yes | Yes |

| District-fixed effects | No | No | No | No | No | Yes | Yes |

| VDC-fixed effects | No | No | No | No | No | No | Yes |

| Observations | 1245 | 1245 | 1245 | 1245 | 1245 | 1245 | 1245 |

| 0.049 | 0.057 | 0.060 | 0.080 | 0.081 | 0.086 | 0.183 | |

| Adjusted | 0.048 | 0.055 | 0.058 | 0.077 | 0.077 | 0.081 | 0.177 |

| Dependent Variable: Household Vulnerability | |||||||

|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| Env. Dependence | 0.106 *** | 0.104 *** | 0.103 *** | 0.128 *** | 0.132 *** | 0.131 *** | 0.141 *** |

| (0.014) | (0.013) | (0.014) | (0.014) | (0.014) | (0.014) | (0.014) | |

| Dependency ratio | 0.009 *** | 0.009 *** | 0.008 *** | 0.008 *** | 0.008 ** | 0.009 *** | |

| (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | ||

| Shock | 0.006 | 0.006 | 0.006 | 0.005 | 0.0002 | ||

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |||

| Debt | −0.006 *** | −0.004 * | −0.004 * | −0.004 ** | |||

| (0.001) | (0.002) | (0.002) | (0.002) | ||||

| Constant | 0.684 *** | 0.679 *** | 0.677 *** | 0.669 *** | 0.666 *** | 0.675 *** | 0.694 *** |

| (0.008) | (0.008) | (0.008) | (0.008) | (0.008) | (0.009) | (0.008) | |

| Year-fixed effects | No | No | No | No | Yes | Yes | Yes |

| District-fixed effects | No | No | No | No | No | Yes | Yes |

| VDC-fixed effects | No | No | No | No | No | No | Yes |

| Observations | 1245 | 1245 | 1245 | 1245 | 1245 | 1245 | 1245 |

| 0.047 | 0.054 | 0.056 | 0.076 | 0.077 | 0.086 | 0.183 | |

| Adjusted | 0.046 | 0.052 | 0.053 | 0.073 | 0.073 | 0.081 | 0.177 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Thapa-Parajuli, R.; Nhemhafuki, S.; Khadka, B.; Pradhananga, R. Environmental Dependence and Economic Vulnerability in Rural Nepal. Sustainability 2025, 17, 2434. https://doi.org/10.3390/su17062434

Thapa-Parajuli R, Nhemhafuki S, Khadka B, Pradhananga R. Environmental Dependence and Economic Vulnerability in Rural Nepal. Sustainability. 2025; 17(6):2434. https://doi.org/10.3390/su17062434

Chicago/Turabian StyleThapa-Parajuli, Resham, Sanjeev Nhemhafuki, Bipin Khadka, and Roja Pradhananga. 2025. "Environmental Dependence and Economic Vulnerability in Rural Nepal" Sustainability 17, no. 6: 2434. https://doi.org/10.3390/su17062434

APA StyleThapa-Parajuli, R., Nhemhafuki, S., Khadka, B., & Pradhananga, R. (2025). Environmental Dependence and Economic Vulnerability in Rural Nepal. Sustainability, 17(6), 2434. https://doi.org/10.3390/su17062434