Examining the Interplay between CEPSA’s ESG Performance and Financial Performance: An Overview of the Energy Sector Transformation

Abstract

1. Introduction

2. Literature Review

2.1. Related Research on the ESG Performance Evaluation

2.2. The Relationship between ESG Performance and Financial Performance

2.3. Transforming the Energy Sector for Sustainable Development

2.4. Research Gap

3. Methods

3.1. Legitimacy Theory

3.2. Data Source and Analysis

4. Results and Discussion

4.1. Environmental Performance

4.1.1. Air Pollution and GHG Emission

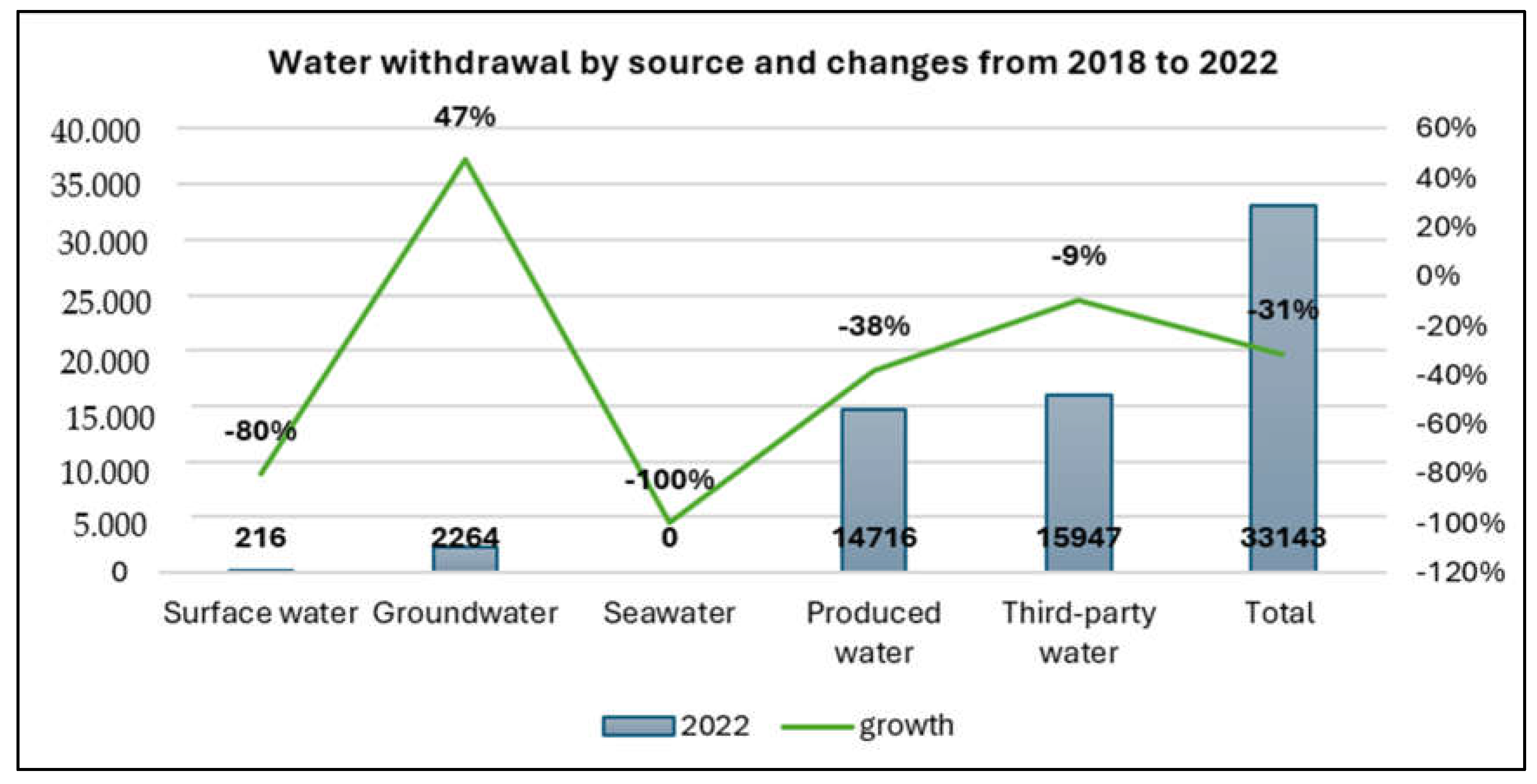

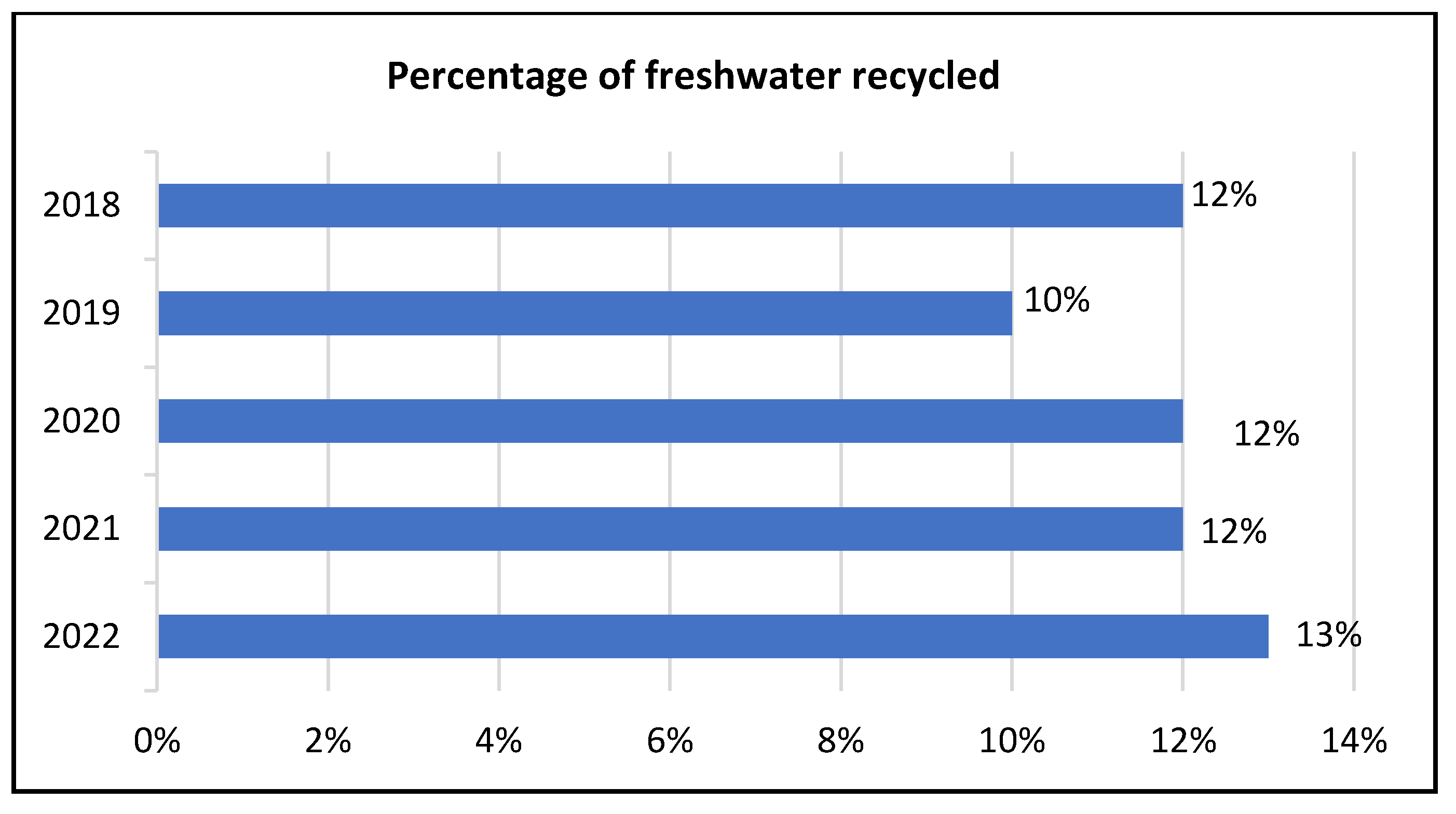

4.1.2. Water Management

4.1.3. Other Renewable Energy Management

4.1.4. Biodiversity Policy and Ecosystem Protection

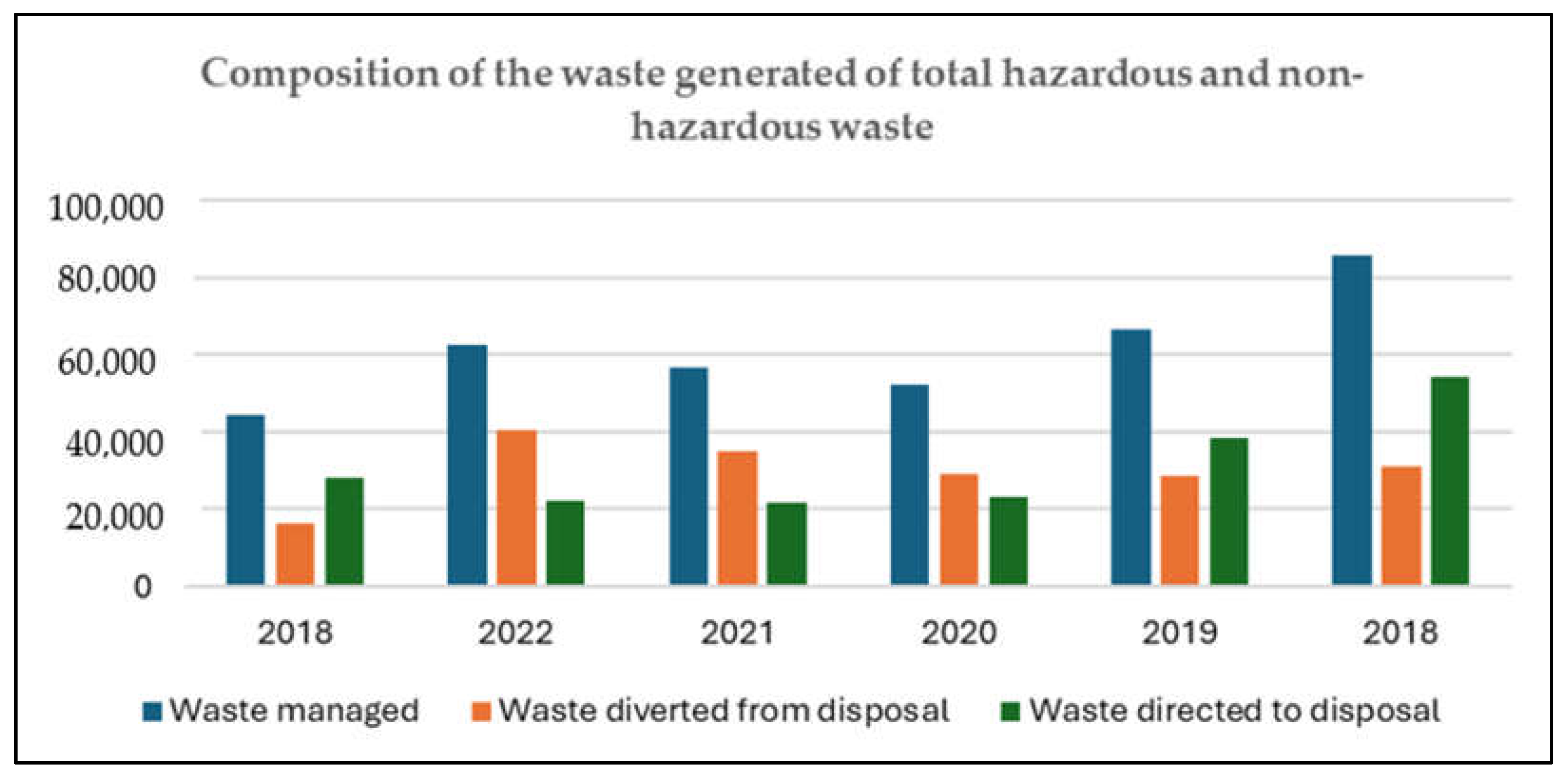

4.1.5. Waste Management

4.2. Social Performance

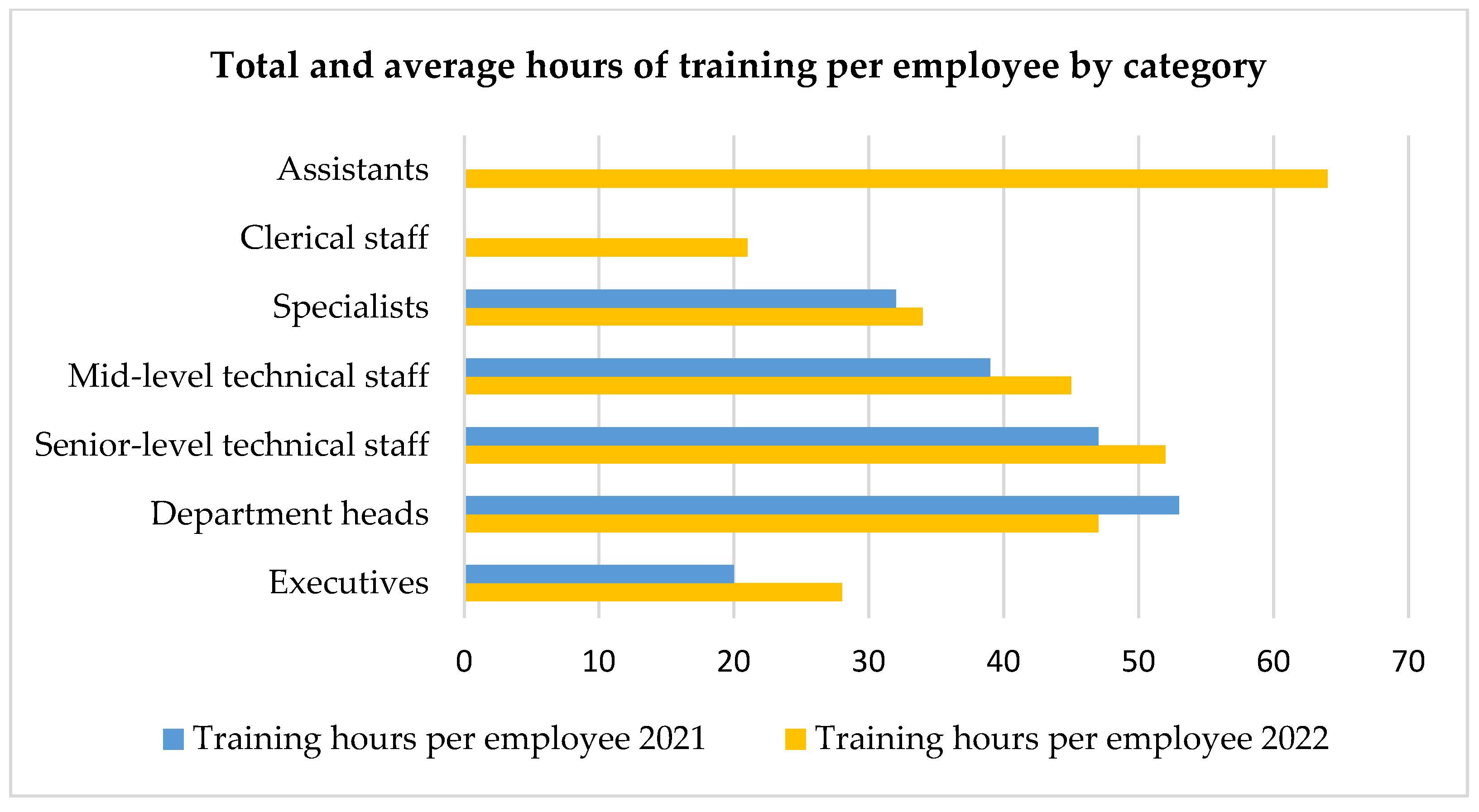

4.2.1. Employee Management in Diversity and Inclusion

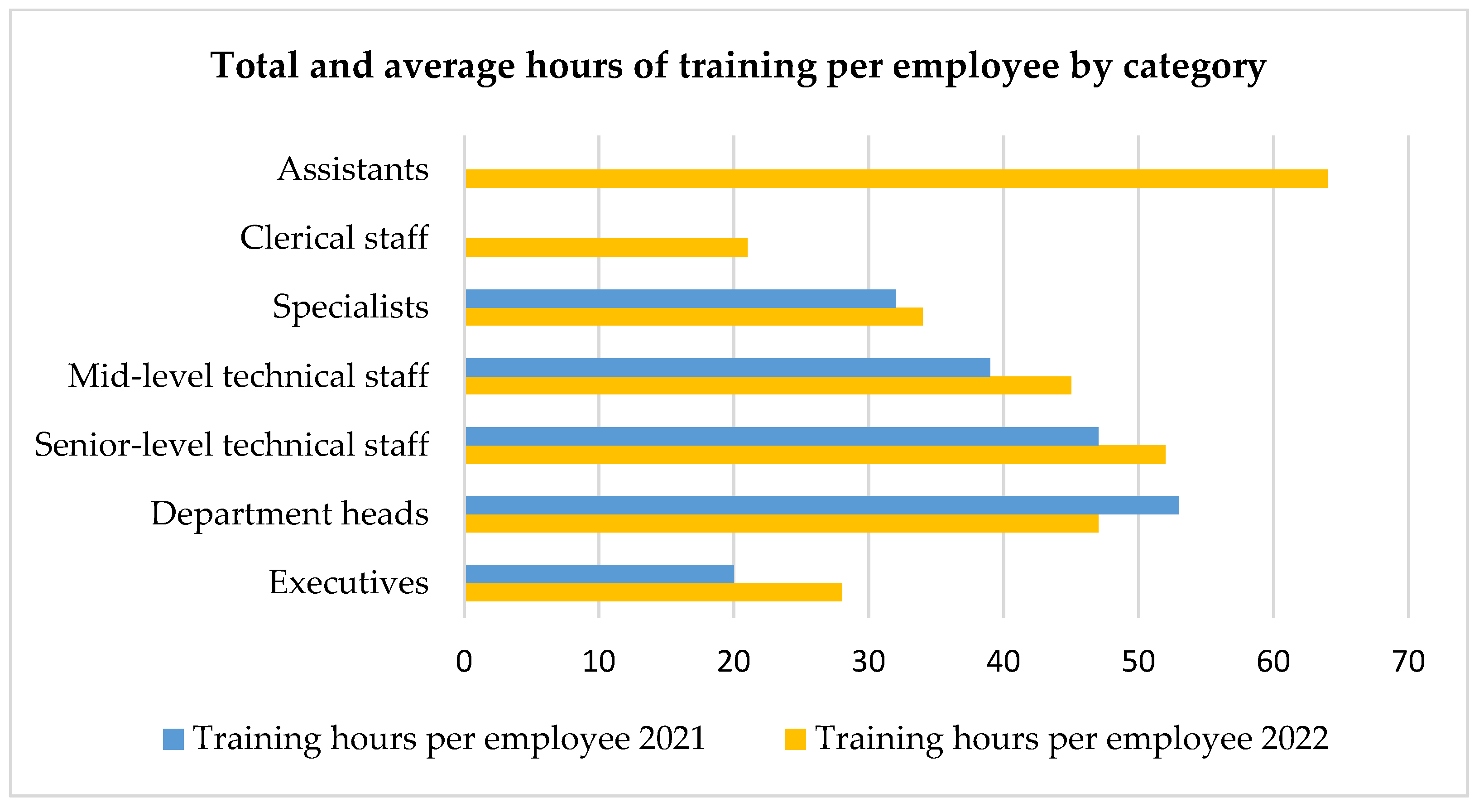

4.2.2. Employee Management in Career Development

4.2.3. Employee Management in Workplace Health and Safety

4.2.4. Collaboration with Community

4.2.5. Collaboration with Customer

4.2.6. Collaboration with the Supplier

4.3. Financial Performance

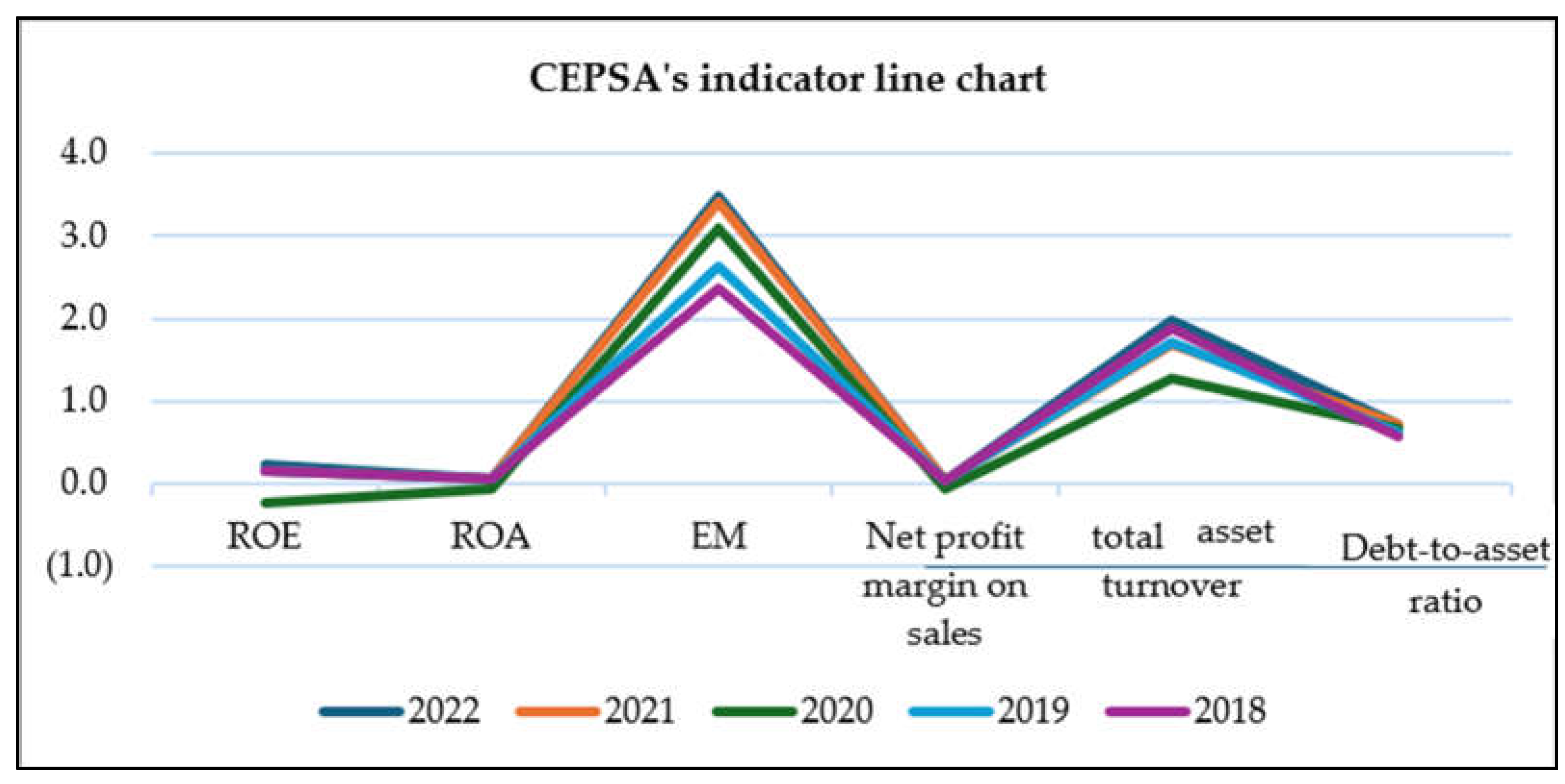

4.3.1. Two-Factor Analysis of Return on Equity (ROE)

4.3.2. Three-Factor Analysis of Return on Equity (ROE)

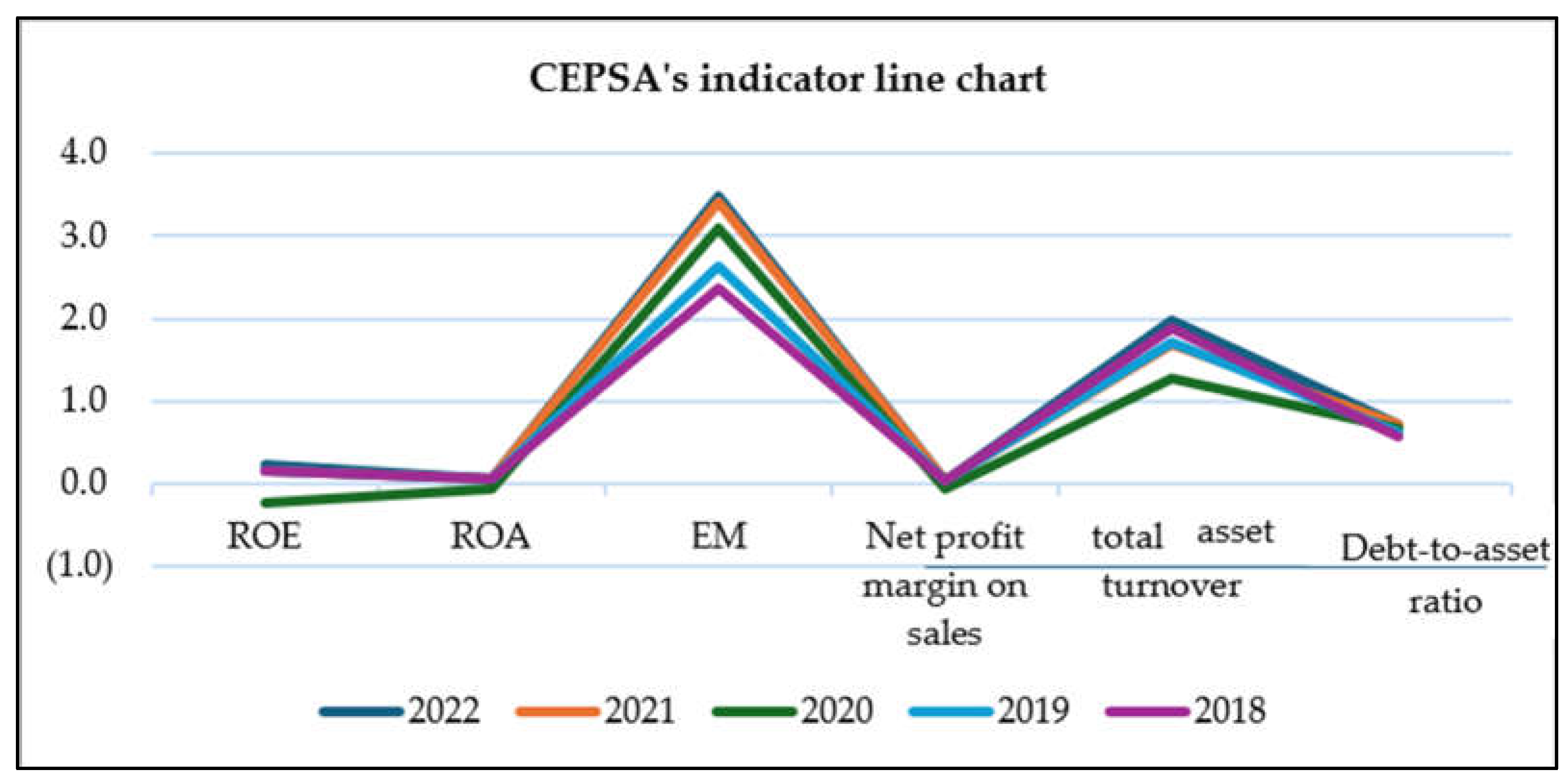

4.3.3. Comparison of ROA, ROE, and EM between CEPSA and Shell

4.3.4. Change in Revenue

4.3.5. Change in Liability

4.3.6. Change in Investment

5. Conclusions

5.1. Limitations and Future Recommendations

5.2. Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Sustainable Stock Exchanges (SSE). Sustainable Stock Exchanges Initiative: Model Guidance on Reporting ESG Information to Investors. 2015. Available online: www.sseinitiative.org/wpcontent/uploads/2015/09/SSE-Model-Guidance-on-Reporting-ESG.pdf (accessed on 23 October 2023).

- Popescu, C.; Hysa, E.; Kruja, A.; Mansi, E. Social innovation, circularity and energy transition for environmental, social and governance (ESG) practices—A comprehensive review. Energies 2022, 15, 9028. [Google Scholar] [CrossRef]

- Hastalona, D.; Sadalia, I. Literature Review ESG and Sustainability Finance. Bp. Int. Res. Crit. Inst.-J. (BIRCI-J.) 2021, 4, 3548–3557. [Google Scholar]

- Hassan, A.; Guo, X. The relationships between reporting format, environmental disclosure and environmental performance: An empirical study. J. Appl. Account. Res. 2017, 18, 425–444. [Google Scholar] [CrossRef]

- Drempetic, S.; Klein, C.; Zwergel, B. The influence of firm size on the ESG score: Corporate sustainability ratings under review. J. Bus. Ethics 2020, 167, 333–360. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Sensitive industries produce better ESG performance: Evidence from emerging markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Galbreath, J. ESG in focus: The Australian evidence. J. Bus. Ethics 2013, 118, 529–541. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Lins, K.V.; Servaes, H.; Tamayo, A. Social capital, trust, and firm performance: The value of corporate social responsibility during the financial crisis. J. Financ. 2017, 72, 1785–1824. [Google Scholar] [CrossRef]

- Kim, J.; Chung, S.; Park, C. Corporate social responsibility and financial performance: The impact of the MSCI ESG ratings on Korean firms. J. Korea Acad.-Ind. Coop. Soc. 2013, 14, 5586–5593. [Google Scholar]

- Milton, F. The social responsibility of business is to increase its profits. In New York Times Magazine; Springer: Berlin/Heidelberg, Germany, 2007; pp. 32–33. [Google Scholar]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar] [CrossRef]

- Cornett, M.M.; Erhemjamts, O.; Tehranian, H. Greed or good deeds: An examination of the relation between corporate social responsibility and the financial performance of US commercial banks around the financial crisis. J. Bank. Financ. 2016, 70, 137–159. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Arlow, P.; Gannon, M.J. Social responsiveness, corporate structure, and economic performance. Acad. Manag. Rev. 1982, 7, 235–241. [Google Scholar] [CrossRef]

- Han, J.J.; Kim, H.J.; Yu, J. Empirical study on relationship between corporate social responsibility and financial performance in Korea. Asian J. Sustain. Soc. Responsib. 2016, 1, 61–76. [Google Scholar] [CrossRef]

- Jha, M.K.; Rangarajan, K. Analysis of corporate sustainability performance and corporate financial performance causal linkage in the Indian context. Asian J. Sustain. Soc. Responsib. 2020, 5, 10. [Google Scholar] [CrossRef]

- Husna, A.; Satria, I. Effects of return on asset, debt to asset ratio, current ratio, firm size, and dividend payout ratio on firm value. Int. J. Econ. Financ. Issues 2019, 9, 50–54. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Derwall, J.; Guenster, N.; Bauer, R.; Koedijk, K. The eco-efficiency premium puzzle. Financ. Anal. J. 2005, 61, 51–63. [Google Scholar] [CrossRef]

- Kluza, K.; Ziolo, M.; Spoz, A. Innovation and environmental, social, and governance factors influencing sustainable business models-Meta-analysis. J. Clean. Prod. 2021, 303, 127015. [Google Scholar] [CrossRef]

- Bauer, R.; Hann, D. Corporate Environmental Management and Credit Risk. Available SSRN 1660470. 2010. Available online: https://ssrn.com/abstract=1660470 (accessed on 16 February 2019).

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Wójcik-Jurkiewicz, M.; Czarnecka, M.; Kinelski, G.; Sadowska, B.; Bilińska-Reformat, K. Determinants of decarbonisation in the transformation of the energy sector: The case of Poland. Energies 2021, 14, 1217. [Google Scholar] [CrossRef]

- Ang, B.W.; Su, B. Carbon emission intensity in electricity production: A global analysis. Energy Policy 2016, 94, 56–63. [Google Scholar] [CrossRef]

- Zenghelis, D. Securing decarbonisation and growth. Natl. Inst. Econ. Rev. 2019, 250, R54–R60. [Google Scholar] [CrossRef]

- Tian, J.; Yu, L.; Xue, R.; Zhuang, S.; Shan, Y. Global low-carbon energy transition in the post-COVID-19 era. Appl. Energy 2022, 307, 118205. [Google Scholar] [CrossRef]

- Eccles, R.G.; Serafeim, G.; Krzus, M.P. Market interest in nonfinancial information. J. Appl. Corp. Financ. 2011, 23, 113–127. [Google Scholar] [CrossRef]

- Jewell, J.J.; Mankin, J.A. What is your ROA? An investigation of the many formulas for calculating return on assets. Acad. Educ. Leadersh. J. 2011, 15, 79–91. [Google Scholar]

- Hallegatte, S.; Heal, G.; Fay, M.; Treguer, D. From Growth to Green Growth—A Framework; No. w17841; National Bureau of Economic Research: Cambridge, MA, USA, 2012. [Google Scholar]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Baran, M.; Kuźniarska, A.; Makieła, Z.J.; Sławik, A.; Stuss, M.M. Does ESG reporting relate to corporate financial performance in the context of the energy sector transformation? Evidence from Poland. Energies 2022, 15, 477. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hörisch, J. In search of the dominant rationale in sustainability management: Legitimacy-or profit-seeking? J. Bus. Ethics 2017, 145, 259–276. [Google Scholar] [CrossRef]

- Vartanian, T.P. Secondary Data Analysis; Oxford University Press: Oxford, UK, 2010. [Google Scholar]

- Dos Santos, M.C.; Pereira, F.H. ESG performance scoring method to support responsible investments in port operations. Case Stud. Transp. Policy 2022, 10, 664–673. [Google Scholar] [CrossRef]

- Yu, W.; Hassan, A.; Adhikariparajuli, M. How Did Amazon Achieve CSR and Some Sustainable Development Goals (SDGs)—Climate Change, Circular Economy, Water Resources and Employee Rights during COVID-19? J. Risk Financ. Manag. 2022, 15, 364. [Google Scholar] [CrossRef]

- Hassan, A.; Roberts, L.; Rodger, K. Corporate accountability for biodiversity and species extinction: Evidence from organisations reporting on their impacts on nature. Bus. Strategy Environ. 2022, 31, 326–352. [Google Scholar] [CrossRef]

- Ates, S. The credibility of corporate social responsibility reports: Evidence from the energy sector in emerging markets. Soc. Responsib. J. 2023, 19, 756–773. [Google Scholar] [CrossRef]

- Santos, M.R.; Rolo, A.; Matos, D.; Carvalho, L. The Circular Economy in Corporate Reporting: Text Mining of Energy Companies’ Management Reports. Energies 2023, 16, 5791. [Google Scholar] [CrossRef]

- Parzonko, A.; Parzonko, A.J.; Bórawski, P.; Wicki, L. Return on Equity in Dairy Farms from Selected EU Countries: Assessment Based on the DuPont Model in Years 2004–2020. Agriculture 2023, 13, 1403. [Google Scholar] [CrossRef]

- Ayaba, M.M.; Amo-Bediako, E.; Takawira, O. Evaluating the financial performance of listed REIT firms in South Africa: A 7-step DuPont model technique. Int. J. Appl. Econ. 2023, 2, 267–278. [Google Scholar] [CrossRef]

- Luo, L.; Tang, Q. The real effects of ESG reporting and GRI standards on carbon mitigation: International evidence. Bus. Strategy Environ. 2023, 32, 2985–3000. [Google Scholar] [CrossRef]

- Nielsen, C. ESG Reporting and Metrics: From Double Materiality to Key Performance Indicators. Sustainability 2023, 15, 16844. [Google Scholar] [CrossRef]

- Das, A.; Peu, S.D.; Akanda, M.A.M.; Islam, A.R.M.T. Peer-to-Peer Energy Trading Pricing Mechanisms: Towards a Comprehensive Analysis of Energy and Network Service Pricing (NSP) Mechanisms to Get Sustainable Enviro-Economical Energy Sector. Energies 2023, 16, 2198. [Google Scholar] [CrossRef]

- Arsad, S.R.; Hasnul Hadi, M.H.; Mohd Afandi, N.A.; Ker, P.J.; Tang, S.G.H.; Mohd Afzal, M.; Ramanathan, S.; Chen, C.P.; Krishnan, P.S.; Tiong, S.K. The Impact of COVID-19 on the Energy Sector and the Role of AI: An Analytical Review on Pre-to Post-Pandemic Perspectives. Energies 2023, 16, 6510. [Google Scholar] [CrossRef]

- KnowESG, Shell plc. Shell Invests $38 Million in Carbon Credit Projects in Brazil, KnowESG. 2022. Available online: https://www.knowesg.com/companies/shell-invests-usd38-million-in-carbon-credit-projects-in-brazil-11072022 (accessed on 7 March 2024).

- Patin, J.C.; Rahman, M.; Mustafa, M. Impact of total asset turnover ratios on equity returns: Dynamic panel data analyses. J. Account. Bus. Manag. (JABM) 2020, 27, 19–29. [Google Scholar] [CrossRef]

- Shell plc. 2022 Annual Report and Accounts. 2022. Available online: https://reports.shell.com/annual-report/2022/ (accessed on 7 March 2024).

- Shell plc. 2019 Annual Report. 2019. Available online: https://reports.shell.com/annual-report/2019/servicepages/disclaimer.php (accessed on 7 March 2024).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Grp. | Section | Metrics | Main Activities in CEPSA |

|---|---|---|---|

| Environmental performance | Environmental performance | Air pollution | Zero net emissions in 2050 |

| Energy park | |||

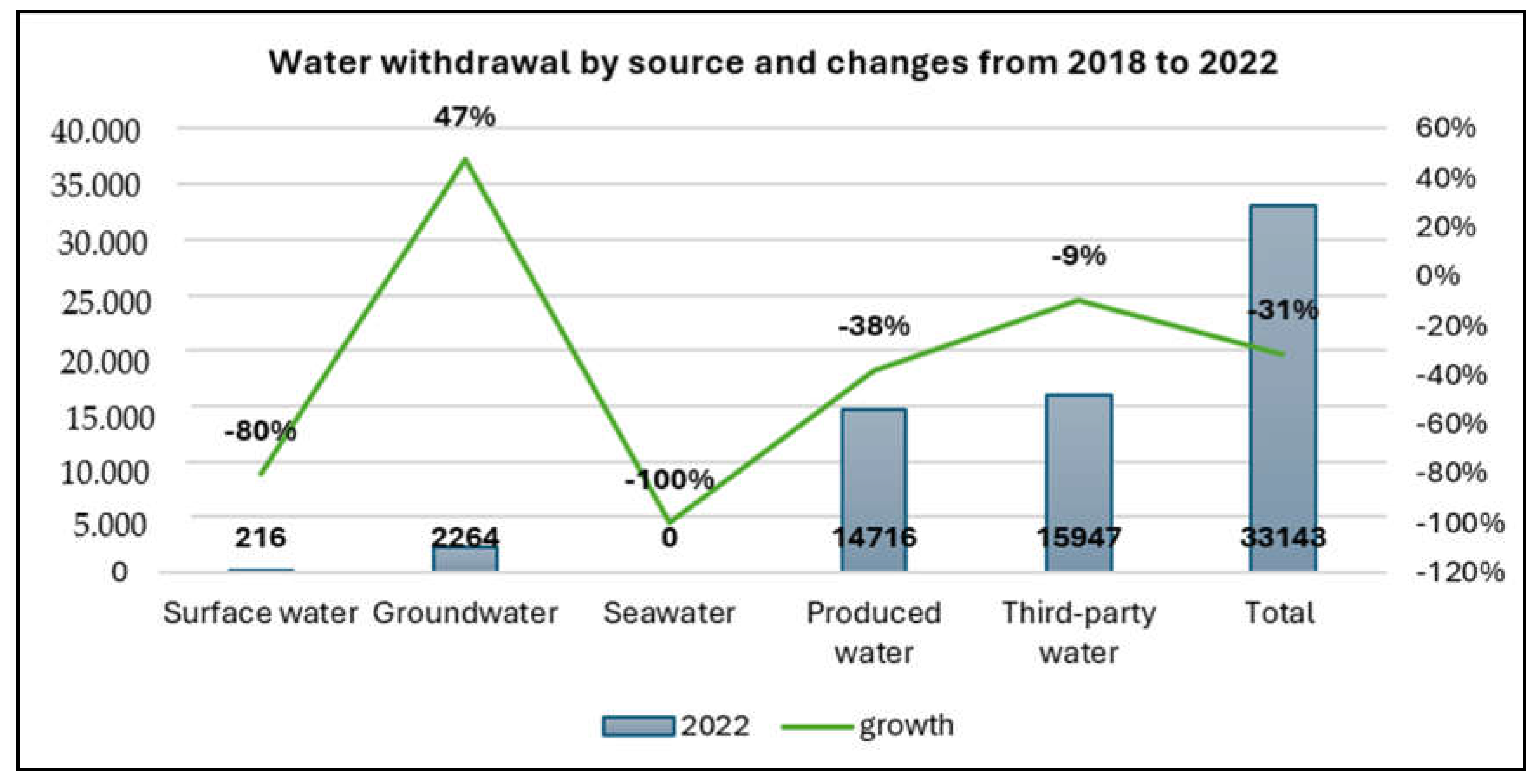

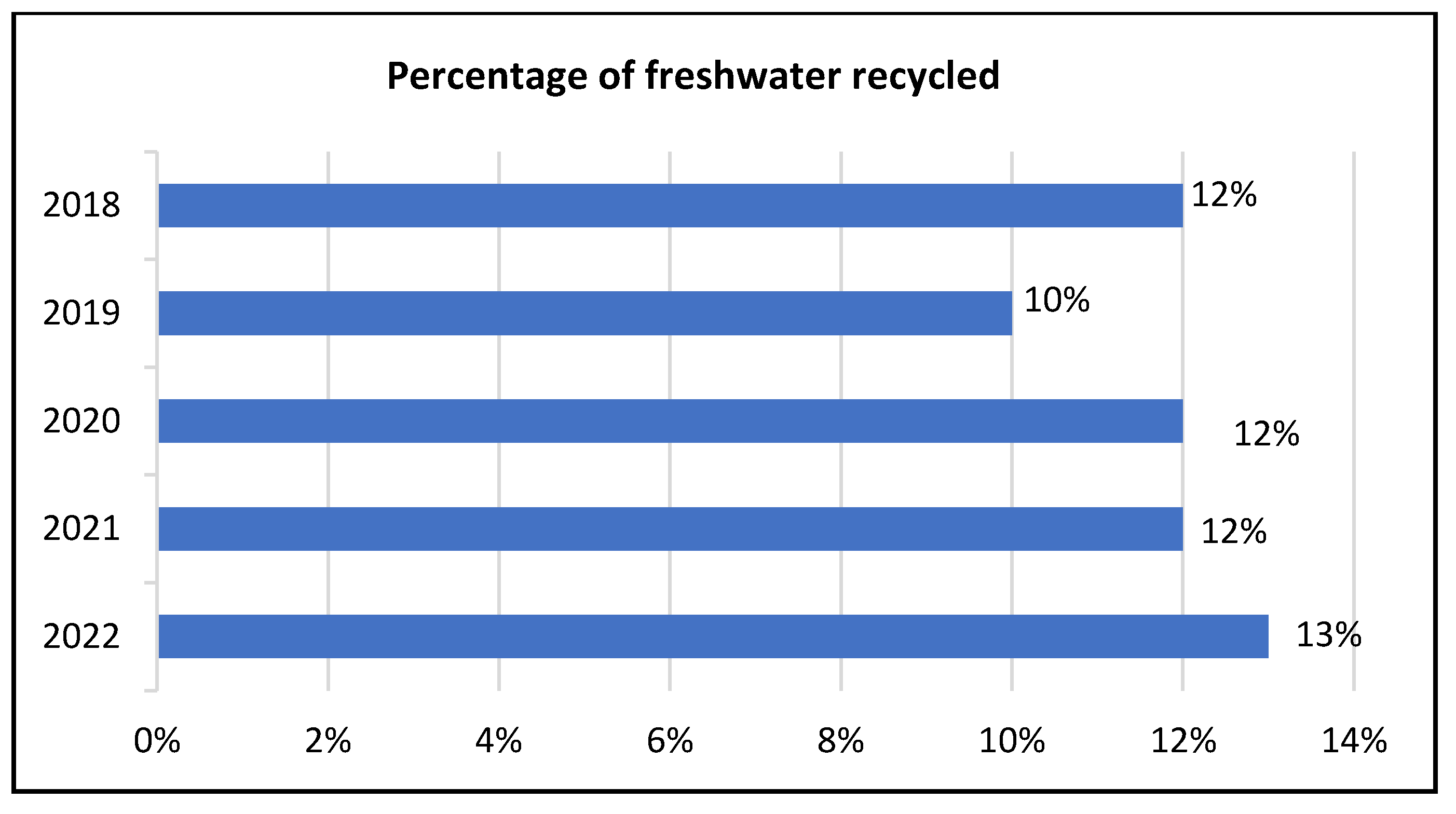

| Water management | Water source and consumption | Our chemical and energy parks use only fresh water that is obtained from the municipal system or other sources; Tenerife uses seawater for more than half of its water supply | |

| Water discharge and reuse project | The La Rabida refinery (Huelva) and the Gibraltar-San Roque refinery (Cádiz) | ||

| Position and Plan for the Use of Wastewater and Water Treatment | |||

| A closed cycle in produced water | |||

| Collaborating with Arcgisa to utilise sewage from cities | |||

| Water risk | At CEPSA, we use the WWF’s Water Risk Filter (WRF) technology to evaluate the water risks related to our facilities | ||

| Other renewable energy | Solar and wind power | The Alijar II Wind Farm in Jerez | |

| Europe’s first network-wide installation of photovoltaic power at service stations | |||

| Biogas | The first European company producing biofuels using co-processing in 2011 | ||

| Collaboration with a bio-methanation plant to achieve filtered soil recovery and make renewable fuels | |||

| Green hydrogen | The Andalusia Green Hydrogen Valley is Spain’s largest green hydrogen park | ||

| The continent of Europe’s northern and southernmost green hydrogen corridor | |||

| Environmental management | Biodiversity policy | HSEQ Policy (Health, Safety, Environment and Quality) | |

| Ecosystem protection, habitats protected or restored | World Database on Protected Areas (WDPA) and BirdLife map | ||

| Achievement in Madrevieja environmental station. | |||

| Achievement in Primera de Palos Lagoon environmental station | |||

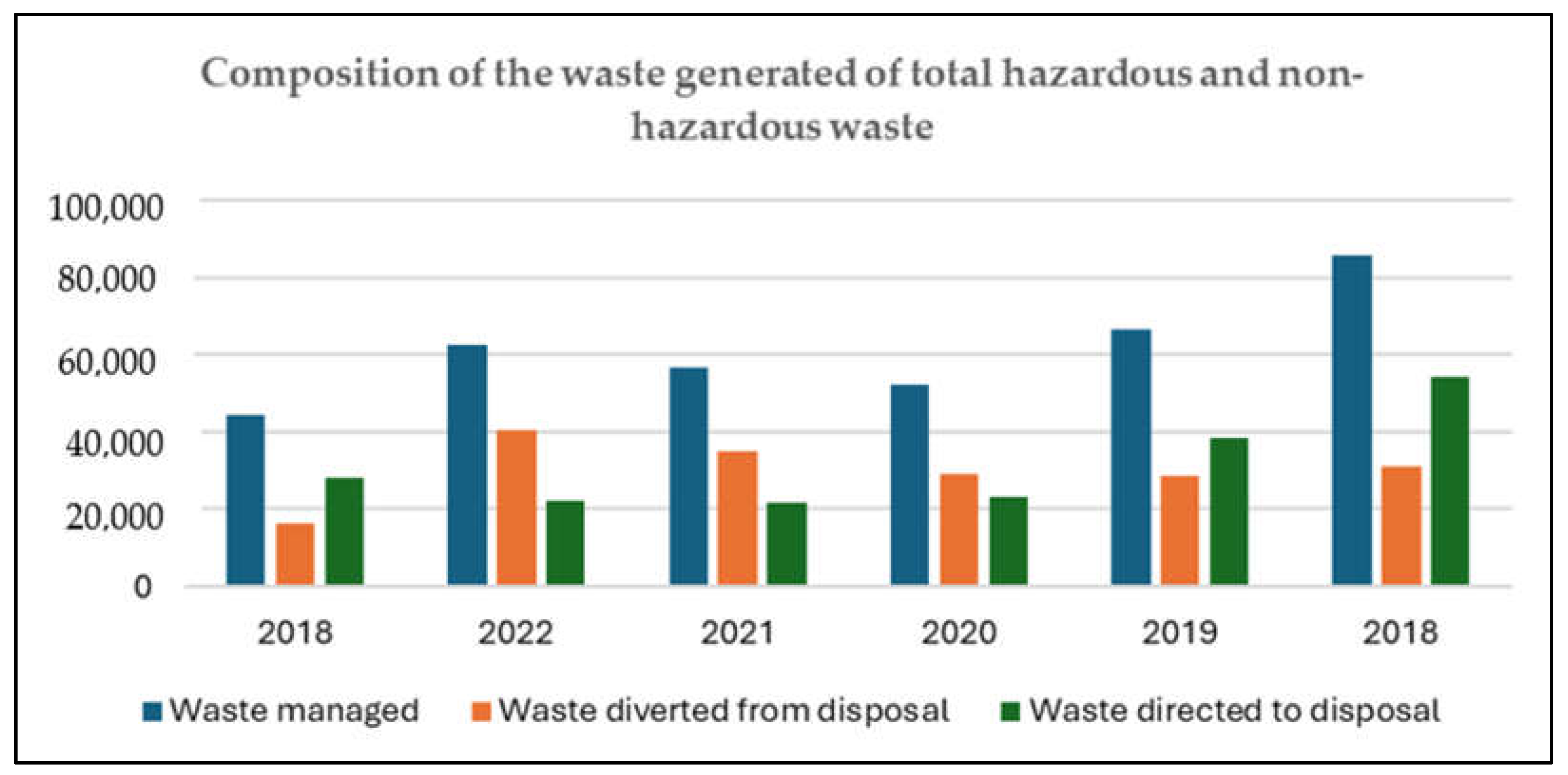

| Waste management | Reintroduction of waste into productive processes. | ||

| Collaboration with a third party to handle the waste generated across our facilities | |||

| Circular business (the waste hierarchy principle, the Circular Economy Board) | |||

| Social Performance | Employee | Diversity and inclusion (gender, ethnicity, demographic, beliefs, and cultures) | Achievement of 30% female participation in leadership positions in business by 2025 |

| Diversity and Inclusion Policy, standards and committees | |||

| Concern for the employment of vulnerable groups | |||

| Career development (professional skills, salaries) | Integrated talent management model | ||

| Integrated evaluation model | |||

| Learning days | |||

| Remuneration | |||

| Health and safety in the workplace | Employee health after COVID-19 | ||

| “Zero-incident” workplace | |||

| Healthy company program | |||

| Health promotion programs | |||

| Collaboration | Community engagement | Sumamos Energías programme | |

| Society relations with indigenous communities | |||

| Social impact assessment in Colombia | |||

| Customer relationship | Developed a model to consistently measure customer experience perception | ||

| Positive motion: new sustainable mobility models and provides the carbon footprints of products | |||

| Commercial and clean energy production | |||

| Supplier relationship | Four-step supplier relationship management process (registration and approval, risk segment and control, performance evaluation, audit) | ||

| wePioneer supplier recognition program | |||

| Procurement |

| GHG Emissions in Scope 1 and Scope 2 | 2022 | 2021 | 2020 | 2019 | 2018 |

|---|---|---|---|---|---|

| Exploration and Production | 168 | 178 | 285 | 468 | 461 |

| Chemicals | 857 | 1069 | 1043 | 1068 | 1102 |

| Energy Parks | 2908 | 2719 | 2802 | 3193 | 3380 |

| Commercial and Clean Energies | 1558 | 1659 | 1649 | 2047 | 1545 |

| Total (Scope 1 and Scope 2) (thousand tCO2eq) | 5491 | 5625 | 5779 | 6776 | 6488 |

| Year | Habitats Protected or Restored | Geographic Location | Size (m2)/Habitat |

|---|---|---|---|

| 2022 | Madrevieja environmental station | San Roque, Spain | 200,000 |

| Primera de Palos lagoon | Huelva, Spain | 335,000 | |

| Las Lagunas de Muelle de las Carabelas | Huelva, Spain | 20,900 | |

| Total size (m2) | 555,900 | ||

| 2021 | Madrevieja environmental station | San Roque, Spain | 200,000 |

| Primera de Palos lagoon | Huelva, Spain | 335,000 | |

| La Rábida | Huelva, Spain | 19,700 | |

| Total size (m2) | 554,700 |

| 2018 | |

|---|---|

| ROE (1) = ROA (2018) ∗ EM (2018) | 15.21% |

| ROE (2) = ROA (2018 + 1) ∗ EM (2018) = ROA (2019) ∗ EM (2018) | 14.17% |

| ROE (3) = ROA (2019) ∗ EM (2018 + 1) = ROA (2019) ∗ EM (2019) | 15.73% |

| The impact of the increase in EM on the ROE in 2019 was as follows: | |

| ROE (3) − ROE (2) | 1.56% |

| The impact of the increase in EM on the ROE in 2019 was as follows: | |

| ROE (3) − ROE (2) | 1.56% |

| 2019 | |

| ROE (1) = ROA (2019) ∗ EM (2019) | 15.73% |

| ROE (2) = ROA (2019 + 1) ∗ EM (2019) = ROA (2020) ∗ EM (2019) | −19.38% |

| ROE (3) = ROA (2020) ∗ EM (2019 + 1) = ROA (2020) ∗ EM (2020) | −22.71% |

| The impact of the decrease in ROA on the ROE in 2020 was as follows: | |

| ROE (2) − ROE (1) | −35.10% |

| The impact of the increase in EM on the ROE in 2020 was as follows: | |

| ROE (3) − ROE (2) | −3.33% |

| 2020 | |

| ROE (1) = ROA (2020) ∗ EM (2020) | −22.71% |

| ROE (2) = ROA (2020 + 1) ∗ EM (2020) = ROA (2021) ∗ EM (2020) | 15.24% |

| ROE (3) = ROA (2021) ∗ EM (2020 + 1) = ROA (2021) ∗ EM (2021) | 16.78% |

| The impact of the increase in ROA on the ROE in 2021 was as follows: | |

| ROE (2) − ROE (1) | 37.94% |

| The impact of the increase in EM on the ROE in 2021 was as follows: | |

| ROE (3) − ROE (2) | 1.54% |

| 2021 | |

| ROE (1) = ROA (2021) ∗ EM (2021) | 16.78% |

| ROE (2) = ROA (2021 + 1) ∗ EM (2021) = ROA (2022) ∗ EM (2021) | 22.81% |

| ROE (3) = ROA (2022) ∗ EM (2021 + 1) = ROA (2022) ∗ EM (2022) | 23.42% |

| The impact of the increase in ROA on the ROE in 2022 was as follows: | |

| ROE (2) − ROE (1) | 6.04% |

| The impact of the increase in EM on the ROE in 2022 was as follows: | |

| ROE (3) − ROE (2) | 0.61% |

| 2018 | |

| ROE (1) = NPMS (2018) * TAT(2018) * EM(2018) | 15.21% |

| ROE (2) = NPMS (2018 + 1) * TAT (2018) * EM (2018) = NPMS (2019) * TAT (2018) * EM (2018) | 15.58% |

| ROE (3) = NPMS (2019) * TAT (2018 + 1) * EM (2018) = NPMS (2019) * TAT (2019) * EM (2018) | 14.17% |

| ROE (4) = NPMS (2019) * TAT (2019) * EM (2018 + 1) = NPMS (2019) * TAT (2019) * EM (2019) | 15.73% |

| The impact of the increase in NPMS on the ROE in 2019 was as follows: | |

| ROE (2)-ROE (1) | 0.37% |

| The impact of the decrease in TAT on the ROE in 2019 was as follows: | |

| ROE (3)-ROE (2) | −1.41% |

| The impact of the increase in EM on the ROE in 2019 was as follows: | |

| ROE (4)-ROE (3) | 1.56% |

| 2019 | |

| ROE (1) = NPMS (2019) * TAT (2019) * EM (2019) | 15.73% |

| ROE (2) = NPMS (2019 + 1) * TAT (2019) * EM (2019) = NPMS (2020) * TAT (2019) * EM (2019) | −26.12% |

| ROE (3) = NPMS (2020) * TAT (2019 + 1) * EM (2019) = NPMS (2020) * TAT (2020) * EM (2019) | −19.38% |

| ROE (4) = NPMS (2020) * TAT (2020) * EM (2019 + 1) = NPMS (2020) * TAT (2020) * EM (2020) | −22.71% |

| The impact of the decrease in NPMS on the ROE in 2020 was as follows: | |

| ROE (2)-ROE (1) | −41.85% |

| The impact of the decrease in TAT on the ROE in 2020 was as follows: | |

| ROE (3)-ROE (2) | 6.75% |

| The impact of the increase in EM on the ROE in 2020 was as follows: | |

| ROE (4)-ROE (3) | −3.33% |

| 2020 | |

| ROE (1) = NPMS (2020) * TAT (2020) * EM (2020) | −22.71% |

| ROE (2) = NPMS (2020 + 1) * TAT (2020) * EM (2020) = NPMS (2021) * TAT (2020) * EM (2020) | 11.52% |

| ROE (3) = NPMS (2021) * TAT (2020 + 1) * EM (2020) = NPMS (2021) * TAT (2021) * EM (2020) | 15.24% |

| ROE (4) = NPMS (2021) * TAT (2021) * EM (2020 + 1)= NPMS (2021) * TAT (2021) * EM (2021) | 16.78% |

| The impact of the increase in NPMS on the return on ROE in 2021 as follows: | |

| ROE (2)-ROE (1) | 34.23% |

| The impact of the increase in TAT on the ROE in 2021 was as follows: | |

| ROE (3)-ROE (2) | 3.71% |

| The impact of the increase in EM on the ROE in 2021 was as follows: | |

| ROE (4)-ROE (3) | 1.54% |

| 2021 | |

| ROE (1) = NPMS (2021) * TAT (2021) * EM (2021) | 16.78% |

| ROE (2) = NPMS (2021 + 1) * TAT (2021) * EM (2021) = NPMS (2022) * TAT (2021) * EM (2021) | 19.27% |

| ROE (3) = NPMS (2022) * TAT (2021 + 1) * EM (2021) = NPMS (2022) * TAT (2022) * EM (2021) | 22.81% |

| ROE (4) = NPMS (2022) * TAT (2022) * EM (2021 + 1) = NPMS (2022) * TAT (2022) * EM (2022) | 23.42% |

| The impact of the increase in NPMS on the ROE in 2022 was as follows: | |

| ROE (2)-ROE (1) | 2.49% |

| The impact of the increase in TAT on the ROE in 2022 was as follows: | |

| ROE (3)-ROE (2) | 3.54% |

| The impact of the increase in EM on the ROE in 2022 was as follows: | |

| ROE (4)-ROE (3) | 0.61% |

| CEPSA | Shell | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Item/Year | 2022 | 2021 | 2020 | 2019 | 2018 | 2022 | 2021 | 2020 | 2019 | 2018 |

| ROE | 23.42% | 16.78% | −22.71% | 15.73% | 15.21% | 22.26% | 11.77% | −13.58% | 8.63% | 11.80% |

| ROA | 6.71% | 4.93% | −7.35% | 5.97% | 6.40% | 9.68% | 5.10% | −5.68% | 4.06% | 5.99% |

| EM | 3.49 | 3.40 | 3.09 | 2.64 | 2.38 | 2.30 | 2.31 | 2.39 | 2.12 | 1.97 |

| net profit margin on sales | 0.03 | 0.03 | −0.06 | 0.03 | 0.03 | 0.11 | 0.08 | −0.12 | 0.05 | 0.06 |

| total asset turnover | 1.98 | 1.67 | 1.27 | 1.71 | 1.88 | 0.87 | 0.67 | 0.48 | 0.87 | 0.99 |

| debt to asset ratio | 0.71 | 0.71 | 0.68 | 0.62 | 0.58 | 0.57 | 0.57 | 0.58 | 0.53 | 0.49 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, Y.; Hassan, A.; Atif, S. Examining the Interplay between CEPSA’s ESG Performance and Financial Performance: An Overview of the Energy Sector Transformation. Sustainability 2024, 16, 2772. https://doi.org/10.3390/su16072772

Hu Y, Hassan A, Atif S. Examining the Interplay between CEPSA’s ESG Performance and Financial Performance: An Overview of the Energy Sector Transformation. Sustainability. 2024; 16(7):2772. https://doi.org/10.3390/su16072772

Chicago/Turabian StyleHu, Yangxueyi, Abeer Hassan, and Sehrish Atif. 2024. "Examining the Interplay between CEPSA’s ESG Performance and Financial Performance: An Overview of the Energy Sector Transformation" Sustainability 16, no. 7: 2772. https://doi.org/10.3390/su16072772

APA StyleHu, Y., Hassan, A., & Atif, S. (2024). Examining the Interplay between CEPSA’s ESG Performance and Financial Performance: An Overview of the Energy Sector Transformation. Sustainability, 16(7), 2772. https://doi.org/10.3390/su16072772