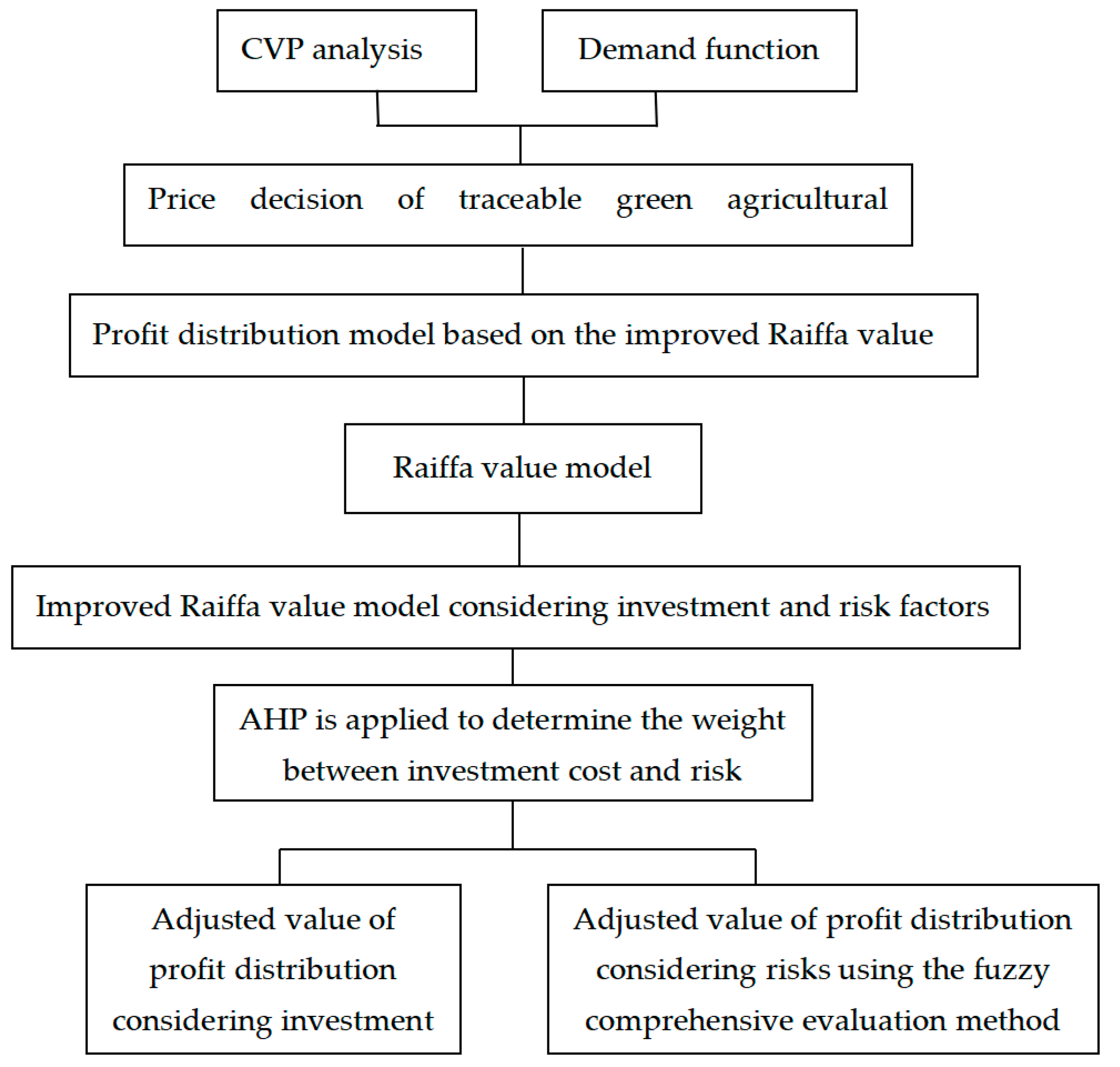

4.2.1. Profit of Each Member under Decentralized Decision-Making

Through in-depth interviews and field visits with relevant personnel of the enterprise, the price of traceable “strawberry tomatoes” sold by the enterprise in supermarkets is 9.2 RMB/catty, while the price of “strawberry tomatoes” sold without the implementation of traceability is 7 RMB/catty, with sales of 200,000 catty, resulting in a premium of 2.2 RMB/catty. According to the survey, the implementation of traceability does not have a significant impact on sales, so it is assumed that the sales volume remains unchanged.

The cost of “strawberry tomato” without traceability is 1 RMB/catty. After the implementation of traceability, the cost of “strawberry tomato” is 1.8 RMB/catty due to the additional cost of purchasing fertilizer and pesticides.

Before the implementation of traceability, farmers were selling “strawberry tomatoes” to wholesalers at the wholesale price of 2.2 RMB/catty; after the implementation of traceability via the acquisition of enterprises, the purchase price was 3.3 RMB/catty; i.e., the enterprise paid more than 1.1 RMB/catty of the cost. Considering the logistics, circulation, and processing, as well as working capital occupancy costs after acquisition by the enterprise, the cost of obtaining traceable “strawberry tomatoes” is about 4.3 RMB/catty, and in addition, there are increased costs of software-development fees, hardware-supporting facilities and equipment, system-maintenance fees, printing fees, marketing fees, and human resources related to traceability, making the average cost of traceable “strawberry tomatoes” increase by 0.8 RMB/catty.

The supermarket collects 15% of the revenue from the sale of “strawberry tomatoes” as a source of profit, and this profit also serves as the opportunity cost of the supermarket.

Since each member has the demand to realize a corresponding profit, the profit from selling “strawberry tomatoes” under decentralized decision-making after the implementation of traceability is calculated for each member:

The sum of the three profits is 300000 + 544000 + 276000 = 1120000 RMB, divided by the total profit of each of the three individually; we obtain that the proportion of the profit of farmers, enterprises, and supermarkets to the overall profit is 26.79%, 48.57%, 24.64%, respectively. Other related data are shown in

Table 1:

As can be seen from

Table 1, after the implementation of traceability, the unit premium obtained by the farmer, enterprise, and supermarket is greater than their additional increase in costs, of which enterprise is the highest, followed by farmer and supermarket, and the reasonableness of the distribution of this premium and whether it is conducive to the long-term and stable development of the implementation of the traceability system need to be further studied.

4.2.3. Adjustment of Profit Distribution of Traceable “Strawberry Tomatoes” Based on Improved Raiffa Values

According to the fixed cost and variable cost apportioned annually by the sales of the corresponding amount of “strawberry tomatoes” as mentioned above, and the small impact on sales due to the increase in selling price after the implementation of traceability, assuming that the sales volume is 200,000 catty, the total cost is RMB.

- (1)

Adjusted value of profit distribution considering investment costs

From the farmer’s perspective, the cost of implementing traceability of “strawberry tomatoes” is 1.8 RMB/catty, and the sales volume at the time of decentralized decision-making is 200,000 catties; then, the investment cost is 360,000 RMB. From the perspective of enterprises, after the implementation of traceability, the purchase price of enterprises is 3.3 RMB/catty; enterprises acquire traceable “strawberry tomatoes” after considering logistics and other costs; the acquisition cost is about 4.3 RMB/catty; in addition to the increased costs associated with the traceability system, the average cost of traceable “strawberry tomatoes” increased by 0.8 RMB/catty, so the cost paid by enterprises is 1.8 RMB/catty, according to the sales volume of decentralized decision-making; then, the enterprise investment cost is RMB 360,000. From the supermarket’s point of view, the profit under decentralized decision-making of RMB 276,000 is the opportunity cost of its centralized decision-making, which can be regarded as the investment cost of the supermarket’s participation in centralized decision-making. Then, the total investment cost is 360,000 + 360,000 + 276,000 = 996,000 RMB; according to Formula (13), we obtain , , ; then, , .

- (2)

Adjusted value of profit distribution considering risks

There are many risks to be borne by each member of the green agricultural product supply chain, and three types of risks are mainly analyzed here: environmental risk, market risk, and dissolution risk. Since it is difficult to obtain objective values of various types of risks in practice, this paper uses the fuzzy comprehensive evaluation method in determining the coefficients of various types of risks to adjust the profit of the agricultural products’ traceability system; the specific steps are as follows.

Using the fuzzy comprehensive evaluation method, we obtain the factor set U = {environmental risk, market risk, dissolution risk}. In accordance with the different degrees of influence of the three risk factors on farmer, enterprise, and supermarket, according to expert opinion and referring to the literature, the corresponding weight vectors = (0.5 0.2 0.3), = (0.1 0.4 0.5), and = (0.1 0.8 0.1) are assigned to each risk factor, respectively. According to the impact of each risk factor on the implementation of traceability in the actual situation, the evaluation set of the degree of impact of each weight vector is assigned as V = {small impact, medium impact, large impact), and the quantitative evaluation set = (0.3 0.5 0.7).

Experts related to agricultural products are invited to form a risk-assessment group, and the experts are asked to evaluate the three risk factors according to the evaluation set. Then, the evaluation results of all the experts are counted, and the evaluation results of the three factors are converted into values in the interval [0, 1] so that the fuzzy vectors

,

,

of the three risks to farmers, enterprises, and supermarkets are obtained. The evaluation results of the experts are synthesized into a matrix. The fuzzy relationship matrix from

to

is obtained as follows.

A fuzzy composite judgment is then performed based on the method of multiplicative-bounded operator:

It happens that the sum of the components in

is 1, and no normalization is carried out. The influence weights of the three risk factors on the farmer are 0.33, 0.22, and 0.45, respectively.

The impact weights of the three risk factors on the enterprise were 0.14, 0.17, and 0.69, respectively.

The impact weights of the three risk factors on the supermarket were 0.72, 0.18, and 0.1, respectively.

Finally, we find the composite score

Enterprise composite score

Supermarket composite score

The final scores of farmer, enterprise, and supermarket were 0.524, 0.61, and 0.376, respectively. After normalization, they were 35%, 40%, and 25%, so the total risk coefficient of farmers was 0.35, the total risk coefficient of enterprises was 0.4, and the total risk coefficient of supermarkets was 0.25. Then, according to , we obtain , and similarly, , ; then, , , .

- (3)

Adjusted profit distribution

The AHP is applied to determine the weight between investment cost and risk. The comparison and quantification of factors are shown in

Table 3.

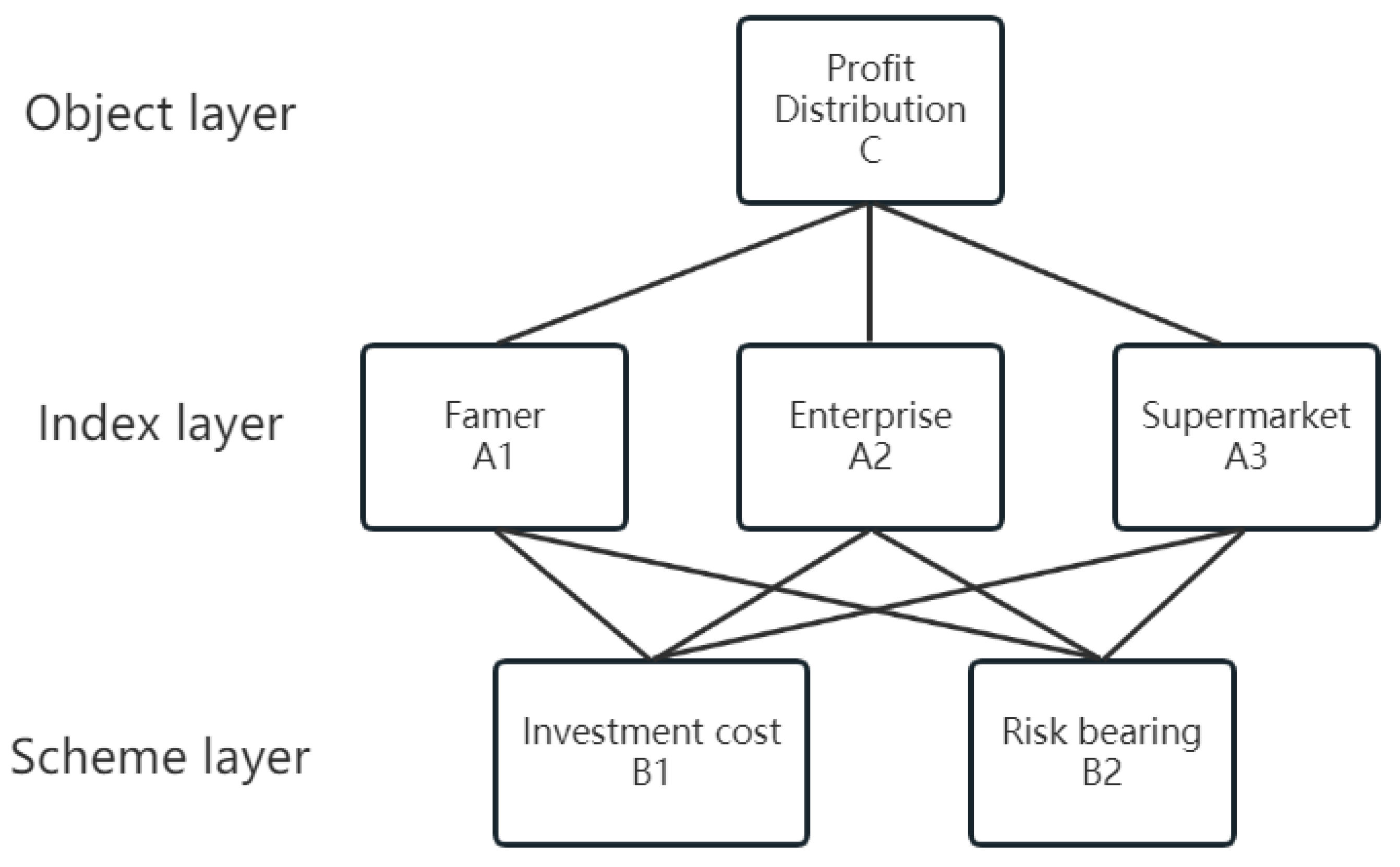

① Taking two factors of investment cost and risk bearing into account, a hierarchical structure model (as shown in

Figure 3) is constructed. The object layer is benefit distribution, the index layer is farmer A1, enterprise A2, and supermarket A3, and the scheme layer is investment cost B1 and risk bearing B2.

The weight of various factors affecting the distribution of interests is determined by the AHP, and the judgment matrix was constructed and normalized for the model after adding the comprehensive factors.

② Judgment matrix processing at the index layer for the object layer.

Based on the quantitative values of the inter-factor comparisons in

Table 3, the scores were assessed by the experts, and two-by-two comparisons were made, as shown in

Table 4.

The data from

Table 4 were normalized via columns, as shown in

Table 5.

The weights of the farmer, enterprise, and supermarket were 0.31, 0.49, and 0.20.

The consistency test is performed on the pairwise comparison matrix. Consistency indicator to find the weight matrix of , n = 3; then, the consistency indicator ; consistency ratio ; according to Satty’s stochastic consistency to take the value of when n = 3, calculate the consistency ratio of ; then, the consistency of the indicator layer to the target layer of the consistency test passed.

③ The judgment matrix processing of the scheme layer to the index layer is shown in

Table 6,

Table 7 and

Table 8.

The weight of the investment cost and risk bearing of farmers, enterprises, and supermarkets were (0.4 0.6), (0.67 0.33), and (0.59994 0.40006), respectively.

A consistency test of the pairwise comparison matrix was carried out. According to

Table 6,

Table 7 and

Table 8, the maximum characteristic roots

,

, and

were calculated to be 2, and the calculated consistency indicators

,

, and

were all 0; the random consistency index

, and the consistency test passed.

④ The final judgment matrix of the scheme layer to the object layer is shown in

Table 12.

The consistency test of hierarchical total ranking is addressed in the following. The consistency ratio of the total hierarchical ordering ; from the aforementioned calculation of the consistency indicators , , and the weights of the indicator layer relative to the target layer , , , the calculation of the total hierarchical ordering ; the consistency test passes.

The weight vector of the adjusted value of the return distribution considering the investment cost and the adjusted value of the return distribution considering the risk is obtained via the AHP as

. Then, in accordance with Formula (15), the final profit allocation of farmers, enterprises, and supermarket members is:

The added value of profit before centralized decision-making is:

{kind=link}

{kind=link}

{kind=link}

{kind=link}