Sustainable Digital Shifts in Chinese Transport and Logistics: Exploring Green Innovations and Their ESG Implications

Abstract

1. Introduction

2. Theoretical Analysis and Hypothesis Development

2.1. Digitalization and ESG Outcomes of Enterprises

2.2. Mechanisms of Corporate Digital Transformation on Corporate ESG Performance

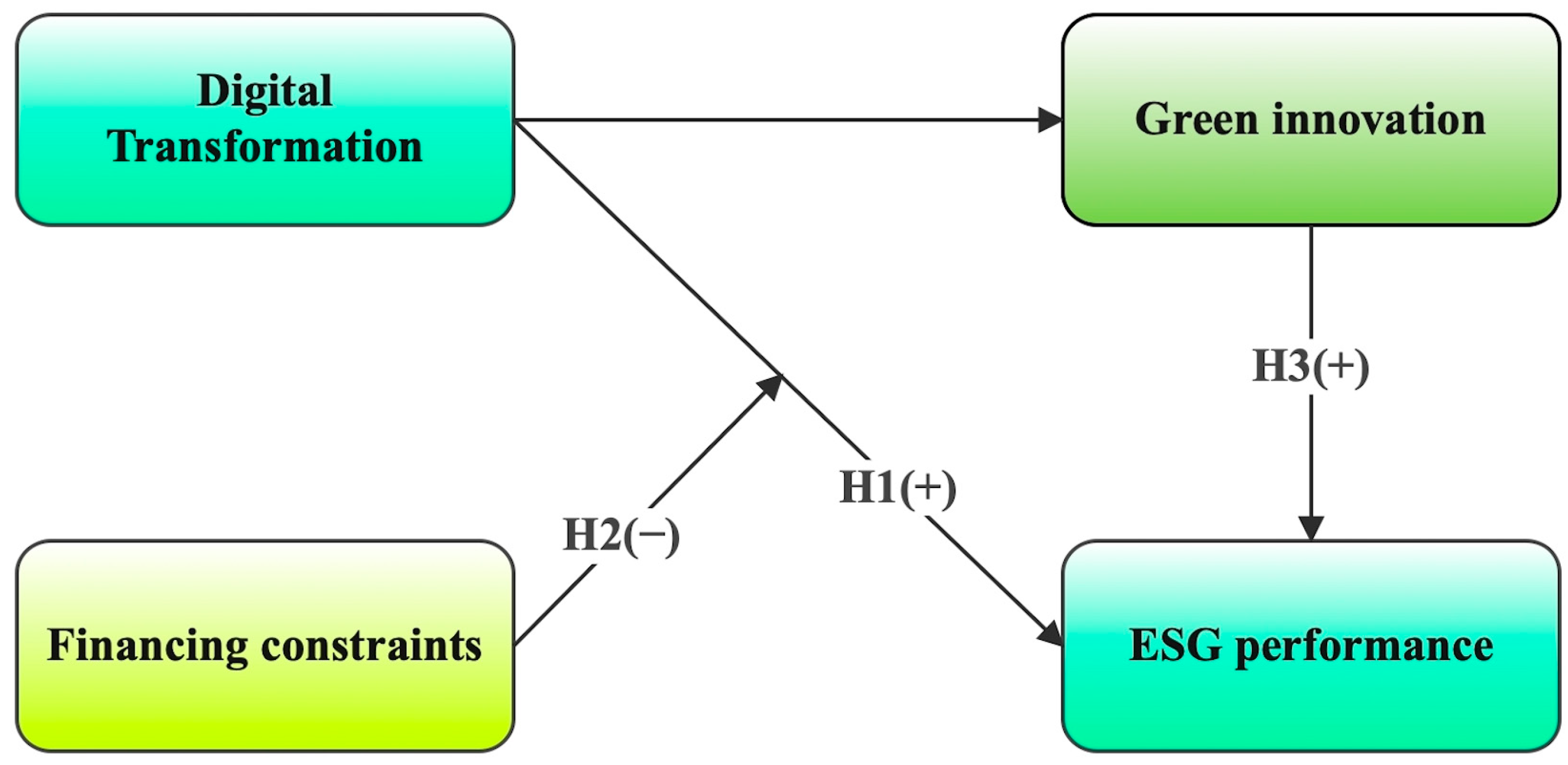

2.2.1. Corporate Digital Transformation, Financing Constraints, and Corporate ESG Performance

2.2.2. Enterprise Digital Transformation, Green Innovation, and Corporate ESG Performance

3. Methodology

3.1. Sample and Data

3.2. Variable Definition

3.2.1. Explained Variables

3.2.2. Core Explanatory Variables

3.2.3. Moderating Variables

3.2.4. Mediating Variable

3.2.5. Control Variables

3.2.6. Descriptive Statistics

3.3. Model Setting

4. Results and Discussion

4.1. Statistical Modeling

4.2. Robustness Test

4.2.1. Replacement of Explanatory Variables

4.2.2. Endogeneity Test

4.2.3. Winsorize

4.3. Heterogeneity Test

4.4. Discussion

5. Conclusions and Implications

5.1. Research Conclusions

5.2. Policy Recommendations

5.2.1. Policy Recommendations for Governments

5.2.2. Recommendations for Transport Enterprises

5.3. Research Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. J. Corp. Financ. 2021, 66, 101889. [Google Scholar] [CrossRef]

- Dong, X.; Sun, Z. Head off a Danger or Overreach Itself: Can ESG Performance Reduce Business Risk? J. Cent. Univ. Financ. Econ. 2023, 7, 57–67. [Google Scholar]

- Li, W. Research on the Relationship between Corporate Social Responsibility and Financial Performance—Based on the Data Analysis of Listed Companies in Transportation Industry. Res. Financ. Econ. Issues 2012, 4, 89–94. [Google Scholar]

- Yang, Y.; Zhao, A. On the Relationship Between the Transportation Industry and Economic Growth. J. Transp. Syst. Eng. Inf. Technol. 2003, 2, 65–71. [Google Scholar]

- Wang, J.; Ma, X. Influencing factors of carbon emissions from transportation in China: Empirical analysis based on two-level econometrics method. Beijing Da Xue Xue Bao 2021, 57, 1133–1142. [Google Scholar]

- Liu, J.; Huang, F.; Chen, B. Research on Influencing Factors and Emission Reduction Strategies of Carbon Emission in Transportation Industry. Highway 2023, 68, 252–259. [Google Scholar]

- Xu, L.; Yang, Z.; Chen, J.; Zou, Z. Spatial-temporal heterogeneity of global ports resilience under Pandemic: A case study of COVID-19. Marit. Policy Manag. 2023. [Google Scholar] [CrossRef]

- Xu, L.; Zou, Z.; Zhou, S. The influence of COVID-19 epidemic on BDI volatility: An evidence from GARCH-MIDAS model. Ocean Coast. Manag. 2022, 229, 106330. [Google Scholar] [CrossRef]

- Guo, X.; Chen, X. The impact of digital transformation on manufacturing-enterprise innovation: Empirical evidence from China. Sustainability 2023, 15, 3124. [Google Scholar] [CrossRef]

- Nambisan, S.; Lyytinen, K.; Majchrzak, A.; Song, M. Digital innovation management. MIS Q. 2017, 41, 223–238. [Google Scholar] [CrossRef]

- Paunov, C.; Rollo, V. Has the internet fostered inclusive innovation in the developing world? World Dev. 2016, 78, 587–609. [Google Scholar] [CrossRef]

- Zhou, H.; Li, X.Y.; Li, X.L. Can the Digital Economy Improve the Level of High-Quality Financial Development? Evidence from China. Sustainability 2023, 15, 7451. [Google Scholar] [CrossRef]

- Karimi, J.; Walter, Z. The role of dynamic capabilities in responding to digital disruption: A factor-based study of the newspaper industry. J. Manag. Inf. Syst. 2015, 32, 39–81. [Google Scholar] [CrossRef]

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research progress and future prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Lee, D. Corporate social responsibility of US-listed firms headquartered in tax havens. Strateg. Manag. J. 2020, 41, 1547–1571. [Google Scholar] [CrossRef]

- Jia, Y.; Gao, X.; Julian, S. Do firms use corporate social responsibility to insure against stock price risk? Evidence from a natural experiment. Strateg. Manag. J. 2020, 41, 290–307. [Google Scholar] [CrossRef]

- Kim, S.; Lee, G.; Kang, H.G. Risk management and corporate social responsibility. Strateg. Manag. J. 2021, 42, 202–230. [Google Scholar] [CrossRef]

- Atan, R.; Alam, M.M.; Said, J.; Zamri, M. The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Manag. Environ. Qual. Int. J. 2018, 29, 182–194. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, social and governance (ESG) scores and financial performance of multilatinas: Moderating effects of geographic international diversification and financial slack. J. Bus. Ethics 2021, 168, 315–334. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. In Corporate Ethics and Corporate Governance; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. [Google Scholar]

- Garcia, A.S.; Orsato, R.J. Testing the institutional difference hypothesis: A study about environmental, social, governance, and financial performance. Bus. Strategy Environ. 2020, 29, 3261–3272. [Google Scholar] [CrossRef]

- Alexander, G.J.; Buchholz, R.A. Corporate social responsibility and stock market performance. Acad. Manag. J. 1978, 21, 479–486. [Google Scholar] [CrossRef]

- Park, S.R.; Oh, K.-S. Integration of ESG information into individual investors’ corporate investment decisions: Utilizing the UTAUT framework. Front. Psychol. 2022, 13, 899480. [Google Scholar] [CrossRef]

- Liu, M.; Luo, X.; Lu, W.-Z. Public perceptions of environmental, social, and governance (ESG) based on social media data: Evidence from China. J. Clean. Prod. 2023, 387, 135840. [Google Scholar] [CrossRef]

- Reber, B.; Gold, A.; Gold, S. ESG disclosure and idiosyncratic risk in initial public offerings. J. Bus. Ethics 2022, 179, 867–886. [Google Scholar] [CrossRef]

- Edmans, A. Does the stock market fully value intangibles? Employee satisfaction and equity prices. J. Financ. Econ. 2011, 101, 621–640. [Google Scholar] [CrossRef]

- Deng, X.; Kang, J.-K.; Low, B.S. Corporate social responsibility and stakeholder value maximization: Evidence from mergers. J. Financ. Econ. 2013, 110, 87–109. [Google Scholar] [CrossRef]

- Flammer, C. Does corporate social responsibility lead to superior financial performance? A regression discontinuity approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Albuquerque, R.; Koskinen, Y.; Zhang, C. Corporate social responsibility and firm risk: Theory and empirical evidence. Manag. Sci. 2019, 65, 4451–4469. [Google Scholar] [CrossRef]

- Shin, D. Corporate Esg Profiles, Matching, and the Cost of Bank Loans; University of Washington: Washington, DC, USA, 2021. [Google Scholar]

- Grimaldi, F.; Caragnano, A.; Zito, M.; Mariani, M. Sustainability engagement and earnings management: The Italian context. Sustainability 2020, 12, 4881. [Google Scholar] [CrossRef]

- Galbreath, J. ESG in focus: The Australian evidence. J. Bus. Ethics 2013, 118, 529–541. [Google Scholar] [CrossRef]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Han, H. Does increasing the QFII quota promote Chinese institutional investors to drive ESG? Asia-Pac. J. Account. Econ. 2023, 30, 1627–1643. [Google Scholar] [CrossRef]

- Chebbi, K.; Ammer, M.A. Board composition and ESG disclosure in Saudi Arabia: The moderating role of corporate governance reforms. Sustainability 2022, 14, 12173. [Google Scholar] [CrossRef]

- Eliwa, Y.; Aboud, A.; Saleh, A. Board gender diversity and ESG decoupling: Does religiosity matter? Bus. Strategy Environ. 2023, 32, 4046–4067. [Google Scholar] [CrossRef]

- Zhang, X.; Zhao, X.; Qu, L. Do green policies catalyze green investment? Evidence from ESG investing developments in China. Econ. Lett. 2021, 207, 110028. [Google Scholar] [CrossRef]

- Lu, S.; Cheng, B. Does environmental regulation affect firms’ ESG performance? Evidence from China. Manag. Decis. Econ. 2023, 44, 2004–2009. [Google Scholar] [CrossRef]

- Ghasemaghaei, M.; Calic, G. Assessing the impact of big data on firm innovation performance: Big data is not always better data. J. Bus. Res. 2020, 108, 147–162. [Google Scholar] [CrossRef]

- Xu, L.; Shi, J.; Chen, J. Agency encroachment and information sharing: Cooperation and competition in freight forwarding market. Marit. Policy Manag. 2023, 50, 321–334. [Google Scholar] [CrossRef]

- Vial, G. Understanding digital transformation: A review and a research agenda. Manag. Digit. Transform. 2021, 28, 13–66. [Google Scholar] [CrossRef]

- Wu, F.; Hu, H.; Lin, H.; Ren, X. Enterprise digital transformation and capital market performance: Empirical evidence from stock liquidity. Manag. World 2021, 37, 130–144. [Google Scholar]

- Liu, F. How digital transformation improve manufacturing’s productivity: Based on three influencing mechanisms of digital transformation. Financ. Econ. 2020, 2020, 93–107. [Google Scholar]

- Zhao, C.; Wang, W.; Li, X. How does digital transformation affect the total factor productivity of enterprises. Financ. Trade Econ 2021, 42, 114–129. [Google Scholar]

- Kane, G.C. How Facebook and Twitter are reimagining the future of customer service. MIT Sloan Manag. Rev. 2014, 55, 1–6. [Google Scholar]

- Chen, J.; Li, P.; Wang, X.; Yi, K. Above management: Scale development and empirical testing for public opinion monitoring of marine pollution. Mar. Pollut. Bull. 2023, 192, 114953. [Google Scholar] [CrossRef]

- Wu, S.; Li, Y. A Study on the Impact of Digital Transformation on Corporate ESG Performance: The Mediating Role of Green Innovation. Sustainability 2023, 15, 6568. [Google Scholar] [CrossRef]

- Lu, Y.; Wang, L.; Zhang, Y. Does digital financial inclusion matter for firms’ ESG disclosure? Evidence from China. Front. Environ. Sci. 2022, 10, 1029975. [Google Scholar] [CrossRef]

- Wang, X.; Luan, X.; Zhang, S. Corporate R&D investment, ESG performance and market value—The Moderating effect of enterprise digital level. Stud. Sci. Sci 2023, 41, 896–904. [Google Scholar]

- Wang, S.; Ouyang, L.; Yuan, Y.; Ni, X.; Han, X.; Wang, F.-Y. Blockchain-enabled smart contracts: Architecture, applications, and future trends. IEEE Trans. Syst. Man Cybern. Syst. 2019, 49, 2266–2277. [Google Scholar] [CrossRef]

- Zhang, Q.; Yang, M.; Lv, S. Corporate digital transformation and green innovation: A quasi-natural experiment from integration of informatization and industrialization in China. Int. J. Environ. Res. Public Health 2022, 19, 13606. [Google Scholar] [CrossRef]

- Frynas, J.G.; Mol, M.J.; Mellahi, K. Management innovation made in China: Haier’s Rendanheyi. Calif. Manag. Rev. 2018, 61, 71–93. [Google Scholar] [CrossRef]

- Zhou, Z.; Li, Z. Corporate digital transformation and trade credit financing. J. Bus. Res. 2023, 160, 113793. [Google Scholar] [CrossRef]

- Fazzari, S.; Hubbard, R.G.; Petersen, B.C. Financing Constraints and Corporate Investment; National Bureau of Economic Research: Cambridge, UK, 1987; pp. 8–32. [Google Scholar]

- Hao, Y.; Zhang, Y. Research on the influence of digital transformation on enterprise ESG performance under the “double carbon” goal. Sci.-Technol. Manag. 2022, 24, 80–91. [Google Scholar] [CrossRef]

- Zhai, H.; Liu, Y. Research on the Relationship among Digital Finance Development, Financing Constraint and Enterprise Green Innovation. Sci. Technol. Prog. Policy 2021, 38, 116–124. [Google Scholar]

- Genzorova, T.; Corejova, T.; Stalmasekova, N. How digital transformation can influence business model, Case study for transport industry. Transp. Res. Procedia 2019, 40, 1053–1058. [Google Scholar] [CrossRef]

- Tsakalidis, A.; Gkoumas, K.; Pekár, F. Digital transformation supporting transport decarbonisation: Technological developments in EU-funded research and innovation. Sustainability 2020, 12, 3762. [Google Scholar] [CrossRef]

- Qing, L.; Chun, D.; Dagestani, A.A.; Li, P. Does proactive green technology innovation improve financial performance? Evidence from listed companies with semiconductor concepts stock in China. Sustainability 2022, 14, 4600. [Google Scholar] [CrossRef]

- Peattie, K.; Ratnayaka, M. Responding to the green movement. Ind. Mark. Manag. 1992, 21, 103–110. [Google Scholar] [CrossRef]

- Wang, D.; Peng, K.; Tang, K.; Wu, Y. Does FinTech development enhance corporate ESG performance? Evidence from an emerging market. Sustainability 2022, 14, 16597. [Google Scholar] [CrossRef]

- Hu, J.; Han, Y.; Zhong, Y. How corporate digital transformation affects corporate ESG performance-evidence from Chinese listed companies [J/OL]. Ind. Econ. Rev. 2022, 1, 1–19. [Google Scholar]

- Qing, L.; Alnafrah, I.; Dagestani, A.A. Does green technology innovation benefit corporate financial performance? Investigating the moderating effect of media coverage. Corp. Soc. Responsib. Environ. Manag. 2023. [Google Scholar] [CrossRef]

- Qing, L.; Usman, M.; Radulescu, M.; Haseeb, M. Towards the vision of going green in South Asian region: The role of technological innovations, renewable energy and natural resources in ecological footprint during globalization mode. Resour. Policy 2024, 88, 104506. [Google Scholar] [CrossRef]

{kind=link}

| Symbol | Variable | Measurement |

|---|---|---|

| ESG | ESG performance | Based on the Huazheng ESG rating scale, the scores range from 1 to 9, ascending from low to high |

| Digital | Digital transformation | Natural log of the total occurrences of digitization-related terms within a corporate annual report, increased by one |

| FC | Financing constraints | SA index |

| Green | Green innovation | Natural log of the count of green invention patents, increased by one |

| Size | Size of enterprise | Natural logarithm of the total assets of the enterprise |

| Age | Age of enterprise | Natural logarithm of the year minus listing year plus one |

| Growth | Increase rate of business revenue | (current period operating income − previous period operating income)/previous period operating income |

| Lev | Asset-liability ratio | Total business liabilities/total assets |

| Indep | Percentage of independent directors | Ratio of independent directors to the total board membership |

| Dual | Two jobs in one | Assigned 1 if the Chairman also serves as the Managing Director, and 0 in all other cases |

| Top1 | Percentage of shareholding of the largest shareholder | Number of shares held by the largest shareholder as a percentage of the total number of shares in the enterprise |

| Board | Board size | Natural logarithm of the number of board members |

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| ESG | 726 | 6.850 | 1.126 | 3.000 | 8.000 |

| Digital | 726 | 2.552 | 1.131 | 0.000 | 5.638 |

| FC | 726 | 3.785 | 0.302 | 2.902 | 4.617 |

| Green | 726 | 0.126 | 0.389 | 0.000 | 2.639 |

| Size | 726 | 23.146 | 1.374 | 20.249 | 26.367 |

| Age | 726 | 2.648 | 0.570 | 1.099 | 3.367 |

| Growth | 726 | 0.132 | 0.466 | −0.652 | 3.116 |

| Lev | 726 | 0.440 | 0.182 | 0.063 | 0.864 |

| Indep | 726 | 0.364 | 0.056 | 0.250 | 0.556 |

| Dual | 726 | 0.107 | 0.310 | 0.000 | 1.000 |

| Top1 | 726 | 42.482 | 13.780 | 14.560 | 75.460 |

| Board | 726 | 2.408 | 0.209 | 1.946 | 2.996 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| ESG | ESG | Green | ESG | |

| Digital | 0.072 ** (2.462) | 0.596 ** (2.159) | 0.052 *** (2.628) | 0.066 ** (2.255) |

| FC | - | −0.763 (−1.596) | - | - |

| Digital FC | - | −0.138 * (−1.910) | - | - |

| Green | - | - | - | 0.112 * (1.878) |

| Size | 0.445 *** (7.042) | 0.465 *** (7.399) | 0.094 ** (2.208) | 0.434 *** (6.862) |

| Age | −0.251 ** (−2.018) | −0.210 (−1.638) | −0.229 *** (−2.715) | −0.225 * (−1.805) |

| Growth | −0.060 * (−1.730) | −0.066 * (−1.912) | 0.054 ** (2.300) | −0.066 * (−1.900) |

| Lev | −0.280 (−1.418) | −0.394 ** (−1.985) | 0.067 (0.498) | −0.288 (−1.458) |

| Indep | 0.311 (0.966) | 0.197 (0.614) | 0.555 ** (2.542) | 0.249 (0.771) |

| Dual | −0.131 * (−1.852) | −0.142 ** (−2.022) | 0.085 * (1.777) | −0.141 ** (−1.986) |

| Top1 | −0.005 (−1.354) | −0.138 * (−1.910) | −0.007 *** (−2.823) | −0.004 (−1.135) |

| Board | −0.017 (−0.155) | 0.018 (0.164) | −0.143 * (−1.952) | −0.001 (−0.007) |

| _cons | −2.660 * (−1.868) | −0.539 (−0.250) | −1.370 (−1.419) | −2.507 * (−1.761) |

| Year & Firm | Yes | Yes | Yes | Yes |

| N | 726 | 726 | 726 | 726 |

| R_square | 0.118 | 0.137 | 0.175 | 0.123 |

| Variables | (1) | (2) |

|---|---|---|

| PESG | ESG | |

| Digital | 1.079 ** | - |

| (2.545) | ||

| L.Digital | - | 0.044 * |

| (1.674) | ||

| Size | 2.195 | 0.387 *** |

| (1.430) | (5.676) | |

| Age | −1.157 | −0.192 |

| (−0.518) | (−1.305) | |

| Growth | 0.837 | −0.056 * |

| (1.349) | (−1.671) | |

| Lev | −3.136 | −0.206 |

| (−0.963) | (−1.074) | |

| Indep | 9.392 ** | 0.035 |

| (2.256) | (0.117) | |

| Dual | 1.677 * | −0.102 |

| (1.732) | (−1.564) | |

| Top1 | −0.129 ** | 0.002 |

| (−2.229) | (0.490) | |

| Board | 1.570 | 0.009 |

| (1.075) | (0.088) | |

| _cons | −29.014 | −1.494 |

| (−0.827) | (−0.977) | |

| Year & Firm | Yes | Yes |

| N | 433 | 578 |

| R_square | 0.714 | 0.100 |

| Variables | (1) |

|---|---|

| ESG_w | |

| Digital_w | 0.071 ** |

| (2.458) | |

| Size_w | 0.450 *** |

| (7.259) | |

| Age_w | −0.243 ** |

| (−1.992) | |

| Growth_w | −0.059 * |

| (−1.680) | |

| Lev_w | −0.307 |

| (−1.579) | |

| Indep_w | 0.354 |

| (1.118) | |

| Dual_w | −0.113 |

| (−1.626) | |

| Top1_w | −0.004 |

| (−1.192) | |

| Board_w | −0.019 |

| (−0.182) | |

| _cons | −2.837 ** |

| (−2.027) | |

| Year & Firm | Yes |

| N | 726 |

| R_square | 0.121 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Large-Size | Small-Size | State-Owned | Non-State-Owned | |

| ESG | ESG | ESG | ESG | |

| Digital | 0.111 *** | 0.030 | 0.083 *** | 0.040 |

| (2.749) | (0.669) | (2.671) | (0.374) | |

| Size | 0.377 ** | 0.469 *** | 0.399 *** | 0.594 ** |

| (2.451) | (6.177) | (5.261) | (2.210) | |

| Age | −0.198 | −0.196 | −0.157 | −0.456 |

| (−0.938) | (−1.166) | (−1.047) | (−1.472) | |

| Growth | −0.022 | −0.089 * | −0.068 * | −0.038 |

| (−0.441) | (−1.684) | (−1.747) | (−0.372) | |

| Lev | −0.134 | −0.399 | −0.310 | 0.137 |

| (−0.405) | (−1.431) | (−1.446) | (0.228) | |

| Indep | 0.408 | 0.235 | 0.367 | −0.460 |

| (0.966) | (0.436) | (1.056) | (−0.470) | |

| Dual | −0.206 * | −0.112 | −0.199 ** | 0.118 |

| (−1.940) | (−1.128) | (−2.471) | (0.658) | |

| Top1 | −0.014 ** | −0.001 | −0.005 | −0.002 |

| (−2.467) | (−0.202) | (−1.291) | (−0.180) | |

| Board | 0.099 | −0.141 | −0.005 | 0.025 |

| (0.682) | (−0.863) | (−0.046) | (0.068) | |

| _cons | −1.359 | −2.957 * | −1.825 | −5.673 |

| (−0.382) | (−1.782) | (−1.057) | (−0.940) | |

| Year & Firm | Yes | Yes | Yes | Yes |

| N | 360 | 366 | 592 | 134 |

| R_square | 0.149 | 0.159 | 0.116 | 0.209 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, L.; Xu, J.; Yuan, X. Sustainable Digital Shifts in Chinese Transport and Logistics: Exploring Green Innovations and Their ESG Implications. Sustainability 2024, 16, 1877. https://doi.org/10.3390/su16051877

Yu L, Xu J, Yuan X. Sustainable Digital Shifts in Chinese Transport and Logistics: Exploring Green Innovations and Their ESG Implications. Sustainability. 2024; 16(5):1877. https://doi.org/10.3390/su16051877

Chicago/Turabian StyleYu, Linxuan, Jing Xu, and Xiang Yuan. 2024. "Sustainable Digital Shifts in Chinese Transport and Logistics: Exploring Green Innovations and Their ESG Implications" Sustainability 16, no. 5: 1877. https://doi.org/10.3390/su16051877

APA StyleYu, L., Xu, J., & Yuan, X. (2024). Sustainable Digital Shifts in Chinese Transport and Logistics: Exploring Green Innovations and Their ESG Implications. Sustainability, 16(5), 1877. https://doi.org/10.3390/su16051877