Research of the Impact of Hydrogen Metallurgy Technology on the Reduction of the Chinese Steel Industry’s Carbon Dioxide Emissions

Abstract

1. Introduction

2. Literature Review

3. Methodology and Scenario Development

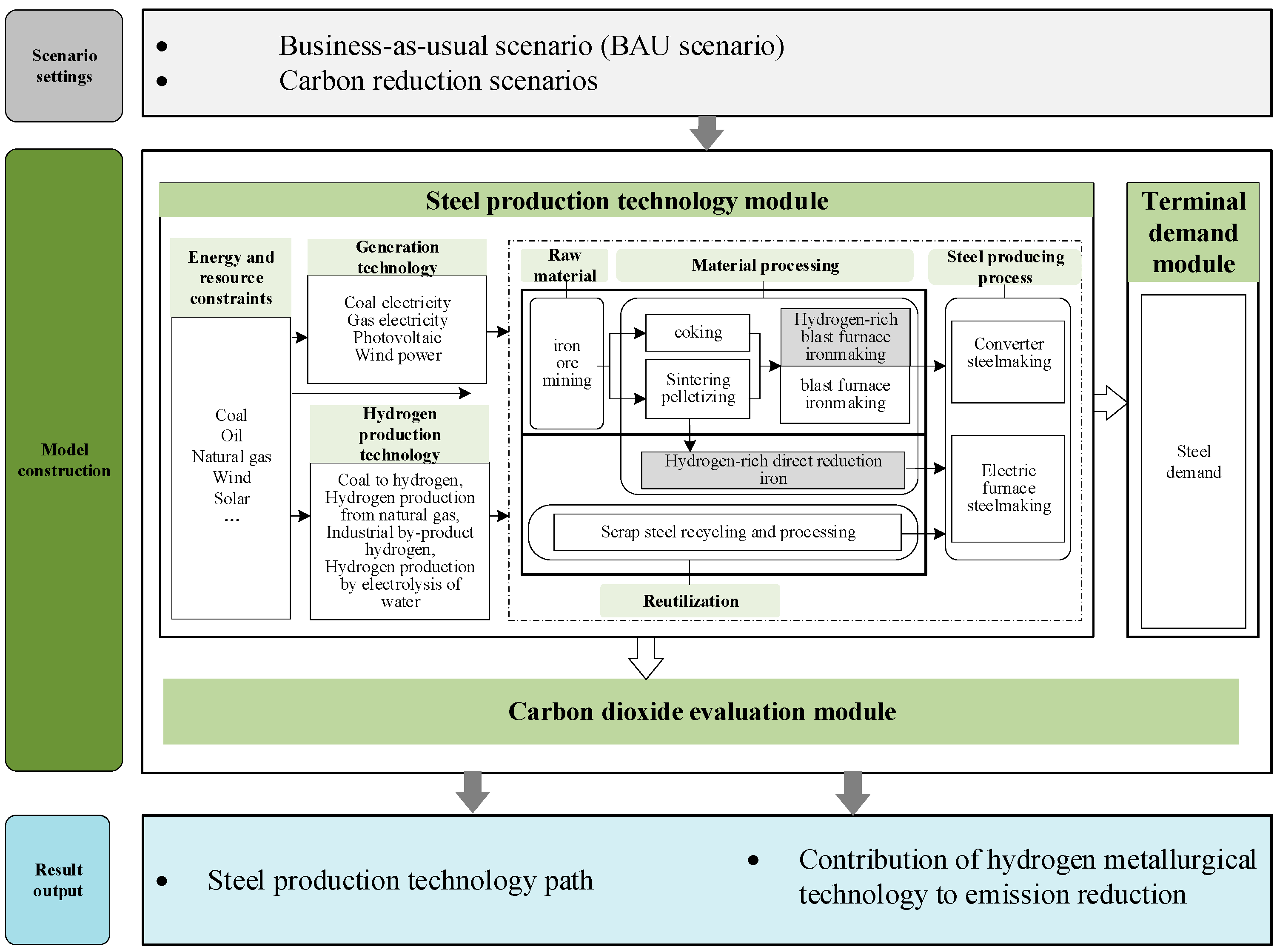

3.1. Constructing a Hydrogen Metallurgy Model for the Chinese Steel Industry

3.2. Model Construction

3.2.1. Terminal Demand Module

3.2.2. Steel Production Technology Module

3.2.3. CO2 Evaluation Module

3.3. Model Parameter Settings

3.3.1. Terminal Requirements Module Parameter Settings

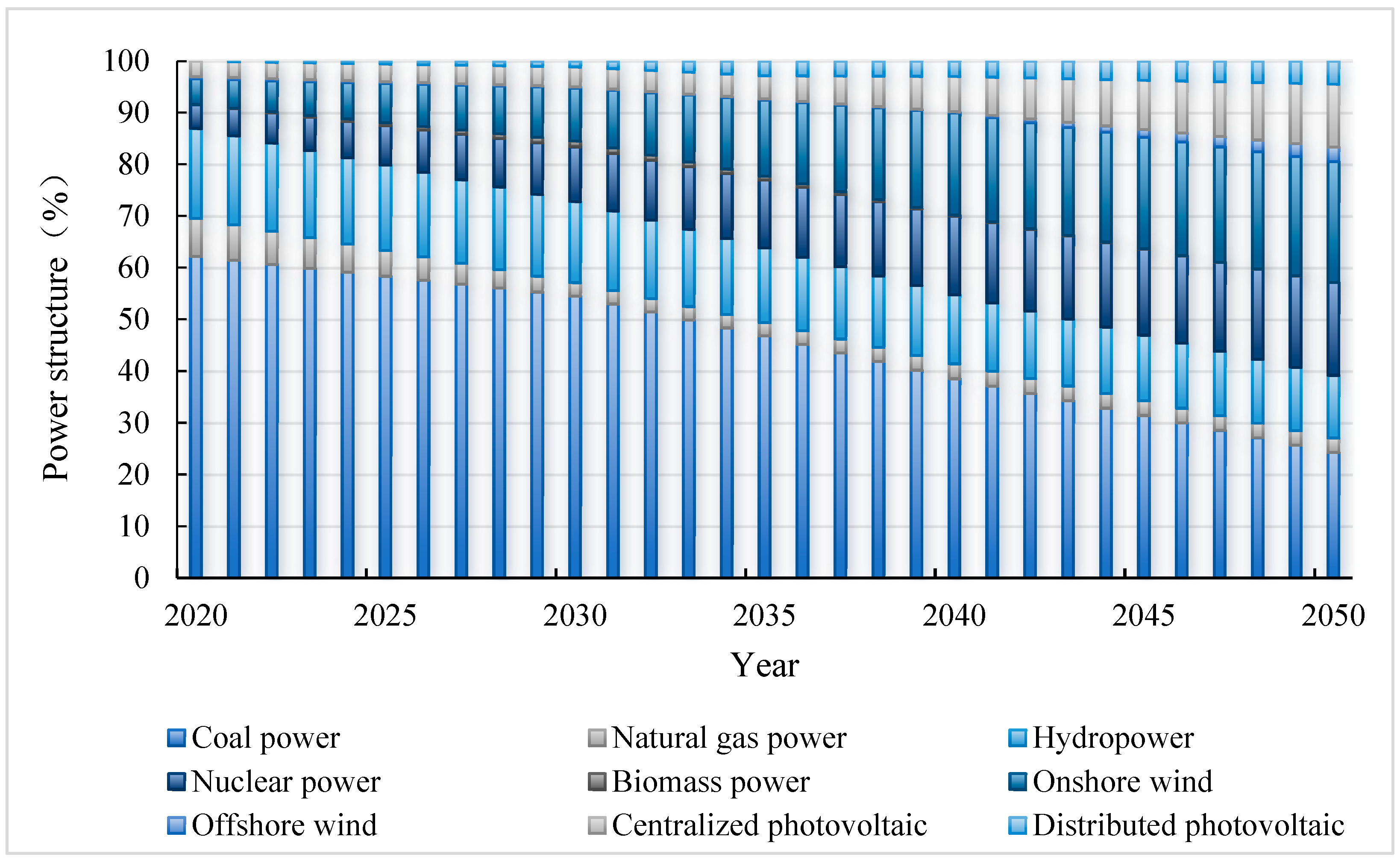

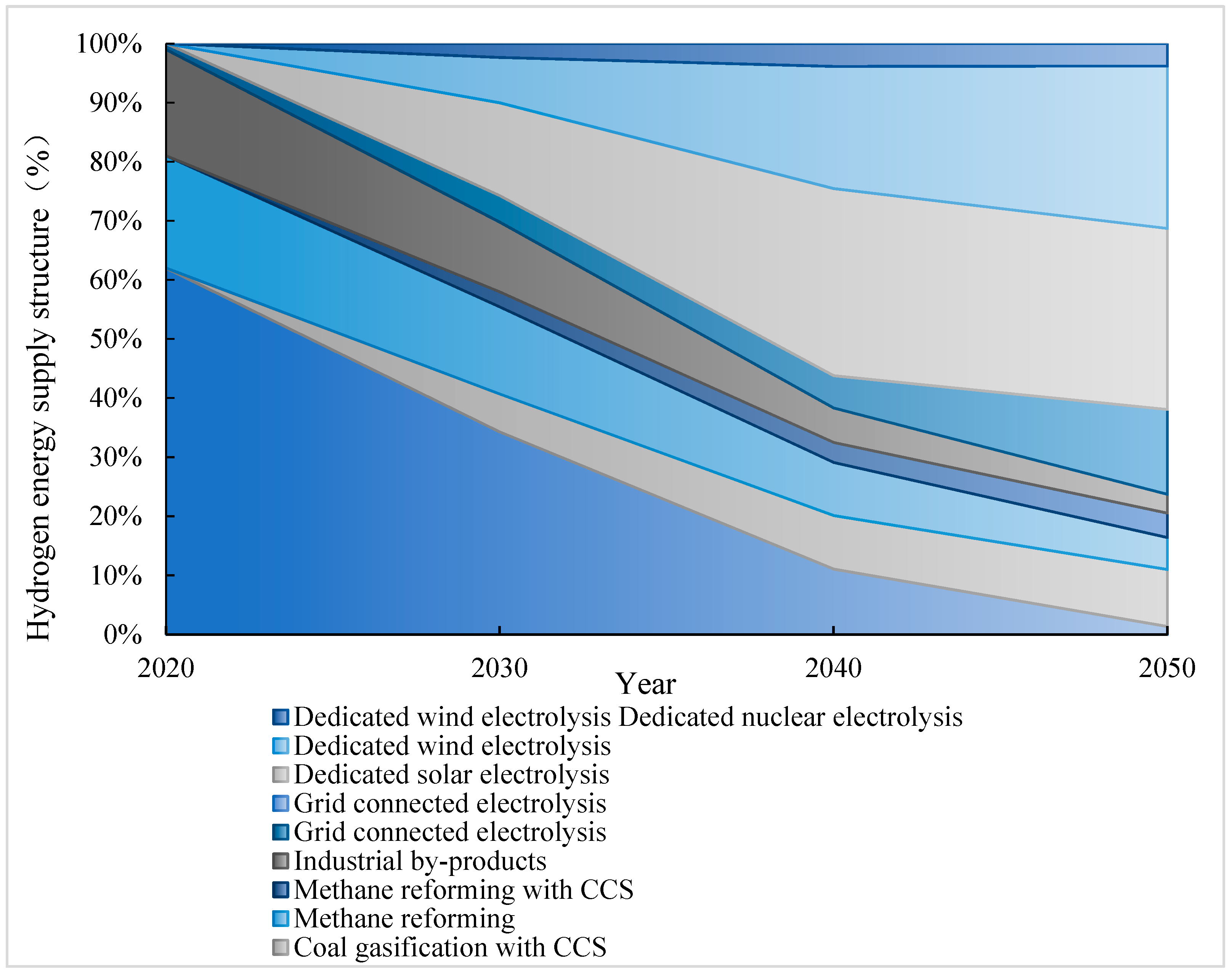

3.3.2. Parameter Settings for Steel Production Technology Modules

- (1)

- Steel production process

- (2)

- Power generation process

- (3)

- Hydrogen production process

3.3.3. CO2 Assessment Module Parameter Settings

- (1)

- CO2 emission parameter setting in the iron and steel production process

- (2)

- CO2 emission parameter settings for hydrogen production and power generation processes

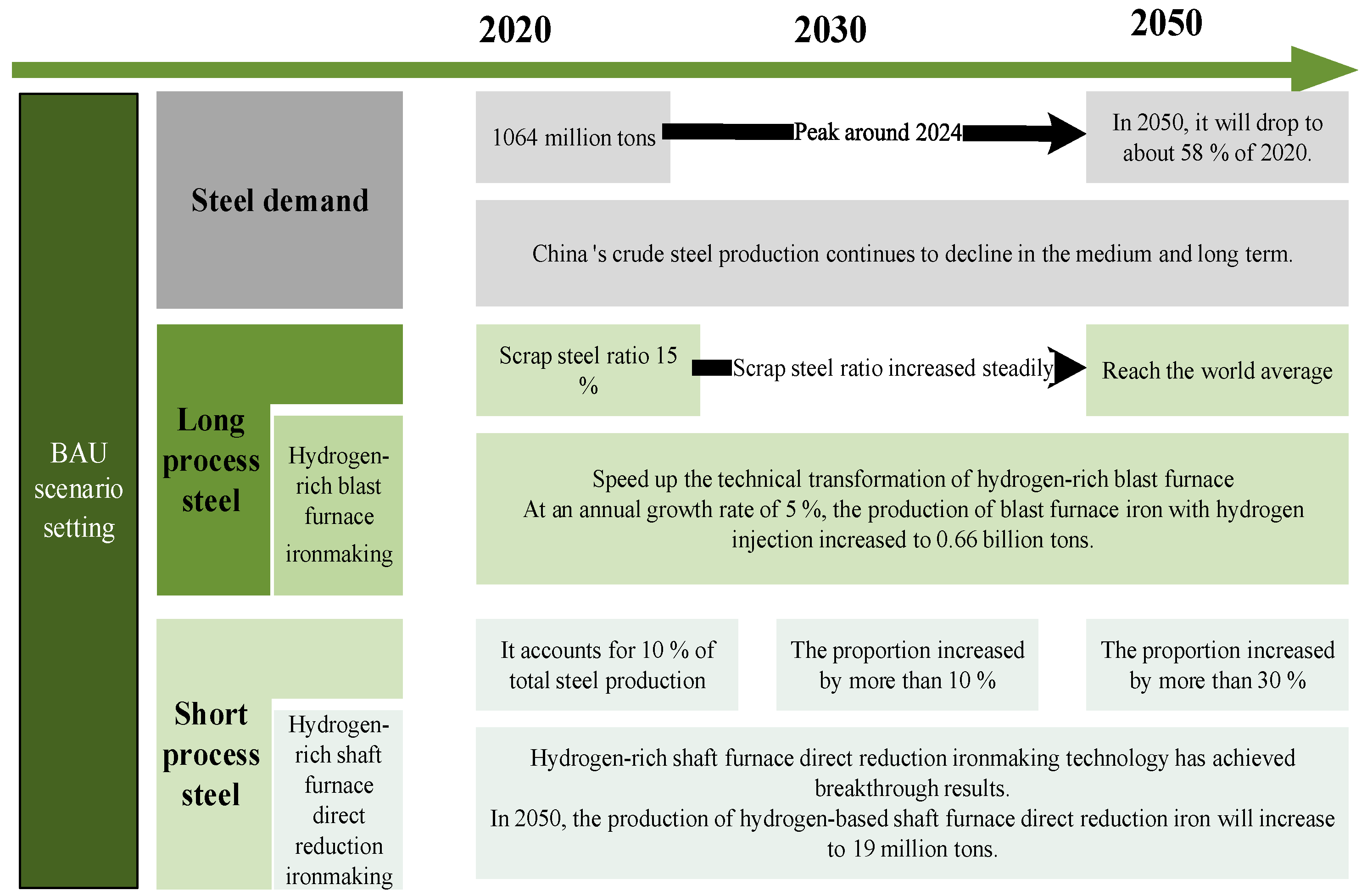

3.4. Scenario Setting

3.4.1. Business-as-Usual Scenario

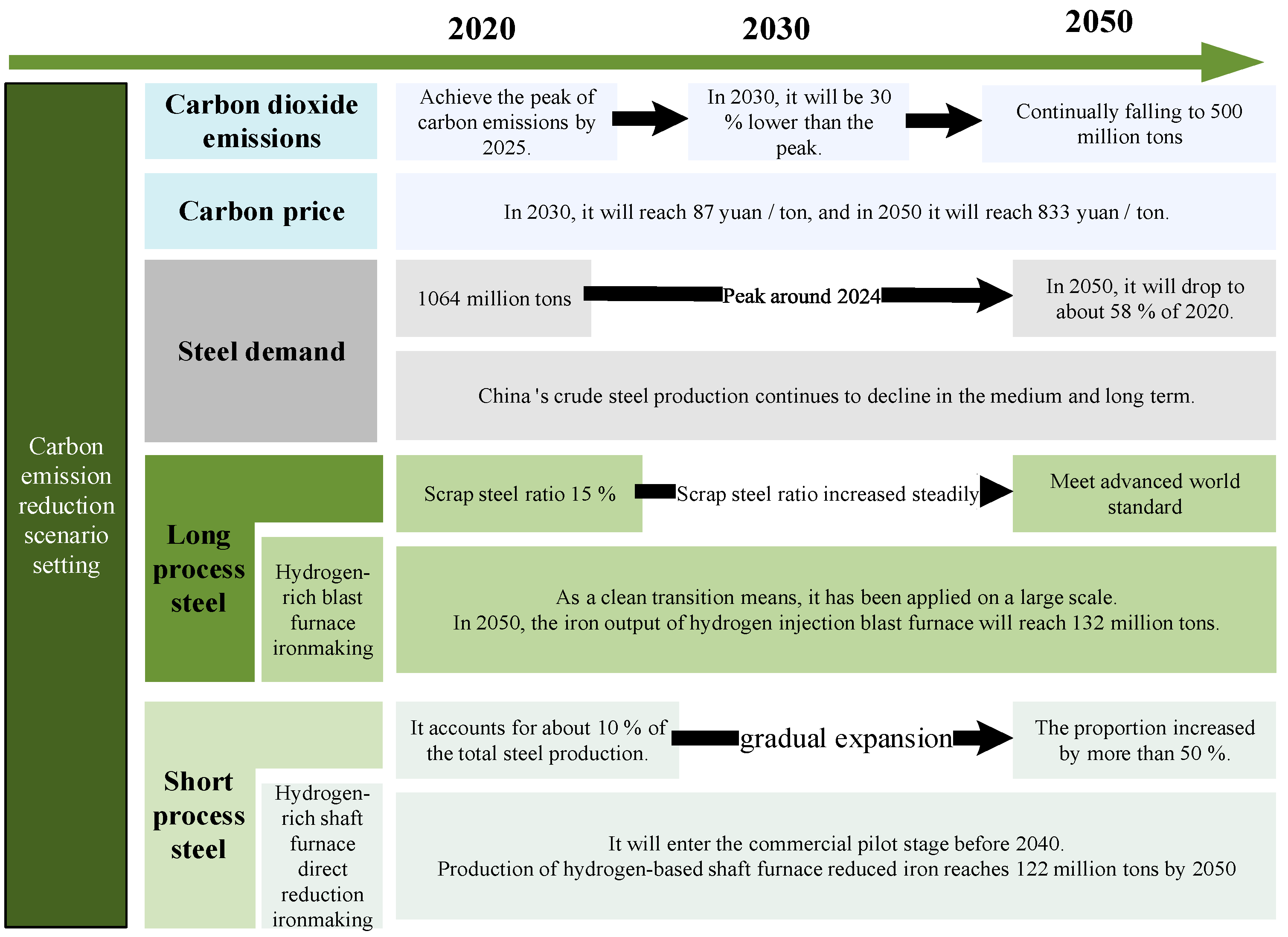

3.4.2. Carbon Emission Reduction Scenario

4. Results and Discussion

4.1. BAU Scenario Results Analysis

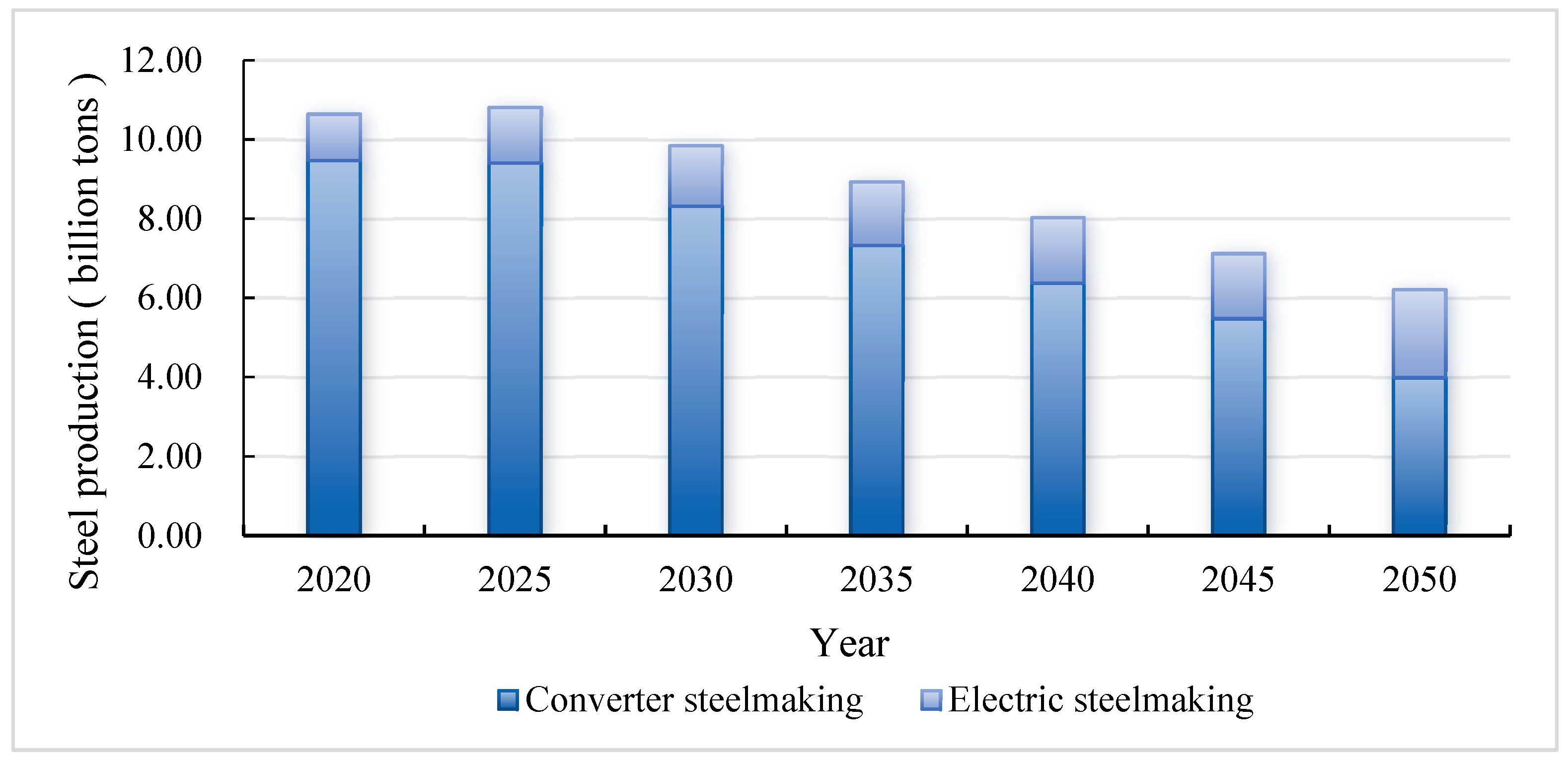

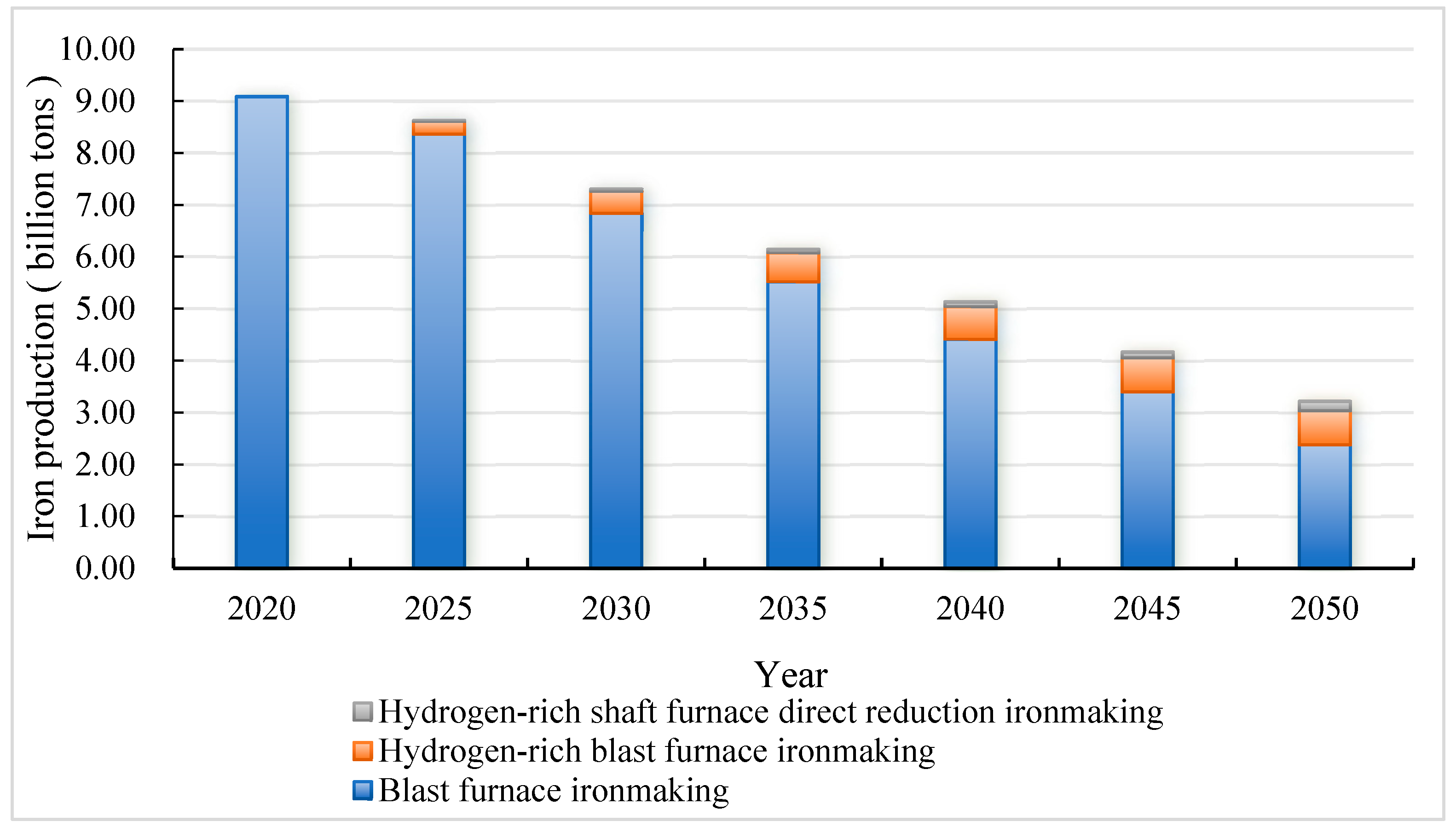

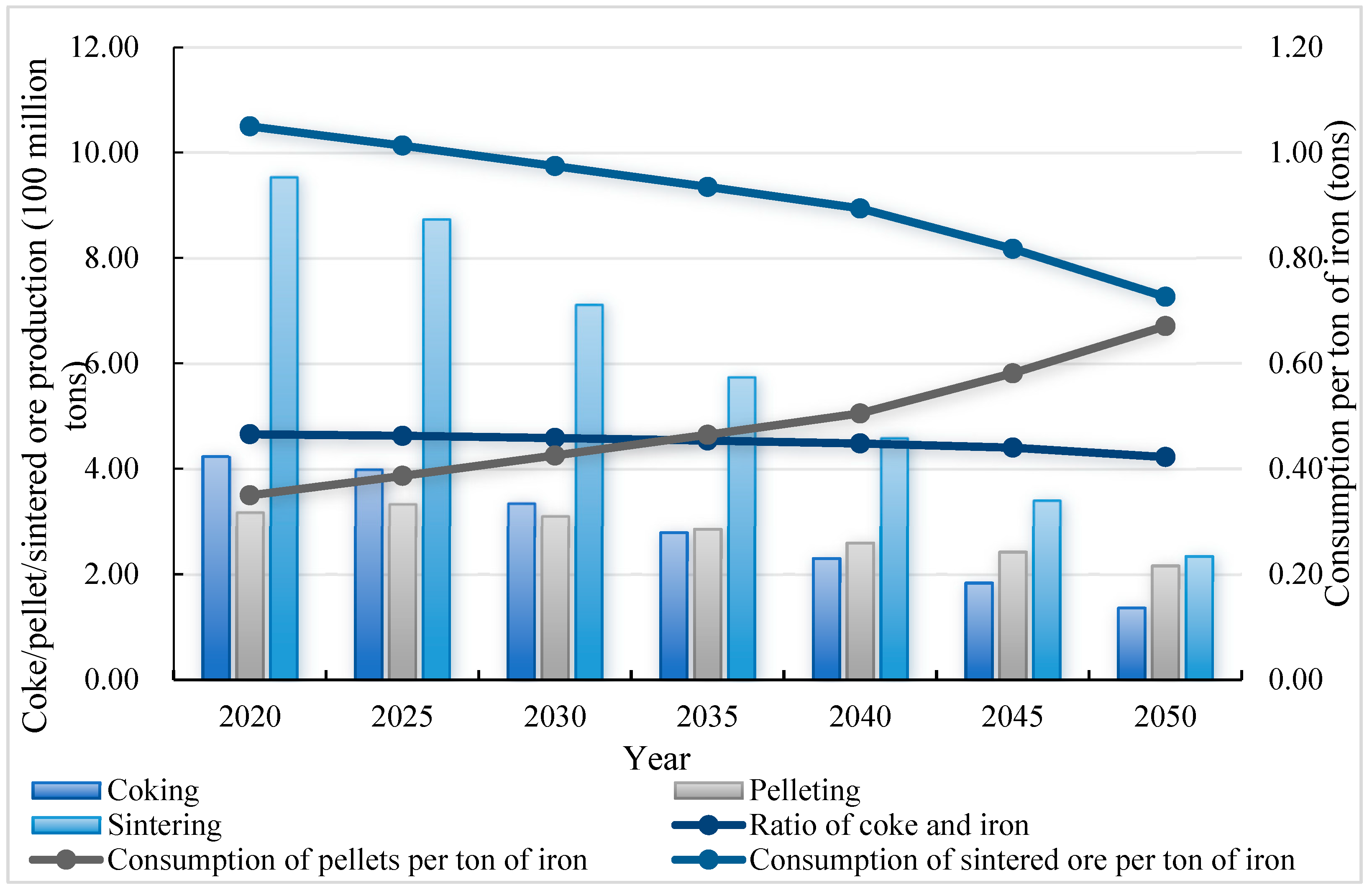

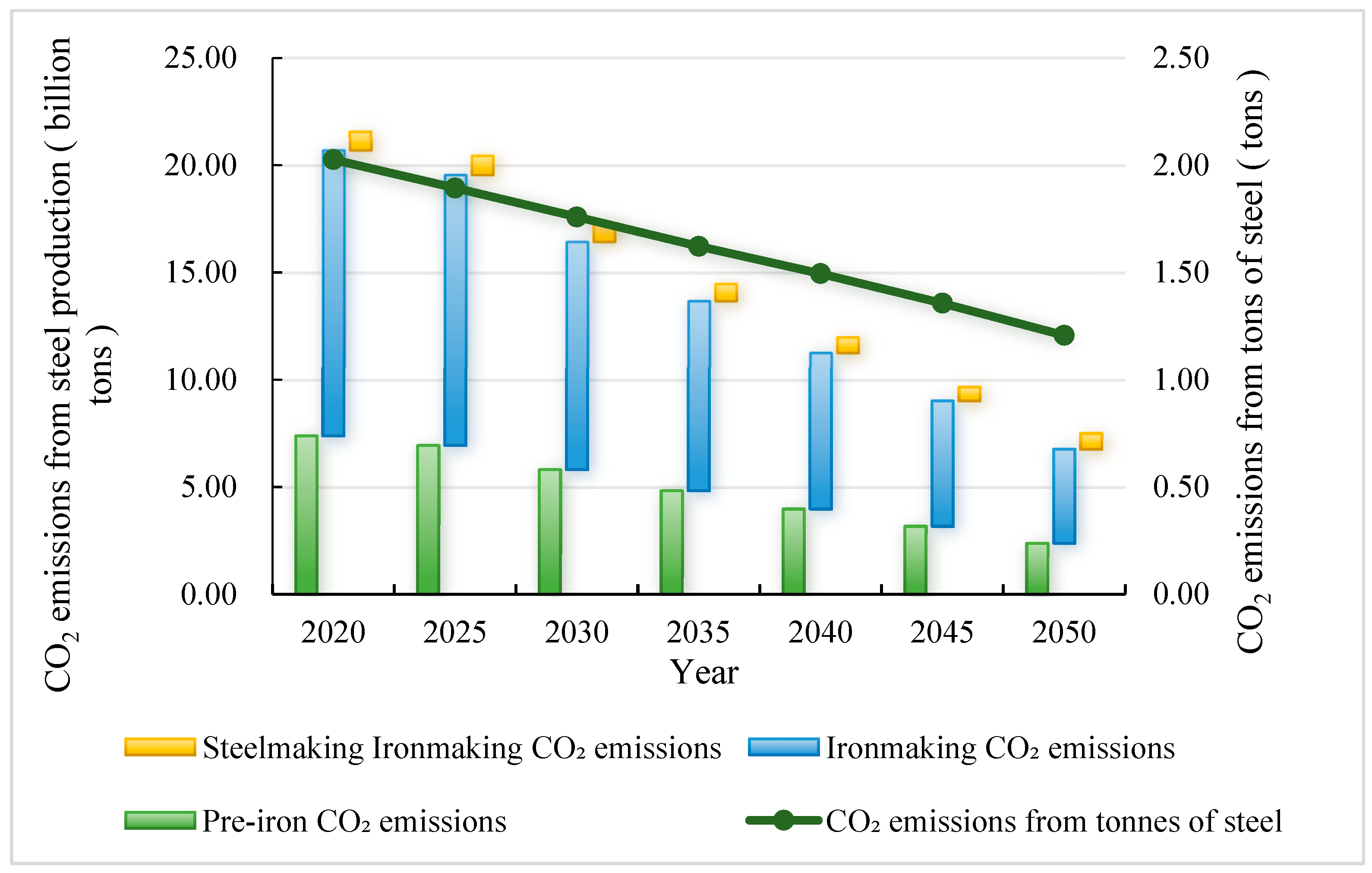

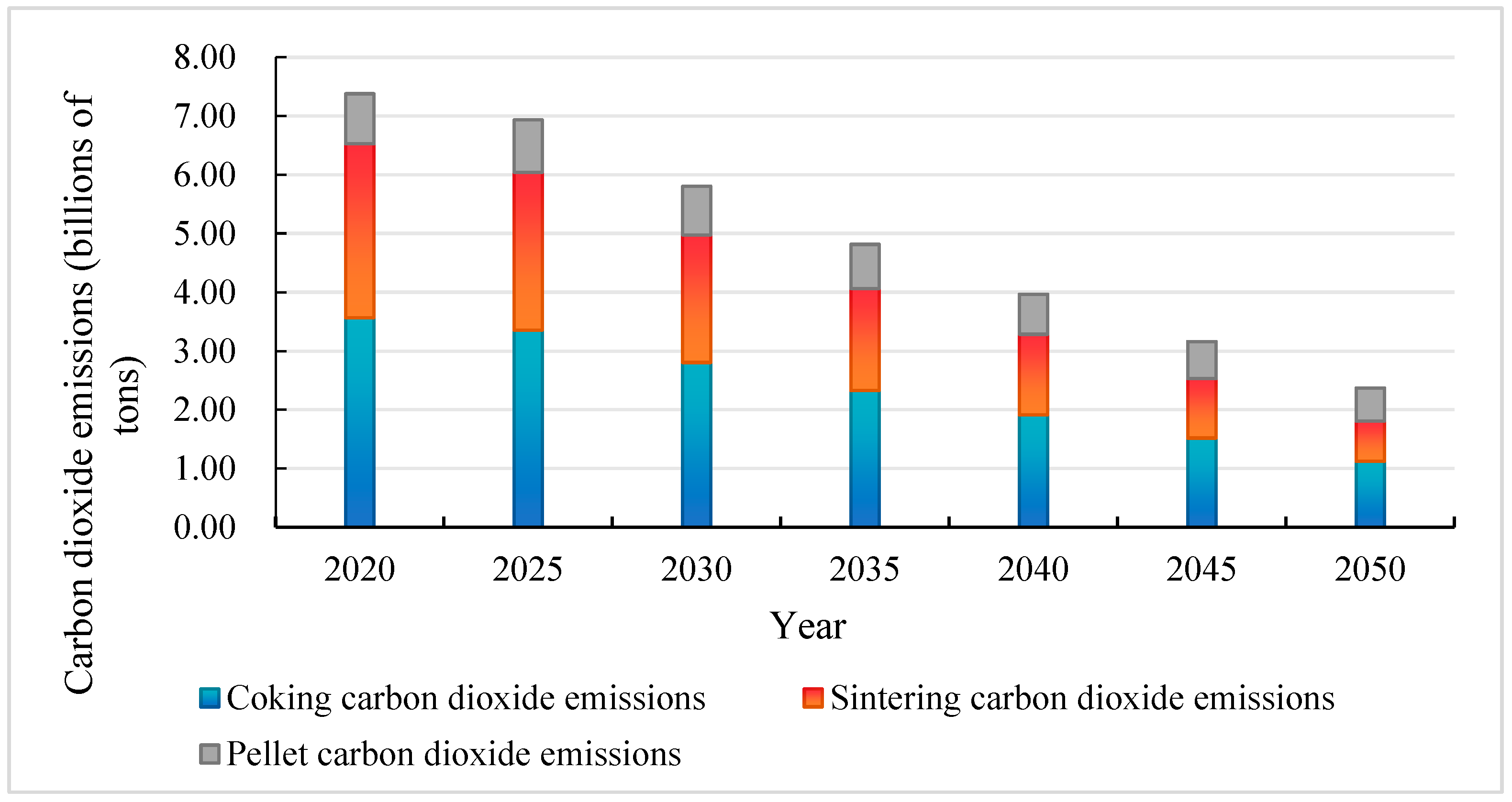

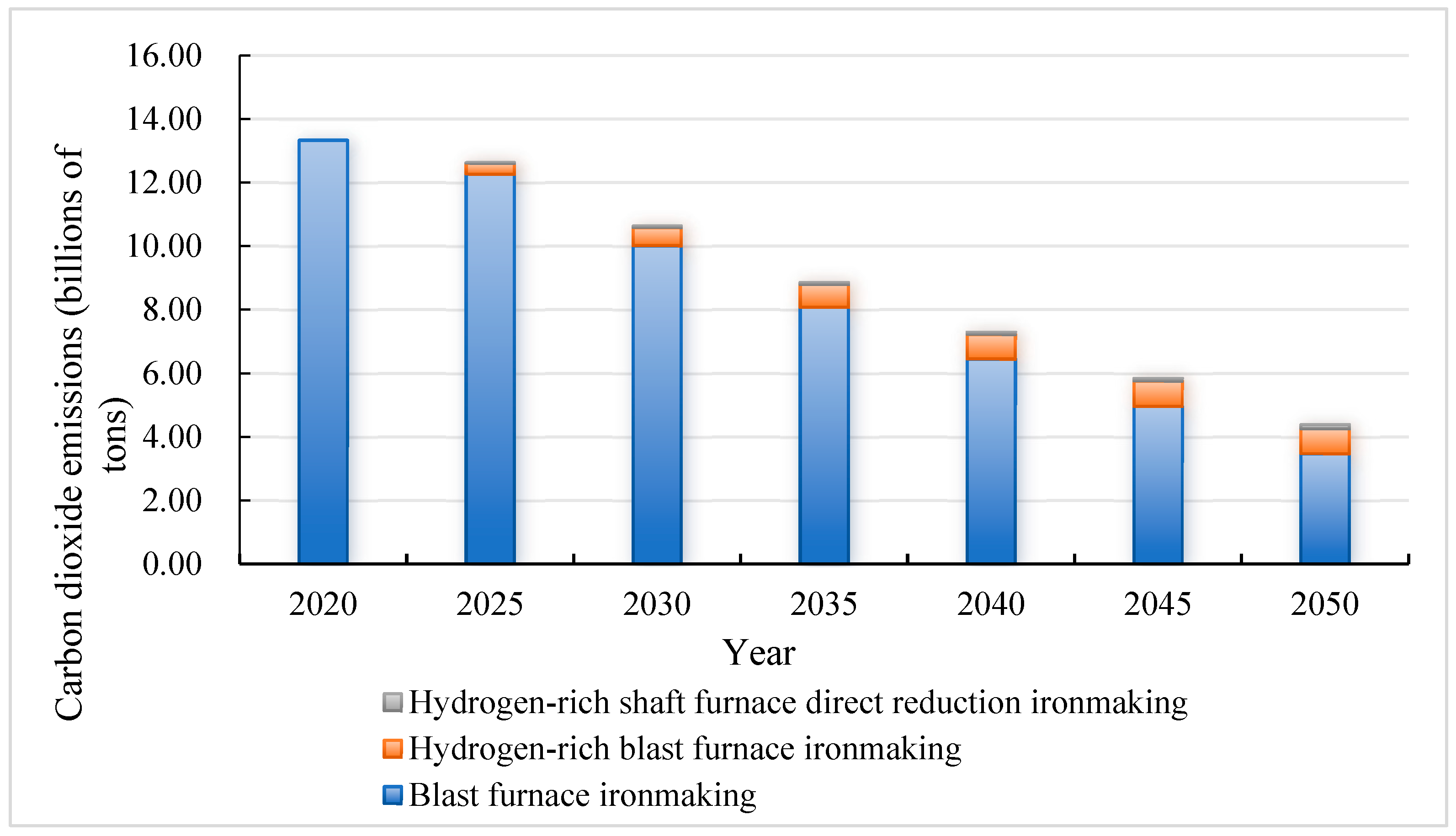

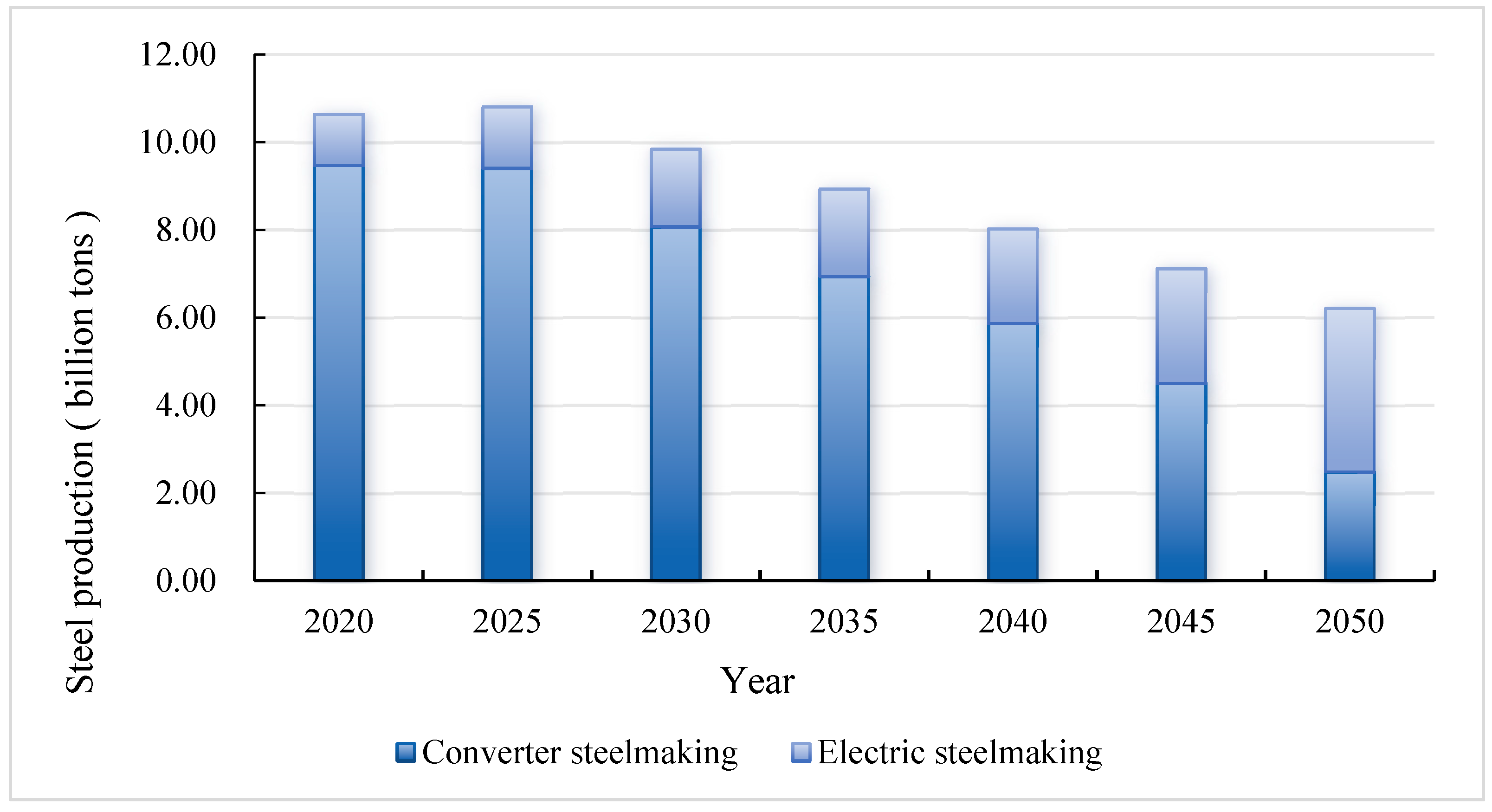

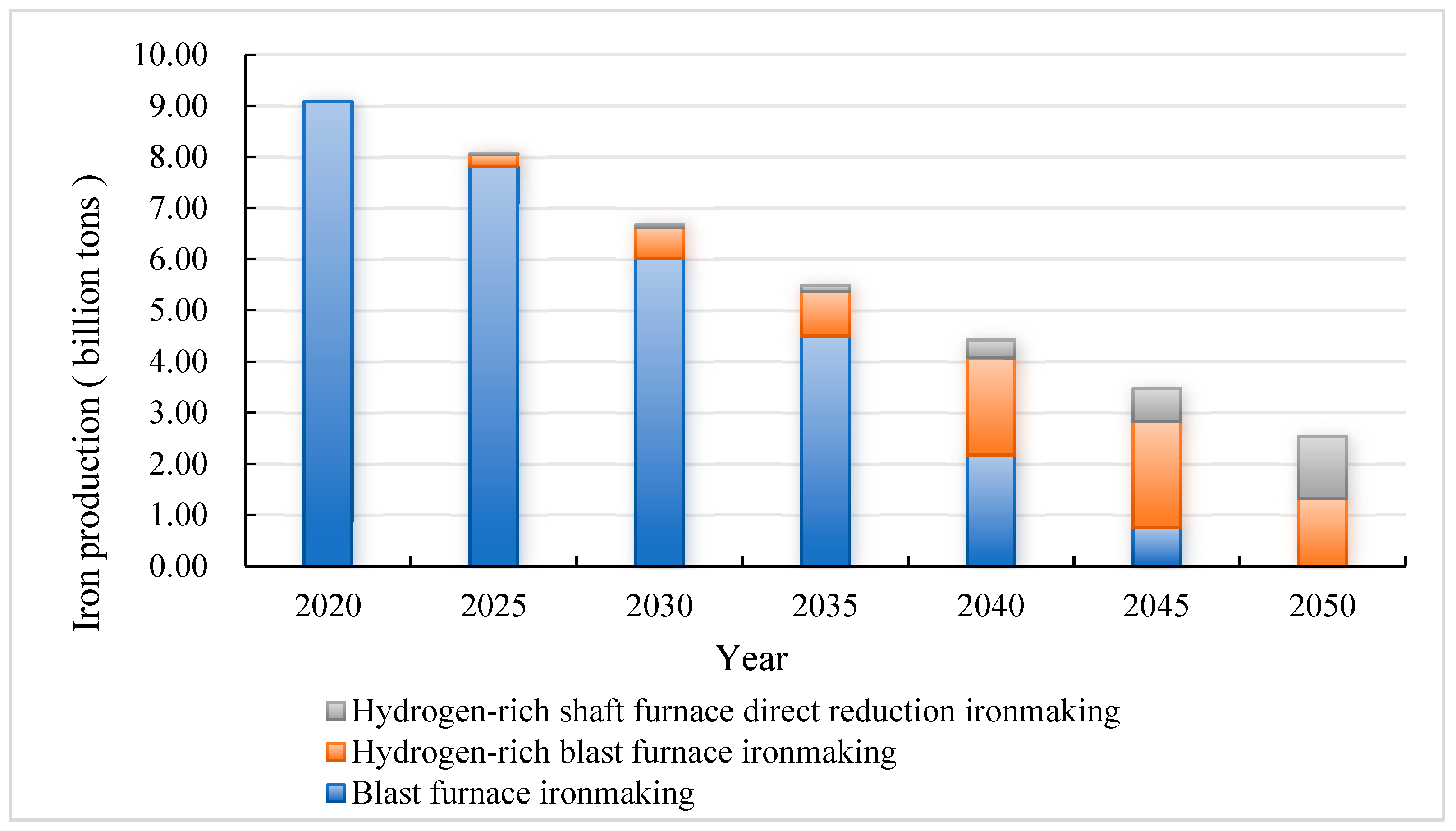

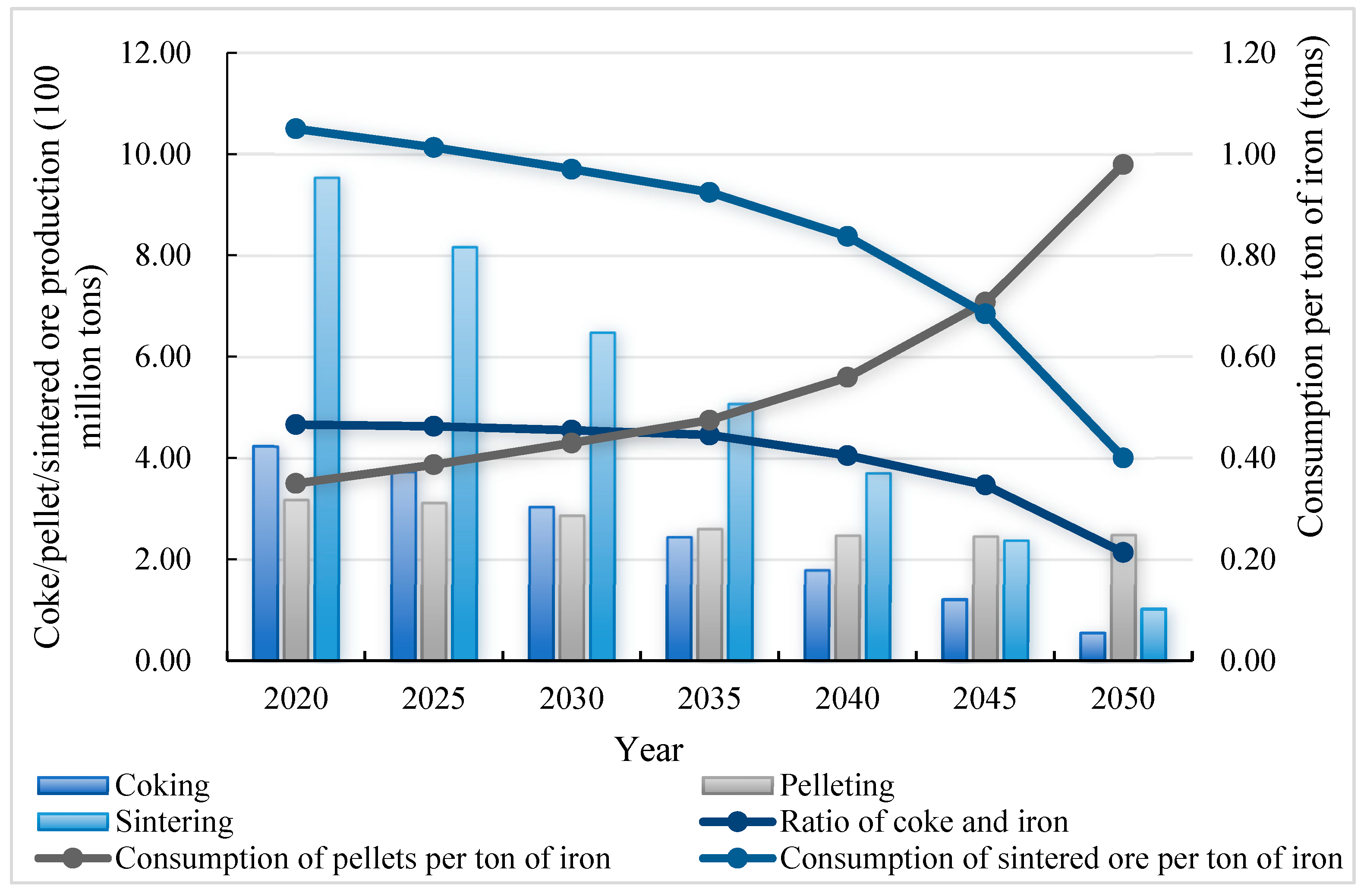

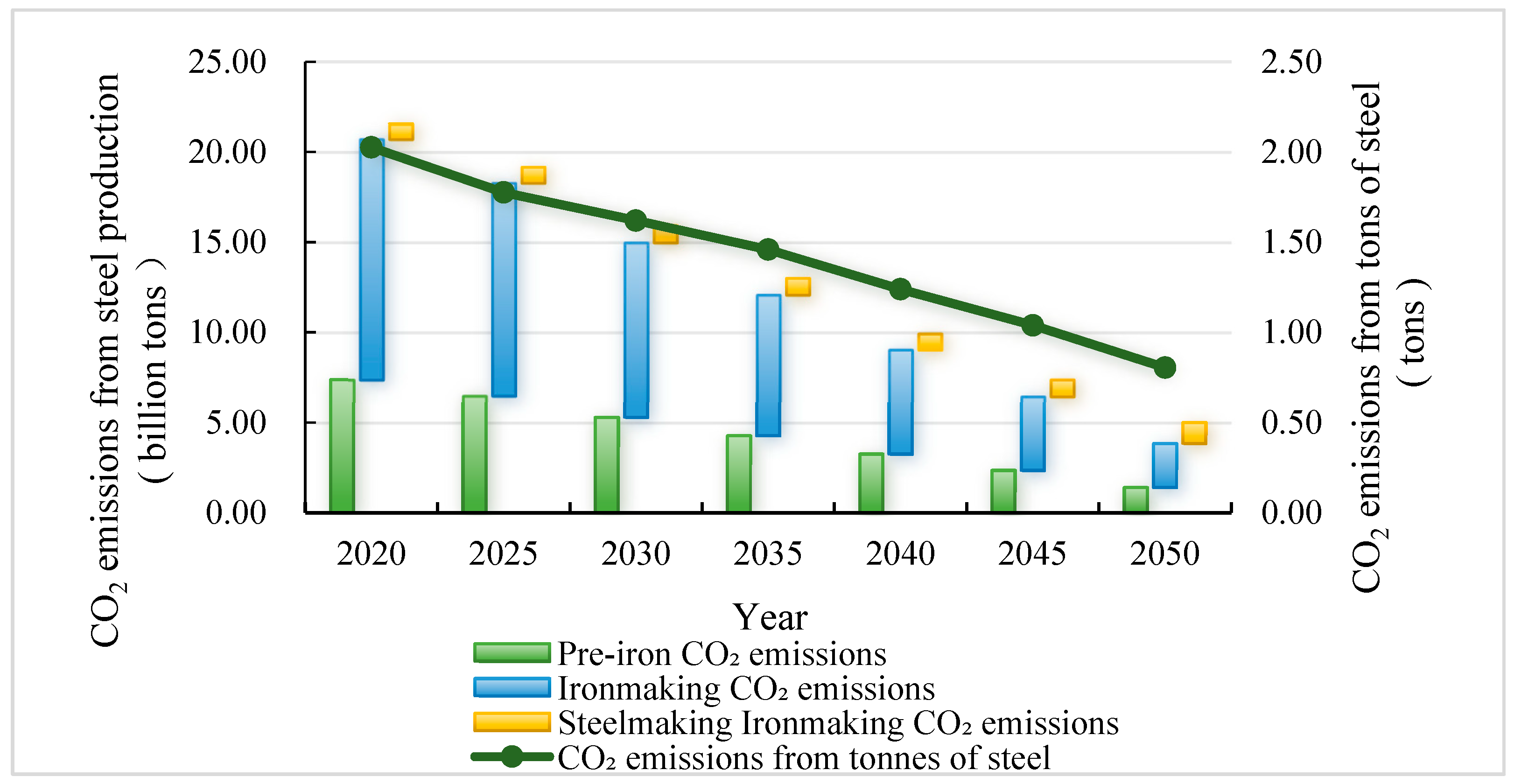

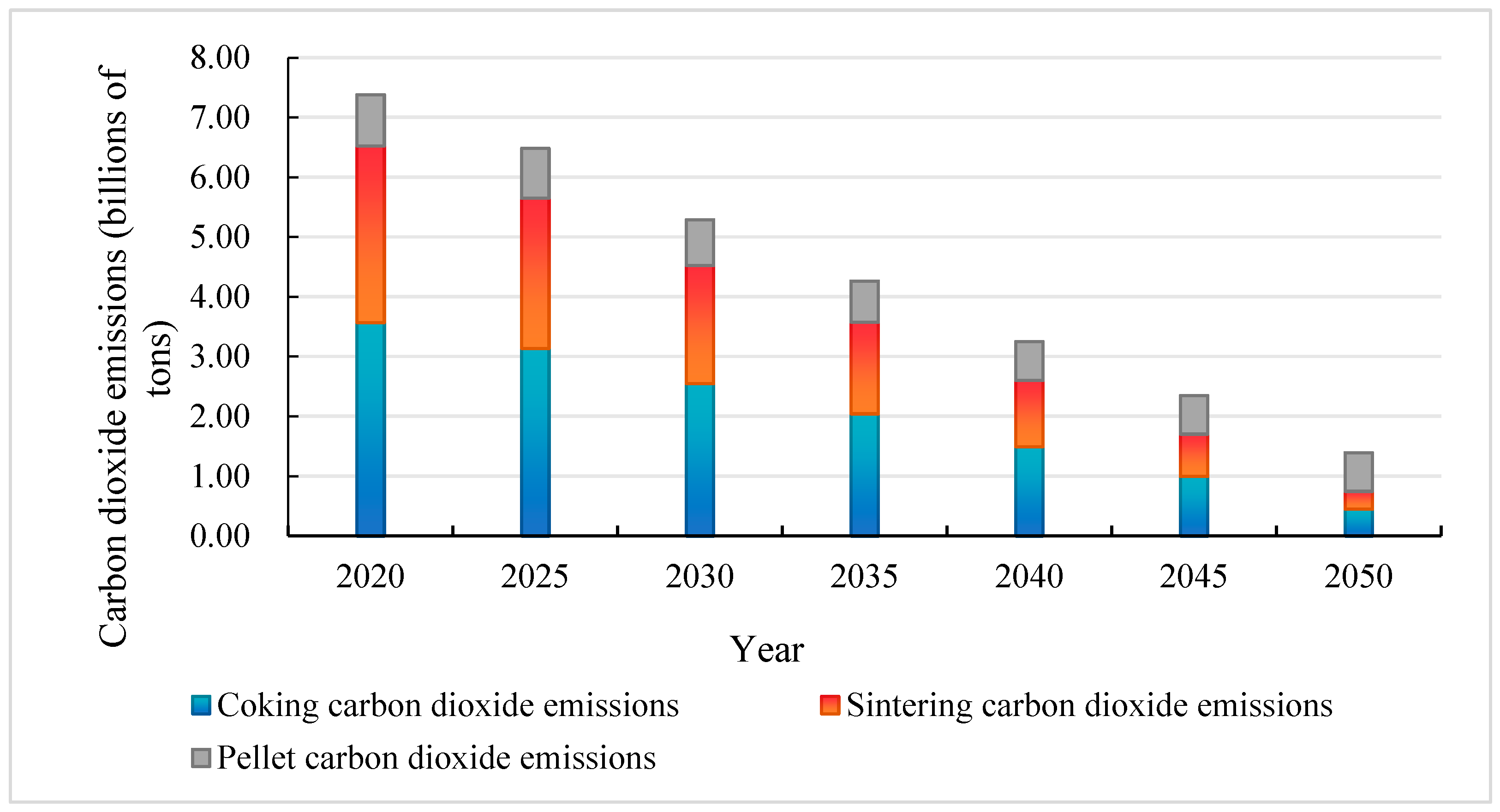

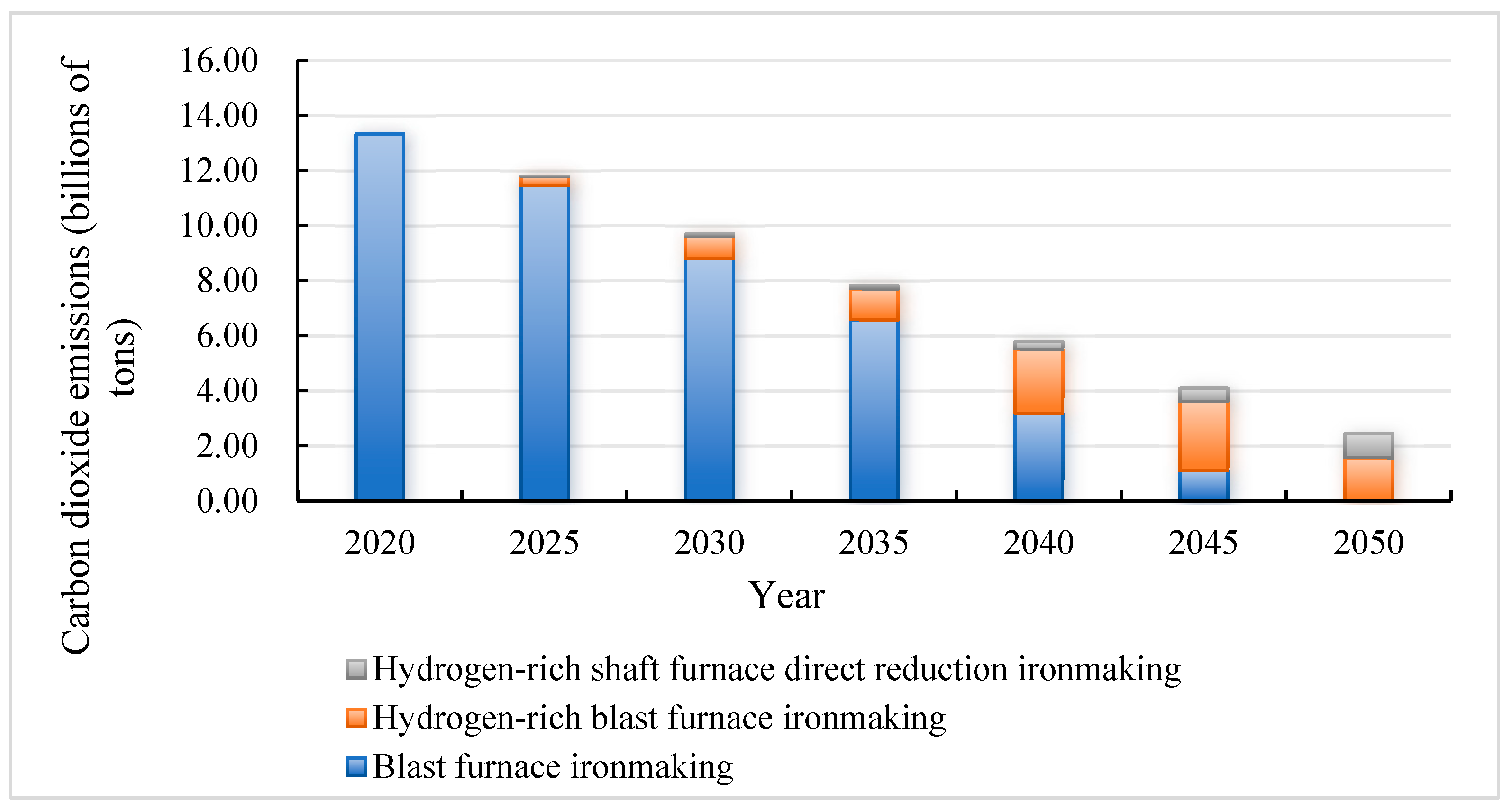

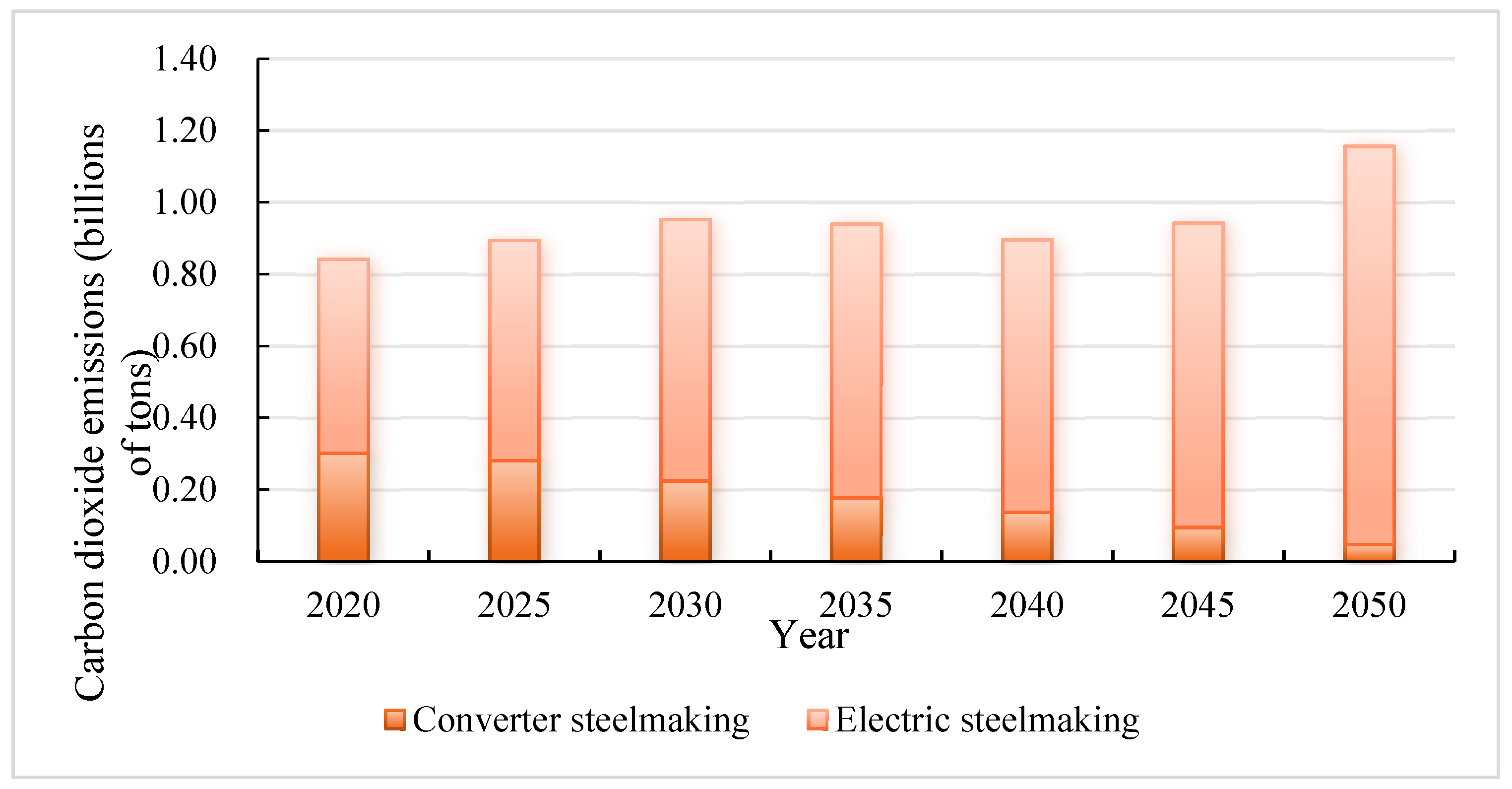

4.1.1. Analysis of Iron and Steel Production Technology Path

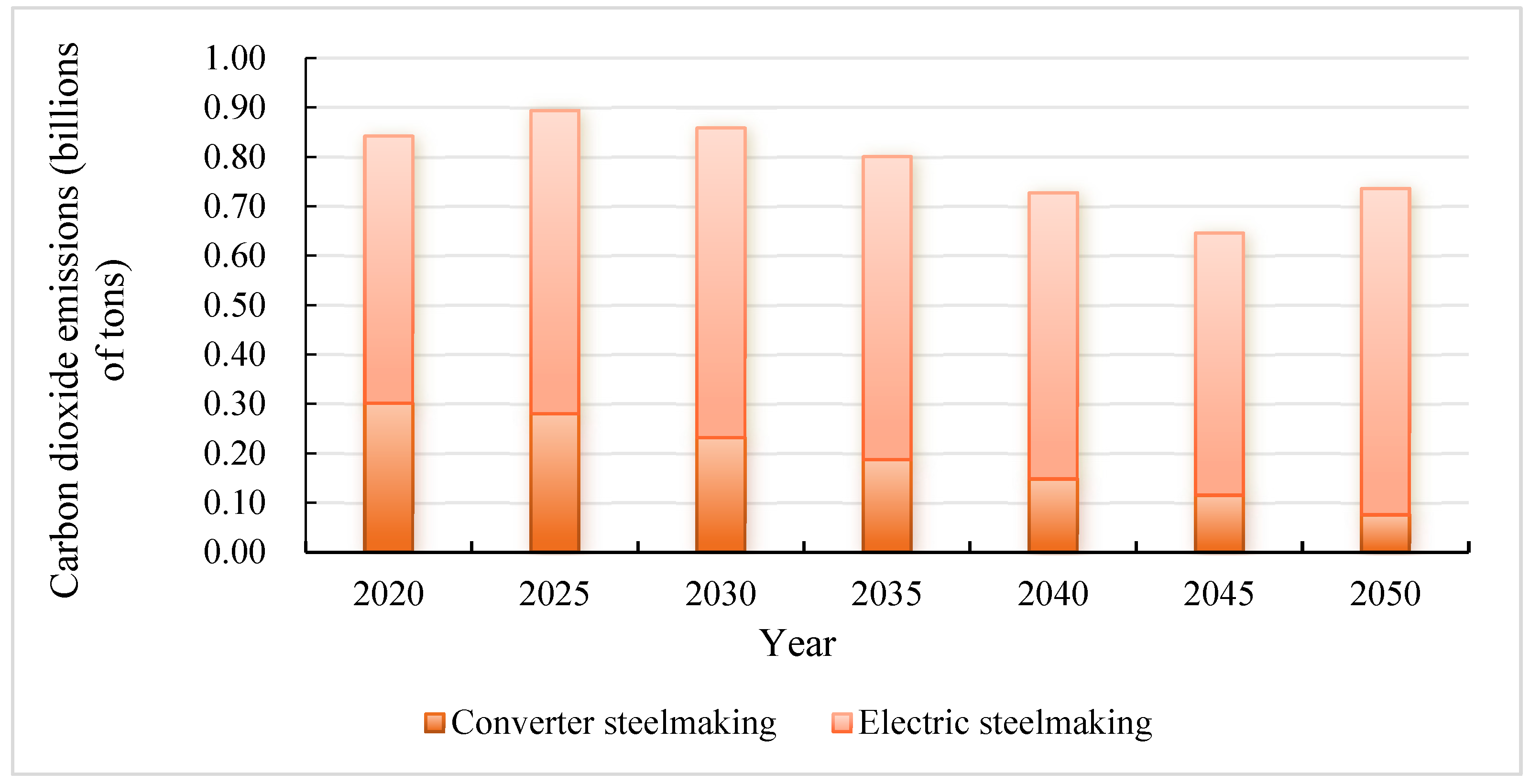

4.1.2. Contribution Analysis of CO2 Emission Reduction in Hydrogen Metallurgy

4.2. Carbon Emission Reduction Scenario Results Analysis

4.2.1. Analysis of the Iron and Steel Production Technology Path

4.2.2. Contribution Analysis of CO2 Emission Reduction in Hydrogen Metallurgy

5. Conclusions

- (1)

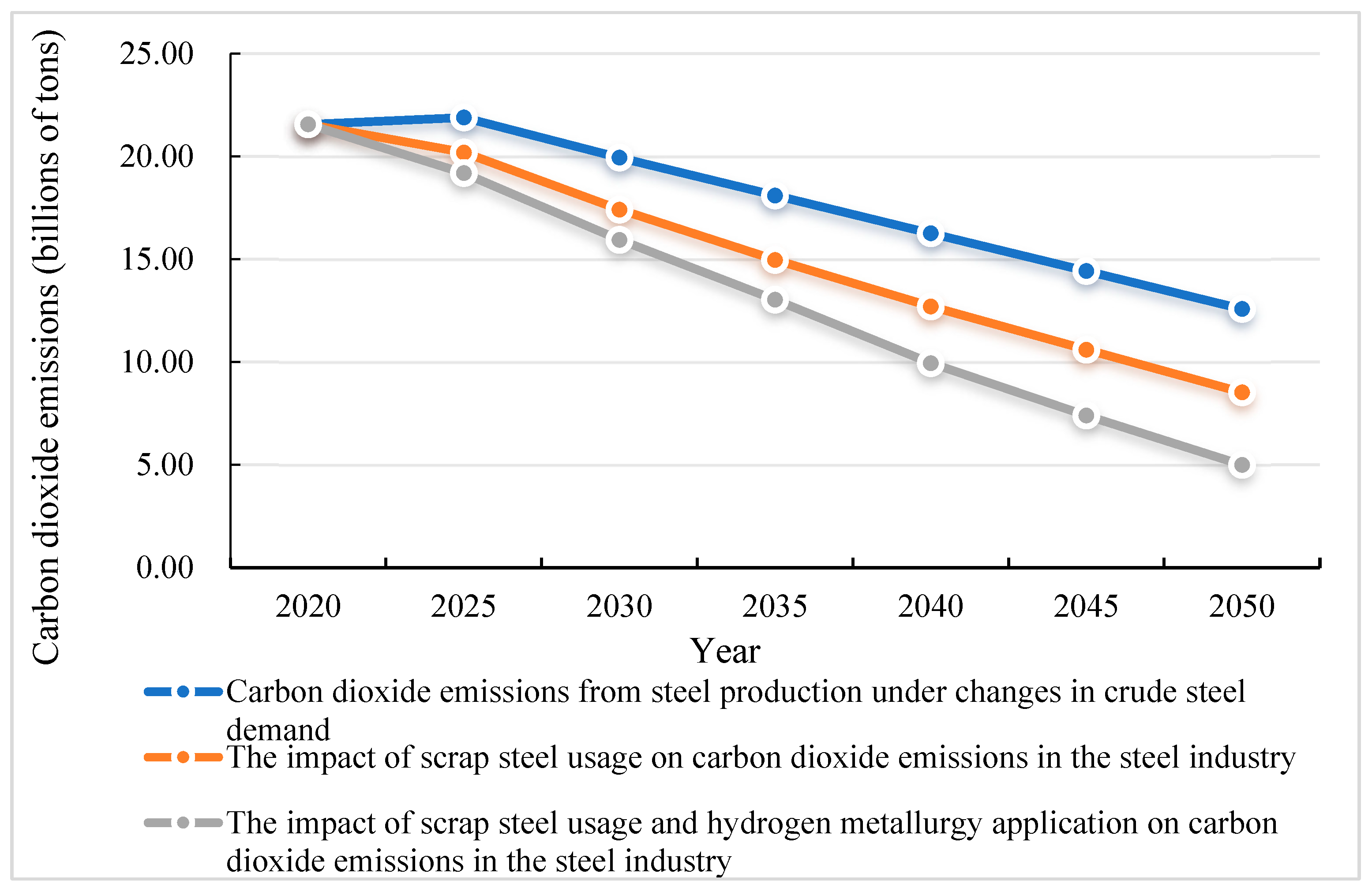

- Reducing steel demand and using scrap steel cannot meet the steel industry’s carbon dioxide emission reduction requirements. The application of hydrogen metallurgy technology is however crucial in the future emission reduction process of the steel industry. In the BAU scenario, the CO2 emissions of the steel industry are reduced, from 2.156 billion tons to 749 million tons, in the period 2020 to 2050. The reduction of steel demand is expected to reduce the CO2 emissions of the steel industry to 1.26 billion tons. The use of scrap steel is expected to reduce emissions by 306 million tons, and the remaining 203 million tons of emission reductions will be achieved by applying hydrogen metallurgy technology. In the carbon emission reduction scenario, steel industry CO2 emissions are expected to be reduced from 2.156 billion tons to 500 million tons in the period 2020 to 2050. The reduction of steel demand is expected to reduce steel industry CO2 emissions to 1.258 billion tons, and the use of scrap steel is expected to, on this basis, reduce emissions by 405 million tons. The remaining 353 million tons of emission reductions will be achieved by applying hydrogen metallurgy technology.

- (2)

- The future application of hydrogen metallurgy technology will rapidly increase demand for hydrogen. In the BAU scenario, the steel industry’s total hydrogen consumption increases to 3.0507 million tons in 2050, and the hydrogen consumption per ton of steel to 491.25 kg/ton. In the carbon emission reduction scenario, the steel industry’s total hydrogen consumption is expected to reach 11.9371 million tons in 2050, and the hydrogen consumption per ton of steel is expected to be 1922.24 kg/ton. However, China’s hydrogen energy industry chain system is not yet complete, as the efficiency of clean energy hydrogen production is low and the cost is high, which highlights the need to increase support for the development of hydrogen energy.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wang, X.Y.; Yu, B.Y.; An, R.Y.; Sun, F.H.; Xu, S. An integrated analysis of China’s iron and steel industry towards carbon neutrality. Appl. Energy 2022, 322, 119453. [Google Scholar] [CrossRef]

- Hasanbeigi, A.; Jiang, Z.; Price, L. Retrospective and prospective analysis of the trends of energy use in Chinese iron and steel industry. J. Clean. Prod. 2014, 74, 105–118. [Google Scholar] [CrossRef]

- Shao, S.; Yang, L.L.; Gan, C.H.; Cao, J.H.; Geng, Y.; Guan, D.B. Using an extended LMDI model to explore techno-economic drivers of energy-related industrial CO2 emission changes: A case study for Shanghai (China). Renew. Sustain. Energy Rev. 2016, 55, 516–536. [Google Scholar] [CrossRef]

- Shao, S.; Liu, J.H.; Geng, Y.; Miao, Z.; Yang, Y.C. Uncovering driving factors of carbon emissions from China’s mining sector. Appl. Energy 2016, 166, 220–238. [Google Scholar] [CrossRef]

- Li, Z.G.; Zhu, Y.M.; Wu, X. GDIM-Based Research on Driving Factors of Carbon Emissions from Manufacturing Industry in Shandong Province. East China Econ. Manag. 2019, 33, 30–36. [Google Scholar]

- Tong, Y.L.; Wang, K.; Liu, J.Y.; Zhang, Y.; Gao, J.J.; Dan, M.; Yue, T.; Zuo, P.L.; Zhao, Z.Y. Refined assessment and decomposition analysis of carbon emissions in high-energy intensive industrial sectors in China. Sci. Total Environ. 2023, 872, 162161. [Google Scholar] [CrossRef] [PubMed]

- Zhou, P.; Ang, B.W. Decomposition of aggregate CO2 emissions: A production-theoretical approach. Energy Econ. 2008, 30, 1054–1067. [Google Scholar] [CrossRef]

- Wang, Z.H.; Yang, L. Delinking indicators on regional industry development and carbon emissions: Beijing–Tianjin–Hebei economic band case. Ecol. Indic. 2015, 48, 41–48. [Google Scholar] [CrossRef]

- Wang, J.F.; He, S.T.; Qiu, Y.; Liu, N.; Li, Y.J.; Dong, Z.F. Investigating driving forces of aggregate carbon intensity of electricity generation in China. Energy Policy 2018, 113, 249–257. [Google Scholar] [CrossRef]

- Feng, K.S.; Davis, S.J.; Sun, L.X.; Hubacek, K. Drivers of the US CO2 emissions 1997–2013. Nat. Commun. 2015, 6, 7714. [Google Scholar] [CrossRef]

- Wei, J.; Huang, K.; Shun, Y.S.; Li, Y.; Hu, T.; Zhang, Y. Driving forces analysis of energy-related carbon dioxide (CO2) emissions in Beijing: An input–output structural decomposition analysis. J. Clean. Prod. 2017, 163, 58–68. [Google Scholar] [CrossRef]

- Zhang, S.H.; Yi, B.W.; Guo, F.; Zhu, P.Y. Exploring selected pathways to low and zero CO2 emissions in China’s iron and steel industry and their impacts on resources and energy. J. Clean. Prod. 2022, 340, 130813. [Google Scholar] [CrossRef]

- An, R.Y.; Yu, B.Y.; Li, R.; Wei, Y.M. Potential of energy savings and CO2 emission reduction in China’s iron and steel industry. Appl. Energy 2018, 226, 862–880. [Google Scholar] [CrossRef]

- Juntueng, S.; Towprayoon, S.; Chiarakorn, S. Energy and carbon dioxide intensity of Thailand’s steel industry and greenhouse gas emission projection toward the year 2050. Resour. Conserv. Recycl. 2014, 87, 46–56. [Google Scholar] [CrossRef]

- United Nations Industrial Development Organization. Industrial Development Report. 2016. Available online: https://www.unido.org/resources-publications-flagship-publications-industrial-development-report-series/industrial-development-report-2016 (accessed on 1 August 2023).

- Tan, X.C.; Li, H.; Guo, J.X.; Gu, B.H.; Zeng, Y. Energy-saving and emission-reduction technology selection and CO2 emission reduction potential of China’s iron and steel industry under energy substitution policy. J. Clean. Prod. 2019, 222, 823–834. [Google Scholar] [CrossRef]

- Klimes, L.; Brezina, M.; Mauder, T.; Charvat, P.; Klemes, J.J.; Stetina, J. Dry cooling as a way toward minimisation of water consumption in the steel industry: A case study for continuous steel casting. J. Clean. Prod. 2020, 275, 123109. [Google Scholar] [CrossRef]

- Ren, M.; Lu, P.T.; Liu, X.R.; Hossain, M.S.; Fang, Y.R.; Hanaoka, T.; O’Gallachoir, B.; Glynn, J.; Dai, H.C. Decarbonizing China’s iron and steel industry from the supply and demand sides for carbon neutrality. Appl. Energy 2021, 298, 117209. [Google Scholar] [CrossRef]

- Quader, M.A.; Ahmed, S.; Ghazilla, R.A.R.; Ahmed, S.; Dahari, M. A comprehensive review on energy efficient CO2 breakthrough technologies for sustainable green iron and steel manufacturing. Renew. Sustain. Energy Rev. 2015, 50, 594–614. [Google Scholar] [CrossRef]

- Liu, X.B.; Gao, X. A survey analysis of low carbon technology diffusion in China’s iron & steel industry. J. Clean. Prod. 2016, 129, 88–101. [Google Scholar]

- Wang, R.R.; Zhao, Y.Q.; Babich, A.; Senk, D.; Fan, X.Y. Hydrogen direct reduction (H-DR) in steel industry—An overview of challenges and opportunities. J. Clean. Prod. 2021, 329, 129797. [Google Scholar] [CrossRef]

- Yilmaz, C.; Wendelstorf, J.; Turek, T. Modeling and simulation of hydrogen injection into a blast furnace to reduce carbon dioxide emissions. J. Clean. Prod. 2017, 154, 488–501. [Google Scholar] [CrossRef]

- Weigel, M.; Fischedick, M.; Marzinkowski, J.; Winzer, P. Multicriteria analysis of primary steelmaking technologies. J. Clean. Prod. 2016, 112, 1064–1076. [Google Scholar] [CrossRef]

- Mohsenzadeh, F.M.; Payab, H.; Abedi, Z.; Abdoli, M.A. Reduction of CO2 emissions and energy consumption by improving equipment in direct reduction ironmaking plant. Clean Technol. Environ. Policy 2019, 21, 847–860. [Google Scholar] [CrossRef]

- Bhaskar, A.; Assadi, M.; Somehsaraei, H.N. Decarbonization of the iron and steel industry with direct reduction of iron ore with green hydrogen. Energies 2020, 13, 758. [Google Scholar] [CrossRef]

- Li, F.; Chu, M.S.; Tang, J.; Liu, Z.G.; Zhao, Z.C.; Liu, P.J.; Yan, R.J. Quantifying the energy saving potential and environmental benefit of hydrogen-based steelmaking process: Status and future prospect. Appl. Therm. Eng. 2022, 211, 118489. [Google Scholar] [CrossRef]

- Chen, Q.Q.; Gu, Y.; Tang, Z.Y.; Wei, W.; Sun, Y. Assessment of low-carbon iron and steel production with CO2 recycling and utilization technologies: A case study in China. Appl. Energy 2018, 220, 192–207. [Google Scholar] [CrossRef]

- Li, F.; Chu, M.; Tang, J.; Liu, Z.; Wang, J.; Li, S. Life-cycle assessment of the coal gasification-shaft furnace-electric furnace steel production process. J. Clean. Prod. 2021, 287, 125075. [Google Scholar] [CrossRef]

- Rechberger, K.; Spanlang, A.; Conde, A.S.; Wolfmeir, H.; Harris, C. Green Hydrogen-Based Direct Reduction for Low-Carbon Steelmaking. Steel Res. Int. 2020, 91, 2000110. [Google Scholar] [CrossRef]

- Wen, Z.G.; Wang, Y.H.; Li, H.F.; Tao, Y.; De Clercq, D. Quantitative analysis of the precise energy conservation and emission reduction path in China’s iron and steel industry. J. Environ. Manag. 2019, 246, 717–729. [Google Scholar] [CrossRef]

- Yan, J.J. Progress and future of ultra-low CO2 steel making program. China Metall. 2017, 27, 6–11. (In Chinese) [Google Scholar]

- Zhang, P.; Wang, L.; Chen, S.; Xu, J. Progress of nuclear hydrogen production through the iodine-sulfur process in China. Renew. Sustain. Energy Rev. 2018, 81, 1802–1812. [Google Scholar]

- Chang, Y.F.; Wan, F.; Yao, X.L.; Wang, J.X.; Han, Y.F.; Li, H. Influence of hydrogen production on the CO2 emissions reduction of hydrogen metallurgy transformation in iron and steel industry. Energy Rep. 2023, 9, 3057–3071. [Google Scholar] [CrossRef]

- Hugues, P.; Assoumou, E.; Maizi, N. Assessing GHG mitigation and associated cost of French biofuel sector: Insights from a TIMES model. Energy 2016, 113, 288–300. [Google Scholar] [CrossRef]

- Postic, S.; Selosse, S.; Maïzi, N. Energy contribution to Latin American INDCs: Analyzing sub-regional trends with a TIMES model. Energy Policy 2017, 101, 170–184. [Google Scholar] [CrossRef]

- Lu, L.W.; Preckel, P.V.; Gotham, D.; Liu, A.L. An assessment of alternative carbon mitigation policies for achieving the emissions reduction of the Clean Power Plan: Case study for the state of Indiana. Energy Policy 2016, 96, 661–672. [Google Scholar] [CrossRef]

- Aitken, M.L.; Loughlin, D.H.; Dodder, R.S.; Yelverton, W.H. Economic and environmental evaluation of coal-and-biomass-to-liquids-and-electricity plants equipped with carbon capture and storage. Clean Technol. Environ. Policy 2016, 18, 573–581. [Google Scholar] [CrossRef]

- Rocky Mountain Institute. Pursuing Zero-Carbon Steel in China. 2021. Available online: https://rmi.org/insight/pursuing-zero-carbon-steel-in-china/ (accessed on 23 August 2023).

- Chang, Y.F.; Wan, F.; Li, J.R.; Liu, N.; Yao, X. The impact of cautious coal power phase-out on decarbonization of China’s iron and steel industry. J. Clean. Prod. 2023, 397, 136447. [Google Scholar] [CrossRef]

- Fan, Z.Y.; Friedmann, S.J. Low-carbon production of iron and steel: Technology options, economic assessment, and policy. Joule 2021, 5, 829–862. [Google Scholar] [CrossRef]

- Wang, X.D.; Li, J.X.; Hu, Q.C. Application practice of source and process sulfur-nitrate reduction technology based on optimization of blast furnace charge structure. Iron Steel 2019, 54, 104–110. [Google Scholar]

- Wang, X.D.; Jin, Y.L. Prospect on high ratio pellet utilized in blast furnace under the backgroundof carbon peaking and carbon neutrality. Chin. J. Process Eng. 2022, 22, 1379–1389. [Google Scholar]

- Institute of Climate Change and Sustainable Development Tsinghua University. Understanding Carbon Neutrality: China’s 2020–2050 Low-Carbon Development Action Road Map; China Citic Press: Beijing, China, 2021. (In Chinese) [Google Scholar]

- Rocky Mountain Institute. The Zero Carbon Path of Chinese Steel under the Goal of Carbon Neutrality; Rocky Mountain Institute: Beijing, China, 2021. (In Chinese) [Google Scholar]

- DNV. Hydrogen Forecast to 2050. 2022. Available online: https://www.dnv.com/focus-areas/hydrogen/forecast-to-2050.html (accessed on 28 August 2023).

- China Hydrogen Alliance. White Paper on China’s Hydrogen Energy and Fuel Cell Industry; China Hydrogen Alliance: Beijing, China, 2019. (In Chinese) [Google Scholar]

- China Electric Vehicle Hundred People Association. China Hydrogen Industry Development Report 2020; China Electric Vehicle Hundred People Association: Beijing, China, 2020. (In Chinese) [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technology | The Main Energy and Raw Materials Input per Unit Product | |||||||

|---|---|---|---|---|---|---|---|---|

| Sintering | Anthracite coal (tce/t sinter) | Iron ore (t/t sinter) | Electricity (kWh/t sinter) | Coke crumbs (tce/t sinter) | Limestone (t/t sinter) | |||

| 0.030 | 0.882 | 45.040 | 0.027 | 0.140 | ||||

| Pelletizing | Raw coal (tce/t pellet) | Iron ore (t/t pellet) | Electricity (kWh/t pellet) | Diesel (tce/t pellet) | Gasoline (tce/t pellet) | Fuel oil (tce/t pellet) | ||

| 0.022 | 1.042 | 24.863 | 0.002 | 0.0004 | 0.002 | |||

| Coking | Washed coal (tce/t coke) | Electricity (kWh/t coke) | ||||||

| 1.017 | 47.326 | |||||||

| Reduction of gas preparation and heating | H2 (m3/m3 reducing gas) | Natural Gas (m3/m3 reducing gas) | Electricity (kWh/m3 reducing gas) | |||||

| 0.570 | 0.142 | 0.007 | ||||||

| Ironmaking: | ||||||||

| Blast furnace ironmaking | Coal and fuel injection (tce/t molten iron) | Coke (t/t molten iron) | Electricity (kwh/t molten iron) | Pellet (t/t molten iron) | Sinter (t/t molten iron) | |||

| 0.134 | 0.437 | 23.648 | 0.360 | 1.040 | ||||

| Hydrogen-rich blast furnace ironmaking | H2 (m3/t molten iron) | Coke (t/t molten iron) | Electricity (kwh/t molten iron) | Pellet (t/t molten iron) | Sinter (t/t molten iron) | |||

| 305.911 | 0.390 | 23.648 | 0.360 | 1.040 | ||||

| Hydrogen-rich shaft furnace–direct reduction ironmaking | Heated reducing gas (m3/t DRI) | Natural Gas (m3/t DRI) | Electricity (kWh/t DRI) | Pellet (t/t DRI) | ||||

| 1326.321 | 41.42 | 19.211 | 1.357 | |||||

| Steelmaking: | ||||||||

| Electric steelmaking | molten iron (t/t Crude steel) | Scrap (t/t Crude steel) | Electricity (kWh/t Crude steel) | Limestone (t/t Crude steel) | ||||

| 0.965 | 0.130 | 36.830 | 0.049 | |||||

| Converter steelmaking | DRI (t/t Crude steel) | Scrap (t/t Crude steel) | Electricity (kWh/t Crude steel) | |||||

| 0.306 | 0.714 | 470.6 | ||||||

| 2025 | 2030 | 2035 | 2040 | 2045 | 2050 | |

|---|---|---|---|---|---|---|

| Proportion of pellets in blast furnace burden | 28–30% | 30–35% | 33–40% | 35–45% | 40–55% | 45–60% |

| Technology | Efficiency (%) | Power Structure for 2020 (%) |

|---|---|---|

| Supercritical coal power generation | 41.00 | 63.38 |

| Supercritical coal power generation + CCS | 41.00 | — |

| Combined gas-steam cycle power generation | 60.00 | 2.57 |

| Hydropower | — | 18.11 |

| Third generation nuclear power generation | 38.00 | 5.41 |

| Biomass power generation | 28.00 | 1.08 |

| Onshore wind | — | 5.68 |

| Offshore wind | — | 0.27 |

| Distributed photovoltaic | — | 0.68 |

| Centralized photovoltaic | — | 2.84 |

| Technology | Efficiency (%) | Hydrogen Energy Supply Structure (%) | |

|---|---|---|---|

| Coal gasification | 63.00 | 62.00 | |

| Coal gasification with CCS | 58.00 | — | |

| Methane reforming | 71.00 | 19.00 | |

| Methane reforming with CCS | 74.00 | — | |

| Industrial by-products | — | 18.00 | |

| Electrolysis | Grid connected electrolysis | 4.70 Kwh/m3 | 1.00 |

| Dedicated solar electrolysis | — | ||

| Dedicated wind electrolysis | — | ||

| Dedicated nuclear electrolysis | — | ||

| 2020 | 2020–2025 | 2026–2035 | 2036–2050 | |

|---|---|---|---|---|

| The cost of hydrogen energy production | Coal to hydrogen Without CCUS: 6–12 yuan/kg With CCUS: 25.8–32.1 yuan/kg | Develop hydrogen production routes according to local conditions; actively use industrial by-product hydrogen; and vigorously develop renewable energy electrolytic water hydrogen production demonstration. The average cost of hydrogen production is not more than 20 yuan/kg. | Actively develop large-scale renewable energy electrolysis of water to produce hydrogen and coal to produce hydrogen centralized hydrogen supply; the average cost of hydrogen production is not higher than 15 yuan/kg. | Sustainable use of renewable energy electrolysis of water to produce hydrogen; vigorously develop biological hydrogen production, solar water splitting to produce hydrogen, and ‘green’ coal to produce hydrogen technology. The average cost of hydrogen production is not more than 10 yuan/kg. |

| Hydrogen production from natural gas 7.5–24.3 yuan/kg (without CCUS) | ||||

| Industrial by-product hydrogen 14.6–26.9 yuan/kg | ||||

| Hydrogen production by electrolysis of water Alkaline electrolysis: 9.2–40 yuan/kg PEM electrolysis: 20.5–48.5 yuan/kg (Electricity price 0.1–0.6 yuan/kWh) |

| Technical Name | Carbon Dioxide Emission Coefficient per Unit Product (kg CO2/t) |

|---|---|

| Sintering | 284.02 |

| Pelleting | 254.21 |

| Coking | 816.38 |

| Preparation and heating of reducing gas | 0.29 |

| Scrap returns | 2.97 |

| Ironmaking | |

| Blast furnace ironmaking | 1454.01 |

| Hydrogen-rich blast furnace ironmaking | 1061.73 |

| Hydrogen-rich shaft furnace–direct reduction ironmaking | 21.96 |

| Steel making | |

| Converter steelmaking | 10.80 |

| Electric steelmaking | 193.34 |

| 2020 | 2025 | 2030 | 2040 | 2050 | |

|---|---|---|---|---|---|

| Carbon emission coefficient of power generation (kg/kwh) | 0.571 | 0.517 | 0.463 | 0.338 | 0.221 |

| Carbon emission coefficient of hydrogen production (kg/m3) | 1.194 | 1.053 | 0.903 | 0.516 | 0.407 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wan, F.; Li, J.; Han, Y.; Yao, X. Research of the Impact of Hydrogen Metallurgy Technology on the Reduction of the Chinese Steel Industry’s Carbon Dioxide Emissions. Sustainability 2024, 16, 1814. https://doi.org/10.3390/su16051814

Wan F, Li J, Han Y, Yao X. Research of the Impact of Hydrogen Metallurgy Technology on the Reduction of the Chinese Steel Industry’s Carbon Dioxide Emissions. Sustainability. 2024; 16(5):1814. https://doi.org/10.3390/su16051814

Chicago/Turabian StyleWan, Fang, Jizu Li, Yunfei Han, and Xilong Yao. 2024. "Research of the Impact of Hydrogen Metallurgy Technology on the Reduction of the Chinese Steel Industry’s Carbon Dioxide Emissions" Sustainability 16, no. 5: 1814. https://doi.org/10.3390/su16051814

APA StyleWan, F., Li, J., Han, Y., & Yao, X. (2024). Research of the Impact of Hydrogen Metallurgy Technology on the Reduction of the Chinese Steel Industry’s Carbon Dioxide Emissions. Sustainability, 16(5), 1814. https://doi.org/10.3390/su16051814