Blueprints to Benefits: Towards an Index to Measure the Impact of Sustainable Product Development on the Firm’s Bottom Line

Abstract

1. Introduction

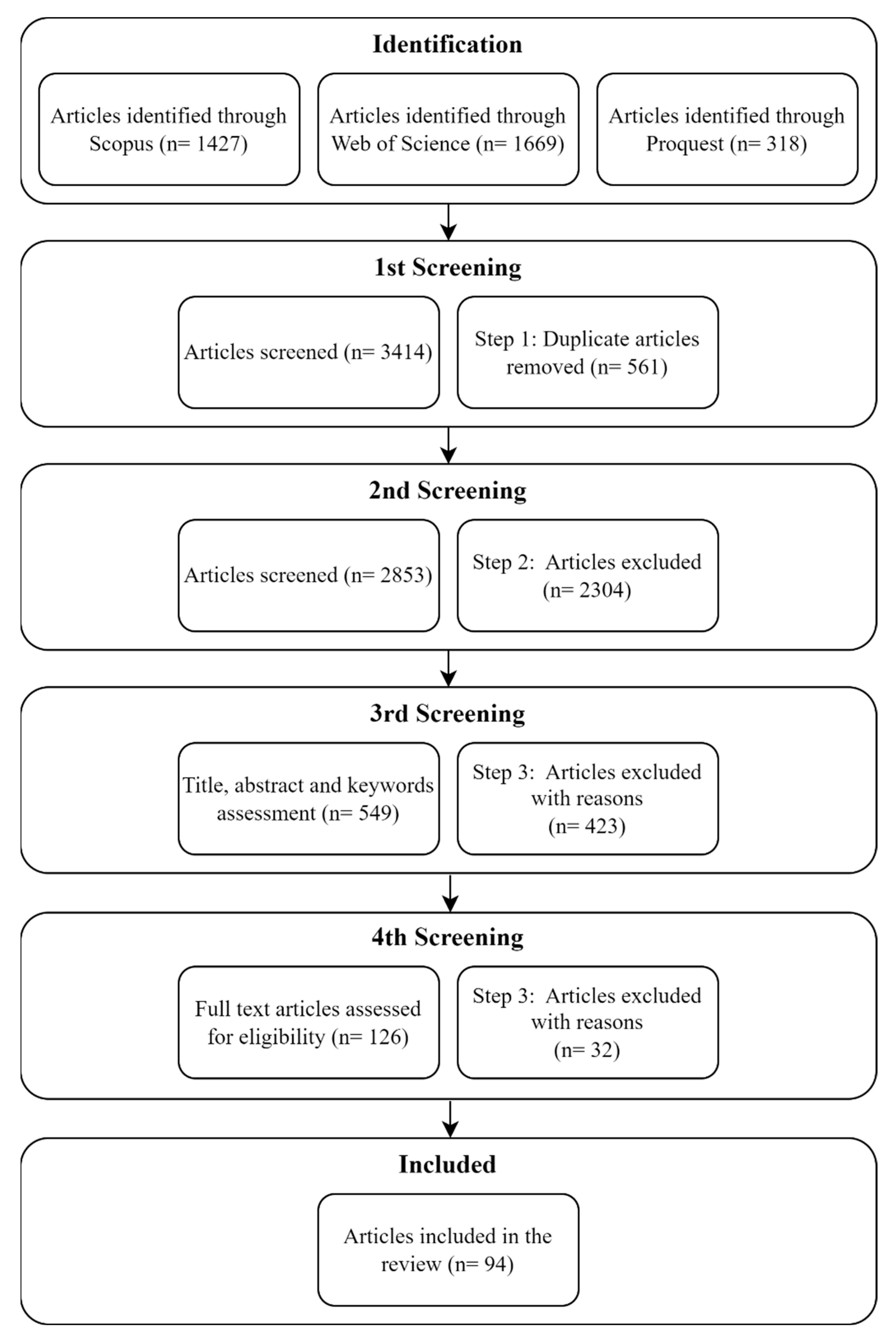

2. Methodology

3. Sustainability Assessment Methods

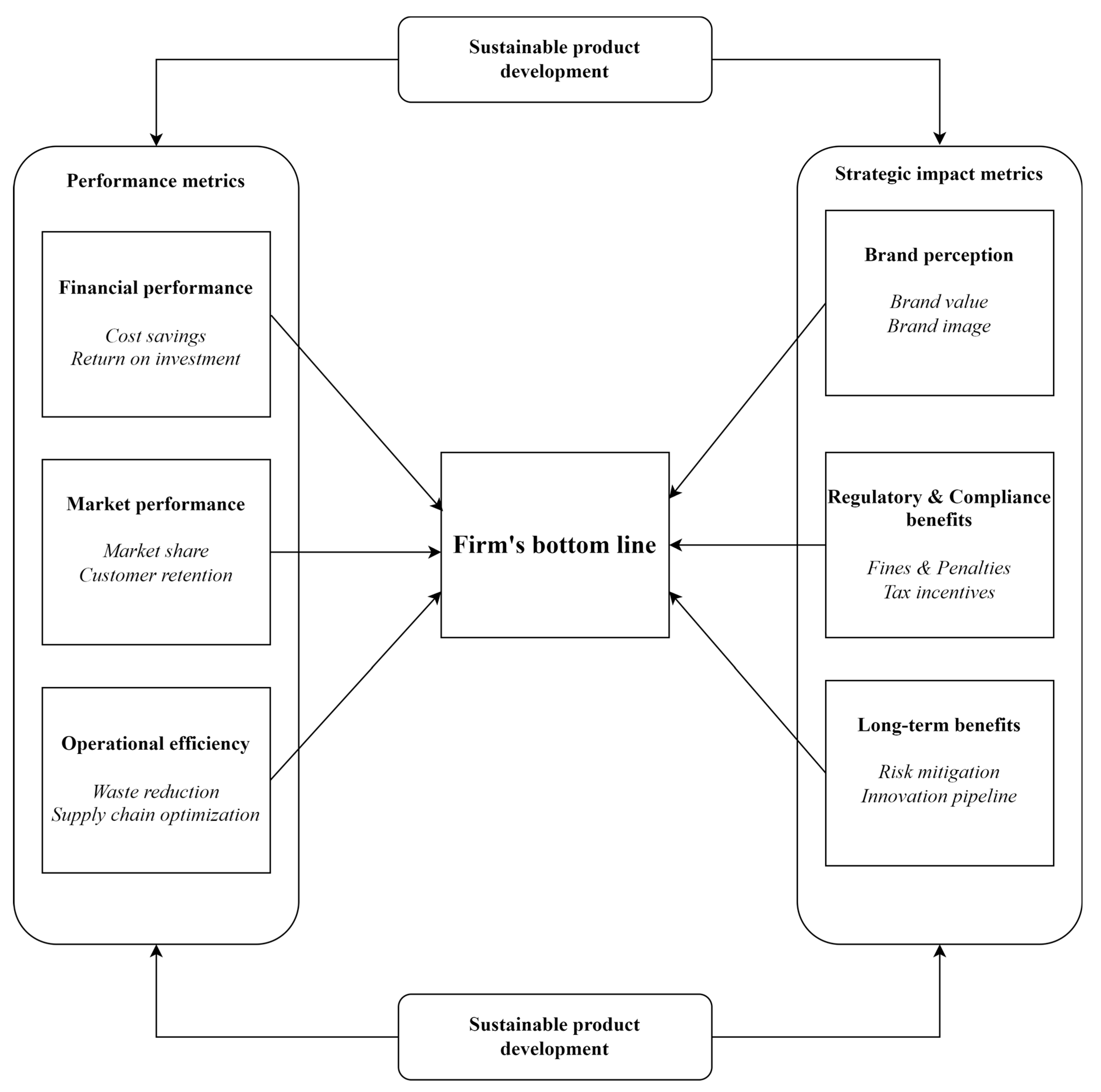

4. Derivation of the Index

4.1. Sustainable Product Development and Financial Performance

4.2. Sustainable Product Development and Market Performance

4.3. Sustainable Product Development and Operational Efficiency

4.4. Sustainable Product Development and Brand Value and Image

4.5. Sustainable Product Development and Regulatory and Compliance Benefits

4.6. Sustainable Product Development and Long-Term Benefits

5. Quantification of the Matrix

5.1. Financial Performance

5.1.1. Cost Savings Measurement

5.1.2. Return on Investment (ROI) Measurement

5.1.3. Quantifying the Financial Performance Matrix

- Weight1 (w1) (Cost Savings Percentage):60%

- Weight2 (w2) (ROI Percentage): 40%

5.2. Market Performance

5.2.1. Market Share Measurement

5.2.2. Customer Retention Measurement

5.2.3. Quantifying the Market Performance Matrix

5.3. Operational Efficiency

5.3.1. Waste Reduction Measurement

5.3.2. Supply Chain Efficiency

5.3.3. Quantifying the Operational Efficiency Matrix

5.4. Increase in Brand Perception

5.5. Regulatory and Compliance Benefits

5.5.1. Reduction in Fines and Penalties Percentage Measurement

5.5.2. Tax Incentives Received Percentage

5.5.3. Quantifying the Regulatory and Compliance Benefits

5.6. Long-Term Benefits

5.6.1. Risk Mitigation Measurement

5.6.2. Innovation Pipeline Measurement

5.6.3. Quantifying the Long-Term Benefits

5.7. Quantifying the Overall Impact

- FPI = Financial Performance Impact

- MPI = Market Performance Impact

- OEI = Operational Efficiency Impact

- WAIB = Weighted average increase in brand perception

- RCB = Regulations and Compliance Benefits

- LTB = Long-term benefits

- wFPI = Weight assigned to FPI

- wMPI = Weight assigned to MPI

- wOEI = Weight assigned to OEI

- wWAIB = Weight assigned to WAIB

- wRCB = Weight assigned to RCB

- wLTB = Weight assigned to LTB

- 75–100%: Optimal—Firms are maximizing the benefits of sustainable product development [96].

- 50–74%: Proficient—Above average practices but not at the pinnacle [97].

- 25–49%: Emerging—Initiating sustainable efforts with substantial room for enhancement [98].

- Below 25%: Lagging—Indicating a dire need for strategic adjustments in sustainable practices [99].

5.8. Case Study

5.8.1. Financial Performance Impact

5.8.2. Market Performance Impact

5.8.3. Operational Efficiency Impact

5.8.4. Weighted Average Increase in Brand Perception

5.8.5. Regulations and Compliance Benefits

5.8.6. Long-Term Benefits

5.8.7. Overall Impact

6. Discussion

6.1. Theoretical Contributions

6.2. Practical Implications

6.3. Limitations and Future Research

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Nguyen-Viet, B. The impact of green marketing mix elements on green customer based brand equity in an emerging market. Asia-Pac. J. Bus. Adm. 2023, 15, 96–116. [Google Scholar] [CrossRef]

- Dinh, K.C.; Nguyen-Viet, B.; Phuong Vo, H.N. Toward Sustainable Development and Consumption: The Role of the Green Promotion Mix in Driving Green Brand Equity and Green Purchase Intention. J. Promot. Manag. 2023, 29, 824–848. [Google Scholar] [CrossRef]

- Wei, X.; Ren, H.; Ullah, S.; Bozkurt, C. Does environmental entrepreneurship play a role in sustainable green development? Evidence from emerging Asian economies. Econ. Res. Istraz. 2023, 36, 73–85. [Google Scholar] [CrossRef]

- Sarkar, B.; Ullah, M.; Sarkar, M. Environmental and economic sustainability through innovative green products by remanufacturing. J. Clean. Prod. 2022, 332, 129813. [Google Scholar] [CrossRef]

- Yadav, D.; Singh, R.; Kumar, A.; Sarkar, B. Reduction of Pollution through Sustainable and Flexible Production by Controlling By-Products. J. Environ. Inform. 2022, 40, 106–124. [Google Scholar] [CrossRef]

- Ching, N.T.; Ghobakhloo, M.; Iranmanesh, M.; Maroufkhani, P.; Asadi, S. Industry 4.0 applications for sustainable manufacturing: A systematic literature review and a roadmap to sustainable development. J. Clean. Prod. 2022, 334, 130133. [Google Scholar] [CrossRef]

- McKerlie, K.; Knight, N. Advancing extended producer responsibility in Canada. J. Clean. Prod. 2006, 14, 616–628. [Google Scholar] [CrossRef]

- Solding, P.; Petku, D.; Mardan, N. Using simulation for more sustainable production systems—Methodologies and case studies. Int. J. Sustain. Eng. 2009, 2, 111–122. [Google Scholar] [CrossRef]

- Wiles, C.; Watts, P. Continuous process technology: A tool for sustainable production. Green. Chem. 2014, 16, 55–62. [Google Scholar] [CrossRef]

- Lundin, M. Indicators for Measuring the Sustainability of Urban Water Systems—A Life Cycle Approach. Ph.D. Thesis, Chalmers University of Technology, Göteborg, Sweden, 2003; pp. 1–47. [Google Scholar]

- Chambers, N.; Simmons, C.; Wackernagel, M. Sharing Nature’s Interest: Ecological Footprints as an Indicator of Sustainability; Routledge: Oxfordshire, UK, 2014; pp. 1–185. [Google Scholar]

- Bazan, G. Our Ecological Footprint: Reducing human impact on the earth. Electron. Green J. 1997, 1. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. Development of composite sustainability performance index for steel industry. Ecol. Indic. 2007, 7, 565–588. [Google Scholar] [CrossRef]

- Jung, E.J.; Kim, J.S.; Rhee, S.K. The measurement of corporate environmental performance and its application to the analysis of efficiency in oil industry. J. Clean. Prod. 2001, 9, 551–563. [Google Scholar] [CrossRef]

- Khan, F.I.; Sadiq, R.; Veitch, B. Life cycle iNdeX (LInX): A new indexing procedure for process and product design and decision-making. J. Clean. Prod. 2004, 12, 59–76. [Google Scholar] [CrossRef]

- Shuaib, M.; Seevers, D.; Zhang, X.; Badurdeen, F.; Rouch, K.E.; Jawahir, I.S. Product sustainability index (ProdSI): A metrics-based framework to evaluate the total life cycle sustainability of manufactured products. J. Ind. Ecol. 2014, 18, 491–507. [Google Scholar] [CrossRef]

- Sun, S.; Ertz, M. Environmental impact of mutualized mobility: Evidence from a life cycle perspective. Sci. Total Environ. 2021, 772, 145014. [Google Scholar] [CrossRef] [PubMed]

- Davidson, A.; Simonetto, M. Pricing strategy and execution: An overlooked way to increase revenues and profits. Strateg. Leadersh. 2005, 33, 25–33. [Google Scholar] [CrossRef]

- Eggert, A.; Hogreve, J.; Ulaga, W.; Muenkhoff, E. Revenue and Profit Implications of Industrial Service Strategies. J. Serv. Res. 2014, 17, 23–39. [Google Scholar] [CrossRef]

- Porter, M.E. Strategy and the Internet. Harvard Business Review, March 2001; pp. 108–115. [Google Scholar]

- Liang, H.; Renneboog, L. Corporate Social Responsibility and Sustainable Business. Oxford Res. Encycl. Econ. Financ. 2021, 9, 26–39. [Google Scholar]

- Cavallaro, F. A comparative assessment of thin-film photovoltaic production processes using the ELECTRE III method. Energy Policy 2010, 38, 463–474. [Google Scholar] [CrossRef]

- Amit, R.; Zott, C. Creating value through business model innovation. MIT Sloan Manag. Rev. 2012, 53, 41–49. [Google Scholar]

- Gramlich, D.; Finster, N. Corporate sustainability and risk. J. Bus. Econ. 2013, 83, 631–664. [Google Scholar] [CrossRef]

- Lu, J.; Rodenburg, K.; Foti, L.; Pegoraro, A. Are firms with better sustainability performance more resilient during crises? Bus. Strateg. Environ. 2022, 31, 3354–3370. [Google Scholar] [CrossRef]

- Ahmad, S.; Wong, K.Y.; Tseng, M.L.; Wong, W.P. Sustainable product design and development: A review of tools, applications and research prospects. Resour. Conserv. Recycl. 2018, 132, 49–61. [Google Scholar] [CrossRef]

- Younesi, M.; Roghanian, E. A framework for sustainable product design: A hybrid fuzzy approach based on Quality Function Deployment for Environment. J. Clean. Prod. 2015, 108, 385–394. [Google Scholar] [CrossRef]

- Kaur, H.; Garg, P. Urban sustainability assessment tools: A review. J. Clean. Prod. 2019, 210, 146–158. [Google Scholar] [CrossRef]

- Waas, T.; Hugé, J.; Block, T.; Wright, T.; Benitez-Capistros, F.; Verbruggen, A. Sustainability assessment and indicators: Tools in a decision-making strategy for sustainable development. Sustainabilty 2014, 6, 5512–5534. [Google Scholar] [CrossRef]

- Stobierski, T. 4 Impactful Sustainable Business Practices to Make a Difference; Harvard Business School: Boston, MA, USA, 2021. [Google Scholar]

- Bodhanwala, S.; Bodhanwala, R. Does corporate sustainability impact firm profitability? Evidence from India. Manag. Decis. 2018, 56, 1734–1747. [Google Scholar] [CrossRef]

- Hernández-Chea, R.; Jain, A.; Bocken, N.M.P.; Gurtoo, A. The business model in sustainability transitions: A conceptualization. Sustainabilty 2021, 13, 5763. [Google Scholar] [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Moher, D. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. Rev. Panam. Salud. Publica/Pan. Am. J. Public Health 2021, 46, 105906. [Google Scholar]

- Goedkoop, M.; Spriensma, R. The Eco-Indicator 99—A Damage Oriented Method for Life Cycle Assessment, Methodology Report. PRé Consult. 2000, pp. 1–132. Available online: https://pre-sustainability.com/legacy/download/EI99_annexe_v3.pdf (accessed on 3 December 2023).

- DeSimone, L.; Popoff, F. Eco-Efficiency: The Business Link to Sustainable Development. Int. J. Sustain. High. Educ. 2000, 1, 305–308. [Google Scholar] [CrossRef]

- Fijał, T. An environmental assessment method for cleaner production technologies. J. Clean. Prod. 2007, 15, 914–919. [Google Scholar] [CrossRef]

- Hermann, B.G.; Kroeze, C.; Jawjit, W. Assessing environmental performance by combining life cycle assessment, multi-criteria analysis and environmental performance indicators. J. Clean. Prod. 2007, 15, 1787–1796. [Google Scholar] [CrossRef]

- WBCSD. Signals of Change: Business Progress Toward Sustainable Development; WBCSD: Geneva, Switzerland, 1997; Volume 60. [Google Scholar]

- Clark, G.; Kosoris, J.; Hong, L.N.; Crul, M. Design for sustainability: Current trends in sustainable product design and development. Sustainability 2009, 1, 409–424. [Google Scholar] [CrossRef]

- Maxwell, D.; Van der Vorst, R. Developing sustainable products and services. J. Clean. Prod. 2003, 11, 883–895. [Google Scholar] [CrossRef]

- Wang, S.; Su, D.; Ma, M.; Kuang, W. Sustainable product development and service approach for application in industrial lighting products. Sustain. Prod. Consum. 2021, 27, 1808–1821. [Google Scholar] [CrossRef]

- Muaz, M.; Choudhury, S.K. Experimental investigations and multi-objective optimization of MQL-assisted milling process for finishing of AISI 4340 steel. Meas. J. Int. Meas. Confed. 2019, 138, 557–569. [Google Scholar] [CrossRef]

- Usmani, Z.; Sharma, M.; Awasthi, A.K.; Sivakumar, N.; Lukk, T.; Pecoraro, L.; Gupta, V.K. Bioprocessing of waste biomass for sustainable product development and minimizing environmental impact. Bioresour. Technol. 2021, 322, 124548. [Google Scholar] [CrossRef]

- Rost, Z. The increasing relevance of product responsibility. uwf UmweltWirtschaftsForum. 2015, 23, 299–305. [Google Scholar] [CrossRef]

- Dey, K.; Roy, S.; Saha, S. The impact of strategic inventory and procurement strategies on green product design in a two-period supply chain. Int. J. Prod. Res. 2019, 57, 1915–1948. [Google Scholar] [CrossRef]

- Romli, A.; Prickett, P.; Setchi, R.; Soe, S. Integrated eco-design decision-making for sustainable product development. Int. J. Prod. Res. 2015, 53, 549–571. [Google Scholar] [CrossRef]

- Muthuveloo, R.; Ping, T.A. Achieving Business Sustainability Via I-Top Model. Am. J. Econ. Bus. Adm. 2013, 5, 15–21. [Google Scholar] [CrossRef]

- Cords, S.S. The Green Scorecard: Measuring the Return on Investment in Green Initiatives. Libr. J. 2010, 135, 83–84. [Google Scholar]

- Ness, D.; Xing, K. Hewlett Packard Australia—Towards Sustainable Product Service Systems. Manufacturing Servitization in the Asia-Pacific; Springer: Berlin/Heidelberg, Germany, 2016; pp. 93–108. [Google Scholar]

- Baker, W.E.; Sinkula, J.M. Environmental marketing strategy and firm performance: Effects on new product performance and market share. J. Acad. Mark. Sci. 2005, 33, 461–475. [Google Scholar] [CrossRef]

- Finster, M.; Eagan, P.; Hussey, D. Linking Industrial Ecology with Business Strategy. J. Ind. Ecol. 2002, 5, 107–125. [Google Scholar] [CrossRef]

- Carus, M.; Eder, A.; Beckmann, J. GreenPremium prices along the value chain of biobased products. Ind. Biotechnol. 2014, 10, 83–88. [Google Scholar] [CrossRef]

- Kahupi, I.; Eiríkur Hull, C.; Okorie, O.; Millette, S. Building competitive advantage with sustainable products—A case study perspective of stakeholders. J. Clean. Prod. 2021, 289, 125699. [Google Scholar] [CrossRef]

- Chang, N.; Fong, C. Green product quality, green corporate image, green customer satisfaction, and green customer loyalty. African J. Bus. Manag. 2010, 4, 2836–2844. [Google Scholar]

- Ahmed, R.R.; Streimikiene, D.; Qadir, H.; Streimikis, J. Effect of green marketing mix, green customer value, and attitude on green purchase intention: Evidence from the USA. Environ. Sci. Pollut. Res. 2023, 30, 11473–11495. [Google Scholar] [CrossRef]

- Riva, F.; Magrizos, S.; Rubel, M.R.B.; Rizomyliotis, I. Green consumerism, green perceived value, and restaurant revisit intention: Millennials’ sustainable consumption with moderating effect of green perceived quality. Bus. Strateg. Environ. 2022, 31, 2807–2819. [Google Scholar] [CrossRef]

- Mohamed, M.; Rady, A.; Fawy, W. The Impact of Floating Hotels’ Green Practices on Customers’ Satisfaction and Retention. Int. J. Tour. Hosp. Manag. 2023, 6, 245–264. [Google Scholar] [CrossRef]

- Martínez-Martínez, A.; Cegarra-Navarro, J.G.; Garcia-Perez, A.; De Valon, T. Active listening to customers: Eco-innovation through value co-creation in the textile industry. J. Knowl. Manag. 2022, 27, 1810–1829. [Google Scholar] [CrossRef]

- Tan, Z.; Sadiq, B.; Bashir, T.; Mahmood, H.; Rasool, Y. Investigating the Impact of Green Marketing Components on Purchase Intention: The Mediating Role of Brand Image and Brand Trust. Sustainabilty 2022, 14, 5939. [Google Scholar] [CrossRef]

- Danko, Y.; Nifatova, O. Agro-sphere determinants of green branding: Eco-consumption, loyalty, and price premium. Humanit. Soc. Sci. Commun. 2022, 9, 77. [Google Scholar] [CrossRef]

- Socaciu, M.I.; Câmpian, V.; Dabija, D.C.; Fogarasi, M.; Semeniuc, C.A.; Podar, A.S.; Vodnar, D.C. Assessing Consumers’ Preference and Loyalty towards Biopolymer Films for Food Active Packaging. Coatings 2022, 12, 1770. [Google Scholar] [CrossRef]

- Fisher, A. Winning the battle for customers. J. Financ. Serv. Mark. 2001, 6, 77–83. [Google Scholar] [CrossRef]

- Duffy, D.L. Internal and external factors which affect customer loyalty. J. Consum. Mark. 2003, 20, 480–485. [Google Scholar] [CrossRef]

- Blengini, G.A.; Busto, M.; Fantoni, M.; Fino, D. Eco-efficient waste glass recycling: Integrated waste management and green product development through LCA. Waste Manag. 2012, 32, 1000–1008. [Google Scholar] [CrossRef] [PubMed]

- Krystofik, M.; Wagner, J.; Gaustad, G. Leveraging intellectual property rights to encourage green product design and remanufacturing for sustainable waste management. Resour. Conserv. Recycl. 2015, 97, 44–54. [Google Scholar] [CrossRef]

- Huang, C.C.; Chuang, H.F.; Chen, S.Y. Corporate Memory: Design to better reduce, reuse and recycle. Comput. Ind. Eng. 2016, 91, 48–65. [Google Scholar] [CrossRef]

- Bag, S.; Wood, L.C.; Xu, L.; Dhamija, P.; Kayikci, Y. Big data analytics as an operational excellence approach to enhance sustainable supply chain performance. Resour. Conserv. Recycl. 2020, 153, 104559. [Google Scholar] [CrossRef]

- Carlson, R.C.; Rafinejad, D. The transition to sustainable product development and manufacturing. Int. Ser. Oper. Res. Manag. Sci. 2011, 151, 45–82. [Google Scholar]

- Lohmer, J.; Bugert, N.; Lasch, R. Analysis of resilience strategies and ripple effect in blockchain-coordinated supply chains: An agent-based simulation study. Int. J. Prod. Econ. 2020, 228, 107882. [Google Scholar] [CrossRef]

- Azadegan, A.; Mellat Parast, M.; Lucianetti, L.; Nishant, R.; Blackhurst, J. Supply Chain Disruptions and Business Continuity: An Empirical Assessment. Decis. Sci. 2020, 51, 38–73. [Google Scholar] [CrossRef]

- Palma, N.C.; Visser, M. Sustainability creates business and brand value. J. Brand. Strateg. 2012, 1, 217–222. [Google Scholar]

- Morea, D.; Gattermann Perin, M.; Kolling, C.; de Medeiros, J.F.; Duarte Ribeiro, J.L. Environmental Product Innovation and Perceived Brand Value: The Mediating Role of Ethical-Related Aspects. Sustainabilty 2023, 15, 10996. [Google Scholar] [CrossRef]

- El Zein, S.A.; Consolacion-Segura, C.; Huertas-Garcia, R. The role of sustainability in brand equity value in the financial sector. Sustainabilty 2020, 12, 254. [Google Scholar] [CrossRef]

- First, I.; Khetriwal, D.S. Exploring the relationship between environmental orientation and brand value: Is there fire or only smoke? Bus. Strateg. Environ. 2010, 19, 90–103. [Google Scholar] [CrossRef]

- Yang, M.; Chen, H.; Long, R.; Wang, Y.; Hou, C.; Liu, B. Will the public pay for green products? Based on analysis of the influencing factors for Chinese’s public willingness to pay a price premium for green products. Environ. Sci. Pollut. Res. 2021, 28, 61408–61422. [Google Scholar] [CrossRef]

- Al Mamun, A.; Rahman, M.K.; Masud, M.M.; Mohiuddin, M. Willingness to pay premium prices for green buildings: Evidence from an emerging economy. Environ. Sci. Pollut. Res. 2023, 30, 78718–78734. [Google Scholar] [CrossRef]

- Chavalittumrong, P.; Speece, M. Three-Pillar Sustainability and Brand Image: A Qualitative Investigation in Thailand’s Household Durables Industry. Sustainability 2022, 14, 11699. [Google Scholar] [CrossRef]

- Loučanová, E.; Šupín, M.; Čorejová, T.; Repková-štofková, K.; Šupínová, M.; Štofková, Z.; Olšiaková, M. Sustainability and branding: An integrated perspective of eco-innovation and brand. Sustainabilty 2021, 13, 732. [Google Scholar] [CrossRef]

- Alif Fianto, A.Y.; Hadiwidjojo, D.; Aisjah, S.; Solimun, S. The Influence of Brand Image on Purchase Behaviour Through Brand Trust. Bus. Manag. Strateg. 2014, 5, 58. [Google Scholar] [CrossRef]

- Xie, J.; Sun, Q.; Wang, S.; Li, X.; Fan, F. Does environmental regulation affect export quality? Theory and evidence from China. Int. J. Environ. Res. Public Health 2020, 17, 8237. [Google Scholar] [CrossRef] [PubMed]

- Fleith de Medeiros, J.; Duarte Ribeiro, J.L.; Nogueira Cortimiglia, M. Success factors for environmentally sustainable product innovation: A systematic literature review. J. Clean Prod. 2014, 66, 79–86. [Google Scholar] [CrossRef]

- Song, M.; Wang, S.; Zhang, H. Could environmental regulation and R&D tax incentives affect green product innovation? J. Clean. Prod. 2020, 258, 120849. [Google Scholar]

- Haji Esmaeili, S.A.; Szmerekovsky, J.; Sobhani, A.; Dybing, A.; Peterson, T.O. Sustainable biomass supply chain network design with biomass switching incentives for first-generation bioethanol producers. Energy Policy 2020, 138, 111222. [Google Scholar] [CrossRef]

- EY. Multinationals and Jurisdictions May need to Rethink their Sustainability Tax Incentives if Countries Adopt 15% Global Minimum Tax Rules. 2023. Available online: www.ey.com (accessed on 25 September 2023).

- Qi, Y.; Zhang, J.; Chen, J. Tax incentives, environmental regulation and firms’ emission reduction strategies: Evidence from China. J. Environ. Econ. Manage. 2023, 117, 102750. [Google Scholar] [CrossRef]

- Kara, S.; Ibbotson, S.; Kayis, B. Sustainable product development in practice: An international survey. J. Manuf. Technol. Manag. 2014, 25, 848–872. [Google Scholar] [CrossRef]

- Zameer, H.; Wang, Y.; Yasmeen, H. Reinforcing green competitive advantage through green production, creativity and green brand image: Implications for cleaner production in China. J. Clean. Prod. 2020, 247, 119119. [Google Scholar] [CrossRef]

- Ceptureanu, S.I.; Ceptureanu, E.G.; Popescu, D.; Orzan, O.A. Eco-innovation capability and sustainability driven innovation practices in Romanian SMEs. Sustainability 2020, 12, 7106. [Google Scholar] [CrossRef]

- Petersen, M.; Brockhaus, S. Dancing in the dark: Challenges for product developers to improve and communicate product sustainability. J. Clean. Prod. 2017, 161, 345–354. [Google Scholar] [CrossRef]

- Heher, A.D. Return on investment in innovation: Implications for institutions and national agencies. J. Technol. Transf. 2006, 31, 403–414. [Google Scholar] [CrossRef]

- Beaumont Smith, M.; Begemann, E. Measuring associations between working capital and return on investment. South Afr. J. Bus. Manag. 1997, 28, 1–5. [Google Scholar] [CrossRef]

- Netemeyer, R.G.; Krishnan, B.; Pullig, C.; Wang, G.; Yagci, M.; Dean, D.; Ricks, J.; Wirth, F. Developing and validating measures of facets of customer-based brand equity. J. Bus. Res. 2004, 57, 209–224. [Google Scholar] [CrossRef]

- Lee, K.; Shavitt, S. Can McDonald’s food ever be considered healthful? Metacognitive experiences affect the perceived understanding of a brand. J. Mark. Res. 2009, 46, 222–233. [Google Scholar] [CrossRef]

- Veloutsou, C.; Moutinho, L. Brand relationships through brand reputation and brand tribalism. J. Bus. Res. 2009, 62, 314–322. [Google Scholar] [CrossRef]

- Thomas Johnson, H.; Kaplan, R.S. Relevance Lost: The Rise and Fall of Management Accounting. J. Acc. 1987, 164, 144. [Google Scholar]

- Elkington, J.; Rowlands, I. Cannibals with forks: The triple bottom line of 21st century business. Altern. J. 1999, 36, 36–3997. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy & society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 359–370. Available online: https://pdfs.semanticscholar.org/77e9/9d84c1574c79cdbf15f1723637f7b24869c1.pdf (accessed on 3 December 2023).

- Hart, S.L. Capitalism at the Crossroads: Aligning Business, Earth, and Humanity; Pearson Prentice Hall: Old Bridge, NJ, USA, 2007; pp. 16–17. [Google Scholar]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Huang, A.; Badurdeen, F. Sustainable Manufacturing Performance Evaluation: Integrating Product and Process Metrics for Systems Level Assessment. Procedia Manuf. 2017, 8, 563–570. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Methodology | Dimensions | Focus | Source |

|---|---|---|---|

| Eco-Points (Eco-Scan) | Life cycle stages, materials, energy, processes, usage, and transportation. | Product and Process Sustainability Assessment | [34] |

| Eco-Compass | Six dimensions: energy intensity, mass intensity, health, resource conservation, re-valorization, and service extension. | Product and Process Sustainability Assessment | [35] |

| Eco-Indicator 99 | Damage-oriented impact assessment (human health, ecosystems, minerals, fossil fuels). | Product and Process Sustainability Assessment | [34] |

| Environment Assessment for Cleaner Production Technologies | Environmental impact of cleaner production technologies. | Product Sustainability Assessment | [36] |

| COMPLIMENT | The environmental impact of industries includes global warming, acidification, eutrophication, ozone precursors, and human health. | Industry Sustainability Assessment | [37] |

| Eco-Efficiency Framework | Economic and environmental sustainability. | Organisational Sustainability Assessment | [38] |

| Product Sustainability Index (ProdSI) | Comprehensive assessment of product sustainability across life cycle stages. | Product Sustainability Assessment | [16] |

| Items | Value |

|---|---|

| Cs | USD 1,230,000 |

| Ct | USD 1,980,000 |

| Net profit from sustainable product development | USD 3,533,890 |

| Initial investment | USD 3,400,000 |

| Weight for CS | 40% |

| Weight for ROI | 60% |

| Ssp | USD 993,000 |

| Stm | USD 4,600,000 |

| Cend | 8912 Consumers |

| Cnew | 2356 Consumers |

| Cstart | 16,345 Consumers |

| Weight for MS | 30% |

| Weight for CRR | 70% |

| Winitial | 145 Kg |

| Wfinal | 97 Kg |

| Cssc | USD 1,300,000 |

| ST | USD 5,700,000 |

| Weight for WR | 50% |

| Weight for SSCER | 50% |

| BVafter | 5.16 |

| BVbefore | 6.33 |

| BIafter | 5.19 |

| BIbefore | 5.24 |

| Weight for BV | 50% |

| Weight for BI | 50% |

| Fines without sustainable practices | USD 17,500 |

| Fines with sustainable practices | USD 9300 |

| Tax credits | 0 |

| Tax deductions | 0 |

| Tax rebates | USD 21,000 |

| Tax exemption | USD 9400 |

| Weight for RFP | 30% |

| Weight for TIR | 70% |

| Number of violations before | 3 |

| Number of violations after | 1 |

| Sustainable material usage | 549 Kg |

| Total material usage | 2000 Kg |

| Weight for CRred | 60% |

| Weight for EMAR | 40% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sajid, M.; Ertz, M. Blueprints to Benefits: Towards an Index to Measure the Impact of Sustainable Product Development on the Firm’s Bottom Line. Sustainability 2024, 16, 537. https://doi.org/10.3390/su16020537

Sajid M, Ertz M. Blueprints to Benefits: Towards an Index to Measure the Impact of Sustainable Product Development on the Firm’s Bottom Line. Sustainability. 2024; 16(2):537. https://doi.org/10.3390/su16020537

Chicago/Turabian StyleSajid, Muhammed, and Myriam Ertz. 2024. "Blueprints to Benefits: Towards an Index to Measure the Impact of Sustainable Product Development on the Firm’s Bottom Line" Sustainability 16, no. 2: 537. https://doi.org/10.3390/su16020537

APA StyleSajid, M., & Ertz, M. (2024). Blueprints to Benefits: Towards an Index to Measure the Impact of Sustainable Product Development on the Firm’s Bottom Line. Sustainability, 16(2), 537. https://doi.org/10.3390/su16020537