Blockchain Technology, Enterprise Risk and Enterprise Performance

Abstract

:1. Introduction

2. Theoretical Analysis and Research Hypotheses

2.1. Blockchain Technology and Enterprise Performance

2.2. The Impact of Enterprise Risk on the Relationship between Blockchain Technology and Enterprise Performance

2.3. Information Disclosure Quality Moderates the Mediating Role of Enterprise Risk between Blockchain Technology and Enterprise Performance

3. Research Design

3.1. Sample Selection and Data Source

3.2. Variable Selection

3.3. Model Building

4. Analysis of Empirical Results

4.1. Descriptive Statistics

4.2. Parallel Trend Test

4.3. Multiple Regression

4.4. Robustness Test

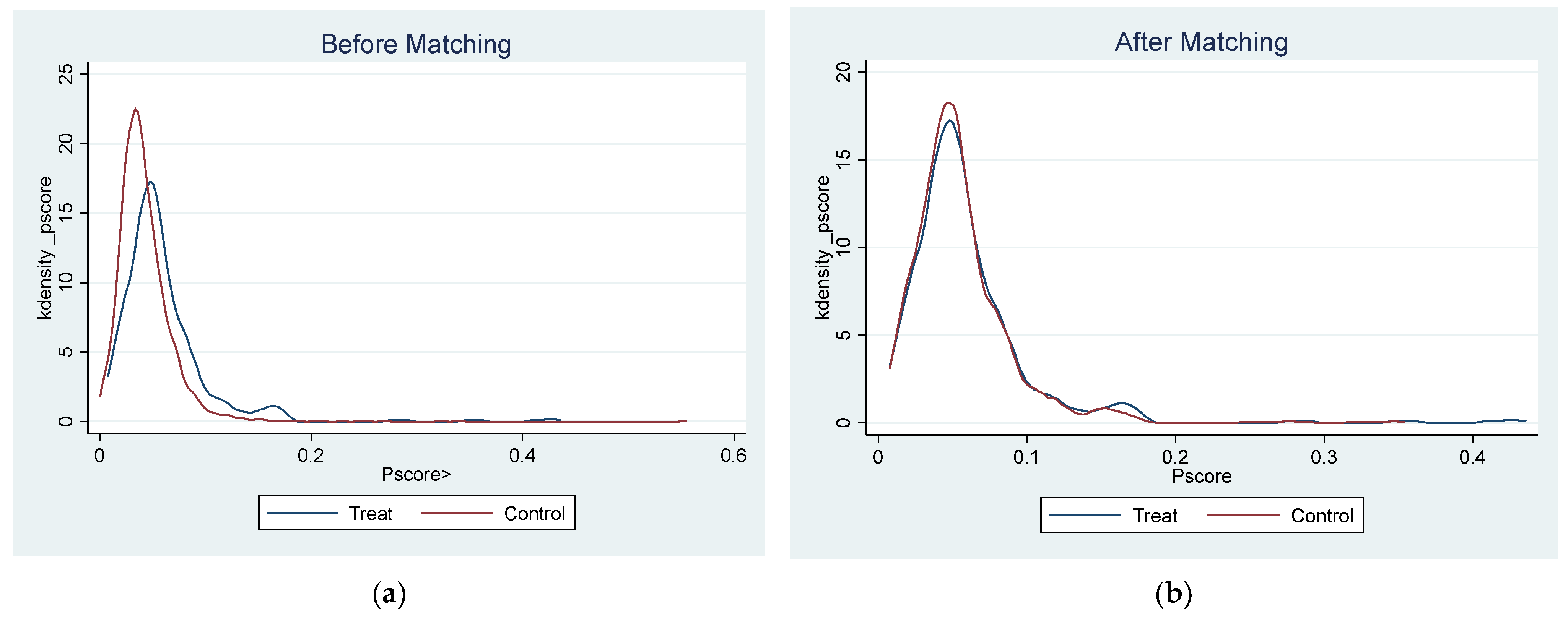

4.4.1. PSM-DID

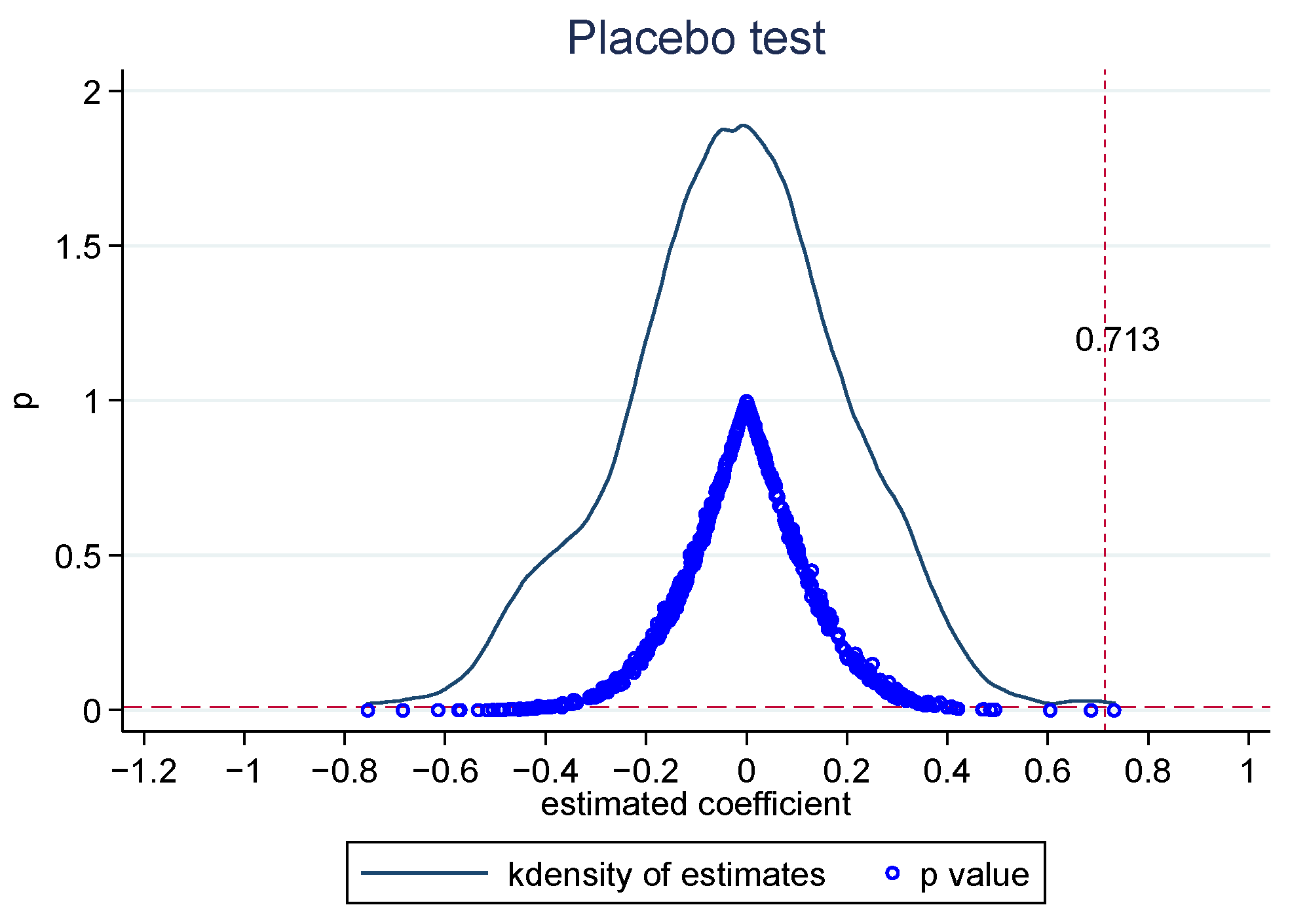

4.4.2. Placebo Testing

4.4.3. Instrumental Variables

5. Expansive Research

5.1. Mediating Effect Test

5.2. Moderating Effect Analysis

6. Conclusions and Apocalypse

6.1. Conclusions

6.2. Apocalypse

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Lumineau, F.; Wang, W.; Schilke, O. Blockchain governance—A new way of organizing collaborations? Organ. Sci. 2021, 32, 500–521. [Google Scholar] [CrossRef]

- Dwivedi, Y.K.; Hughes, L.; Baabdullah, A.M.; Ribeiro-Navarrete, S.; Giannakis, M.; Al-Debei, M.M.; Dennehy, D.; Metri, B.; Buhalis, D.; Cheung, C.M.; et al. Metaverse beyond the hype: Multidisciplinary perspectives on emerging challenges, opportunities, and agenda for research, practice and policy. Int. J. Inform. Manag. 2022, 66, 102542. [Google Scholar] [CrossRef]

- Zhu, R.; Liu, W.; Fu, Y.M. A study on the reconstruction of cultural heritage value in the context of Web 3.0. J. Chin. L. 2023, 1, 16. [Google Scholar]

- Kshetri, N. 1 Blockchain’s roles in meeting key supply chain management objectives. Int. J. Inform. Manag. 2018, 39, 80–89. [Google Scholar] [CrossRef]

- Wamba, S.F.; Queiroz, M.M. Blockchain in the operations and supply chain management: Benefits, challenges and future research opportunities. Int. J. Inform. Manag. 2020, 52, 102064. [Google Scholar] [CrossRef]

- Del Giudice, M.; Di Vaio, A.; Hassan, R.; Palladino, R. Digitalization and new technologies for sustainable business models at the ship–port interface: A bibliometric analysis. Marit. Policy Manag. 2022, 49, 410–446. [Google Scholar] [CrossRef]

- Suvarna, M.; Yap, K.S.; Yang, W.; Li, J.; Ng, Y.T.; Wang, X. Cyber-Physical Production Systems for Data-Driven, Decentralized, and Secure Manufacturing—A Perspective. Engineering 2021, 7, 46–69. [Google Scholar] [CrossRef]

- Funk, E.; Riddell, J.; Ankel, F.; Cabrera, D. Blockchain technology: A Data Framework to Improve Validity, Trust, and Accountability of Information Exchange in Health Professions Education. J. Acad. Med. 2018, 93, 1791–1794. [Google Scholar] [CrossRef]

- Morkunas, V.J.; Paschen, J.; Boon, E. How Blockchain Technologies Impact Your Business Model. Bus. Horiz. 2019, 62, 295–306. [Google Scholar] [CrossRef]

- Pan, X.; Pan, X.; Song, M.; Ai, B.; Ming, Y. Blockchain Technology and Enterprise Operational Capabilities: An Empirical Test. Int. J. Inf. Manag. 2019, 52, 101946. [Google Scholar] [CrossRef]

- Ko, K.; Lee, J.; Ryu, D. Blockchain Technology and Manufacturing Industry: Real-Time Transparency and Cost Savings. Sustainability 2018, 10, 4274. [Google Scholar] [CrossRef]

- Karamchandani, A.; Srivastava, S.K.; Kumar, S.; Srivastava, A. Analyzing perceived role of blockchain technology in SCM context for the manufacturing industry. Int. J. Prod. Res. 2021, 59, 3398–3429. [Google Scholar] [CrossRef]

- Yang, X.; Tan, Q. Research on Intelligent Operation of High-end Equipment Manufacturing Enterprises Based on Blockchain Technology. Bus. Res. 2018, 11, 12–17. [Google Scholar]

- Wan, Y.L.; Gao, Y.C.; Hu, Y.M. Blockchain application and collaborative innovation in the manufacturing industry: Based on the perspective of social trust. Technol. Forecast. Soc. Change 2022, 177, 121540. [Google Scholar] [CrossRef]

- Gerakoudi-Ventouri, K. Review of studies of blockchain technology effects on the shipping industry. J. Shipp. Trade 2022, 7, 2. [Google Scholar] [CrossRef]

- Li, R.S.; Wan, Y.L. The Impact of Blockchain on Business Operational Efficiency—Trust Booster or Hype? Friends Account. 2021, 1, 153–160. [Google Scholar]

- Deng, X.Z.; Wang, Y.M. The Impact of Blockchain Application on Corporate Performance—Analysis of Listed Companies Based on Blockchain Concept. Friends Account. 2021, 9, 156–161. [Google Scholar]

- Lin, X.Y.; Wu, D. Blockchain Technology and Corporate Performance: The Moderating Role of Corporate Governance Structure. Manag. Rev. 2021, 33, 341–352. [Google Scholar]

- Di Vaio, A.; Varriale, L. Blockchain technology in supply chain management for sustainable performance: Evidence from the airport industry. Int. J. Inform. Manag. 2020, 52, 102014. [Google Scholar] [CrossRef]

- Lu, S.J.; Ru, Z.; Han, L.F. Research on the impact of blockchain on corporate financial risk—Based on the multi-point DID-PSM model. Friends Account. 2022, 9, 138–145. [Google Scholar]

- Xu, C.Y.; Chen, Y.J.; Wang, H.J. The impact of blockchain enabled diversification on the level of corporate risk taking—Based on the perspective of the digital economy era. China Soft Sci. 2022, 1, 121–131. [Google Scholar]

- Chen, Z.B.; Pan, H.Q.; Qi, J. Construction of enterprise risk management system based on blockchain technology. Fin. Res. 2022, 3, 35–43. [Google Scholar]

- Wang, Y.Q. Research on the impact of listed companies’ governance ability, disclosure quality on financial performance. Price Theory Pract. 2022, 3, 106–109. [Google Scholar]

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Liu, X. Research on Supply Chain Finance Model Empowered by Blockchain Technology. Friends Account. 2021, 23, 148–152. [Google Scholar]

- Liu, L. Application of Blockchain Technology in the Financial Field and Compliance Regulation. Manag. Mod. 2020, 40, 10–12. [Google Scholar]

- Sun, G.M.; Li, M. Blockchain Trust Mechanism and Social Order—Analysis Based on Epidemic Isolation and Prevention and Control. Shandong Soc. Sci. 2020, 4, 24–30. [Google Scholar]

- Zeng, J.H.; Ma, R.Z. The Impact of R&D Investment on IPO Price Suppression of Entrepreneurial Firms—Moderation of Disclosure Quality. China Soft Sci. 2021, 35, 15–21. [Google Scholar]

- Qin, J.P.; Li, Y. Relaxation of Short-Selling Constraints and the Cost of Debt Financing—Mediating Effects Based on Disclosure Quality of Listed Companies. Wuhan Fin. 2021, 5, 29–38. [Google Scholar]

- Big Data Development Authority of Guizhou Province, 2022 Top 100 Industrial Blockchain Companies in China. Available online: http://dsj.guizhou.gov.cn/xwzx/gnyw/202207/t20220715_75561605.html (accessed on 15 July 2022).

- General Office of the Ministry of Industry and Information Technology, Notice of the General Office of the Ministry of Industry and Information Technology on the Announcement of the List of Typical Application Cases of Blockchain in 2022. Available online: https://wap.miit.gov.cn/zwgk/zcwj/wjfb/tz/art/2023/art_61ebb423b7f64bb0bfdd15a4a1b77b9f.html (accessed on 6 February 2022).

- Hai, B.L.; Gao, Q.Z.; Yin, X.M.; Yang, J.X. Executive Overconfidence, R&D Investment Jumps and Firm Performance—Empirical Evidence from Chinese Listed Companies. Sci. Technol. Prog. Policy 2020, 37, 136–145. [Google Scholar]

- Altman, E.I. Financial Rations, Discriminant Analysis and the Prediction of Corporate Bankruptcy. J. Finance 1968, 23, 589–609. [Google Scholar] [CrossRef]

- Xu, S.F.; Xu, L.B. Information Disclosure Quality and Valuation Bias in Capital Markets. Account. Res. 2015, 36, 40–47. [Google Scholar]

- Beck, T.; Levine, R.; Levkov, A. A Big Bad Banks? The Winners and Losers from Bank Deregulation in the United States. J. Finance 2010, 65, 1637–1667. [Google Scholar] [CrossRef]

- Wen, Z.L.; Ye, B.J. Mediation effects analysis: Methods and Model Development. Adv. Psychol. Sci. 2014, 22, 731–745. [Google Scholar] [CrossRef]

- Xie, z.; Yu, J.; Wang, S. Can the establishment of development zones encourage firms’ green innovation?—Empirical evidence based on different levels of development zones. J. Nanjing Univ. Finance Econ. 2022, 1, 75–85. [Google Scholar]

- Heckman, J.J.; Ichimura, H.; Todd, P.E. Matching as an Econometric Evaluation Estimator: Evidence from Evaluating a Job Training Program. Rev. Econ. Study 1997, 64, 605–654. [Google Scholar] [CrossRef]

- He, D.J.; Sun, Y.P.; Lv, J.Y. Research on the Incentive Effect of Tax and Fee Reduction on Enterprise Technological Innovation. Fisc. Sci. 2021, 12, 117–131. [Google Scholar]

- Cai, X.; Lu, Y.; Wu, M.; Yu, L. Does environmental regulation drive away inbound foreign direct investment? Evidence from a quasi-natural experiment in China. J. Dev. Econ. 2016, 123, 73–85. [Google Scholar] [CrossRef]

- Lu, Y.; Tao, Z.; Zhu, L. Identifying FDI spillovers. J. Int. Econ. 2017, 107, 75–90. [Google Scholar] [CrossRef]

- Cai, Q.F.; Wang, H.Y.; Li, D.X. Internet Lending, Labor Productivity and Firm Transformation—A Perspective Based on Labor Mobility. China Ind. Econ. 2021, 12, 146–165. [Google Scholar]

- Li, S.L.; Feng, Y.F. How Can Blockchain Promote the Green Development of Manufacturing Industry?—A Quasi-Natural Experiment Based on Environmentally Focused Cities. China Environ. Sci. 2021, 41, 1455–1466. [Google Scholar]

- Yang, D.M.; Lu, M. Do Internet Business Models Affect Audit Fees of Listed Companies? Audit. Res. 2017, 6, 84–90. [Google Scholar]

- Yang, D.; Xia, S.; Jin, S.Y.; Lin, D.; Ma, Q. Big Data, Blockchain and Audit Fees of Listed Companies. Audit. Res. 2020, 4, 68–79. [Google Scholar]

- Xu, N.; Zhang, Y.; Xu, X.Y. Can the “ability of the competent person” Protect the Interests of Small and Medium-Sized Shareholders of Subsidiaries?—Perspectives on “two-way governance” of parent-subsidiary companies. China Ind. Econ. 2019, 11, 155–173. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Type | Variable Name | Variable Symbol | Variable Definition | ||

|---|---|---|---|---|---|

| Dependent variable | Enterprise performance | Q | Expressed in terms of Tobin’s Q-value Tobin’s Q = market capitalization/total assets | ||

| Independent variable | Blockchain technology | Blockchain (treat× post) | Firm i adopts blockchain technology in year t, taking the value of 1, otherwise. | treat | Group virtual variable |

| post | Time virtual variable | ||||

| Mediating variable | Enterprise Risks | Z | Computed by the Altman Z-score model (1968) [33] | ||

| Moderating variable | Information disclosure quality | KV | Referring to the approach of Xu et al. (2015) [34] | ||

| Control variables | Current ratio | CR | liquid asset/liquid liability × 100% | ||

| Asset–liability ratio | Lev | Total liabilities/Total assets × 100% | |||

| Total asset turnover | Turnover | Total sales revenue/average total assets × 100% | |||

| Ratio of profits to cost | RPCE | Total profit/total cost × 100% | |||

| Gross operating income growth rate | Growth | 100% | |||

| Governance structure | Gov | Number of independent directors/ numbers of Director | |||

| Shareholding structure | Top1 | Percentage of shares held by the largest shareholder | |||

| Age of the company | Age | Logarithmic values for observation year − IPO year values | |||

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| Q | 360 | 2.22 | 2.04 | 0.14 | 13.45 |

| Z | 360 | 6.21 | 9.23 | −1.65 | 90.92 |

| KV | 360 | 0.47 | 0.20 | 0.02 | 1.23 |

| CR | 360 | 3.05 | 4.93 | 0.49 | 49.63 |

| Lev | 360 | 0.38 | 0.20 | 0.03 | 0.93 |

| Turnover | 360 | 0.51 | 0.29 | 0.01 | 1.66 |

| RPCE | 360 | 0.06 | 0.31 | −3.49 | 0.66 |

| Growth | 360 | 0.12 | 0.48 | −0.67 | 5.39 |

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| Q | 8032 | 1.99 | 1.68 | 0.10 | 25.71 |

| Z | 8032 | 5.21 | 6.69 | −5.10 | 160.85 |

| KV | 8006 | 0.52 | 0.23 | 0 | 2.03 |

| CR | 8032 | 2.26 | 2.18 | 0.11 | 42.72 |

| Lev | 8032 | 0.41 | 0.18 | 0.01 | 1.72 |

| Turnover | 8032 | 0.67 | 0.40 | 0.01 | 3.70 |

| RPCE | 8032 | 0.10 | 0.23 | −3.56 | 5.38 |

| Growth | 8032 | 0.20 | 1.62 | −0.91 | 82.70 |

| Variable | Q | Z | Q |

|---|---|---|---|

| Model (1) | Model (2) | Model (3) | |

| Blockchain | 0.713 *** | 2.317 *** | 0.266 ** |

| (5.22) | (5.38) | (2.44) | |

| Z | 0.193 *** | ||

| (65.60) | |||

| Constant | 11.239 *** | 22.333 *** | 7.122 *** |

| (32.48) | (19.56) | (25.27) | |

| Control | Yes | Yes | Yes |

| Individual FE | Yes | Yes | Yes |

| N | 8392 | 8392 | 8392 |

| R-squared | 0.15 | 0.547 | 0.467 |

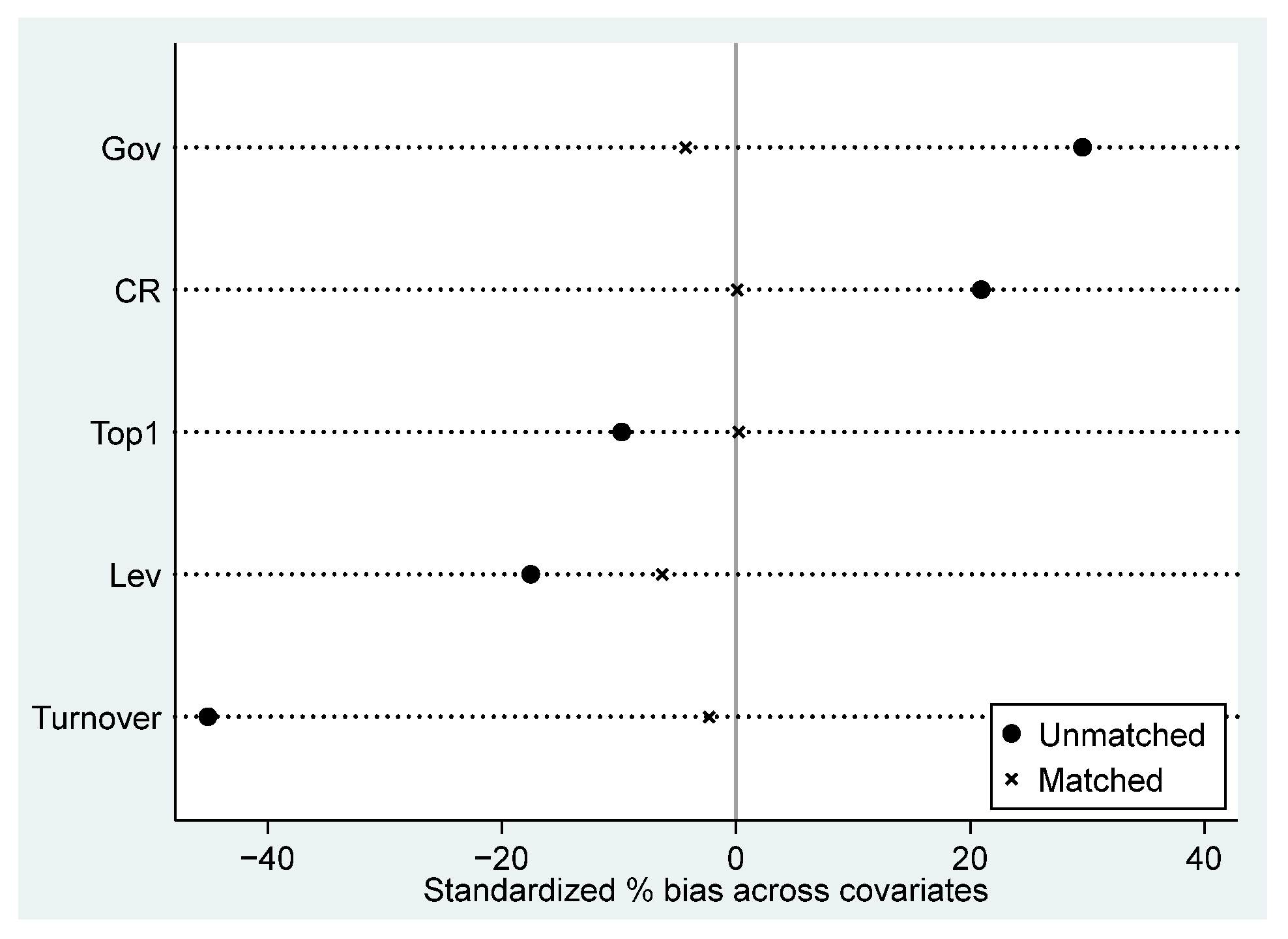

| Variable | Unmatched | Mean | %Bias | %Reduct |Bias| | t | P > |t| | |

|---|---|---|---|---|---|---|---|

| Matched | Treated | Control | |||||

| CR | U | 3.05 | 2.26 | 20.9 | 99.6 | 6.27 | 0.000 |

| M | 2.80 | 2.79 | 0.1 | 0.01 | 0.991 | ||

| Lev | U | 0.38 | 0. 41 | −17.5 | 64.0 | −3.42 | 0.001 |

| M | 0.38 | 0.40 | −6.3 | −0.82 | 0.414 | ||

| Turnover | U | 0.51 | 0.67 | −45.1 | 94.9 | −7.42 | 0.000 |

| M | 0.51 | 0.52 | −2.3 | −0.37 | 0.712 | ||

| Gov | U | 0.39 | 0.38 | 29.6 | 85.4 | 5.86 | 0.000 |

| M | 0.40 | 0.40 | −4.3 | −0.52 | 0.603 | ||

| Top1 | U | 3.06 | 4.01 | −9.8 | 97.6 | −1.64 | 0.101 |

| M | 3.07 | 3.05 | 0.2 | 0.03 | 0.973 | ||

| Variable | Q | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Blockchain | 0.524 ** | 0.598 *** | 0.607 *** | 0.619 *** |

| (2.26) | (2.71) | (3.00) | (3.23) | |

| Constant | 9.186 *** | 10.274 *** | 10.298 *** | 10.362 *** |

| (7.50) | (9.43) | (10.83) | (11.95) | |

| Control | Yes | Yes | Yes | Yes |

| Individual FE | Yes | Yes | Yes | Yes |

| N | 1013 | 1315 | 1592 | 1869 |

| R-squared | 0.182 | 0.171 | 0.167 | 0.161 |

| Variable | First Phase | Second Phase |

|---|---|---|

| ) | Q | |

| City post | 0.94 *** | |

| (79.63) | ||

| Blockchain (treat post) | 0.517 ** | |

| (2.57) | ||

| Constant | −0.38 *** | 11.107 *** |

| (−17.92) | (30.85) | |

| Control | Yes | Yes |

| Individual FE | Yes | Yes |

| N | 8392 | 8392 |

| R-squared | 0.53 | |

| F-value | 904.67 |

| Coef. | P > |Z| | Normal-Based [95% Conf. Interval] | |||

|---|---|---|---|---|---|

| Sobel | Sobel | 0.44729341 | 8.213 × 10−8 | ||

| Goodman-1 (Aroian) | 0.44729341 | 8.241 × 10−8 | |||

| Goodman-2 | 0.44729341 | 8.185 × 10−8 | |||

| Indirect effect | 0.447293 | 8.2 × 10−8 | |||

| Direct effect | 0.265679 | 0.014564 | |||

| Total effect | 0.712972 | 1.8 × 10−7 | |||

| Bootstrap | ind_dff | 0.4472934 | 0.000 | 0.1991548 | 0.6954321 |

| dir_dff | 0.2656785 | 0.032 | 0.0225232 | 0.5088339 | |

| Variable | Z | Z | Q | Q |

|---|---|---|---|---|

| Model (4) | Model (5) | Model (6) | Model (7) | |

| Blockchain | 2.315 *** | 0.834 | 0.271 ** | 0.279 ** |

| (5.38) | (1.06) | (2.50) | (2.59) | |

| KV | 1.565 *** | 1.503 *** | 0.533 *** | 0.734 *** |

| (6.92) | (7.34) | (9.36) | (10.56) | |

| Z | 0.191 *** | 0.211 *** | ||

| (64.90) | (42.56) | |||

| KV | 3.242 ** | |||

| (2.25) | ||||

| Z | −0.033 *** | |||

| (−5.02) | ||||

| Constant | 20.782 *** | 20.75 *** | 6.995 *** | 6.764 *** |

| (19.02) | (19.00) | (24.91) | (23.81) | |

| Control | Yes | Yes | Yes | Yes |

| Individual FE | Yes | Yes | Yes | Yes |

| N | 8366 | 8366 | 8366 | 8366 |

| R-squared | 0.551 | 0.552 | 0.474 | 0.476 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhen, Y.; Qiao, W.; Wang, R.; Wang, W. Blockchain Technology, Enterprise Risk and Enterprise Performance. Sustainability 2024, 16, 70. https://doi.org/10.3390/su16010070

Zhen Y, Qiao W, Wang R, Wang W. Blockchain Technology, Enterprise Risk and Enterprise Performance. Sustainability. 2024; 16(1):70. https://doi.org/10.3390/su16010070

Chicago/Turabian StyleZhen, Ye, Wen Qiao, Ruyuan Wang, and Wenli Wang. 2024. "Blockchain Technology, Enterprise Risk and Enterprise Performance" Sustainability 16, no. 1: 70. https://doi.org/10.3390/su16010070

APA StyleZhen, Y., Qiao, W., Wang, R., & Wang, W. (2024). Blockchain Technology, Enterprise Risk and Enterprise Performance. Sustainability, 16(1), 70. https://doi.org/10.3390/su16010070