1. Introduction

In recent times, an increasing number of stakeholders have expressed interest in environmental, social, and governance (ESG) risks faced by organizations and their respective management strategies. The integration of ESG elements into a company’s strategy aligns with the concept of risk governance, which covers both macro- and-micro risk management, with the macro level focusing on Corporate Social Responsibility (CSR) requirements and the micro level on operational and financial risks [

1,

2]. Evidence shows that a company’s ESG profile is linked to economic results, with studies such as Giese et al. (2019) [

3] revealing a connection between firm-level ESG ratings and performance. As a result, ESG investing strategies have gained popularity, with investors considering ESG factors in addition to traditional financial elements when making investment decisions. The relevance of ESG investment strategies is supported by the fact that investment managers used ESG criteria to allocate approximately USD 11.6 trillion in U.S. domiciled assets in 2018, representing a 44% increase in two years, according to the US SIF Foundation.

The fact that ESG ratings include information able to affect the firm value has significant effects for a big number of market transactions [

4]. The initial public offerings (IPOs) are perhaps important in the information asymmetry that influence the IPO participants [

5,

6]. Information on IPO issuers is often not complete because they are not subject to the same kind of disclosure as listed companies. Therefore, information that reduces uncertainty is appreciated by IPO participants.

It may be that a higher transparency level of a company’s ESG risks supports a diminution of information asymmetry and creates a stronger request for company ESG disclosure [

7]. Despite the documented need for a better ESG disclosure, the answer of the national and international regulations has been diversified. In fact, the European Union (EU) has forced ESG disclosure from many years, while the United States regulatory bodies have lately excluded ESG disclosure such as the one in the EU. However, considering the investors’ interest, a rising number of organizations have decided to build proprietary ESG ratings (Morgan Stanley Capital International).

Similarly, the concept of a circular economy has gained significant attention in recent years as a model for sustainable development. It promotes a regenerative approach that aims to maintain the value of products, materials, and resources in the economy for as long as possible while minimizing waste generation. In this context, ESG disclosure has emerged as a means of communicating information to stakeholders about a firm’s sustainability performance. Circular economy and ESG disclosure are closely linked, as both promote sustainable practices that aim to minimize negative environmental impacts while creating value for businesses. The adoption of circular economy principles requires firms to design products with a focus on durability, recyclability, and repairability, and to optimize the use of resources. This approach enables firms to reduce their environmental footprint and achieve cost savings through improved resource efficiency. In turn, the adoption of circular economy principles can lead to better ESG performance, as firms are likely to achieve reduced environmental impact, improved social outcomes, and better governance practices. We believe that firms that adopt circular economy principles are likely to benefit from ESG disclosure, particularly in terms of improved performance and reduced IPO underpricing.

One area where the benefits of a circular economy and ESG disclosure may be particularly relevant is in IPO underpricing. The reasons for IPO underpricing are complex and multifaceted, but one factor that has been identified is information asymmetry, where investors lack complete information about the firm’s value and performance. ESG disclosure has been shown to reduce information asymmetry by providing stakeholders with more comprehensive information about a firm’s ESG risks and opportunities. Firms that disclose ESG information are also more likely to be seen as trustworthy and credible, which can increase investor confidence.

Our research aims to investigate the relationship between ESG factors and underpricing in IPOs by utilizing the disclosure report on ESG issued by companies. We posit that this report contains value-relevant information, and therefore can be used to examine the impact of ESG policies on IPO underpricing. This assumption is supported by Dyck et al. (2019) [

8], who found that institutional investors from countries with strong ESG disclosure regulations have a positive impact on companies’ ESG policies. Since institutional investors are often significant IPO stakeholders and regularly communicate with companies during the IPO process, they can influence companies’ ESG policies and decisions to disclose ESG reports.

If, as prior studies show, higher ESG ratings are correlated to better quality disclosures [

9] and a reduced information asymmetry [

10], IPO underpricing should be lesser for firms with a higher ESG rating.

The economic and financial performance as a consequence of ESG practices has been widely studied; some other effects of ESG practices should be analyzed, given the growing interest in those practices of the last years. The interest of the stakeholders and shareholders on ESG practices should not be focused only on economic and financial traditional indicators (ROI, ROE, ROA, ROS, EBITDA, etc.), but also on new indicators of performance. From this, the present study wants to enrich the actual literature showing that there are also other elements affected by ESG disclosure, showing how important it is for companies to invest and to disclose information in terms of ESG. Past studies analyzed only the correlation between ESG ratings and quality disclosure, and in some cases analyzing firm economic and financial performance, but they do not pay attention to how the performance in terms of IPO underpricing is affected by ESG elements, and that, therefore, remains an open question.

The research question consequently aims to analyze the direction of the possible consequence of the presence of the disclosure of non-financial information on the performance in the IPO phase, represented by the underpricing. The analysis has been executed on the European IPOs which took place between 01.01.2017 and 30.04.2021, considering a sample of 100 companies, of which 50 disclosed the ESG report prior to the IPO, and 50 companies, comparable to the previous ones, which did not disclose the report. The target of the research is therefore to comprehend the perception of ESG factors by investors, represented in this analysis by the existence of the ESG report disclosure. The work represents a new contribution concerning the motivation of firms to integrate sustainability elements within their business strategies and to disclose this activity, thus mounting the level of transparency towards all the categories of stakeholders.

To inspect if sustainability reports published prior to the IPO can influence the performance obtained by a firm in the IPO phase as a dependent variable, we used the underpricing during the IPO, which is defined as the initial return on the first day of listing [

11].

Consequently, with the findings that higher ESG ratings are correlated to a reduced information asymmetry, we discover a negative correlation between the ESG disclosure and firm-level IPO underpricing. In fact, our analyzes demonstrate that the disclosure of a sustainable report before an IPO reduces the underpricing and, consequently, the higher disclosure of ESG information is appreciated and valuable to investors. In this sense, this corroborates the fact that the market rewards firms that show disclosure of sustainability factors not only in the long term [

12] but also in the short term during an IPO, accrediting to them a lower level of underpricing and a subsequent higher valuation. Our results are robust since they are confirmed by three different models: (i) MLR, (ii) mixed effect model, and (iii) random forest.

Our results provide new understandings to different areas of investigation in the academic literature.

First, we provide proof that ESG disclosure makes available value-relevant information of new shares issued during an IPO. To the best of our knowledge, this study is the first to show that ESG disclosure is correlated to lower IPO underpricing. Since underpricing is a significant cost for companies that choose to be listed on a financial market [

13], our results suggest that rules issued to improve a company’s quality information in terms of ESG may reduce IPO costs and facilitate the gate for private firms to the capital markets.

Our research findings are consistent with the previous literature that has investigated information asymmetry as an explanation for IPO underpricing. Specifically, Ljungqvist (2007) [

14] highlights information asymmetry as one of the primary reasons for IPO underpricing, which is supported by our study results. Furthermore, our analysis indicates that information asymmetry is a mechanism through which ESG disclosure affects IPO underpricing, contributing to the existing literature on this topic. These findings complement recent studies, such as Lopez-de-Silanes et al. (2019) [

9], which found a positive impact of ESG disclosure on firm disclosure quality, and El Ghoul et al. (2011) [

10], which showed a negative correlation between higher ESG ratings and information asymmetry.

4. Results

The descriptive statistic of each variable is presented in

Table 2.

In

Table 3 the correlation statistics are shown.

The results of the correlation analysis, contrary to our expectations, explain the absence of correlation between the publication of ESG reports and the underpricing.

The results, in line with our expectations, confirm that the variable ESG reporting is statically significant at 10% with a negative impact on the underpricing. This analysis confirms, therefore, the fact that the publication of a sustainable report before an IPO has a positive effect on the underpricing by reducing it. The results seem, therefore, to suggest that companies that publish sustainability reports are perceived to be less risky. Given the various scandals over the past few years related to ESG issues, investors seem to value ESG disclosure rather than being unaware of the related risks/problems the company is facing. Sustainability factors are an essential component to improve and ensure the competitiveness, health, and longevity of a company [

48]. Reporting the business model of a company from an ESG point of view allows investors to observe and consider it in their valuation process.

These results confirm that investors are attributing long-term value to companies that tend to disclose ESG data. This is in line with the tendency of investors to allocate more and more of their capital to companies that seize the green economy as an opportunity, with the aim of protecting their investments from environmental, social, and governance risks [

49]. Companies that would like to list should, therefore, be aligned with this trend by publishing high-quality information about their ESG strategy in order to attract long-term investors with the possibility also of reducing their cost of capital [

12].

Robustness Tests

Several additional analyzes were done in order to harden the results and validate them further. Specifically, we conducted the following tests: (i) VIF test in order to test multicollinearity; (ii) residuals versus fitted plot in order to detect non-linearity, unequal error variances, and outliers; (iii) Breusch–Pagan to test homoscedasticity; and (iv) the Shapiro–Wilk for verifying the normality hypotheses of the MLR model.

Firstly, a VIF test was performed. The results in

Table 5 show that the VIF values do not overcome the critical threshold of 5, typically used to indicate high multicollinearity.

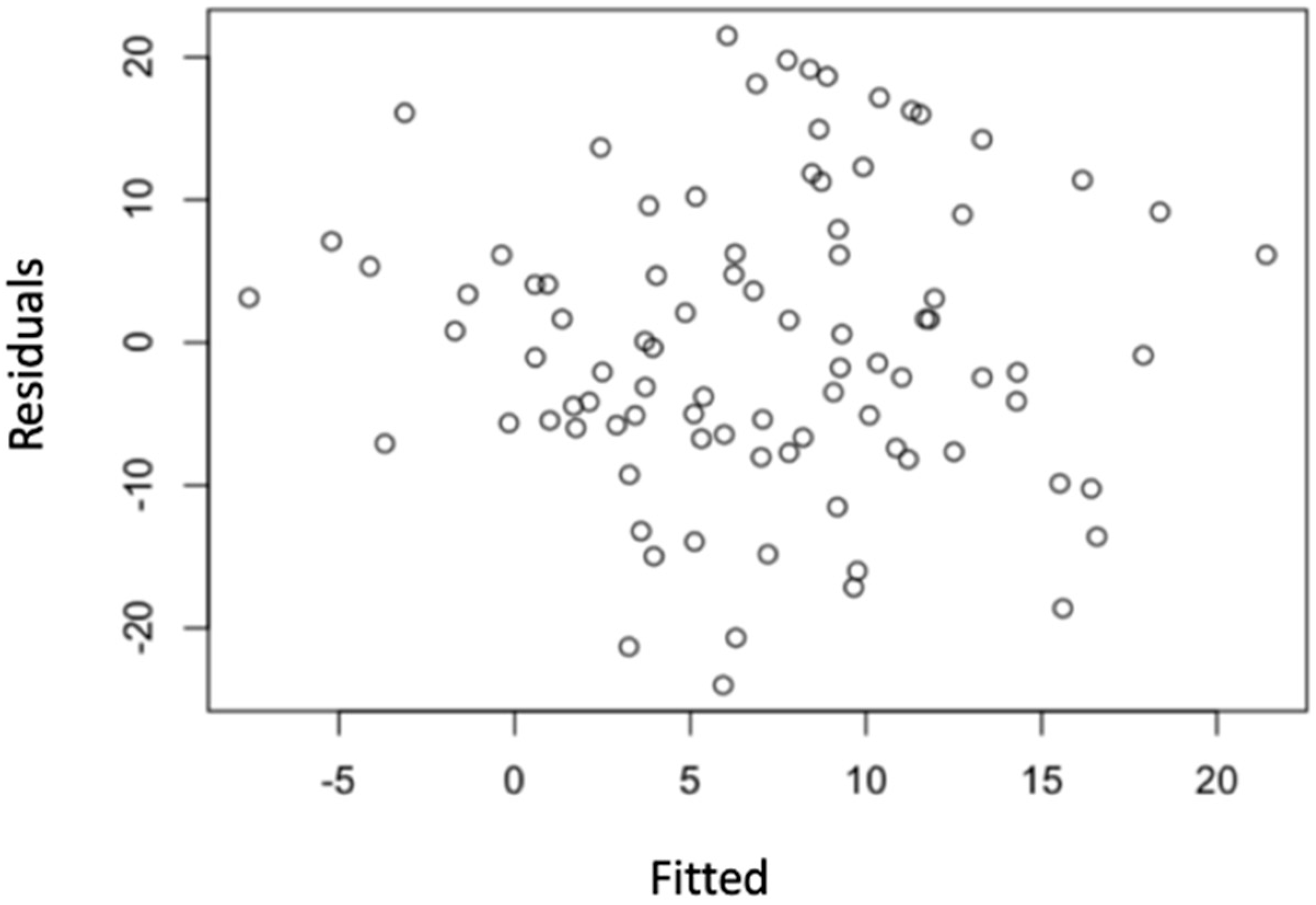

Similarly, the residuals versus fitted plot in

Figure 1 provides proof of the consistency of the linearity hypothesis of the MLR model.

Secondly, the Breusch–Pagan and the Shapiro–Wilk test were performed. Results confirm the homoscedasticity and the normality hypotheses of the MLR model.

However, in order to reinforce our results, we ran the MLF model in two other different versions: (i) in the first we deleted the variable total revenues given its high correlation with the variable total assets; and (ii) in the second version, in order to reduce the impact of outliers, we applied the winsorisation technique at the 95%. Results are shown in

Table 6 and they confirm the previous analysis.

Furthermore, the other two statistical models were performed as robustness tests: the mixed effect model and the random forest model. The mixed effect model is a statistical model which contains both random and fixed effect. The mixed effect model is particularly suitable where measurements are made on clusters of related statistical units. In

Table 7 the results are shown.

In the mixed effect model, the variable ESG reporting is statically significant at 5% with a negative impact on the underpricing. Therefore, the results confirm the previous analysis of the MLR model.

The random forest model is a machine learning model which, by applying the bagging technique, allows us to randomly select a subset of characteristics from each node of a tree. In this sense, past research [

50,

51] have shown that the machine learning model, and specifically the random forest model, are able to perform better than “traditional models” such as logit and MLR. Moreover, machine learning models are robust to outlier and missing data [

51].

However, one of the main issues of this models is their lack of interpretability [

41]. Therefore, in order to interpret the results, the relative variables importance was applied. The relative variables importance shows the variables on a scale ranging from 0 to 1, depending on the number of times they are used by the decision trees [

50]. The more the value tends towards 1, the greater the importance and, therefore, the significance of the variable. The results of the random forest model are shown in

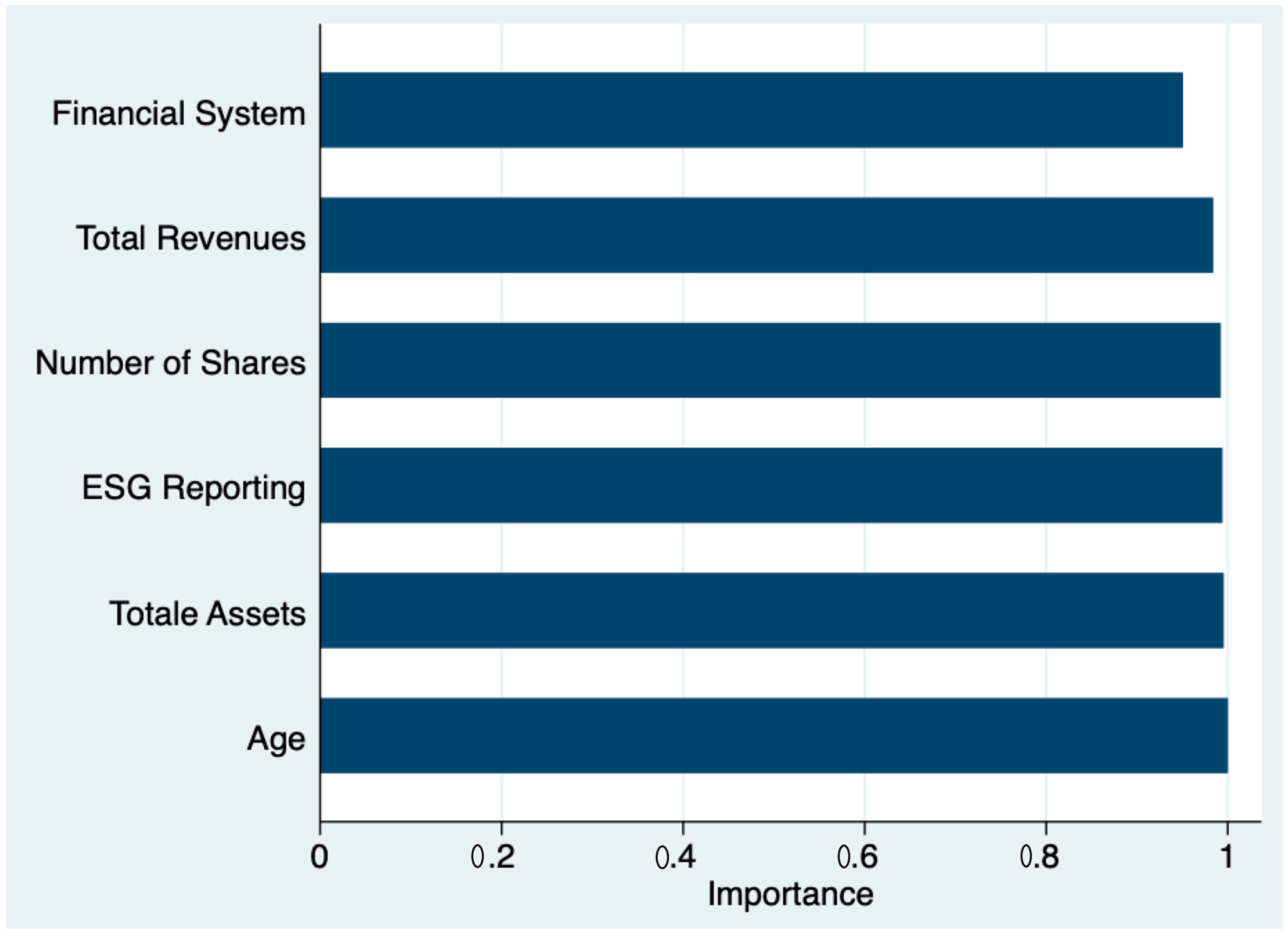

Table 8 and

Figure 2.

The results of our analysis demonstrate the effectiveness and reliability of the random forest model. As shown in

Table 8, the model has a low out-of-bag (OOB) error rate, indicating its ability to accurately predict the underpricing of IPOs.

Furthermore, the variable importance analysis reveals that ESG reporting is one of the most significant variables in the model, with a score near 1, which means it is almost always used in every decision tree. This highlights the importance of ESG reporting in predicting IPO underpricing and suggests that companies that disclose ESG information are perceived as less risky by investors.

Interestingly, the relative importance of ESG reporting is even higher than that of total revenues, suggesting that sustainability variables are becoming increasingly important in comparison to financial variables. This finding is consistent with the growing awareness among investors of the importance of ESG factors in evaluating a company’s performance and long-term viability.

Moreover,

Figure 2 provides further evidence of the significant impact of ESG reporting on IPO underpricing. The plot clearly shows that companies that disclose their ESG performance before an IPO experience lower levels of underpricing compared to those that do not. This finding reinforces the conclusion of our MLR model analysis and underscores the importance of ESG reporting as a tool for reducing information asymmetries and mitigating risk.

Therefore, all the robustness tests have shown the relationship with the underpricing and the significance of publishing an ESG report before an IPO. Our results support the notion that ESG disclosure is a significant factor in predicting IPO underpricing, and our random forest model provides a reliable and accurate means of evaluating the impact of ESG variables on IPO pricing. These findings have important implications for companies seeking to go public, as they suggest that adopting and disclosing ESG strategies and data can increase the likelihood of a successful IPO by reducing perceived risk and increasing investor confidence.

5. Discussion

This study aimed to examine the impact of ESG reporting on underpricing during IPOs. The results showed that ESG reporting is statistically significant with a negative impact on underpricing, indicating that the publication of a sustainable report before an IPO has a positive effect on underpricing by reducing it. This finding suggests that companies that publish sustainability reports are perceived to be less risky, and investors value ESG disclosure as a tool to reduce the risks associated with ESG issues.

The study also found that ESG disclosure Is increasingly important for firms that adopt circular economy principles and disclose their ESG performance. Such disclosure can provide investors with valuable information about a firm’s sustainability performance, particularly in terms of resource efficiency and environmental impact, which can contribute to reducing performance and risk. As a result, firms that disclose their ESG performance are likely to experience reduced IPO underpricing as investors have more complete information about the firm’s value and performance. Our results confirm that stock markets tend to reward the release of ESG data not only in the long term [

12] but also in the short term during an IPO, by attributing to them a higher valuation. Specifically, given the coefficient of the variable ESG reporting in

Table 4 and

Table 7, we can determine that the publication of the ESG reporting can reduce the IPO underpricing by 8% and, thus, its magnitude is extremely significant given the fact that the average IPO underpricing is between 15–25% [

11].

Furthermore, this study contributes to the empirical evidence that investors and stakeholders are increasingly interested in the disclosure of extra financial information and, in general, sustainability. The release of an ESG report can reduce information asymmetries and be considered a transparency tool, making ESG reports a significant factor for the success of an IPO. Companies that are transparent about their ESG practices are more likely to attract investment capital, as investors are increasingly focused on ESG factors.

Moreover, in the context of a circular economy, ESG disclosure can provide investors with valuable information about a firm’s sustainability performance, particularly in terms of resource efficiency and environmental impact. These factors can contribute to reducing performance and risk, which can be communicated through ESG disclosure. As a result, firms that adopt circular economy principles and disclose their ESG performance are likely to experience reduced IPO underpricing, as investors have more complete information about the firm’s value and performance.

The study shows that ESG reporting is a crucial factor in reducing the underpricing of IPOs, and firms that adopt circular economy principles and disclose their ESG performance are likely to experience a reduced IPO underpricing. The research highlights the growing importance of ESG disclosure and sustainability reporting in the business world, where investors and stakeholders are increasingly interested in extra financial information to make informed decisions.

6. Conclusions

In recent years, there has been growing attention towards the role of ESG factors in the financial industry. The increasing importance of ESG disclosure is a result of heightened awareness and concern about the impact of corporations on the environment and society, as well as the belief that strong ESG practices can lead to better long-term financial performance. In this context, knowledge disclosure plays a critical role in capital markets as it helps investors make informed decisions about companies and their potential for growth.

The objective was to demonstrate the importance of knowledge disclosure in terms of ESG information [

14] on capital markets and its impact on firm value, specifically on the underpricing during an IPO. In this sense, this research analyzed the relationship between the disclosure of ESG data/report and the underpricing during an IPO, given the growing interest of investors in ESG companies [

49].

The importance of ESG disclosure in capital markets can be understood in the context of the information asymmetry that often exists between companies and investors. Companies typically have more information about their operations, financials, and prospects than the public, creating an asymmetry of information. This information asymmetry can lead to inefficient capital markets, where investors cannot accurately price securities due to a lack of information. ESG disclosure helps to reduce this information asymmetry by providing investors with more detailed information about a company’s ESG practices. In particular, ESG disclosure can provide valuable information about a company’s potential risks and opportunities related to environmental and social issues. For example, disclosure of a company’s environmental practices can provide insight into the potential costs of compliance with environmental regulations, or the impact of climate change on the company’s operations. Similarly, disclosure of a company’s social practices can provide insight into the company’s treatment of employees, supply chain practices, or community relations. In turn, this information can help investors make more informed decisions about the potential long-term financial performance of a company.

However, our study is limited by the dimension of the sample, which is limited and only focused on European companies, and the type of data used. Secondly, our pairwise sampling procedure did not consider the year of the IPO, even though every comparable IPO was chosen in order to be dated not more than three years. Future research could use a more variable and international sample, by also including different ESG variables in order to analyze the impact of environment, social, and governance variables separately given the limited literature on the matter.

{kind=link}

{kind=link}