Mapping Financial Literacy: A Systematic Literature Review of Determinants and Recent Trends

,

,  ,

,  , and

, and

Abstract

1. Introduction

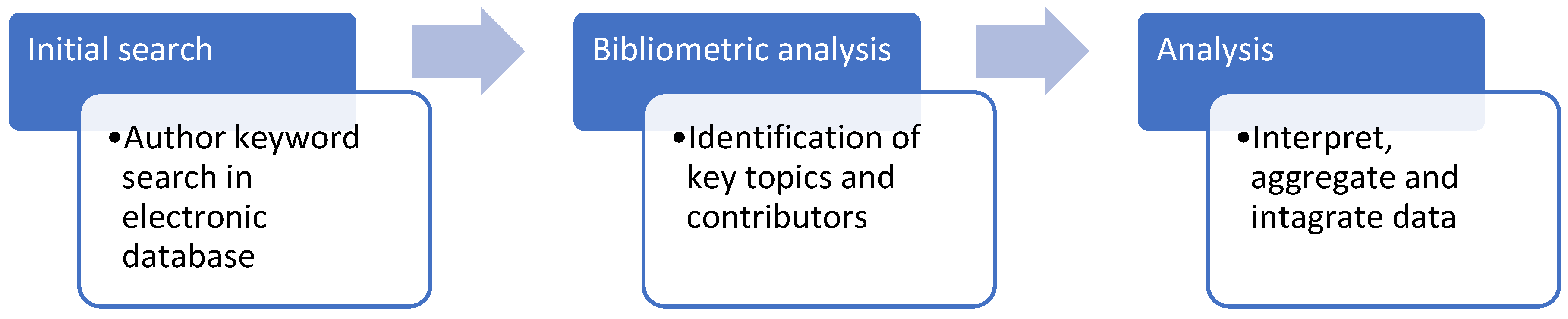

2. Data and Methods

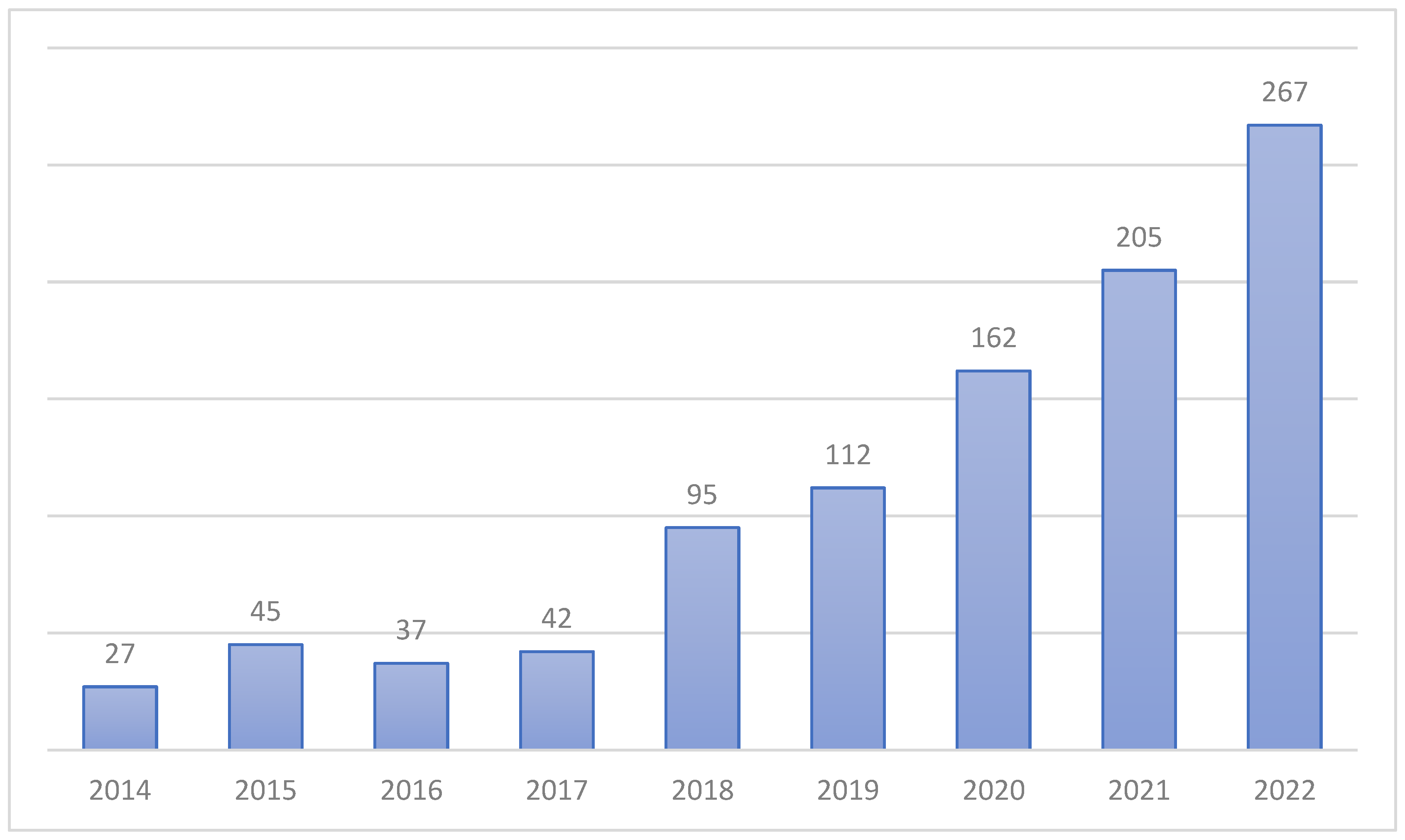

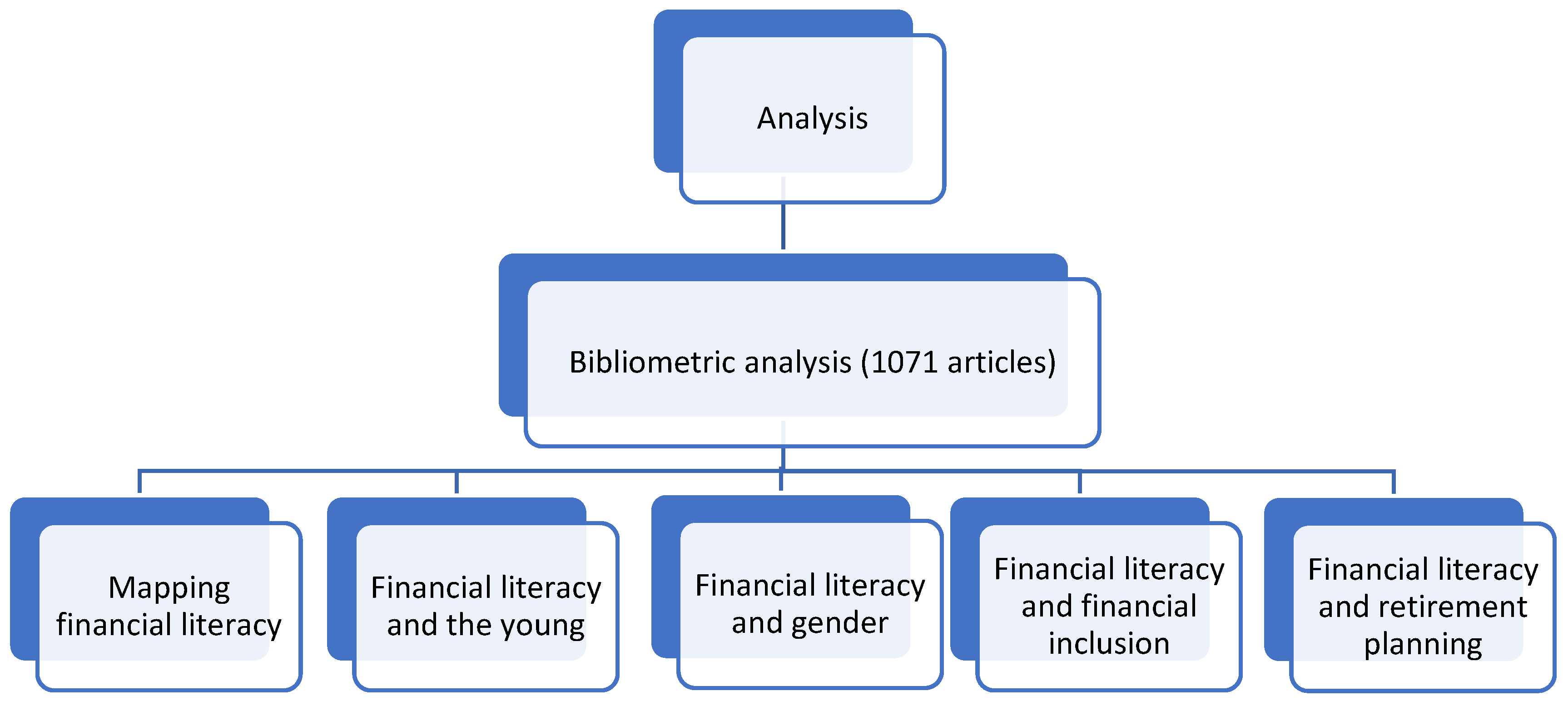

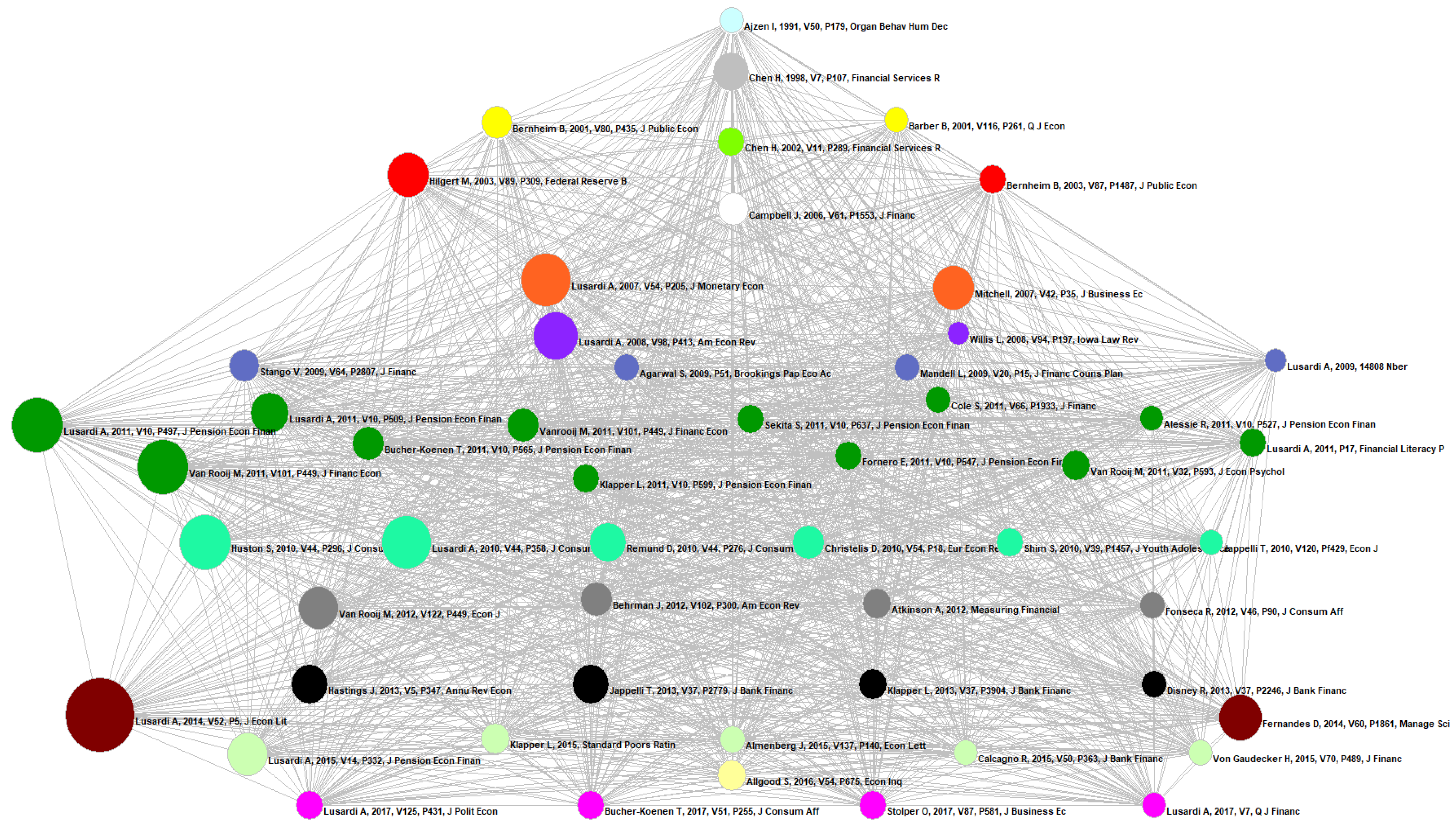

3. Bibliometric Analysis

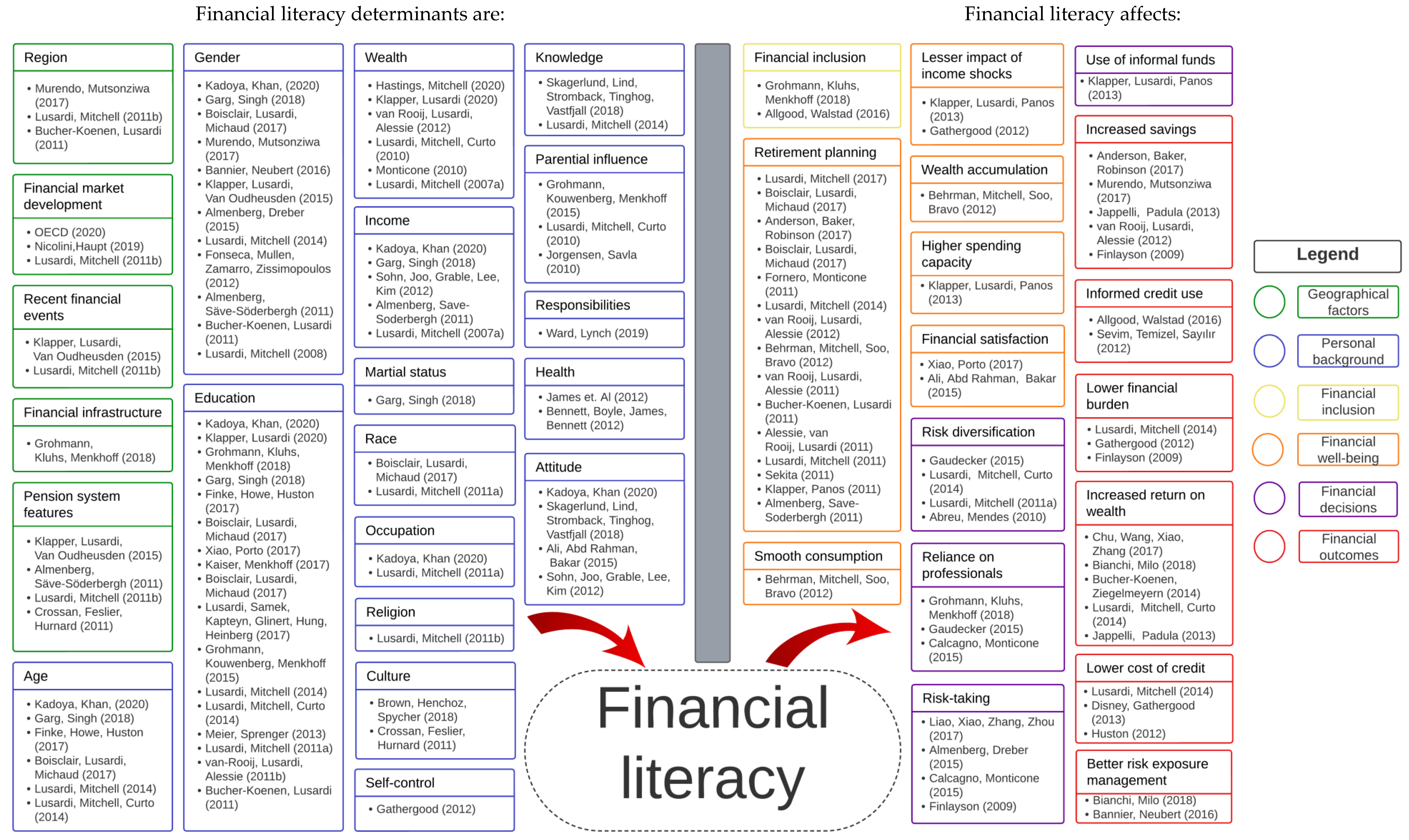

4. Mapping Financial Literacy—Financial Literacy Determinants and Outcomes

5. Trends in Financial Literacy Literature

5.1. Financial Literacy of the Youth

5.2. Financial Literacy and Gender

5.3. Financial Literacy and Financial Inclusion

5.4. Financial Literacy and Retirement Planning

6. Financial Literacy and Technology

6.1. Financial Literacy and Digital Finance

6.2. Digital Financial Literacy

7. Discussion

8. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- OECD. OECD/INFE 2020 International Survey of Adult Financial Literacy. 2020. Available online: www.oecd.org/financial/education/launchoftheoecdinfeglobalfinancialliteracysurveyreport.htm (accessed on 10 October 2022).

- Lusardi, A.; Mitchell, O.S. The economic importance of financial literacy: Theory and evidence. J. Econ. Lit. 2014, 52, 5–44. [Google Scholar] [CrossRef] [PubMed]

- Huston, S.J. Measuring financial literacy. J. Consum. Aff. 2010, 44, 296–316. [Google Scholar] [CrossRef]

- U.S. Financial Literacy and Education Commission. U.S. National Strategy for Financial Literacy 2020, U.S. Department of the Treasury. 2020. Available online: https://home.treasury.gov/policy-issues/consumer-policy/financial-literacy-and-education-commission (accessed on 28 November 2022).

- Nicolini, G.; Haupt, M. The assessment of financial literacy: New evidence from Europe. Int. J. Financ. Stud. 2019, 7, 54. [Google Scholar] [CrossRef]

- Klapper, L.; Lusardi, A.; Van Oudheusden, P. Financial literacy around the world. World Bank 2015, 2, 218–237. [Google Scholar]

- Pașa, A.T.; Picatoste, X.; Gherghina, E.M. Financial Literacy and Economic Growth: How Eastern Europe is Doing? Economics 2022, 16, 27–42. [Google Scholar] [CrossRef]

- Grohmann, A.; Klühs, T.; Menkhoff, L. Does financial literacy improve financial inclusion? Cross country evidence. World Dev. 2018, 111, 84–96. [Google Scholar] [CrossRef]

- French, D.; McKillop, D. Financial literacy and over-indebtedness in low-income households. Int. Rev. Financ. Anal. 2016, 48, 1–11. [Google Scholar] [CrossRef]

- Fernandes, D.; Lynch, J.G., Jr.; Netemeyer, R.G. Financial literacy, financial education, and downstream financial behaviors. Manag. Sci. 2014, 60, 1861–1883. [Google Scholar] [CrossRef]

- Goyal, K.; Kumar, S. Financial literacy: A systematic review and bibliometric analysis. Int. J. Consum. Stud. 2020, 45, 80–105. [Google Scholar] [CrossRef]

- Xiao, Y.; Watson, M. Guidance on conducting a systematic literature review. J. Plan. Educ. Res. 2019, 39, 93–112. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior. Organ. Behave. Human Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Chen, H.; Volpe, R.P. An analysis of personal financial literacy among college students. Financ. Serv. Rev. 1998, 7, 107–128. [Google Scholar] [CrossRef]

- Bernheim, B.D.; Garrett, D.M.; Maki, D.M. Education and saving: The long-term effects of high school financial curriculum mandates. J. Public Econ. 2001, 80, 435–465. [Google Scholar] [CrossRef]

- Barber, B.M.; Odean, T. Boys will be boys: Gender, overconfidence, and common stock investment. Q. J. Econ. 2001, 116, 261–292. [Google Scholar] [CrossRef]

- Campbell, J.Y. Household finance. J. Financ. 2006, 61, 1553–1604. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Baby boomer retirement security: The roles of planning, financial literacy, and housing wealth. J. Monet. Econ. 2007, 54, 205–224. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial Literacy and Retirement Preparedness: Evidence and Implications for Financial Education. Bus. Econ. 2007, 42, 35–44. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Planning and financial literacy: How do women fare? Am. Econ. Rev. 2008, 98, 413–417. [Google Scholar] [CrossRef]

- Hilgert, M.A.; Hogarth, J.M.; Beverly, S.G. Household financial management: The connection between knowledge and behavior. Fed. Res. Bull. 2003, 89, 309–322. [Google Scholar]

- Bernheim, B.D.; Garrett, D.M. The effects of financial education in the workplace: Evidence from a survey of households. J. Public Econ. 2003, 87, 1487–1519. [Google Scholar] [CrossRef]

- Willis, L.E. Against financial-literacy education. Iowa L. Rev. 2008, 94, 197. [Google Scholar]

- Stango, V.; Zinman, J. Exponential growth bias and household finance. J. Financ. 2009, 64, 2807–2849. [Google Scholar] [CrossRef]

- Agarwal, S.; Driscoll, J.C.; Gabaix, X.; Laibson, D. The age of reason: Financial decisions over the life-cycle with implications for regulation. Brook. Pap. Econ. Act. 2009, 40, 51–118. [Google Scholar] [CrossRef]

- Mandell, L.; Klein, L.S. The impact of financial literacy education on subsequent financial behavior. J. Financ. Couns. Plan. 2009, 20, 15–24. [Google Scholar]

- Lusardi, A.; Tufano, P. Debt Literacy, Financial Experiences and over Indebtedness. 2009. Available online: https://www.nber.org/papers/w14808 (accessed on 28 November 2022).

- Lusardi, A.; Mitchell, O.S. Financial literacy around the world: An overview. J. Pension Econ. Financ. 2011, 10, 497–508. [Google Scholar] [CrossRef] [PubMed]

- Lusardi, A.; Mitchell, O.S. Financial literacy and retirement planning in the United States. J. Pension Econ. Financ. 2011, 10, 509–525. [Google Scholar] [CrossRef]

- Van Rooij, M.; Lusardi, A.; Alessie, R. Financial literacy and stock market participation. J. Financ. Econ. 2011, 101, 449–472. [Google Scholar] [CrossRef]

- Sekita, S. Financial literacy and retirement planning in Japan. J. Pension Econ. Financ. 2011, 10, 637–656. [Google Scholar] [CrossRef]

- Cole, S.; Sampson, T.; Zia, B. Prices or knowledge? What drives demand for financial services in emerging markets? J. Finance. 2011, 66, 1933–1967. [Google Scholar] [CrossRef]

- Alessie, R.; Van Rooij, M.; Lusardi, A. Financial literacy and retirement preparation in the Netherlands. J. Pension Econ. Financ. 2011, 10, 527–545. [Google Scholar] [CrossRef]

- Bucher-Koenen, T.; Lusardi, A. Financial literacy and retirement planning in Germany. J. Pension Econ. Financ. 2011, 10, 565–584. [Google Scholar] [CrossRef]

- Klapper, L.; Panos, G.A. Financial literacy and retirement planning: The Russian case. J. Pension Econ. Financ. 2011, 10, 599–618. [Google Scholar] [CrossRef]

- Fornero, E.; Monticone, C. Financial literacy and pension plan participation in Italy. J. Pension Econ. Financ. 2011, 10, 547–564. [Google Scholar] [CrossRef]

- Van Rooij, M.C.; Lusardi, A.; Alessie, R.J. Financial literacy and retirement planning in the Netherlands. J. Econ. Psychol. 2011, 32, 593–608. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial literacy and planning: Implications for retirement wellbeing. Natl. Bur. Econ. Res. 2011, w17078. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S.; Curto, V. Financial literacy among the young. J. Consum. Aff. 2010, 44, 358–380. [Google Scholar] [CrossRef]

- Remund, D.L. Financial literacy explicated: The case for a clearer definition in an increasingly complex economy. J. Consum. Aff. 2010, 44, 276–295. [Google Scholar] [CrossRef]

- Christelis, D.; Jappelli, T.; Padula, M. Cognitive abilities and portfolio choice. Eur. Econ. Rev. 2010, 54, 18–38. [Google Scholar] [CrossRef]

- Shim, S.; Barber, B.L.; Card, N.A.; Xiao, J.J.; Serido, J. Financial socialization of first-year college students: The roles of parents, work, and education. J. Youth Adolesc. 2010, 39, 1457–1470. [Google Scholar] [CrossRef]

- Jappelli, T. Economic literacy: An international comparison. Econ. J. 2010, 120, 429–451. [Google Scholar] [CrossRef]

- Van Rooij, M.C.; Lusardi, A.; Alessie, R.J. Financial literacy, retirement planning and household wealth. Econ. J. 2012, 122, 449–478. [Google Scholar] [CrossRef]

- Behrman, J.R.; Mitchell, O.S.; Soo, C.K.; Bravo, D. How financial literacy affects household wealth accumulation. Am. Econ. Rev. 2012, 102, 300–304. [Google Scholar] [CrossRef]

- Atkinson, A.; Messy, F.A. Measuring financial literacy: Results of the OECD/International Network on Financial Education (INFE) pilot study. OECD Work. Pap. Financ. Insur. Priv. Pensions 2012, 15. [Google Scholar] [CrossRef]

- Fonseca, R.; Mullen, K.J.; Zamarro, G.; Zissimopoulos, J. What explains the gender gap in financial literacy? The role of household decision making. J. Consum. Aff. 2012, 46, 90–106. [Google Scholar] [CrossRef] [PubMed]

- Hastings, J.S.; Madrian, B.C.; Skimmyhorn, W.L. Financial literacy, financial education, and economic outcomes. Annu. Rev. Econ. 2013, 5, 347–373. [Google Scholar] [CrossRef]

- Jappelli, T.; Padula, M. Investment in financial literacy and saving decisions. J. Bank. Financ. 2013, 37, 2779–2792. [Google Scholar] [CrossRef]

- Klapper, L.; Lusardi, A.; Panos, G.A. Financial literacy and its consequences: Evidence from Russia during the financial crisis. J. Bank. Financ. 2013, 37, 3904–3923. [Google Scholar] [CrossRef]

- Disney, R.; Gathergood, J. Financial literacy and consumer credit portfolios. J. Bank. Financ. 2013, 37, 2246–2254. [Google Scholar] [CrossRef]

- Lusardi, A.; Tufano, P. Debt literacy, financial experiences, and overindebtedness. J. Pension Econ. Financ. 2015, 14, 332–368. [Google Scholar] [CrossRef]

- Almenberg, J.; Dreber, A. Gender, stock market participation and financial literacy. Econ. Lett. 2015, 137, 140–142. [Google Scholar] [CrossRef]

- Calcagno, R.; Monticone, C. Financial literacy and the demand for financial advice. J. Bank. Financ. 2015, 50, 363–380. [Google Scholar] [CrossRef]

- Allgood, S.; Walstad, W.B. The effects of perceived and actual financial literacy on financial behaviors. Econ. Inq. 2016, 54, 675–697. [Google Scholar] [CrossRef]

- Gaudecker, H.M.V. How does household portfolio diversification vary with financial literacy and financial advice? J. Financ. 2015, 70, 489–507. [Google Scholar] [CrossRef]

- Lusardi, A.; Michaud, P.C.; Mitchell, O.S. Optimal financial knowledge and wealth inequality. J. Political Econ. 2017, 125, 431–477. [Google Scholar] [CrossRef]

- Bucher-Koenen, T.; Lusardi, A.; Alessie, R.; Van Rooij, M. How financially literate are women? An overview and new insights. J. Consum. Aff. 2017, 51, 255–283. [Google Scholar] [CrossRef]

- Stolper, O.A.; Walter, A. Financial literacy, financial advice, and financial behavior. J. Bus. Econ. 2017, 87, 581–643. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. How ordinary consumers make complex economic decisions: Financial literacy and retirement readiness. Q. J. Financ. 2017, 7, 1750008. [Google Scholar] [CrossRef]

- Drexler, A.; Fischer, G.; Schoar, A. Keeping it simple: Financial literacy and rules of thumb. Am. Econ. J. Appl. Econ. 2014, 6, 1–31. [Google Scholar] [CrossRef]

- Kaiser, T.; Menkhoff, L. Does financial education impact financial literacy and financial behavior, and if so, when? World Bank Econ. Rev. 2017, 31, 611–630. [Google Scholar] [CrossRef]

- Servon, L.J.; Kaestner, R. Consumer financial literacy and the impact of online banking on the financial behavior of lower-income bank customers. J. Consum. Aff. 2008, 42, 271–305. [Google Scholar] [CrossRef]

- Gathergood, J. Self-control, financial literacy and consumer over-indebtedness. J. Econ. Psychol. 2012, 33, 590–602. [Google Scholar] [CrossRef]

- Grohmann, A.; Kouwenberg, R.; Menkhoff, L. Childhood roots of financial literacy. J. Econ. Psychol. 2015, 51, 114–133. [Google Scholar] [CrossRef]

- Sohn, S.H.; Joo, S.H.; Grable, J.E.; Lee, S.; Kim, M. Adolescents’ financial literacy: The role of financial socialization agents, financial experiences, and money attitudes in shaping financial literacy among South Korean youth. J. Adolesc. 2012, 35, 969–980. [Google Scholar] [CrossRef] [PubMed]

- Skagerlund, K.; Lind, T.; Strömbäck, C.; Tinghög, G.; Västfjäll, D. Financial literacy and the role of numeracy–How individuals’ attitude and affinity with numbers influence financial literacy. J. Behav. Exp. Econ. 2018, 74, 18–25. [Google Scholar] [CrossRef]

- Atkinson, A.; Messy, F.A. Assessing financial literacy in 12 countries: An OECD/INFE international pilot exercise. J. Pension Econ. Financ. 2011, 10, 657–665. [Google Scholar] [CrossRef]

- Murendo, C.; Mutsonziwa, K. Financial literacy and savings decisions by adult financial consumers in Zimbabwe. Int. J. Consum. Stud. 2017, 41, 95–103. [Google Scholar] [CrossRef]

- Almenberg, J.; Säve-Söderbergh, J. Financial literacy and retirement planning in Sweden. J. Pension Econ. Financ. 2011, 10, 585–598. [Google Scholar] [CrossRef]

- Crossan, D.; Feslier, D.; Hurnard, R. Financial literacy and retirement planning in New Zealand. J. Pension Econ. Financ. 2011, 10, 619–635. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial literacy and retirement planning: New evidence from the Rand American Life Panel. Mich. Retire. Res. Cent. Res. Pap. 2007, 157. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S.; Curto, V. Financial literacy and financial sophistication in the older population. J. Pension Econ. Financ. 2014, 13, 347–366. [Google Scholar] [CrossRef]

- Ali, A.; Rahman, M.S.A.; Bakar, A. Financial satisfaction and the influence of financial literacy in Malaysia. Soc. Indic. Res. 2015, 120, 137–156. [Google Scholar] [CrossRef]

- Kadoya, Y.; Khan, M.S.R. What determines financial literacy in Japan? J. Pension Econ. Financ. 2020, 19, 353–371. [Google Scholar] [CrossRef]

- Garg, N.; Singh, S. Financial literacy among youth. Int. J. Soc. Econ. 2018, 45, 173–186. [Google Scholar] [CrossRef]

- Finke, M.S.; Howe, J.S.; Huston, S.J. Old age and the decline in financial literacy. Manag. Sci. 2017, 63, 213–230. [Google Scholar] [CrossRef]

- Boisclair, D.; Lusardi, A.; Michaud, P.C. Financial literacy and retirement planning in Canada. J. Pension Econ. Financ. 2017, 16, 277–296. [Google Scholar] [CrossRef]

- Bannier, C.E.; Neubert, M. Gender differences in financial risk taking: The role of financial literacy and risk tolerance. Econ. Lett. 2016, 145, 130–135. [Google Scholar] [CrossRef]

- Klapper, L.; Lusardi, A. Financial literacy and financial resilience: Evidence from around the world. Financ. Manag. 2020, 49, 589–614. [Google Scholar] [CrossRef]

- Xiao, J.J.; Porto, N. Financial education and financial satisfaction: Financial literacy, behavior, and capability as mediators. Int. J. Bank Mark. 2017, 35, 805–817. [Google Scholar] [CrossRef]

- Lusardi, A.; Samek, A.; Kapteyn, A.; Glinert, L.; Hung, A.; Heinberg, A. Visual tools and narratives: New ways to improve financial literacy. J. Pension Econ. Financ. 2017, 16, 297–323. [Google Scholar] [CrossRef]

- Meier, S.; Sprenger, C.D. Discounting financial literacy: Time preferences and participation in financial education programs. J. Econ. Behav. Organ. 2013, 95, 159–174. [Google Scholar] [CrossRef]

- Hastings, J.; Mitchell, O.S. How financial literacy and impatience shape retirement wealth and investment behaviors. J. Pension Econ. Financ. 2020, 19, 1–20. [Google Scholar] [CrossRef] [PubMed]

- Monticone, C. How much does wealth matter in the acquisition of financial literacy? J. Consum. Aff. 2010, 44, 403–422. [Google Scholar] [CrossRef]

- Brown, M.; Henchoz, C.; Spycher, T. Culture and financial literacy: Evidence from a within-country language border. J. Econ. Behav. Organ. 2018, 150, 62–85. [Google Scholar] [CrossRef]

- Jorgensen, B.L.; Savla, J. Financial literacy of young adults: The importance of parental socialization. Fam. Relat. 2010, 59, 465–478. [Google Scholar] [CrossRef]

- Ward, A.F.; Lynch, J.G., Jr. On a need-to-know basis: How the distribution of responsibility between couples shapes financial literacy and financial outcomes. J. Consum. Res. 2019, 45, 1013–1036. [Google Scholar] [CrossRef]

- James, B.D.; Boyle, P.A.; Bennett, J.S.; Bennett, D.A. The impact of health and financial literacy on decision making in community-based older adults. Gerontology 2012, 58, 531–539. [Google Scholar] [CrossRef]

- Bennett, J.S.; Boyle, P.A.; James, B.D.; Bennett, D.A. Correlates of health and financial literacy in older adults without dementia. BMC Geriatr. 2012, 12, 1–9. [Google Scholar] [CrossRef]

- Anderson, A.; Baker, F.; Robinson, D.T. Precautionary savings, retirement planning and misperceptions of financial literacy. J. Financ. Econ. 2017, 126, 383–398. [Google Scholar] [CrossRef]

- Abreu, M.; Mendes, V. Financial literacy and portfolio diversification. Quant. Financ. 2010, 10, 515–528. [Google Scholar] [CrossRef]

- Liao, L.; Xiao, J.J.; Zhang, W.; Zhou, C. Financial literacy and risky asset holdings: Evidence from China. Account. Financ. 2017, 57, 1383–1415. [Google Scholar] [CrossRef]

- Finlayson, A. Financialisation, financial literacy and asset-based welfare. Br. J. Politics Int. Relat. 2009, 11, 400–421. [Google Scholar] [CrossRef]

- Sevim, N.; Temizel, F.; Sayılır, Ö. The effects of financial literacy on the borrowing behavior of Turkish financial consumers. Int. J. Consum. Stud. 2012, 36, 573–579. [Google Scholar] [CrossRef]

- Chu, Z.; Wang, Z.; Xiao, J.J.; Zhang, W. Financial literacy, portfolio choice and financial well-being. Soc. Indic. Res. 2017, 132, 799–820. [Google Scholar] [CrossRef]

- Bianchi, M. Financial literacy and portfolio dynamics. J. Financ. 2018, 73, 831–859. [Google Scholar] [CrossRef]

- Bucher-Koenen, T.; Ziegelmeyer, M. Once burned, twice shy? Financial literacy and wealth losses during the financial crisis. Rev. Financ. 2014, 18, 2215–2246. [Google Scholar] [CrossRef]

- Huston, S.J. Financial literacy and the cost of borrowing. Int. J. Consum. Stud. 2012, 36, 566–572. [Google Scholar] [CrossRef]

- Moreno-Herrero, D.; Salas-Velasco, M.; Sánchez-Campillo, J. Factors that influence the level of financial literacy among young people: The role of parental engagement and students’ experiences with money matters. Child. Youth Serv. Rev. 2018, 95, 334–351. [Google Scholar] [CrossRef]

- Breitbach, E.; Walstad, W.B. Financial literacy and financial behavior among young adults in the United States. In Economic Competence and Financial Literacy of Young Adults—Status and Challenges; Verlag Barbara Budrich: Leverkusen, Germany, 2016; pp. 81–100. [Google Scholar]

- Folke, T.; Gjorgjiovska, J.; Paul, A.; Jakob, L.; Ruggeri, K. Asset: A new measure of economic and financial literacy. Eur. J. Psychol. Assess. 2021, 37, 65–80. [Google Scholar] [CrossRef]

- Caplinska, A.; Ohotina, A. Analysis of financial literacy tendencies with young people. Entrep. Sustain. Issues 2019, 6, 1736–1749. [Google Scholar] [CrossRef]

- Taft, M.K.; Hosein, Z.Z.; Mehrizi, S.M.T.; Roshan, A. The relation between financial literacy, financial wellbeing and financial concerns. Int. J. Bus. Manag. 2013, 8, 63–75. [Google Scholar] [CrossRef]

- Shim, S.; Serido, J.; Tang, C.; Card, N. Socialization processes and pathways to healthy financial development for emerging young adults. J. Appl. Dev. Psychol. 2015, 38, 29–38. [Google Scholar] [CrossRef]

- Abdullah, N.; Fazli, S.M.; Muhammad Arif, A.M. The Relationship between Attitude towards Money, Financial Literacy and Debt Management with Young Worker’s Financial Well-being. Pertanika J. Soc. Sci. Humanit. 2019, 27, 361–378. [Google Scholar]

- Mata, O. The effect of financial literacy and gender on retirement planning among young adults. Int. J. Bank Mark. 2021, 39, 1068–1090. [Google Scholar] [CrossRef]

- Munyuki, T.; Jonah, C.M.P. The nexus between financial literacy and entrepreneurial success among young entrepreneurs from a low-income community in Cape Town: A mixed-method analysis. J. Entrep. Emerg. Econ. 2021, 14, 137–157. [Google Scholar] [CrossRef]

- Bilal, M.A.; Khan, H.H.; Irfan, M.; Ul Haq, S.M.; Ali, M.; Kakar, A.; Ahmed, W.; Rauf, A. Influence of Financial Literacy and Educational Skills on Entrepreneurial Intent: Empirical Evidence from Young Entrepreneurs of Pakistan. J. Asian Financ. Econ. Bus. 2021, 8, 697–710. [Google Scholar]

- Gathergood, J.; Weber, J. Financial literacy, present bias and alternative mortgage products. J. Bank. Financ. 2017, 78, 58–83. [Google Scholar] [CrossRef]

- Lusardi, A.; Tufano, P. Teach workers about the perils of debt. Harv. Bus. Rev. 2009, 87, 22–24. [Google Scholar]

- Van Rooij, M.; Lusardi, A.; Alessie, R. Financial Literacy and Stock Market Participation. National Bureau of Economic Research. 2007. Available online: https://www.nber.org/papers/w13565 (accessed on 18 December 2007).

- Hastings, J.S.; Tejeda-Ashton, L. Financial literacy, information, and demand elasticity: Survey and experimental evidence from Mexico. Natl. Bur. Econ. Res. 2008, w14538. [Google Scholar] [CrossRef]

- Lusardi, A. Financial literacy and financial education: Review and policy implications. NFI Policy Brief 2006, 2006-PB, 11. [Google Scholar] [CrossRef]

- Dundure, E.; Sloka, B. Financial Literacy Self-Evaluation of Young People in Latvia. Eur. Integr. Stud. 2021, 15, 160–169. [Google Scholar] [CrossRef]

- Fletschner, D.; Mesbah, D. Gender disparity in access to information: Do spouses share what they know? World Dev. 2011, 39, 1422–1433. [Google Scholar] [CrossRef]

- Chen, H.; Volpe, R.P. Gender differences in personal financial literacy among college students. Financ. Serv. Rev. 2002, 11, 289–307. [Google Scholar]

- Siegfried, C.; Wuttke, E. What Influences the Financial Literacy of Young Adults? A Combined Analysis of Socio-Demographic Characteristics and Delay of Gratification. Front. Psychol. 2021, 12, 5318. [Google Scholar] [CrossRef] [PubMed]

- Lučić, A.; Barbić, D.; Uzelac, M. The role of financial education in adolescent consumers’ financial knowledge enhancement. Market-Tržište 2020, 32, 115–130. [Google Scholar] [CrossRef]

- Shim, S.; Xiao, J.J.; Barber, B.L.; Lyons, A.C. Pathways to life success: A conceptual model of financial well-being for young adults. J. Appl. Dev. Psychol. 2009, 30, 708–723. [Google Scholar] [CrossRef]

- Bhatia, S.; Chawla, D.; Singh, S. Determinants of financial literacy of young adults: Testing the influence of parents and socio-demographic variables. Int. J. Indian Cult. Bus. Manag. 2021, 22, 256–271. [Google Scholar] [CrossRef]

- Pandey, A.; Ashta, A.; Spiegelman, E.; Sutan, A. Catch them young: Impact of financial socialization, financial literacy and attitude towards money on financial well-being of young adults. Int. J. Consum. Stud. 2020, 44, 531–541. [Google Scholar]

- Vijaykumar, J.H. The Association of Financial Socialization with Financial Self-Efficacy and Autonomy: A Study of Young Students in India. J. Fam. Econ. Issues 2022, 43, 397–414. [Google Scholar] [CrossRef]

- Bamforth, J.; Jebarajakirthy, C.; Geursen, G. Understanding undergraduates’ money management behaviour: A study beyond financial literacy. Int. J. Bank Mark. 2018, 36, 1285–1310. [Google Scholar] [CrossRef]

- Esmail Alekam, J.M. The effect of family, peer, behavior, saving and spending behavior on financial literacy among young generations. Int. J. Organ. Leadersh. 2018, 7, 309–323. [Google Scholar] [CrossRef]

- Pahlevan Sharif, S.; Ahadzadeh, A.S.; Turner, J.J. Gender differences in financial literacy and financial behaviour among young adults: The role of parents and information seeking. J. Fam. Econ. Issues 2020, 41, 672–690. [Google Scholar] [CrossRef]

- Zsoter, B. Examining the Financial Literacy of Young Adults. Public Financ. Q. 2018, 63, 39–54. [Google Scholar]

- Cwynar, A.; Cwynar, W.; Patena, W.; Sibanda, W. Young adults’ financial literacy and overconfidence bias in debt markets. Int. J. Bus. Perform. Manag. 2020, 21, 95–113. [Google Scholar] [CrossRef]

- Mancebon, M.J.; Ximénez-de-Embún, D.P.; Mediavilla, M.; Gómez-Sancho, J.M. Factors that influence the financial literacy of young Spanish consumers. Int. J. Consum. Stud. 2019, 43, 227–235. [Google Scholar] [CrossRef]

- Totenhagen, C.J.; Casper, D.M.; Faber, K.M.; Bosch, L.A.; Wiggs, C.B.; Borden, L.M. Youth financial literacy: A review of key considerations and promising delivery methods. J. Fam. Econ. Issues 2015, 36, 167–191. [Google Scholar] [CrossRef]

- Potrich, A.C.G.; Vieira, K.M.; Kirch, G. How well do women do when it comes to financial literacy? Proposition of an indicator and analysis of gender differences. J. Behav. Exp. Financ. 2018, 17, 28–41. [Google Scholar] [CrossRef]

- Lotto, J. Understanding sociodemographic factors influencing households’ financial literacy in Tanzania. Cogent Econ. Financ. 2020, 8, 1792152. [Google Scholar] [CrossRef]

- Rink, U.; Walle, Y.M.; Klasen, S. The financial literacy gender gap and the role of culture. Q. Rev. Econ. Financ. 2021, 80, 117–134. [Google Scholar] [CrossRef]

- Bahovec, V.; Barbić, D.; Palić, I. The regression analysis of individual financial performance: Evidence from Croatia. Business Systems Research. Int. J. Soc. Adv. Innov. Res. Econ. 2017, 8, 1–13. [Google Scholar] [CrossRef]

- Preston, A.C.; Wright, R.E. Understanding the gender gap in financial literacy: Evidence from Australia. Econ. Rec. 2019, 95, 1–29. [Google Scholar] [CrossRef]

- Driva, A.; Lührmann, M.; Winter, J. Gender differences and stereotypes in financial literacy: Off to an early start. Econ. Lett. 2016, 146, 143–146. [Google Scholar] [CrossRef]

- Agnew, S.; Cameron-Agnew, T. The influence of consumer socialisation in the home on gender differences in financial literacy. Int. J. Consum. Stud. 2015, 39, 630–638. [Google Scholar] [CrossRef]

- Bottazzi, L.; Lusardi, A. Stereotypes in financial literacy: Evidence from PISA. J. Corp. Financ. 2021, 71, 101831. [Google Scholar] [CrossRef]

- Longobardi, S.; Pagliuca, M.M.; Regoli, A. Can problem-solving attitudes explain the gender gap in financial literacy? Evidence from Italian students’ data. Qual. Quant. 2018, 52, 1677–1705. [Google Scholar] [CrossRef]

- Arellano, A.; Cámara, N.; Tuesta, D. Explaining the gender gap in financial literacy: The role of non-cognitive skills. Econ. Notes Rev. Bank. Financ. Monet. Econ. 2018, 47, 495–518. [Google Scholar] [CrossRef]

- Tinghög, G.; Ahmed, A.; Barrafrem, K.; Lind, T.; Skagerlund, K.; Västfjäll, D. Gender differences in financial literacy: The role of stereotype threat. J. Econ. Behav. Organ. 2021, 192, 405–416. [Google Scholar] [CrossRef]

- Kubak, M.; Gavurova, B.; Majcherova, N.; Nemec, J. Gender Differences in Rationality and Financial Literacy. Transform. Bus. Econ. 2021, 20, 558–571. [Google Scholar]

- Al-Bahrani, A.; Buser, W.; Patel, D. Early causes of financial disquiet and the gender gap in financial literacy: Evidence from college students in the Southeastern United States. J. Fam. Econ. Issues 2020, 41, 558–571. [Google Scholar] [CrossRef]

- Moon, C.S.; Ohk, K.; Choi, C. Gender differences in financial literacy among Chinese university students and the influential factors. Asian Women 2014, 30, 3–25. [Google Scholar]

- Yu, K.M.; Wu, A.M.; Chan, W.S.; Chou, K.L. Gender differences in financial literacy among Hong Kong workers. Educ. Gerontol. 2015, 41, 315–326. [Google Scholar] [CrossRef]

- Marinelli, N.; Mazzoli, C.; Palmucci, F. How does gender really affect investment behavior? Econ. Lett. 2017, 151, 58–61. [Google Scholar] [CrossRef]

- Cupák, A.; Fessler, P.; Schneebaum, A. Gender differences in risky asset behavior: The importance of self-confidence and financial literacy. Financ. Res. Lett. 2021, 42, 101880. [Google Scholar] [CrossRef]

- Bannier, C.; Meyll, T.; Röder, F.; Walter, A. The gender gap in ‘Bitcoin literacy’. J. Behav. Exp. Financ. 2019, 22, 129–134. [Google Scholar] [CrossRef]

- Chen, J.; Jiang, J.; Liu, Y.J. Financial literacy and gender difference in loan performance. J. Empir. Financ. 2018, 48, 307–320. [Google Scholar] [CrossRef]

- Meyll, T.; Pauls, T. The gender gap in over-indebtedness. Financ. Res. Lett. 2019, 31, 398–404. [Google Scholar] [CrossRef]

- Cwynar, A. Do women behave financially worse than men? Evidence from married and cohabiting couples. Cent. Eur. Bus. Rev. 2021, 10, 81–98. [Google Scholar] [CrossRef]

- Cupák, A.; Fessler, P.; Schneebaum, A.; Silgoner, M. Decomposing gender gaps in financial literacy: New international evidence. Econ. Lett. 2018, 168, 102–106. [Google Scholar] [CrossRef]

- Škreblin Kirbiš, I.; Vehovec, M.; Galić, Z. Relationship between financial satisfaction and financial literacy: Exploring gender differences. Društvena Istraživanja Časopis Za Opća Društvena Pitanja 2017, 26, 165–185. [Google Scholar] [CrossRef]

- Chhatwani, M.; Mishra, S.K. Financial fragility and financial optimism linkage during COVID-19: Does financial literacy matter? J. Behav. Exp. Econ. 2021, 94, 101751. [Google Scholar] [CrossRef]

- Furrebøe, E.F.; Nyhus, E.K. Financial self-efficacy, financial literacy, and gender: A review. J. Consum. Aff. 2022, 56, 743–765. [Google Scholar] [CrossRef]

- Adetunji, O.M.; David-West, O. The relative impact of income and financial literacy on financial inclusion in Nigeria. J. Int. Dev. 2019, 31, 312–335. [Google Scholar] [CrossRef]

- Morgan, P.J.; Long, T.Q. Financial literacy, financial inclusion, and savings behavior in Laos. J. Asian Econ. 2020, 68, 101197. [Google Scholar] [CrossRef]

- Ferrada, L.M.; Montaña, V. Inclusion and financial literacy: The case of higher education student workers in Los Lagos, Chile. Estud. Gerenc. 2022, 38, 211–221. [Google Scholar] [CrossRef]

- Rastogi, S.; Ragabiruntha, E. Financial inclusion and socioeconomic development: Gaps and solution. Int. J. Soc. Econ. 2018, 45, 1122–1140. [Google Scholar] [CrossRef]

- Mindra, R.; Moya, M. Financial self-efficacy: A mediator in advancing financial inclusion. Equal. Divers. Incl. Int. J. 2017, 36, 128–149. [Google Scholar] [CrossRef]

- Shen, Y.; Hueng, C.J.; Hu, W. Using digital technology to improve financial inclusion in China. Appl. Econ. Lett. 2020, 27, 30–34. [Google Scholar] [CrossRef]

- Hasan, M.; Le, T.; Hoque, A. How does financial literacy impact on inclusive finance? Financ. Innov. 2021, 7, 1–23. [Google Scholar] [CrossRef]

- Tinta, A.A.; Ouédraogo, I.M.; Al-Hassan, R.M. The micro determinants of financial inclusion and financial resilience in Africa. Afr. Dev. Rev. 2022, 34, 293–306. [Google Scholar] [CrossRef]

- Lyons, A.C.; Kass-Hanna, J. Financial inclusion, financial literacy and economically vulnerable populations in the Middle East and North Africa. Emerg. Mark. Financ. Trade 2021, 57, 2699–2738. [Google Scholar] [CrossRef]

- Koomson, I.; Villano, R.A.; Hadley, D. Intensifying financial inclusion through the provision of financial literacy training: A gendered perspective. Appl. Econ. 2020, 52, 375–387. [Google Scholar] [CrossRef]

- Geraldes, H.S.A.; Gama, A.P.M.; Augusto, M. Reaching Financial Inclusion: Necessary and Sufficient Conditions. Soc. Indic. Res. 2022, 162, 599–617. [Google Scholar] [CrossRef]

- Singh, A. Exploring demand-side barriers to credit uptake and financial inclusion. Int. J. Soc. Econ. 2021, 48, 898–913. [Google Scholar] [CrossRef]

- Bongomin, G.O.C.; Munene, J.C.; Ntayi, J.M.; Malinga, C.A. Nexus between financial literacy and financial inclusion: Examining the moderating role of cognition from a developing country perspective. Int. J. Bank Mark. 2018, 36, 1190–1212. [Google Scholar] [CrossRef]

- Liu, S.; Gao, L.; Latif, K.; Dar, A.A.; Zia-UR-Rehman, M.; Baig, S.A. The Behavioral Role of Digital Economy Adaptation in Sustainable Financial Literacy and Financial Inclusion. Front. Psychol. 2021, 12, 742118. [Google Scholar] [CrossRef]

- Ofosu-Mensah, A.J.; Attah-Botchwey, E.; Osei-Assibey, E.; Barnor, C. Financial inclusion and human development in frontier countries. Int. J. Financ. Econ. 2021, 26, 42–59. [Google Scholar] [CrossRef]

- Kodongo, O. Financial regulations, financial literacy, and financial inclusion: Insights from Kenya. Emerg. Mark. Financ. Trade 2018, 54, 2851–2873. [Google Scholar] [CrossRef]

- Agrawal, G.; Jain, P. Digital financial inclusion in India: A review. Behav. Financ. Decis. -Mak. Model. 2019, 195–203. [Google Scholar] [CrossRef]

- Jonker, N.; Kosse, A. The interplay of financial education, financial inclusion and financial stability and the role of Big Tech. Contemp. Econ. Policy 2022, 40, 612–635. [Google Scholar] [CrossRef]

- Jungo, J.; Madaleno, M.; Botelho, A. Financial literacy and financial inclusion effects on stability and competitiveness indicators in the banking sector: Cross country evidence for Africa and the world. Glob. Econ. J. 2021, 21, 2150009. [Google Scholar] [CrossRef]

- Akpene, A.A.; Amidu, M.; Coffie, W.; Abor, J.Y. Financial literacy, financial inclusion and participation of individual on the Ghana stock market. Cogent Econ. Financ. 2022, 10, 2023955. [Google Scholar] [CrossRef]

- Didenko, I.V.; Vasylieva, T.A.; Osadcha, O.; Shymanska, K. The influence of the financial inclusion of the population on the level of illegally income in countries with different levels of economic development. Financ. Credit Act. Probl. Theory Pract. 2021, 6, 268–276. [Google Scholar]

- Sarpong-Kumankoma, E. Financial literacy and retirement planning in Ghana. Rev. Behav. Finance. 2023, 15, 103–118. [Google Scholar] [CrossRef]

- Niu, G.; Zhou, Y. Financial literacy and retirement planning: Evidence from China. Appl. Econ. Lett. 2018, 25, 619–623. [Google Scholar] [CrossRef]

- Niu, G.; Zhou, Y.; Gan, H. Financial literacy and retirement preparation in China. Pac. -Basin Financ. J. 2020, 59, 101262. [Google Scholar] [CrossRef]

- Kalmi, P.; Ruuskanen, O.P. Financial literacy and retirement planning in Finland. J. Pension Econ. Financ. 2018, 17, 335–362. [Google Scholar] [CrossRef]

- Tan, S.; Singaravelloo, K. Financial literacy and retirement planning among government officers in Malaysia. Int. J. Public Adm. 2020, 43, 486–498. [Google Scholar] [CrossRef]

- Yeh, T.M. An empirical study on how financial literacy contributes to preparation for retirement. J. Pension Econ. Financ. 2022, 21, 237–259. [Google Scholar] [CrossRef]

- Nguyen, T.A.N.; Polách, J.; Vozňáková, I. The role of financial literacy in retirement investment choice. Equilib. Q. J. Econ. Econ. Policy 2019, 14, 569–589. [Google Scholar] [CrossRef]

- Sun, R.; Zhang, H.; Turvey, C.G.; Xiong, X. Impact of Financial Literacy on Retirement Financial Portfolio: Evidence from China. Asian Econ. J. 2021, 35, 390–412. [Google Scholar] [CrossRef]

- Clark, R.; Lusardi, A.; Mitchell, O.S. Financial knowledge and 401 (k) investment performance: A case study. J. Pension Econ. Financ. 2017, 16, 324–347. [Google Scholar] [CrossRef]

- Kristjanpoller, W.D.; Olson, J.E. The effect of financial knowledge and demographic variables on passive and active investment in Chile’s pension plan. J. Pension Econ. Financ. 2015, 14, 293–314. [Google Scholar] [CrossRef]

- Chua, S.M.; Chin, P.N. What drives working adults to be better prepared for their retirements? Manag. Financ. 2022, 48, 1317–1333. [Google Scholar] [CrossRef]

- Fernández-López, S.; Otero, L.; Vivel, M.; Rodeiro, D. What Are the Driving Forces of Individuals’ Retirement Savings? Financ. A Uver Czech J. Econ. Financ. 2010, 60, 226–251. [Google Scholar]

- Ricci, O.; Caratelli, M. Financial literacy, trust and retirement planning. J. Pension Econ. Financ. 2017, 16, 43–64. [Google Scholar] [CrossRef]

- Koh, B.S.; Mitchell, O.S.; Fong, J.H. Trust and retirement preparedness: Evidence from Singapore. J. Econ. Ageing 2021, 18, 100283. [Google Scholar] [CrossRef]

- Fang, J.; Hao, W.; Reyers, M. Financial advice, financial literacy and social interaction: What matters to retirement saving decisions? Appl. Econ. 2022, 54, 1–24. [Google Scholar] [CrossRef]

- Angrisani, M.; Casanova, M. What you think you know can hurt you: Under/over confidence in financial knowledge and preparedness for retirement. J. Pension Econ. Financ. 2021, 20, 516–531. [Google Scholar] [CrossRef]

- Clark, R.; Lusardi, A.; Mitchell, O.S. Employee financial literacy and retirement plan behavior: A case study. Econ. Inq. 2017, 55, 248–259. [Google Scholar] [CrossRef]

- Holland, J.H.; Goodman, D.; Stich, B. Defined contribution plans emerging in the public sector: The manifestation of defined contributions and the effects of workplace financial literacy education. Rev. Public Pers. Adm. 2008, 28, 367–384. [Google Scholar] [CrossRef]

- Mahdzan, N.S.; Mohd-Any, A.A.; Chan, M.K. The influence of financial literacy, risk aversion and expectations on retirement planning and portfolio allocation in Malaysia. Gadjah Mada Int. J. Bus. 2017, 19, 267–288. [Google Scholar] [CrossRef]

- Nguyen, L.T.M.; Nguyen, P.T.; Tran, Q.N.N.; Trinh, T.T.G. Why does subjective financial literacy hinder retirement saving? The mediating roles of risk tolerance and risk perception. Rev. Behav. Financ. 2022, 14, 627–645. [Google Scholar] [CrossRef]

- Park, H.; Martin, W. Effects of risk tolerance, financial literacy, and financial status on retirement planning. J. Financ. Serv. Mark. 2022, 27, 167–176. [Google Scholar] [CrossRef]

- OECD (2022), OECD/INFE Toolkit for Measuring Financial Literacy and Financial Inclusion in 2022. Available online: https://www.oecd.org/finance/financial-education/toolkit-for-measuring-financial-literacy-and-financial-inclusion.htm (accessed on 10 August 2022).

- Prete, A.L. Digital and financial literacy as determinants of digital payments and personal finance. Econ. Lett. 2022, 213, 110378. [Google Scholar] [CrossRef]

- Andreou, P.C.; Anyfantaki, S. Financial literacy and its influence on internet banking behavior. Eur. Manag. J. 2021, 39, 658–674. [Google Scholar] [CrossRef]

- Meoli, M.; Rossi, A.; Vismara, S. Financial literacy and security-based crowdfunding. Corp. Gov. Int. Rev. 2022, 30, 27–54. [Google Scholar] [CrossRef]

- Mahdzan, N.S.; Sabri, M.F.; Husniyah, A.R.; Magli, A.S.; Chowdhury, N.T. Digital financial services usage and subjective financial well-being: Evidence from low-income households in Malaysia. Int. J. Bank Mark. 2022. ahead of print. [Google Scholar] [CrossRef]

- Frimpong, S.E.; Agyapong, G.; Agyapong, D. Financial literacy, access to digital finance and performance of SMEs: Evidence From Central region of Ghana. Cogent Econ. Financ. 2022, 10, 2121356. [Google Scholar] [CrossRef]

- Thathsarani, U.S.; Jianguo, W. Do Digital Finance and the Technology Acceptance Model Strengthen Financial Inclusion and SME Performance? Information 2022, 13, 390. [Google Scholar] [CrossRef]

- Luo, Y.; Peng, Y.; Zeng, L. Digital financial capability and entrepreneurial performance. Int. Rev. Econ. Financ. 2021, 76, 55–74. [Google Scholar] [CrossRef]

- Luo, Y.; Zeng, L. Digital financial capabilities and household entrepreneurship. Econ. Political Stud. 2020, 8, 165–202. [Google Scholar] [CrossRef]

- Lin, A.; Peng, Y.; Wu, X. Digital finance and investment of micro and small enterprises: Evidence from China. China Econ. Rev. 2022, 75, 101846. [Google Scholar] [CrossRef]

- Guo, C.; Wang, X.; Yuan, G. Digital finance and the efficiency of household investment portfolios. Emerg. Mark. Financ. Trade 2022, 58, 2895–2909. [Google Scholar] [CrossRef]

- Lu, X.; Guo, J.; Zhou, H. Digital financial inclusion development, investment diversification, and household extreme portfolio risk. Account. Financ. 2021, 61, 6225–6261. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J.J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Hu, X.; Wang, Z.; Liu, J. The impact of digital finance on household insurance purchases: Evidence from micro data in China. Geneva Pap. Risk Insur. -Issues Pract. 2022, 47, 538–568. [Google Scholar] [CrossRef]

- Barik, R.; Sharma, P. Analyzing the progress and prospects of financial inclusion in India. J. Public Aff. 2019, 19, e1948. [Google Scholar] [CrossRef]

- Senou, M.M.; Ouattara, W.; Acclassato Houensou, D. Is there a bottleneck for mobile money adoption in WAEMU? Transnatl. Corp. Rev. 2019, 11, 143–156. [Google Scholar] [CrossRef]

- Hasan, R.; Ashfaq, M.; Parveen, T.; Gunardi, A. Financial inclusion–does digital financial literacy matter for women entrepreneurs? Int. J. Soc. Econ. 2022. ahead of print. [Google Scholar] [CrossRef]

- Li, J.; Meyer-Cirkel, A. Promoting financial literacy through a digital platform: A pilot study in Luxembourg. Int. J. Financ. Econ. 2021, 26, 73–87. [Google Scholar] [CrossRef]

- Banciu, D.; Arulanandam, B.V.; Munhenga, T.; Ivascu, L. Digital financial literacy and microfinancing among underprivileged communities in Cambodia. Rom. J. Inform. Technol. Autom. Control 2022, 32, 77–92. [Google Scholar]

- Raidev, A.A.; Modhvadiya, T.; Sudra, P. An Analysis of Digital Financial Literacy among College Students. Pac. Bus. Rev. Int. 2020, 13, 32–40. [Google Scholar]

- Ravikumar, T.; Suresha, B.; Prakash, N.; Vazirani, K.; Krishna, T.A. Digital financial literacy among adults in India: Measurement and validation. Cogent Econ. Financ. 2022, 10, 2132631. [Google Scholar] [CrossRef]

- Kass-Hanna, J.; Lyons, A.C.; Liu, F. Building financial resilience through financial and digital literacy in South Asia and Sub-Saharan Africa. Emerg. Mark. Rev. 2022, 51, 100846. [Google Scholar] [CrossRef]

- Setiawan, M.; Effendi, N.; Santoso, T.; Dewi, V.I.; Sapulette, M.S. Digital financial literacy, current behavior of saving and spending and its future foresight. Econ. Innov. New Technol. 2022, 31, 320–338. [Google Scholar] [CrossRef]

- Tian, G. Influence of Digital Finance on Household Leverage Ratio from the Perspective of Consumption Effect and Income Effect. Sustainability 2022, 14, 16271. [Google Scholar] [CrossRef]

- Su, L.; Peng, Y.; Kong, R.; Chen, Q. Impact of e-commerce adoption on farmers’ participation in the digital financial market: Evidence from rural China. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1434–1457. [Google Scholar] [CrossRef]

- Divaeva, E.; Kukharenko, O.; Gizyatova, A. Considering susceptibility of individuals to digital finance as a factor of increasing its prosperity. Int. Rev. 2021, 1–2, 137–145. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Top 10 Journals | Top 10 Authors | |||||

|---|---|---|---|---|---|---|

| Journal of Consumer Affairs | 34 | 3.18% | Lusardi A | 26 | 2.43% | |

| Journal of Pension Economics Finance | 34 | 3.18% | Mitchell OS | 18 | 1.68% | |

| International Journal of Consumer Studies | 25 | 2.33% | Kadoya Y | 15 | 1.40% | |

| International Journal of Bank Marketing | 22 | 2.05% | Khan MSR | 15 | 1.40% | |

| Sustainability | 22 | 2.05% | Bennett DA | 10 | 0.93% | |

| Managerial Finance | 20 | 1.87% | Boyle PA | 10 | 0.93% | |

| Frontiers in Psychology | 16 | 1.49% | Xiao JJ | 10 | 0.93% | |

| Journal of Family and Economic Issues | 14 | 1.31% | Bongomin GOC | 8 | 0.75% | |

| International Journal of Social economics | 13 | 1.21% | Cwynar A | 8 | 0.75% | |

| Journal of Behavioral and Experimental Finance | 13 | 1.21% | De Witte K | 7 | 0.65% | |

| Top 10 Affiliates | Top 10 Countries | |||||

| University of Pennsylvania | 24 | 2.24% | USA | 294 | 27.45% | |

| George Washington University | 21 | 1.96% | China | 96 | 8.96% | |

| Hiroshima University | 14 | 1.31% | India | 80 | 7.47% | |

| University of London | 14 | 1.31% | Australia | 62 | 5.79% | |

| Monash University | 11 | 1.03% | England | 48 | 4.48% | |

| University of Massachusetts System | 11 | 1.03% | Italy | 48 | 4.48% | |

| University of Southern California | 11 | 1.03% | Malaysia | 47 | 4.39% | |

| University System of Ohio | 11 | 1.03% | Germany | 45 | 4.20% | |

| European Central Bank | 10 | 0.93% | Indonesia | 38 | 3.55% | |

| Ku Leuven | 10 | 0.93% | Japan | 34 | 3.18% | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zaimovic, A.; Torlakovic, A.; Arnaut-Berilo, A.; Zaimovic, T.; Dedovic, L.; Nuhic Meskovic, M. Mapping Financial Literacy: A Systematic Literature Review of Determinants and Recent Trends. Sustainability 2023, 15, 9358. https://doi.org/10.3390/su15129358

Zaimovic A, Torlakovic A, Arnaut-Berilo A, Zaimovic T, Dedovic L, Nuhic Meskovic M. Mapping Financial Literacy: A Systematic Literature Review of Determinants and Recent Trends. Sustainability. 2023; 15(12):9358. https://doi.org/10.3390/su15129358

Chicago/Turabian StyleZaimovic, Azra, Anes Torlakovic, Almira Arnaut-Berilo, Tarik Zaimovic, Lejla Dedovic, and Minela Nuhic Meskovic. 2023. "Mapping Financial Literacy: A Systematic Literature Review of Determinants and Recent Trends" Sustainability 15, no. 12: 9358. https://doi.org/10.3390/su15129358

APA StyleZaimovic, A., Torlakovic, A., Arnaut-Berilo, A., Zaimovic, T., Dedovic, L., & Nuhic Meskovic, M. (2023). Mapping Financial Literacy: A Systematic Literature Review of Determinants and Recent Trends. Sustainability, 15(12), 9358. https://doi.org/10.3390/su15129358