1. Introduction

The fourth industrial revolution led to a widespread use of digital technologies, the Internet, social networks, etc. Roblek et al. consider that the fourth industrial revolution is characterized as an era of digital transformation, which holds great potential for sustainability [

1]. As a result, a greater diversity of new business models is emerging in the financial sector. A new emerging set of companies, known as FinTech companies, is taking advantage of this digitalization, such as digital platforms and advanced technologies, to provide financial products and services [

2].

The rapid development of new technologies has had a significant effect on the financial sector. Digitalization is a management tool and digital transformation (DT) is the process of integrating digital technologies into the value chain of activities, in order to deliver added value to both customers and broader stakeholders, which leads to improving organizational performance. Moreover, digitalization is a helpful tool in contributing to sustainable development, thus emphasizing its strategic orientation for the benefits of stakeholders. Adaptation of new technologies in the financial sector leads to the development of new value in a form of offering, value proposition and business model innovation, transformation of value chains, ecosystems, development of new product delivery channels, changing the relationship between companies in the financial sector, etc., which increases the operational efficiency and effectiveness of financial institutions and enables a sustainable development path. Digital transformation enables social benefits by improving financial inclusion, which provides more personalized financial products and usable digital access channels.

Authors have observed that the amount of research on sustainable development of different economy sectors based on digital transformation as one of key drivers has increased. Digital transformation of the financial sector is important for sustainable development; however, academic studies on the topic are very limited.

The aim of the research is to determine the trends in digital transformation of the financial sector and to explore how digital transformation due to the application of innovative technologies and solutions, especially digital payments, is leading to the financial sector sustainable development through financial inclusion and operational efficiency. Researchers state that sustainable finance has emerged as an important concept at the intersection of finance and the sustainable development goals (SDG) and propose that sustainable finance should encompass all activities and factors that would make finance sustainable and contribute to sustainability [

3].

This research contributes to the overall scientific discussion on digital transformation of the financial sector, digital technologies, and financial institutions’ sustainable development. The research results indicate two main directions: (1) Digital transformation trends and digital technology usage for sustainable development of financial institutions and (2) a digital payment intensity increase and its relationship with financial institutions’ operational efficiency and financial inclusion, as well as the differences between the digital transformation aims and progress of financial institutions in Baltic states compared to other European countries. At present, there is no common understanding among researchers of the digital transformation (DT) concept in the literature and its role in sustainable development since it is a rather complex issue. Both academic researchers and researchers from global consulting companies (MIT, Deloitte, etc.) emphasize that digital technology is only one element of the puzzle in organizations’ efforts to increase competitiveness in the digital world [

4]. Accordingly, the process of selecting, developing or adapting technologies is complex, including a wide range of organizational processes, and permeates the structure of the whole organization. Digital transformation is a term that, in an academic and practical discourse, refers to the complex nature of digital technology adaptation, given that this process stems from the strategic choice of building, adapting, and transforming internal processes, customer relationships and customer experiences, value propositions and business models using a defined infrastructure, and resources to enable an organization to navigate effectively in digital ecosystems. Liu et al. describe the digital transformation as the integration of digital technologies into business processes [

5]. Shim and Shin recognize that the rapid development of information and communications technology (ICT) is transforming the whole industry landscape, heralding a new era of convergence services [

6]. From the authors’ point of view, DT is aimed at improving the overall performance of the organization, ensuring its sustainable development. In addition, it is a process, which requires a holistic, systemic, and systematic approach to create a favorable environment for its successful delivery.

Several studies reveal that it is possible to suggest a research framework that considers digital transformation as a driver and a predecessor of sustainability. To survive in the digital revolution, companies need to enhance their digital capabilities and balance their economic, environmental, and social impacts [

7]. However, while sustainability is undisputedly one of the most growing phenomena, it is still an insufficiently discussed field of application for digital technology [

8,

9]. There are studies on how digital transformation in the financial sector affects sustainability while the financial inclusion is left outside the scope [

10]. Flejterski defines that the key objectives in the financial sector and in the financial system will be sustainability, stability, and safety [

11]. Schilirò emphasizes that sustainability requires efficiency [

12].

Digitalization and financial sector transformation issues are topics that have already gained particular interest among researchers from Baltic countries. Therefore, there is extensive literature available on this topic, which were studied by Rupeiga-Apoga, Lace, Mavlutova, Andriuskevicius, Volkova, Arefjevs, Spilbergs, Natrins, etc. [

13,

14,

15,

16,

17,

18,

19]. Other authors including Tambovceva, Uvarova, Romānova, Rupeika-Apoga, Atstaja, Brizga, and Titko have researched various aspects of sustainable development of Baltic countries [

20,

21,

22,

23].

The Baltic (defined as Estonia, Latvia, and Lithuania) marketplace is considered to be dominated by Nordic financial groups [

24]. In recent years, there was an exit by Nordea and DNB banking groups, which sold their holdings to the Blackstone-led consortium [

25]. The transaction has strengthened the United States domiciled ownership of Baltic financial groups to a certain extent. The overall trend of foreign ownership of the financial groups in the Baltics has not changed.

Banks are traditionally the biggest market players in the EU and in the Baltic countries, which form a backbone of the financial sector. According to the European Banking Federation, credit institutions’ assets vary from EUR 24 billion in Latvia to EUR 40 billion in Lithuania. Loan amounts are nearly balanced with deposits in Estonia (both stand at nearly EUR 26 billion) and Latvia (both figures are at EUR ~18 billion) while Lithuania stands out as a clear net lender with loans totaling to EUR 29 billion and deposits exceeding EUR 33 billion (European Banking Federation 2021). The statistics are available in

Table 1, as presented below.

The COVID-19 pandemic has affected the transformation of business and the financial sector toward sustainability, requiring not only environmental, but also financial and social sustainability priorities. Financial and social sustainability issues have increasingly become more important along with Russia’s invasion of Ukraine.

Financial inclusion has been identified as an enabler for nine of the seventeen UN sustainable development goals (SDG) aimed at building resilient infrastructure, promoting inclusive and sustainable industrialization, and fostering innovation, particularly to increase access to financial services and markets and to support domestic technology development and industrial diversification, as well as universal access to information and communications technologies [

26]. The aim of the Recovery Plan for Europe (2021–2027) is to reduce the economic and social impact of the coronavirus pandemic and make the European economy and society more sustainable, resilient, and better prepared for the tasks and opportunities of not only green, but also digital transformation [

27]. The importance of the digital transformation, which is addressed with The Digital Education Action Plan (2021–2027), is aimed at supporting the sustainable and effective adaptation of EU Member States’ education and training systems for the digital age [

28].

The current study consists of the literature analysis and the quantitative research. The content analysis was performed by investigating academic publications of digital transformation, and the impact of digital technologies on the sustainable development of the financial sector. The quantitative research was based on the statistical data analysis of the financial sector and its development trends. Structured interviews were applied for an investigation of the financial sector’s current situation concerning technological changes and sustainability empowerment in the Baltic countries. The results of this study assist in understanding the financial sector’s contribution to sustainable development and in further developing new approaches for decision making toward meeting sustainability agenda goals in general, as well as sustainability of the financial sector in particular. Moreover, the findings are useful to academics for an investigation of recent trends on digital transformation and usage of digital technologies to ensure the sustainable development of financial institutions. Research limitations are the legal aspects of the digital transformation of financial institutions, as well as the environmental dimension of the financial sector sustainable development, all of which are outside the scope of the current research.

3. Research Methodology and Results

To achieve the purpose of the study, the authors analyzed statistics on the digital transformation of the financial sector and chose digital payments as the most popular digital technology to identify the relationship between the intensity of financial inclusion and its dynamics across the Globe and in the European Union. For the empirical analysis, the authors collected data from two main sources: Global Financial Inclusion Database (WB 2022) for financial inclusion variables and European Central Bank Consolidated Banking Database (ECB 2022) for the bank expense variables. The data were collected from 26 European Union countries for the years 2014, 2017, and 2021. Luxemburg was excluded from the analysis since the data for 2021 were not available at the time of the study.

In the empirical study, the authors used two control variables:

made a digital payment, % age 15+ (MDP);

received digital payments, % age 15+ (RDP);

and support variables:

account, % age 15+ (ACC);

made a deposit, % with a financial institution account, age 15+ (DEP);

saved any money, % age 15+ (SAV);

saved at a financial institution, % age 15+ (SAF);

saved for old age, % age 15+ (SAO);

borrowed any money, % age 15+ (BOR);

total operating expenses, % of total assets (TOE);

staff expenses, % of total assets (STE).

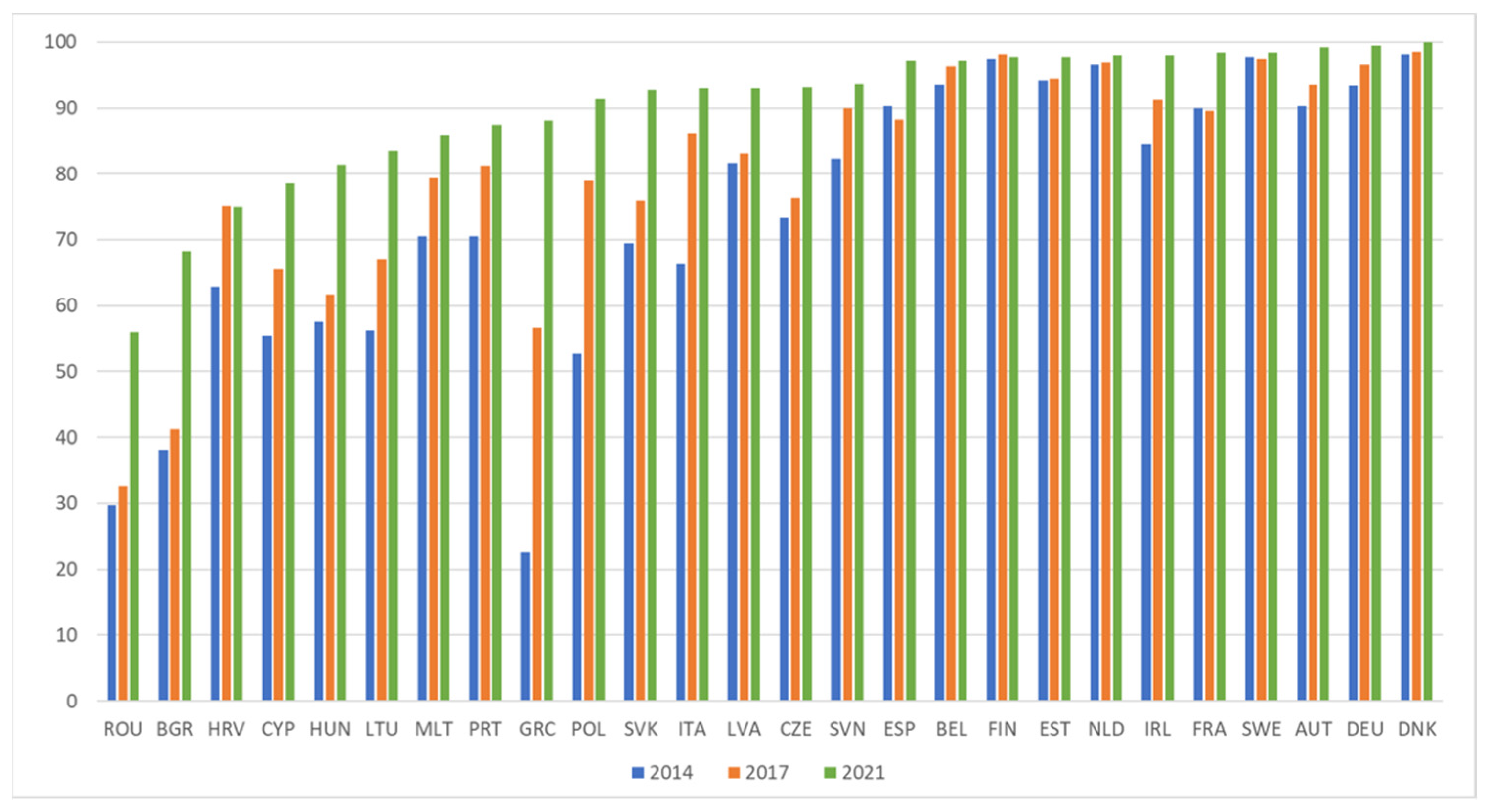

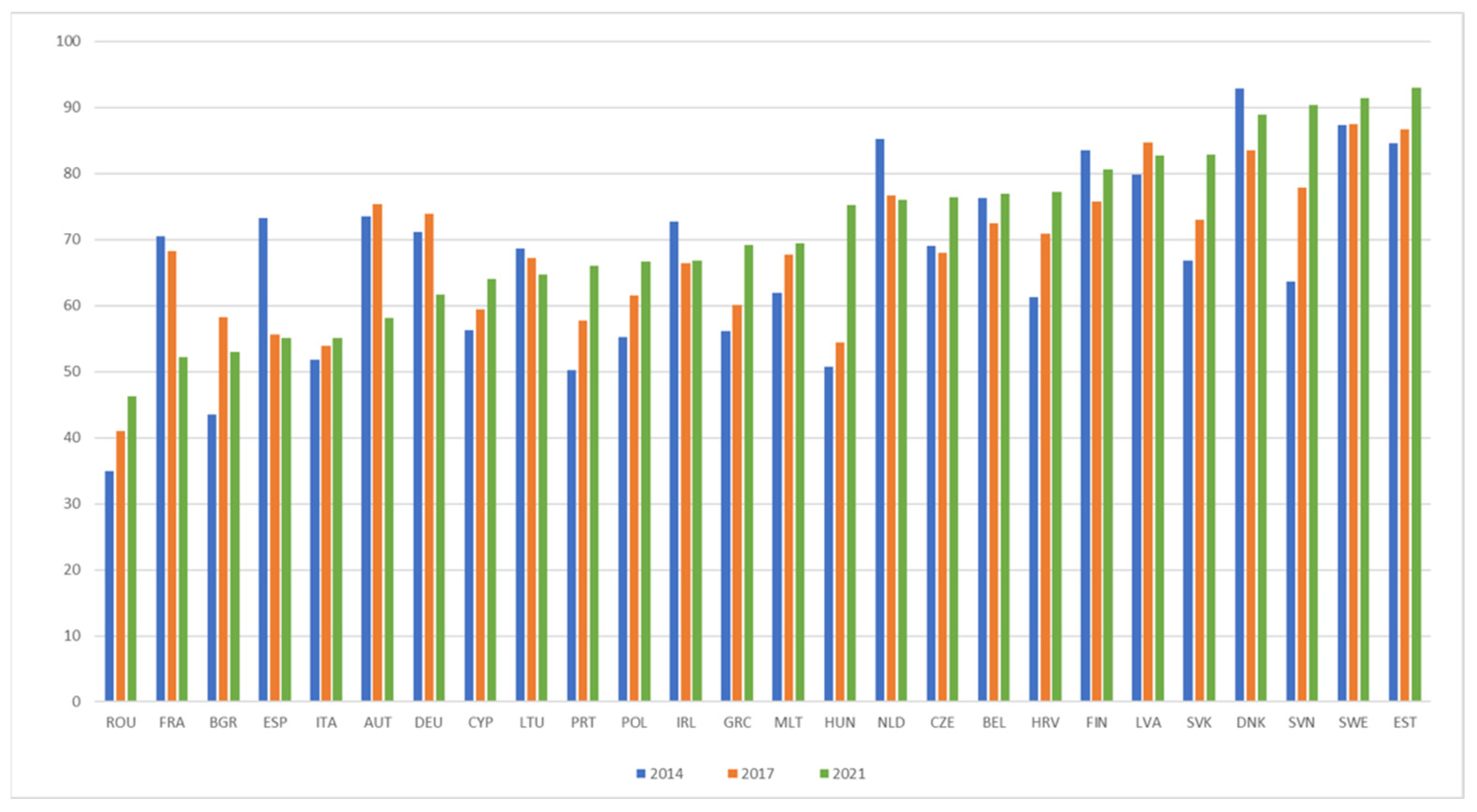

As shown in

Figure 4, in 2021, the highest intensity of digital payments in the EU countries was in Denmark—99.9% of the population aged 15 and over made digital payments—followed by Germany (99.5%), Austria (99.2%), Sweden (98.4%), and France (98.4%). The indicators of Estonia (97.7%) and Latvia (93.0%) of the Baltic countries are also above average, while Lithuania (83.4%) is slightly lower.

The fastest growth of digital payments made in the last 8 years was in Greece (290.3%), Romania (88.8%), and Bulgaria (79.5%), which is largely explained by the low intensity of digital payments in 2014. Among the Baltic states, the fastest growth in 2021 compared to 2014 was in Lithuania (48.2%), compared with Latvia (14.0%) and Estonia (3.7%).

As shown in

Figure 5, in 2021, Estonia (93.0%), followed by Sweden (91.4%), Slovenia (90.4%), Denmark (88.9%), Slovakia (82.9%), and Latvia (82.8%) were the leaders in the EU in terms of the intensity of digital payments received. The intensity of digital payments received in Lithuania was the lowest in the Baltics (64.7%). The fastest growth in digital payments received over the last 8 years was in Hungary (48.1%), Slovenia (42.0%), and Romania (32.1%), which is largely explained by the low intensity of received digital payments in 2014. Among the Baltic states, the fastest growth in 2021 compared to 2014 was in Estonia (9.8%) and Latvia (3.6%), while the decrease was seen in Lithuania (−5.7%).

To assess the dynamics of the intensity of digital payments, the authors use the chi-squared test and the statistic is calculated as follows:

where

is the observed (2021) intensity of digital payments in

i-th country and

is the expected (2014 or 2017 accordingly) intensity of digital payments in

i-th country.

The following table summarizes the results of chi-squared test.

As can be seen from the data in

Table 3 on the digital payments made, the chi-square statistic is greater than the chi-square critical values (37.7); therefore, the authors can conclude that the increase in digital payments made, comparing the year 2021 with both 2014 and 2017, is statistically significant at a confidence level greater than 95%. A similar conclusion can be drawn about the increase in digital payments received in 2021 compared to 2014. However, compared to 2017, the increase in digital payments received is not statistically significant. Moreover, these conclusions are confirmed by the

p-values summarized in

Table 3. The results of the chi-square test allow for the confirmation of hypothesis H1.

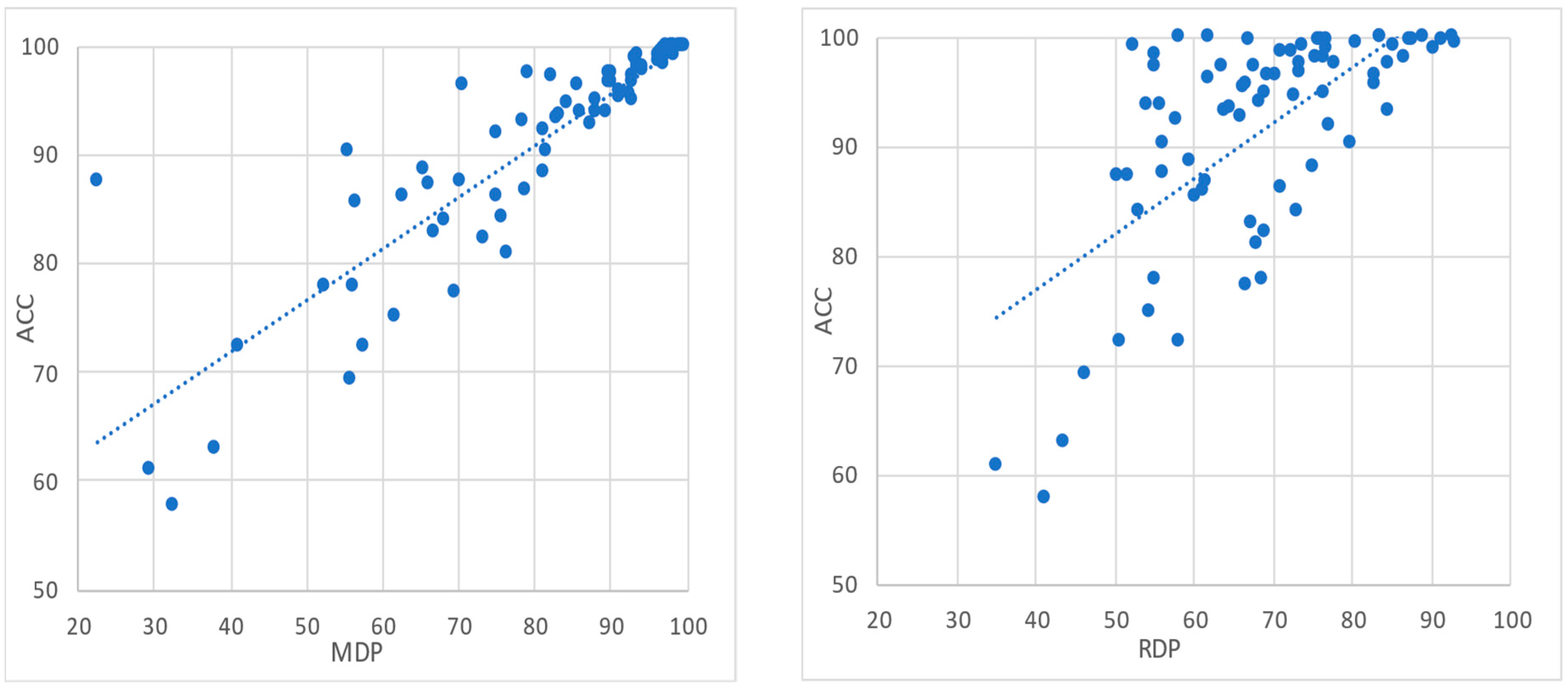

In order to assess the relationship between the intensity of digital payments and the indicators of financial inclusion in the EU countries, the authors performed a Pearson correlation analysis, and the results obtained with the RStudio cor.test () function are summarized in

Table 4.

As can be seen from the data in

Table 4 for digital payments made, all Pearson correlation coefficients values are larger than 0.5, indicating a strong positive relationship with all analyzed financial inclusion indicators for the EU countries. A similar conclusion can be drawn in regard to the digital payments received. However, the relationship between digital payments received and borrowing is rather weak. These conclusions are confirmed by the

p-values and Pearson correlation coefficients of 95% confidence intervals summarized in

Table 4. The Pearson correlation analysis results allow for the confirmation of hypothesis H2.

To evaluate the relationship between the intensity of digital payments and the operational efficiency of financial institutions in the EU countries, the authors provided regression analysis. A regression analysis has been widely used in similar studies, for example, by Allen et al., Demir et al., Son and Kim, that proved its ability to provide the necessary justifications for the validation of the proposed hypothesis [

70,

74,

80]. To test the proposed hypothesis, the following four regression equations were developed:

where

total costs (% of assets) depending on the intensity of digital payments made;

—total costs (% of assets) depending on the intensity of digital payments received;

—intercepts of respective regression model;

—regression coefficients of respective regression model;

—error terms of respective regression model.

Regression model’s calibration and evaluation results obtained with the RStudio are summarized in

Table 5 and

Table 6.

As shown in

Table 6, all estimated regression model’s coefficients are statistically significant at level <1%. The results obtained allow for the conclusion that a positive relationship between digital payments’ intensity and the operational efficiency of financial institutions exists—when the intensity of digital payments increases, both banks’ total costs to assets and staff costs to assets decrease.

Since the tests of correlation coefficients substantiate the statistical significance of the relationship between the intensity of digital payments and financial inclusion identifiers, the authors conclude that with increased opportunities to make and receive digital payments, the proportion of account owners in the 15+ population group increases linearly (see

Figure 6).

In addition, when the intensity of digital payments made increases by 1%, the intensity of accounts increases by 0.48%. Regarding digital payments received, the increase in accounts is slightly higher (0.51%).

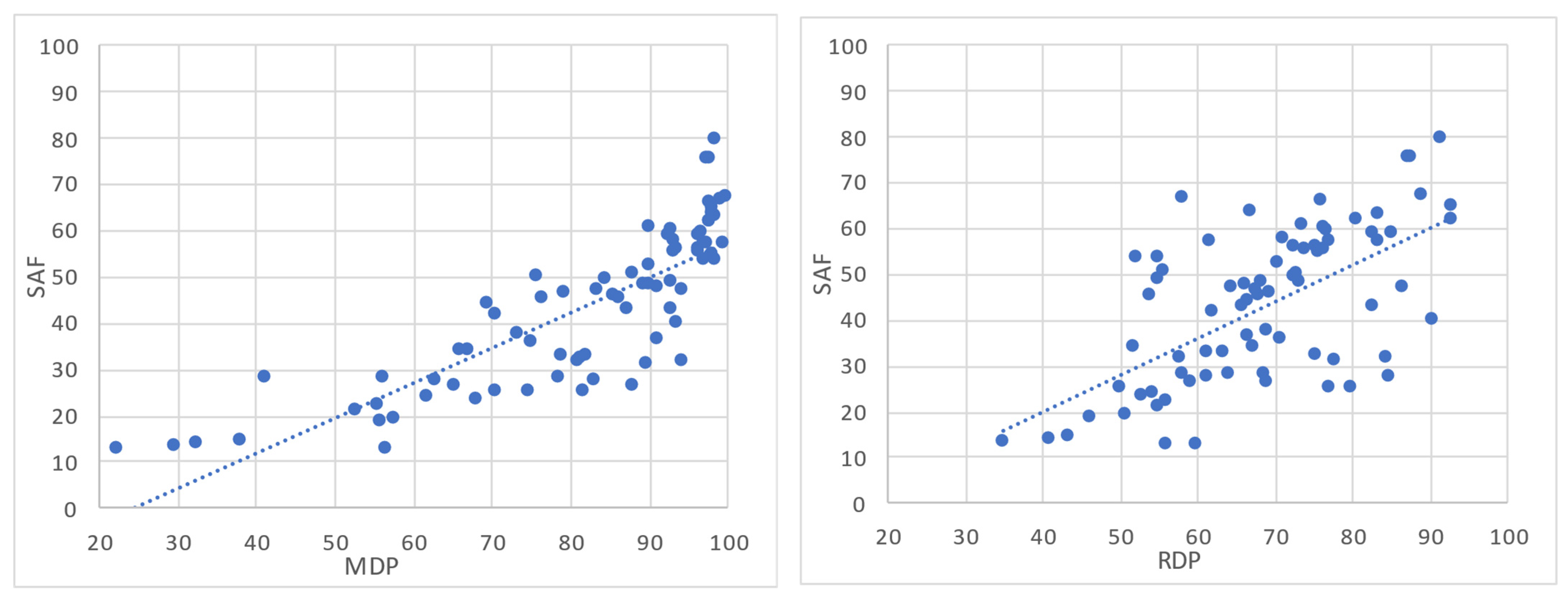

Regarding the relationship between digital payments and the intensity of savings at financial institutions, the results of the analysis allow for the conclusion that with increasing opportunities to make and receive digital payments, the intensity of savings at financial institutions in the 15+ population group increases linearly, as shown in

Figure 7. In addition, as the intensity of digital payments increases by 1%, the intensity of savings increases by 0.75%. With regard to digital payments received, the growth of savings intensity is slightly higher (0.81%), which can be logically explained, since upon receiving a payment there is an additional opportunity to save money.

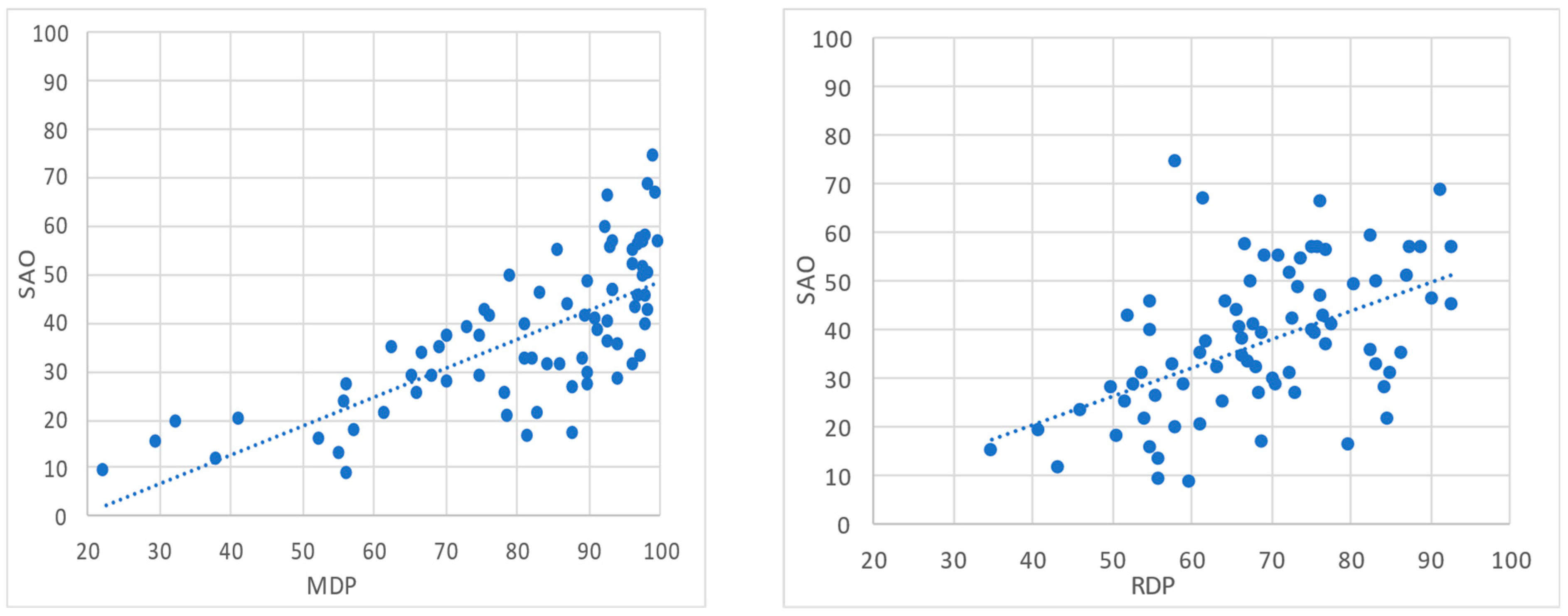

Regarding the relationship between digital payments and the intensity of savings for old age customers, the results of the analysis allow for the conclusion that with increasing opportunities to make and receive digital payments, the intensity of savings for old age in the 15+ population group increases linearly, as shown in

Figure 8. In addition, as the intensity of digital payments increases by 1%, the intensity of savings increases by 0.60%. Regarding received digital payments, the growth of savings intensity is similar (0.59%).

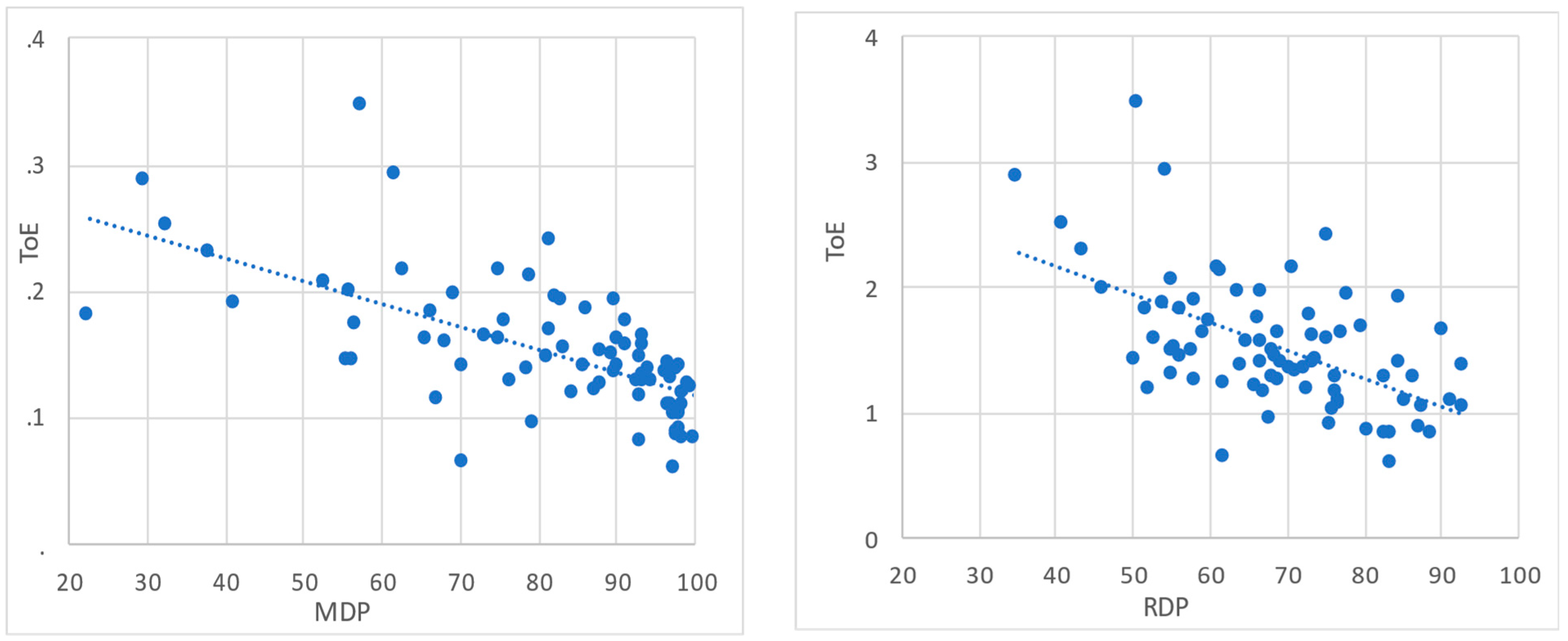

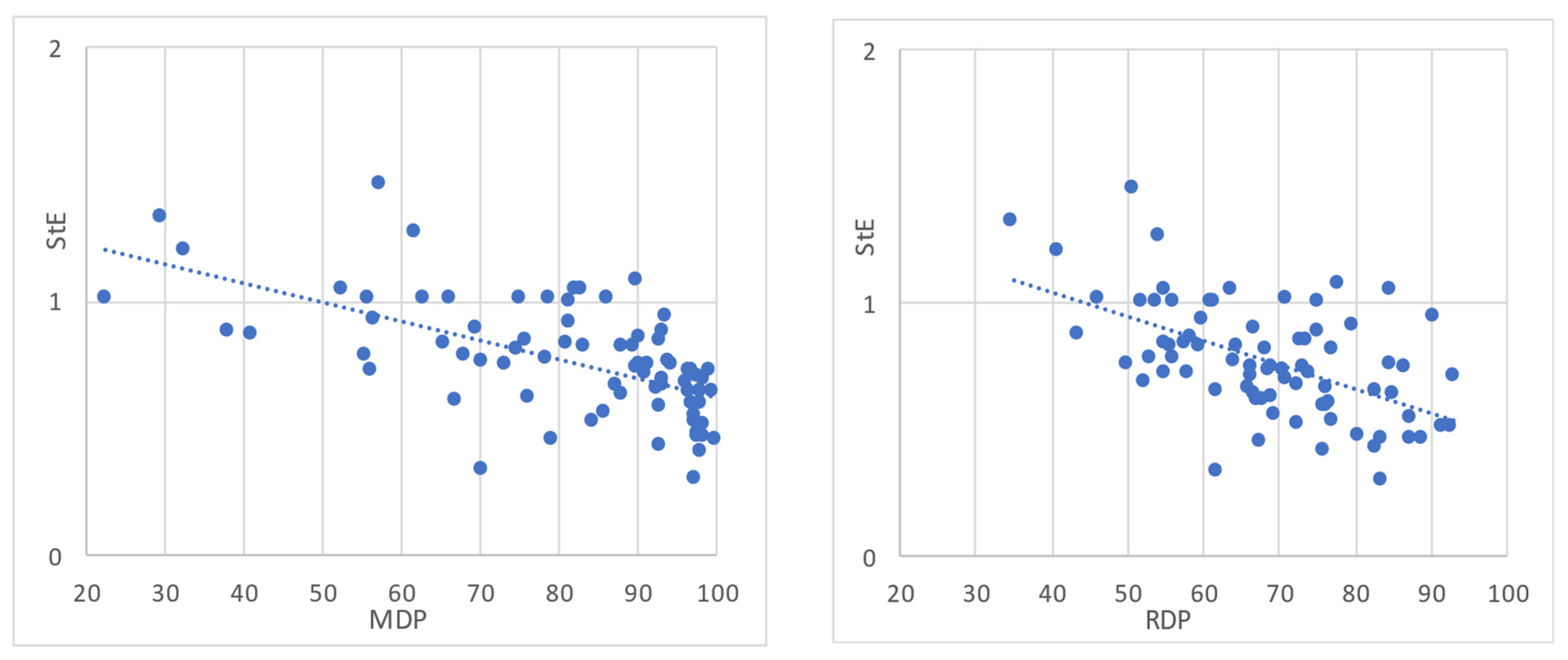

Since the tests of regression models and coefficients substantiate the statistical significance of the relationship between the intensity of digital payments and financial institutions operational efficiency, the authors concluded that with the increased intensity of digital payments, the total and staff costs to bank assets decrease, as shown in

Figure 9 and

Figure 10. In addition, as the intensity of digital payments made increases by 1%, the total costs to assets decrease by 0.018% on average. Regarding received digital payments, the decrease in total costs to assets is slightly higher (0.023%). Among the Baltic states, Latvia showed slightly lower total costs than the EU average—with the digital payments made factor as −0.49% and the digital payments received factor as −0.38%. On the other hand, Estonia’s result is +0.16% and +0.41%, and Lithuania is +0.07% and −0.05%, respectively.

Regarding staff costs to assets, when the intensity of digital payments increases by 1%, the staff costs to assets decrease by 0.0074% on average. For digital payments received, the decrease in staff costs to assets is slightly higher (0.0096%). Among the Baltic states, Latvia showed slightly lower total costs than the EU average—with the digital payments made factor as −0.26% and digital payments received factor as −0.21%. On the other hand, Estonia’s result is +0.06% and +0.017%, and Lithuania is +0.07% and +0.02%, respectively.

All the results of the above analysis allow for the confirmation of hypothesis H3.

To conduct an in-depth study of the digital transformation and sustainable development of financial sector participants in Baltic countries, semi-structured expert interviews were used to validate research findings. In line with the research objectives, special attention has been paid to issues in relation to the cost efficiency of the sustainable development of the financial sector.

In total, nine top level experts participated in the interviews. The overall summary of the expert group is presented in the

Table 7.

The authors believe that the expert composition is representative to a sufficient extent since experts cover key industries and the area related to the financial sector, as well as possess local, regional, and global views on the studied topic. The interviews took place during the time period from September to October 2022.

As an opening question, the progress of digital transformation in a represented financial sector participant was described by experts mainly in the following way:

A specific number of delivered solutions, technology projects, and improvement initiatives implemented per year in accordance with a technology strategy;

Partnerships with service providers with strategic competence in the area;

Implementation of machine learning techniques to shorten the process execution time and advance the quality of decision making.

Furthermore, in relation to sustainable development goals standing at the forefront of financial sector participant’s long-term development and related operational plans, experts mentioned:

Setting strategic objectives for particular sustainability goals;

Sustainability integrated in the application of business practices;

Sustainability dimensions are included in the key strategic areas of the company (e.g., staff, risk management, partnerships).

The experts mentioned the following technological solutions for businesses that were most often considered for achieving sustainability goals:

Artificial intelligence (incl. machine learning and processing big data);

Digital payments, e-wallets, and remote customer onboarding;

Cloud computing;

Blockchain technology;

Process automation.

According to the experts, technology plays a prominent role in balancing the relationship between the company’s sustainability and the sustainable development objectives. Technology can be considered as a foundation for further actions. However, it was also stressed that technology is merely a tool to achieve the goal. Practitioners, who work with technology, are the most important element of ensuring sustainability.

Experts cited digital payments as a key product or priority that tends to become more advanced. Traditionally, digital solutions including digital payments are heavily used for achieving cost efficiency objectives. In particular, experts emphasized that cost efficiency became the main goal to accelerate digitization at a time when the economy, and thus business activities, were slowing down. Nevertheless, the main goal of digitalization is manifested in the improvement in customer experience. Process automation deserves a special place in digitalization initiatives.

In terms of contribution of digital technology to sustainable development, digital technology enables the use of human capital in a smarter way (i.e., less manual work, more intellectual tasks). Moreover, it eliminates a wide range of risks, which can arise from human factors (varying from errors to conflict of interest) as well as save costs by not consuming excessive resources.

Currently, the following technological solutions that are most often in use as mentioned by the experts include data models and analytics, robotics, and basic artificial intelligence tools. Among the solutions that were mentioned in the pipeline are the introduction of various application programming interfaces (APIs), more advanced artificial intelligence tools, as well as various digital platforms.

Finally, with regard to the open-ended questions, the approach toward financial inclusion was described as:

Special focus on underserved and potentially discriminated segments of customers (e.g., easing barriers for receiving financial services using digital technology);

Indirectly by offering a regulatory sandbox and innovation hubs (by financial regulators).

During the interview, the experts were asked to answer specific questions by choosing the most appropriate score ranging from 1 (not important) to 5 (very important). The summary of the questionnaire with expert answers is provided in

Table 8.

As shown in

Table 8, the digital transformation was assessed as a key method by experts for improving product development (4.8), developing financial sector participant customer base and customer relationships (4.8), as well as access to channel management (4.7). It is peculiar that experts do not consider digital transformation as the main method for optimizing internal processes and increasing the operative efficiency of financial institutions (4.3). In connection with the application of innovative digital technologies, expert evaluations show that the most important solutions are related to the development of digital payments (e.g., remote authentication tools (4.6), API platform technologies (4.4), process automation (4.3).

4. Discussion

In discussions, researchers from academia and practitioners from financial institutions and global consulting firms define digital transformation as a complex process of adapting digital technologies, which results from the strategic goal of creating, adapting, and transforming internal processes, customer relationships and customer experiences, value propositions and business models, with the aim of increasing the efficiency of financial institutions [

4,

5]. Liu et al. believe that the digital transformation is characterized by the integration of digital technologies into business processes. Shim and Shin recognize that the rapid development of ICT is transforming the landscape of the financial industry and starting a new era of convergence services [

5,

6]. Kotarba considers the digital transformation to be the modification of business models, which results from the dynamic of technological progress and innovation that triggers changes in consumer and social behaviors. Therefore, it is important to understand the role of digital transformation in bringing about beneficial changes in organizational strategies and behaviors [

84]. All these considerations allow the authors to conclude that digital transformation is a driving force for the sustainable development of financial institutions, which coincides with the opinions of Flejterski, Schilirò, Yu et al. [

10,

11,

12].

The results of both the recent academic and the current empirical research show that digital payments are the most affected area of digital transformation [

43,

47,

49]. The current research reveals that the intensity and progress of digital payments made and received differ significantly between the EU countries; similar results have been shown by other research works (e.g., Mishra, Sarma, Allen, etc. [

47,

69,

70]). Sarma proposes a comprehensive vision of the financial inclusion based on the dimensions of accessibility, availability, and use of the formal financial system by all agents within the economy, and explains the differences in the use of financial services with different income levels [

69]. The results of our research do not provide a sufficient justification for this statement due to the gross national income per capita, which indicates a moderately strong correlation with the intensity of digital payments made in the EU countries in 2021 (coefficient of −0.649), while a correlation with the intensity of digital payments received in the EU countries in 2021 indicates a weak relationship (coefficient of −0.162). Allen et al. found that greater financial inclusion is associated with lower account costs and increases in savings. The authors explain the differences with greater proximity to financial intermediaries, stronger legal rights, and more politically stable environments. However, Sahi et al. explains the differences in cultural backgrounds [

43,

70]. The current study shows that the digital transformation in the financial sector significantly reduces the impact of income level on financial service penetration—the availability of digital payments is closely correlated with both account ownership and any savings intensity. Moreover, similar relationships are substantiated in the studies by Arner et al. 2020, Galvez-Sanchez et al. 2021 [

71,

73].

Digital transformation of the financial sector not only contributes to the increase in the intensity of financial services, but also provides an opportunity to reduce the costs of manual work and reduce operational risk losses. Moreover, the study by Ahamed and Mallick provides comprehensive empirical evidence that greater financial inclusion is positively associated with individual bank stability. Furthermore, the study substantiates that the channels through which financial inclusion impacts bank soundness and increases financial inclusion act as an instrument to reduce the marginal cost of outputs [

81]. Similar conclusions can be derived from the research by Andersen on Norwegian banks’ online and mobile banking, payment apps, and other web-based services. The authors stated that these services led the bank customers to be more self-sufficient and reduced the need for bank personnel and bank offices. Therefore, automation and the digitalization of banks’ operations have played a key role in improving cost efficiency [

83].

However, digital transformation in the financial sector of the Baltic states is insufficient compared to the EU as a whole. Of note, interviews with the expert group of financial sector institutions of the Baltic states revealed that experts do not consider digital transformation as the main method for optimizing internal processes and increasing the operational efficiency of financial institutions.

In general, the authors agree with the findings by Danisman and Tarazi, which suggest that advances in financial inclusion through increased account ownership and digital payments stabilize the banking industry in the EU [

68].

5. Conclusions

The authors conclude that the digital transformation of the financial sector takes place under the influence of the fourth industrial revolution and is characterized by the integration of digital technologies into business processes, providing new innovative opportunities, thus directly affecting the operation of financial sector institutions. The rapid development of technologies changed the landscape of the financial sector. Therefore, development of technologies could be considered to be a driving force for the sustainable development of financial institutions.

There is no standardized solution for the digital transformation of financial institutions to promote sustainable development, as the sustainable development is a continuous process and requires contextualization.

The bibliometric analysis linking sustainable development and the financial sector, despite the growing interest of researchers, showed that the regularities of financial systems and sustainability were studied the least. The authors of the current study have paid attention to the economic aspect of sustainability since it was studied the least. In addition, by critically analyzing the latest research, they have concluded that the sustainability of a financial institution could be also characterized by the financial inclusion and operational efficiency aspects enabled by digital transformation.

The statistical analysis of the digital transformation of the financial sector was performed by the authors. Digital payments were selected as the most popular digital technology, in order to determine the relationship between the intensity of financial inclusion and its dynamics across the Globe and in the European Union. With three tested hypotheses, the authors concluded that in the financial sector of the EU countries significant progress in the intensity of digital payments was observed, and a positive relationship between the intensity of digital payments and financial inclusion was found. In addition, a positive relationship between the intensity of digital payments and the efficiency of financial institutions in the EU countries was proven.

Based on the analysis of semi-structured interviews of the expert group from the financial sector institutions of the Baltic countries to validate research findings, the authors believe that there is an evident basis for the conclusion that digital transformation is a key method for improving product development, developing a financial sector institution customer base, customer relationships, as well as access to channel management. Nevertheless, there is room for improvement in digital transformation solutions for optimizing internal processes and increasing the operational efficiency of financial institutions in the Baltic countries.

The authors conclude that digital transformation is beneficial for the clients of financial institutions and for the financial institutions themselves by ensuring the availability of financial services 24/7 even in conditions of a pandemic and similar restrictions, saving personal time for financial transactions and reducing logistics costs for financial institutions; cost savings by reducing manual operations, the need for offices and logistics; customer satisfaction, as the probability of errors in the execution of financial transactions decreases; reducing operational risk and its consequences (costs of operational risk insurance and the amount of capital required to cover operational risk are reduced); as well reducing the impact on the environment—the ecological footprint decreases by giving up material money carriers, diminishing the need for office space and logistics services.

For further research, it is suggested to study how financial inclusion interacts with different sustainability aspects while taking into account the hierarchy within the context of digital transformation of financial institutions, as well as the environment dimension of the sustainable development of the financial sector. Provided that digital transformation of financial institutions is possible only when appropriate legal framework is developed and adopted, regulatory aspects of digital transformation in the financial sector are important for further research, as well. In the context of the Baltic countries, in-depth research is needed to explain the differences between the dynamic of digital payments in all Baltic countries in general and the underlying reasons for a decrease in digital payments received in Lithuania in 2021 compared to 2014 in particular.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}