1. Introduction

Peer effect, in which decision makers imitate the behaviors of their peers, has been widely recognized as a phenomenon that arises when firms make operational decisions such as financing, investment and innovation. By following each other’s behavior, firms can obtain more information, gain valuable experience and reduce risks, especially when they are faced with a complicated and unpredictable external economic environment [

1,

2,

3]. However, peer effect could have adverse consequences for business at times and needs to be taken seriously [

4,

5,

6]. In the case of merger and acquisition (M&A) activities, there seemingly should not be a peer effect, since they often involve greater complexity and heterogeneity than regular investments; however, a few scholars have noticed that M&As may also be affected by peers [

7,

8,

9]. To this end, it is vital to better understand the existence and potential impact of peer effect, because M&A is one of the most important means for corporate restructuring and strategic development. If firms’ M&A decisions are indeed affected by their peers, it may have a significant but ambiguous or even negative impact on firms’ value or sustainable development [

10,

11,

12].

Meanwhile, the world is undergoing profound changes, and the world economy is unstable and clouded by various risks, including new virus variants, unanchored inflation expectations, and financial stress [

13]. The monthly global economic policy uncertainty (EPU) index developed by scholars from Northwestern University, Stanford University and University of Chicago has surged from 53.23 to 238.71 during the first two decades in the 21st century. In addition, as the world’s second largest economy, the stable development of China’s capital market and enterprises is of great importance. On the one hand, the EPU index of China has increased significantly from 9.07 to 755.26 within the last 20 years, indicating that the economic policy uncertainty of China is growing quickly and exceeding the world average. Consequently, firms may tend to imitate others for the sake of obtaining more information and reducing risks. On the other hand, M&A activities in China have risen sharply from 2000 to 2019, with an average annual growth rate of 14.7%. Against this background, the existence and impact of imitation behaviors among firms in M&As has received greater attention and demands for further research.

At present, the majority of studies related to peer effect concentrate on the imitation of peer firms in activities such as financing, regular investments and innovation [

14,

15,

16]. Little research on M&A peer effect has been conducted, most of which focuses on examining the existence of M&A peer effect [

7,

8]. There is little attention paid to the analysis of the mechanism and impact of M&A peer effect, and thus scholars have little insight into which factors will have impacts on the M&A peer effect, not to mention how the M&A peer effect will affect the development of firms, particularly their sustainable development.

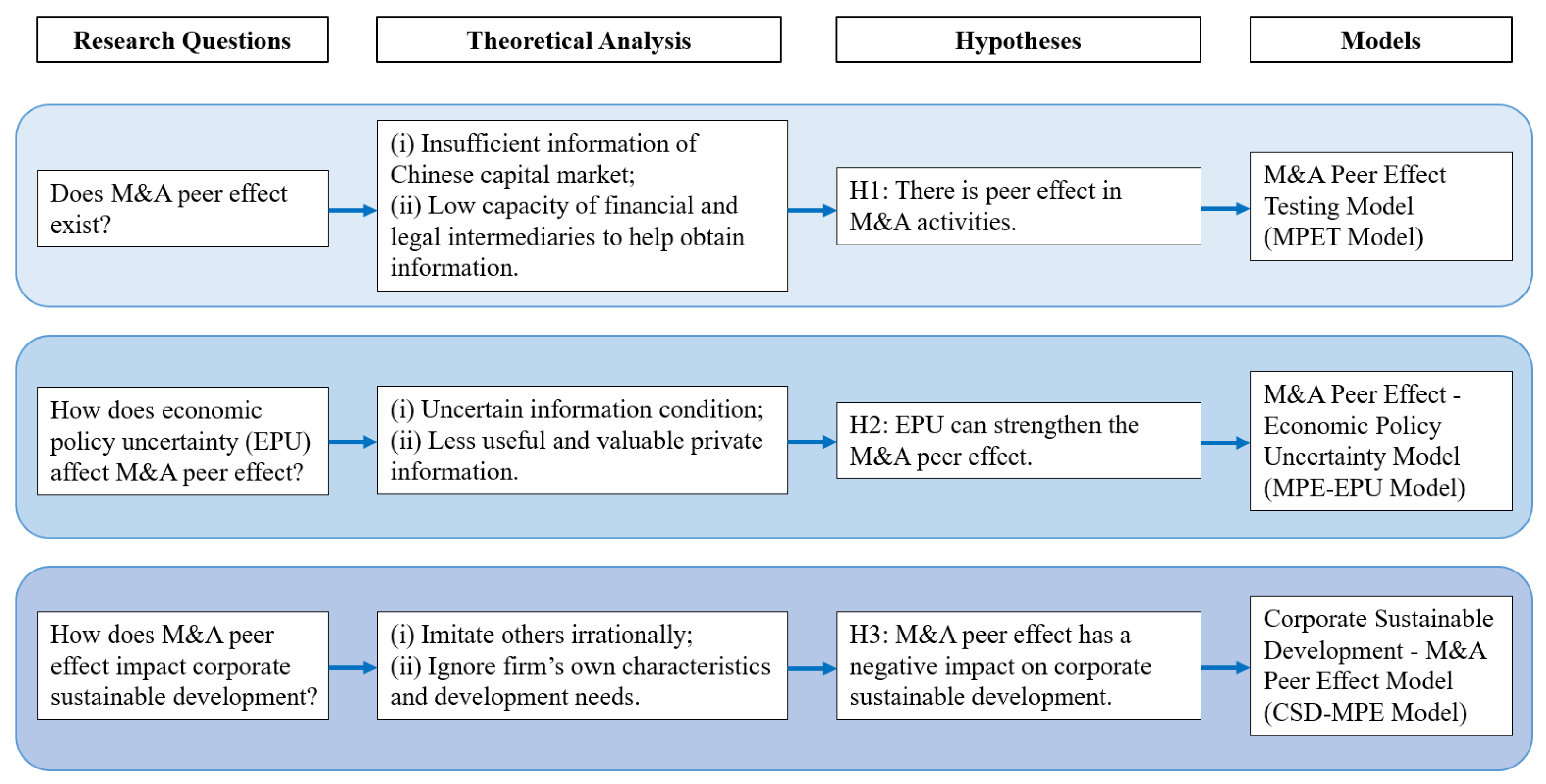

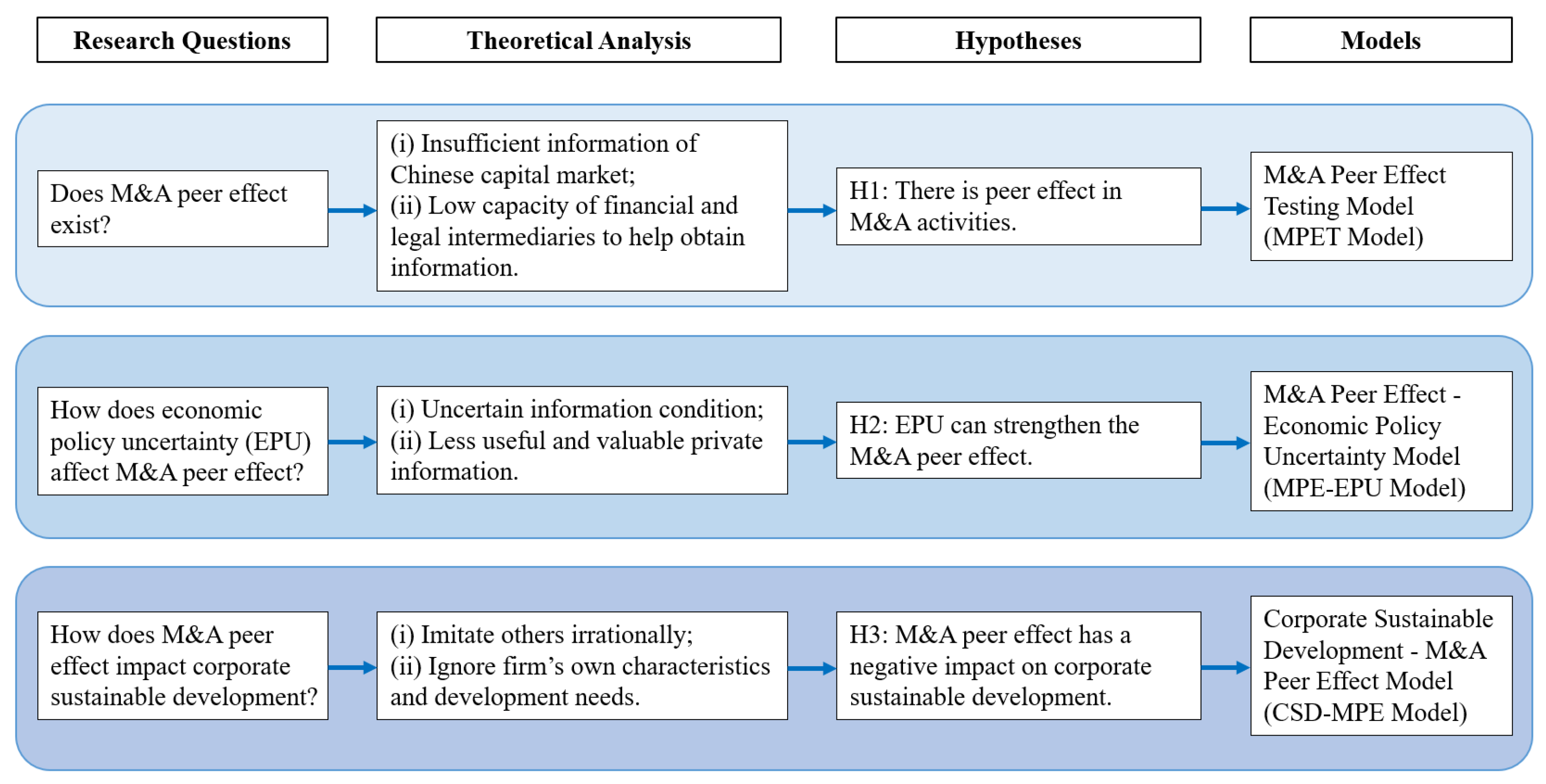

This research explores the existence, moderating factors and consequences of peer effect in M&A activities through the employment of three models. First, it constructs an M&A peer effect testing model to examine whether peers’ M&A activities would affect the firm’s M&A decisions. The findings show that peer firms’ M&A number and value will increase the firm’s M&A possibilities, number and value in the same industry, i.e., there is peer effect in M&As. The results of further moderating effect model suggest that the economic policy uncertainty could strengthen the overall peer effect in M&A activities. More importantly, the study builds a CSD-MPE model to investigate the impact of M&A peer effect on corporate sustainable development. The results show that M&A peer effect can negatively affect corporate sustainable development, which is more significant within a shorter period (e.g., one quarter after the M&A).

The study enriches the understanding of peer effect in M&A activities, and the main contributions are as follows: First, the study examines the existence of M&A peer effect based on 79,207 firm-quarter observations related to M&A in China from 1 January 2005 to 31 December 2019. Compared to the annual data used in earlier literature, the quarterly data in this paper helps capture the peer effect more accurately and offers a more solid conclusion. Second, the research investigates the impact of economic policy uncertainty on M&A peer effect by building a moderating effect model. This fills the mechanism research gap of previous work on M&A peer effect. Third, this study explores the correlation between M&A peer effect and corporate sustainable development for the first time, based on a novel measurement of M&A peer effect, by calculating the degree of deviation of a firm’s M&A number or value from its peer averages.

It is noteworthy that this paper offers three important implications. Theoretically, this paper establishes a systematic framework of M&A peer effect for the first time by analyzing its existence, moderating factors and impact on corporate sustainable development. This will enrich the theoretical research of behavior science in M&A activities as well as corporate sustainable development. Methodologically, this research improves the testing model of M&A peer effect at a quarterly rather than annual frequency, which could reflect information in a timelier fashion and provide more details of the peer effect. Practically, this research also provides an important reference for firms and policymakers to better understand the M&A peer effect and reduce irrational imitation in M&As, thus achieving sustainable development goals.

The remainder of this paper is organized as follows.

Section 2 reviews the relevant literature and develops three hypotheses.

Section 3 introduces the data selection and the three models.

Section 4 analyzes the empirical results and tests the robustness.

Section 5 summarizes the theoretical, methodological and practical implications of this paper.

Section 6 concludes the paper.

4. Empirical Results and Discussions

4.1. Descriptive Statistics

Table 1 summarizes the descriptive statistics for this study. It should be noted that the sample number is different for these empirical models due to the difference of calculation. The basic statistics of these models’ dependent and independent variables are reported in panel A/B/C separately, and the descriptive statistics of control variables are reported with the complete dataset.

Panel A reports the main variables used to examine whether there is peer effect in M&A activities. The average M&A possibility (MP) of each listed Chinese company between 2005 and 2019 is 0.051, with a standard deviation of 0.221. The volatility of the M&A value is larger than that of the number, both for firms (MV is 3.996 and MN is 0.250) and peer firms (PMV is 5.480 and PMN is 0.035). Panel B and C are different for the measurements of corporate sustainable growth rate (SGR). It is found that the observations of Panel C are less than Panel B since some samples are excluded for the lack of ΔSGRi,t−1,t+4. The mean and maximum value of ΔSGR in Panel B (Panel C) are −0.004 and 0.273 (−0.006 and 0.338), respectively, which indicates that although there exists positive ΔSGR, most companies’ SGR decreases. The mean value of PEN and PEV in Panel B (Panel C) is −1.960 and −0.780 (−1.961 and −0.780), respectively, suggesting that the M&A peer effect calculated by the M&A value is stronger than that calculated by the M&A number. As for the control variables, the overall characteristics of the remaining firm-specific control variables are generally consistent with the current economic conditions in China.

4.2. Peer Effect in M&A Activities and EPU’s Moderating Effect

4.2.1. Peer Effect in M&A Activities

Table 2 demonstrates the results of multiple regressions of the M&A peer effect testing model (MPET model). As mentioned before, the model is used to investigate the impact of peer firms’ M&A number and value on firm’s M&A decisions, which are measured by the M&A possibility (MP

i,t), M&A number (MN

i,t) and M&A value (MV

i,t). The results are shown in columns (1) and (4), columns (2) and (5), and columns (3) and (6), respectively.

All the coefficients of PMN−i,p,t−1 and PMV−i,p,t−1 in columns (1) through (6) are significant statistically. This indicates that the peer effect in M&A activities does exist, and peer firms’ M&A number and value will significantly impact the firm’s M&A possibility, number and value, regardless of whether there are control variables involved. In addition, the use of control variables helps to improve the goodness of fit of the model. It can be seen that adjusted R2 in columns (4) through (6) are higher than those in columns (1) through (3), while the coefficients of PMN−i,p,t−1 and PMV−i,p,t−1 decline slightly.

Furthermore, in the case of a better fit, the coefficient of PMN−i,p,t−1 is 0.086 with statistical significance, which means that a one-unit increase of peer firms’ M&A number at time t−1 will lead to an increase of 0.086 in the firm’s M&A possibility. The significantly positive coefficient of PMN−i,p,t−1 shown in column (5) indicates that a one-unit increase of the peer firms’ M&A number at time t−1 could also make the firm’s M&A number increase by 0.089. In addition, the coefficient of PMV−i,p,t−1 is 0.009 at a significance level of 1%, suggesting that a one-unit increase of peer firms’ M&A value at time t−1 could make the firm’s M&A value increase by 0.009. Namely, the more active the peer firms’ M&As are, the more active the firm’s M&As are, and vice versa. This is probably because peer firms’ M&As may send out a positive signal that the overall business environment (including economic environment, policy environment, etc.) is becoming friendly to M&A activities. It may prompt the firm to imitate others and conduct M&As as well. Moreover, sometimes it is inevitable for firms to emulate the strategies and decisions of their rivals in order to keep their position or reputation in the market, even though this may result in some negative effects.

In summary, the results of the MPET model show that the peer effect exists in the M&A activities of listed Chinese companies. Although the phenomenon has been studied by a few researchers, this paper offers a more solid conclusion based on a larger number of variables and a higher frequency of data. On the one hand, in previous studies, the industry M&A peer effect was only tested by assessing the correlation between the firm’s M&A possibility and its peer firms’ M&A number (i.e., MP and PMN) [

7]. This paper, however, utilizes three sets of variables (i.e., MP-PMN, MN-PMN and MV-PMV) to examine the M&A peer effect, which could provide a more comprehensive picture of this phenomenon. On the other hand, almost all scholars have studied the M&A peer effect based on annual data [

7,

8], assuming that peer firms’ M&A behavior in last year would affect the firm’s M&A decision in the current year; in this case, the information might already be out of date. This paper improves the testing model by using quarterly data instead, in order to capture the peer effect on M&A activities more accurately.

4.2.2. EPU’s Moderating Effect on M&A Peer Effect

Since the existence of peer effect in M&A activities has been proven above, this research will use the MPE-EPU model to explore how the M&A peer effect (MPE) is affected by economic policy uncertainty (EPU). The results of the regression are shown in

Table 3.

It can be noticed that the coefficients of PMN−i,p,t−1 and PMV−i,p,t−1 in columns (1) through (6) are still significantly positive when the regression adds EPU as a moderating variable. This means that peer firms’ M&A number and value will significantly increase firm’s M&A possibility, number and value, with the consideration of the external economic policy environment. In addition, the coefficient estimates of EPUt−1 are significantly negative in columns (1) through (3), and negative but insignificant in columns (4) through (6). This means that, on the one hand, when the economic development and policy environment uncertainty increases, the firm will be more cautious about its M&A decisions, thus reducing the M&A number and value. On the other hand, the negative impact of economic policy uncertainty on the M&A is not determinant, because whether or not to initiate an M&A deal is a complicated and comprehensive decision, which depends more on a firm’s strategy, resources, financial condition, etc.

More importantly, the coefficients of PMN−i,p,t−1 × EPUt−1 and PMV−i,p,t−1 × EPUt−1 reflect the moderating effect of EPU on M&A peer effect. The coefficients’ significance of these two variables are different, which indicates that there is a different moderating effect of economic policy uncertainty on peer M&A number and peer M&A value. Specifically, all the coefficient estimates of PMN−i,p,t−1 × EPUt−1 are statistically significant in columns (1), (2), (4) and (5), suggesting that the economic policy uncertainty of China could strengthen the impact of peer firms’ M&A number by enhancing the firm’s M&A possibility and M&A number. In other words, firms are more likely to be influenced by their peers’ M&A activities in the same industry during periods of higher economic policy uncertainty. As for the reasons, it is mainly because the higher the EPU, the harder it is for firms to obtain sufficient information to decide whether to initiate an M&A deal independently. In order to reduce risks, firms prefer to take peers’ M&A activities as an important information resource and tend to imitate peers’ behavior.

However, the insignificant positive coefficient estimates in columns (3) and (6) indicate that even though the economic policy uncertainty could strengthen the impact of peer firms’ M&A value by enhancing the firm’s M&A value, the moderating effect is not strong enough. This means that the impact of EPU on the relationship of peer firms’ and the firm’s M&A value is not as strong as that on M&A number. This is also because of M&A’s high heterogeneity, i.e., a firm might prefer to imitate its peers to initiate an M&A deal in an uncertain economic policy environment, but the sizes of the M&As are still more closely related to the firm’s unique characteristics.

It is worth mentioning that, although some scholars have recognized EPU’s moderating effect on imitation in firms’ regular investment and innovation [

3,

7], this paper studies EPU’s moderating mechanism of the M&A peer effect for the first time. The results in this research are valuable because they confirm that the information environment (which is measured by EPU) is significant not only for the peer effect in firms’ regular decisions (e.g., regular investment and innovation), but also for the peer effect in firms’ major and complicated decisions (e.g., M&A). In addition, the finding that EPU does not strengthen PMV’s impact on MV differs from previous studies, which examined the peer effect in firms’ regular decisions. This is another important contribution of this paper, which suggests that even though EPU could strengthen the peer effect both in M&A and firms’ regular decisions, there are still differences that need to be taken into consideration in the future.

4.3. The Impact of M&A Peer Effect on Corporate Sustainable Development

This paper constructs a CSD-MPE model to study how M&A peer effect (MPE) affects corporate sustainable development (CSD), and uses the change of sustainable growth rate to measure the variation of corporate sustainability.

As shown in

Table 4, first, when the change of sustainable growth rate is ΔSGR

i,t−1,t+1, the coefficient estimate of M&A peer effect degree calculated by the M&A number (PEN

i,p,t) in column (1) is −0.0001 at a significance level of 10%, and that of M&A peer effect degree calculated by M&A value (PEV

i,p,t) in column (2) is −0.0013 at a significance level of 5%. These results suggest that M&A peer effect has a significantly negative impact on corporate sustainable development, both in terms of M&A number and value. This is partly supported by previous research that suggests the peer effect is detrimental to firms’ value. For instance, Huang and Zhao [

4] put forward a similar idea when they studied how the corporate value changed when the firm imitated its peer firms’ dividend policy, and they indicated that by ignoring the differences between the firm itself and its peers, it might set dividend policies that do not meet its own characteristics, ultimately reducing its corporate value. A plausible explanation is that M&A peer effect may cause irrational M&A activities, which means the firm may initiate an M&A deal beyond its own development needs or without adequate preparation. This will negatively impact the sustainable development of firms after M&A. It is obvious that the complexity and systematic nature of M&A projects calls for extra caution; even a well-planned and well-discussed M&A might encounter many difficulties and problems, not to mention irrational deals.

Second, when the change of sustainable growth rate is ΔSGR

i,t−1,t+4, the coefficient estimate of M&A peer effect degree calculated by M&A number (PEN

i,p,t) in column (3) is still −0.0001 but is insignificant statistically, and that of M&A peer effect degree calculated by M&A value (PEV

i,p,t) in column (4) is −0.0017 at a significance level of 5%. The results in

Table 4 illustrate that the negative impact of M&A peer effect is more significant within a shorter period (e.g., one quarter after the M&A), since the longer the period is, the more factors there are to possibly affect the corporate sustainable growth rate, and thus the influence of the peer effect will be weakened.

Third, the impact of M&A peer effect degree calculated by the M&A value is stronger than that calculated by M&A number. This is because the M&A value contains more unique information about each firm. Therefore, the M&A peer effect degree calculated by the M&A value is more closely related to corporate sustainable development.

Overall, the findings above suggest that firms may jeopardize their own sustainable development when imitating others in M&A activities, and the negative influence varies with time as well as the measurement of peer effect degree. This brings a new perspective on understanding imitation in M&A activities and its impact, which is important both theoretically and practically.

4.4. Robustness Test

4.4.1. Alternative Measures of Peer Firms’ M&A Activities

In order to test the robustness of the results on whether there is a peer effect in China’s M&A market and EPU’s moderating effect on it, this study remeasured peer firms’ M&A activities by the ratio of peer firms that initiated M&As at time

t−1 (PR

−i,p,t−1). The results in

Table 5 indicate that the baseline findings are robust to the alternative measure of peer firms’ M&A activities with PR

−i,p,t−1.

More precisely, all the coefficients of PR−i,p,t−1 in columns (1) through (6) above are significantly positive, suggesting that the larger the PR−i,p,t−1 (i.e., the more peers take part in M&As), the greater the M&A peer effect (i.e., the greater the impact it has on a firm’s M&A decisions). Columns (2), (4) and (6) present EPU’s impact on the M&A peer effect. The coefficients of PR−i,p,t−1 × EPUt−1 are 0.0391, 0.0476 and 0.7607 at a significance level of 5%. This means that when the external economic policy uncertainty increases, firms tend to become increasingly dependent on their peers and attempt to obtain more information from them in order to diminish uncertainty. That is to say, economic policy uncertainty could motivate the firm to imitate peers’ M&A behavior.

4.4.2. Controlling for Industry-Level Factors

It is argued that firms might make the same decisions because they are facing the same conditions, rather than trying to imitate one another [

45,

46]. As firm-specific characteristics were already controlled in the baseline regression, for robustness, this study further controlled related industry-level factors to eliminate the effect of industrial characteristics (which represents the same conditions firms are facing).

Table 6 below shows the results of the examination of M&A peer effect. On the one hand, with industry-level factors controlled, the coefficient estimates of PMN

−i,p,t−1 and PMV

−i,p,t−1 in columns (1), (3) and (5) are also significantly positive but smaller than those in

Table 3 (which doesn’t control the industry-level factors). This means that even when considering the influence of industry factors, the M&A peer effect exists. Meanwhile, the industrial characteristics also affect firms’ M&A decisions; therefore, the addition of these characteristics will reduce the M&A peer effect to a certain extent. On the other hand, the coefficients of PMN

−i,p,t−1 × EPU

t−1 are positive at a significance level of 5% in columns (2) and (4), while the coefficient of PMV

−i,p,t−1 × EPU

t−1 is insignificantly positive in column (6). This is also consistent with the results in

Table 3. Therefore, the baseline findings of the existence of M&A peer effect and EPU’s moderating effect are robust to a stricter controlling regression.

Table 7 shows the correlation between the M&A peer effect and corporate sustainable development. It is found that the coefficient estimates in

Table 7 are almost the same as those in

Table 4 (which doesn’t control for the industry-level factors). This also provides robust evidence for the baseline findings of the negative impact of M&A peer effect on corporate sustainable development. It indicates that the industry-level factors have a limited influence on specific corporate sustainability. This is because a firm’s sustainable growth rate depends more on its own strategies, resources and operating conditions, etc., and all of these may adjust to its industrial environment but are not necessarily determined by it.

4.4.3. Adjusting Industry Classification Standards

Although the industry classification standards in this study are generally adopted [

20,

47,

48], the paper adjusts the standards by applying a three-digit SIC code to all industries for the robustness test. After the adjustment, the industry number of the research increased from 47 to 65. The peer firms’ M&A variables were recalculated accordingly.

With the new classification of industries, it can be seen in

Table 8 that most of the coefficient estimates are significantly positive. This means that peer firms’ M&A activities have a significant positive impact on the firm’s M&A decisions, which is consistent with the baseline regression. However, it is found that the coefficients are less significant and smaller than those in

Table 3. In addition, EPU’s positive moderating effect remains almost the same as the results in

Table 3, indicating that even when the peer groups in the same industry become smaller, an uncertain economic policy environment can still strengthen the M&A peer effect.

As shown in

Table 9, the M&A peer effect degree still has a negative impact on corporate sustainable growth rate with the new classification of industries. All of the results are consistent with the baseline findings in

Table 4, which prove the robustness of the models.

5. Implications

5.1. Theoretical Implications

This study analyzes the peer effect in M&A activities and its impact on corporate sustainable development. The findings show that the peer effect in M&A activities does exist, can be strengthened when the economic policy uncertainty increases, and has a negative influence on firms’ sustainability.

Peer effect has become an increasingly common phenomenon, based on the fact that it can be seen not only in firms’ regular decisions (e.g., regular investment and innovation) [

4,

5,

16,

20,

21,

22,

23] but also in firms’ major decisions, such as mergers and acquisitions [

7,

8]. This paper provides evidence that there is a significantly positive correlation between a firm’s M&A decisions and its peers’ previous M&A activities in the same industry. This means that the previous behavior of peers would become one of the most important sources of information for the firm, especially when firm’s private information is limited due to its low capacity of information collection or the imperfect market [

18].

The results of the paper reveal that the external uncertainty could strengthen the M&A peer effect. The examination of the moderating effect of economic policy uncertainty on the M&A peer effect in this study suggests that firms are more likely to imitate their peers to initiate an M&A deal in an uncertain economic policy environment. This is because the higher the uncertain economic policy environment, the harder it is for firms to obtain sufficient information to make decisions independently. In order to reduce risks, firms tend to rely on their peers’ previous behavior [

3]. This imitation may help them to maintain the same condition as others. Thus, improving the information environment (i.e., diminishing the economic policy uncertainty) and enhancing the capacity of firms to acquire and manage information are effective ways to reduce the peer effect in M&A activities.

Furthermore, firms should pay more attention to the M&A peer effect and be more cautious with their imitation in M&A deals, because the M&A peer effect has a significantly negative impact on their sustainability. Some previous studies on the peer effect in firms’ regular decisions have concluded that the peer effect is beneficial for firms, since it can help them to obtain more information and experience from peers [

31,

32], while others argue that it is detrimental because firms might imitate their peers without taking into account their own characteristics [

4,

6]. The findings of this paper indicate that the complexity and systematic nature of M&A projects calls for extra caution; even a well-planned and well-discussed M&A might come across many difficulties and problems, not to mention irrational deals as a result of imitating peers. That is to say, although firms might attempt to imitate peers’ M&A behaviors as a way of obtaining more information, reducing risks, maintaining their competence or reputation, etc., the resulting M&A peer effect will unfortunately undermine their sustainable development.

5.2. Methodological Implications

This study constructs three models to examine the research hypotheses.

First, it builds the M&A peer effect testing model (MPET model) to investigate the peer effect in M&A activities. With this model, the accuracy of peer effect testing for M&As is improved, which is important for the research on this topic. Specifically, unlike previous research, the MPET model examines the existence of the peer effect in M&A activities at a quarterly rather than annual frequency, which could reflect the information in a timelier fashion and provide more details about the influence of peer firms’ M&A previous behavior on the firm’s M&A decision.

Second, the M&A peer effect-economic policy uncertainty model (MPE-EPU model) is constructed to explore EPU’s moderating effect on M&A peer effect. Although the moderating effect of EPU is widely recognized in the research of peer effect in firms’ investment and innovation [

3,

7], the moderating effect of EPU is tested in the M&A peer effect for the first time.

Third, the paper proposes the corporate sustainability development-M&A peer effect model (CSD-MPE model) to study how M&A peer effect impacts corporate sustainable development. It is worth noting that the research innovatively measures the M&A peer effect degree by the deviation between the firm’s M&A number/value and its peers’ average M&A number/value. The combined measures of number and value allow exploration of the M&A peer effect from different perspectives, thus facilitating more comprehensive and integrated analysis and conclusions.

5.3. Practical Implications

The economic policy uncertainty index of China has surged from 9.07 to 755.26 from 2000 to 2019, which is much faster than the world average (53.23 to 238.71). At the same time, M&A activities in China have risen sharply, with an average annual growth rate of 14.7%. This means that the imitation (including irrational imitation) in M&A activities could have increased as well, which should be taken into account. Hence, the findings of this study offer great practical value to Chinese firms and policymakers, especially when the world is undergoing unprecedented changes.

As for firms, given the negative impact that M&A peer effect could have on corporate sustainable development, firms should be more cautious when engaging in M&A activities and should give careful consideration to the timing, target and purpose of M&As. Meanwhile, by leveraging technologies such as big data and artificial intelligence, companies can improve the way they acquire, process, and manage information. This will help them become less dependent on peers’ information and make better decisions.

As for policymakers, based on the findings that economic policy uncertainty could strengthen the M&A peer effect, they should find a way to diminish economic policy uncertainty. Aiming to achieve this goal, policymakers should try to enhance the continuity of policies and improve transparency in information disclosure and sharing. Additionally, it is important for policymakers to strengthen investor education, accelerate the establishment and improvement of the vocational education system, and provide better guidance and advisory support, so as to help firms reduce irrational imitation in M&A activities.

6. Conclusions and Future Work

This study enriches the research on the M&A peer effect by employing a comprehensive M&A dataset for China between 1 January 2005 and 31 December 2019, to investigate the existence of the peer effect in M&As and study its impact on corporate sustainable development. The analysis began with constructing an MPET model with quarterly data to examine whether there is peer effect in M&A activities. Then, the MPE-EPU model was built to evaluate the moderating effect of economic policy uncertainty on M&A peer effect. Finally, the research proposed the CSD-MPE model to explore the correlation between M&A peer effect and corporate sustainable development. The findings of this paper offer theoretical, methodological and practical implications, especially within the context of China’s M&A market.

It was found that the M&A peer effect does exist in listed Chinese companies. Firms tend to imitate their industry peers’ M&A behaviors, which means that peer firms’ M&A number and value will increase the firm’s M&A possibility, number and value. The economic policy uncertainty has a significantly positive moderating effect on the M&A peer effect. In other words, the increase of external uncertainty could strengthen a firm’s tendency to imitate its peers in M&A deals. Furthermore, M&A peer effect has a negative influence on corporate sustainable development, using both the M&A peer effect and M&A number or value. And the negative impact calculated by M&A value is significantly stronger than that which calculated by M&A frequency, it is most likely because the M&A value contains more unique information for each firm. Also, the negative impact of M&A peer effect is more significant within a shorter period after the M&A (e.g., after one quarter), since the longer the period, the more factors will affect the corporate sustainable development, thus the influence of the peer effect will be weakened.

The theoretical contributions of this research are mainly based on its innovative investigation of the M&A peer effect in a more systematic way by conducting theoretical analysis, proposing an innovative way to measure the M&A peer effect, examining its existence, studying EPU’s impact on the peer effect and the peer effect’s influence on corporate sustainable development. All of these could fill the research gap of behavior science studies on M&A activities as well as corporate sustainability. Methodologically, the study improves the accuracy of the testing model of M&A peer effect based on quarterly data, which captures the peer effect more accurately and offers a more solid conclusion compared to the annual data used in earlier literature. Moreover, the findings provide further practical support for both Chinese firms and policymakers to mitigate irrational imitation in M&A activities, thus achieving the corporate sustainable development goals.

Although the study has contributed to explore the peer effect in M&A activities and its impact on corporate sustainable development, it is subject to certain limitations worth noting. First, the empirical results are only based on the data of acquiring firms and may not be able to reflect the peer effect and its impact on acquirees. Therefore, in order to improve the completeness of the findings, it is necessary to investigate M&A peer effect from the perspective of acquirees. Second, it is believed that competition pressure and managers’ desire to maintain their reputation will also increase firms’ tendency to imitate their peers. These variables can be further used to complete the moderating mechanisms of M&A peer effect. Third, the indicators to reflect corporate sustainable development are limited in this paper. Future research can attempt to measure the corporate sustainability through risk management, market position maintenance, etc., to refine the CSD-MPE model. Last, this paper pays more attention to the M&A peer effect’s influence on the firm itself, while its influence on other stakeholders (e.g., industry, M&A market, etc.) is worth studying as well. Hence the research can be further improved by broadening the research objects.

{kind=link}