The Effect of COVID-Related EU State Aid on the Level Playing Field for Airlines

Abstract

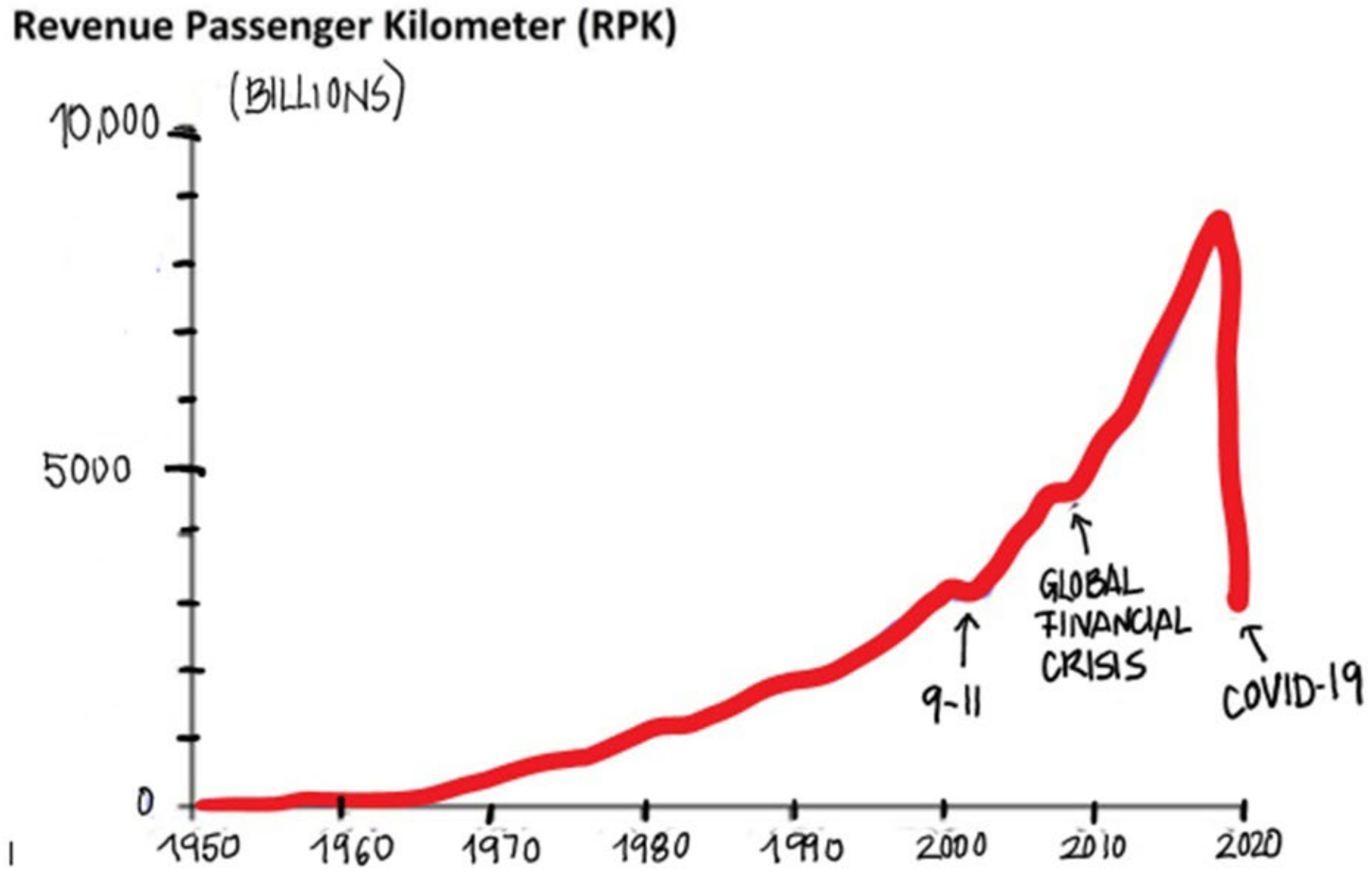

:1. Introduction

2. Materials and Methods

2.1. Literature Review

2.2. COVID-19 State Aid to EU Airlines

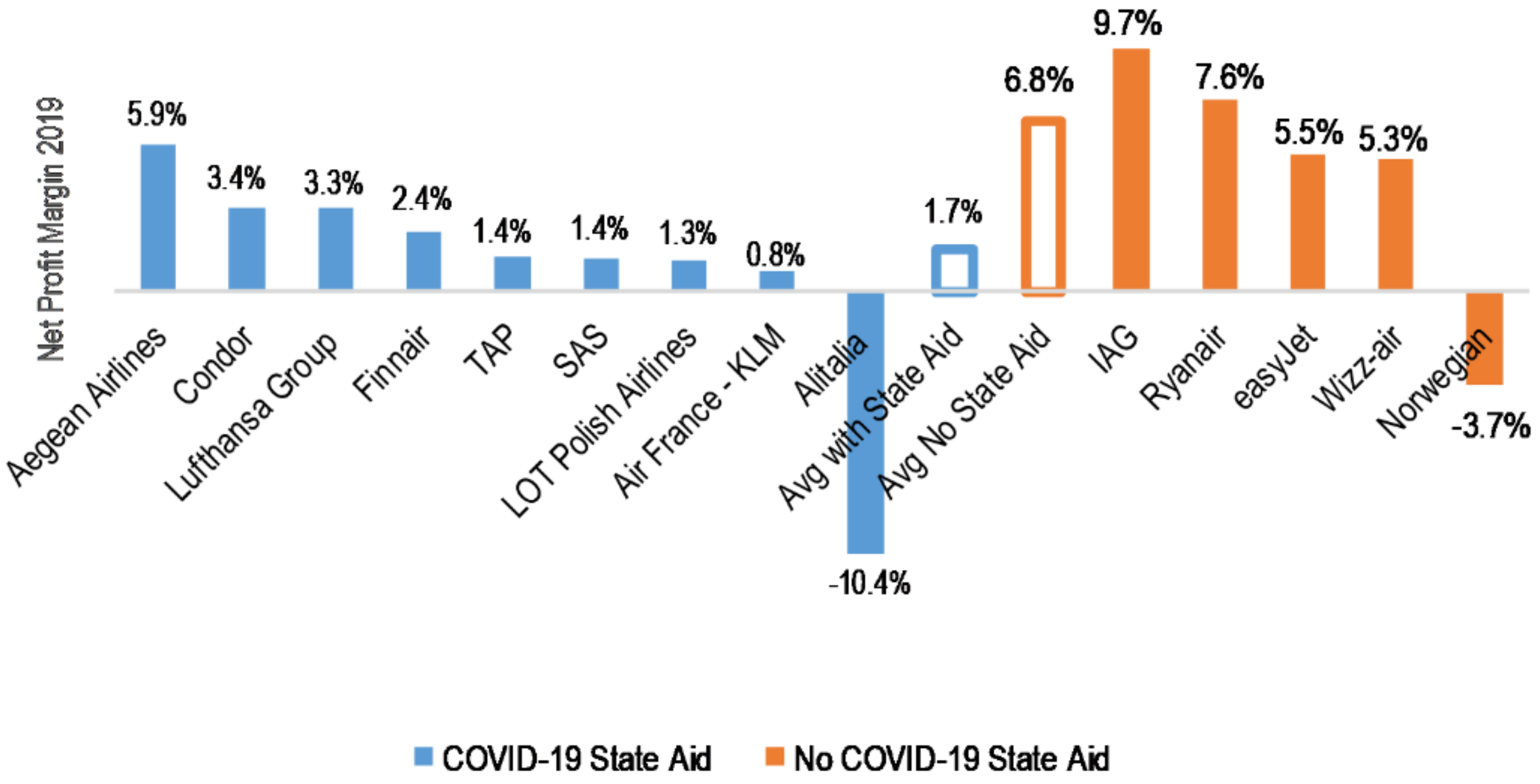

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| ID | Case Code | Country | Airline | Aid € Million | Instrument | EC Decision | Date |

|---|---|---|---|---|---|---|---|

| 1 | SA.55373 | Croatia | Croatia Airlines | 17 | Direct Grant | No Objections | 30 November 2020 |

| 2 | SA.56795 | Denmark | SAS | 137 | Guarantee | No Objections | 15 April 2020 |

| 3 | SA.56809 | Finland | Finnair | 600 | Guarantee | No Objections + Corrigendum | 29 July 2020 |

| 4 | SA.56810 | Romania | TAROM | 19 | Guarantee | No Objections | 2 October 2020 |

| 5 | SA.56867 | Germany | Condor | 550 | Loan | No Objections | 26 July 2021 |

| 6 | SA.56943 | Latvia | Air Baltic | 250 | Recapitalization | No Objections | 3 July 2020 |

| 7 | SA.57026 | Romania | Blue Air | 62 | Guarantee | No Objections | 20 August 2020 |

| 8 | SA.57061 | Sweden | SAS | 137 | Guarantee | No Objections | 24 April 2020 |

| 9 | SA.57082 | France | Air France–KLM | 7000 | Guarantee | No Objections + Corrigendum | 26 July 2021 |

| 10 | SA.57116 | Netherlands | Air France–KLM | 3400 | Guarantee | No Objections | 16 July 2021 |

| 11 | SA.57153 | Germany | Lufthansa Group | 6000 | Recapitalization | No Objections | 5 November 2020 |

| 12 | SA.57153 | Germany | Lufthansa Group | 3000 | Guarantee | No Objections | 5 November 2020 |

| 13 | SA.57410 | Finland | Finnair | 286 | Recapitalization | No Objections | 9 June 2020 |

| 14 | SA.57539 | Austria | Lufthansa Group | 150 | Direct Grant | No Objections | 6 July 2020 |

| 15 | SA.57543 | Denmark | SAS | 1000 | Recapitalization | No Objections + Corrigendum | 23 February 2021 |

| 16 | SA.57544 | Belgium | Lufthansa Group | 290 | Loan | No Objections + Corrigendum | 30 September 2020 |

| 17 | SA.57586 | Estonia | Nordica | 30 | Recapitalization | No Objections | 11 August 2020 |

| 18 | SA.58114 | Italy | Alitalia | 200 | Direct grant | No Objections | 4 September 2020 |

| 19 | SA.58125 | France | Corsair | 140 | Direct grant | No Objections | 11 December 2020 |

| 20 | SA.58342 | Sweden | SAS | 1000 | Recapitalization | No Objections + Corrigendum | 23 February 2021 |

| 21 | SA.59158 | Poland | LOT Polish Airlines | 400 | Loan | No Objections | 22 December 2020 |

| 22 | SA.59158 | Poland | LOT Polish Airlines | 250 | Recapitalization | No Objections | 22 December 2020 |

| 23 | SA.59462 | Greece | Aegean Airlines | 120 | Direct Grant | No Objections | 23 December 2020 |

| 24 | SA.59913 | France | Air France–KLM | 4000 | Recapitalization | No Objections | 5 April 2021 |

| 25 | SA.60113 | Finland | Finnair | 350 | Loan | No Objections | 12 March 2021 |

| 26 | SA.62304 | Portugal | TAP | 462 | Direct Grant | No Objections | 23 April 2021 |

| 27 | SA.62304 | Portugal | TAP | 1200 | Loan | No Objections | 23 April 2021 |

References

- International Air Transport Association (IATA). Airline Investor Report. Available online: https://www.iata.org/en/iata-repository/publications/economic-reports/new-study-on-airline-investor-returns/ (accessed on 1 November 2021).

- International Air Transport Association (IATA). IATA’s Annual Review 2020. Available online: https://www.iata.org/en/publications/annual-review/ (accessed on 2 November 2021).

- Organisation for Economic Cooperation and Development (OECD). State Support to the Air Transport Sector: Monitoring Developments Related to the COVID-19 Crisis. Available online: https://www.oecd.org/corporate/State-Support-to-the-Air-Transport-Sector-Monitoring-Developments-Related-to-the-COVID-19-Crisis.pdf (accessed on 1 November 2021).

- US-Congress. Coronavirus Aid, Relief, and Economic Security Act—CARES Act (2019/2020) [Legislation]. Available online: https://www.congress.gov/bill/116th-congress/senate-bill/3548/text (accessed on 1 November 2021).

- GAO Financial Assistance: Lessons Learned from CARES Act Loan Program for Aviation and Other Eligible Businesses. Available online: https://www.gao.gov/products/gao-21-198 (accessed on 1 November 2021).

- EU European Union. Available online: https://europa.eu/european-union/about-eu/institutions-bodies/european-commission_en (accessed on 1 November 2021).

- EC Treaty on the Functioning of the European Union (TFEU)—Chapter 1: Rules on Competition—Section 2: Aids Granted by States—Article 107. Available online: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:12012E/TXT:en:PDF (accessed on 1 November 2021).

- International Air Transport Association (IATA). COVID 19 Impact on Global and Regional Flight Departures. Available online: https://www.iata.org/contentassets/91cf8136124a4bc3a62625539188b107/covid19-flight-impact_pax_060720.pdf (accessed on 2 November 2021).

- Eurocontrol COVID_7D_portal. Google Data Studio. Available online: http://datastudio.google.com/reporting/b2b43aeb-ce1d-4c7e-961a-8bb646368111/page/jwMJB?feature=opengraph (accessed on 1 November 2021).

- European Commission. Temporary Framework for State Aid Measures to Support the Economy in the Current COVID-19 Outbreak 2020/C 91 I/01. Available online: https://ec.europa.eu/competition-policy/state-aid/coronavirus/temporary-framework_en (accessed on 1 November 2021).

- European Commission. Amendments to the State Aid Temporary Framework. Available online: https://ec.europa.eu/competition-policy/state-aid/coronavirus/temporary-framework/amendments_en (accessed on 1 November 2021).

- International Air Transport Association (IATA). COVID-Government Aid. Available online: https://www.iata.org/en/iata-repository/publications/economic-reports/government-aid-and-airlines-debt/ (accessed on 2 November 2021).

- Abate, M.; Christidis, P.; Purwanto, A.J. Government support to airlines in the aftermath of the COVID-19 pandemic. J. Air Transp. Manag. 2020, 89, 101931. [Google Scholar] [CrossRef] [PubMed]

- Tretheway, M.W.; Markhvida, K. The aviation value chain: Economic returns and policy issues. J. Air Transp. Manag. 2014, 41, 3–16. [Google Scholar] [CrossRef]

- Halpern, N.; Graham, A. The Routledge Companion to Air Transport Management; Routledge: Abingdon, UK, 2018. [Google Scholar]

- Tretheway, M.; Andriulaitis, R. What do we mean by a level playing fi eld in international aviation ? Transp. Policy 2015, 43, 96–103. [Google Scholar] [CrossRef] [Green Version]

- Österman, C.; Boström, M. Workplace bullying and harassment at sea: A structured literature review. Mar. Policy 2022, 136, 104910. [Google Scholar] [CrossRef]

- Gössling, S.; Fichert, F.; Forsyth, P. Subsidies in Aviation. Sustainability 2017, 9, 1295. [Google Scholar] [CrossRef] [Green Version]

- Organisation for Economic Cooperation and Development (OECD). Environmentally Harmful Subsidies. Challenges for Reform; OECD: Paris, France, 2005. [Google Scholar]

- Steinrücken, T.; Jaenichen, S. Towards the conformity of infrastructure policy with European laws: The case of government aid for Ryanair. Intereconomics 2004, 39, 97–102. [Google Scholar] [CrossRef]

- Eaton, J. Flying the flag for subsidies-Prospects for Airline Deregulation in Europe. Intereconomics 1996, 31, 147–152. [Google Scholar] [CrossRef] [Green Version]

- Abate, M.; Christidis, P. Economics of Transportation The impact of air transport market liberalization: Evidence from EU’s external aviation policy. Econ. Transp. 2020, 22, 100164. [Google Scholar] [CrossRef]

- Budd, T. ‘The end of liberalization?’—Selected papers from the 4th European Aviation Conference (EAC), UK, 2015. J. Air Transp. Manag. 2019, 74, 20–21. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research: Design and Methods; SAGE Publications: London, UK, 1989. [Google Scholar]

- European Commission. Competition Policy—Search Competition Cases (All Policy Areas). Available online: https://ec.europa.eu/competition/elojade/isef/index.cfm?clear=1&policy_area_id=3 (accessed on 1 November 2021).

- Air France-KLM. Appointment Of The Monitoring Trustee In Case SA.59913–Recapitalization of Air France and the Air France-KLM Holding. Air France-KLM Publications. Available online: https://www.airfranceklm.com/en/system/files/appointment_of_the_monitoring_trustee.pdf (accessed on 2 November 2021).

- European Commission. State Aid: Award of Slots at Paris-Orly to Vueling. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_21_4805 (accessed on 2 November 2021).

- Laborda, J.; Rivera-Torres, P.; Salas-Fumas, V.; Suárez, C. Is there life beyond the Spanish government’s aid to furloughed employees by COVID-19? PLoS ONE 2021, 16, e0253331. [Google Scholar] [CrossRef] [PubMed]

- World Bank. Population, Total|Data. Available online: https://data.worldbank.org/indicator/SP.POP.TOTL?name_desc=false (accessed on 2 November 2021).

- Macilree, J.; Duval, D.T. Aeropolitics in a post-COVID-19 world. J. Air Transp. Manag. 2020, 88, 101864. [Google Scholar] [CrossRef] [PubMed]

- Raidió Teilifís Éireann (RTE). Norwegian Air to Furlough 1600 Staff after Government Said It Would Not Support Airline. Available online: https://www.rte.ie/news/business/2020/1109/1176863-norwegian-air-funding/ (accessed on 4 January 2022).

- European Commision. State Aid SA.59913—France COVID-19—Recapitalisation of Air France and the Air France—KLM Holding. 2021. Available online: https://ec.europa.eu/competition/elojade/isef/case_details.cfm?proc_code=3_SA_59913 (accessed on 4 January 2022).

- Bock, S.; Forsyth, P.; Niemeier, H.M.; Mantin, B. Chapter 11 and the level playing field: Should chapter 11 be considered as a subsidy? J. Air Transp. Manag. 2019, 74, 39–46. [Google Scholar] [CrossRef]

- Albers, S.; Rundshagen, V. European airlines′ strategic responses to the COVID-19 pandemic (January–May, 2020). J. Air Transp. Manag. 2020, 87, 101863. [Google Scholar] [CrossRef] [PubMed]

- Partnership for Open & Fair Skies. Massive Subsidies Are Distorting the International Aviation Market. Available online: https://skift.com/wp-content/uploads/2015/03/White.Paper-2.pdf%0A (accessed on 2 January 2022).

- Shepardson, D.; Bayoumy, Y.U.S. and UAE Sign Pact to Resolve Airline Competition Claims. Available online: https://www.reuters.com/article/us-usa-airlines-emirates-idUSKBN1IC2BK (accessed on 2 January 2022).

- European Commission. Subject: State Aid SA. 57153 (2020/N)—Germany—COVID-19-Aid to Lufthansa Excellency, Following Pre-Notification Contacts, 1 by Electronic Notification of 12 June 2020, Germany Notified Aid in the Form of a Recapitalisation of Deutsche Luftha. Available online: https://ec.europa.eu/competition/elojade/isef/case_details.cfm?proc_code=3_SA_57153 (accessed on 2 January 2022).

- Kovac, M.; Elkanawati, A.; Gjikolli, V.; Vandenberghe, A.-S. The COVID-19 Pandemic: Collective Action and European Public Policy under Stress. Cent. Eur. J. Public Policy. 2020, 14, 47–59. [Google Scholar] [CrossRef]

- Martín, J.C.; Román, C. The effects of COVID-19 on EU federalism. East. J. Eur. Stud. 2021, 12, 126–148. [Google Scholar] [CrossRef]

- Meidute-Kavaliauskiene, I.; Yıldız, B.; Çiğdem, Ş.; Činčikaitė, R. The effect of COVID-19 on airline transportation services: A study on service robot usage intention. Sustainability 2021, 13, 12571. [Google Scholar] [CrossRef]

| Airline | Revenue 2019 € Million | Aid € Million | Percentage Aid/Rev |

|---|---|---|---|

| Air France–KLM | 27,189 | 14,400 | 53% |

| SAS | 4381 | 2274 | 52% |

| TAP | 3298 | 1662 | 50% |

| Air Baltic | 503 | 250 | 50% |

| Finnair | 3097 | 1236 | 40% |

| LOT Polish Airlines | 1695 | 650 | 38% |

| Condor | 1700 | 550 | 32% |

| Corsair | 438 | 140 | 32% |

| Nordica | 104 | 30 | 29% |

| Lufthansa Group | 36,424 | 9440 | 26% |

| Blue Air | 458 | 62 | 14% |

| Aegean Airlines | 1328 | 120 | 9% |

| Croatia Airlines | 231 | 17 | 7% |

| TAROM | 302 | 19 | 6% |

| Alitalia | 4056 | 200 | 5% |

| Total | 85,204 | 31,050 | 36% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Martín-Domingo, L.; Martín, J.C. The Effect of COVID-Related EU State Aid on the Level Playing Field for Airlines. Sustainability 2022, 14, 2368. https://doi.org/10.3390/su14042368

Martín-Domingo L, Martín JC. The Effect of COVID-Related EU State Aid on the Level Playing Field for Airlines. Sustainability. 2022; 14(4):2368. https://doi.org/10.3390/su14042368

Chicago/Turabian StyleMartín-Domingo, Luis, and Juan Carlos Martín. 2022. "The Effect of COVID-Related EU State Aid on the Level Playing Field for Airlines" Sustainability 14, no. 4: 2368. https://doi.org/10.3390/su14042368

APA StyleMartín-Domingo, L., & Martín, J. C. (2022). The Effect of COVID-Related EU State Aid on the Level Playing Field for Airlines. Sustainability, 14(4), 2368. https://doi.org/10.3390/su14042368