How Do Mobile Wallets Improve Sustainability in Payment Services? A Comprehensive Literature Review

Abstract

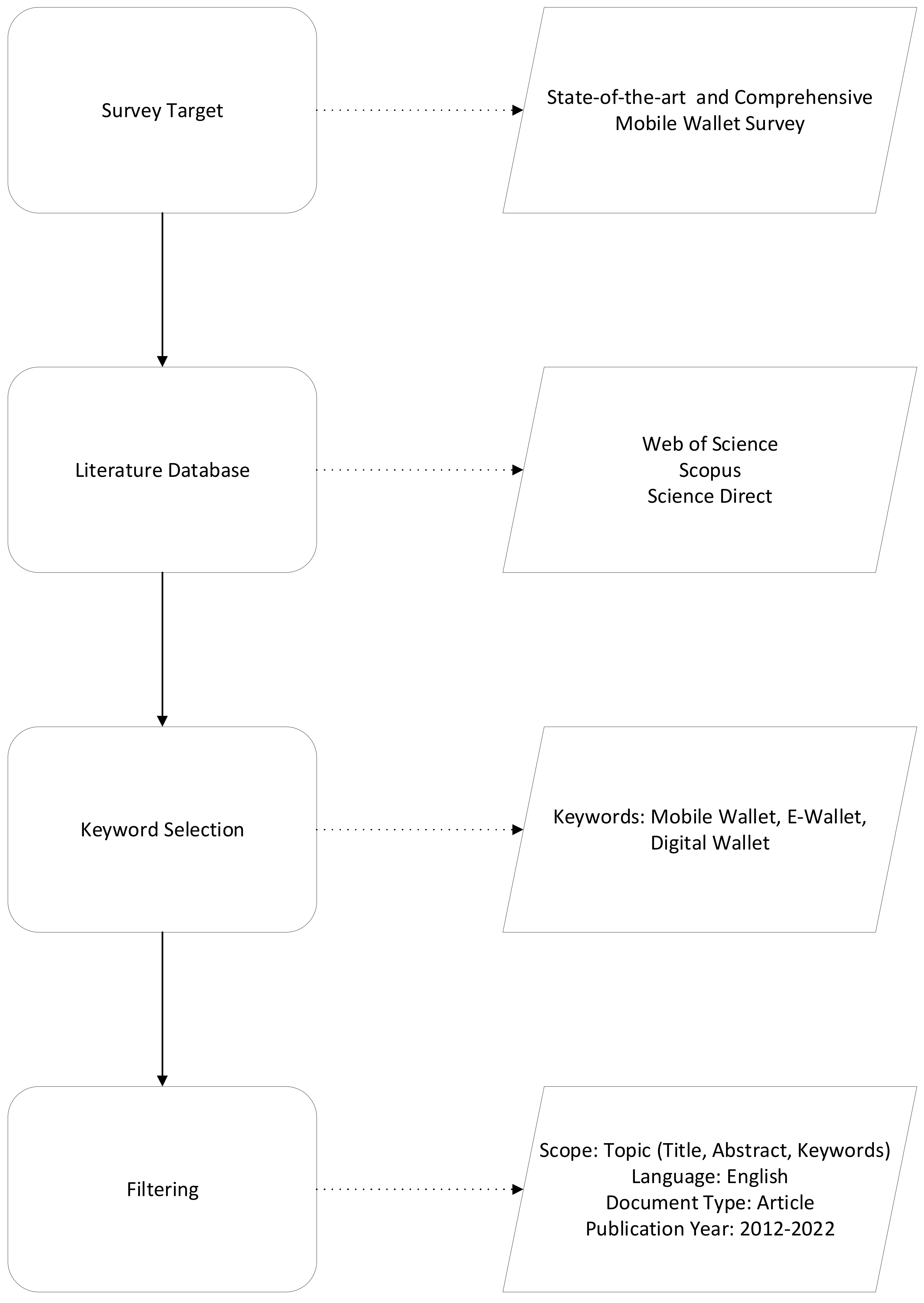

1. Introduction

2. Methods

3. Results

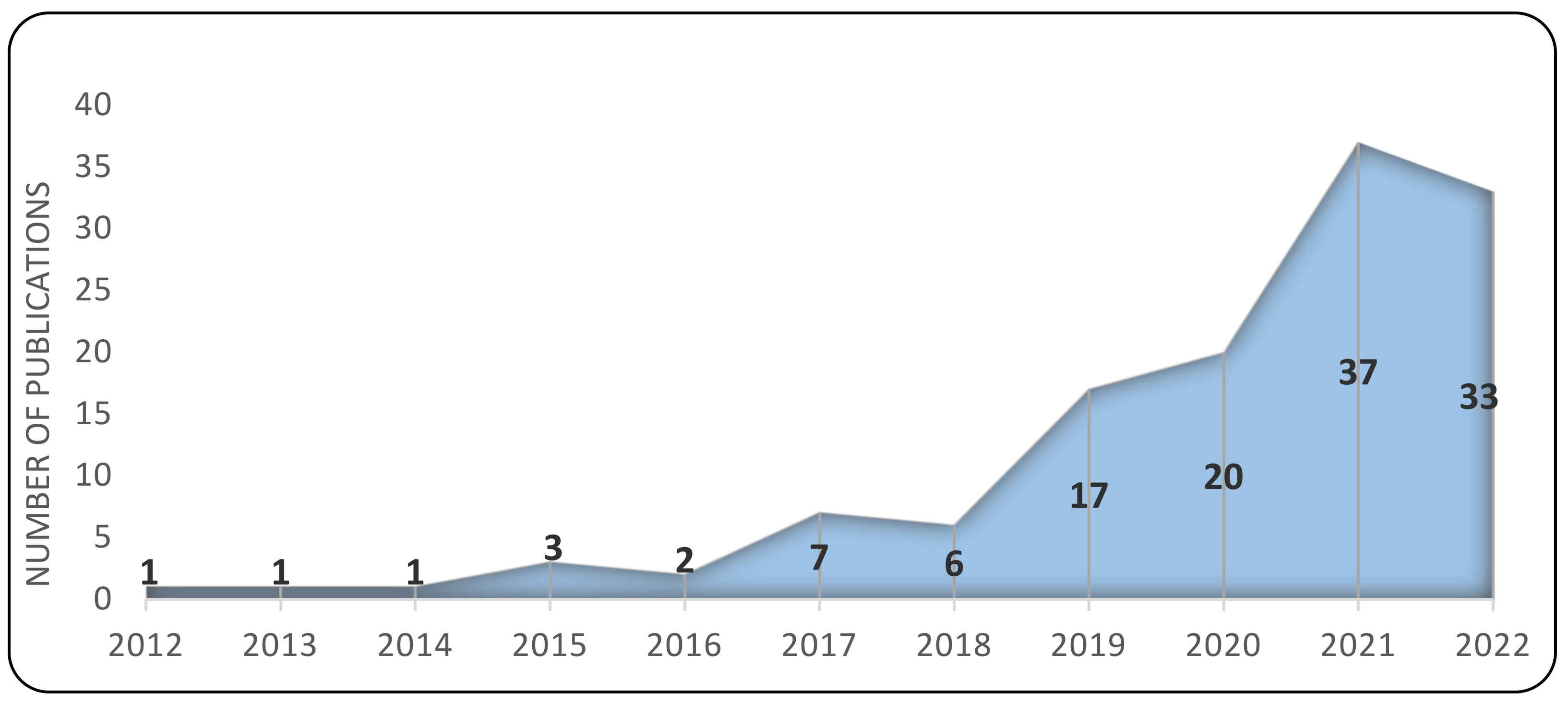

3.1. Years of Publication

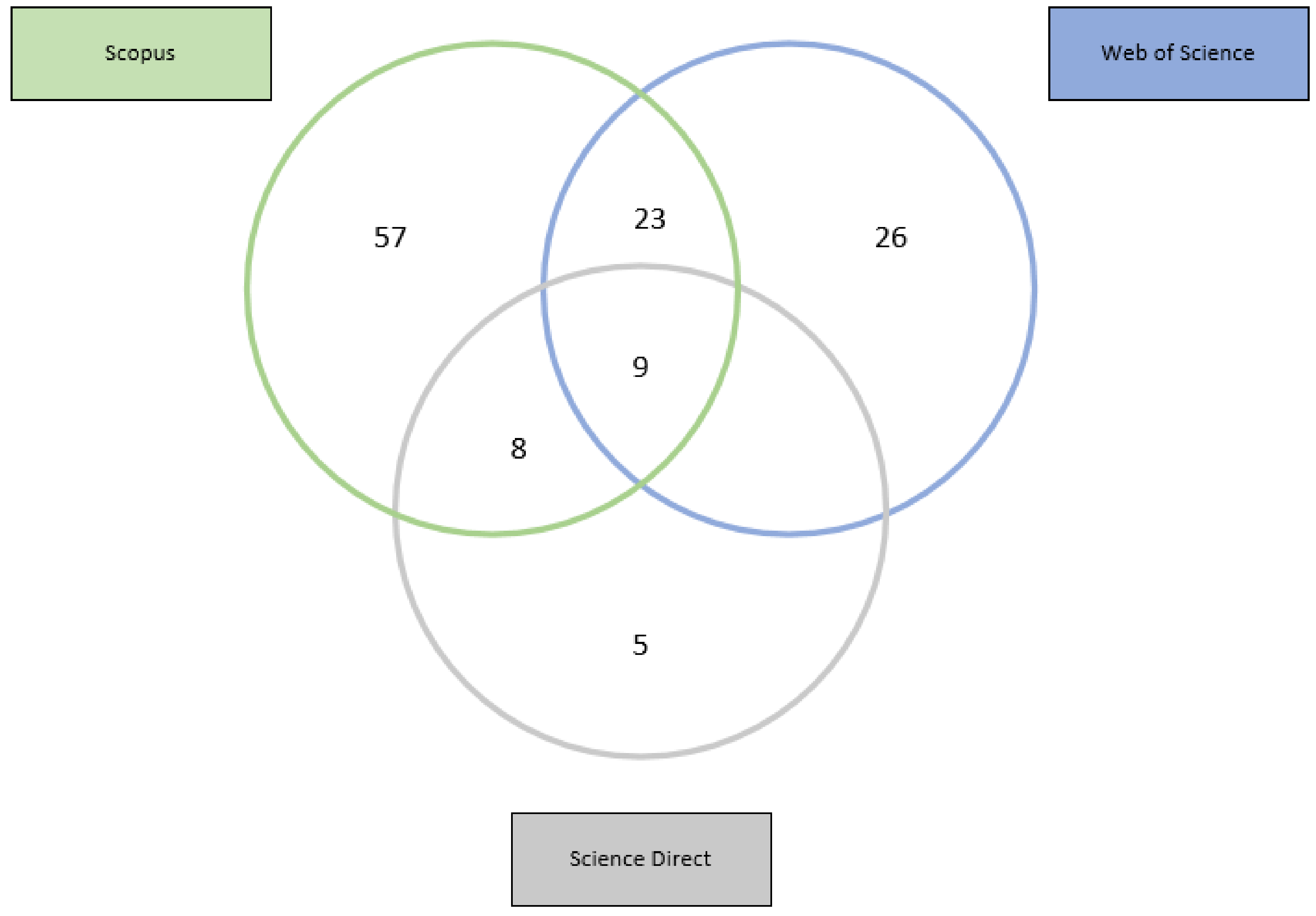

3.2. Academic Research Databases

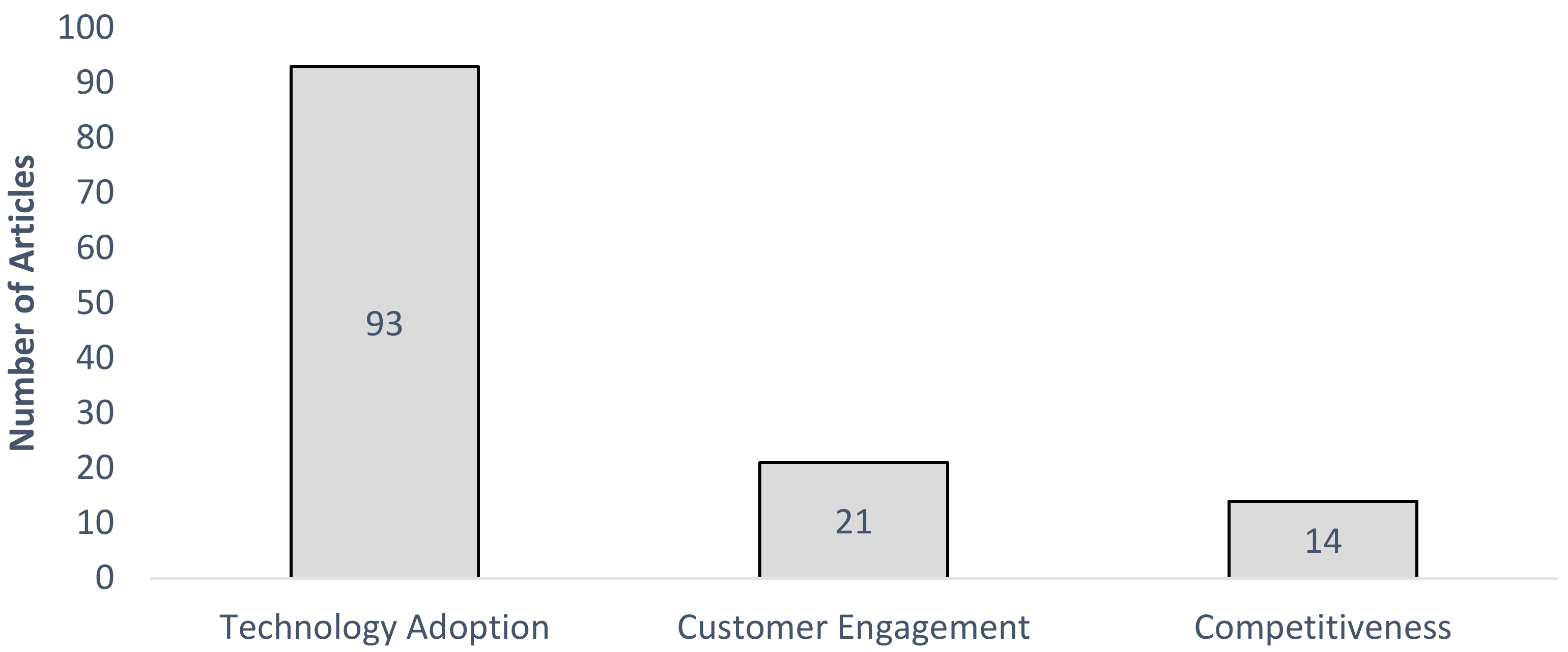

3.3. Research Topics

4. Analysis of Results

4.1. Technology Adoption

4.1.1. Intention to Use of Customers and Merchants

4.1.2. Drivers and Barriers

4.1.3. Differences in Perception of Technology

4.2. Customer Engagement

4.3. Competitiveness

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| N | Year | Authors | Article Title | Method |

|---|---|---|---|---|

| 1 | 2012 | Amoroso, D.L., Magnier-Watanabe, R. | Building a Research Model for Mobile Wallet Consumer Adoption: The Case of Mobile Suica in Japan | Case Study |

| 2 | 2013 | Ariguzo, G.C., White, D.S. | Exploring Demographic Differences in the Adoption of Mobile Money: M-PESA in Kenya | Survey |

| 3 | 2014 | Shaw, N. | The Mediating Influence of Trust in the Adoption of the Mobile Wallet | Survey, SEM |

| 4 | 2015 | Dauda, S. Y., Lee, J. | Technology Adoption: A Conjoint Analysis of Consumers’ Preference on Future Online Banking Services | Survey, Conjoint Analysis |

| 5 | 2015 | Pham, T. T. T., Ho, J. C. | The Effects of Product-Related, Personal-Related Factors and Attractiveness of Alternatives on Consumer Adoption of NFC-Based Mobile Payments | Survey, SEM |

| 6 | 2015 | Boro, K. | Prospects and Challenges of Technological Innovation in Banking Industry of North East India | Interview |

| 7 | 2016 | Madan, K., Yadav, R. | Behavioural Intention to Adopt Mobile Wallet: A Developing Country Perspective | Survey, SEM |

| 8 | 2016 | Taheam, K., Sharma, R., Goswami, S. | Drivers of Digital Wallet Usage: Implications for Leveraging Digital Marketing | Survey, SEM |

| 9 | 2017 | Campbell, D., Singh, C.B. | A Study of Customer Innovativeness for the Mobile Wallet Acceptance in Rajasthan | Survey, SEM |

| 10 | 2017 | Seetharaman, A., Kumar, K. N., Palaniappan, S., Weber, G. | Factors Influencing Behavioural Intention to Use the Mobile Wallet in Singapore | Survey, CFA |

| 11 | 2017 | Singh, N., Srivastava, S., Sinha, N. | Consumer Preference and Satisfaction of M-wallets: a Study on North Indian Consumers | Survey, Correlation and Regression Analysis |

| 12 | 2017 | Amoroso, D., Ackaradejruangsri, P. | How Consumer Attitudes Improve Repurchase Intention | Survey, SEM |

| 13 | 2017 | Shah, B., Ullatil, D.S., Nagendra, A. | Analysis of the Inception, Acceptance and Future of E-Wallets | Survey, Correlation and Regression Analysis |

| 14 | 2017 | Campbell, D., Singh, C.B. | A Study of Customer Innovativeness for the Mobile Wallet Acceptance in Rajasthan | Survey, SEM |

| 15 | 2017 | Ocak, N., Cagiltay, K. | Comparison of Cognitive Modeling and User Performance Analysis for Touch Screen Mobile Interface Design | Statistical Analysis, Video Analysis |

| 16 | 2018 | Sharma, S. K., Mangla, S. K., Luthra, S., Al-Salti, Z. | Mobile Wallet Inhibitors: Developing a Comprehensive Theory Using an Integrated Model | Interpretive Structural Modelling (ISM), fuzzy MICMAC |

| 17 | 2018 | Kumar, A., Adlakaha, A., Mukherjee, K. | The Effect of Perceived Security and Grievance Redressal on Continuance Intention to Use M-wallets in a Developing Country | Survey, SEM |

| 18 | 2018 | Alaeddin, O., Rana, A., Zainudin, Z., Kamarudin, F. | From Physical to Digital: Investigating Consumer Behaviour of Switching to Mobile Wallet | Survey, SEM |

| 19 | 2018 | Matemba, E. D., Li, G., Maiseli, B. J. | Consumers’ Stickiness to Mobile Payment Applications: An Empirical Study of WeChat Wallet | Survey, SEM |

| 20 | 2018 | Bagla, R.K., Sancheti, V. | Gaps in Customer Satisfaction with Digital Wallets: Challenge for Sustainability | Survey, Inferential Analysis |

| 21 | 2018 | Omarini, A.E. | Fintech and the Future of the Payment Landscape: The Mobile Wallet Ecosystem—A Challenge for Retail Banks? | Case Study |

| 22 | 2019 | Phutela, N., Altekar, S. | Mobile Wallets in India: A Framework for Consumer Adoption | Survey |

| 23 | 2019 | Shaw, B., Kesharwani, A. | Moderating Effect of Smartphone Addiction on Mobile Wallet Payment Adoption | Survey, SEM, Multi-group Analysis |

| 24 | 2019 | Chawla, D., Joshi, H. | Consumer Attitude and Intention to Adopt Mobile Wallet in India—An Empirical Study | Survey, SEM |

| 25 | 2019 | Sobti, N. | Impact of Demonetization on Diffusion of Mobile Payment Service in India Antecedents of Behavioral Intention and Adoption Using Extended UTAUT Model | Survey, SEM |

| 26 | 2019 | Sharma, D., Aggarwal, D., Gupta, A. | A Study of Consumer Perception Towards Mwallets | Survey, Interview, Regression Analysis |

| 27 | 2019 | Reddy, T.T., Rao, B.M. | The Moderating Effect of Gender on Continuance Intention Toward Mobile Wallet Services in India | Survey, SEM |

| 28 | 2019 | Malik, A., Suresh, S., Sharma, S. | An Empirical Study of Factors Influencing Consumers’ Attitude Towards Adoption of Wallet Apps | Survey, Correlation and Regression Analysis |

| 29 | 2019 | Vasantha, S., Sarika, P. | Empirical Analysis of Demographic Factors Affecting Intention to Use Mobile Wallet | Comparison Analysis |

| 30 | 2019 | Menon, M.M., Ramakrishnan, H.S. | Revolution of E-wallets Usage among Indian Millennial | Survey, SEM |

| 31 | 2019 | Kumar, V., Nim, N., Sharma, A. | Driving Growth of Mwallets in Emerging Markets: a Retailer’s Perspective | Qualitative Study |

| 32 | 2019 | Semerikova, E. | Payment Instruments Choice of Russian Consumers: Reasons and Pain Points | Exploratory Study |

| 33 | 2019 | Sarika, P., Vasantha, S. | Impact of Mobile Wallets on Cashless Transaction | Survey |

| 34 | 2019 | Mathiraj, S.P., Geeta, S.D.T., Saroja Devi, R. | Consumer Acuity on Select Digital Wallets | Survey, ANOVA, Hendry Garret Ranking Method |

| 35 | 2019 | Aparna, H., Karthika, S., Rajalakshmi, V.R. | A Study on the Digital Wallet Usage among Citizens of Kochi using FP-growth Algorithm | Survey, FP-Growth Algorithm |

| 36 | 2019 | Ilankumaran, G. | Payment System Indicators of Digital Banking Ecosystem in India | Trend Analysis |

| 37 | 2019 | Nair, A.K.S., Bhattacharyya, S.S. | Is Sustainability a Motive to Buy? An Exploratory Study in the Context of Mobile Applications Channel among Young Indian Consumers | Survey, CFA |

| 38 | 2019 | David, S., Kathrine, J.W. | An Investigative Report on Encryption Based Security Mechanisms for E-Wallets | Review |

| 39 | 2020 | Leong, L. Y., Hew, T. S., Ooi, K. B., Wei, J. | Predicting Mobile Wallet Resistance: A Two-Staged Structural Equation Modeling-Artificial Neural Network Approach | Survey, SEM, ANN |

| 40 | 2020 | Talwar, S., Dhir, A., Khalil, A., Mohan, G., Islam, A. N. | Point of Adoption And Beyond. Initial trust and Mobile-Payment Continuation Intention | Survey, SEM |

| 41 | 2020 | Gupta, A., Yousaf, A., Mishra, A. | How Pre-Adoption Expectancies Shape Post-Adoption Continuance Intentions: An Extended Expectation-Confirmation Model | Survey, SEM |

| 42 | 2020 | Kaur, P., Dhir, A., Bodhi, R., Singh, T., Almotairi, M. | Why do People Use and Recommend M-Wallets? | Survey, SEM |

| 43 | 2020 | Kavitha, K., Kannan, D. | Factors Influencing Consumers Attitude towards Mobile Payment Applications | Survey, SEM |

| 44 | 2020 | Chawla, D., Joshi, H. | The Moderating Role Of Gender and Age in the Adoption Of Mobile Wallet | Survey, MGA |

| 45 | 2020 | Adjei, J.K., Odei-Appiah, S., Tobbin, P.E. | Explaining the Determinants of Continual Use of Mobile Financial Services | Survey, SEM |

| 46 | 2020 | Singh, N., Sinha, N. | How Perceived Trust Mediates Merchant’s Intention to use a Mobile Wallet Technology | Survey, SEM |

| 47 | 2020 | Lew, S., Tan, G. W. H., Loh, X. M., Hew, J. J., Ooi, K. B. | The Disruptive Mobile Wallet in the Hospitality Industry: An Extended Mobile Technology Acceptance Model | Survey, SEM |

| 48 | 2020 | Mombeuil, C. | An Exploratory Investigation of Factors Affecting and Best Predicting the Renewed Adoption of Mobile Wallets | Survey, Hierarchical Ordinary Least Squares (OLS) Regression |

| 49 | 2020 | Phuong, N. N. D., Luan, L. T., Dong, V. V., Khanh, N. L. N. | Examining Customers’ Continuance Intentions towards E-wallet Usage: The Emergence of Mobile Payment Acceptance in Vietnam | Survey, SEM |

| 50 | 2020 | Soodan, V., Rana, A. | Modeling Customers’ Intention to Use E-Wallet in a Developing Nation: Extending UTAUT2 With Security, Privacy and Savings | Survey |

| 51 | 2020 | Iqbal, S., Irfan, M., Ahsan, K., Hussain, M. A., Awais, M., Shiraz, M., Hamdi, M., Alghamdi, A. | A Novel Mobile Wallet Model for Elderly Using Fingerprint as Authentication Factor | Survey, Association Analysis |

| 52 | 2020 | Grover, P., Kar, A. K. | User Engagement for Mobile Payment Service Providers—Introducing the Social Media Engagement Model | Content Analysis, Geospatial Analysis |

| 53 | 2020 | Gong, X., Cheung, C. M., Zhang, K. Z., Chen, C., Lee, M. K. | Cross-Side Network Effects, Brand Equity, and Consumer Loyalty: Evidence from Mobile Payment Market | Survey, SEM |

| 54 | 2020 | Singh, N., Sinha, N., Liébana-Cabanillas, F. J. | Determining Factors in the Adoption and Recommendation of Mobile Wallet Services in India: Analysis of the Effect of Innovativeness, Stress to Use and Social Influence | Survey, SEM |

| 55 | 2020 | Hoang, H., Le, T.T. | The Role of Promotion in Mobile Wallet Adoption—A Research in Vietnam | Survey, SEM |

| 56 | 2020 | Akanfe, O., Valecha, R., Rao, H.R. | Design of a Compliance Index for Privacy Policies: A Study of Mobile Wallet and Remittance Services | NLP, LDA |

| 57 | 2020 | Kapoor, A., Sindwani, R., Goel, M. | Mobile Wallets: Theoretical and Empirical Analysis | Fuzzy TOPSIS |

| 58 | 2020 | Akanfe, O., Valecha, R., Rao, H. R. | Assessing Country-Level Privacy Risk for Digital Payment Systems | Privacy Policy Analysis |

| 59 | 2021 | Talwar, M., Talwar, S., Kaur, P., Islam, A. N., Dhir, A. | Positive and Negative Word Of Mouth (WOM) are not Necessarily Opposites: A Reappraisal Using the Dual Factor Theory | Survey, SEM |

| 60 | 2021 | Mombeuil, C., Uhde, H. | Relative Convenience, Relative Advantage, Perceived Security, Perceived Privacy, and Continuous Use Intention of China’s WeChat Pay: A Mixed-Method Two-Phase Design Study | Survey, Hierarchical Ordinary Least Squares (OLS) Regression |

| 61 | 2021 | León, C. | The Adoption of a Mobile Payment System: The User Perspective | Network Analysis |

| 62 | 2021 | Estiyanti, N. M., Agustia, D., Mulia, R. A., Alfarisyi, R., Frandha, R., Hidayanto, A. N., Kurnia, S. | The Impact of Perceived Usability on Mobile Wallet Acceptance: A Case of Gopay Indonesia | Survey, SEM |

| 63 | 2021 | George, A., Sunny, P. | Developing a Research Model for Mobile Wallet Adoption and Usage | Hypothesis Testing |

| 64 | 2021 | Sarmah, R., Dhiman, N., Kanojia, H. | Understanding Intentions and Actual Use of Mobile Wallets By Millennial: an Extended TAM Model Perspective | Survey, SEM |

| 65 | 2021 | To, A.T., Trinh, T.H.M. | Understanding Behavioral Intention to Use Mobile Wallets in Vietnam: Extending the Tam Model with Trust and Enjoyment | Survey, SEM |

| 66 | 2021 | Singh, S., Ghatak, S. | Investigating E-Wallet Adoption in India: Extending the TAM Model | Survey, SEM |

| 67 | 2021 | Thanigan, J., Reddy, S. N., Sethuraman, P., Rajesh, J. I. | Understanding Consumer Acceptance of M-Wallet Apps: The Role of Perceived Value, Perceived Credibility, and Technology Anxiety | Survey, SEM |

| 68 | 2021 | Amoroso, D., Lim, R., Roman, F.L. | The Effect of Reciprocity on Mobile Wallet Intention: A Study of Filipino Consumers | Survey, SEM |

| 69 | 2021 | Persada, S. F., Dalimunte, I., Nadlifatin, R., Miraja, B. A., Redi, A. A. N. P., Prasetyo, Y. T., Chin, J., Lin, S. | Revealing the Behavior Intention of Tech-savvy Generation Z to Use Electronic Wallet Usage: A Theory of Planned Behavior Based Measurement | Survey, SEM |

| 70 | 2021 | Anshari, M., Arine, M. A., Nurhidayah, N., Aziyah, H., Salleh, M. H. A. | Factors Influencing Individual in Adopting Ewallet | Survey, Correlation and Regression Analysis |

| 71 | 2021 | Alswaigh, NY., Aloud, M.E. | Factors Affecting User Adoption of E-Payment Services Available in Mobile Wallets in Saudi Arabia | Survey, Correlation and Regression Analysis |

| 72 | 2021 | Chawla, D., Joshi, H. | Importance-Performance Map Analysis to Enhance the Performance of Attitude Towards Mobile Wallet Adoption among Indian Consumer Segments | Survey, SEM |

| 73 | 2021 | Wamba, S.F., Queiroz, M.M., Blome, C., Sivarajah, U. | Fostering Financial Inclusion in a Developing Country: Predicting User Acceptance of Mobile Wallets in Cameroon | Survey, SEM |

| 74 | 2021 | Hor, H. L., Wong, W. L., Ho, S. K., Tan, J. H., Teo, S. X., Foo, P. Y. | The Leading Edge of NFC Mobile Wallet Adoption: An Empirical Analysis from an Emerging Economy’s Perspective | Survey, SEM |

| 75 | 2021 | Reddy, T.T., Rao, B.M. | Determinants of Continuance Intention to Use Mobile Wallet Services: Light Users vs Heavy Users | Survey, Multivariate Data Analysis Techniques |

| 76 | 2021 | Tran Le Na, N., Hien, N. N. | A Study of User’s M-Wallet Usage Behavior: The Role of Long-Term Orientation and Perceived Value | Survey, SEM |

| 77 | 2021 | Garrouch, K. | Does the Reputation of the Provider Matter? A Model Explaining the Continuance Intention of Mobile Wallet Applications | Survey, SEM |

| 78 | 2021 | Malik, A., Sharma, S. | Antecedents of Wallet App Adoption | Weight Analysis |

| 79 | 2021 | Limantara, N., Jovandy, J., Wardhana, A.K., Steven, Jingga, F. | Evaluation of One of Leading Indonesia’s Digital Wallet Using the Unified Theory of Acceptance and Use of Technology | Survey, SEM |

| 80 | 2021 | Vidushi, V., Kashyap, R. | Reconfigure the Apparel Retail Stores with Interactive Technologies | Survey, SEM |

| 81 | 2021 | Chaddha, P., Agarwal, B., Zareen, A. | Investigating the Effect of the Credibility of Celebrity Endorsement on the Intent of Consumers to Buy Digital Wallets in India | Survey, SEM |

| 82 | 2021 | Fanuel, P.N., Fajar, A.N. | Digital Wallet War in Asia: Finding the Drivers of Digital Wallet Adoption | Survey |

| 83 | 2021 | Lui, T.K., Zainuldin, M.H., Yii, K.J., Lau, L.S., Go, Y.H. | Consumer Adoption of Alipay in Malaysia: The Mediation Effect of Perceived Ease of Use and Perceived Usefulness | Survey, SEM |

| 84 | 2021 | Aji, H.M., Adawiyah, W.R. | How E-Wallets Encourage Excessive Spending Behavior among Young Adult Consumers? | Survey, SEM |

| 85 | 2021 | Lo, K., Liu, F., Huang, J. | OneFeather Mobile Wallet: A Digital Solution for Indigenous Peoples in Canada? | Case Study |

| 86 | 2021 | Budiarani, V.H., Maulidan, R., Setianto, D.P., Widayanti, I. | The Kano Model: How the Pandemic Influences Customer Satisfaction with Digital Wallet Services in Indonesia | Kano Model, Survey, Exploratory Factor Analysis (EFA), CFA |

| 87 | 2021 | Kapoor, A., Sindwani, R., Goel, M. | Ranking Mobile Wallet Service Providers Using Fuzzy Multi-Criteria Decision-Making Approach | Fuzzy TOPSIS |

| 88 | 2021 | Nurcahyo, R., Putra, P.A. | Critical Factors in Indonesia’s E-Commerce Collaboration | AHP, TOPSIS |

| 89 | 2021 | Alam, M. M., Awawdeh, A. E., Muhamad, A. I. B. | Using E-Wallet for Business Process Development: Challenges and Prospects in Malaysia | SWOT Analysis |

| 90 | 2021 | Kumar, V., Lai, K. K., Chang, Y. H., Bhatt, P. C., Su, F. P. | A Structural Analysis Approach to Identify Technology Innovation and Evolution Path: A Case of M-Payment Technology Ecosystem | Network Establishment, Main Path Analysis |

| 91 | 2021 | Schlatt, V., Sedlmeir, J., Feulner, S., Urbach, N. | Designing a Framework for Digital KYC Processes Built on Blockchain-Based Self-Sovereign Identity | Applied DSR Process |

| 92 | 2021 | Akanfe, O., Valecha, R., Rao, H.R. | Design of an Inclusive Financial Privacy Index (INF-PIE): A Financial Privacy and Digital Financial Inclusion Perspective | LDA, PCA |

| 93 | 2021 | Hassan, M. A., Shukur, Z. | Device Identity-Based User Authentication on Electronic Payment System for Secure E-Wallet Apps. | Simulation |

| 94 | 2021 | Teng, S., Khong, K. W. | Examining Actual Consumer Usage of E-wallet: A Case Study of Big Data Analytics | Clustering, SEM |

| 95 | 2021 | Shankar, A., Behl, A. | How to Enhance Consumer Experience over Mobile Wallet: a Data-Driven Approach | Survey, Text Mining |

| 96 | 2022 | Abbasi, G.A., Sandran, T., Ganesan, Y., Iranmanesh, M. | Go Cashless! Determinants of Continuance Intention to Use E-wallet apps: A Hybrid Approach Using PLS-SEM and fsQCA | SEM, Fuzzy Set Qualitative Comparative Analysis (fsQCA) |

| 97 | 2022 | Shaw, N., Eschenbrenner, B., Brand, B. M. | Towards a Mobile App Diffusion of Innovations model: A Multinational Study of Mobile Wallet Adoption | Survey, SEM |

| 98 | 2022 | Thaker, H.M.T., Subramaniam, N.R., Qoyum, A., Hussain, H.I. | Cashless Society, E-Wallets and Continuous Adoption | Survey, SEM |

| 99 | 2022 | Chauhan, V., Yadav, R., Choudhary, V. | Adoption of Electronic Banking Services in India: an Extension of UTAUT2 model | Survey, SEM |

| 100 | 2022 | Tripathi, S.N., Srivastava, S., Vishnani, S. | Mobile Wallets: Achieving Intention to Recommend by Brick and Mortar Retailers | Reliability, Validity, and Mediation Analyses |

| 101 | 2022 | Lee, Y.Y., Gan, C.L., Liew, T.W. | Do E-wallets Trigger Impulse Purchases? An Analysis of Malaysian Gen-Y and Gen-Z Consumers | Survey, SEM |

| 102 | 2022 | Jaiswal, D., Kaushal, V., Mohan, A., Thaichon, P. | Mobile Wallets Adoption: Pre- and Post-Adoption Dynamics of Mobile Wallets Usage | Survey, Moderation and Multi-Group Analysis |

| 103 | 2022 | Ly, H.T.N., Khuong, N.V., Son, T.H. | Determinants Affect Mobile Wallet Continuous Usage in COVID 19 Pandemic: Evidence from Vietnam | Survey, SEM |

| 104 | 2022 | Sukwadi, R., Caroline, L.S., Chen, G.Y.H. | Extended Technology Acceptance Model for Indonesian Mobile Wallet: Structural Equation Modeling Approach | Survey, SEM |

| 105 | 2022 | Kumar, R., Ratra, V., Mandava, S. | Mobile Wallet Payments in the Time of COVID-19: The Indian Experience | Time-Series Technique |

| 106 | 2022 | Muhtasim, D.A., Tan, S.Y., Hassan, M.A., Pavel, M.I., Susmit, S. | Customer Satisfaction with Digital Wallet Services: An Analysis of Security Factors | Survey, Correlation and Regression Analysis |

| 107 | 2022 | Obidat, A., Almahameed, M., Alalwan, M. | An Empirical Examination of Factors Affecting the Post-Adoption Stage of Mobile Wallets by Consumers: A Perspective from a Developing Country | Survey, SEM |

| 108 | 2022 | Okonkwo, C.W., Amusa, L.B., Twinomurinzi, H., Fosso Wamba, S. | Mobile Wallets in Cash-Based Economies during COVID-19 | Survey, SEM |

| 109 | 2022 | George, A., Sunny, P. | Why do People Continue Using Mobile Wallets? An Empirical Analysis Amid COVID-19 pandemic | Survey, SEM |

| 110 | 2022 | Gupta, R.K. | Adoption of Mobile Wallet Services: An Empirical Analysis | Survey, Regression Analysis, SEM |

| 111 | 2022 | Gupta, S., Dhingra, S., Tanwar, S., Aggarwal, R. | What Explains the Adoption of Mobile Wallets? A Study from Merchants’ Perspectives | Survey, SEM |

| 112 | 2022 | Rana, N.P., Luthra, S., Rao, H.R. | Assessing Challenges to the Mobile Wallet Usage in India: An Interpretive Structural Modelling Approach | Interpretive Structural Modelling (ISM) |

| 113 | 2022 | Kavitha, R., Rajeswari, R., Mukherjee, P., Rout, S., Patra, S.S. | Performance Measures of Blockchain-Based Mobile Wallet Using Queueing Model | Queueing Model |

| 114 | 2022 | Al-Badi, A.H., Govindaluri, S.M., Sharma, S.K., Khan, A.I. | Global and Local Perspective on the Usage of Mobile Wallet | Interview, Statistics |

| 115 | 2022 | Manickam, T., Vinayagamoorthi, G., Gopalakrishnan, S., Sudha, M., Mathiraj, S.P. | Customer Inclination on Mobile Wallets with Reference to Google-Pay and PayTM in Bengaluru City | Survey, CFA |

| 116 | 2022 | Chohan, F., Aras, M., Indra, R., Wicaksono, A., Winardi, F. | Building Customer Loyalty in Digital Transaction Using QR Code: Quick Response Code Indonesian Standard (QRIS) | Survey, Statistics |

| 117 | 2022 | Astari, A.A.E., Yasa, N.N.K., Sukaatmadja, I.P.G., Giantari, I.G.A.K. | Integration of Technology Acceptance Model (TAM) and Theory of Planned Behavior (TPB): An E-Wallet Behavior with Fear of COVID-19 as a Moderator Variable | Survey, SEM |

| 118 | 2022 | Foster, B., Hurriyati, R., Johansyah, M.D. | The Effect of Product Knowledge, Perceived Benefits, and Perceptions of Risk on Indonesian Student Decisions to Use E-Wallets for Warunk Upnormal | Survey, SEM |

| 119 | 2022 | Senali, M. G., Iranmanesh, M., Ismail, F. N., Rahim, N. F. A., Khoshkam, M., Mirzaei, M. | Determinants of Intention to Use e-Wallet: Personal Innovativeness and Propensity to Trust as Moderators | Survey, SEM |

| 120 | 2022 | Nguyen, H.T., Nguyen, N.T. | Identifying the Factors Affecting the Consumer Behavior in Switching to e-wallets in Payment Activities | Survey, Correlation and Regression Analysis |

| 121 | 2022 | Soe, M.H. | Do They Really Intend to Adopt E-Wallet? Prevalence Estimates for Government Support and Perceived Susceptibility | Survey, SEM |

| 122 | 2022 | Lim, X. J., Ngew, P., Cheah, J. H., Cham, T. H., Liu, Y. | Go Digital: Can the Money-Gift Function Promote the Use of E-Wallet Apps | Survey, SEM |

| 123 | 2022 | Ojo, A.O., Fawehinmi, O., Ojo, O.T., Arasanmi, C., Tan, C.N.L. | Consumer Usage Intention of Electronic Wallets during the COVID-19 Pandemic in Malaysia | Survey, Partial Modelling Analysis |

| 124 | 202022 | Ming, K.L.Y., Jais, M. | Factors Affecting the Intention to Use E-Wallets During the COVID-19 Pandemic | Survey, SEM |

| 125 | 202022 | Al-Qudah, A. A., Al-Okaily, M., Alqudah, G., Ghazlat, A. | Mobile Payment Adoption in the Time of the COVID-19 Pandemic | Survey, SEM |

| 126 | 2022 | Shekhar, R., Jaidev, U.P. | Intention to Use Mobile Wallets: An Application of the Technology Acceptance Model | Survey, SEM |

| 127 | 2022 | Bailey, A. A., Bonifield, C. M., Arias, A., Villegas, J. | Mobile Payment Adoption in Latin America | Survey, SEM |

| 128 | 2022 | Bommer, W.H., Rana, S., Milevoj, E. | A Meta-Analysis of Ewallet Adoption Using the UTAUT Model | Meta Analysis, Relative Weight Analysis |

References

- 2030 Climate & Energy Framework. Available online: https://ec.europa.eu/clima/policies/strategies/2030_en (accessed on 8 February 2021).

- Lindgreen, E.R.; van Schendel, M.; Jonker, N.; Kloek, J.; de Graaff, L.; Davidson, M. Evaluating the environmental impact of debit card payments. Int. J. Life Cycle Assess. 2018, 23, 1847–1861. [Google Scholar] [CrossRef]

- Dhanabalan, T.; Sathish, A. Transforming Indian industries through artificial intelligence and robotics in industry 4.0. Int. J. Mech. Eng. Technol. 2018, 9, 835–845. [Google Scholar]

- Mashelkar, R.A. Exponential technology, industry 4.0 and future of jobs in India. Rev. Mark. Integr. 2018, 10, 138–157. [Google Scholar] [CrossRef]

- Shim, Y.; Shin, D.H. Analyzing China’s fintech industry from the perspective of actor–network theory. Telecommun. Policy 2016, 40, 168–181. [Google Scholar] [CrossRef]

- Brem, A.; Maier, M.; Wimschneider, C. Competitive advantage through innovation: The case of Nespresso. Eur. J. Innov. Manag. 2016, 19, 133–148. [Google Scholar] [CrossRef]

- Gozman, D.; Liebenau, J.; Mangan, J. The innovation mechanisms of fintech start-ups: Insights from SWIFT’s innotribe competition. J. Manag. Inf. Syst. 2018, 35, 145–179. [Google Scholar] [CrossRef]

- Jiao, Z.; Shahid, M.S.; Mirza, N.; Tan, Z. Should the fourth industrial revolution be widespread or confined geographically? A country-level analysis of fintech economies. Technol. Forecast. Soc. Chang. 2021, 163, 120442. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, H. Mobile banking adoption: A literature review. Telemat. Inform. 2015, 32, 129–142. [Google Scholar] [CrossRef]

- Dauda, S.Y.; Lee, J. Technology adoption: A conjoint analysis of consumers’ preference on future online banking services. Inf. Syst. 2015, 53, 1–15. [Google Scholar] [CrossRef]

- Amoroso, D.L.; Magnier-Watanabe, R. Building a research model for mobile wallet consumer adoption: The case of mobile Suica in Japan. J. Theor. Appl. Electron. Commer. Res. 2012, 7, 94–110. [Google Scholar] [CrossRef]

- Wadhera, T.; Dabas, R.; Malhotra, P. Adoption of M-wallet: A way ahead. Int. J. Eng. Manag. Res. 2017, 7, 1–7. [Google Scholar]

- Wu, H.C.; Ai, C.H.; Cheng, C.C. Experiential quality, experiential psychological states and experiential outcomes in an unmanned convenience store. J. Retail. Consum. Serv. 2019, 51, 409–420. [Google Scholar] [CrossRef]

- Leong, L.Y.; Hew, T.S.; Ooi, K.B.; Wei, J. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. Int. J. Inf. Manag. 2020, 51, 102047. [Google Scholar] [CrossRef]

- Pham, T.T.T.; Ho, J.C. The effects of product-related, personal-related factors and attractiveness of alternatives on consumer adoption of NFC-based mobile payments. Technol. Soc. 2015, 43, 159–172. [Google Scholar] [CrossRef]

- Kumar, V.; Anand, A.; Song, H. Future of retailer profitability: An organizing framework. J. Retail. 2017, 93, 96–119. [Google Scholar] [CrossRef]

- Caro, F.; Sadr, R. The Internet of Things (IoT) in retail: Bridging supply and demand. Bus. Horiz. 2019, 62, 47–54. [Google Scholar] [CrossRef]

- Ruiz-Martínez, A. Towards a web payment framework: State-of-the-art and challenges. Electron. Commer. Res. Appl. 2015, 14, 345–350. [Google Scholar] [CrossRef]

- Chopdar, P.K.; Korfiatis, N.; Sivakumar, V.J.; Lytras, M.D. Mobile shopping apps adoption and perceived risks: A cross-country perspective utilizing the Unified Theory of Acceptance and Use of Technology. Comput. Hum. Behav. 2018, 86, 109–128. [Google Scholar] [CrossRef]

- Chopdar, P.K.; Balakrishnan, J. Consumers response towards mobile commerce applications: SOR approach. Int. J. Inf. Manag. 2020, 53, 102106. [Google Scholar] [CrossRef]

- Lee, J.; Ryu, M.H.; Lee, D. A study on the reciprocal relationship between user perception and retailer perception on platform-based mobile payment service. J. Retail. Consum. Serv. 2019, 48, 7–15. [Google Scholar] [CrossRef]

- Park, J.; Ahn, J.; Thavisay, T.; Ren, T. Examining the role of anxiety and social influence in multi-benefits of mobile payment service. J. Retail. Consum. Serv. 2019, 47, 140–149. [Google Scholar] [CrossRef]

- Türkmen, C.; Değerli, A. Transformation of consumption perceptions: A Survey on innovative trends in Banking. Procedia-Soc. Behav. Sci. 2015, 195, 376–382. [Google Scholar] [CrossRef]

- Karsen, M.; Chandra, Y.U.; Juwitasary, H. Technological factors of mobile payment: A systematic literature review. Procedia Comput. Sci. 2019, 157, 489–498. [Google Scholar] [CrossRef]

- Dennehy, D.; Sammon, D. Trends in mobile payments research: A literature review. J. Innov. Manag. 2015, 3, 49–61. [Google Scholar] [CrossRef]

- Ramli, F.A.A.; Hamzah, M.I. Mobile payment and e-wallet adoption in emerging economies: A systematic literature review. J. Emerg. Econ. Islam. Res. 2021, 9, 1–39. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Bodhi, R.; Singh, T.; Almotairi, M. Why do people use and recommend m-wallets? J. Retail. Consum. Serv. 2020, 56, 102091. [Google Scholar] [CrossRef]

- Bezovski, Z. The future of the mobile payment as electronic payment system. Eur. J. Bus. Manag. 2016, 8, 127–132. [Google Scholar]

- León, C. The adoption of a mobile payment system: The user perspective. Lat. Am. J. Cent. Bank. 2021, 2, 100042. [Google Scholar] [CrossRef]

- Junadi, S. A model of factors influencing consumer’s intention to use e-payment system in Indonesia. Procedia Comput. Sci. 2015, 59, 214–220. [Google Scholar] [CrossRef]

- Sharma, S.K.; Mangla, S.K.; Luthra, S.; Al-Salti, Z. Mobile wallet inhibitors: Developing a comprehensive theory using an integrated model. J. Retail. Consum. Serv. 2018, 45, 52–63. [Google Scholar] [CrossRef]

- Slade, E.; Williams, M.; Dwivedi, Y.; Piercy, N. Exploring consumer adoption of proximity mobile payments. J. Strateg. Mark. 2015, 23, 209–223. [Google Scholar] [CrossRef]

- Malik, A.; Sharma, S. Antecedents of Wallet App Adoption. Int. J. Web-Based Learn. Teach. Technol. 2021, 16, 12–31. [Google Scholar] [CrossRef]

- Vasantha, S.; Sarika, P. Empirical analysis of demographic factors affecting intention to use mobile wallet. Int. J. Eng. Adv. Technol. 2019, 8, 768–776. [Google Scholar]

- Shekhar, R.; Jaidev, U.P. Intention to use mobile wallets: An application of the technology acceptance model. Int. J. Appl. Manag. Sci. 2022, 14, 258–280. [Google Scholar] [CrossRef]

- Ariguzo, G.C.; White, D.S. Exploring demographic differences in the adoption of mobile money: M-PESA in Kenya. Int. J. Electron. Mark. Retail. 2013, 5, 340–358. [Google Scholar] [CrossRef]

- Abbasi, G.A.; Sandran, T.; Ganesan, Y.; Iranmanesh, M. Go Cashless! Determinants of Continuance Intention to Use E-Wallet Apps: A Hybrid Approach Using PLS-SEM and fsQCA. Technol. Soc. 2022, 68, 101937. [Google Scholar] [CrossRef]

- Hor, H.L.; Wong, W.L.; Ho, S.K.; Tan, J.H.; Teo, S.X.; Foo, P.Y. The leading edge of NFC mobile wallet adoption: An empirical analysis from an emerging economy’s perspective. Int. J. Serv. Econ. Manag. 2021, 12, 228–253. [Google Scholar] [CrossRef]

- Shaw, N.; Eschenbrenner, B.; Brand, B.M. Towards a Mobile App Diffusion of Innovations model: A multinational study of mobile wallet adoption. J. Retail. Consum. Serv. 2022, 64, 102768. [Google Scholar] [CrossRef]

- Soodan, V.; Rana, A. Modeling customers’ intention to use e-wallet in a developing nation: Extending UTAUT2 with security, privacy and savings. J. Electron. Commer. Organ. 2020, 18, 89–114. [Google Scholar] [CrossRef]

- Garrouch, K. Does the reputation of the provider matter? A model explaining the continuance intention of mobile wallet applications. J. Decis. Syst. 2021, 30, 150–171. [Google Scholar] [CrossRef]

- Nguyen, H.T.; Nguyen, N.T. Identifying the Factors Affecting the Consumer Behavior in Switching to e-wallets in Payment Activities. Pol. J. Manag. Stud. 2022, 25, 292–311. [Google Scholar] [CrossRef]

- Phuong, N.N.D.; Luan, L.T.; Dong, V.V.; Khanh, N.L.N. Examining customers’ continuance intentions towards e-wallet usage: The emergence of mobile payment acceptance in Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 505–516. [Google Scholar] [CrossRef]

- Talwar, S.; Dhir, A.; Khalil, A.; Mohan, G.; Islam, A.N. Point of adoption and beyond. Initial trust and mobile-payment continuation intention. J. Retail. Consum. Serv. 2020, 55, 102086. [Google Scholar] [CrossRef]

- Gupta, A.; Yousaf, A.; Mishra, A. How pre-adoption expectancies shape post-adoption continuance intentions: An extended expectation-confirmation model. Int. J. Inf. Manag. 2020, 52, 102094. [Google Scholar] [CrossRef]

- Obidat, A.; Almahameed, M.; Alalwan, M. An empirical examination of factors affecting the post-adoption stage of mobile wallets by consumers: A perspective from a developing country. Decis. Sci. Lett. 2022, 11, 273–288. [Google Scholar] [CrossRef]

- Menon, M.M.; Ramakrishnan, H.S. Revolution of E-wallets usage among Indian millennial. Int. J. Recent Technol. Eng. 2019, 8, 8306–8312. [Google Scholar] [CrossRef]

- Shaw, B.; Kesharwani, A. Moderating effect of smartphone addiction on mobile wallet payment adoption. J. Internet Commer. 2019, 18, 291–309. [Google Scholar] [CrossRef]

- Amoroso, D.; Lim, R.; Roman, F.L. The effect of reciprocity on mobile wallet intention: A study of filipino consumers. Int. J. Asian Bus. Inf. Manag. 2021, 12, 57–83. [Google Scholar] [CrossRef]

- Singh, N.; Sinha, N. How perceived trust mediates merchant’s intention to use a mobile wallet technology. J. Retail. Consum. Serv. 2020, 52, 101894. [Google Scholar] [CrossRef]

- Gupta, S.; Dhingra, S.; Tanwar, S.; Aggarwal, R. What Explains the Adoption of Mobile Wallets? A Study from Merchants’ Perspectives. Int. J. Hum.–Comput. Interact. 2022, 38, 1–13. [Google Scholar] [CrossRef]

- Shaw, N. The mediating influence of trust in the adoption of the mobile wallet. J. Retail. Consum. Serv. 2014, 21, 449–459. [Google Scholar] [CrossRef]

- Tripathi, S.N.; Srivastava, S.; Vishnani, S. Mobile wallets: Achieving intention to recommend by brick and mortar retailers. J. Mark. Theory Pract. 2022, 30, 240–256. [Google Scholar] [CrossRef]

- Shah, B.; Ullatil, D.S.; Nagendra, A. Analysis of the inception, acceptance and future of e-wallets. Int. J. Appl. Bus. Econ. Res. 2017, 15, 207–215. [Google Scholar]

- Gupta, R.K. Adoption of mobile wallet services: An empirical analysis. Int. J. Intellect. Prop. Manag. 2022, 12, 341–353. [Google Scholar] [CrossRef]

- Mombeuil, C.; Uhde, H. Relative convenience, relative advantage, perceived security, perceived privacy, and continuous use intention of China’s WeChat Pay: A mixed-method two-phase design study. J. Retail. Consum. Serv. 2021, 59, 102384. [Google Scholar] [CrossRef]

- Mombeuil, C. An exploratory investigation of factors affecting and best predicting the renewed adoption of mobile wallets. J. Retail. Consum. Serv. 2020, 55, 102127. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Consumer attitude and intention to adopt mobile wallet in India–An empirical study. Int. J. Bank Mark. 2019, 37, 1590–1618. [Google Scholar] [CrossRef]

- Talwar, M.; Talwar, S.; Kaur, P.; Islam, A.N.; Dhir, A. Positive and negative word of mouth (WOM) are not necessarily opposites: A reappraisal using the dual factor theory. J. Retail. Consum. Serv. 2021, 63, 102396. [Google Scholar] [CrossRef]

- Singh, N.; Sinha, N.; Liébana-Cabanillas, F.J. Determining factors in the adoption and recommendation of mobile wallet services in India: Analysis of the effect of innovativeness, stress to use and social influence. Int. J. Inf. Manag. 2020, 50, 191–205. [Google Scholar] [CrossRef]

- Hassan, M.A.; Shukur, Z. Device Identity-Based User Authentication on Electronic Payment System for Secure E-Wallet Apps. Electronics 2021, 11, 4. [Google Scholar] [CrossRef]

- Schlatt, V.; Sedlmeir, J.; Feulner, S.; Urbach, N. Designing a framework for digital KYC processes built on blockchain-based self-sovereign identity. Inf. Manag. 2021, 59, 103553. [Google Scholar] [CrossRef]

- Muhtasim, D.A.; Tan, S.Y.; Hassan, M.A.; Pavel, M.I.; Susmit, S. Customer Satisfaction with Digital Wallet Services: An Analysis of Security Factors. Int. J. Adv. Comput. Sci. Appl. 2022, 13, 195–206. [Google Scholar] [CrossRef]

- David, S.; Kathrine, J.W. An investigative report on encryption based security mechanisms for e-wallets. J. Sci. Technol. Res. 2019, 8, 1755–1769. [Google Scholar]

- Kavitha, R.; Rajeswari, R.; Mukherjee, P.; Rout, S.; Patra, S.S. Performance Measures of Blockchain-Based Mobile Wallet Using Queueing Model. Intell. Syst. Sustain. Comput. 2022, 289, 269–277. [Google Scholar]

- Akanfe, O.; Valecha, R.; Rao, H.R. Assessing country-level privacy risk for digital payment systems. Comput. Secur. 2020, 99, 102065. [Google Scholar] [CrossRef]

- Akanfe, O.; Valecha, R.; Rao, H.R. Design of a Compliance Index for Privacy Policies: A Study of Mobile Wallet and Remittance Services. IEEE Trans. Eng. Manag. 2020, 67, 1–13. [Google Scholar] [CrossRef]

- Iqbal, S.; Irfan, M.; Ahsan, K.; Hussain, M.A.; Awais, M.; Shiraz, M.; Hamdi, M.; Alghamdi, A. A novel mobile wallet model for elderly using fingerprint as authentication factor. IEEE Access 2020, 8, 177405–177423. [Google Scholar] [CrossRef]

- Akanfe, O.; Valecha, R.; Rao, H.R. Design of an inclusive financial privacy index (INF-PIE): A financial privacy and digital financial inclusion perspective. ACM Trans. Manag. Inf. Syst. 2020, 12, 1–21. [Google Scholar] [CrossRef]

- Lew, S.; Tan, G.W.H.; Loh, X.M.; Hew, J.J.; Ooi, K.B. The disruptive mobile wallet in the hospitality industry: An extended mobile technology acceptance model. Technol. Soc. 2020, 63, 101430. [Google Scholar] [CrossRef]

- Campbell, D.; Singh, C.B. A study of customer innovativeness for the mobile wallet acceptance in Rajasthan. Pac. Bus. Rev. Int. 2017, 10, 7–15. [Google Scholar]

- Madan, K.; Yadav, R. Behavioural intention to adopt mobile wallet: A developing country perspective. J. Indian Bus. Res. 2016, 8, 227–244. [Google Scholar] [CrossRef]

- Amoroso, D.; Ackaradejruangsri, P. How consumer attitudes improve repurchase intention. Int. J. E-Serv. Mob. Appl. 2017, 9, 38–61. [Google Scholar] [CrossRef]

- Senali, M.G.; Iranmanesh, M.; Ismail, F.N.; Rahim, N.F.A.; Khoshkam, M.; Mirzaei, M. Determinants of Intention to Use e-Wallet: Personal Innovativeness and Propensity to Trust as Moderators. Int. J. Hum. –Comput. Interact. 2022, 38, 1–13. [Google Scholar] [CrossRef]

- Adjei, J.K.; Odei-Appiah, S.; Tobbin, P.E. Explaining the Determinants of Continual Use of Mobile Financial Services. Digit. Policy Regul. Gov. 2020, 22, 15–31. [Google Scholar] [CrossRef]

- Chaddha, P.; Agarwal, B.; Zareen, A. Investigating the effect of the credibility of celebrity endorsement on the intent of consumers to buy digital wallets in India. Indian J. Econ. Bus. 2021, 20, 63–79. [Google Scholar]

- Vidushi, V.; Kashyap, R. Reconfigure the apparel retail stores with interactive technologies. Res. J. Text. Appar. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Phutela, N.; Altekar, S. Mobile wallets in India: A framework for consumer adoption. Int. J. Online Mark. 2019, 9, 27–38. [Google Scholar] [CrossRef]

- Estiyanti, N.M.; Agustia, D.; Mulia, R.A.; Alfarisyi, R.; Frandha, R.; Hidayanto, A.N.; Kurnia, S. The impact of perceived usability on mobile wallet acceptance: A case of Gopay Indonesia. Int. J. Innov. Learn. 2021, 30, 154–174. [Google Scholar] [CrossRef]

- To, A.T.; Trinh, T.H.M. Understanding behavioral intention to use mobile wallets in vietnam: Extending the tam model with trust and enjoyment. Cogent Bus. Manag. 2021, 8, 1891661. [Google Scholar] [CrossRef]

- George, A.; Sunny, P. Developing a research model for mobile wallet adoption and usage. IIM Kozhikode Soc. Manag. Rev. 2021, 10, 82–98. [Google Scholar] [CrossRef]

- Seetharaman, A.; Kumar, K.N.; Palaniappan, S.; Weber, G. Factors influencing behavioural intention to use the mobile wallet in Singapore. J. Appl. Econ. Bus. Res. 2017, 7, 116–136. [Google Scholar]

- Singh, N.; Srivastava, S.; Sinha, N. Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. Int. J. Bank Mark. 2017, 35, 944–965. [Google Scholar] [CrossRef]

- Chauhan, V.; Yadav, R.; Choudhary, V. Adoption of electronic banking services in India: An extension of UTAUT2 model. J. Financ. Serv. Mark. 2022, 27, 27–40. [Google Scholar] [CrossRef]

- Alaeddin, O.; Rana, A.; Zainudin, Z.; Kamarudin, F. From physical to digital: Investigating consumer behaviour of switching to mobile wallet. Pol. J. Manag. Stud. 2018, 17, 18–30. [Google Scholar] [CrossRef]

- Anshari, M.; Arine, M.A.; Nurhidayah, N.; Aziyah, H.; Salleh, M.H.A. Factors influencing individual in adopting eWallet. J. Financ. Serv. Mark. 2021, 26, 10–23. [Google Scholar] [CrossRef]

- Soe, M.H. Do They Really Intend to Adopt E-Wallet? Prevalence Estimates for Government Support and Perceived Susceptibility. Asian J. Bus. Res. 2022, 12, 77–98. [Google Scholar]

- Singh, S.; Ghatak, S. Investigating E-Wallet adoption in India: Extending the TAM model. Int. J. E-Bus. Res. 2021, 17, 42–54. [Google Scholar] [CrossRef]

- Persada, S.F.; Dalimunte, I.; Nadlifatin, R.; Miraja, B.A.; Redi, A.A.N.P.; Prasetyo, Y.T.; Chin, J.; Lin, S.C. Revealing the behavior intention of tech-savvy generation Z to use electronic wallet usage: A theory of planned behavior based measurement. Int. J. Bus. Soc. 2021, 22, 213–226. [Google Scholar] [CrossRef]

- Thanigan, J.; Reddy, S.N.; Sethuraman, P.; Rajesh, J.I. Understanding Consumer Acceptance of M-Wallet Apps: The Role of Perceived Value, Perceived Credibility, and Technology Anxiety. J. Electron. Commer. Organ. 2021, 19, 65–91. [Google Scholar] [CrossRef]

- Bommer, W.H.; Rana, S.; Milevoj, E. A meta-analysis of eWallet adoption using the UTAUT model. Int. J. Bank Mark. 2022, 40, 791–819. [Google Scholar] [CrossRef]

- Bailey, A.A.; Bonifield, C.M.; Arias, A.; Villegas, J. Mobile payment adoption in Latin America. J. Serv. Mark. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Sobti, N. Impact of demonetization on diffusion of mobile payment service in India: Antecedents of behavioral intention and adoption using extended UTAUT model. J. Adv. Manag. Res. 2019, 16, 472–497. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Importance-performance map analysis to enhance the performance of attitude towards mobile wallet adoption among Indian consumer segments. Aslib J. Inf. Manag. 2021, 73, 946–966. [Google Scholar] [CrossRef]

- Wamba, S.F.; Queiroz, M.M.; Blome, C.; Sivarajah, U. Fostering financial inclusion in a developing country: Predicting user acceptance of mobile wallets in Cameroon. J. Glob. Inf. Manag. 2021, 29, 195–220. [Google Scholar] [CrossRef]

- Sukwadi, R.; Caroline, L.S.; Chen, G.Y.H. Extended technology acceptance model for Indonesian mobile wallet: Structural equation modeling approach. Eng. Appl. Sci. Res. 2022, 49, 146–154. [Google Scholar]

- Limantara, N.; Jovandy, J.; Wardhana, A.K.; Steven, S.; Jingga, F. Evaluation of one of leading Indonesia’s digital wallet using the unified theory of acceptance and use of technology. Indones. J. Electr. Eng. Comput. Sci. 2021, 24, 1036–1046. [Google Scholar] [CrossRef]

- Lee, Y.Y.; Gan, C.L.; Liew, T.W. Do E-wallets trigger impulse purchases? An analysis of Malaysian Gen-Y and Gen-Z consumers. J. Mark. Anal. 2022, 10, 1–18. [Google Scholar] [CrossRef]

- Sarmah, R.; Dhiman, N.; Kanojia, H. Understanding intentions and actual use of mobile wallets by millennial: An extended TAM model perspective. J. Indian Bus. Res. 2021, 13, 361–381. [Google Scholar] [CrossRef]

- Kumar, A.; Adlakaha, A.; Mukherjee, K. The effect of perceived security and grievance redressal on continuance intention to use M-wallets in a developing country. Int. J. Bank Mark. 2018, 36, 1170–1189. [Google Scholar] [CrossRef]

- Taheam, K.; Sharma, R.; Goswami, S. Drivers of digital wallet usage: Implications for leveraging digital marketing. Int. J. Econ. Res. 2016, 13, 175–186. [Google Scholar]

- Alswaigh, N.Y.; Aloud, M.E. Factors Affecting User Adoption of E-Payment Services Available in Mobile Wallets in Saudi Arabia. Int. J. Comput. Sci. Netw. Secur. 2021, 21, 222–230. [Google Scholar]

- Ly, H.T.N.; Khuong, N.V.; Son, T.H. Determinants Affect Mobile Wallet Continuous Usage in COVID 19 Pandemic: Evidence from Vietnam. Cogent Bus. Manag. 2022, 9, 2041792. [Google Scholar] [CrossRef]

- Al-Qudah, A.A.; Al-Okaily, M.; Alqudah, G.; Ghazlat, A. Mobile payment adoption in the time of the COVID-19 pandemic. Electron. Commer. Res. 2022, 22, 1–25. [Google Scholar] [CrossRef]

- Ming, K.L.Y.; Jais, M. Factors affecting the intention to use e-wallets during the COVID-19 pandemic. Gadjah Mada Int. J. Bus. 2022, 24, 82–100. [Google Scholar] [CrossRef]

- Astari, A.; Yasa, N.; Sukaatmadja, I.; Giantari, I. Integration of technology acceptance model (TAM) and theory of planned behavior (TPB): An e-wallet behavior with fear of COVID-19 as a moderator variable. Int. J. Data Netw. Sci. 2022, 6, 1427–1436. [Google Scholar] [CrossRef]

- Ojo, A.O.; Fawehinmi, O.; Ojo, O.T.; Arasanmi, C.; Tan, C.N.L. Consumer usage intention of electronic wallets during the COVID-19 pandemic in Malaysia. Cogent Bus. Manag. 2022, 9, 2056964. [Google Scholar] [CrossRef]

- Jaiswal, D.; Kaushal, V.; Mohan, A.; Thaichon, P. Mobile wallets adoption: Pre-and post-adoption dynamics of mobile wallets usage. Mark. Intell. Plan. 2022, 40, 573–588. [Google Scholar] [CrossRef]

- Thaker, M.T.H.; Subramaniam, N.R.; Qoyum, A.; Iqbal Hussain, H. Cashless society, e-wallets and continuous adoption. Int. J. Financ. Econ. 2022, 27, 1–21. [Google Scholar]

- Lui, T.K.; Zainuldin, M.H.; Yii, K.J.; Lau, L.S.; Go, Y.H. Consumer Adoption of Alipay in Malaysia: The Mediation Effect of Perceived Ease of Use and Perceived Usefulness. Pertanika J. Soc. Sci. Humanit. 2021, 29, 389–418. [Google Scholar] [CrossRef]

- Reddy, T.T.; Rao, B.M. Determinants of Continuance Intention to Use Mobile Wallet Services: Light Users vs Heavy Users. Indian J. Mark. 2021, 51, 29–42. [Google Scholar] [CrossRef]

- Tran Le Na, N.; Hien, N.N. A study of user’s m-wallet usage behavior: The role of long-term orientation and perceived value. Cogent Bus. Manag. 2021, 8, 1899468. [Google Scholar] [CrossRef]

- Fanuel, P.N.; Fajar, A.N. Digital wallet war in Asia: Finding the drivers of digital wallet adoption. J. Paym. Strategy Syst. 2021, 15, 79–91. [Google Scholar]

- Chawla, D.; Joshi, H. The moderating role of gender and age in the adoption of mobile wallet. Foresight 2020, 22, 483–504. [Google Scholar] [CrossRef]

- Reddy, T.T.; Rao, B.M. The moderating effect of gender on continuance intention toward mobile wallet services in India. Indian J. Mark. 2019, 49, 48–62. [Google Scholar] [CrossRef]

- Sharma, D.; Aggarwal, D.; Gupta, A. A study of consumer perception towards mwallets. Int. J. Sci. Technol. 2019, 8, 3892–3895. [Google Scholar]

- Malik, A.; Suresh, S.; Sharma, S. An empirical study of factors influencing consumers’ attitude towards adoption of wallet apps. Int. J. Manag. Pract. 2019, 12, 426–442. [Google Scholar] [CrossRef]

- Kavitha, K.; Kannan, D.D. Factors Influencing Consumers Attitude Towards Mobile Payment Applications. Int. J. Manag. 2020, 11, 140–150. [Google Scholar]

- Kumar, V.; Nim, N.; Sharma, A. Driving growth of Mwallets in emerging markets: A retailer’s perspective. J. Acad. Mark. Sci. 2019, 47, 747–769. [Google Scholar] [CrossRef]

- Shankar, A.; Behl, A. How to enhance consumer experience over mobile wallet: A data-driven approach. J. Strateg. Mark. 2021, 29, 1–18. [Google Scholar] [CrossRef]

- Ocak, N.; Cagiltay, K. Comparison of cognitive modeling and user performance analysis for touch screen mobile interface design. Int. J. Hum. –Comput. Interact. 2017, 33, 633–641. [Google Scholar] [CrossRef]

- Gong, X.; Cheung, C.M.; Zhang, K.Z.; Chen, C.; Lee, M.K. Cross-side network effects, brand equity, and consumer loyalty: Evidence from mobile payment market. Int. J. Electron. Commer. 2020, 24, 279–304. [Google Scholar] [CrossRef]

- Manickam, T.; Vinayagamoorthi, G.; Gopalakrishnan, S.; Sudha, M.; Mathiraj, S.P. Customer Inclination on Mobile Wallets with Reference to Google-Pay and PayTM in Bengaluru City. Int. J. E-Bus. Res. 2022, 18, 1–16. [Google Scholar] [CrossRef]

- Matemba, E.D.; Li, G.; Maiseli, B.J. Consumers’ stickiness to mobile payment applications: An empirical study of WeChat wallet. In Research Anthology on Social Media Advertising and Building Consumer Relationships; Information Resources Management Association, IGI Global: Hershey, PA, USA, 2022; pp. 731–756. [Google Scholar]

- Chohan, F.; Aras, M.; Indra, R.; Wicaksono, A.; Winardi, F. Building Customer Loyalty in Digital Transaction Using QR Code: Quick Response Code Indonesian Standard (QRIS). J. Distrib. Sci. 2022, 20, 1–11. [Google Scholar]

- Aparna, H.; Karthika, S.; Rajalakshmi, V.R. A study on the digital wallet usage among citizens of Kochi using FP-growth algorithm. Int. J. Recent Technol. Eng. 2019, 7, 1315–1322. [Google Scholar]

- Semerikova, E. Payment instruments choice of Russian consumers: Reasons and pain points. J. Enterprising Communities People Places Glob. Econ. 2019, 14, 22–41. [Google Scholar] [CrossRef]

- Lo, K.; Liu, F.; Huang, J. OneFeather Mobile Wallet: A Digital Solution for Indigenous Peoples in Canada? Account. Perspect. 2021, 20, 403–419. [Google Scholar] [CrossRef]

- Mathiraj, S.P.; Geeta, S.D.T.; Devi, R.S. Consumer acuity on select digital wallets. Int. J. Sci. Technol. Res. 2019, 8, 3551–3556. [Google Scholar]

- Budiarani, V.H.; Maulidan, R.; Setianto, D.P.; Widayanti, I. The kano model: How the pandemic influences customer satisfaction with digital wallet services in Indonesia. J. Indones. Econ. Bus. 2021, 36, 62–82. [Google Scholar] [CrossRef]

- Foster, B.; Hurriyati, R.; Johansyah, M.D. The Effect of Product Knowledge, Perceived Benefits, and Perceptions of Risk on Indonesian Student Decisions to Use E-Wallets for Warunk Upnormal. Sustainability 2022, 14, 6475. [Google Scholar] [CrossRef]

- George, A.; Sunny, P. Why do people continue using mobile wallets? An empirical analysis amid COVID-19 pandemic. J. Financ. Serv. Mark. 2022, 27, 1–15. [Google Scholar] [CrossRef]

- Okonkwo, C.W.; Amusa, L.B.; Twinomurinzi, H.; Wamba, S.F. Mobile wallets in cash-based economies during COVID-19. Ind. Manag. Data Syst. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Grover, P.; Kar, A.K.; Ilavarasan, P.V. Understanding nature of social media usage by mobile wallets service providers–an exploration through SPIN framework. Procedia Comput. Sci. 2017, 122, 292–299. [Google Scholar] [CrossRef]

- Hoang, H.; Le, T.T. The Role of Promotion in Mobile Wallet Adoption–A Research in Vietnam. Adv. Sci. Technol. Eng. Syst. 2020, 5, 290–298. [Google Scholar] [CrossRef]

- Grover, P.; Kar, A.K. User engagement for mobile payment service providers–introducing the social media engagement model. J. Retail. Consum. Serv. 2020, 53, 101718. [Google Scholar] [CrossRef]

- Lim, X.J.; Ngew, P.; Cheah, J.H.; Cham, T.H.; Liu, Y. Go digital: Can the money-gift function promote the use of e-wallet apps? Internet Res. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Teng, S.; Khong, K.W. Examining actual consumer usage of E-wallet: A case study of big data analytics. Comput. Hum. Behav. 2021, 121, 106778. [Google Scholar] [CrossRef]

- Aji, H.M.; Adawiyah, W.R. How E-Wallets Encourage Excessive Spending Behavior among Young Adult Consumers? J. Asia Bus. Stud. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Kapoor, A.; Sindwani, R.; Goel, M. Mobile wallets: Theoretical and empirical analysis. Glob. Bus. Rev. 2020, 21, 0972150920961254. [Google Scholar] [CrossRef]

- Kapoor, A.; Sindwani, R.; Goel, M. Ranking Mobile Wallet Service Providers Using Fuzzy Multi-Criteria Decision-Making Approach. Int. J. E-Bus. Res. 2021, 17, 19–39. [Google Scholar] [CrossRef]

- Ilankumaran, G. Payment System Indicators of Digital Banking Ecosystem in India. Clearing 2019, 1273, 114. [Google Scholar]

- Kumar, R.; Ratra, V.; Mandava, S. Mobile wallet payments in the time of COVID-19: The Indian experience. J. Paym. Strategy Syst. 2022, 16, 7–16. [Google Scholar]

- Nair, A.K.; Bhattacharyya, S.S. Is sustainability a motive to buy? An exploratory study in the context of mobile applications channel among young Indian consumers. Foresight 2018, 21, 177–199. [Google Scholar] [CrossRef]

- Al-Badi, A.H.; Govindaluri, S.M.; Sharma, S.K.; Khan, A.I. Global and local perspective on the usage of mobile wallet. Int. J. Bus. Inf. Syst. 2022, 39, 550–568. [Google Scholar]

- Bagla, R.K.; Sancheti, V. Gaps in customer satisfaction with digital wallets: Challenge for sustainability. J. Manag. Dev. 2018, 37, 442–451. [Google Scholar] [CrossRef]

- Rana, N.P.; Luthra, S.; Rao, H.R. Assessing challenges to the mobile wallet usage in India: An interpretive structural modelling approach. Inf. Technol. People 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Kumar, V.; Lai, K.K.; Chang, Y.H.; Bhatt, P.C.; Su, F.P. A structural analysis approach to identify technology innovation and evolution path: A case of m-payment technology ecosystem. J. Knowl. Manag. 2020, 25, 477–499. [Google Scholar] [CrossRef]

- Alam, M.M.; Awawdeh, A.E.; Muhamad, A.I.B. Using e-wallet for business process development: Challenges and prospects in Malaysia. Bus. Process Manag. J. 2021, 27, 1142–1162. [Google Scholar] [CrossRef]

- Sarika, P.; Vasantha, S. Impact of mobile wallets on cashless transaction. Int. J. Recent Technol. Eng. 2019, 7, 1164–1171. [Google Scholar]

- Yang, M.; Mamun, A.A.; Mohiuddin, M.; Nawi, N.C.; Zainol, N.R. Cashless transactions: A study on intention and adoption of e-wallets. Sustainability 2021, 13, 831. [Google Scholar] [CrossRef]

- Nurcahyo, R.; Putra, P.A. Critical factors in indonesia’s e-commerce collaboration. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 2458–2469. [Google Scholar] [CrossRef]

- Boro, K. Prospects and challenges of technological innovation in banking industry of North East India. J. Internet Bank. Commer. 2015, 20, 1–18. [Google Scholar] [CrossRef]

- Omarini, A.E. Fintech and the future of the payment landscape: The mobile wallet ecosystem. A challenge for retail banks? Int. J. Financ. Res. 2018, 9, 97–116. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hopalı, E.; Vayvay, Ö.; Kalender, Z.T.; Turhan, D.; Aysuna, C. How Do Mobile Wallets Improve Sustainability in Payment Services? A Comprehensive Literature Review. Sustainability 2022, 14, 16541. https://doi.org/10.3390/su142416541

Hopalı E, Vayvay Ö, Kalender ZT, Turhan D, Aysuna C. How Do Mobile Wallets Improve Sustainability in Payment Services? A Comprehensive Literature Review. Sustainability. 2022; 14(24):16541. https://doi.org/10.3390/su142416541

Chicago/Turabian StyleHopalı, Egemen, Özalp Vayvay, Zeynep Tuğçe Kalender, Deniz Turhan, and Ceyda Aysuna. 2022. "How Do Mobile Wallets Improve Sustainability in Payment Services? A Comprehensive Literature Review" Sustainability 14, no. 24: 16541. https://doi.org/10.3390/su142416541

APA StyleHopalı, E., Vayvay, Ö., Kalender, Z. T., Turhan, D., & Aysuna, C. (2022). How Do Mobile Wallets Improve Sustainability in Payment Services? A Comprehensive Literature Review. Sustainability, 14(24), 16541. https://doi.org/10.3390/su142416541