Corporate Social Responsibility of Chinese Multinational Enterprises: A Review and Future Research Agenda

Abstract

1. Introduction

2. Literature Review Methodology

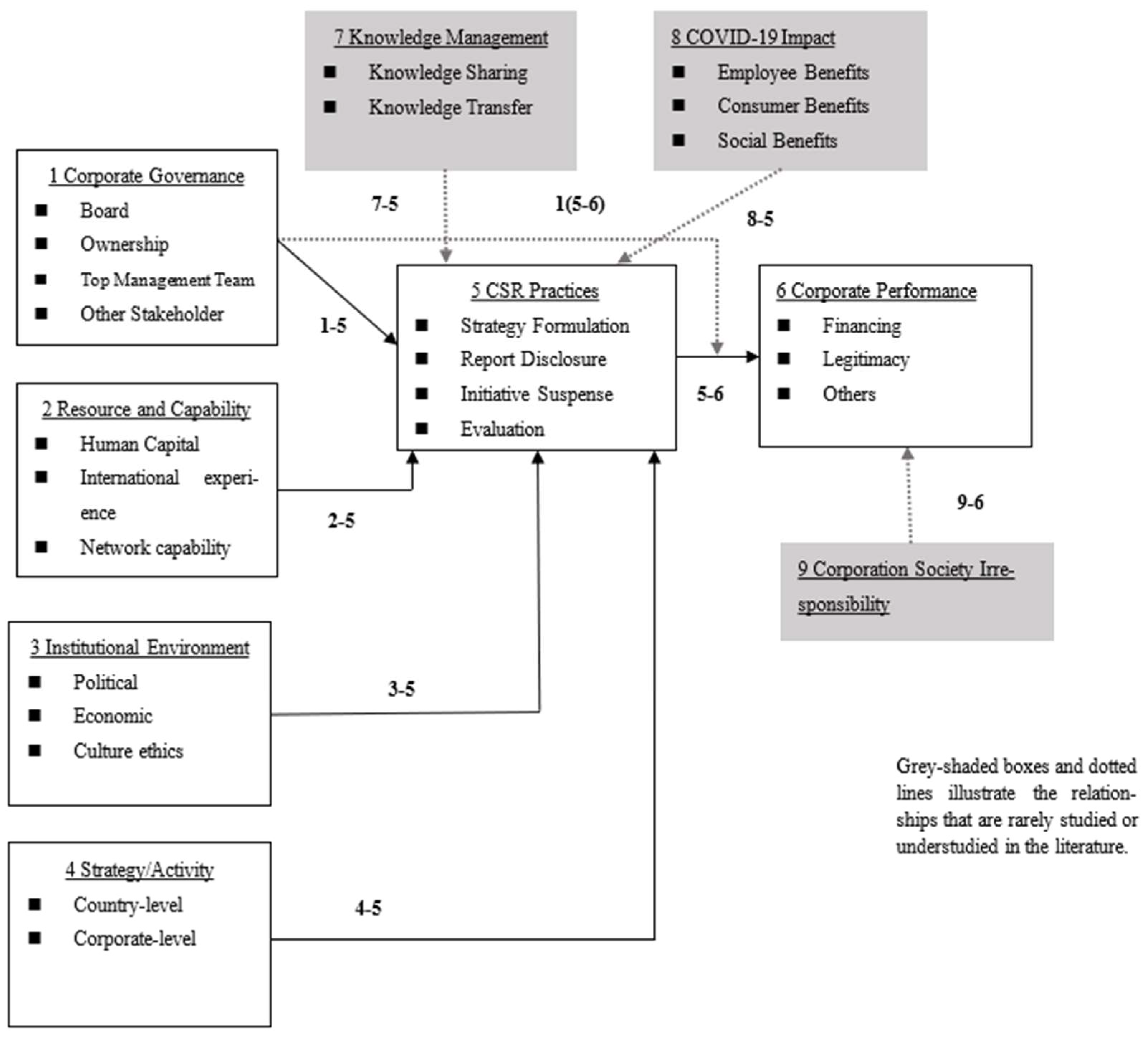

3. Research on the CMNEs’ CSR

3.1. The Relationship between Corporation Governance and CSR Practices

{kind=link}

| Authors | Year | Theory | Concepts | Findings |

|---|---|---|---|---|

| Lau et al. [11] | 2016 | Institutional theory, Agency theory, Upper echelons theory | CSR disclosures, CSR strategies | Compared to TMT, board may have a more active and effective elicit CMNE’s CSR to serve the performance of public |

| Khalid et al. [35] | 2021 | Legitimacy theory Stakeholder Theory | Environmental CSR, Globalization of CSR | Chinese non-state-owned MNEs outperform their peers on environmental and governance performance. |

| Wang et al. [31] | 2015 | Upper echelons theory | CSR donation | Pressure from stakeholders influences the perception of corporate charitable giving management decisions |

| Zamir1 and Saeed [41] | 2020 | Legitimacy theory and institutional theory | CSR disclosures, CSR reporting | MNEs close to financial centers exhibit more CSR disclosure. |

| Liao et al. [36] | 2018 | Resource dependence theory, agency theory, and critical mass theory | CSR assurance | MNEs with larger boards, more women directors can devote more energy and resources. |

| Fu et al. [39] | 2020 | Upper echelons theory | CSR Commitment | The presence of a chief sustainability officer (CSO) increases CSR activities and reduces corporate social irresponsibility activities (CSIR) |

3.2. The Relationship between Institutional Environment and CSR Practices

| Authors | Year | Theory | Concepts | Findings |

|---|---|---|---|---|

| Marquis et al. [33] | 2017 | Stakeholder theory | CSR diffuses, CSR reporting | The political mechanisms of state-mediated globalization allow corporations to adopt and adapt global normative practices while meeting the political legitimacy needs of key stakeholders. |

| LI and LU [53] | 2020 | Institutional theory | CSR reporting, external-oriented | Corporations are more likely to increase CSR when public agents are more motivated to seek promotion to the central government, or when private agents are more concerned with legitimacy. |

| Du et al. [52] | 2016 | Legitimacy theory | Rankins CSR Ratings | Religious climate plays an important role in strengthening CSR and has a substitute role with law enforcement. |

| Yin and Zhang [42] | 2012 | Grounded theory-building | CSR diffuses, Corporate philanthropy | Institutional infrastructure and cultural ethics have a continuing impact on the approach to CSR in emerging economies |

| Liu et al. [14] | 2021 | Upper echelons theory and stakeholder theory, | CSR strategies | Entrepreneurs with higher social status in China are more inclined to CSR efforts. |

| Hah and Freeman [6] | 2014 | Stakeholder theory and institutional theory | Corporate ethics, CSR security | MNEs are pressured by host country constituencies to engage in CSR activities when the ethical standards of the host and home countries differ. |

3.3. The Relationship between CSR Practice and Corporate Performance

| Authors | Year | Theory | Concepts | Findings |

|---|---|---|---|---|

| Wang et al. [58] | 2011 | Portfolio theory Stakeholder theory | Rankins CSR Ratings | Too low or too high CSR performance may lead to adverse reactions from investors. |

| Huang et al. [47] | 2022 | Signaling theory Stakeholder theory | CSR disclosure | CSR performance is associated with access to bank credit facilities, and this positive relationship is more pronounced in long-term loans |

| Zhang et al. [62] | 2010 | Agency theory | Corporate philanthropy | Advertising intensity is positively correlated with the category of CSR |

| Gong et al. [56] | 2021 | Information asymmetry theory | CSR reporting | Conducting CSR activities can partially offset CMNE’s negative impact on the cost of debt due to corporate law violations. |

| Zhao [49] | 2012 | Grounded theory | CSR initiatives legitimacy | MNEs may regard CSR as an extension of their efforts to seek legitimacy in the state. |

| Zhang et al. [64] | 2020 | Institutional theory | CSR legitimacy | Conformity in CSR legitimizes enterprises in the analyst group and positively affects analyst coverage. |

| Ye and Zhang [65] | 2011 | Risk mitigation theory | CSR reporting Corporate philanthropy | The u-shaped relationship between CSR and the cost of debt financing in China in the context of emerging markets. |

| Liu et al. [53] | 2015 | stakeholder theory. | CSR suspension | Suspension of CSR can harm stakeholder relationships and threaten the survival of the business. |

3.4. The Relationship between Strategy/Activity and CSR Practice

| Authors | Year | Theory | Concepts | Findings |

|---|---|---|---|---|

| Yang et al. [5] | 2020 | Institutional theory | CSR strategies | The positive impact of Belt and Road on the CSR performance of MNEs is stronger in host countries with higher levels of institutional pressure |

| Zhang and Luo [66] | 2013 | Agency theory and institutional theory | Self-Presentation of CSR, CSR donation, and corporate philanthropy | CSR increase the importance of external social forces that motivate MNEs to act. |

| Zeng et al. [68] | 2013 | Institutional theory | CSR reporting, Environmental CSR | Conducting marketing activities contribute to building CSR legitimacy |

3.5. The Relationship between Resource/Capacity and CSR Practice

| Authors | Year | Theory | Concepts | Findings |

|---|---|---|---|---|

| Li et al. [15] | 2022 | Legitimacy theory Stakeholder theory Resource-based view | CSR disclosures | Director network centrality has a significant positive effect on the quality of CSR disclosure, especially when the board devotes less to advertising |

| Ma et al. [69] | 2020 | Upper echelons theory | CSR disclosure | Executives with academic backgrounds are more willing to provide stakeholders with more CSR disclosure information |

| Cui et al. [55] | 2015 | Stakeholder theory | CSR Commitment | The relationship between private MNE commitment to CSR and average sales growth in the weak institutional environment |

4. Results

5. Suggestions for Future Research Directions

5.1. Developing CSR Theory on Chinese MNEs

5.2. The Relationship between Corporate Governance and CSR in CME

5.3. CMNEs’ Corporation Society Irresponsibility

5.4. Impact of COVID-19 on CSR of Chinese MNEs

5.5. Methodological Approaches

Author Contributions

Funding

Informed Consent Statement

Conflicts of Interest

Appendix A

| Authors | Year | Sample Period | Theory leans | Focus | Findings |

|---|---|---|---|---|---|

| Luo et al. [80] | 2017 | 2008–2011 | Organizational theory | 3–5 | CSR reporting is seen as an organizational response to the institutional complications resulting from conflicting requirements of central and local government |

| LI and LU [45] | 2020 | Not specified | Institutional theory | 3–5 | Corporations are more likely to increase CSR when public agents are more motivated to seek promotion to central government. |

| Zhu et al. [54] | 2014 | Not specified | Stakeholder theory | 2–5 | There is a positive relationship between ethical leadership and CSR. |

| Du et al. [52] | 2016 | 2007–2009 | Legitimacy theory | 3–5 | Religious climate plays an important role in strengthening CSR and has a substitute role with law enforcement. |

| Zamir and Saeed [41] | 2020 | 2010 to 2015 | Legitimacy theory Institutional theory | 3–5 | Corporations faced institutional pressures depending on location, with those close to financial centers more legally committed to CSR disclosure. |

| Shen et al. [81] | 2020 | 2012 | Institutional perspective | 2–5 | Investing in CSR can help corporations create value from intangible assets. |

| Yang et. al [5] | 2020 | Not specified | Institutional theory | 4–5 | The positive impact of Belt and Road on the CSR performance of MNEs is stronger in host countries with higher levels of institutional pressure |

| Ding et al. [82] | 2022 | 2008–2015 | Institutional theory Strategic view | 1–5 | Board interlocking causes an integration in the CSR structure of the interlocked companies, increasing the probability that CSR activities will be implemented, which facilitates CSR discussion. |

| Zhang et al. [64] | 2020 | 2008–2014 | Institutional theory | 5–6 | Conformity in CSR legitimizes enterprises in the analyst group and positively affects analyst coverage. |

| Miska et al. [43] | 2016 | 2012 | Institutional theory | 3–5 | States effect Chinese MNEs’ global CSR integration and local CSR responsiveness strategies. |

| Zhou and Wang [83] | 2020 | 2009–2016 | Reputation risk view | 3–5 | The positive relationship between parent company reputation risk and CSR activities of foreign subsidiaries is impacted by differences in institutional context between host and home countries. |

| Wang, et al. [31] | 2015 | Not specified | Stakeholder theory and upper echelons theory | 1–5 | Personal values and perceptions of the CEO’s attitudes toward philanthropy can influence corporate charitable donation decisions. |

| Li et al. [15] | 2022 | 2010–2018 | Legitimacy theory Stakeholder theory Resource-based view | 2–5 | Director network centrality has a significant positive effect on the quality of CSR disclosure, especially when the board devotes less to advertising. |

| Moon J, Shen [84] | 2010 | 1993–2007 | Not specified | 3–5 | The focus of CSR in Chinese enterprises has evolved from ethical issues to social, environmental and stakeholder focus. |

| Li and Zhang, [21] | 2010 | 2008 | Type II agency problem | 1–5 | Dispersion of corporate ownership mitigates the risk of minority shareholders’ self-interest. For non-SOEs, the dispersion of corporate ownership is positively related to CSR |

| Xu and Yang [18] | 2010 | 2006 | Not specified | 3–5 | CSR dimensions of Chinese enterprises are strongly linked to their socio-cultural background and are different from those of Western countries. |

| Wang et al. [58] | 2011 | 2007–2008 | Portfolio theory and stakeholder theory | 5–6 | Avoid investing too little or too much in CSR may mitigate adverse investor reactions resulting in low financial performance |

| Ye and Zhang [65] | 2011 | 2007–2008 | Risk mitigation theory | 5–6 | The u-shaped relationship between CSR and the cost of debt financing in China in the context of emerging markets |

| Liu et al. [53] | 2015 | 2009–2011 | Stakeholder theory. | 5–6 | Suspension of CSR can harm stakeholder relationships and threaten the survival of the business. |

| Yin and Zhang [42] | 2012 | 2009 | Grounded-theory-building | 3–5 | Institutional infrastructure and cultural ethical factors have a strong relationship with the CSR performance of Chinese corporations. |

| Hah and Freeman [6] | 2014 | Not specified | Stakeholder theory and institutional theory | 3–5 | MNE subsidiaries respond to pressures from host countries by adopting globally integrated or locally responsive (or a combination of both) CSR strategies. |

| Cumming et al. [85] | 2016 | 1982–2014 | Not specified | 5 | Trust and fraud issues related to CSR are a rising concern for Chinese enterprises. |

| Lau et al. [11] | 2016 | 2010–2011 | Stakeholder theory Agency theory | 1–5 | The concentration of shareholding can reduce the diversity of CSR activities. Compared to the TMT, the board may have a more active and effective elicit CMNE’s CSR to serve the performance of the public. |

| Wang and Li [86] | 2016 | 2007–2012. | Stakeholder theory. | 5–6 | The market valuations of CSR initiators dominated by central and local governments are lesser than those of non- initiators and those owned by private shareholders. |

| Liao et al. [36] | 2018 | 2008–2012 | Resource dependence theory Agency theory Critical mass theory | 1–5 | Corporations with larger boards, more female directors, and separate CEO and board positions can dedicate more effort and resources and are more prone to CSR assurance |

| Gong et al. [87] | 2018 | 2010–2013 | Information theory | 5–6 3–5 | The stronger the negative relationship between the quality of CSR disclosure and the cost of corporate bonds when corporations are located in areas with weak corporate governance and institutional environments |

| Ma and Bu [16] | 2021 | Not specified | Not specified | 5 | In order to explore CSR performance in CMNES`, contextualized CSR theories need to be developed by combining Chinese social contexts. |

| Gong et al. [56] | 2021 | 2011–2017 | Information asymmetry theory | 5–6 | Conducting CSR activities can partially offset CMNE’s negative impact on the cost of debt due to corporate law violations. |

| Liu et al. [14] | 2021 | 2000–2012 | Upper echelons theory Stakeholder theory Social stratification view | 3–5 | Enterprises make strategic CSR decisions to satisfy their stakeholders (employees, environmental agencies, and communities). Entrepreneurs with higher social status and stronger political ties are more inclined to commit to CSR. |

| Tsoi [88] | 2010 | 2004–2005 | Stakeholder theory | 5–6 | Local and regional stakeholders believe that CSR is important to primarily export-oriented businesses. |

| Zheng et al. [38] | 2015 | 2006–2008 | Stakeholder theory Institutional theory | 5–6 | Corporations can pursue stakeholder legitimacy through strategies of passive conformity and intentional adaptation to stakeholder CSR requirement. |

| Sun et al. [48] | 2015 | 2006-2011 | Institutional theory | 3–5 | If banks in communities where more companies report CSR or where there are principles encouraging CSR practices, they are more probable to be early adopters of CSR reporting. |

| Cui et al. [55] | 2015 | 2008 | Stakeholder theory | 5–6 | The relationship between privately-owned enterprises’ commitment to CSR and average sales growth is related to the size of the enterprise. |

| Han and Zheng [89] | 2016 | 2004–2005 | Organizational theory | 1–5 | the imprinting effects of a company’s founding ownership on labor and environmental protections, two critical CSR practices. |

| Ge, and Zhao [44] | 2017 | 2006 | Organizational theory Institutional theory | 3–5 | The choice of external or internal CSR practices is related to how strongly the enterprise is linked to the state system. |

| Marquis and Qian [73] | 2014 | 2009–2013 | Stakeholder theory | 3–5 | The political mechanisms of state-mediated globalization allow corporations to adopt and adapt global normative practices while meeting the political legitimacy needs of key stakeholders. |

| Ma et al. [69] | 2020 | 2008–2014 | Upper echelons theory | 2–5 | Executives with academic backgrounds are more willing to provide stakeholders with more CSR disclosure information. |

| Li et al. [90] | 2010 | Not specified | Institutional theory | 1–5 | Corporations with a high percentage of outside directors tend to have stronger corporate governance and more CSR. |

| Zeng et al. [68] | 2013 | 2010–2011 | Institutional theory | 4–5,5–6 | Social marketing activities that contribute to the legitimacy of CSR and positive corporate performance. |

| Marquis et al. [33] | 2017 | 2009–2013 | Stakeholder theory | 1–5 | The Chinese government, as a stakeholder, can guide enterprises in employing and adapting global CSR practices. |

| Cheng et al. [91] | 2014 | Not specified | Agency theory Stakeholder theory | 5–6 | Transparency in CSR performance is essential to reducing capital constraints. |

| Flammer [92] | 2015 | 1972–2005 | Neoclassical trade theory Stakeholder theory | 4–5 | Trade liberalization is an important factor in shaping CSR practices. |

| Duanmu, et al. [59] | 2018 | 2000–2005 | Institutional theory | 5 | It should be considered prudent to invest in CSR strategies as a competitive approach, due to enterprises are unable to avoid competition by environmental differentiation. |

| Fu et al. [39] | 2020 | 2005–2014 | Upper echelons theory | 1–5 | The presence of a chief sustainability officer (CSO) increases CSR activities and reduces corporate social irresponsibility activities (CSIR) |

| Gatignon [63] | 2022 | Not specified | Human capital management perspective | 5–6 | boundary-spanning CSR program and nonprofit peer mission-dependent employee identity pressure can be reduced by developing a sense of CSR among employees. |

| Doh et al. [93] | 2013 | Not specified | Stakeholder theory Institutional theory | 3–5 5–6 | Under the influence of institutional hollowness and duality, DMNEs use CSR as a signaling mechanism to obtain legitimacy and a “license to operate” in developed countries. |

| Huang et al. [47] | 2022 | 2009–2016, | Signaling theory | 5–6 | CSR performance is related to access to bank credit, and this positive relationship is more significant for long-term loans than for short-term loans. |

| Tian et al. [94] | 2011 | 2009 | Information Theory | 5–6 | Corporations that sell experiential products (as opposed to seek-and-trust products) are more likely to obtain positive consumer evaluate with products and purchase by CSR practices |

| Luger et al. [95] | 2022 | Not specified | Cross-cultural perspective | 3–5 | consumer attitudes toward CSR in advanced European markets and emerging Asian markets and confirms that consumers’ attitudes toward CSR support influence their purchasing behavior. |

| Zhang et al. [62] | 2010 | 2008 | Agency theory | 5–6 | Advertising intensity is positively correlated with the category of CSR |

| Zhao [49] | 2012 | 2009 | Grounded-theory- | 5–6 | MNE may regard CSR as an extension of their efforts to seek legitimacy in the state |

| Wei et al. [96] | 2017 | Not specified | Signaling theory Institutional theory | 5–6 | Environmental Corporate social responsibility can impact business and political legitimacy, as well as corporate performance. |

| Wang et al. [31] | 2015 | Not specified | Upper echelons theory | 1–5 | Pressure from stakeholders influences the perception of corporate charitable giving management decisions |

| Zamir1 and Saeed [41] | 2020 | 2010–2015. | Legitimacy theory and institutional theory | 1–5 | MNE close to financial centers exhibit more CSR disclosure. |

| Zhang and Luo [66] | 2013 | 2008 | Agency theory and institutional theory | 4–5 | CSR increase the importance of external social forces that motivate MNE to act. |

References

- Ma, Z. The status of contemporary business ethics research: Present and future. J. Bus. Ethics 2009, 90, 255–265. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Friedman, M.A. Friedman doctrine: The social responsibility of business is to increase its profits. N.Y. Times Mag. 1970, 13, 32–33. [Google Scholar]

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations. Acad. Manag. Rev. 2007, 32, 836–863. [Google Scholar] [CrossRef]

- Yang, N.; Wang, J.; Liu, X.; Huang, L. Home-country institutions and corporate social responsibility of emerging economy multinational enterprises: The belt and road initiative as an example. Asia Pac. J. Manag. 2020, 39, 927–965. [Google Scholar] [CrossRef]

- Hah, K.; Freeman, S. Multinational enterprise subsidiaries and their CSR: A conceptual framework of the management of CSR in smaller emerging economies. J. Bus. Ethics 2014, 122, 125–136. [Google Scholar] [CrossRef]

- Cui, X.J. A study on using foreign investment to accelerate the construction of innovative countries under the current situation. Int. Econ. Coop. 2017, 9, 23–27. [Google Scholar]

- Campbell, J.T.; Eden, L.; Miller, S.R. Multinationals and corporate social responsibility in host countries: Does distance matter. J. Int. Bus. Stud. 2012, 43, 84–106. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Corporate social responsibility in the multinational enterprise: Strategic and institutional approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef]

- Muller, A. Global versus local CSR strategies. Eur. Manag. J. 2006, 24, 189–198. [Google Scholar] [CrossRef]

- Lau, C.M.; Lu, Y.; Liang, Q. Corporate social responsibility in China: A corporate governance approach. J. Bus. Ethics 2016, 136, 73–87. [Google Scholar] [CrossRef]

- Snyder, H. Literature review as a research methodology: An overview and guidelines. J. Bus. Res. 2019, 104, 333–339. [Google Scholar] [CrossRef]

- Garriga, E.; Mele, D. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Liu, Y.; Dai, W.; Liao, M.; Wei, J. Social status and corporate social responsibility: Evidence from Chinese privately owned firms. J. Bus. Ethics 2021, 169, 651–672. [Google Scholar] [CrossRef]

- Li, W.; Zhang, J.Z.; Ding, R. Impact of Directors’ Network on Corporate Social Responsibility Disclosure: Evidence from China. J. Bus. Ethics 2022, 1–33. [Google Scholar] [CrossRef]

- Ma, Z.; Bu, M. A new research horizon for mass entrepreneurship policy and Chinese firms’ CSR: Introduction to the thematic symposium. J. Bus. Ethics 2021, 169, 603–607. [Google Scholar] [CrossRef]

- Cui, X.J. The conceptual framework of social responsibility of multinational corporations. World Econ. Stud. 2007, 4, 64–68. [Google Scholar]

- Ye, S.; Yang, R. Indigenous characteristics of Chinese corporate social responsibility conceptual paradigm. J. Bus. Ethics 2010, 93, 321–333. [Google Scholar]

- Ministry of Commence of The People’s Republic of China. 2022 January-May China’s Foreign Direct Investment in the Whole Industry Concise Statistics. Available online: http://www.mofcom.gov.cn/article/tongjiziliao/dgzz/202206/20220603322653.shtml (accessed on 28 June 2022).

- Fortune China. Fortune 500 List for 2022. Available online: http://www.fortunechina.com/fortune500/c/2022-08/03/content_415683.htm (accessed on 3 August 2022).

- Li, W.; Zhang, R. Corporate social responsibility, ownership structure, and political interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Li, X.; Zhou, Y.M. Offshoring pollution while offshoring production? Strateg. Manag. J. 2017, 38, 2310–2329. [Google Scholar] [CrossRef]

- Xiao, Y.; Watson, M. Guidance on conducting a systematic literature review. J. Plan. Educ. Res. 2019, 39, 93–112. [Google Scholar] [CrossRef]

- Pisani, N.; Kourula, A.; Kolk, A.; Meijer, R. How global is international CSR research? Insights and recommendations from a systematic review. J. World Bus. 2017, 52, 591–614. [Google Scholar] [CrossRef]

- Rodriguez, P.; Siegel, D.S.; Hillman, A.; Eden, L. Three lenses on the multinational enterprise: Politics, corruption, and corporate social responsibility. J. Int. Bus. Stud. 2006, 37, 733–746. [Google Scholar] [CrossRef]

- Torraco, R.J. Writing integrative literature reviews: Guidelines and examples. Hum. Resour. Dev. Rev. 2005, 4, 356–367. [Google Scholar] [CrossRef]

- Colli, A.; Colpan, A.M. Business groups and corporate governance: Review, synthesis, and extension. Corp. Gov. Int. Rev. 2016, 24, 274–302. [Google Scholar] [CrossRef]

- Holmes, R.M., Jr.; Hoskisson, R.E.; Kim, H.; Wan, W.P.; Holcomb, T.R. International strategy and business groups: A review and future research agenda. J. World Bus. 2018, 53, 134–150. [Google Scholar] [CrossRef]

- Gallo, M.A. The Family Business and Its Social Responsibilities. Fam. Bus. Rev. 2014, 17, 135–148. [Google Scholar] [CrossRef]

- Meyer, K.E.; Li, C.; Schotter, A.P.J. Managing the MNE subsidiary: Advancing a multi-level and dynamic research agenda. J. Int. Bus Stud. 2020, 51, 538–576. [Google Scholar]

- Wang, S.; Gao, Y.; Hodgkinson, G.P.; Rousseau, D.M.; Flood, P.C. Opening the black box of CSR decision making: A policy-capturing study of charitable donation decisions in China. J. Bus. Ethics 2015, 128, 665–683. [Google Scholar] [CrossRef]

- Gulzar, M.A.; Cherian, J.; Hwang, J.; Jiang, Y.; Sial, M.S. The impact of board gender diversity and foreign institutional investors on the corporate social responsibility (CSR) engagement of Chinese listed companies. Sustainability 2019, 11, 307. [Google Scholar] [CrossRef]

- Marquis, C.; Yin, J.; Yang, D. State-mediated globalization processes and the adoption of corporate social responsibility reporting in China. Manag. Organ. Rev. 2017, 13, 167–191. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, P.; Kwon, J. CSR in China: Does being close to the central or local government matter? Sustainability 2021, 13, 8770. [Google Scholar] [CrossRef]

- Khalid, F.; Sun, J.; Huang, G.; Su, C.Y. Environmental, social and governance performance of Chinese multinationals: A comparison of state-and non-state-owned enterprises. Sustainability 2021, 13, 4020. [Google Scholar] [CrossRef]

- Liao, L.; Lin, T.P.; Zhang, Y. Corporate board and corporate social responsibility assurance: Evidence from China. J. Bus. Ethics. 2018, 150, 211–225. [Google Scholar] [CrossRef]

- Hillman, A.; Cannella, A.; Paetzold, R. The resource dependence role of corporate directors: Strategic adaptation of board composition in response to environmental change. J. Manag. Stud. 2000, 37, 213–255. [Google Scholar] [CrossRef]

- Zheng, Q.; Luo, Y.; Maksimov, V. Achieving legitimacy through corporate social responsibility: The case of emerging economy firms. J. World Bus. 2015, 50, 389–403. [Google Scholar] [CrossRef]

- Fu, R.; Tang, Y.; Chen, G. Chief sustainability officers, and corporate social (Ir) responsibility. Strateg. Manag. J. 2020, 41, 656–680. [Google Scholar] [CrossRef]

- Frynas, J.G. Corporate social responsibility and societal governance: Lessons from transparency in the oil and gas sector. J. Bus. Ethics 2010, 93, 163–179. [Google Scholar] [CrossRef]

- Zamir, F.; Saeed, A. Location matters: Impact of geographical proximity to financial centers on corporate social responsibility (CSR) disclosure in emerging economies. Asia Pac. J. Manag. 2020, 37, 263–295. [Google Scholar] [CrossRef]

- Yin, J.; Zhang, Y. Institutional dynamics and corporate social responsibility (CSR) in an emerging country context: Evidence from China. J. Bus. Ethics 2012, 111, 301–316. [Google Scholar] [CrossRef]

- Miska, C.; Witt, M.A.; Stahl, G.K. Drivers of global CSR integration and local CSR responsiveness: Evidence from Chinese MNEs. Bus. Ethics Q. 2016, 26, 317–345. [Google Scholar] [CrossRef]

- Ge, J.; Zhao, W. Institutional linkages with the state and organizational practices in corporate social responsibility: Evidence from China. Manag. Organ. Rev. 2017, 13, 539–573. [Google Scholar] [CrossRef]

- Li, S.; Lu, J.W. A dual-agency model of firm CSR in response to institutional pressure: Evidence from Chinese publicly listed firms. Acad. Manag. J. 2020, 63, 2004–2032. [Google Scholar] [CrossRef]

- Wei, Z.; Wu, S.; Li, C.; Chen, W. Family control, institutional environment and cash dividend policy: Evidence from China. China J. Account. Res. 2011, 4, 29–46. [Google Scholar] [CrossRef]

- Huang, G.; Ye, F.; Li, Y.; Chen, L.; Zhang, M. Corporate social responsibility and bank credit loans: Exploring the moderating effect of the institutional environment in China. Asia Pac. J. Manag. 2022, 1–36. [Google Scholar] [CrossRef]

- Sun, J.; Wang, F.; Wang, F.; Yin, H. Community institutions and initial diffusion of corporate social responsibility practices in China’s banking industry. Manag. Organ. Rev. 2015, 11, 441–468. [Google Scholar] [CrossRef]

- Zhao, M. CSR-based political legitimacy strategy: Managing the state by doing good in China and Russia. J. Bus. Ethics 2012, 111, 439–460. [Google Scholar] [CrossRef]

- Freeman, S.; Edwards, R.; Schroder, B. How smaller born-global firms use networks and alliances to overcome constraints to rapid internationalization. J. Int. Mark. 2006, 14, 33–63. [Google Scholar] [CrossRef]

- Cruz, L.B.; Boehe, D.M. How do leading retail MNCs leverage CSR globally? Insights from Brazil. J. Bus. Ethics 2010, 91, 243–263. [Google Scholar] [CrossRef]

- Du, X.; Du, Y.; Zeng, Q.; Pei, H.; Chang, Y. Religious atmosphere, law enforcement, and corporate social responsibility: Evidence from China. Asia Pac. J. Manag. 2016, 33, 229–265. [Google Scholar] [CrossRef]

- Liu, Y.; Feng, T.; Li, S. Stakeholder influences and organization responses: A case study of corporate social responsibility suspension. Manag. Organ. Rev. 2015, 11, 469–491. [Google Scholar] [CrossRef]

- Zhu, Y.; Sun, L.Y.; Leung, A.S.M. Corporate social responsibility, firm reputation, and firm performance: The role of ethical leadership. Asia Pac. J. Manag. 2014, 31, 925–947. [Google Scholar] [CrossRef]

- Cui, Z.; Liang, X.; Lu, X. Prize or price? Corporate social responsibility commitment and sales performance in the Chinese private sector. Manag. Organ. Rev. 2015, 11, 25–44. [Google Scholar] [CrossRef]

- Gong, G.; Huang, X.; Wu, S.; Tian, H.; Li, W. Punishment by securities regulators, corporate social responsibility and the cost of debt. J. Bus. Ethics 2021, 171, 337–356. [Google Scholar] [CrossRef]

- Cheung, Y.L.; Tan, W.; Ahn, H.J.; Zhang, Z. Does corporate social responsibility matter in Asian emerging markets? J. Bus. Ethics 2010, 92, 401–413. [Google Scholar] [CrossRef]

- Wang, M.; Qiu, C.; Kong, D. Corporate social responsibility, investor behaviors, and stock market returns: Evidence from a natural experiment in China. J. Bus. Ethics 2011, 101, 127–141. [Google Scholar] [CrossRef]

- Duanmu, J.L.; Bu, M.; Pittman, R. Does market competition dampen environmental performance? Evidence from China. Strateg. Manag. J. 2018, 39, 3006–3030. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Alford, R.R.; Friedland, R. Powers of Theory: Capitalism, the State, and Democracy; Cambridge University Press: New York, NY, USA, 1985; pp. 11–75. ISBN 0-521-31635-9. [Google Scholar]

- Zhang, R.; Zhu, J.; Yue, H.; Zhu, C. Corporate philanthropic giving, advertising intensity, and industry competition level. J. Bus. Ethics 2010, 94, 39–52. [Google Scholar] [CrossRef]

- Gatignon, A. The double-edged sword of boundary-spanning Corporate Social Responsibility programs. Strateg. Manag. J. 2022, 43, 2156–2184. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, H.; Zhou, X. Dare to be different? Conformity versus differentiation in corporate social activities of Chinese firms and market responses. Acad. Manag. J. 2020, 63, 717–742. [Google Scholar] [CrossRef]

- Ye, K.; Zhang, R. Do lenders value corporate social responsibility? Evidence from China. J. Bus. Ethics 2011, 104, 197–206. [Google Scholar] [CrossRef]

- Zhang, J.; Luo, X.R. Dared to care: Organizational vulnerability, institutional logics, and MNCs’ social responsiveness in emerging markets. Organ. Sci. 2013, 24, 1742–1764. [Google Scholar] [CrossRef]

- Zhang, Q.; de Vries, A. Seeking Moral Legitimacy through Corporate Social Responsibility: Evidence from Chinese Manufacturing Multinationals. Sustainability 2022, 14, 5245. [Google Scholar] [CrossRef]

- Zeng, F.; Li, J.; Zhu, H.; Cai, Z.; Li, P. How international firms conduct societal marketing in emerging markets. Manag. Int. Rev. 2013, 53, 841–868. [Google Scholar] [CrossRef]

- Ma, Z.; Zhang, H.; Zhong, W.; Zhou, K. Top management teams’ academic experience and firms’ corporate social responsibility voluntary disclosure. Manag. Organ. Rev. 2020, 16, 293–333. [Google Scholar] [CrossRef]

- Juergensen, J.J.; Narula, R.; Surdu, I. A systematic review of the relationship between international diversification and innovation: A firm-level perspective. Int. Bus. Rev. 2021, 31, 101955. [Google Scholar] [CrossRef]

- Michailova, S.; Fee, A.; DeNisi, A. Research on host-country nationals in multinational enterprises: The last five decades and ways forward. J. World Bus. 2022, 58, 101383. [Google Scholar] [CrossRef]

- Ponomareva, Y.; Uman, T.; Bodolica, V.; Wennberg, K. Cultural diversity in top management teams: Review and agenda for future research. J. World Bus. 2022, 57, 101328. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Luo, J.; Kaul, A.; Seo, H. Winning us with trifes: Adverse selection in the use of philanthropy as insurance. Strateg. Manag. J. 2018, 39, 2591–2617. [Google Scholar] [CrossRef]

- Kotchen, M.; Moon, J.J. Corporate social responsibility for irresponsibility. BE J. Econ. Anal. Policy 2012, 12. [Google Scholar] [CrossRef]

- Strike, V.M.; Gao, J.; Bansal, P. Being good while being bad: Social responsibility and the international diversification of US firms. J. Int. Bus. Stud. 2006, 37, 850–862. [Google Scholar] [CrossRef]

- Cui, X.J.; Peng, X.H. New trends in the corporate social responsibility of multinational companies under the impact of COVID-19. Int. Trade 2020, 9, 14–21. [Google Scholar]

- Huang, Y.J. Technological progress under open conditions—From technology introduction to independent innovation. World Econ. Stud. 2008, 6, 14–18+37+86. [Google Scholar]

- Tsui, A.S. Contributing to Global Management Knowledge: A Case for High Quality Indigenous Research’. Asia Pac. J. Manag. 2004, 21, 491–513. [Google Scholar] [CrossRef]

- Luo, X.R.; Wang, D.; Zhang, J. Whose call to answer: Institutional complexity and firms’ CSR reporting. Acad. Manag. J. 2017, 60, 321–344. [Google Scholar] [CrossRef]

- Shen, N.; Au, K.; Li, W. Strategic alignment of intangible assets: The role of corporate social responsibility. Asia Pac. J. Manag. 2020, 37, 1119–1139. [Google Scholar] [CrossRef]

- Ding, H.; Hu, Y.; Yang, X.; Zhou, X. Board interlock and the diffusion of corporate social responsibility among Chinese listed firms. Asia Pac. J. Manag. 2022, 39, 1287–1320. [Google Scholar] [CrossRef]

- Zhou, N.; Wang, H. Foreign subsidiary CSR as a buffer against parent firm reputation risk. J. Int. Bus. Stud. 2020, 51, 1256–1282. [Google Scholar] [CrossRef]

- Moon, J.; Shen, X. CSR in China research: Salience, focus and nature. J. Bus. Ethics 2010, 94, 613–629. [Google Scholar] [CrossRef]

- Cumming, D.; Hou, W.; Lee, E. Business ethics and finance in greater China: Synthesis and future directions in sustainability, CSR, and fraud. J. Bus. Ethics 2016, 138, 601–626. [Google Scholar] [CrossRef]

- Wang, K.T.; Li, D. Market reactions to the first-time disclosure of corporate social responsibility reports: Evidence from China. J. Bus. Ethics 2016, 138, 661–682. [Google Scholar] [CrossRef]

- Gong, G.; Xu, S.; Gong, X. On the value of corporate social responsibility disclosure: An empirical investigation of corporate bond issues in China. J. Bus. Ethics 2018, 150, 227–258. [Google Scholar] [CrossRef]

- Tsoi, J. Stakeholders’ perceptions and future scenarios to improve corporate social responsibility in Hong Kong and Mainland China. J. Bus. Ethics 2010, 91, 391–404. [Google Scholar] [CrossRef]

- Han, Y.; Zheng, E. Why firms perform differently in corporate social responsibility? Firm ownership and the persistence of organizational imprints. Manag. Organ. Rev. 2016, 12, 605–629. [Google Scholar] [CrossRef]

- Li, S.; Fetscherin, M.; Alon, I.; Lattemann, C.; Yeh, K. Corporate social responsibility in emerging markets. Manag. Int. Rev. 2010, 50, 635–654. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Flammer, C. Does product market competition foster corporate social responsibility? Evidence from trade liberalization. Strateg. Manag. J. 2015, 36, 1469–1485. [Google Scholar] [CrossRef]

- Doh, J.; Husted, B.; Yang, X. Ethics, Corporate Social Responsibility, and Developing Country Multinationals. Bus. Ethics Q. 2013, 23, 638–639. [Google Scholar] [CrossRef][Green Version]

- Tian, Z.; Wang, R.; Yang, W. Consumer responses to corporate social responsibility (CSR) in China. J. Bus. Ethics 2011, 101, 197–212. [Google Scholar] [CrossRef]

- Luger, M.; Hofer, K.M.; Floh, A. Support for corporate social responsibility among generation Y consumers in advanced versus emerging markets. Int. Bus. Rev. 2022, 31, 101903. [Google Scholar] [CrossRef]

- Wei, Z.; Shen, H.; Zhou, K.Z.; Li, J.J. How does environmental corporate social responsibility matter in a dysfunctional institutional environment? Evidence from China. J. Bus. Ethics 2017, 140, 209–223. [Google Scholar] [CrossRef]

| Journal | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Academy of Management Journal | 2 | 1 | 3 | |||||||||||

| Administrative Science Quarterly | 0 | |||||||||||||

| Asia Pacific Journal of Management | 1 | 1 | 1 | 1 | 2 | 2 | 8 | |||||||

| Business Ethics Quarterly | 2 | 2 | ||||||||||||

| Global Strategy Journal | 0 | |||||||||||||

| International Business Review | 1 | 1 | ||||||||||||

| Journal of International Business Studies | 1 | 1 | ||||||||||||

| Journal of International Management | 0 | |||||||||||||

| Journal of Business Ethics | 6 | 4 | 2 | 1 | 3 | 2 | 2 | 1 | 1 | 22 | ||||

| Journal of World Business | 1 | 1 | 2 | |||||||||||

| Management and Organization Review | 3 | 1 | 2 | 1 | 7 | |||||||||

| Management International Review | 1 | 1 | 2 | |||||||||||

| Management Science | 0 | |||||||||||||

| Organization Science | 2 | 2 | ||||||||||||

| Strategic Management Journal | 1 | 1 | 1 | 1 | 1 | 5 | ||||||||

| Total | 8 | 4 | 2 | 5 | 3 | 7 | 5 | 4 | 2 | 2 | 7 | 4 | 2 | 55 |

| Theory | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Agency theory | 1 | 1 | 1 | 1 | 1 | 5 | ||||||||

| Attention-based view | 1 | 1 | ||||||||||||

| Boundary-spanning learning | 1 | 1 | ||||||||||||

| Chief sustainability officer view | 1 | 1 | 2 | |||||||||||

| Collective action theory | 1 | 1 | ||||||||||||

| Corporate social irresponsibility | 1 | 1 | ||||||||||||

| Critical mass theory | 1 | 1 | ||||||||||||

| Cross-cultural perspective | 1 | 1 | ||||||||||||

| direct benefits/indirect costs | 1 | 1 | ||||||||||||

| Elaboration Likelihood Model | 1 | 1 | ||||||||||||

| Grounded-theory-building | 2 | 2 | ||||||||||||

| Human capital management perspective | 1 | 1 | ||||||||||||

| Information asymmetry theory | 1 | 1 | 2 | |||||||||||

| Information Theory | 1 | 1 | 2 | |||||||||||

| Institutional Theory | 1 | 3 | 1 | 2 | 1 | 2 | 1 | 3 | 2 | 1 | 17 | |||

| Integrative social contracts theory | 1 | 1 | ||||||||||||

| International business theory | 1 | 1 | ||||||||||||

| legitimacy theory | 1 | 2 | 1 | 4 | ||||||||||

| Neoclassical trade theory | 1 | 1 | ||||||||||||

| Organizational Theory | 1 | 2 | 3 | |||||||||||

| Portfolio theory | 1 | 1 | ||||||||||||

| Product classification theory | 1 | 1 | ||||||||||||

| Reputation risk view | 1 | 1 | ||||||||||||

| Resource-based View | 1 | 1 | ||||||||||||

| Resource dependence theory | 1 | 1 | ||||||||||||

| Risk mitigation theory | 1 | 1 | ||||||||||||

| Signaling theory | 1 | 1 | 2 | |||||||||||

| Societal marketing perspective | 1 | 1 | ||||||||||||

| Social stratification view | 1 | 1 | ||||||||||||

| Stakeholder theory | 1 | 1 | 1 | 4 | 5 | 2 | 1 | 1 | 1 | 17 | ||||

| Strategic view | 1 | 1 | ||||||||||||

| Task interdependence | 1 | 1 | ||||||||||||

| Type II agency problem | 1 | 1 | ||||||||||||

| Upper echelons theory | 2 | 2 | 1 | 5 | ||||||||||

| Total | 5 | 7 | 3 | 6 | 7 | 10 | 7 | 6 | 4 | 3 | 11 | 5 | 10 | 84 |

| Topic | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Corporate Governance → CSR | 2 | 2 | 2 | 1 | 1 | 2 | 1 | 11 | ||||||

| CSR → Performance | 2 | 3 | 1 | 2 | 1 | 3 | 1 | 1 | 1 | 2 | 1 | 1 | 19 | |

| Institutional environments → CSR | 2 | 1 | 1 | 2 | 1 | 2 | 2 | 1 | 3 | 1 | 1 | 17 | ||

| Resource and Capability → CSR | 1 | 2 | 1 | 4 | ||||||||||

| Strategy/Activity → CSR | 2 | 1 | 1 | 4 | ||||||||||

| Total | 6 | 3 | 2 | 5 | 4 | 7 | 5 | 4 | 3 | 0 | 10 | 2 | 4 | 55 |

| Concepts | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Corporate ethics | 2 | 1 | 3 | |||||||||||

| CSR assurance | 1 | 1 | 2 | |||||||||||

| CSR Commitment | 1 | 1 | 1 | 3 | ||||||||||

| CSR communication | 1 | 1 | 1 | 3 | ||||||||||

| CSR donation | 1 | 1 | 1 | 1 | 1 | 5 | ||||||||

| CSR diffuse | 1 | 1 | 2 | 1 | 5 | |||||||||

| CSR disclosures | 1 | 1 | 1 | 2 | 2 | 7 | ||||||||

| CSR security | 1 | 1 | 2 | |||||||||||

| CSR initiatives legitimacy | 1 | 1 | 2 | 1 | 5 | |||||||||

| CSR reporting | 1 | 1 | 1 | 2 | 2 | 2 | 1 | 1 | 11 | |||||

| CSR strategies | 1 | 1 | 1 | 2 | 1 | 1 | 2 | 1 | 1 | 1 | 12 | |||

| CSR suspension | 1 | 1 | 2 | |||||||||||

| Corporate philanthropy | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7 | ||||||

| Corporate volunteer assignments | 1 | 1 | ||||||||||||

| Environmental CSR | 1 | 2 | 1 | 4 | ||||||||||

| external-oriented CSR practices. | 1 | 1 | 2 | |||||||||||

| Globalization of CSR | 1 | 1 | 1 | 3 | ||||||||||

| intangible assets | 1 | 1 | ||||||||||||

| Internal CSR structures | 1 | 2 | 3 | |||||||||||

| Rankins CSR Ratings | 2 | 1 | 2 | 5 | ||||||||||

| Reputation risk spillover | 1 | 1 | ||||||||||||

| Self-Presentation of CSR | 1 | 1 | 2 | |||||||||||

| Total | 1 | 3 | 3 | 5 | 7 | 5 | 9 | 9 | 12 | 7 | 15 | 9 | 4 | 88 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Du, S.-Y.; Shao, X.-C.; Jiménez, A.; Lee, J.Y. Corporate Social Responsibility of Chinese Multinational Enterprises: A Review and Future Research Agenda. Sustainability 2022, 14, 16199. https://doi.org/10.3390/su142316199

Du S-Y, Shao X-C, Jiménez A, Lee JY. Corporate Social Responsibility of Chinese Multinational Enterprises: A Review and Future Research Agenda. Sustainability. 2022; 14(23):16199. https://doi.org/10.3390/su142316199

Chicago/Turabian StyleDu, Shu-Yun, Xiao-Chen Shao, Alfredo Jiménez, and Jeoung Yul Lee. 2022. "Corporate Social Responsibility of Chinese Multinational Enterprises: A Review and Future Research Agenda" Sustainability 14, no. 23: 16199. https://doi.org/10.3390/su142316199

APA StyleDu, S.-Y., Shao, X.-C., Jiménez, A., & Lee, J. Y. (2022). Corporate Social Responsibility of Chinese Multinational Enterprises: A Review and Future Research Agenda. Sustainability, 14(23), 16199. https://doi.org/10.3390/su142316199