Abstract

Social reporting has become a critical area of interest in healthcare systems, and it has also become increasingly important for the academic community and practitioners in recent decades. Recent studies have found the existence of a slow spread of social reporting initiatives in public hospitals and a lack of guidelines and homogeneity in social reporting documents. This study aims to contribute to the literature, offering updated evidence from Italy. Through a document analysis, we (a) assessed the trends of social reporting initiatives in the Italian public hospital sector; (b) analyzed the current forms, contents, and quality, of social reporting documents, in order to isolate common elements, differentiation and emerging trends; (c) analyzed the informational power of social reporting documents for public hospitals stakeholder. Data were extracted from the public hospital website. The results confirm the scarce dissemination and homogeneity of social reporting documents and highlight the need for non-financial reporting standardization in public hospitals.

1. Introduction

In response to society’s growing expectations of accountability, organizations are increasingly disclosing social, environmental, economic, safety, and health performance [1] through reporting tools for so-called “corporate social responsibility” (CSR) [2]. CSR refers to the obligations of the firm to society or, more specifically, the firm’s stakeholders—those affected by corporate policies and practices [3].

The EU Commission describes CSR as “…a concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis” [4].

Organizations are part of society: any actions undertaken have an effect upon itself but also upon the external environment within which that organization resides [5]. This effect can take different forms: enrichment of a local community through the creation of employment opportunities and distribution of wealth created, respect for workers’ rights and well-being (social impact), and utilization of natural resources (with a consequent environmental impact). In this context, stakeholders are concerned about whether a company is following a socially responsible path and is acting in an environmentally friendly way [6].

In this scenery, starting from the 1970s, many authors [7,8,9,10], recognizing that the activities of an organization impact upon the external and social environment, have suggested that one of the roles of accounting should be to report upon the impact of an organization in this respect. Following these suggestions, during the last years, CSR has become dominant in organizations’ reporting. Every corporation has a policy concerning CSR and produces a report annually detailing its activity.

In this context, the social report (SR) is an external communication document initially developed and disseminated in the private sphere as a reporting tool for CSR. The SR aims to represent both information of economic and financial nature, and the effects produced by the business activity on the various categories of stakeholders, in terms of current and future social and environmental effects [11]. The SR represents, on the one hand, a communication and public relations management tool aimed at improving the perceived image of the company towards the external environment; on the other, the SR is a tool included in the broader cycle of corporate planning, control, and reporting. It allows for supporting corporate strategies aimed at achieving greater “accountability” and “sustainability”. These last two concepts are strongly correlated.

The concept of “accountability” refers to the responsibility of the organization for reporting allocation choices of public resources used in carrying out its business, the results achieved, and the resulting effects [12].

Accountability implies the need to produce clear, truthful, and understandable reporting on the economic and financial performance and on the social and environmental effects induced in the community. The reporting activity must therefore not stop only at the results expressed in monetary terms but must go further, considering also the social and territorial effects.

In this sense, the overall value created by the organization includes not only the economic but also has consideration for the social and environmental dimensions [13].

The maximization of the value created according to this perspective configures the concept of “sustainability”.

Private companies are shifting from the 1990s’ social and environmental types of reports to sustainability ones. This trend has been corroborated by the dissemination of the Global Reporting Initiative (GRI) guidelines, a reporting standard conceived in 1997 that encourages the use of the term sustainability to describe triple bottom-line disclosures, that is, comprehensive disclosures of environmental, social, and economic issues [14,15].

Over time, the standards described by the GRI have given rise to various social reporting tools, which have taken on different names: social report (documents the company’s social performance), sustainability report (focused on the impacts of activities with respect to the environmental dimension and social), and environmental balance (represents the company-environment relationship). Finally, the latest evolution of the sustainability management process in a company is the Integrated Report, a document that integrates the traditional economic report with information concerning the three dimensions of economic, social, and environmental sustainability.

The main purpose of private companies is to create wealth; accordingly, the need to give their stakeholders an account of their social function is an implicit function.

In the public sector, the SR takes on different meanings: the public company carries out activities and delivers services aimed at satisfying the needs of the local community; social reporting represents a form of control and representation of the overall performance of the public company [16], in line with the principles of transparency and accountability. In addition, the SR supports the strategic management of relations between the public company and its stakeholders (public governance) [17]. Finally, the diffusion of social reporting is associated with the growing “sensitivity” towards the measurement and communication of effects in terms of social and environmental sustainability.

In Italy, the phenomenon of social reporting has involved and is currently widespread in various types of public organizations [18,19,20]. In the public healthcare sector, social reporting represents a critical area of interest: through the social reporting documents, public healthcare structures present their activity (list of healthcare services), their results (health outcomes), and the value created in relation to one or more categories of stakeholders in order to satisfy specific information needs [21,22].

However, Italian public healthcare structures only started producing social reporting documents in 2003 [23,24]. The publication trend has been slow: since 2003, in 2006, only 22 healthcare structures had published social reporting documents [24].

The phenomenon initially involved much more local health authorities (Aziende Sanitarie Locali (ASLs)) (19 ASLs out of 146) and much fewer public hospitals (Aziende Ospedaliere (AOs)) (3 AOs out of 113) [24]. To date, the publication of documents continues to grow for the ASLs; on the contrary, the number of documents published by the AOs remains very low. Despite this, there are still few research studies on the topic of social reporting in healthcare structures [23,24]; in addition, to the best of our knowledge, there are no Italian studies that have specifically investigated the critical issues that characterize social reporting in AOs.

Part of the results of the most recent studies only showed [23,24]:

- -

- The existence of a slow trend of social reporting initiatives;

- -

- A lack of homogeneity in SRs of AOs (in terms of structure, content, methods of dissemination of documents, etc.).

In this study, we conducted a document analysis of Italian AOs’ social reporting documents. The aim was threefold:

- (1)

- To assess the trends of social reporting initiatives in the Italian public hospital sector;

- (2)

- To analyze the current forms, contents, and quality of social reporting documents, in order to isolate common elements, differentiation, and emerging trends;

- (3)

- To analyze the informational power of social reporting documents for public AOs’ stakeholders, describing their information needs and comparing these with information deduced from reading the document.

The study is part of a broader ongoing research project aimed at understanding: (a) the usefulness and information capacity of the SR in AOs and (b) the potential obstacles to the publication of the SR.

The paper is organized as follows: the following sub-section describes the Italian National Health System providing a framework of Italian public healthcare structures; Section 2 describes the method, selection, and analysis criteria; Section 3 reports the results organized consistently with the previously defined objectives; Section 4 presents conclusions about the current information value and the potential of social reporting documents in Italian AOs.

The Italian National Health System

Over the last three decades, the INHS has been gradually but substantially transformed, switching from a centralized system (1980s) to one characterized by the devolution of control to the regional level (1990s) [25]: the central government maintains a guiding role in defining basic health objectives and controlling health outcomes; Italian regions develop their regional health plans and define their health care priorities to achieve health objectives defined by the central government [26,27].

The major effect of the decentralization process has been the creation of 21 regional health systems autonomous and responsible for the organization of healthcare services [28].

Four types of public facilities provided healthcare services. At the local level, the most important units are the ASLs. Besides providing outpatient assistance and a number of community services, an ASL manages one or more small District General Hospital (Presidi Ospedalieri) directly.

In addition to ASL, three other kinds of healthcare facilities exist, which complete the level II hospitals. The most important one is the AO. AOs are independent of the local ASL, directly accountable to the regions, and characterized by highly specialized departments that deal with more complex medical conditions than ASLs.

The two remaining facilities are the Scientific Institutes for Research, Hospitalization and Healthcare (Istituti di Ricovero e Cura a Carattere Scientifico (IRCCS)) and the Teaching Hospitals (Azienda Ospedaliera Universitaria (AOU)) that differentiate from the AOs mainly for their scientific research and/or training responsibilities.

At the time of this study, the Minister of Italian Health declared that the following healthcare facilities were present in Italian regions (https://www.dati.salute.gov.it/) (accessed on 1 April 2022).

In this study, we focused our attention on AOs. This choice is justified by two reasons: first, the greater complexity that characterizes both the organization of these structures and the healthcare interventions provided makes the process of sharing the strategic choices adopted and the results achieved with the stakeholders even more necessary. Secondly, the inclusion of only AOs makes the comparison more coherent, as the different functions performed by the healthcare structures could affect the contents of the documents, making the comparison insignificant. Indeed, on the one hand, the information contents of the reporting documents are similar for AOs and ASLs, on the other, the social reporting document takes on different meanings for AOUs and IRCCS. These differences are mainly due to the significant role of teaching and research activities, and to the different funding mechanisms.

2. Materials and Methods

2.1. Method and Selection Criteria

We used document analysis as a qualitative research method of data collection and analysis [29]. Document analysis is a systematic procedure for reviewing and evaluating documents that entails finding, selecting, appraising, and synthesizing data contained within them.

According to this, data were examined and interpreted in order to elicit meaning, gain understanding, and develop empirical knowledge [30,31].

We started searching and reviewing all social reporting documents published by Italian AOs. Accordingly, from the official websites of each AO, we started.

Documents were identified using two strategies: in a first step, we visited the section “Transparent Administration” (where all the official documents intended for stakeholders are published); in a second step, we used the website search bar to find any possible social reporting document using short phrase or keywords (i.e., social report or sustainability). The initial sample was composed of 53 AOs (see Table 1).

Table 1.

Italian healthcare structures.

2.2. Document Analysis Criteria

This section describes the criteria used in document evaluation. The first two aims of this study are the following: (1) to assess the trends of social reporting initiatives in the Italian public hospital sector; (2) to analyze the current forms, contents, and quality of social reporting documents, in order to isolate common elements, differentiation, and emerging trends.

Considering the absence of specific guidelines for Italian AOs, documents were analyzed referring to:

- -

- The standards proposed by the Italian study group for the SR (Gruppo di studio per il bilancio sociale (GBS)) published since 2001 (with specific reference to the public sector) [32];

- -

- The guidelines on social reporting for public administrations, drawn up in 2006 by the Department of Public Administration [33].

Specifically, these are “general principles” with which to standardize the SR. The principles include:

- (a)

- The publication, “preferably” on an annual basis, of the documents;

- (b)

- The presence of minimal information content. Table 2 shows the description of the information required according to the two standards.

Table 2. General principles for standardization of SR documents (GBS and Department of Public Administration standards): required information content.

3. Results

3.1. Social Reporting in Italian Public Hospitals: State of the Art

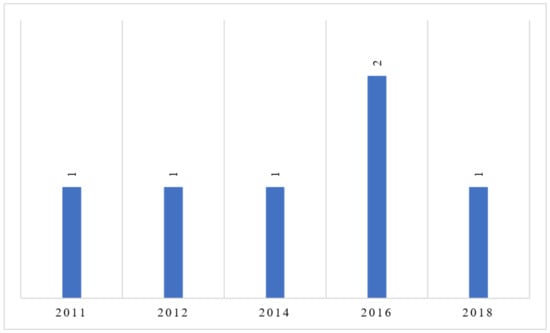

The first aim of this paper was to assess the trends of social reporting initiatives in the Italian public hospital sector. In general, social reporting has affected the health sector since 2003. With specific reference to AOs, 2 documents were published from 2003 to 2006 [24].

According to our search, in April 2022, we extracted 6 social reporting documents published on the official website of AOs. Documents were published between 2011 and 2018 (Figure 1). Regarding the trend shown, it is noted that in 2016 GRI transitioned from providing guidance to setting universal standards (https://www.globalreporting.org/standards/standards-development/universal-standards/) (accessed on 1 April 2022). This could explain the low number of documents published up to 2015 and the consequent increase in 2016.

Figure 1.

Reference year of SRs. (Source: The Authors).

Despite the slight increase, it is possible to note that the requirement to publish social reporting documents “preferably” annually is unsatisfactory. In fact, the six AOs published the documents in different years, and the most recent SR is published in 2018.

3.2. Structure, Content, and Quality of Documents

The second aim of this study was to analyze the current forms, contents, and quality of social reporting documents, in order to isolate common elements, differentiation, and emerging trends.

First, we compared the structure and content of the different documents. Table 3 shows our results.

Table 3.

Analysis of social reporting documents.

SRs show poor homogeneity in terms of general presentation and breadth of information. In some cases, the document is wider (N. SR 2, 4, 5, and 6—number of pages); in others, more content (N. SR 1 and 3—number of pages).

The SR is an external communication tool aimed primarily at improving the perceived image of the structure towards the external environment. In this context, the number of figures and graphs is relevant. In addition, in this case, in some documents tables and figures have a primary role (N. SR 2 and 5), while in others the figures are absent, and the document only shows graphs referring to the values of the activity (N. SR 6).

There is no homogeneity in terms of the structure of the documents, although there is a partial similarity in terms of the content of the Section 1 and in a few cases of homogeneity in the name of the section.

Specifically, the Section 1 focuses in all cases on the description of the AO and its identity. The main contents concern:

- -

- Institutional structure and AO organizational system (departments and their functions);

- -

- Principles and reference values;

- -

- Strategies and policies implemented;

- -

- Guidelines, objectives, and future strategies.

The content of the Section 1 is therefore similar in most cases (five out of six documents); in only one case (N. SR 5), the information on hospital identity is reported in Section 2, after limiting Section 1 to the definition of the guidelines and objectives of the three-year period.

However, there is a lack of homogeneity in terms of the section name: only in two cases the section is called “Hospital identity”.

The Section 2 focuses on information about the used resources, the investments made, and the purchases (activity economic report). Only in one case (N. SR 6), Section 2 is intended for information on relations with patients and users’ satisfaction. The denomination is homogeneous only in two cases (N. SR 1 and 4).

The Section 3 focuses on stakeholders (internal and external). Specifically, the key information is the following:

- -

- Composition and roles of internal human resources (employees);

- -

- providers;

- -

- Patients, users, and level of satisfaction.

Only in one case (N. SR 6), the Section 3 is dedicated to information concerning the communication channels used by the hospital, as well as the social profiles on which the hospital is active (Twitter, Instagram, YouTube, etc.).

Section 4 reports information about the results of the activities (emergency, outpatient, and hospitalization activities); in only one case (N. SR 2), Section 4 is dedicated to the presentation of employees and their training.

Section 5 is present in four out of six cases (N. SR 2, 3, 5, and 6), and reports generally inconsistent information: two SRs concern the corporate communication system (N. SR 2 and 5), or relations with stakeholders; three SRs report the satisfaction levels of patients (N. SR 2, 3, and 5); one SR reports information about the weight of women in hospital activities and hospital policies for the well-being of female workers (N. SR 6—gender balance).

Section 6 is present only in two cases (N. SR 3 and 6) and reports information about the performance plan (the planned objectives and the employee evaluation system in relation to their contribution to the achievement of the objectives).

Sections 7 to 13 concern only one AO (N. SR 6) and reports the following information:

- -

- Available technological resources (Technologies and innovation—Section 7);

- -

- Resources used to carry out hospital activities, investments, and purchases (Economic report—Section 8);

- -

- Information about the out-of-court and judicial management system, or the assignment of legal appointments, liquidation, and risk assessment systems (Litigation—Section 9);

- -

- Quality management system, i.e., assistance paths created for the adaptation of the various professional skills to the production of effective and appropriate assistance, as well as centered on the patients’ needs and on the continuous improvement of quality (quality and accreditation—Section 10);

- -

- Hospital information system, or description of the network infrastructure available to the hospital, to allow patients and employees to use the information and online services (Section 11);

- -

- Performance plan or strategic and operational guidelines and objectives defined, and indicators for their measurement and evaluation. Finally, description of the transparency and corruption plan (Performance, transparency, and corruption prevention—Section 12);

- -

- Description of the health objectives and services targets defined by the region (Regional objectives—Section 13).

Finally, two out of six documents report the appendixes. Appendixes present the results of the interviews with stakeholders (Appendix 1—N. SR 5). Results are divided into interviews conducted through telephone questionnaires (Appendix 1—N. SR 6), inpatient and outpatient questionnaires (Appendix 2—N. SR 7), or using social networks (Appendix 3—N. SR 6).

At the end of this first phase of analysis, we assessed the quality of the documents, considering the degree of adherence to the minimum contents set by the GBS and Department of Public Administration standards (see Table 2). The following table shows the correspondence between the information required by the two standards and the content of the documents. Specifically, after analyzing each SR, we show whether the expected information is contained in the documents (X) and in which section (Section) (Table 4).

Table 4.

Overall quality of SRs.

On the one hand, the documents show sufficient information capacity: most of the information required by the two standards is contained in the documents, even if in often different sections; on the other hand, information regarding improvement actions and objectives is contained in only one document (SR1), and additional information concerning stakeholder opinions is contained in only two documents (SR5 and 6). Wanting to assign a score from 0 to 7 to each SR (0: none of the information required by the standards is contained in the document; 7: all the information required by the standards is contained in the document), it is possible to note that no document reaches the maximum score. Only three documents reach a score of 6. The remaining three documents reach a score of 5.

3.3. Informational Power of SR for Public Hospital Stakeholders

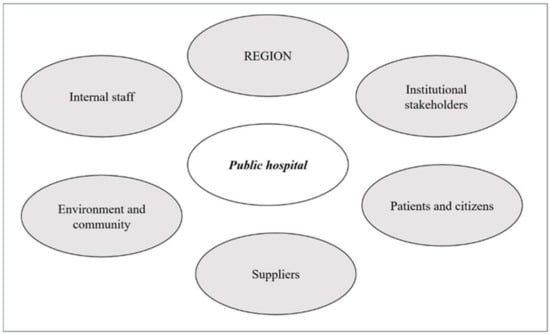

The third aim of document analysis was to investigate the informational power of SR for hospital stakeholders. The SR aims to report the value created by the AO in relation to each category of key stakeholders.

Figure 2 shows AO stakeholders. We describe the information that the stakeholders draw from reading the documents.

Figure 2.

Public hospitals’ stakeholders. (Source: The Authors).

In general, SR documents of AOs have an internal and external value. For internal stakeholders, the document seems to be aimed at improving the sense of belonging to the structure and describes the strategic vision of the hospital in relation to stakeholders.

For external stakeholders, reading the document allows learning more about the role and management methods of the hospital, strengthening relationships with patients, communities, suppliers, and other institutional interlocutors.

The region is in charge of the regional health system. Regions are responsible for the definition, coordination, and monitoring of regional health policies. Reading the SR allows the region to understand:

- -

- The role of the hospital with respect to the achievement of the objectives of the entire regional health system;

- -

- The level of efficiency, effectiveness, and overall cost-effectiveness;

- -

- The implementation of projects for improvement, innovation, and requalification of assistance models.

For other institutional stakeholders (Conferences of Mayors, other health companies, non-profit organizations, etc.), reading the document allows acquiring information on the health policies implemented, on the assistance models, and on the renewal projects implemented.

Patients and citizens are interested in knowing the availability, accessibility, and quality of services, the achievement of the expected results in terms of the health of the population, as well as the opinions and the level of satisfaction of other patients.

For hospital suppliers (suppliers of health and non-health goods and services), the SR provides information concerning the purchasing planning policy, the supplier selection procedures, the payment management policy, and the conditions of solidity and solvency of hospitals.

Regarding the environment and community, the SR provides information concerning the use of resources and the impact on the external environment.

Finally, for the internal staff, the SR meets common information needs, which concern the organizational changes, the institutional mission of the hospital, and the social value of the hospital work. Reading the SR makes it possible to know the personnel policies, training, incentive, and evaluation systems.

4. Discussion, Limitations, and Conclusions

The first aim of this study was to assess the trends of social reporting initiatives in the Italian public hospital sector. Results show the scarcity of social reporting documents published by the AOs. Accordingly, the level of continuity of social reporting experiences in Italian AOs cannot be considered satisfactory. In some regions, the presentation of social reporting documents is mandatory only for the ASLs (i.e., Emilia Romagna). As regards the AOs, the results of this study only allow us to conclude that the publication of social reporting documents has gone from three documents in 2006 [24] to six in 2022 (the analysis included only the SRs published on the institutional websites of AOs). This may be the result of the lack of specific guidelines for AOs, but also of the scarcity of resources (staff devoted to the creation of the SR or resources to invest in specific projects) and time (the complex activity carried out by hospitals certainly is to be considered a priority). Further investigations are needed.

Regarding the characteristics and contents of the documents, results show a strong lack of homogeneity, both in terms of general structure and denomination of the sections.

This is certainly due to the lack of specific guidelines for AOs. SRs are generally inspired by “reporting standards” known nationally or internationally. To date, there are different standards [34]. In addition, in the public sector, standards that register a greater number of applications in operational practice are:

- -

- The Accountability 1000 (AA1000) [35];

- -

- The GRI [36];

- -

- The standards proposed by the Copenhagen Charter [37];

- -

- At the national level, the standards proposed by the Italian study group for the SR (GBS) published since 2001 (with specific reference to the public sector) [32];

- -

- The guidelines on social reporting for public administrations, drawn up in 2006 by the Department of Public Administration [33].

- -

- This has led to divergences in the documents, as the healthcare structures prepare their SRs referring to different standards, or in some cases referring to multiple standards at once.

With general reference to healthcare structures, only in 2016, the GBS published Document No. 9, entitled “Social reporting for healthcare structures” with the aim of adapting the standards of the public sector SR to the national healthcare system [38].

Regarding the overall quality of the documents, the documents show sufficient information capacity. Indeed, the documents contained most of the information required by national standards, even if in often different sections. However, information about future actions and improvement objectives, and additional information concerning stakeholder opinions, was present only in three SRs (see Section 3.2). AOs could answer these problems through more careful planning of the process of elaboration of social reporting documents.

Finally, as regards the informational power of documents, social reporting can significantly contribute to meeting the information needs of stakeholders. However, the contents of the documents can be further expanded and improved. At present, the lack of specific guidelines constitutes an obstacle to improving the quality of documents.

This study has some limitations. First, the focus on Italian AOs does not allow for a complete update of the state of the art in the field of social reporting of Italian healthcare structures; however, this choice makes the comparison more coherent, as the different functions performed by the healthcare structures could affect the contents of the documents, making the comparison insignificant.

Another limitation is due to the choice to include only the official documents published on the hospital websites. Consequently, we excluded documents currently in the process of publication, and documents not published on official websites but, for example, presented during institutional conferences (i.e., Conferences of Mayors), press conferences, or distributed in paper form to citizens and institutional interlocutors. These forms of distribution can be traced back to the will of the healthcare structures to consider the SR, not as a tool for relating and communicating with external stakeholders, but as a planning, control, and reporting tool aimed primarily at institutional interlocutors [24]. However, this is to be considered reductive, as it limits the informational power of SR. Indeed, SR documents should allow the strengthening of accountability relationships, and therefore it would be essential to guarantee the involvement of both internal and external stakeholders. Future research developments require the use of a questionnaire intended for AOs that allows:

- (a)

- To acquire information about the documents being processed or completed;

- (b)

- To understand any difficulties or barriers in social reporting documents development, also in light of the lack of specific guidelines for hospitals;

- (c)

- To develop a basic reference model to support the process of preparing social reporting documents for AOs, which takes into account the specific characteristics of this type of structure.

This study contributes to providing updated learning pathways for policymakers. Worldwide policymakers have widely considered the themes related to sustainability and social reporting. The attention on this topic is driven by the external pressure made by stakeholders in order to support the achievement of the highest degree of worldwide sustainability also in the healthcare sector. In this sense, national and international governments have started to introduce a new form of regulation in order to sustain these practices. Despite these interventions, in some countries, the regulation is still not uniform; this makes it difficult to compare documents drawn up by structures belonging to the same sector. In this sense, we contribute to the literature on this topic, offering evidence from the Italian healthcare sector. The Italian legislation is still confusing. and there are no specific reporting standards for AOs. This should cause some worries in policymakers: the creation of standards for social reporting calibrated on the reality of AOs can perform an important function in terms of comparability and homogeneity of contents, promoting transparency, and reducing the self-referentiality of reporting. It is therefore desirable to provide a more coherent picture of the heterogeneous panorama of elements that relate to the choice of social reporting models, as part of a superior design to support both the need of AOs to adapt to the CSR requirements, and of policymakers to sustain the diffusion of CSR practices and initiatives in the healthcare sector.

Author Contributions

Contributed equally to this work, M.G. and M.M.; the extraction and collection of data, V.C. All authors have read and agreed to the published version of the manuscript.

Funding

The authors of this paper wish to thank the Department of Experimental and Clinical Medicine of Magna Graecia University for the financial support.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data/documents were extracted from the official websites of Italian public hospitals.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Fonseca, A.; Macdonald, A.; Dandy, E.; Valenti, P. The state of sustainability reporting at Canadian universities. Int. J. Sustain. High. Educ. 2011, 12, 22–40. [Google Scholar] [CrossRef]

- Adams, C.; Zutshi, A. Corporate social responsibility: Why business should act responsibly and be accountable. Aust. Account. Rev. 2004, 14, 31–39. [Google Scholar] [CrossRef]

- Smith, N.C. Corporate social responsibility: Whether or how? Calif. Manag. Rev. 2003, 45, 52–76. [Google Scholar] [CrossRef]

- EU Commission. Communication from the Commission Concerning Corporate Social Responsibility: A Business Contribution to Sustainable Development 5 (COM(2002) 347 Final, Brussels, 2 July 2002). Available online: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2002:0347:FIN:en:pdf (accessed on 15 November 2022).

- Crowther, D.; Aras, G. Corporate Social Responsibility; Bookboon: London, UK, 2008. [Google Scholar]

- Jennifer Ho, L.C.; Taylor, M.E. An empirical analysis of triple bottom-line reporting and its determinants: Evidence from the United States and Japan. J. Int. Financ. Manag. Account. 2007, 18, 123–150. [Google Scholar] [CrossRef]

- Hetherington, J.A.C. Corporate Social Responsibility Audit: A Management Tool for Survival; The Foundation for Business Responsibilities: London, UK, 1973. [Google Scholar]

- Dahl, R.A. A prelude to corporate reform. Bus. Soc. Rev. 1972, 1, 17–23. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Davis, K. The Case for and against Business Assumption of Social Responsibilities. Acad. Manag. J. 1973, 16, 312–322. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Romolini, A. Accountability E Bilancio Sociale Negli Enti Locali; FrancoAngeli: Milan, Italy, 2007. [Google Scholar]

- Van Marrewijk, M. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Elkington, J. Enter the Triple Bottom Line. In The Triple Bottom Line: Does It All Add up, 1st ed.; Routledge: London, UK, 2004; pp. 1–16. [Google Scholar]

- Brown, H.S.; De Jong, M.; Levy, D.L. Building institutions based on information disclosure: Lessons from GRI’s sustainability reporting. J. Clean. Prod. 2009, 17, 571–580. [Google Scholar] [CrossRef]

- Marcuccio, M. La rendicontazione sociale per le amministrazioni locali come strumento di accountability e controllo strategico. Azienda Pubblica 2002, 6, 637–672. [Google Scholar]

- Meneguzzo, M. Innovazione, Managerialità E Governance. In La PA Verso Il 2000; Aracne: Roma, Italy, 2001; pp. 1–426. [Google Scholar]

- Secchi, D. The Italian experience in social reporting: An empirical analysis. Corp. Soc. Responsib. Environ. Manag. 2006, 13, 135–149. [Google Scholar] [CrossRef]

- Albareda, L.; Lozano, J.M.; Ysa, T. Public policies on corporate social responsibility: The role of governments in Europe. J. Bus. Ethics 2007, 74, 391–407. [Google Scholar] [CrossRef]

- Guthrie, J.; Manes-Rossi, F.; Orelli, R.L. Integrated reporting and integrated thinking in Italian public sector organisations. Meditari Account. Res. 2017, 25, 553–573. [Google Scholar] [CrossRef]

- Macuda, M.; Toledo, M.A.R. The scope of environmental disclosure in the European healthcare sector–an empirical study. Zesz. Teor. Rachun. 2020, 110, 105–132. [Google Scholar] [CrossRef]

- Rodriguez, R.; Svensson, G.; Wood, G. Sustainability trends in public hospitals: Efforts and priorities. Eval. Program Plan. 2020, 78, 101742. [Google Scholar] [CrossRef]

- Alesani, D.; Marcuccio, M.; Trinchero, E. Bilancio sociale e aziende sanitarie: Stato dell’arte e prospettive di sviluppo. Mecosan 2005, 55, 9–34. [Google Scholar]

- Alesani, D.; Cantu, E.; Marcuccio, M.; Trinchero, E. La Rendicontazione Sociale Nelle Aziende Sanitarie: Funzionalità E Potenzialità. In Rapporto Oasi; Egea: Utrecht, The Netherlands, 2006; pp. 617–663. [Google Scholar]

- Del Vecchio, M.; De Pietro, C. Italian public health care organizations: Specialization, institutional deintegration, and public networks relationships. Int. J. Health Serv. 2011, 41, 757–774. [Google Scholar] [CrossRef]

- Mauro, M.; Giancotti, M. Italian responses to the COVID-19 emergency: Overthrowing 30 years of health reforms? Health Policy 2021, 125, 548–552. [Google Scholar] [CrossRef]

- Ferrè, F.; Cuccurullo, C.; Lega, F. The challenge and the future of health care turnaround plans: Evidence from the Italian experience. Health Policy 2012, 106, 3–9. [Google Scholar] [CrossRef]

- De Belvis, A.G.; Ferrè, F.; Specchia, M.L.; Valerio, L.; Fattore, G.; Ricciardi, W. The financial crisis in Italy: Implications for the healthcare sector. Health Policy 2012, 106, 10–16. [Google Scholar] [CrossRef] [PubMed]

- Bowen, G.A. Document analysis as a qualitative research method. Qual. Res. J. 2009, 9, 27–40. [Google Scholar] [CrossRef]

- Corbin, J.; Strauss, A. Book review: Basics of qualitative research: Techniques and procedures for developing grounded theory (3rd ed.). Thousand Oaks CA Sage. Organ. Res. Methods 2008, 12, 614–617. [Google Scholar]

- Rapley, T. Doing Conversation, Discourse and Document Analysis; Sage: London, UK, 2007. [Google Scholar]

- GBS Gruppo Di Studio Per Il Bilancio Sociale. Available online: http://www.gruppobilanciosociale.org/ (accessed on 2 April 2022).

- Dipartimento Della Funzione Pubblica. Direttiva 17 Febbraio 2006. In Rendicontazione Sociale Nelle Amministrazioni Pubbliche (Gazzetta Ufficiale Serie Generale n.63 del 16-03-2006); Dipartimento Della Funzione Pubblica: Roma, Italy, 2016. [Google Scholar]

- Hinna, L. Il Bilancio Sociale Nelle Amministrazioni Pubbliche. In Processi, Strumenti, Strutture E Valenze; Franco Angeli: Milano, Italy, 2008; pp. 1–272. [Google Scholar]

- Beckett, R.; Jonker, J. Accountability 1000: A new social standard for building sustainability. Manag. Audit. J. 2002, 17, 36–42. [Google Scholar] [CrossRef]

- Wilburn, K.; Wilburn, R. Using global reporting initiative indicators for CSR programs. J. Glob. Responsib. 2013, 4, 62–75. [Google Scholar] [CrossRef]

- The Copenhagen Charter. A Management Guide to Stakeholder Reporting. 1999. Available online: http://base.socioeco.org/docs/doc-822_en.pdf (accessed on 2 April 2022).

- La Rendicontazione Sociale Delle Aziende Sanitarie. Available online: http://www.gruppobilanciosociale.org/pubblicazioni/la-rendicontazione-sociale-delle-aziende-sanitarie-documenti-di-ricerca-n-9/ (accessed on 2 April 2022).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).