How Does Corporate Charitable Giving Affect Enterprise Innovation? A Literature Review and Research Directions

Abstract

1. Introduction

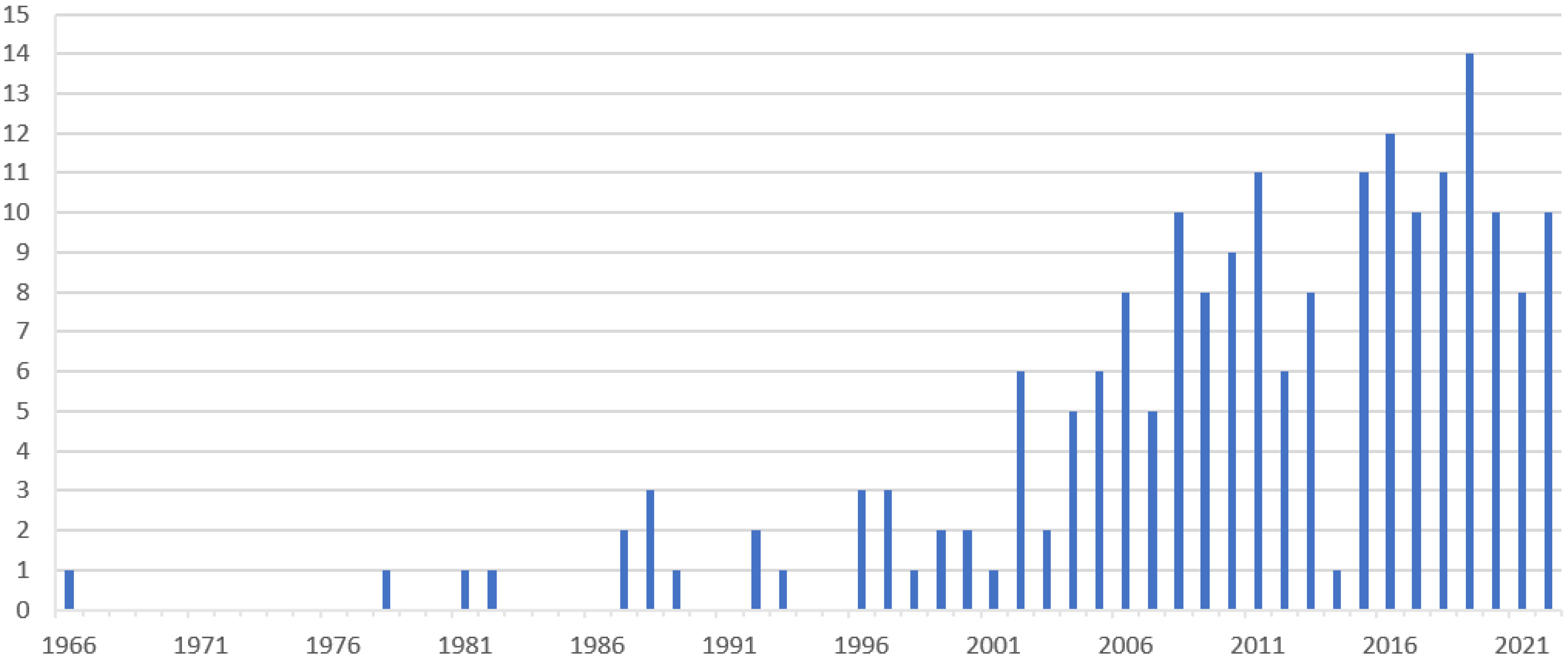

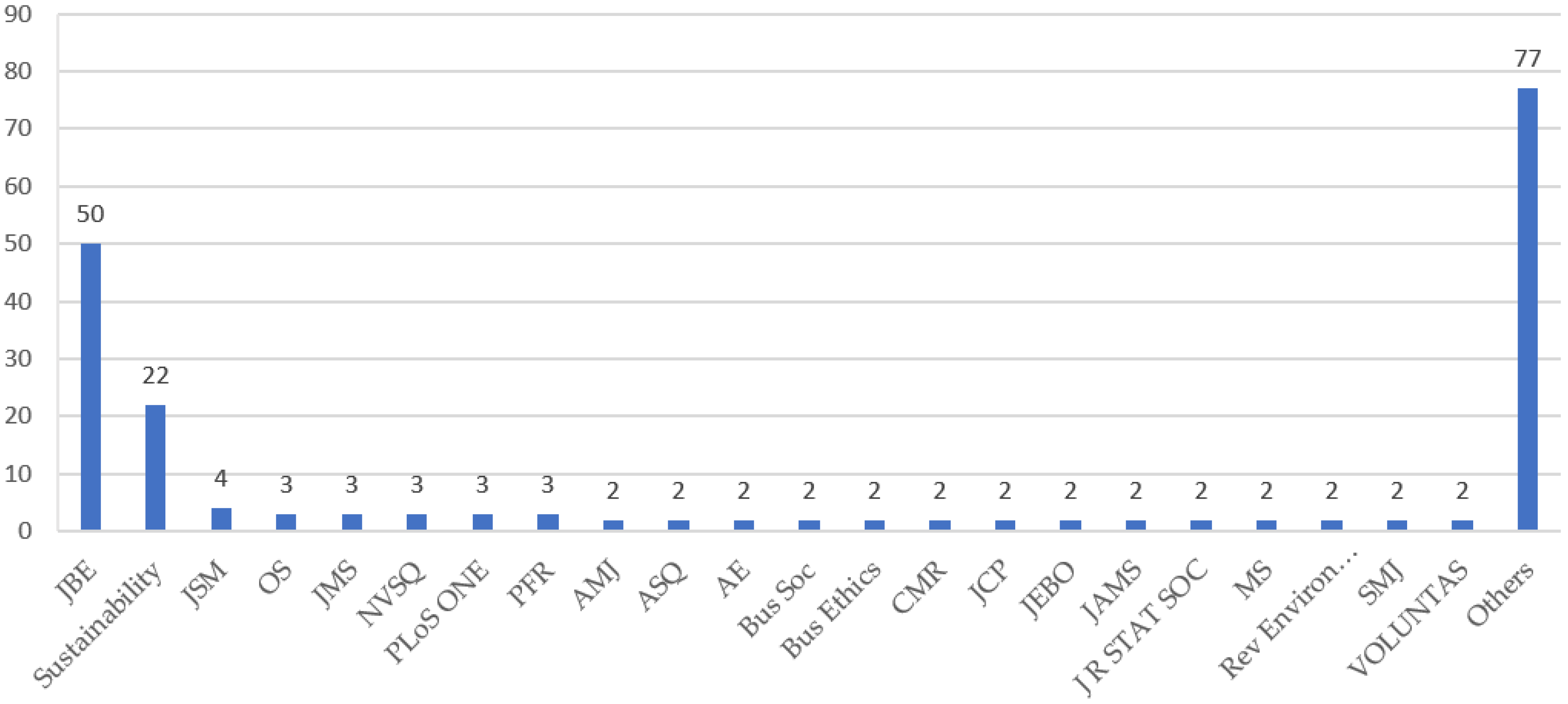

2. Methodology

2.1. Data Characteristics

{kind=link}

{kind=link}

{kind=link}

| Application Fields | Number of Paper | Percentage |

|---|---|---|

| Corporate Charitable Giving and Performance | 19 | 10.20% |

| Corporate Charitable Giving and Innovation | 7 | 3.06% |

| Corporate Charitable Giving and Corporate Social Responsibility | 46 | 23.47% |

| Factors Influencing Corporate Charitable Giving | 30 | 15.31% |

| The Impact of Corporate Charitable Giving on Business | 52 | 26.53% |

| Some Literature Reviews related to Corporate Charitable Giving | 4 | 2.04% |

| Others | 38 | 19.39% |

| Total | 196 | 100% |

2.2. Data Generalization

3. Theoretical Development of Corporate Charitable Giving

3.1. The Altruism of Corporate Charitable Giving

3.2. The Strategic Nature of Corporate Charitable Giving

4. Perspectives on Corporate Charitable Giving and Enterprise Innovation

4.1. Perspective of Technological Network

4.2. Perspective of Political Reputation

4.3. Perspective of Media Attention

4.4. Perspective of Resource Regulation

4.5. Theoretical Basis and Potential Mechanisms

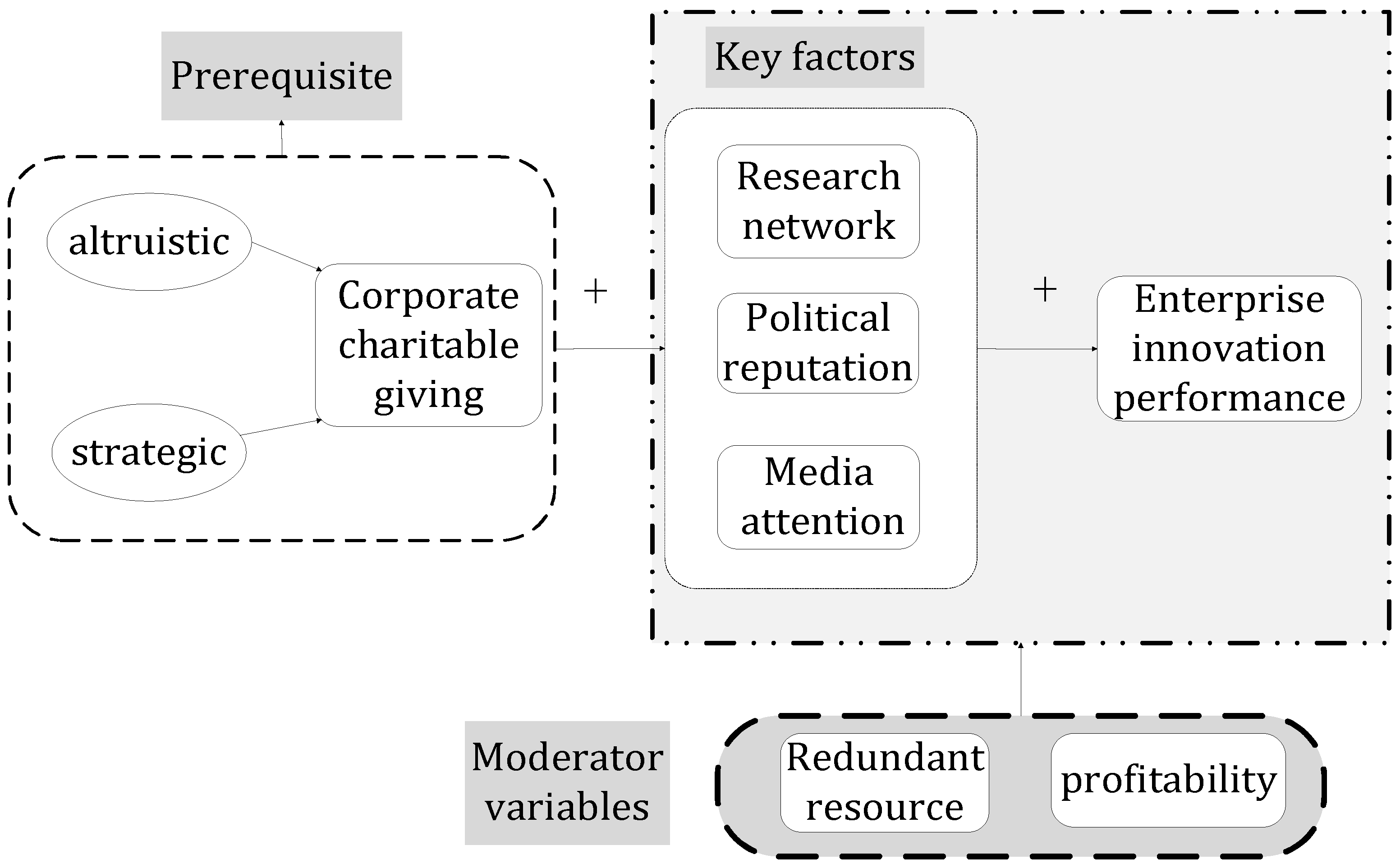

5. Conclusions and Discussion

5.1. Conclusions

5.2. Discussion

Author Contributions

Funding

Conflicts of Interest

References

- FASB. Statement of Financial Accounting Standards No. 116: Accounting for Contributions Received and Contributions Made; Financial Accounting Standards Board: Norwalk, CT, USA, 1993. [Google Scholar]

- Gautier, A.; Pache, A.C. Research on corporate philanthropy: A review and assessment. J. Bus. Ethics 2015, 126, 343–369. [Google Scholar] [CrossRef]

- Zhang, Z.; Li, Y.; Li, L. A Study on the Relationship between Corporate Philanthropy, Science and Technology Resource Acquisition and Innovation Performance: Perspective of Resource Exchange between Enterprises and Government. Nankai. Bus. Rev. 2016, 19, 13. [Google Scholar]

- Bereskin, F.L.; Campbell, T.L.; Hsu, P.H. Corporate philanthropy, research networks, and collaborative innovation. J. Financ. Manag. 2016, 45, 175–206. [Google Scholar] [CrossRef]

- Bereskin, F.L.; Hsu, P.H. Corporate philanthropy and innovation: The case of the pharmaceutical industry. J. Appl. Corp. Finance 2016, 28, 80–86. [Google Scholar]

- Wang, H.; Qian, C. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Brammer, S.; Brooks, C.; Pavelin, S. Corporate Social Performance and Stock Returns: UK Evidence from Disaggregate Measures. J. Financ. Manag. 2006, 35, 97–116. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Corporate reputation and philanthropy: An empirical analysis. J. Bus. Ethics 2005, 61, 29–44. [Google Scholar] [CrossRef]

- Young, D.R.; Burlingame, D.F. Paradigm lost: Research toward a new understanding of corporate philanthropy. In Corporate Philanthropy at the Crossroads; Indiana University Press: Bloomington, IN, USA, 1996; pp. 158–176. [Google Scholar]

- Bekkers, R.; Wiepking, P. A Literature Review of Empirical Studies of Philanthropy: Eight Mechanisms That Drive Charitable Giving. Nonprofit Volunt. Sect. Q. 2011, 40, 924–973. [Google Scholar] [CrossRef]

- Cha, W.; Rajadhyaksha, U. What do we know about corporate philanthropy? A review and research directions. Bus. Ethics Eur. Rev. 2021, 40, 924–973. [Google Scholar]

- Eells, R. Corporate giving: Theory and policy. Calif. Manag. Rev. 1958, 1, 37–46. [Google Scholar] [CrossRef]

- Horner, J.E. The Development of Corporate Giving to Private Higher Education: With Special Reference to the Rise and Growth of State and Regional College Foundations, Including the Ohio Foundation of Independent Colleges. Ph.D. Thesis, Electronic Thesis or Dissertation. The Ohio State University, Columbus, OH, USA, 1955. [Google Scholar]

- Kasper, G.; Fulton, K. The Future of Corporate Philanthropy: A Framework for Understanding Your Options; Monitor Institute Cambridge: Cambridge, UK, 2006. [Google Scholar]

- Marinetto, M. The historical development of business philanthropy: Social responsibility in the new corporate economy. Bus. His. 1999, 41, 1–20. [Google Scholar] [CrossRef] [PubMed]

- Porter, M.E.; Kramer, M.R. The competitive advantage of corporate philanthropy. Harv. Bus. Rev. 2002, 80, 56–68. [Google Scholar] [PubMed]

- Jiang, S.; Mi, J.; Tao, X.; Hu, W. Corporate Philanthropy and Innovation Performance. Int. J. Bus. Manag. 2018, 13, 173. [Google Scholar] [CrossRef][Green Version]

- Chen, S.; Zhou, J. The Influence of Corporate Philanthropy on Innovation: Evidence from Chinese Manufacturing Industry. Manag Rev. 2018, 30, 57–67. [Google Scholar]

- Ou, J.; Chen, Y.; Lin, Z. Media Attention of Charitable Donations and Enterprise Innovation. FEM 2021, 43, 111–122. [Google Scholar]

- Campbell, D.; Slack, R. The Influence of mutual status on rates of corporate charitable contributions. J. Bus. Ethics 2007, 74, 191–200. [Google Scholar] [CrossRef]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef]

- Cowton, C.J. Corporate Philanthropy in the United Kingdom. J. Bus. Ethics 1987, 6, 553–558. [Google Scholar] [CrossRef]

- Useem, M. Market and institutional factors in corporate contributions. Calif. Manag. Rev. 1998, 30, 77–88. [Google Scholar] [CrossRef]

- Sharfman, M. Changing institutional rules: The evolution of corporate philanthropy, 1883–1953. Bus. Soc. 1994, 33, 236–269. [Google Scholar] [CrossRef]

- Andreoni, J. Giving with Impure Altruism: Applications to Charity and Ricardian Equivalence. J. Polit. Econ. 1989, 97, 1447–1458. [Google Scholar] [CrossRef]

- Shaw, B.; Post, F.R. A moral basis for corporate philanthropy. J. Bus. Ethics 1993, 12, 745–751. [Google Scholar] [CrossRef]

- Neiheisel, S.R. Corporate Strategy and the Politics of Goodwill: A Political Analysis of Corporate Philanthropy in America; Peter Lang: New York, NY, USA, 1994. [Google Scholar]

- File, K.M.; Prince, R.A. Cause related marketing and corporate philanthropy in the privately held enterprise. J. Bus. Ethics 1998, 17, 1529–1539. [Google Scholar] [CrossRef]

- Campbell, L.; Gulas, C.S.; Gruca, T.S. Corporate giving behavior and decision-maker social consciousness. J. Bus. Ethics 1999, 19, 375–383. [Google Scholar] [CrossRef]

- Valor, C. Why do managers give? Applying pro-social behaviour theory to understand firm giving. Int. Rev. Public Nonprofit Mark. 2006, 3, 17–28. [Google Scholar]

- Choi, J.; Wang, H. The promise of a managerial values approach to corporate philanthropy. J. Bus. Ethics 2007, 75, 345–359. [Google Scholar] [CrossRef]

- Mescon, T.S.; Tilson, D.J. Corporate Philanthropy: A Strategic Approach to the Bottom-Line. Calif. Manag. Rev. 1987, 29, 49–61. [Google Scholar] [CrossRef]

- Navarro, P. Why do corporations give to charity? J. Bus. Ethics 1988, 61, 65–93. [Google Scholar] [CrossRef]

- Haley, U.C.V. Corporate contributions as managerial masques: Reframing corporate contributions as strategies to influence society. J. Manag. Stud. 1991, 28, 485–510. [Google Scholar] [CrossRef]

- Collins, M. Corporate Philanthropy—Potential Threat or Opportunity? Bus. Ethics Eur. Rev. 1995, 4, 102–108. [Google Scholar] [CrossRef]

- Sanchez, C.M. Motives for corporate philanthropy in El Salvador: Altruism and political legitimacy. J. Bus. Ethics 2000, 27, 363–375. [Google Scholar] [CrossRef]

- Williams, R.J.; Barrett, J.D. Corporate philanthropy, criminal activity, and firm reputation: Is there a link? J. Bus. Ethics 2000, 26, 341–350. [Google Scholar] [CrossRef]

- Saiia, D.H.; Carroll, A.B.; Buchholtz, A.K. Philanthropy as strategy: When corporate charity “begins at home”. Bus Soc. 2003, 42, 169–201. [Google Scholar] [CrossRef]

- Patten, D.M. Does the Market Value Corporate Philanthropy? Evidence from the Response to the 2004 Tsunami Relief Effort. J. Bus. Ethics 2008, 81, 599–607. [Google Scholar]

- Gao, F.; Faff, R.; Navissi, F. Corporate Philanthropy: Insights from the 2008 Wenchuan Earthquake in China. Pac.-Basin Finance J. 2012, 20, 363–377. [Google Scholar] [CrossRef]

- Masulis, R.W.; Reza, S.W. Agency Problems of Corporate Philanthropy. Rev. Financ. Stud. 2015, 28, 592–636. [Google Scholar] [CrossRef]

- Xu, L.; Zhang, S.; Xu, P.; Liu, N.; Zhao, G.; Zhao, L. A Concealed Wrongdoing of Corporate Philanthropy: Evidence from China. Volunt. Int. J. Volunt. Nonprofit Organ. 2017, 28, 721–744. [Google Scholar] [CrossRef]

- Oh, W.-Y.; Chang, Y.K.; Lee, G.; Seo, J. Intragroup Transactions, Corporate Governance, and Corporate Philanthropy in Korean Business Groups. J. Bus. Ethics 2018, 153, 1031–1049. [Google Scholar] [CrossRef]

- Chen, J.; Dong, W.; Tong, J.; Zhang, F. Corporate Philanthropy and Tunneling: Evidence from China. J. Bus. Ethics 2018, 150, 135–157. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Du, S.L.; Bhattacharya, C.B.; Sen, S. Maximizing business returns to corporate social responsibility(csr): The role of csr communication. Int. J. Manag. Rev. 2010, 12, 8–19. [Google Scholar] [CrossRef]

- Bertrand, M.; Bombardini, M.; Fisman, R.; Trebbi, F. Tax-Exempt Lobbying: Corporate Philanthropy as a Tool for Political Influence. Am. Econ. Rev. 2020, 110, 2065–2102. [Google Scholar] [CrossRef]

- Li, S.; Song, X.; Wu, H. Political Connection, Ownership Structure, and Corporate Philanthropy in China: A Strategic-Political Perspective. J. Bus. Ethics 2015, 129, 399–411. [Google Scholar] [CrossRef]

- Zhang, J.; Marquis, C.; Qiao, K. Do Political Connections Buffer Firms from or Bind Firms to the Government? A Study of Corporate Charitable Donations of Chinese Firms. Organ. Sci. 2016, 27, 1307–1324. [Google Scholar]

- Zhang, M.; Ma, L.; Zhang, W. The political-enterprise bonding effect of corporate charitable giving—Empirical evidence based on listed companies in China. Manag. World. 2013, 7, 163–171. [Google Scholar]

- Jia, M.; Zhang, Z. The role of corporate donations in Chinese political markets. J. Bus. Ethics 2018, 153, 519–545. [Google Scholar] [CrossRef]

- Jia, M.; Zhang, Z. News Visibility and Corporate Philanthropic Response: Evidence from Privately Owned Chinese Firms Following the Wenchuan Earthquake. J. Bus. Ethics 2015, 129, 93–114. [Google Scholar] [CrossRef]

- Ritter, T.; Gemünden, H.G. Network Competence. J. Bus. Res. 2003, 56, 745–755. [Google Scholar] [CrossRef]

- Tambe, P.; Hitt, L.M.; Brynjolfsson, E. The Extroverted Firm: How External Information Practices Affect Innovation and Productivity. Manag. Sci. 2012, 58, 843–859. [Google Scholar] [CrossRef]

- Hillman, A.J.; Wan, W.P. The determinants of MNE subsidiaries’ political strategies: Evidence of institutional duality. J. Int. Bus. Stud. 2005, 36, 322–340. [Google Scholar] [CrossRef]

- Fuertes-Callén, Y.; Cuéllar-Fernández, B. What Is the Role of Commercialisation and Reputation in Product Innovation Success? Innovation 2014, 16, 96–105. [Google Scholar] [CrossRef]

- Keshta, M.S.; Talla, S.A.E.; Shobaki, M.J.A.; Abu-Naser, S.S. Perceived Organizational Reputation and Its Impact on Achieving Strategic Innovation. Corp. Reput. Rev. 2020, 4, 27. [Google Scholar]

- Flipse, S.M.; Osseweijer, P. Media Attention to GM Food Cases: An Innovation Perspective. Public Underst. Sci. 2013, 22, 185–202. [Google Scholar] [CrossRef] [PubMed]

- Mount, M.; Martinez, M.G. Social Media: A Tool for Open Innovation. Calif. Manag. Rev. 2014, 56, 124–143. [Google Scholar] [CrossRef]

- Bhimani, H.; Mention, A.-L.; Barlatier, P.-J. Social Media and Innovation: A Systematic Literature Review and Future Research Directions. Technol. Forecast. Soc. Change 2019, 144, 251–269. [Google Scholar] [CrossRef]

- Bourgeois, L.J. On the Measurement of Organizational Slack. Acad. Manag. Rev. 1981, 6, 29–39. [Google Scholar] [CrossRef]

- Collis, D.J. A resource-based analysis of global competition: The case of the bearings industry. Strateg. Manag. J. 1991, 12, 49–68. [Google Scholar] [CrossRef]

- Tan, J.; Peng, M.W. Organizational Slack and Firm Performance During Economic Transitions: Two Studies from an Emerging Economy. SSRN Electron. J. 2003, 24, 1249–1263. [Google Scholar]

- Morrison, P.D.; Roberts, J.H.; von Hippel, E. Determinants of User Innovation and Innovation Sharing in a Local Market. Manag. Sci. 2000, 46, 1513–1527. [Google Scholar] [CrossRef]

- Geiger, S.W.; Cashen, L.H. A Multidimensional Examination Of Slack And Its Impact On Innovation. J. Manag. Issue 2002, 18, 68–84. [Google Scholar]

- Choi, M.; Hong, S. Another Form of Greenwashing: The Effects of Chaebol Firms’ Corporate Governance Performance on the Donations. Sustainability 2022, 14, 3373. [Google Scholar] [CrossRef]

- Chen, L.-M.; Yang, S.-J.S. Are Purchase-Triggered Donations Advantageous with Competition? J. Oper. Res. Soc. 2017, 68, 237–252. [Google Scholar] [CrossRef]

- Schulze, D.; Heinitz, K.; Lorenz, T. Comparative Organizational Research Starts with Sound Measurement: Validity and Invariance of Turker’s Corporate Social Responsibility Scale in Five Cross-Cultural Samples. PLoS ONE 2018, 13, e0207331. [Google Scholar] [CrossRef]

- Walker, M.; Kent, A. Consumer Perceptions of Strategic Corporate Philanthropy in the Sport Industry. Res. Q. Exerc. Sport. 2008, 79, A100. [Google Scholar]

- Wakefield, T.; Glantz, S.A.; Apollonio, D.E. Content Analysis of the Corporate Social Responsibility Practices of 9 Major Cannabis Companies in Canada and the US. Jama Netw. Open. 2022, 5, e2228088. [Google Scholar] [CrossRef]

- de-Miguel-Molina, B.; Chirivella-Gonzalez, V.; Garcia-Ortega, B. Corporate Philanthropy and Community Involvement. Analysing Companies from France, Germany, the Netherlands and Spain. Qual. Quant. 2016, 50, 2741–2766. [Google Scholar] [CrossRef]

- Shah, N.K. Corporate Philanthropy and Conflicts of Interest in Public Health: ExxonMobil, Equatorial Guinea, and Malaria. J. Public Health Policy 2013, 34, 121–136. [Google Scholar] [CrossRef] [PubMed]

- Yu, H.-C.; Kuo, L. Corporate Philanthropy Strategy and Sustainable Development Goals. Sustainability 2021, 13, 5655. [Google Scholar] [CrossRef]

- Fooks, G.J.; Gilmore, A.B. Corporate Philanthropy, Political Influence, and Health Policy. PLoS ONE 2013, 8, e80864. [Google Scholar] [CrossRef]

- Packer, H.; Swartz, W.; Ota, Y.; Bailey, M. Corporate Social Responsibility (CSR) Practices of the Largest Seafood Suppliers in the Wild Capture Fisheries Sector: From Vision to Action. Sustainability 2019, 11, 2254. [Google Scholar] [CrossRef]

- Nazri, M.A.; Omar, N.A.; Aman, A.; Ayob, A.H.; Ramli, N.A. Corporate Social Responsibility and Business Performance in Takaful Agencies: The Moderating Role of Objective Environment. Sustainability 2020, 12, 8291. [Google Scholar] [CrossRef]

- Ji, H.; Miao, Z. Corporate Social Responsibility and Collaborative Innovation: The Role of Government Support. J. Clean. Prod. 2020, 260, 121028. [Google Scholar] [CrossRef]

- Walzel, S.; Robertson, J.; Anagnostopoulos, C. Corporate Social Responsibility in Professional Team Sports Organizations: An Integrative Review. J. Sport Manag. 2018, 32, 511–530. [Google Scholar] [CrossRef]

- Cheruiyot-Koech, R.; Reddy, C.D. Corporate Social Responsibility Preferences in South Africa. Sustainability 2022, 14, 3792. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Shao, Y.; Gao, S. CSR and Firm Value: Evidence from China. Sustainability 2018, 10, 4597. [Google Scholar] [CrossRef]

- Inoue, Y.; Kent, A.; Lee, S. CSR and the Bottom Line: Analyzing the Link Between CSR and Financial Performance for Professional Teams. J. Sport Manag. 2011, 25, 531–549. [Google Scholar] [CrossRef]

- Ali, W.; Wilson, J.; Husnain, M. Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature. Sustainability 2022, 14, 3474. [Google Scholar] [CrossRef]

- Xiong, C.; Zhang, K.; Zhao, X. Do Political Ties Cause Over-Investment in Corporate Social Responsibility? Empirical Evidence from Chinses Private Firms. Sustainability 2020, 12, 7203. [Google Scholar]

- Yen, G.-F.; Yang, H.-T. Does Consumer Empathy Influence Consumer Responses to Strategic Corporate Social Responsibility? The Dual Mediation of Moral Identity. Sustainability 2018, 10, 1812. [Google Scholar]

- Wang, K.; Miao, Y.; Su, C.-H.; Chen, M.-H.; Wu, Z.; Wang, T. Does Corporate Charitable Giving Help Sustain Corporate Performance in China? Sustainability 2019, 11, 1491. [Google Scholar] [CrossRef]

- Li, W.; Lu, Y.; Li, W. Does CSR Action Provide Insurance-Like Protection to Tax-Avoiding Firms? Evidence from China. Sustainability 2019, 11, 5297. [Google Scholar] [CrossRef]

- Deng, X.; Long, X. Financial Performance Gaps and Corporate Social Responsibility. Sustainability 2019, 11, 3438. [Google Scholar] [CrossRef]

- Werner, T. Gaining Access by Doing Good: The Effect of Sociopolitical Reputation on Firm Participation in Public Policy Making. Manag. Sci. 2015, 61, 1989–2011. [Google Scholar] [CrossRef]

- Yang, D.; Babiak, K. How League and Community Affect Corporate Philanthropy in Professional Sport: A Multiple Field Embeddedness Perspective. J. Sport Manag. 2021, 35, 395–406. [Google Scholar] [CrossRef]

- Singh, P.J.; Sethuraman, K.; Lam, J.Y. Impact of Corporate Social Responsibility Dimensions on Firm Value: Some Evidence from Hong Kong and China. Sustainability 2017, 9, 1532. [Google Scholar] [CrossRef]

- Ahen, F.; Amankwah-Amoah, J. Institutional Voids and the Philanthropization of CSR Practices: Insights from Developing Economies. Sustainability 2018, 10, 2400. [Google Scholar] [CrossRef]

- Jones, P.; Comfort, D.; Hillier, D. Marketing and Corporate Social Responsibility within Food Stores. Br. Food J. 2007, 109, 582–593. [Google Scholar] [CrossRef]

- Qiao, L.; Wu, J. Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums. Sustainability 2019, 11, 1291. [Google Scholar] [CrossRef]

- Singh, J.; Teng, N.; Netessine, S. Philanthropic Campaigns and Customer Behavior: Field Experiments on an Online Taxi Booking Platform. Manag. Sci. 2019, 65, 913–932. [Google Scholar] [CrossRef]

- Wang, C.; Zhou, H.; Zhang, Y.; Liu, L. Promotion Pathways of Financial Performance: A Configuration Analysis of Corporate Social Responsibility Based on a Fuzzy Set Qualitative Comparative Analysis Approach. IEEE Access. 2022, 10, 10970–10982. [Google Scholar] [CrossRef]

- Gneezy, A.; Gneezy, U.; Nelson, L.D.; Brown, A. Shared Social Responsibility: A Field Experiment in Pay-What-You-Want Pricing and Charitable Giving. Science 2010, 329, 325–327. [Google Scholar] [CrossRef] [PubMed]

- Hou, X.; Wang, B.; Gao, Y. Stakeholder Protection, Public Trust, and Corporate Social Responsibility: Evidence from Listed SMEs in China. Sustainability 2020, 12, 6085. [Google Scholar] [CrossRef]

- Hategan, C.-D.; Curea-Pitorac, R.-I. Testing the Correlations between Corporate Giving, Performance and Company Value. Sustainability 2017, 9, 1210. [Google Scholar] [CrossRef]

- Shou, Y.; Shao, J.; Wang, W.; Lai, K. The Impact of Corporate Social Responsibility on Trade Credit: Evidence from Chinese Small and Medium-Sized Manufacturing Enterprises. Int. J. Prod. Econ. 2020, 230, 107809. [Google Scholar] [CrossRef]

- Grassmann, M. The Relationship between Corporate Social Responsibility Expenditures and Fi Rm Value: The Moderating Role of Integrated Reporting. J. Clean. Prod. 2021, 285, 124840. [Google Scholar] [CrossRef]

- Zheng, Q.; Lin, D. Top Management Team Stability and Corporate Social Responsibility: The Moderating Effects of Performance Aspiration Gap and Organisational Slack. Sustainability 2021, 13, 13972. [Google Scholar] [CrossRef]

- Zhang, J.; Han, J.; Yin, M. A Female Style in Corporate Social Responsibility? Evidence from Charitable Donations. Int. J. Discl. Gov. 2018, 15, 185–196. [Google Scholar] [CrossRef]

- Bassi, V.; Huck, S.; Rasul, I. A Note on Charitable Giving by Corporates and Aristocrats: Evidence from a Field Experiment. J. Behav. Exp. Econ. 2017, 66, 104–111. [Google Scholar] [CrossRef][Green Version]

- Douglas Beets, S.; Beets, M.G. An Absence of Transparency: The Charitable and Political Contributions of US Corporations. J. Bus. Ethics 2019, 155, 1101–1113. [Google Scholar] [CrossRef]

- Feicht, R.; Grimm, V.; Seebauer, M. An Experimental Study of Corporate Social Responsibility through Charitable Giving in Bertrand Markets. J. Econ. Behav. Organ. 2016, 124, 88–101. [Google Scholar] [CrossRef]

- Wang, J.; Coffey, B.S. Board Composition and Corporate Philanthropy. J. Bus. Ethics 1992, 11, 771–778. [Google Scholar] [CrossRef]

- Buchholtz, A.K.; Amason, A.C.; Rutherford, M.A. Beyond Resources: The Mediating Effect of Top Management Discretion and Values on Corporate Philanthropy. Bus. Soc. 1999, 38, 167–187. [Google Scholar] [CrossRef]

- Epstein, E.M. Business Ethics, Corporate Good Citizenship and the Corporate Social Policy Process: A View from the United States. J. Bus. Ethics 1989, 8, 583–595. [Google Scholar] [CrossRef]

- Kim, B.; Pae, J.; Yoo, C.-Y. Business Groups and Tunneling: Evidence from Corporate Charitable Contributions by Korean Companies. J. Bus. Ethics 2019, 154, 643–666. [Google Scholar] [CrossRef]

- Michalos, B.L. Canadian Corporate Charitable Contributions: Trends and Policies. Soc. Indic. Res. 1981, 9, 127–153. [Google Scholar] [CrossRef]

- Varadarajan, P.R.; Menon, A. Cause-Related Marketing: A Coalignment of Marketing Strategy and Corporate Philanthropy. J. Mark. 1988, 52, 58–74. [Google Scholar] [CrossRef]

- Atkinson, A.B.; Backus, P.G.; Micklewright, J.; Pharoah, C.; Schnepf, S.V. Charitable Giving for Overseas Development: UK Trends over a Quarter Century: Charitable Giving for Overseas Development. J. R. Stat. Soc. Ser. A Stat. Soc. 2012, 175, 167–190. [Google Scholar] [CrossRef]

- Krawczyk, K.; Wooddell, M.; Dias, A. Charitable Giving in Arts and Culture Nonprofits: The Impact of Organizational Characteristics. Nonprofit Volunt. Sect. Q. 2017, 46, 817–836. [Google Scholar] [CrossRef]

- Dienhart, J.W. Charitable Investments: A Strategy for Improving the Business Environment. J. Bus. Ethics 1988, 7, 63–71. [Google Scholar] [CrossRef]

- Fenclova, E.; Coles, T. Charitable Partnerships among Travel and Tourism Businesses: Perspectives from Low-Fares Airlines: Charitable Partnerships among Travel and Tourism Businesses. Int. J. Tour. Res. 2011, 13, 337–354. [Google Scholar] [CrossRef]

- Fehrler, S.; Przepiorka, W. Choosing a Partner for Social Exchange: Charitable Giving as a Signal of Trustworthiness. J. Econ. Behav. Organ. 2016, 129, 157–171. [Google Scholar] [CrossRef]

- Hoi, C.K.; Wu, Q.; Zhang, H. Community Social Capital and Corporate Social Responsibility. J. Bus. Ethics 2018, 152, 647–665. [Google Scholar] [CrossRef]

- Bae, J.; Cameron, G.T. Conditioning Effect of Prior Reputation on Perception of Corporate Giving. Public Relat. Rev. 2006, 32, 144–150. [Google Scholar] [CrossRef]

- Lee, M.-D.P. Configuration of External Influences: The Combined Effects of Institutions and Stakeholders on Corporate Social Responsibility Strategies. J. Bus. Ethics 2011, 102, 281–298. [Google Scholar] [CrossRef]

- Campbell, D.; Slack, R. Corporate “Philanthropy Strategy” and “Strategic Philanthropy”: Some Insights From Voluntary Disclosures in Annual Reports. Bus. Soc. 2008, 47, 187–212. [Google Scholar] [CrossRef]

- Weinblatt, J. Corporate Charitable Contributions to Not-for-Profit Organizations in Israel. Nonprofit Manag. Leadersh. 1992, 3, 183–198. [Google Scholar] [CrossRef]

- Chen, C.J.; Patten, D.M.; Roberts, R.W. Corporate Charitable Contributions: A Corporate Social Performance or Legitimacy Strategy? J. Bus. Ethics 2008, 82, 131–144. [Google Scholar] [CrossRef]

- Yoo, C.-Y.; Pae, J. Corporate Charitable Contributions: Business Award Winners’ Giving Behaviors. Bus. Ethics Eur. Rev. 2016, 25, 25–44. [Google Scholar] [CrossRef]

- Brammer, S.J.; Pavelin, S.; Porter, L.A. Corporate Charitable Giving, Multinational Companies and Countries of Concern. J. Manag. Stud. 2009, 46, 575–596. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Corporate Community Contributions in the United Kingdom and the United States. J. Bus. Ethics 2005, 56, 15–26. [Google Scholar] [CrossRef]

- Fry, L.W.; Keim, G.D.; Meiners, R.E. Corporate Contributions: Altruistic or For-Profit? Acad. Manag. J. 1982, 25, 94–106. [Google Scholar] [CrossRef]

- Cho, M.; Kelly, K.S. Corporate Donor–Charitable Organization Partners: A Coorientation Study of Relationship Types. Nonprofit Volunt. Sect. Q. 2014, 43, 693–715. [Google Scholar] [CrossRef]

- Sargeant, A.; Stephenson, H. Corporate Giving: Targeting the Likely Donor: Corporate Giving: Targeting the Likely Donor. Int. J. Nonprofit Volunt. Sect. Mark. 1997, 2, 64–79. [Google Scholar] [CrossRef]

- Webb, N.J.; Farmer, A. CORPORATE GOODWILL: A Game Theoretic Approach to the Effect of Corporate Charitable Expenditures on Firm Behaviour. Ann. Public Coop. Econ. 1996, 67, 29–50. [Google Scholar] [CrossRef]

- Zhang, R.; Rezaee, Z.; Zhu, J. Corporate Philanthropic Disaster Response and Ownership Type: Evidence from Chinese Firms’ Response to the Sichuan Earthquake. J. Bus. Ethics 2010, 91, 51–63. [Google Scholar] [CrossRef]

- Zhang, R.; Zhu, J.; Yue, H.; Zhu, C. Corporate Philanthropic Giving, Advertising Intensity, and Industry Competition Level. J. Bus. Ethics 2010, 94, 39–52. [Google Scholar] [CrossRef]

- Hogarth, K.; Hutchinson, M.; Scaife, W. Corporate Philanthropy, Reputation Risk Management and Shareholder Value: A Study of Australian Corporate Giving. J. Bus. Ethics 2018, 151, 375–390. [Google Scholar] [CrossRef]

- Stendardi, E.J. Corporate Philanthropy: The Redefinition of Enlightened Self-Interest. Soc. Sci. J. 1992, 29, 21–30. [Google Scholar] [CrossRef]

- Cooper, M.J.; Gulen, H.; Ovtchinnikov, A.V. Corporate Political Contributions and Stock Returns. J. Finance 2010, 65, 687–724. [Google Scholar] [CrossRef]

- Webb, N.J. Corporate Profits and Social Responsibility: “Subsidization” of Corporate Income under Charitable Giving Tax Laws. J. Econ. Bus. 1996, 48, 401–421. [Google Scholar] [CrossRef]

- Jamali, D.; Mirshak, R. Corporate Social Responsibility (CSR): Theory and Practice in a Developing Country Context. J. Bus. Ethics 2007, 72, 243–262. [Google Scholar] [CrossRef]

- Brønn, P.S.; Vrioni, A.B. Corporate Social Responsibility and Cause-Related Marketing: An Overview. Int. J. Advert. 2001, 20, 207–222. [Google Scholar] [CrossRef]

- Becchetti, L.; Di Giacomo, S.; Pinnacchio, D. Corporate Social Responsibility and Corporate Performance: Evidence from a Panel of US Listed Companies. Appl. Econ. 2008, 40, 541–567. [Google Scholar] [CrossRef]

- Mishra, S.; Modi, S.B. Corporate Social Responsibility and Shareholder Wealth: The Role of Marketing Capability. J. Mark. 2016, 80, 26–46. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Corporate Social Responsibility and the Environment: A Theoretical Perspective. Rev. Environ. Econ. Policy 2008, 2, 240–260. [Google Scholar] [CrossRef]

- Kim, S.-Y.; Park, H. Corporate Social Responsibility as an Organizational Attractiveness for Prospective Public Relations Practitioners. J. Bus. Ethics 2011, 103, 639–653. [Google Scholar] [CrossRef]

- Knudsen, S. Corporate Social Responsibility in Local Context: International Capital, Charitable Giving and the Politics of Education in Turkey. Southeast Eur. Black Sea Stud. 2015, 15, 369–390. [Google Scholar] [CrossRef]

- Reinhardt, F.L.; Stavins, R.N.; Vietor, R.H.K. Corporate Social Responsibility Through an Economic Lens. Rev. Environ. Econ. Policy 2008, 2, 219–239. [Google Scholar] [CrossRef]

- Vlachos, P.A.; Tsamakos, A.; Vrechopoulos, A.P.; Avramidis, P.K. Corporate Social Responsibility: Attributions, Loyalty, and the Mediating Role of Trust. J. Acad. Mark. Sci. 2009, 37, 170–180. [Google Scholar] [CrossRef]

- Whitehouse, L. Corporate Social Responsibility: Views from the Frontline. J. Bus. Ethics 2006, 63, 279–296. [Google Scholar] [CrossRef]

- Bennett, C.M.; Kim, H.; Loken, B. Corporate Sponsorships May Hurt Nonprofits: Understanding Their Effects on Charitable Giving. J. Consum. Psychol. 2013, 23, 288–300. [Google Scholar] [CrossRef]

- Ye, K.; Zhang, R. Do Lenders Value Corporate Social Responsibility? Evidence from China. J. Bus. Ethics 2011, 104, 197–206. [Google Scholar] [CrossRef]

- Gao, Y.; Hafsi, T. Does Charitable Giving Substitute or Complement Firm Differentiation Strategy? Evidence from Chinese Private SMEs. Eur. Manag. Rev. 2019, 16, 633–646. [Google Scholar] [CrossRef]

- Bartkus, B.R.; Morris, S.A.; Seifert, B. Governance and Corporate Philanthropy: Restraining Robin Hood? Bus. Soc. 2002, 41, 319–344. [Google Scholar] [CrossRef]

- Seifert, B.; Morris, S.A.; Bartkus, B.R. Having, Giving, and Getting: Slack Resources, Corporate Philanthropy, and Firm Financial Performance. Bus. Soc. 2004, 43, 135–161. [Google Scholar] [CrossRef]

- Reichert, B.E.; Sohn, M. How Corporate Charitable Giving Reduces the Costs of Formal Controls. J. Bus. Ethics 2022, 176, 689–704. [Google Scholar] [CrossRef]

- Campbell, J.L. Institutional Analysis and the Paradox of Corporate Social Responsibility. Am. Behav. Sci. 2006, 49, 925–938. [Google Scholar] [CrossRef]

- Koehn, D.; Ueng, J. Is Philanthropy Being Used by Corporate Wrongdoers to Buy Good Will? J. Manag. Gov. 2010, 14, 1. [Google Scholar] [CrossRef]

- Jones, J.C.H.; Laudadio, L. Market Structure and Corporate Charitable Donations: Some Canadian Evidence for 1976 and 1981. Appl. Econ. 1991, 23, 1237–1244. [Google Scholar] [CrossRef]

- Ricks, J.M.; Peters, R.C. Motives, Timing, and Targets of Corporate Philanthropy: A Tripartite Classification Scheme of Charitable Giving: Business and Society Review. Bus. Soc. Rev. 2013, 118, 413–436. [Google Scholar] [CrossRef]

- Mullen, J. Performance-Based Corporate Philanthropy: How “Giving Smart” Can Further Corporate Goals. Public Relat. Q. 1997, 42, 42–48. [Google Scholar]

- Wang, H.; Zhang, Y.; Tian, M.; Wang, Z.; Ding, Y. Promoting and Inhibiting: Corporate Charitable Donations and Innovation Investment under Different Motivation Orientations—Evidence from Chinese Listed Companies. PLoS ONE 2022, 17, e0266199. [Google Scholar] [CrossRef] [PubMed]

- Campbell, D.; Slack, R. Public Visibility as a Determinant of the Rate of Corporate Charitable Donations. Bus. Ethics Eur. Rev. 2006, 15, 19–28. [Google Scholar] [CrossRef]

- Tilcsik, A.; Marquis, C. Punctuated Generosity: How Mega-Events and Natural Disasters Affect Corporate Philanthropy in U. S. Communities. Adm. Sci. Q. 2013, 58, 111–148. [Google Scholar] [CrossRef]

- Du, X.; Jian, W.; Du, Y.; Feng, W.; Zeng, Q. Religion, the Nature of Ultimate Owner, and Corporate Philanthropic Giving: Evidence from China. J. Bus. Ethics 2014, 123, 235–256. [Google Scholar] [CrossRef]

- Amato, L.H.; Amato, C.H. Retail Philanthropy: Firm Size, Industry, and Business Cycle. J. Bus. Ethics 2012, 107, 435–448. [Google Scholar] [CrossRef]

- Cuypers, I.R.P.; Koh, P.-S.; Wang, H. Sincerity in Corporate Philanthropy, Stakeholder Perceptions and Firm Value. Organ. Sci. 2016, 27, 173–188. [Google Scholar] [CrossRef]

- Crampton, W.; Patten, D. Social Responsiveness, Profitability and Catastrophic Events: Evidence on the Corporate Philanthropic Response to 9/11. J. Bus. Ethics 2008, 81, 863–873. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Stakeholder Pressure, Organizational Size, and the Allocation of Departmental Responsibility for the Management of Corporate Charitable Giving. Bus. Soc. 2004, 43, 268–295. [Google Scholar] [CrossRef]

- Arya, A.; Mittendorf, B. Supply Chain Consequences of Subsidies for Corporate Social Responsibility. Prod. Oper. Manag. 2015, 24, 1346–1357. [Google Scholar] [CrossRef]

- Boatsman, J.R.; Gupta, S. Taxes and corporate charity: Empirical evidence from microlevel panel data. Natl. Tax J. 1996, 49, 193–213. [Google Scholar] [CrossRef]

- Carroll, R.; Joulfaian, D. Taxes and Corporate Giving to Charity. Public Finance Rev. 2005, 33, 300–317. [Google Scholar] [CrossRef]

- Werbel, J.D.; Carter, S.M. The CEO’s Influence on Corporate Foundation Giving. J. Bus. Ethics 2002, 40, 47–60. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. The Development of Corporate Charitable Contributions in the UK: A Stakeholder Analysis. J. Manag. Stud. 2004, 41, 1411–1434. [Google Scholar] [CrossRef]

- Meijer, M.-M. The Effects of Charity Reputation on Charitable Giving. Corp. Reput. Rev. 2009, 12, 33–42. [Google Scholar] [CrossRef]

- Amato, L.H.; Amato, C.H. The Effects of Firm Size and Industry on Corporate Giving. J. Bus. Ethics 2007, 72, 229–241. [Google Scholar] [CrossRef]

- Peng, S.; Kim, M.; Deat, F. The Effects of Nonprofit Reputation on Charitable Giving: A Survey Experiment. Volunt. Int. J. Volunt. Nonprofit Organ. 2019, 30, 811–827. [Google Scholar] [CrossRef]

- Levy, F.K.; Shatto, G.M. The Evaluation of Corporate Contributions. Public Choice 1978, 33, 19–28. [Google Scholar] [CrossRef]

- Epstein, M.J. The Fall of Corporate Charitable Contributions. Public Relat. Q. 1993, 38, 37. [Google Scholar]

- Chen, M.-H.; Lin, C.-P. The Impact of Corporate Charitable Giving on Hospitality Firm Performance: Doing Well by Doing Good? Int. J. Hosp. Manag. 2015, 47, 25–34. [Google Scholar] [CrossRef] [PubMed]

- Kabongo, J.D.; Chang, K.; Li, Y. The Impact of Operational Diversity on Corporate Philanthropy: An Empirical Study of U. S. Companies. J. Bus. Ethics 2013, 116, 49–65. [Google Scholar] [CrossRef]

- Gan, A. The Impact of Public Scrutiny on Corporate Philanthropy. J. Bus. Ethics 2006, 69, 217–236. [Google Scholar] [CrossRef]

- Venable, B.T. The Role of Brand Personality in Charitable Giving: An Assessment and Validation. J. Acad. Mark. Sci. 2005, 33, 295–312. [Google Scholar] [CrossRef]

- Walker, M.; Kent, A. The Roles of Credibility and Social Consciousness in the Corporate Philanthropy-Consumer Behavior Relationship. J. Bus. Ethics 2013, 116, 341–353. [Google Scholar] [CrossRef]

- Chai, K.-C.; Zhu, J.; Lan, H.-R.; Lu, Y.; Chang, K.-C. The Spillover Effects of Corporate Giving in China: Effects of Enterprise Charitable Giving and Exposure on Enterprise Performance. Appl. Econ. 2022, 7, 1–9. [Google Scholar] [CrossRef]

- Campbell, D.; Slack, R. The Strategic Use of Corporate Philanthropy: Building Societies and Demutualisation Defences. Bus. Ethics Eur. Rev. 2007, 16, 326–343. [Google Scholar] [CrossRef]

- Leslie, L.M.; Snyder, M.; Glomb, T.M. Who Gives? Multilevel Effects of Gender and Ethnicity on Workplace Charitable Giving. J. Appl. Psychol. 2013, 98, 49–62. [Google Scholar] [CrossRef]

- Bernardi, R.A.; Threadgill, V.H. Women Directors and Corporate Social Responsibility. EJBO Electron. J. Bus. Ethics Organ. Stud. 2010, 15, 15–21. [Google Scholar]

- Williams, R.J. Women on Corporate Boards of Directors and Their Influence on Corporate Philanthropy. J. Bus. Ethics 2003, 42, 1–10. [Google Scholar] [CrossRef]

- Ohreen, D.E.; Petry, R.A. Imperfect Duties and Corporate Philanthropy: A Kantian Approach. J. Bus. Ethics 2012, 106, 367–381. [Google Scholar] [CrossRef]

- Liket, K.; Simaens, A. Battling the Devolution in the Research on Corporate Philanthropy. J. Bus. Ethics 2015, 126, 285–308. [Google Scholar] [CrossRef]

- Su, J.; He, J. Does Giving Lead to Getting? Evidence from Chinese Private Enterprises. J. Bus. Ethics 2010, 93, 73–90. [Google Scholar] [CrossRef]

- Muller, A.; Whiteman, G. Exploring the Geography of Corporate Philanthropic Disaster Response: A Study of Fortune Global 500 Firms. J. Bus. Ethics 2009, 84, 589–603. [Google Scholar] [CrossRef]

- Halme, M.; Laurila, J. Philanthropy, Integration or Innovation? Exploring the Financial and Societal Outcomes of Different Types of Corporate Responsibility. J. Bus. Ethics 2009, 84, 325–339. [Google Scholar] [CrossRef]

- Wang, H.; Choi, J.; Li, J. Too Little or Too Much? Untangling the Relationship Between Corporate Philanthropy and Firm Financial Performance. Organ. Sci. 2008, 19, 143–159. [Google Scholar] [CrossRef]

- Haruvy, E.; Popkowski Leszczyc, P.T.L. Bidder Motives in Cause-Related Auctions. Int. J. Res. Mark. 2009, 26, 324–331. [Google Scholar] [CrossRef]

| Author(s) | Technique and Approach | Key Findings |

|---|---|---|

| Bereskin et al. (2016) [4] | Empirical Analysis | Direct-giving activities are positively associated both with higher levels of innovation and innovation that is more influential, collaborative, and original. |

| Zhang et al. (2016) [3] | Empirical Analysis | Charitable giving has a significant inverted U-curve predictive effect on innovation performances. |

| Bereskin and Hsu (2016) [5] | Empirical Analysis | Direct giving is associated with obtaining patents that have the potential to expand the companies’ expertise and range of investment opportunities. |

| Jiang et al. (2018) [17] | Empirical Analysis | There is an obviously positive correlation between philanthropic donations and innovation performance, which will be affected by the scale of the enterprise. |

| Chen and Zhou (2018) [18] | Empirical Analysis | There is a significant positive relationship between the amount of corporate charitable giving and the innovative-output performance of the firm. |

| Ou et al. (2021) [19] | Empirical Analysis | Media attention from charitable giving promotes corporate innovation in terms of both innovation intentions and innovation resources, by strengthening long-term strategic orientation for corporate development and attracting more technological resources. |

| Research Theme: Concept | |

|---|---|

| Level of Analysis | Key Ideas |

| The altruism of corporate charitable giving | Altruistic motives are the main reason for corporate charitable giving. (Cowton 1987) [22] The altruistic model of corporate philanthropy is considered to be a non-strategic interpretation of corporate giving. Companies use social standards as the basis for correct, good and just social action. Firms engage in altruistic philanthropy with the single goal of helping others. (Useem 1988; Sharfman 1994) [23,24] One possible motivation is that a person actually prefers the public benefit provided by the donation. In this case, the money belonging to the charity has a utility (or reward value) that is independent of the individual’s contribution. This preference for public goods can be considered “altruism”, and if this is the only motivation for the donation, the behavior is called “pure altruism”. (Andreoni 1989) [25] There is an ethical element to the decision to engage in corporate philanthropy that cannot be ignored. (Shaw and Post 1993) [26] Despite its noble goals, the altruistic model itself is often not a strong explanation for corporate philanthropy, even in the most diverse societies, which is because it ignores the profit maximization goals and other strategic objectives of corporations. (Neiheisel 1994) [27] Corporate philanthropy can be driven by factors such as the sense of aesthetic pleasure. (File and Prince 1998) [28] The study shows that firms who have a history of giving to charity cite altruistic motives for their behavior. (Campbell et al., 1999) [29] Pro-social behavior theorists claim that managers’ behavior is also motivated by ethical norms, which is a strong reason for corporate giving. (Valor 2006) [30] Corporate philanthropy may be the result of top management’s values of benevolence and integrity. (Choi and Wang 2007) [31] |

| The strategic nature of corporate charitable giving | Many companies which have a strong sense of corporate social responsibility, however, are turning away from traditional giving and toward a more market-driven strategic management, bottom-line approach to philanthropy. (Mescon and Tilson 1987) [32] |

| The strategic nature of corporate charitable giving | Profit maximization is an important motivation driving corporate charitable giving. (Navarro 1988) [33] Managers use corporate philanthropy to promote management and corporate interests. (Haley 1991) [34] From a strategic perspective, corporate philanthropy can be further divided into economic or political dimensions. (Neiheisel 1994; Young and Burlingame 1996) [9,27] When companies engage in philanthropy in a more strategic and professional way, they can not only do work that has a greater impact on society, but they can also create tangible and intangible benefits for themselves in terms of goodwill, employee morale and public support. (Collins 1995) [35] Firms engage in philanthropic activities as a means of improving the financial performance of their organizations. (Sanchez 2000) [36] While corporate violations of environmental and labor regulations can reduce their public image, charitable giving can reduce the extent of the decline. (Williams and Barrett 2000) [37] Corporate philanthropy has a positive impact on corporate financial performance because decisions about charitable giving can strategically enhance a firm’s image and reputation (Porter and Kramer 2002; Godfrey 2005) [16,21] Firms are becoming increasingly strategic in their philanthropic activities. (Saiia et al., 2003) [38] Some companies are increasingly emphasizing corporate charitable giving as a strategic tool. (Patten 2008) [39] High social sentiment and politically-related economic motivations should trigger a more efficient market reaction to corporate philanthropic involvement, which could then address more directly and effectively the strategic motivation and the “insurance-like” protection property of reputational capital behind corporate philanthropy. (Gao et al., 2012) [40] Managed rent withdrawals are motivated as corporate donations. (Masulis and Reza 2015) [41] Corporate reputation effects emphasize on altruistic motivation, while strategic philanthropy focuses more on egoism. (Xu et al., 2017) [42] Corporate decisions to be charitable are not based solely on purely philanthropic motives, but depend more on the source of revenue. (Oh et al., 2018) [43] When controlling shareholders intend to transfer wealth out of the company, they may use the company’s resources for charitable giving. (Chen et al., 2018) [44] |

| Category | Author(s) | Technique and Approach | Conclusion |

|---|---|---|---|

| Technological Network | Bereskin and Hsu (2016) [5] | Empirical Analysis | Direct giving is associated with obtaining patents that have the potential to expand the companies’ expertise and range of investment opportunities. |

| Wang (2011) [6] | Empirical Analysis | The positive philanthropy–performance relationship is stronger for firms with greater public visibility and for those with better past performance. | |

| Political Reputation | Godfrey (2005) [21] | Literature Review | Corporate philanthropy can generate positive moral capital among communities and stakeholders. Moral capital can provide shareholders with insurance-like protection for a firm’s relationship-based intangible assets. |

| Chen et al. (2018) [44] | Empirical Analysis | The negative association between philanthropy and tunneling is stronger when firms are faced with more severe agency conflicts, as indicated by lower largest-shareholding, fewer growth opportunities, lower state-ownership, and weaker product-market competition. | |

| Campbell and Slack (2007) [20] | Empirical Analysis | Individual societies privilege local (to themselves) causes over others when it comes to the distribution of charitable and community donations. | |

| Bertrand et al. (2020) [47] | Empirical Analysis | In the absence of disclosure requirements, charitable giving may be a form of corporate political-influence undetected by voters and subsidized by taxpayers. | |

| Li et al. (2015) [48] | Empirical Analysis | A significant and positive relationship between political connections and the likelihood and extent of firm contributions. A stronger relationship between political connections and corporate philanthropy in non-state-owned firms. | |

| Zhang et al. (2016) [49] | Empirical Analysis | Firms whose executives have ascribed bureaucratic connections are more likely to use their connections as a buffer from governmental donation-pressure. | |

| Zhang et al. (2013) [50] | Empirical Analysis | The government–enterprise bonding effect of charitable giving is more pronounced among state-owned corporations than among non-state-owned corporations. | |

| Media Attention | Jia and Zhang (2018) [51] | Empirical Analysis | Firms that make generous donations at the beginning of a new city secretary’s tenure receive more attention from representatives of new local leaders, especially firms that were politically disadvantaged under a predecessor’s governance. |

| Ou et al. (2021) [19] | Empirical Analysis | Media attention from charitable giving promotes corporate innovation in terms of both innovation intentions and innovation resources, by strengthening long-term strategic orientation for corporate development and attracting more technological resources. | |

| Jia and Zhang (2015) [52] | Empirical Analysis | Corporations that are highly visible in the news media are more likely to engage in CPR and donate more money. | |

| Resource Regulation | Chen and Zhou (2018) [18] | Empirical Analysis | There is a significant positive relationship between the amount of corporate charitable giving and the innovative-output performance of the firm. |

| Cha (2021) [11] | Literature Review | The underlying mechanisms of corporate philanthropy–firm performance relationship. |

| Category | Author(s) | Technique and Approach | Conclusion |

|---|---|---|---|

| Technological Network | Ritter and Gemünden (2003) [53] | Empirical Analysis | Network competence has a strong positive influence on the extent of interorganizational technological-collaborations and on a firm’s product- and process-innovation success. |

| Tambe et al. (2012) [54] | Empirical Analysis | External focus, decentralization, and IT are associated with improved product-innovation capabilities. | |

| Political Reputation | Fuertes-Callén and Cuéllar-Fernández (2014) [56] | Empirical Analysis | Commercialization and reputation of innovative product intervene in the relationship between innovation and product success. |

| Keshta et al. (2020) [57] | Empirical Analysis | There is a direct relationship of statistical significance between the level of enhancing the perceived organizational reputation and achieving strategic creativity. | |

| Media Attention | Flipse and Osseweijer (2013) [58] | Empirical Analysis | The quick response-speed of media promotes innovative practices. |

| Mount and Martinez (2014) [59] | Cases Overview | Collective intelligence emerges from the many-to-many interactions supported by social media during open-innovation activities. | |

| Bhimani et al. (2019) [60] | Literature Review | Social media is seen as enabler and driver of innovation. | |

| Resource Regulation | Morrison et al. (2000) [64] | Empirical Analysis | Redundant resources in firms can help encourage an environment conducive to innovation and thus drive innovation-output in firms. |

| Resource Regulation | Geiger and Cashen (2002) [65] | Empirical Analysis | Internal redundancy may become a resource supply-channel for firms to implement innovation projects. |

| Tan and Peng (2003) [63] | Empirical Analysis | The impact of different types of organizational slack on the innovation activities of enterprises differs significantly, depending on their individual characteristics. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, L.; Guo, X.; Liu, Y.; Sun, X.; Ji, J. How Does Corporate Charitable Giving Affect Enterprise Innovation? A Literature Review and Research Directions. Sustainability 2022, 14, 15603. https://doi.org/10.3390/su142315603

Xu L, Guo X, Liu Y, Sun X, Ji J. How Does Corporate Charitable Giving Affect Enterprise Innovation? A Literature Review and Research Directions. Sustainability. 2022; 14(23):15603. https://doi.org/10.3390/su142315603

Chicago/Turabian StyleXu, Lei, Xiaoning Guo, Yan Liu, Xiaochen Sun, and Jie Ji. 2022. "How Does Corporate Charitable Giving Affect Enterprise Innovation? A Literature Review and Research Directions" Sustainability 14, no. 23: 15603. https://doi.org/10.3390/su142315603

APA StyleXu, L., Guo, X., Liu, Y., Sun, X., & Ji, J. (2022). How Does Corporate Charitable Giving Affect Enterprise Innovation? A Literature Review and Research Directions. Sustainability, 14(23), 15603. https://doi.org/10.3390/su142315603