The Impact of Environmental Tax Reform on Total Factor Productivity of Heavy-Polluting Firms Based on a Dual Perspective of Technological Innovation and Capital Allocation

Abstract

1. Introduction

2. Literature Review and System Background

2.1. Literature Review

2.2. System Background

3. Research Design

3.1. Model Specification

3.2. Data Source

3.3. Variable Selection

- (1)

- Explained variable: Total factor productivity (TFP)

- (2)

- Core independent variable: Dummy variable of environmental tax policy

- (3)

- Control variable

4. Empirical Analysis

4.1. Benchmark Regression

4.2. Robustness Test

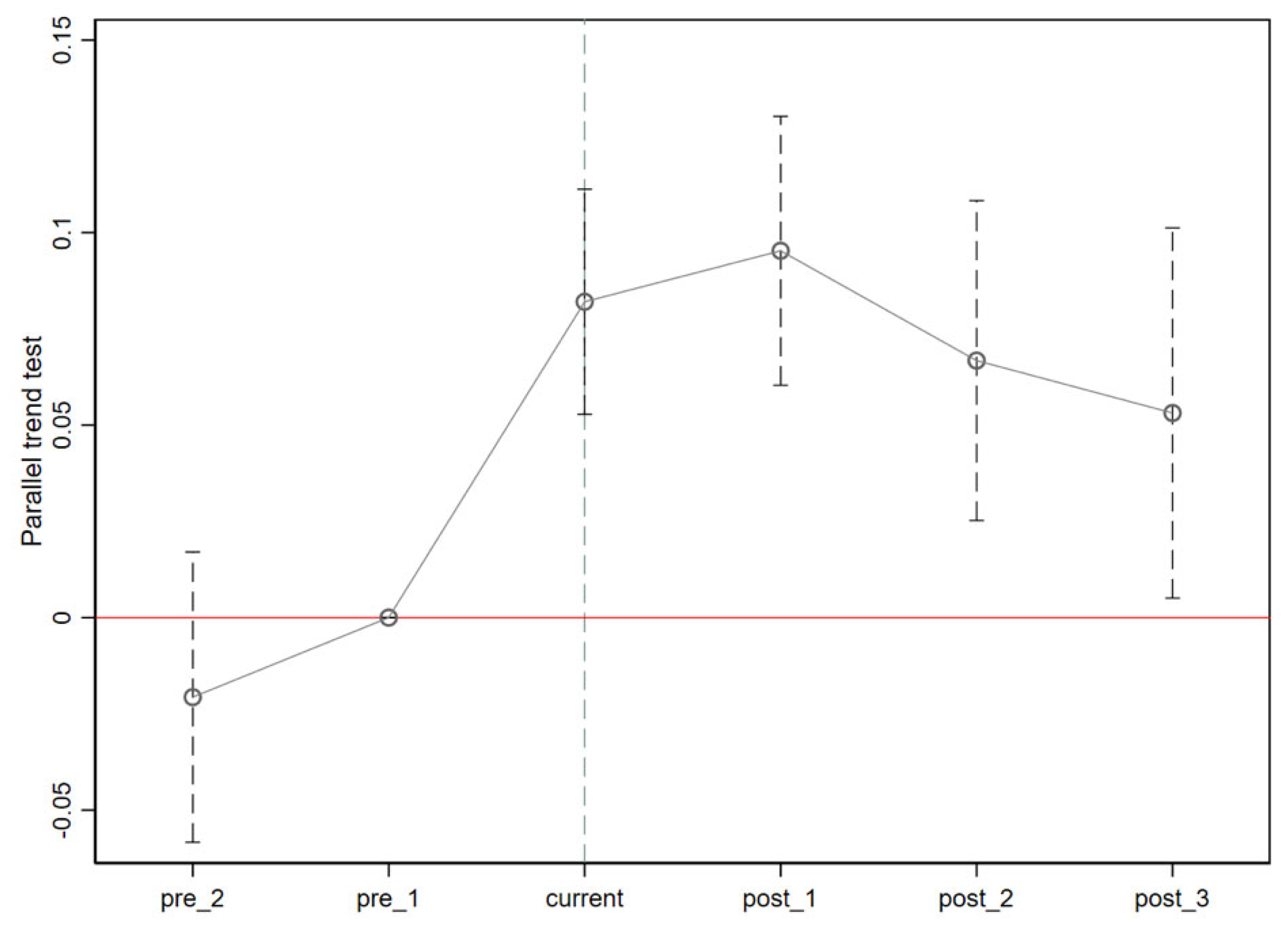

4.2.1. Parallel Trend Test

4.2.2. Replace Dependent Variable

4.2.3. Replacement Industry Classification Standard

4.3. Mechanism Analysis

- (1)

- Technological innovation effect

- (2)

- Capital allocation effect

4.4. Analysis of Heterogeneity

- (1)

- Regression analysis conducted according to different regions

- (2)

- Regression analysis conducted according to different nature of property rights

5. Discussion

6. Conclusions

7. Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Jin, Y.L.; Gu, J.R.; Zeng, H.X. Does “Environmental Protection Fees Replaced with Environmental Protection Taxes” Affect Corporate Performance? Account. Res. 2020, 5, 117–133. [Google Scholar]

- Zhang, L.; Zhu, G.S.; Li, S.G.; Li, X.Y. Market environment, key industrial policy and enterprise productivity difference. J. Manag. World 2019, 3, 114–126. [Google Scholar]

- Solow, R.M. Technical change and the aggregate production function. Rev. Econ. Stat. 1957, 39, 312–320. [Google Scholar] [CrossRef]

- Olley, S.; Pakes, A. The Dynamics of Productivity in the Telecommunications Equipment Industry. Econometrica 1996, 64, 1263–1297. [Google Scholar] [CrossRef]

- Levinsohn, J.; Petrin, A. Estimating production functions using inputs to control for unobservables. Rev. Econ. Stud. 2003, 70, 317–341. [Google Scholar] [CrossRef]

- Wang, J.; Liu, B. Environmental Regulation and Enterprise’ TFP—An Empirical Analysis Based on China’s Industrial Enterprise Data. China Ind. Econ. 2014, 3, 44–56. [Google Scholar]

- Xu, B.C.; Xie, J.G. How Pollution Charges Affect the Enterprise Productivity? Evidence from the Chinese Manufacturing Industry. J. World Econ. 2016, 39, 143–168. [Google Scholar]

- Blundell, R.; Bond, S. Initial conditions and moment restrictions in dynamic panel data models. J. Econom. 1998, 87, 115–143. [Google Scholar] [CrossRef]

- Ren, S.G.; Zheng, J.J.; Liu, D.H.; Chen, X.H. Does Emissions Trading System Improve Firm’s Total Factor Productivity—Evidence from Chinese Listed Companies. China Ind. Econ. 2019, 5, 5–23. [Google Scholar]

- Xu, X.; Huang, X.; Huang, J.; Gao, X.; Chen, L. Spatial-temporal characteristics of agriculture green total factor productivity in China, 1998–2016: Based on more sophisticated calculations of carbon emissions. Int. J. Environ. Res. Public Health 2019, 16, 3932. [Google Scholar] [CrossRef]

- Caves, D.W.; Christensen, L.R.; Diewert, W.E. Multilateral comparisons of output, input, and productivity using superlative index numbers. Econ. J. 1982, 92, 73–86. [Google Scholar] [CrossRef]

- Färe, R.; Grosskopf, S.; Lovell, C.A.K.; Pasurka, C. Multilateral productivity comparisons when some outputs are undesirable: A nonparametric approach. Rev. Econ. Stat. 1989, 71, 90–98. [Google Scholar] [CrossRef]

- Wang, M.; Li, Y.; Liao, G. Research on the impact of green technology innovation on energy total factor productivity, based on provincial data of China. Front. Environ. Sci. 2021, 9, 710931. [Google Scholar] [CrossRef]

- Song, M.; Peng, L.; Shang, Y.; Zhao, X. Green technology progress and total factor productivity of resource-based enterprises: A perspective of technical compensation of environmental regulation. Technol. Forecast. Soc. Change 2022, 174, 121276. [Google Scholar] [CrossRef]

- Wang, H.; Cui, H.; Zhao, Q. Effect of green technology innovation on green total factor productivity in China: Evidence from spatial durbin model analysis. J. Clean. Prod. 2021, 288, 125624. [Google Scholar] [CrossRef]

- Furceri, D.; Celik, S.K.; Jalles, J.T.; Koloskova, K. Recessions and total factor productivity: Evidence from sectoral data. Econ. Model. 2021, 94, 130–138. [Google Scholar] [CrossRef]

- Liu, Y.; Yang, Y.; Li, H.; Zhong, K. Digital economy development, industrial structure upgrading and green total factor productivity: Empirical evidence from China’s cities. Int. J. Environ. Res. Public Health 2022, 4, 2414. [Google Scholar] [CrossRef]

- Yu, D.; Li, X.; Yu, J.; Li, H. The impact of the spatial agglomeration of foreign direct investment on green total factor productivity of Chinese cities. J. Environ. Manag. 2021, 290, 112666. [Google Scholar] [CrossRef]

- Lee, C.C.; Lee, C.C. How does green finance affect green total factor productivity? Evidence from China. Energy Econ. 2022, 107, 105863. [Google Scholar] [CrossRef]

- Zhang, Y.; Song, Y.; Zou, H. Transformation of pollution control and green development: Evidence from China’s chemical industry. J. Environ. Manag. 2020, 275, 111246. [Google Scholar] [CrossRef]

- Zhang, W.; Meng, J.; Tian, X. Does de-capacity policy enhance the total factor productivity of China’s coal companies? A regression discontinuity design. Resour. Policy 2020, 68, 101741. [Google Scholar] [CrossRef]

- Feng, Y.; Wang, X.; Liang, Z.; Hu, S.; Xie, Y.; Wu, G. Effects of emission trading system on green total factor productivity in China: Empirical evidence from a quasi-natural experiment. J. Clean. Prod. 2021, 294, 126262. [Google Scholar] [CrossRef]

- Chen, H.; Guo, W.; Feng, X.; Wei, W.; Liu, H.; Feng, Y.; Gong, W. The impact of low-carbon city pilot policy on the total factor productivity of listed enterprises in China. Resour. Conserv. Recycl. 2021, 169, 105457. [Google Scholar] [CrossRef]

- Tang, H.; Liu, J.; Wu, J. The impact of command-and-control environmental regulation on enterprise total factor productivity: A quasi-natural experiment based on China’s “Two Control Zone” policy. J. Clean. Prod. 2020, 254, 120011. [Google Scholar] [CrossRef]

- Yuan, J.; Zhang, D. Research on the Impact of Environmental Regulations on Industrial Green Total Factor Productivity: Perspectives on the Changes in the Allocation Ratio of Factors among Different Industries. Sustainability 2021, 23, 12947. [Google Scholar] [CrossRef]

- Cheng, B.; Xiong, T.; Yin, M.J. The Stones of those Hills, Serve to Polish Gems: Spillover Effect of Green Tax System on Firm’s Innovation. Account. Res. 2021, 6, 176–188. [Google Scholar]

- Liu, Y.G.; Liu, M.N. Have Smog Affected earnings management of heavily polluting enterprises?—Based on the political-cost hypothesis. Account. Res. 2015, 3, 26–33. [Google Scholar]

- Liu, X.H. Public Pressure, Property rights and Corporate Financing Behavior: A study based on the “PM2.5 Explosion” Event. Econ. Sci. 2016, 2, 67–80. [Google Scholar]

- Li, J.L.; Yang, Z.; Chen, J. Mixed Ownership Reform and Social Responsibility of State-owned Firms-Investigation Based on the Dual Perspectives of Quality and Quantity. Shanghai J. Econ. 2021, 11, 35–47. [Google Scholar]

- Guo, Y.; Su, C.Z.; Zhang, Y. Does disclosure of social responsibility information improve the market performance of enterprises? Syst. Eng. Theory Pract. 2019, 4, 881–892. [Google Scholar]

- Wang, M.; Wang, W.; Wu, L. Application of a new grey multivariate forecasting model in the forecasting of energy consumption in 7 regions of China. Energy 2022, 243, 123024. [Google Scholar] [CrossRef]

- Xu, S.Y.; Chen, J.; Zhao, G. How Does the Land Leasing Marketization Affect the Economic Growth. China Ind. Econ. 2018, 3, 44–61. [Google Scholar]

- Zhang, C.S.; Liu, G.C. The Existence and Dynamic Characteristics of Optimal Financial Structure and Its Effect on Economic Growth. J. Manag. World 2016, 1, 66–77. [Google Scholar]

- Xie, R.; Yuan, Y.; Huang, J. Different types of environmental regulations and heterogeneous influence on “green” productivity: Evidence from China. Ecol. Econ. 2017, 132, 104–112. [Google Scholar] [CrossRef]

- Porter, M.E.; Van, D.L.C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Feng, F.; Feng, X.G.; Hou, J.C.; Huo, D.M.; Tang, R. Effectiveness of regional environmental regulation, economic growth and environmental pollution: An empirical study of the Beijing-Tianjin-Hebei region. Resour. Sci. 2020, 42, 2341–2353. [Google Scholar] [CrossRef]

- Zhang, P.; Zhang, P.P.; Cai, G.Q. Comparative Study on Impacts of Different Types of Environmental Regulation on Enterprise Technological Innovation. China Popul. Resour. Environ. 2016, 4, 8–13. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Time | Related Courses |

|---|---|

| 13 September 1979 | The 11th Session of the Standing Committee of the Fifth National People’s Congress deliberated and adopted the Environmental Protection Law (Trial Implementation) |

| 5 February 1982 | The State Council issued Interim Measures of Collection of Sewage Charges |

| 28 July 1988 | The State Council issued Interim Measures of Paid Use of Special Fund for Pollution Source Control |

| 15 August 1993 | The State Planning Commission (SPC) and Ministry of Finance printed and distributed Notice of Collection of Sewage Charges |

| 2 January 2003 | The State Council issued Management Ordinance of Collection and Use of Sewage Charges |

| 1 September 2014 | National Development and Reform Commission, Ministry of Finance and Ministry of Environmental Protection printed Notice on Adjustment of the Standards for Collection of Pollutant Discharge Fees and Other Relevant Issues |

| 13 November 2014 | The Ministry of Finance, the Ministry of Environmental Protection and the State Taxation Administration jointly submitted the Environmental Protection Tax Law of the People’s Republic of China (draft) to the State Council |

| 10 June 2015 | Office of Legislative Affairs of the State Council issued Notice on Soliciting Public Opinions on the Environmental Protection Tax Law of the People’s Republic of China (Draft) |

| 5 August 2015 | The Environmental Protection Tax Law was to the legislative plan of the Standing Committee of the 12th Standing Committee of the National People’s Congress |

| 29 August 2016–3 September 2016 | The 20th Meeting of 12th Standing Committee of the National People’s Congress reviewed the Environmental Protection Tax Law of the People’s Republic of China (draft) for the first time |

| 25 December 2016 | The 25th meeting of the 12th Standing Committee of the National People’s Congress approved the Environmental Protection Tax Law of the People’s Republic of China |

| 1 January 2018 | The Environmental Protection Tax Law of the People’s Republic of China and Enforcement Regulations of the Environmental Protection Tax Law of the People’s Republic of China take effect synchronously |

| Sign | Variables | Mean | Standard Deviation | Min | Max |

|---|---|---|---|---|---|

| TFP | Total factor productivity | 15.4240 | 1.0242 | 6.9078 | 19.9872 |

| DID | Interaction item | 0.1527 | 0.3597 | 0.0000 | 1.0000 |

| size | Enterprise scale | 22.2606 | 1.3305 | 15.9792 | 28.6365 |

| lev | Asset-liability ratio | 0.4164 | 0.2340 | 0.0084 | 10.4953 |

| life | Enterprise age | 3.1048 | 0.2524 | 1.7918 | 4.1589 |

| liquid | Liquidity ratio | 2.5609 | 2.9808 | 0.0642 | 80.6637 |

| manage | Management cost | 18.8503 | 1.1853 | 15.0646 | 25.1682 |

| hhi | Industry competitiveness | 0.2060 | 0.0077 | 0.2003 | 0.3054 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| DID | 0.0739 *** (0.0135) | 0.0910 *** (0.0118) | 0.0844 *** (0.0138) | 0.0912 *** (0.0118) |

| Control variable | No | Yes | Yes | Yes |

| Fixed effect of the year | Yes | Yes | Yes | Yes |

| Fixed effect of enterprise | Yes | Yes | Yes | Yes |

| R2 | 0.1832 | 0.4049 | 0.1842 | 0.4051 |

| (1) | (2) | |

|---|---|---|

| 2015 | 0.0119 (0.0231) | 0.0206 (0.0192) |

| 2017 | 0.0626 *** (0.0183) | 0.0820 *** (0.0149) |

| 2018 | 0.0974 *** (0.0216) | 0.0952 *** (0.0178) |

| 2019 | 0.0830 *** (0.0246) | 0.0667 *** (0.0211) |

| 2020 | 0.0737 ** (0.0287) | 0.0531 ** (0.0245) |

| Control variable | No | Yes |

| Fixed effect of the year | Yes | Yes |

| Fixed effect of enterprise | Yes | Yes |

| R2 | 0.1834 | 0.4051 |

| DID | LP | OP | GMM |

|---|---|---|---|

| 0.0912 *** (0.0118) | 0.1222 *** (0.0105) | 0.1008 *** (0.0152) | |

| Control variable | Yes | Yes | Yes |

| Fixed effect of the year | Yes | Yes | Yes |

| Fixed effect of enterprise | Yes | Yes | Yes |

| R2 | 0.4051 | 0.1288 | 0.1011 |

| (1) | (2) | (3) | |

|---|---|---|---|

| DID | 0.0912 *** (0.0118) | 0.0558 *** (0.0109) | 0.0687 *** (0.0105) |

| Other control variables | Yes | Yes | Yes |

| Fixed effect of the year | Yes | Yes | Yes |

| Fixed effect of enterprise | Yes | Yes | Yes |

| R2 | 0.4051 | 0.4040 | 0.4044 |

| Technological Innovation Effect | Capital Allocation Effect | |||

|---|---|---|---|---|

| Explained variables | (1) | (2) | (3) | (4) |

| DID | 0.1661 * (0.0914) | 0.0405 ** (0.0193) | 0.0506 *** (0.0140) | 0.0901 * (0.0460) |

| Fixed effect of the year | Yes | Yes | Yes | Yes |

| Fixed effect of enterprise | Yes | Yes | Yes | Yes |

| Control variable | Yes | Yes | Yes | Yes |

| R2 | 0.0116 | 0.0187 | 0.4751 | 0.3069 |

| Region Heterogeneity | Equity Heterogeneity | |||||

|---|---|---|---|---|---|---|

| Explained Variables | Eastern Region | Central Region | Western Region | Northeast Region | State-Owned Enterprise | Non-State-Owned Enterprise |

| DID | 0.0621 *** | 0.1089 ** | 0.1468 *** | 0.1209 * | 0.1236 *** | 0.1209 * |

| (0.0146) | (0.0193) | (0.0345) | (0.0460) | (0.0176) | (0.0460) | |

| Fixed effect of the year | Yes | Yes | Yes | Yes | Yes | Yes |

| Fixed effect of enterprise | Yes | Yes | Yes | Yes | Yes | Yes |

| Control variable | Yes | Yes | Yes | Yes | Yes | Yes |

| R2 | 0.3795 | 0.3765 | 0.4936 | 0.3069 | 0.3765 | 0.3987 |

| Heavy Pollution Industry | Eastern Region | Central Region | Western Region | Northeast Region |

|---|---|---|---|---|

| Quantity | 2498 | 746 | 715 | 171 |

| Ratio to the total quantity | 18.45% | 30.88% | 31.10% | 23.75% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

He, X.; Jing, Q.-L. The Impact of Environmental Tax Reform on Total Factor Productivity of Heavy-Polluting Firms Based on a Dual Perspective of Technological Innovation and Capital Allocation. Sustainability 2022, 14, 14946. https://doi.org/10.3390/su142214946

He X, Jing Q-L. The Impact of Environmental Tax Reform on Total Factor Productivity of Heavy-Polluting Firms Based on a Dual Perspective of Technological Innovation and Capital Allocation. Sustainability. 2022; 14(22):14946. https://doi.org/10.3390/su142214946

Chicago/Turabian StyleHe, Xu, and Qin-Lei Jing. 2022. "The Impact of Environmental Tax Reform on Total Factor Productivity of Heavy-Polluting Firms Based on a Dual Perspective of Technological Innovation and Capital Allocation" Sustainability 14, no. 22: 14946. https://doi.org/10.3390/su142214946

APA StyleHe, X., & Jing, Q.-L. (2022). The Impact of Environmental Tax Reform on Total Factor Productivity of Heavy-Polluting Firms Based on a Dual Perspective of Technological Innovation and Capital Allocation. Sustainability, 14(22), 14946. https://doi.org/10.3390/su142214946